Saudi Arabia Commercial Vehicle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

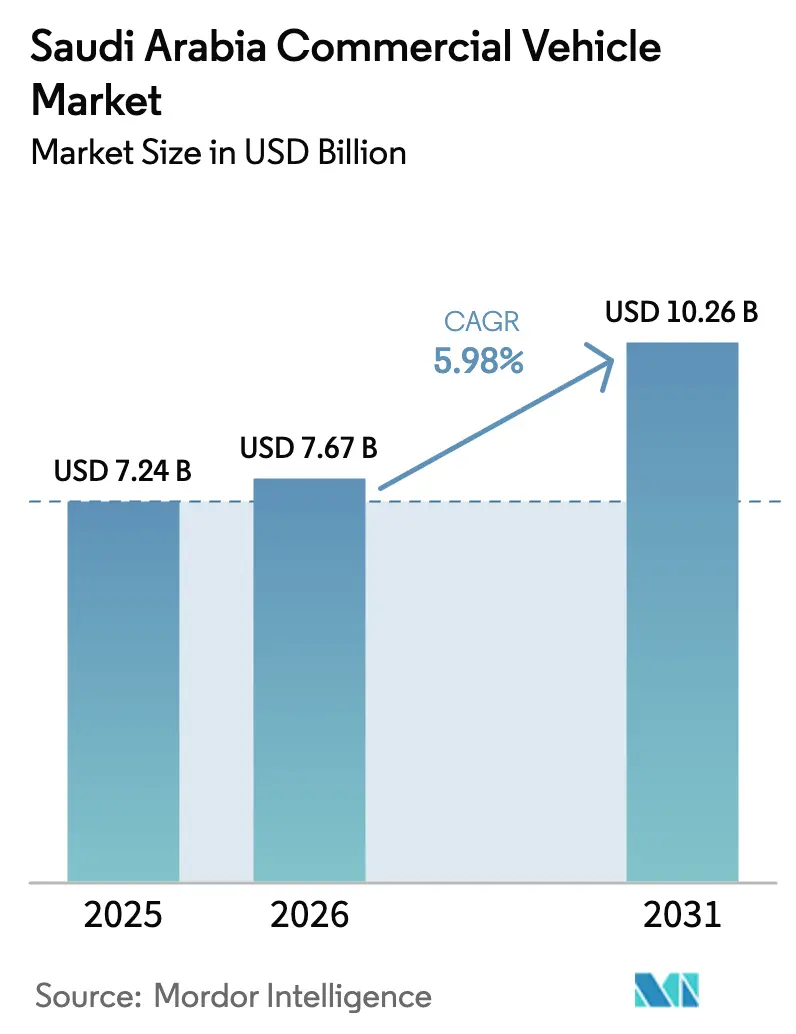

| Base Year Market Size (2025) | USD 7.24 Billion |

| Market Size (2026) | USD 7.67 Billion |

| Market Size (2031) | USD 10.26 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Commercial Vehicle Market Analysis by Mordor Intelligence

The Saudi Arabia commercial vehicle market size was valued at USD 7.24 billion in 2025 and estimated to grow from USD 7.67 billion in 2026 to reach USD 10.26 billion by 2031, at a CAGR of 5.98% during the forecast period (2026-2031). Strong public-sector spending on roads, ports, mineral processing hubs, and next-generation urban districts under Vision 2030 anchors this expansion. The National Transport and Logistics Strategy earmarks USD 133 billion for infrastructure, translating into continuous fleet orders for construction, mining, and distribution uses [1]“Saudi Arabia – Transportation Infrastructure,” International Trade Administration, trade.gov. Giga-projects such as NEOM, the Red Sea Project, and Qiddiya collectively demand tens of thousands of specialized trucks, cranes, and buses, creating a structural upward shift in annual vehicle procurement schedules. Parallel growth in e-commerce- supported by 99% internet penetration- elevates requirements for agile, technology-ready light commercial units that can operate profitably in congested city centers. Meanwhile, a digital-tachograph mandate and fleet-localization incentives compress average fleet age as operators migrate toward compliant, locally assembled models with embedded telematics. Severe desert operating conditions and route lengths above the global average keep total cost of ownership in focus; suppliers able to bundle predictive maintenance and driver-training programs gain a competitive advantage.

Key Report Takeaways

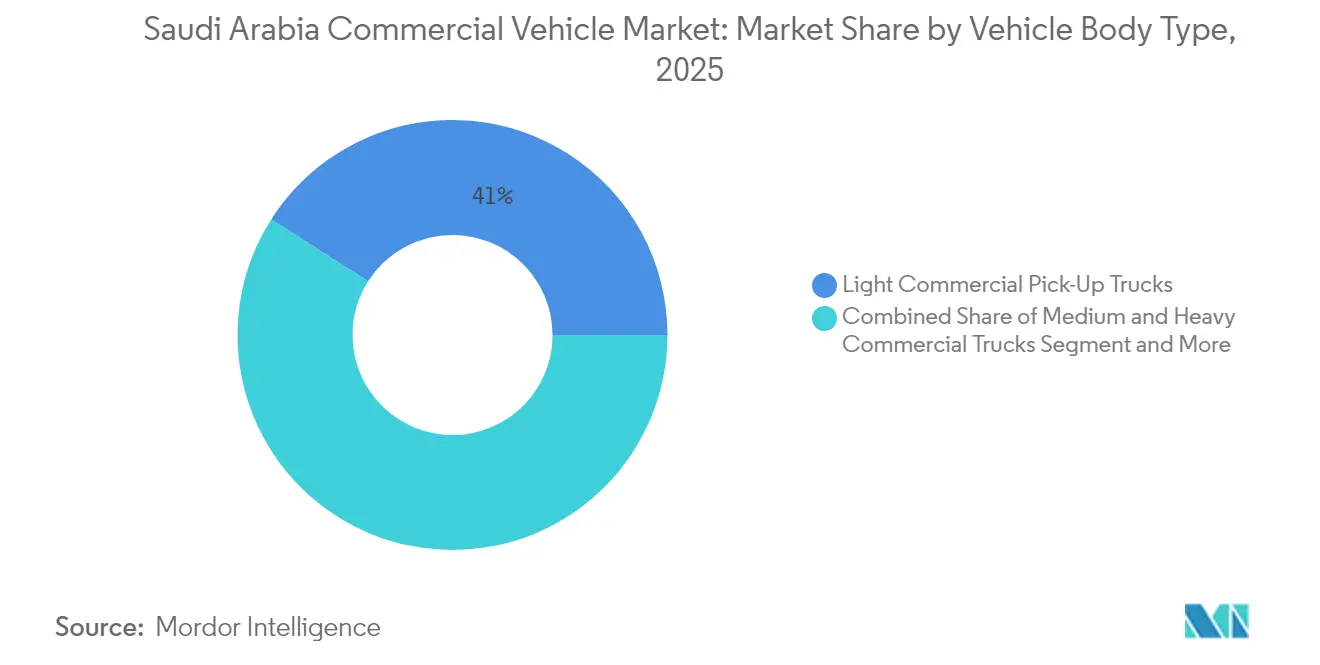

- By vehicle body type, light commercial pick-up trucks led with 40.97% of the Saudi Arabia commercial vehicle market share in 2025, while light commercial vans are projected to grow at a 7.32% CAGR through 2031.

- By propulsion type, internal-combustion engine models retained 90.12% share of the Saudi Arabia commercial vehicle market size in 2025, while hybrids and electrics are projected to grow at an 8.49% CAGR through 2031.

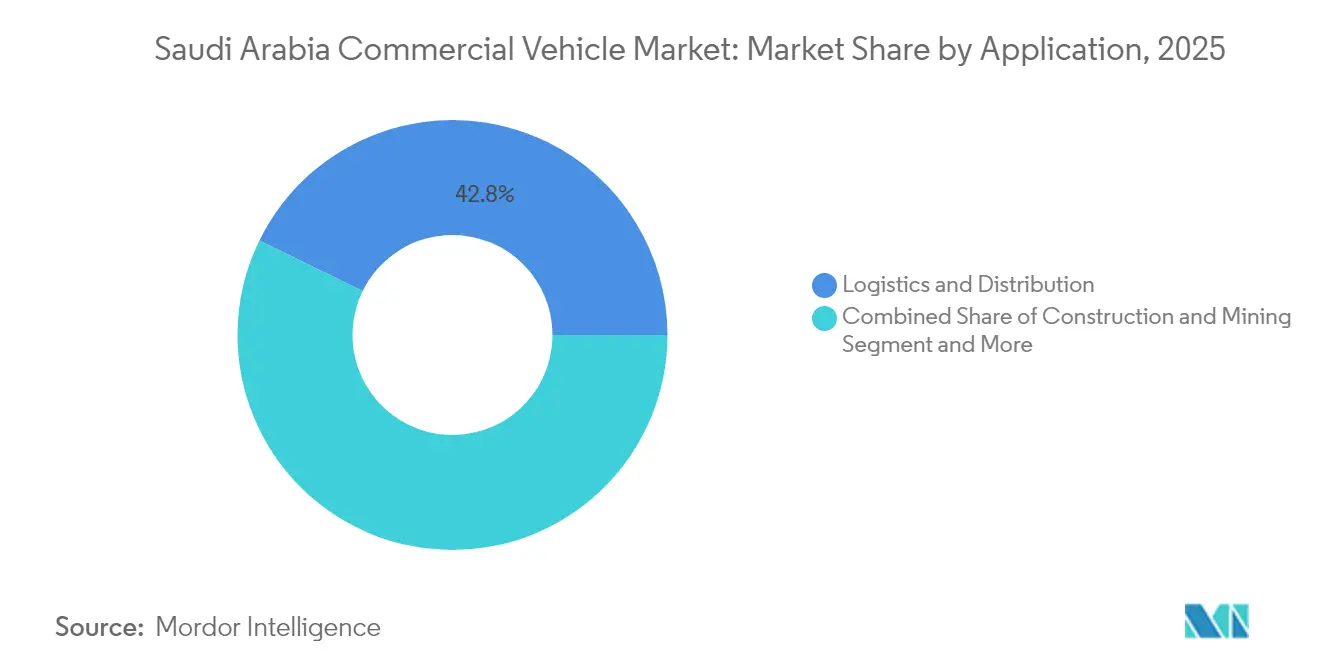

- By application, logistics and distribution represented 42.76% of the Saudi Arabia commercial vehicle market size in 2025; public transport and mobility is expanding at a 6.62% CAGR through 2031.

- By tonnage class, light vehicles (Less than 3.5 tons) captured 41.12% of the Saudi Arabia commercial vehicle market share in 2025, while heavy vehicles (More than 16 tons) are scaling at an 7.86% CAGR to 2031.

- By region, the Western region accounted for a 35.86% slice of the Saudi Arabia commercial vehicle market size in 2025, whereas the Northern and Central regions are advancing fastest at 7.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Commercial Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Giga-Projects | +0.9% | Northern, Western, Central | Long term (≥ 4 years) |

| E-commerce and Last-mile Boom | +0.7% | National; urban Western and Central | Medium term (2-4 years) |

| Mining-Sector Haulage Surge | +0.6% | Northern and Eastern zones | Long term (≥ 4 years) |

| Fleet Localization Incentives | +0.5% | National; Central and Eastern hubs | Medium term (2-4 years) |

| Digital-Tachograph Mandate | +0.4% | National corridors | Short term (≤ 2 years) |

| Hydrogen/LNG Corridor Build-out | +0.4% | Eastern, expanding to Northern | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Projects Buoy Demand

Saudi Arabia has budgeted more than USD 500 billion for flagship developments that span desert smart cities, tourism archipelagos, and entertainment megacenters. NEOM alone is estimated to require around 20,000 construction vehicles at peak, while the Red Sea Project and Qiddiya each carry multiyear procurement pipelines for heavy trucks, concrete mixers, and lifting equipment. Because sites are located in previously under-served areas, new freight corridors, logistics centers, and depots are being built in tandem, accelerating orders for tippers, low-bed trailers, and fuel tankers. Contractors run fleets at higher utilization than typical oil-sector norms, shortening replacement cycles and increasing demand for premium driveline and cooling systems that can withstand extreme heat. As these urban districts transition from construction to operations, secondary demand appears in municipal services, waste-handling, and mass-transit fleets, locking in long-tail volumes for the Saudi Arabia commercial vehicle market.

E-Commerce and Last-Mile Boom

Online retail sales exceeded USD 8 billion in 2025, rising more than 24% annually as smartphone penetration approaches saturation. Rapid-fire same-day delivery pledges compel logistics players to deploy compact vans and pick-ups capable of multiple stops per hour in Jeddah, Riyadh, and Dammam. International integrators and local third-party logistics specialists are enlarging fleets and incorporating route-optimization software to trim dwell time. Holiday peaks during Ramadan and the Hajj season routinely boost daily parcel volumes by double digits, forcing operators to add spare vehicles rather than risk service lapses. Consequently, the Saudi Arabia commercial vehicle market records disproportionate demand for Euro-VI-compliant vans outfitted with temperature-controlled compartments for pharmaceuticals and grocery delivery.

Mining-Sector Haulage Surge

Targeting USD 75 billion in mining GDP by 2035, Saudi Arabia is scaling up phosphate, bauxite, and copper output. Projects occur in remote deserts, so 90-tonne dump trucks, water tankers, and service vehicles must withstand abrasive terrain and high ambient temperatures. Ma’aden’s expansion programs specify trucks with reinforced suspensions and high-capacity cooling, signaling ongoing demand for specialized heavy equipment fleets. Transport distances from mine to port extend 1,200 km in some cases, necessitating redundant powertrains and staged service depots along new freight highways, fueling incremental growth in the Saudi Arabia commercial vehicle market.

Fleet Localization Incentives

The Ministry of Industry ties government contracts and soft financing to locally assembled vehicles, offering duty exemptions and land grants for factories that meet content thresholds. Over 160 automotive facilities, spanning chassis assembly, body stamping, and component machining are now active nationwide [2]“Automotive Localization Drive,” Arab News, arabnews.com . OEMs such as Tata Daewoo and Lucid have committed to multi-billion-dollar investments to tap these perks, leading to shorter delivery lead times and growing aftermarket parts availability. Localization also stipulates workforce development, which boosts training demand for Saudi nationals in welding, robotics, and diagnostics. For fleet buyers, domestic sourcing brings faster warranty turnaround and easier specification adjustments, reinforcing a preference for locally built units over imports.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-Price Cyclicality | −0.5% | National; energy fleets | Short term (≤ 2 years) |

| Semiconductor Shortages | −0.4% | All regions | Medium term (2-4 years) |

| Saudization Cost Pressure | −0.3% | National; labor-intensive transport | Medium term (2-4 years) |

| Battery Thermal-Degradation Issues | −0.2% | Desert interiors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Cyclicality

Fuel accounts for one-third of fleet operating expense, so oil price swings immediately alter cash flow and capital-renewal plans. When prices dip, government hydrocarbons revenue softens, occasionally delaying infrastructure disbursements that drive truck demand. Conversely, low pump prices relax operating margins, encouraging route expansion among private carriers. These mixed effects create visibility challenges for manufacturers who must balance factory scheduling against fluctuating tender volumes. Diversification into non-oil sectors is progressing, yet the linkage between crude prices and public-works spending will remain a short-term volatility factor.

Semiconductor Shortages

Global chip scarcity continues to elongate build times for advanced drivelines, braking systems, and infotainment modules. Import dependency magnifies the bottleneck because Saudi assemblers source high-value electronics from Europe and East Asia. Delivery slots favor premium passenger vehicles, occasionally relegating commercial chassis to lower priority in OEM allocation queues. Fleet managers prolong service life, heightening demand for maintenance contracts and used-vehicle imports, although the latter are curtailed by age restrictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Body Type: Versatile Pick-Ups Outperform

Light pick-ups generated 40.97% of the Saudi Arabia commercial vehicle market share in 2025, underscoring their dual urban-off-road utility. Contractors use them for crew transport and light materials, while SMEs favor them for affordability and resale value. Public-sector agencies likewise adopt double-cab models outfitted with telemetry, accelerating bulk tenders. Light vans, in contrast, are scaling at a 7.32% CAGR on the back of parcel-delivery and cold-chain needs. Their enclosed cargo area, flat floor, and rising electrification readiness align with urban emission zones under design in Riyadh and Jeddah. Medium trucks remain steady, mostly in cement, steel, and beverage distribution, whereas bus bodies benefit from the Riyadh Metro feeder network roll-out. Import rules limiting vehicle age spur replacement demand, skewing purchases toward modern cabins with driver-fatigue monitoring.

The Saudi Arabia commercial vehicle market rewards body builders that can integrate telemetry, load-sensing, and advanced cooling into OEM chassis without compromising warranty. Growing pain points in pharmaceutical delivery trigger demand for insulated van bodies certified to GDP (Good Distribution Practice) standards, a niche that several local fabricators now serve. At the heavy end, low-bed trailers capable of transporting 120-tonne modules to NEOM wind-farm sites illustrate the intricate specialization emerging. Fleet audits under the Wasl platform create paper trails that favor modular body designs, enabling quick adaptation; examples include swap-body systems for construction debris by day and palletized goods at night. These trends cement diversified uptake across body types, giving the Saudi Arabia commercial vehicle market a balanced demand structure that limits oversupply risk in any single segment.

By Propulsion Type: Conventional Engines Hold the Line

Internal-combustion engines still account for 90.12% of units and dominate the Saudi Arabia commercial vehicle market size due to fuel subsidies and decentralized service infrastructure. Nevertheless, hybrids and full electrics are projected to compound at 8.49% annually, helped by the Electric Vehicle Infrastructure Company and early commitments from food-service and postal fleets. Battery-electric vans cover city routes below 200 km a day, while fast-charging plazas along the Riyadh–Dammam corridor trial megawatt chargers for pilot heavy trucks. Hydrogen options are also in validation, with Aramco operating a small demonstration fleet out of Dhahran . The government’s objective of 45% clean-mobility penetration by 2030 nudges procurement guidelines toward low-emission drivetrains in ministries and municipalities. Resale uncertainty and high first cost remain hurdles; yet, localized battery-assembly ventures promise to trim price points over the forecast horizon.

For operators, the break-even calculus now weighs fuel savings against battery thermal-management overhead under desert conditions. Route-planning software that aggregates load, topography, and ambient heat helps fleets decide when battery electric or hydrogen variants outperform diesel for specific duty cycles. Telematics data supports financing packages that lower upfront spending through pay-per-kilometer contracts backed by OEM maintenance guarantees. The Saudi Arabia commercial vehicle market therefore exhibits a dual-speed trajectory: diesel remains predominant in long-haul and remote mining, while electrification gains mindshare in urban delivery and public-service sub-fleets.

By Application: Logistics Commands Spending

Logistics and distribution captured 42.76% of the Saudi Arabia commercial vehicle market size in 2025, driven by a national network of 59 logistics centers spanning 100 million m². Cross-docking facilities near Jeddah Islamic Port and King Abdulaziz Port integrate automated sorters that require just-in-time truck arrivals, inflating demand for telematics-equipped tractors. Public transport and mobility are pacing ahead at 6.62% CAGR, catalyzed by Riyadh Metro’s bus-feeder strategy and municipal clean-air targets. Construction and mining continue to furnish stable baseline volumes through heavy-duty tippers, while oilfield services diversify into multipurpose rigs capable of chemical injection and well intervention.

Seasonal tourism for Hajj funnels upwards of 20 million visitors into Makkah and Madinah, necessitating charter bus fleets with luggage holds and high ambient-temperature air-conditioning systems, which expands the public-transport application category every summer. E-tailers introduce micro-fulfillment nodes inside malls, generating shuttle traffic for 5-tonne dry-box trucks. Mining consortiums place long-term lease orders for chassis capable of remote diagnostics, given intervention costs in the desert can exceed USD 50,000 per incident. These multi-front requirements sustain a diversified application profile, immunizing the Saudi Arabia commercial vehicle market against single-sector downturns.

By Tonnage Class: Light Leads, Heavy Accelerates

Light commercial vehicles up to 3.5 tons claimed 41.12% of the Saudi Arabia commercial vehicle market share in 2025, aligning with urban parcel density and parking constraints. They dominate courier, pharmaceutical, and bakery routes under 150 km. Heavy vehicles above 16 tons are registering the fastest growth at 7.86% CAGR, propelled by giga-project material movements and bulk mineral haulage to Gulf ports. Medium trucks fill regional delivery niches, particularly for FMCG and construction materials moving between secondary cities.

Road expansion exceeds 3,500 km over 2024-2025, allowing tri-drive tractor configurations up to 85 tons gross weight without axle stress penalties. Heavy-haul licenses now embed digital-tachograph validation, steering demand toward factory-installed systems. Light-vehicle customers focus on payload-to-gross-weight ratios and driver-comfort features to aid Saudization recruitment. Consequently, body builders recalibrate chassis ratings and wheelbase options to align with emerging transport-authority norms, reinforcing a nuanced tonnage landscape inside the Saudi Arabia commercial vehicle market.

Geography Analysis

The Western region, anchored by Jeddah and bolstered by the USD 500 billion Red Sea tourism complex, held 35.86% of the Saudi Arabia commercial vehicle market size in 2025. Its deep-water ports and free-zone warehouses make it the preferred entry point for imported chassis and spare parts. Port of NEOM, designed for full automation and powered by renewables, is expected to drive incremental heavy-haul and drayage demand once container operations commence in 2026. Tourism-led construction plus ongoing religious-sites upgrades sustain year-round equipment utilization, prompting fleet managers to pre-order stock rather than rely on spot rentals.

The Northern and Central region posts the highest growth at 7.54% CAGR to 2031 as NEOM’s 170-km linear city, Riyadh’s King Salman Park, and multiple inland logistics parks step up procurement. Government ministries headquartered in Riyadh award bundled contracts that include supply-chain, passenger shuttle, and waste-management vehicles, consolidating order books for the Saudi Arabia commercial vehicle market. Expanded rail freight between the capital and the Red Sea will augment first-mile and last-mile truck activity once operational.

Eastern and Southern provinces contribute complementary but vital volumes. The Eastern region’s petrochemical clusters in Jubail and mining developments in Ras Al-Khair require corrosive-material tankers, high-temperature dumpers, and multi-axle flatbeds. The Southern highlands, meanwhile, nurture agribusiness and nascent eco-tourism, expanding demand for refrigerated vans, mini buses, and 4×4 maintenance trucks suited to mountainous terrain. Collectively, these patterns create a geographically balanced demand profile that underpins long-term stability for the Saudi Arabia commercial vehicle market.

Competitive Landscape

Competition is moderate, with global OEMs- Isuzu, Hino, Daimler Truck, Volvo, and Tata- operating alongside Chinese entrants such as Foton and state-linked developers like Lucid’s EV unit. Localization imperatives spur assembly plants in Dammam, Jeddah, and King Abdullah Economic City, lifting total installed capacity above 30,000 units per year in 2025. Partnerships with local distributors- Electromin-Quantron for electric heavy trucks and FAMCO-Ashok Leyland for buses- illustrate a pivot toward technology-rich propositions. Telematics, over-the-air software updates, and autonomous-ready sensor suites are emerging as table stakes in fleet tenders governed by Wasl compliance.

Traditional OEMs hedge by offering retrofit telematics packages and extended warranties to keep legacy fleets in their service networks. Newcomers focus on total-cost-of-ownership calculations powered by real-time data, often bundling trucks, chargers, and energy contracts under multiyear leasing structures. The Saudi Arabia commercial vehicle industry, therefore, witnesses a fusion of hardware and digital service models, pushing price competition into lifecycle-cost metrics rather than sticker price.

Government procurement still favors proven incumbents for mission-critical roles, but greener technologies create an opening for niche manufacturers specializing in battery-electric, hydrogen, or LNG drivelines. As semiconductor supply normalizes and local battery plants come online, late-cycle entrants could seize share by shaving months off delivery timelines-reinforcing the competitive fluidity characterizing the Saudi Arabia commercial vehicle market.

Saudi Arabia Commercial Vehicle Industry Leaders

Isuzu Motors Saudi Arabia

Hino Motors (Toyota)

Daimler Truck AG (Mercedes-Benz Trucks)

Volvo Trucks

Scania AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Foton signed an MoU with Petromin, the Ministry of Investment, and the National Industrial Development Center to evaluate a multi-segment commercial-vehicle plant in Saudi Arabia.

- January 2025: Isuzu introduced its S&E Series heavy-duty truck in Riyadh, emphasizing region-specific cooling and durability.

- November 2024: Tata Motors launched the Prima 4440.S AMT tractor in Saudi Arabia, marking its first automated-manual offering in the Kingdom.

- June 2024: FAMCO KSA formed a distribution alliance with Ashok Leyland to deepen bus and truck penetration across Saudi Arabia.

Saudi Arabia Commercial Vehicle Market Report Scope

| Buses |

| Medium and Heavy Commercial Trucks |

| Light Commercial Pick-Up Trucks |

| Light Commercial Vans |

| Hybrid and Electric Vehicles |

| ICE |

| Logistics and Distribution |

| Construction and Mining |

| Public Transport and Mobility |

| Oil and Gas Field Services |

| Light (Less than 3.5 t) |

| Medium (3.6 –16 t) |

| Heavy (Above 16 t) |

| Northern and Central |

| Western |

| Eastern |

| Southern |

| By Vehicle Body Type | Buses |

| Medium and Heavy Commercial Trucks | |

| Light Commercial Pick-Up Trucks | |

| Light Commercial Vans | |

| By Propulsion Type | Hybrid and Electric Vehicles |

| ICE | |

| By Application | Logistics and Distribution |

| Construction and Mining | |

| Public Transport and Mobility | |

| Oil and Gas Field Services | |

| By Tonnage Class | Light (Less than 3.5 t) |

| Medium (3.6 –16 t) | |

| Heavy (Above 16 t) | |

| By Region | Northern and Central |

| Western | |

| Eastern | |

| Southern |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia commercial vehicle market?

The Saudi Arabia commercial vehicle market size is USD 7.67 billion in 2026, with projections indicating USD 10.26 billion by 2031 at a 5.98% CAGR.

Which segment holds the largest Saudi Arabia commercial vehicle market share?

Light commercial pick-up trucks lead, accounting for 40.97% of sales in 2025 due to their versatility across construction and urban delivery tasks.

How fast are electric and hybrid commercial vehicles growing in Saudi Arabia?

Hybrid and battery-electric models are expected to expand at an 8.49% CAGR through 2031, driven by infrastructure investment and clean-mobility mandates.

Which region is growing fastest for commercial vehicle demand?

The Northern and Central region, propelled by NEOM and Riyadh infrastructure projects, is registering the highest growth at 7.54% CAGR to 2031.

Page last updated on: