Saudi Arabia Spare Parts Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 5.42 Billion |

| Market Size (2030) | USD 7.18 Billion |

| Growth Rate (2025 - 2030) | 5.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Spare Parts Market Analysis by Mordor Intelligence

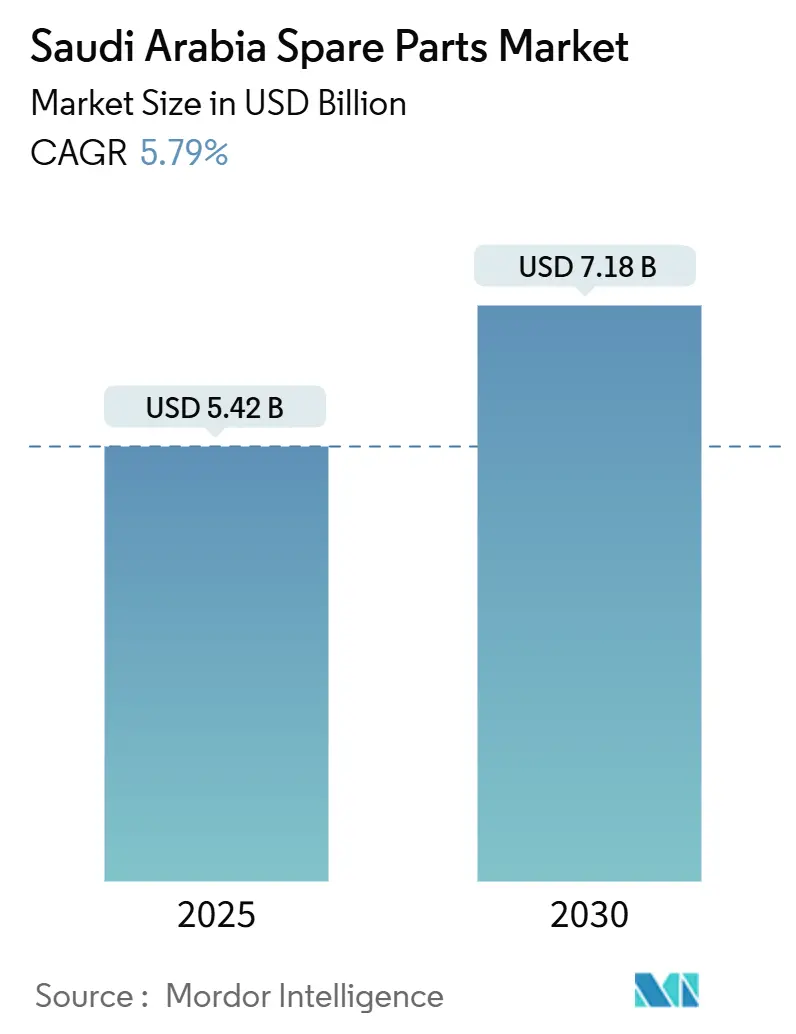

The Saudi Arabia Spare Parts Market size is estimated at USD 5.42 billion in 2025, and is expected to reach USD 7.18 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030). Saudi Arabia's Vision 2030 manufacturing incentives, combined with a significant vehicle parc and robust e-commerce penetration, are bolstering replacement demand, especially in urban and industrial corridors. In a strategic move, localization agreements have been inked with industry giants like Lucid, Hyundai, and Ceer. These agreements are not only redirecting the flow of imported components to in-Kingdom production but are also significantly reducing lead times. Digital platforms, notably Spiro and Odiggo, are enhancing parts accessibility. Simultaneously, the Motor Vehicle Periodic Inspection (MVPI) regime is instituting annual safety checks, further driving routine purchases. While enforcement against counterfeit goods and the expansion of logistics zones are redefining supply-chain risks, challenges like freight volatility and illicit trade continue to temper growth expectations in Saudi Arabia's spare parts market.

Key Report Takeaways

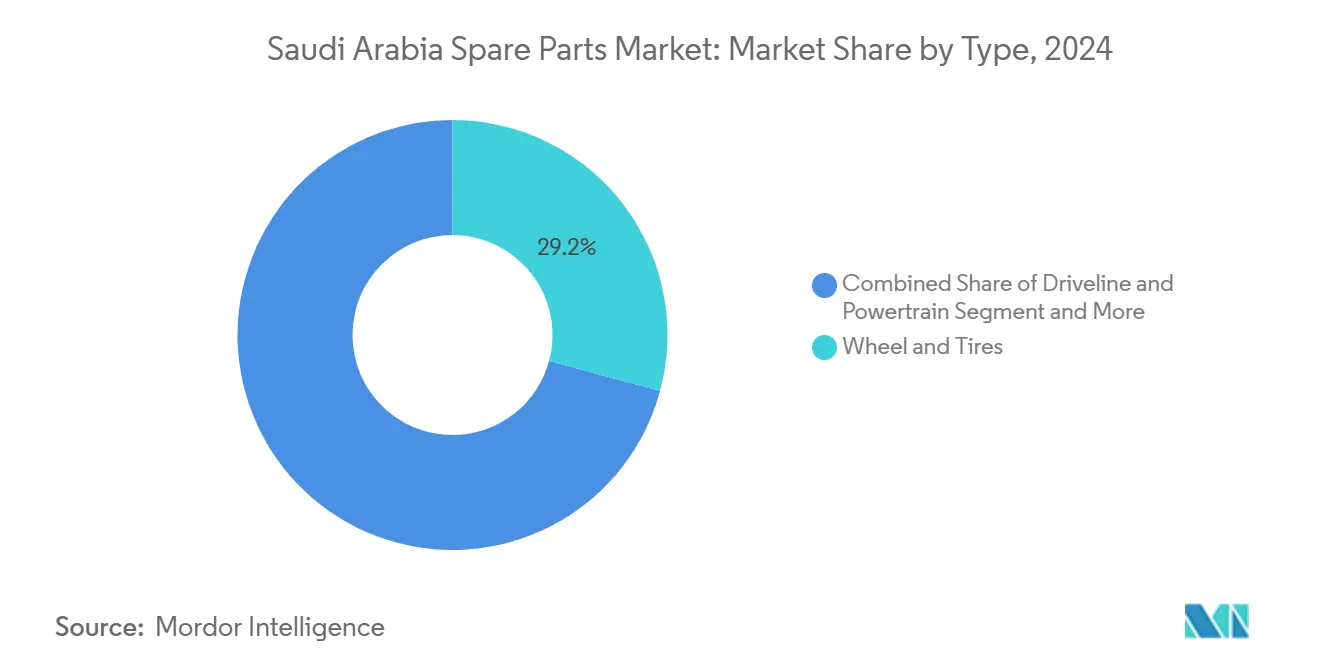

- By type, Wheel & Tires led with a 29.17% of the Saudi Arabia spare parts market share in 2024. Electrical & Electronics is forecast to expand at a 5.81% CAGR to 2030, outpacing all other categories.

- By propulsion, Internal Combustion Engine vehicles accounted for 73.37% of the Saudi Arabia spare parts market share in 2024, while Battery-Electric Vehicles recorded the fastest 5.83% CAGR through 2030.

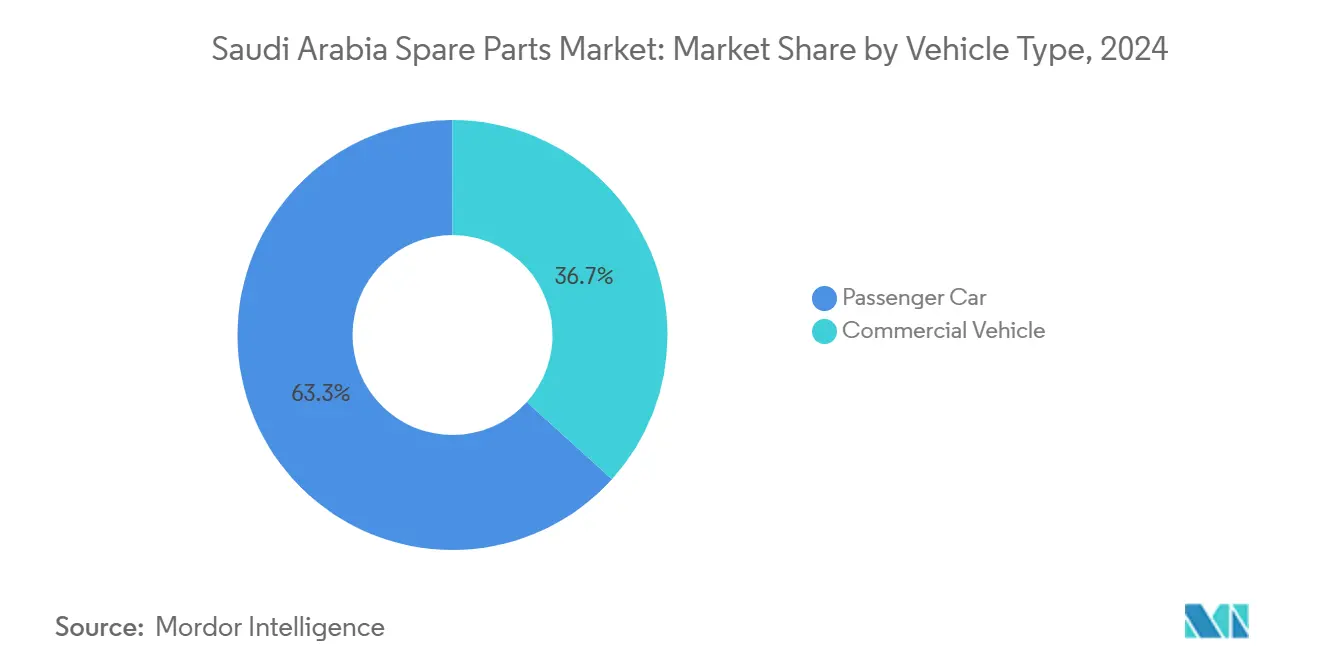

- By vehicle type, Passenger Cars captured 63.31% of the Saudi Arabia spare parts market share in 2024 and are advancing at a 5.88% CAGR through 2030.

- By sales channel, the Aftermarket maintained 65.42% of the Saudi Arabia spare parts market share in 2024 and is growing at a 5.87% CAGR on the strength of independent repair networks.

Saudi Arabia Spare Parts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Vehicle PARC | +1.8% | National, concentrated in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Vision 2030 Localisation | +1.5% | KAEC, Eastern Province, industrial clusters | Long term (≥ 4 years) |

| Rapid Rise Of E-Commerce Parts Platforms | +1.2% | National, with early gains in Riyadh, Jeddah | Short term (≤ 2 years) |

| Stricter Periodic Technical Inspection Regime | +0.9% | National coverage via 36 MVPI stations | Medium term (2-4 years) |

| Telematics-Driven Predictive Fleet Maintenance | +0.7% | Commercial hubs in Eastern Province, Riyadh | Long term (≥ 4 years) |

| SEZ Incentives | +0.6% | KAEC, Ras Al-Khair, Jazan SEZs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Vehicle PARC & Aging Fleet

In 2025, Saudi Arabia's fleet swelled to millions of units, buoyed by an ambitious infrastructure build-out and a tourism vision targeting millions of visitors. After three years, vehicles are mandated to undergo MVPI inspections, creating a steady demand for batteries, cooling parts, and driveline components. From now until 2028, commercial vehicle registrations are projected to grow at a significant CAGR. In 2023 alone, thousands of medium and heavy trucks hit the market, already populating nationwide service bays. Light commercial vehicles now dominate, accounting for a significant share of sales, which in turn is driving up the demand for tire and brake replacements in Saudi Arabia's spare parts market[1]“Annual Transport Statistics 2025,” Ministry of Transport, mot.gov.sa . Harsh climatic conditions accelerate wear and shorten average replacement intervals, emphasizing the importance of inventory depth and rapid distribution.

Vision 2030 Localization & OEM Investment Push

With OEM inflows surpassing billions, the focus has shifted towards domestic sourcing. By Q4 2026, Hyundai Motor Manufacturing Middle East plans to produce units annually from the King Salman Automotive Cluster. Ceer has committed significant investments in parts, collaborating with hundreds of Saudi suppliers for components like plastics, castings, and alloy wheels. The PIF-Pirelli partnership, with a substantial tire facility, is set to boost capacity starting in 2026, streamlining logistics for fleet operators. Saudi Aramco's IKTVA initiative directs oil-and-gas fleet needs to certified local vendors. Collectively, these initiatives bolster supply resilience and facilitate technology transfer to domestic tier-two firms in Saudi Arabia's spare parts market [2]“Automotive Investments Fact Sheet 2025,” Public Investment Fund, pif.gov.sa .

Rapid Rise of E-Commerce Parts Platforms

In 2024, online retail volumes in Saudi Arabia grew exponentially, marking a robust year-on-year growth. A notable shopper penetration and the widespread adoption of digital wallets bolstered this surge. In the B2C arena, Spiro clinched a considerable share to amplify its parts delivery services. At the same time, Odiggo garnered a vast amount, enabling it to expand its offerings to SKUs for users in Saudi Arabia. With same-day fulfillment services now available in Riyadh and Jeddah, both workshops and DIY enthusiasts are experiencing reduced service downtimes. Furthermore, the Saudi government's e-commerce registration initiatives and consumer protection laws are instilling regulatory confidence, solidifying the legitimacy of online parts sourcing in the nation's spare parts market [3]“E-Commerce Indicators 2025,” Ministry of Commerce, mci.gov.sa .

Stricter Periodic Technical Inspection Regime

MVPI’s multiple stations now enforce online booking and all-system checks on steering, suspension, brakes, lighting, tires, and emissions. Private vehicles undergo annual tests after year three, while commercial units face biennial cycles, creating predictable upticks in sales of compliance-critical components. Fees that vary incentivize motorists to remediate defects swiftly. Real-time defect reporting through SASO’s electronic portal links inspection outcomes to parts distributors, streamlining supply planning in the Saudi Arabia spare parts market [4]“MVPI Inspection Procedures,” Saudi Standards, Metrology and Quality Organization, saso.gov.sa .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation Of Counterfeit Parts | -0.8% | National, concentrated at Jeddah, Dammam, Jubail ports | Short term (≤ 2 years) |

| Global Supply-Chain Shocks | -0.6% | Import-dependent regions, Eastern Province ports | Medium term (2-4 years) |

| Fewer Replaceable Parts | -0.4% | National, with early impact in Riyadh, KAEC EV clusters | Long term (≥ 4 years) |

| OEM Captive Parts-Distribution Strategies | -0.3% | National, concentrated in major dealer network cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Parts

Saudi Customs destroyed numerous fake components in 2020, yet small-parcel smuggling via courier networks persists. Anti-Commercial Fraud Law penalties grew exponentially, including one year of imprisonment, and offenders must publish product recalls in national newspapers within a few days. The Saudi Authority for Intellectual Property mandates traceable documentation, compelling distributors to maintain chain-of-custody logs. Though enforcement improves, counterfeit goods still erode consumer trust and siphon revenue from genuine suppliers in the Saudi Arabia spare parts market.

Global Supply-Chain Shocks & Freight Volatility

Heavy reliance on imports from Japan, Germany, China, and South Korea exposes dealers to Red Sea rerouting and container-rate spikes. The Master Logistics Centers Plan sets out multiple hubs to bolster storage resilience, and the Special Integrated Logistics Zone at King Khalid International Airport offers bonded facilities for time-critical shipments. Yet unforeseen freight surcharges and vessel delays can still skew inventory cycles, tempering the growth tempo of the Saudi Arabia spare parts market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wheel & Tires Dominance Meets Electronics Innovation

Wheel & Tires accounted for 29.17% of the Saudi Arabia spare parts market share in 2024, underpinned by desert heat, rough road surfaces, and high daily mileage among ride-hailing and logistics fleets. Average tire life can fall below 40,000 km, driving multiple annual replacement events for heavy-use vehicles. PIF-Pirelli’s huge plant, coming online in 2026, will produce many units, reducing import dependence while supporting aftermarket price stability.

Electrical & Electronics, though smaller in absolute terms, posts the highest 5.81% CAGR and anchors sensor, telematics, and charging hardware supply chains. EV adoption and fleet digitization propelled Saudi Arabia's spare parts market size gains. The rollout of multiple BYD-EVIQ charging stations by 2030 forces workshops to stock high-voltage harnesses and battery thermal-management modules. Bundled maintenance contracts for smart-mobility pilots at NEOM further expand electronics throughput.

By Propulsion: ICE Dominance Faces EV Disruption

Internal combustion engine vehicles generated 73.37% of the Saudi Arabia spare parts market share in 2024, but the ICE share will gradually slip as the Kingdom targets one-third of EV penetration in Riyadh by 2030. Lucid’s expansion and Ceer’s factory will pump locally built EVs into showrooms, shifting demand toward battery-pack cooling plates, inverters, and DC-DC converters, which are propelling battery-electric vehicles at a robust CAGR of 5.83% through 2030. Saudi Arabia's spare parts market size for EV drivetrains is forecast to outpace ICE replacement spend, though hybrid systems will act as an adoption bridge in the interim.

Hedging the transition, Aramco purchased a large chunk of HORSE Powertrain Limited, ensuring advanced ICE development can coexist with growing electrification portfolios. Suppliers must, therefore, straddle dual technology tracks to remain competitive.

By Vehicle Type: Passenger Car Leadership Sustains Growth

Passenger Cars represented 63.31% of the Saudi Arabia spare parts market share in 2024 and will climb at a 5.88% CAGR through 2030 as rising female licensure and steady household formation sustain car ownership. Ride-hailing expansion in Riyadh and Jeddah magnifies high-mileage service intervals, boosting lubrication, brake, and HVAC component turnover.

Commercial Vehicles capture incremental growth from logistics and construction projects. Fleet operators like Lumi oversee multiple vehicles and reported a huge maintenance spend in H1 2024, a four-fifth increase YoY. Service contracts bundled with predictive analytics anchor long-term volume commitments to Saudi Arabia's spare parts market suppliers.

By Sales Channel: Aftermarket Strength Reflects Service Independence

The Aftermarket captured a 65.42% of the Saudi Arabia spare parts market share in 2024, aided by Ministry of Commerce rulings that dealership service is not mandatory for warranty validity, which is also growing at a CAGR of 5.87% till 2030. Independent workshops are sourced from multi-brand distributors, and they are advantaged by digital platforms that aggregate SKUs and offer same-day delivery. Saudi Arabia's spare parts market size growth here aligns with consumer price sensitivity and DIY culture among motor enthusiasts.

OEM channels, however, protect complex electronics niches through proprietary diagnostics and software calibrations. New entrants like Hyundai and Dongfeng extend dealer footprints into secondary cities, leveraging warranty retention periods to lock in early-life service revenue. ACDelco’s 25-year domestic tenure illustrates long-term brand loyalty potential for OEM-backed aftermarket labels.

Geography Analysis

The Eastern Province commands roughly one-third of national demand, anchored by Aramco operations, petrochemical clusters, and ports at Dammam and Jubail. King Abdulaziz Port funnels the bulk of automotive imports, while Ras Al-Khair SEZ nurtures metal-fabrication suppliers that feed OEM plants. Desert haulage and high-temperature cycles in this region intensify replacement rates for cooling and filtration components, reinforcing the prominence of the Saudi Arabian spare parts market.

Riyadh Region contributes nearly one-third of turnover, buoyed by administrative functions and an expanding logistics web. The Special Integrated Logistics Zone at King Khalid International Airport lures tech brands requiring expedited customs clearance. Twelve planned logistics centers further embed warehousing nodes that streamline last-mile deliveries, cementing Riyadh’s role as a distribution nexus within the Saudi Arabia spare parts market.

Western Province, driven by Jeddah Islamic Port and KAEC, accounts for about one-quarter of sales. Lucid, Hyundai, and Ceer plants clustered in KAEC create a dense supplier ecosystem supporting vehicle rollout and aftermarket provisioning. Pilgrimage seasons spike transport activity, swelling demand for brake, cooling, and tire replacements. Northern and Southern regions share the remaining one-tenth, yet Vision 2030 tourism corridors and NEOM smart-mobility pilots promise to lift their future share of the Saudi Arabia spare parts market.

Competitive Landscape

Market concentration is moderate, with longstanding distributors such as Abdul Latif Jameel IPR, Aljomaih Automotive, and United Motors Company holding entrenched agency rights. These firms combine nationwide parts warehouses, mobile service fleets, and integrated financing packages to lock in corporate accounts.

Digital insurgents like Spiro and Odiggo amplify price transparency and SKU breadth, compelling traditional players to launch omnichannel portals and click-and-collect options. Investors favor scale at the intersection of inventory depth and data analytics, rewarding platforms capable of predictive stocking tied to telematics alerts.

Localization mandates reset bargaining power, as OEMs source around half of inputs locally under Ceer guidelines. Domestic SMEs with injection-molding and aluminum-casting lines capitalize on SEZ incentives to displace imports. Technology adoption, notably IoT telemetry and AI-based demand forecasting, differentiates suppliers vying for multi-year fleet contracts in the spare parts market in Saudi Arabia.

Saudi Arabia Spare Parts Industry Leaders

Abdul Latif Jameel IPR Co. Ltd.

Aljomaih Automotive Co.

Universal Motors Agencies

Zahid Tractor & Heavy Machinery

Al Jazirah Vehicles

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Lucid Group and King Abdullah University of Science and Technology signed an R&D pact covering autonomous driving and advanced materials.

- May 2025: Hyundai Motor Manufacturing Middle East broke ground on a 50,000-unit plant at King Salman Automotive Cluster, targeting Q4 2026 production.

- April 2025: Dongfeng Motor entered a distribution alliance with Universal Motors Agencies to supply 10,000 vehicles and launch Saudi-specific models.

Saudi Arabia Spare Parts Market Report Scope

| Driveline & Powertrain |

| Interior & Exterior |

| Electrical & Electronics |

| Body & Chassis |

| Wheel & Tires |

| Other Types |

| Internal Combustion Engine |

| Battery-Electric Vehicle |

| Hybrid Electric Vehicle |

| Plug-in Hybrid Electric Vehicle |

| Fuel-Cell Electric Vehicle |

| Passenger Car |

| Commercial Vehicle |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| By Type | Driveline & Powertrain |

| Interior & Exterior | |

| Electrical & Electronics | |

| Body & Chassis | |

| Wheel & Tires | |

| Other Types | |

| By Propulsion | Internal Combustion Engine |

| Battery-Electric Vehicle | |

| Hybrid Electric Vehicle | |

| Plug-in Hybrid Electric Vehicle | |

| Fuel-Cell Electric Vehicle | |

| By Vehicle Type | Passenger Car |

| Commercial Vehicle | |

| By Sales Channel | Original Equipment Manufacturer (OEM) |

| Aftermarket |

Key Questions Answered in the Report

What is the present value of the Saudi Arabia spare parts market, and where will it be by 2030?

It generated USD 5.42 billion in 2025 and is forecast to reach USD 7.18 billion by 2030, reflecting a 5.79% CAGR.

How is Vision 2030 changing the spare-parts landscape?

Over USD 3 billion in localization deals with Lucid, Hyundai, Ceer, and Pirelli are shifting component sourcing to domestic plants, shortening lead times and boosting local content to about 45% for new models.

Which component categories are expanding the fastest?

Electrical & Electronics heads growth at a 5.81% CAGR through 2030, fueled by EV adoption, telematics integration, and the rollout of 5,000 charging stations.

What share does e-commerce hold in parts distribution?

Online platforms leverage a 91% shopper penetration rate; start-ups like Spiro and Odiggo already fulfill nationwide same-day orders, steadily drawing transactions away from brick-and-mortar counters.

How significant a threat are counterfeit parts in the Kingdom?

Customs destroyed more than 2 million fake components in 2020; new penalties of up to SAR 1 million and mandatory recalls are curbing illicit trade. However, small-parcel smuggling still shaves 0.8 percentage points off CAGR potential.

Which regions generate the most demand for replacement components?

The Eastern Province leads with roughly one-third of national turnover, followed by the Riyadh Region at 30% and the Western Province at about oen-fourth, while Northern and Southern areas collectively contribute the remaining 10%.

Page last updated on: