Saudi Arabia Automobile Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

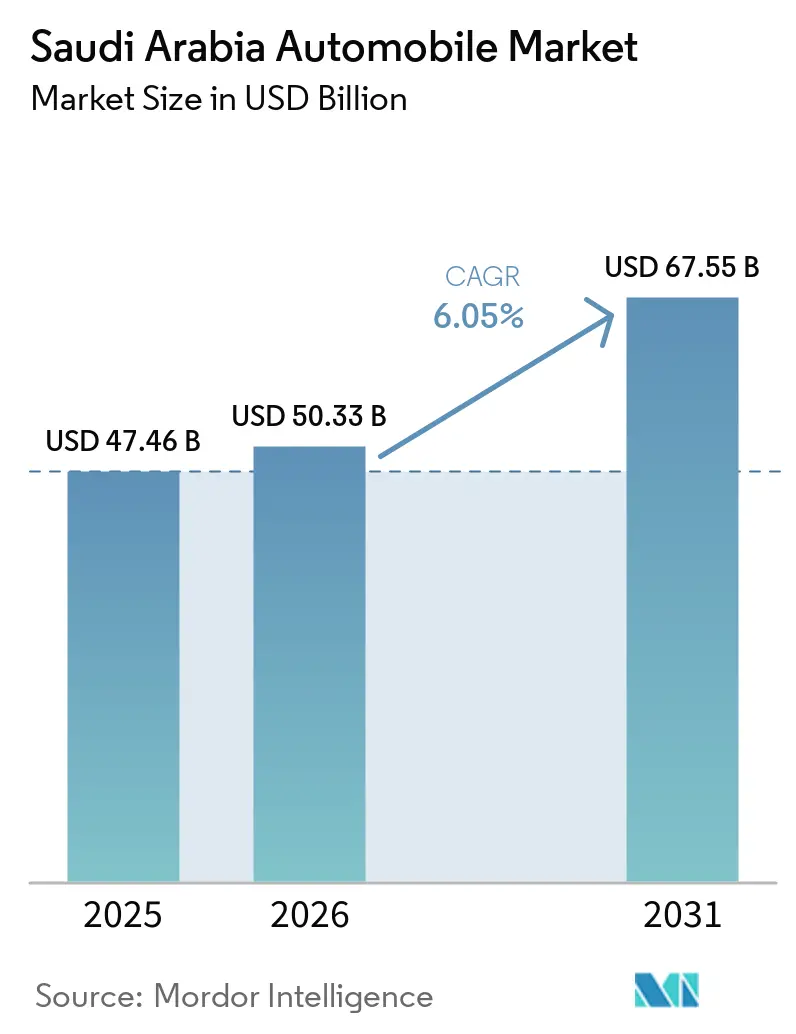

| Base Year Market Size (2025) | USD 47.46 Billion |

| Market Size (2026) | USD 50.33 Billion |

| Market Size (2031) | USD 67.55 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Automobile Market Analysis by Mordor Intelligence

The Saudi Arabia Automobile Market size was valued at USD 47.46 billion in 2025 and estimated to grow from USD 50.33 billion in 2026 to reach USD 67.55 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Vision 2030 investments, rising household income, and expanded female labor force participation underpin the increased demand. Passenger cars dominate current volumes, yet electric‐vehicle (EV) incentives and localized production commitments from Lucid and Ceer herald an accelerated power-train transition. Rapid Chinese brand penetration heightens competitive intensity and compresses dealer margins, while digital retail platforms recast the traditional purchase journey. Simultaneously, subscription and fleet models mature as younger consumers favor flexible access over outright ownership, and public-transport upgrades influence modal choices.

Key Report Takeaways

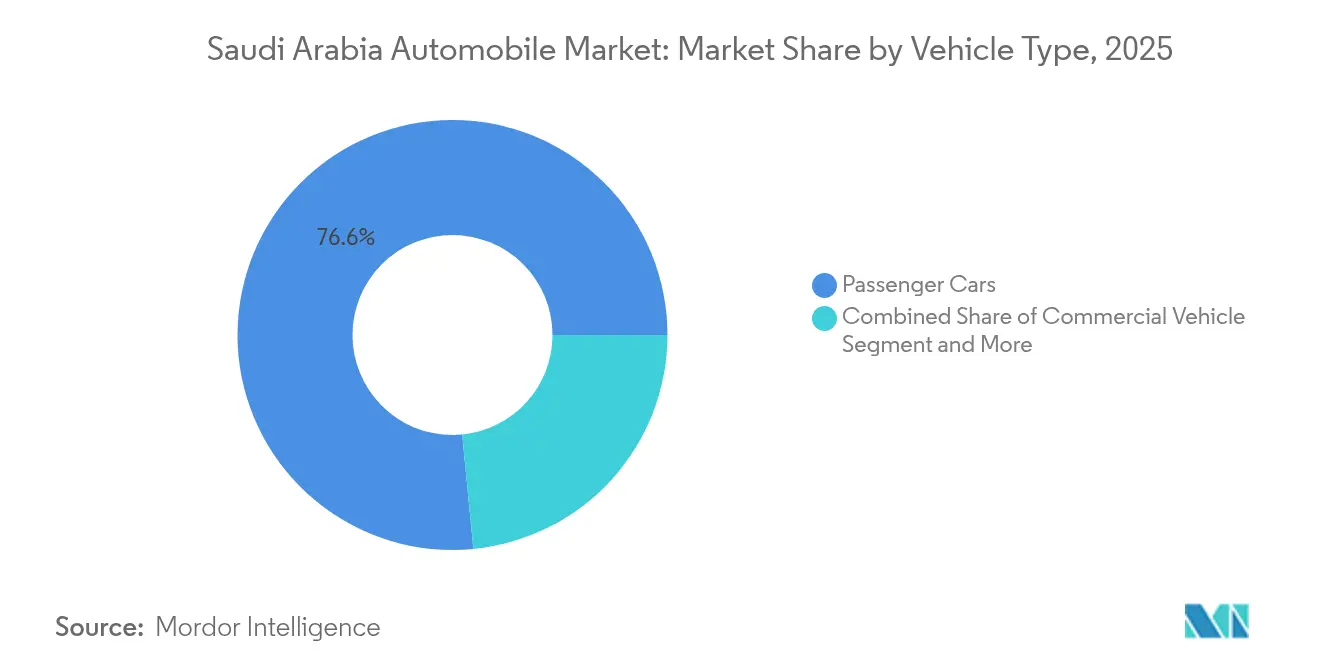

- By vehicle type, passenger cars held a 76.55 % share in the Saudi Arabia Automobile market in 2025; passenger cars are projected to advance at a 6.12 % CAGR through 2031.

- By propulsion type, internal combustion engines commanded 86.35 % share in the Saudi Arabia Automobile market in 2025, while electric vehicles is expected to record the fastest 6.32 % CAGR to 2031.

- By application, personal use accounted for a 70.85 % share in the Saudi Arabia automobile market in 2025 and public transport is rising at a 6.2 % CAGR through 2031.

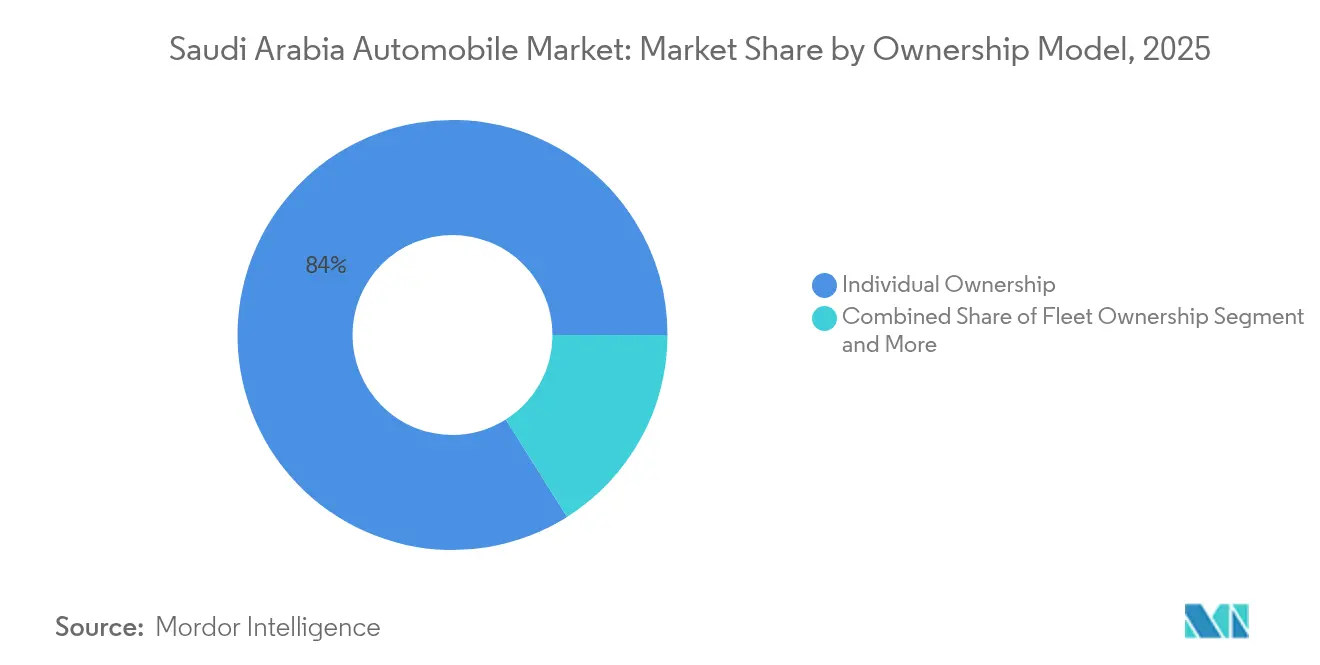

- By ownership model, individual ownership represented an 83.95 % share in the Saudi Arabia Automobile market in 2025; subscription services post a 6.27 % CAGR during the forecast horizon.

- By sales channel, OEM dealers secured a 60.60 % share in the Saudi Arabia Automobile market in 2025, whereas online platforms grow at a 6.18 % CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Automobile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Disposable Income-Levels | +1.8% | National, with early gains in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Vision 2030 Investments | +1.5% | KAEC, NEOM, King Salman Energy Park | Long term (≥ 4 years) |

| Government Incentives | +1.2% | Urban centers: Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| SUV/Off-Road Preference | +0.9% | National, particularly rural and desert regions | Short term (≤ 2 years) |

| Growth Of Subscription-Based Ownership | +0.7% | Major cities with expatriate populations | Short term (≤ 2 years) |

| Fleet Digitalisation Driving Predictive-Maintenance Upgrades | +0.6% | Commercial hubs and logistics corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Disposable Income & Lifting of the Women-Driving Ban

Female labor-force participation climbed steadily after 2018, prompting households to shift from single to multi-car ownership. Concurrently, higher per-capita income expanded financing eligibility and boosted dealer footfall. The Saudi Central Bank recorded a huge investment in corporate lending during March 2025, supporting consumer liquidity for vehicle purchases. New policy flexibility also stimulated ancillary demand for insurance, aftermarket parts, and service contracts. Combined, these factors create a reinforcing feedback loop that sustains annual showroom traffic even as economic diversification alters employment patterns[1]Saudi Central Bank, “Monthly Statistical Bulletin March 2025,” sama.gov.sa .

Vision 2030 Investments & Influx of Automotive FDI

The Public Investment Fund earmarked for automotive projects through 2035, catalyzing large-scale assembly and components initiatives inside King Abdullah Economic City. Lucid’s 150,000-unit annual plant and Ceer’s complex will embed R&D, logistics, and supplier ecosystems locally. Special Economic Zone incentives minimal corporate tax for 20 years and customs relief—further improve investor economics. These greenfield commitments reduce import dependency over time and foster skill transfer to a domestic workforce[2]Public Investment Fund, “PIF Annual Report 2025,” pif.gov.sa.

Growth of Subscription-Based Ownership Among Young/Expat Users

Platforms such as Carasti and Key streamline vehicle access into a single monthly fee covering insurance, maintenance, and roadside assistance. Users enjoy the flexibility to swap models seasonally, aligning with expatriate work-contract cycles and emerging consumer aversion to long-term liabilities. OEMs and large dealer groups pilot white-label subscription plans to capture residual value and data on usage behavior, which informs targeted up-selling at contract renewal[3]Carasti, “Subscription Adoption Trends 2025,” carasti.com.

Fleet Digitalization Driving Predictive-Maintenance Upgrades

Logistics operators adopt telematics and AI-driven diagnostics to optimize routes and prolong asset life. Zain KSA’s 100 % Saudi-developed fleet solution integrates GPS, driver behavior analytics, and predictive maintenance alerts, cutting unplanned downtime. OEMs embed over-the-air update capabilities in new commercial models to secure after-sale software revenue. These efficiency gains reduce operating costs and free capital for fleet expansion across parcel, grocery, and ride-share verticals[4]Zain KSA, “Fleet Management Solutions Overview,” zain.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import-Dependent Supply Chain | -1.1% | National, particularly port cities | Short term (≤ 2 years) |

| Margin Squeeze From Rapid Chinese-Brand Penetration | -0.9% | Competitive pressure across all regions | Short term (≤ 2 years) |

| High EV Sticker-Price And Sparse Charging Network | -0.8% | Urban centers and intercity routes | Medium term (2-4 years) |

| Emission-Linked Fees & Mandatory 3-Year Insurance | -0.5% | National regulatory compliance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Import-Dependent Supply Chain & Logistics Bottlenecks

Over a million vehicles entered Saudi ports during the 15 months to March 2024, reflecting the scale of the automotive industry in Saudi Arabia. Congestion, container shortages, and geopolitical flashpoints routinely lengthen lead times and escalate freight costs. Although planned inland dry ports and digitized customs clearance ease some friction, multilayered sourcing from Japan, Korea, Germany, and China complicates inventory planning and raises working-capital requirements for dealers.

Margin Squeeze From Rapid Chinese-Brand Penetration

Chinese OEMs lifted combined share from below one-tenth in 2020 to more than the latter in 2024, led by competitive price–feature matrices and aggressive warranty offers, intensifying competition in the automotive industry in Saudi Arabia. Incumbent Japanese and Korean brands respond with rebates and financing incentives, eroding dealer gross margins. Inventory proliferation also inflates marketing expenditure as showrooms allocate floor space to more nameplates. Over time, only scale-efficient networks with robust after-sale capabilities sustain profitability under compressed unit economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Sustain Broad-Based Growth

Passenger cars held 76.55 % of the Saudi Arabia automobile market share in 2025 and are forecast to register a 6.12 % CAGR through 2031 as rising female mobility needs and multi-car households support sustained purchasing cycles. Commercial vehicle demand tracks infrastructure and e-commerce logistics expansion, with heavy-duty trucks supplied by global players such as Tata Daewoo entering local partnerships. Two-wheelers remain marginal owing to cultural preferences and safety perceptions, although courier firms explore scooter fleets for last-mile delivery. Three-wheelers stay niche, hampered by road-design norms favoring larger vehicles. Off-highway equipment sees cyclical peaks linked to mining and mega-project workloads.

Although passenger cars lead volumes, the margin per unit in the SUV crossover sub-segment exceeds sedan averages, incentivizing OEMs to load high-spec trims. Enhanced financing availability and low default ratios improve bank appetite for auto loans at competitive rates, amplifying the Saudi Arabia automobile market’s expansion path. Concurrently, spare-parts suppliers and service centers gravitate to cities with dense passenger car clusters, reinforcing aftermarket revenue pools.

By Propulsion Type: ICE Dominance Meets Electric Inflection

Internal combustion engines accounted for 86.35 % of the Saudi Arabia automobile market size in 2025. Favorable fuel prices, familiarity, and extensive service infrastructure underpin the incumbent advantage. Yet EVs, propelled by a 6.32 % CAGR, shift the propulsion mix as local output from Lucid and Ceer tempers price gaps and shortens delivery times. Hybrid offerings provide an interim alternative, but limited model range and moderate tax benefits restrain rapid uptake.

Ceer’s plan to integrate 45 % local content intensifies supplier localization for battery packs, inverters, and thermal-management subsystems. The Saudi Green Initiative’s three-tenth EV sales target by 2030 adds policy certainty and compels OEMs to advance product roadmaps. Notwithstanding, high ambient heat necessitates enhanced cooling loops and battery chemistries, raising component bills and slowing parity with ICE sticker prices.

By Application: Personal Mobility Commands Volume; Public Transport Gains Pace

Personal use comprised 70.85 % of 2025 automotive registrations, reflecting cultural reliance on private vehicles and limited mature transit alternatives. Public transport showings scale at a 6.2 % CAGR through 2031 on the back of Jeddah’s 91 new buses and Riyadh Metro progress. Commercial fleet operators upgrade units to comply with new fuel-efficiency benchmarks and telematics mandates. Industrial uses, including mining and hydrocarbon operations, sustain baseline demand for heavy-duty pickups and off-highway trucks.

The Saudi Arabia automobile market size for public transport stands to widen further as municipalities phase in low-emission bus fleets backed by soft financing from the Public Investment Fund. Personal mobility nevertheless retains primacy, spurring tire, oil, and accessory sales within the independent aftermarket channel.

By Ownership Model: Individual Dominance Endures; Subscriptions Bloom

Individual ownership delivered 83.95 % of the 2025 registration tally and benefits from favorable loan-to-value regulations and competitive insurance products. Subscription services achieve a 6.27 % CAGR by simplifying access: a fixed monthly fee covers usage, maintenance, and insurance, addressing expatriate turnover and millennial preference for asset-light living. Fleet ownership encompasses government authorities, rent-a-car operators, and corporate entities leveraging bulk procurement and centralized maintenance.

Subscription platforms act as data conduits, collecting telemetry that informs OEM design tweaks and residual-value calibration. Banks partner with these platforms to structure asset-backed revolving credit lines, demonstrating institutional recognition of emerging business models within the Saudi Arabia automobile market.

By Sales Channel: OEM Dealers Lead; Digital Platforms Accelerate

OEM dealers retained 60.60 % of transactions in 2025. Established workshop networks and brand warranties reinforce consumer trust. Online channels, though only a fraction of total volumes, grow at a 6.18 % CAGR as Syarah, Motor Souq, and Silaa provide transparent pricing and end-to-end financing checkout. Independent dealers focus on used-car arbitrage and niche imports, while direct-to-consumer pilots remain small.

Dealers increasingly adopt omnichannel strategies, such as virtual showrooms, home test drives, and e-contracting, to match digital competitor convenience. Simultaneously, refurbishment hubs like Syarah’s new 100,000 sq m facility professionalize used-vehicle reconditioning, lifting residual values, and amplifying cross-border export options to neighboring Gulf markets.

Geography Analysis

Riyadh is the largest demand center, benefiting from governmental hiring, expansion of financial services, and tech-sector clustering. Metro construction lowers congestion on arterial routes yet triggers replacement demand for smaller commuter models. The EVIQ charging network prioritizes Riyadh ring roads, granting early-mover advantage to EV dealerships. Jeddah follows as the western gateway, where port throughput supports wholesale imports and domestic redistribution. The city’s newly added 383 bus stops stimulate public fleet upgrades, spurring procurement of low-emission buses and dedicated maintenance contracts.

Eastern Province hubs Dammam, Dhahran, and Khobar draw high-income energy workers who purchase premium SUVs and pickups. King Abdullah Economic City hosts Lucid’s factory and Ceer’s supplier park, positioning the corridor as an automotive manufacturing nucleus. Access to Bahrain and Kuwait encourages cross-border sales and service agreements, expanding the Saudi Arabia automobile market’s regional footprint. NEOM, while still in construction, outlines autonomous-vehicle and hydrogen-fuel pilot programs, hinting at disruptive modalities in the second half of the decade. Secondary cities such as Medina, Taif, and Abha attract vehicle purchases linked to tourism and public-sector employment growth. The Medina bus rapid transit blueprint indicates decentralization of sustainable mobility spending beyond the three significant metro areas. Rural provinces maintain an outsized demand for high-clearance SUVs with desert-tuned suspension due to gravel roads and extreme heat, while also lagging in EV adoption, given sparse charging availability. Collectively, spatial consumption patterns reaffirm that infrastructure investment directionality, population growth, and income dispersion dictate automotive sales distribution.

Competitive Landscape

Global incumbents—Toyota, Hyundai, Nissan—retain brand equity built on perceived reliability and low total cost of ownership. They anchor extensive service networks and command favorable inventory financing from local banks. Nonetheless, Chinese marques have expanded Saudi Arabia's automobile market share to one-fifth by bundling advanced infotainment and ADAS features into attractive models. BYD's partnership with Saudi Aramco for battery-tech localization exemplifies how Chinese firms align with national energy diversification agendas.

Lucid leverages its "Made in Saudi" status to tap institutional fleet contracts and premium EV early adopters. Ceer's domestic brand aims for 240,000 units annually by 2030, signaling a sovereign effort to cultivate indigenous R&D and supply-chain depth. Japanese suppliers fast-track hybrid powertrain introductions to pre-empt carbon-tax escalation. Dealer groups respond to narrowing margins by consolidating showrooms, investing in certified used-vehicle programs, and diversifying into subscription fleets.

Digital disruptors intensify competition. Syarah's Series C haul is a considerable investment, which underwrites AI-driven price valuation tools and nationwide reconditioning. Motor Souq aggregates 120+ dealers, delivering transparent market intelligence and frictionless comparison shopping. Independent aftermarket players adapt through e-commerce storefronts and on-demand service booking apps. Strategic differentiation now hinges on localized manufacturing, digital customer engagement, and sustainable powertrain portfolios rather than pure scale economics.

Saudi Arabia Automobile Industry Leaders

Toyota Motor Corporation

Hyundai Motor Co.

Nissan Motor Co., Ltd.

General Motors

SAIC-MG Motor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Jeddah Transport Company launched a 91-bus network, including three electric units, expanding routes from 6 to 14 and stops from 46 to 383. The company's target annual ridership is 9 million.

- February 2025: Ceer signed SAR 5.5 billion (USD 1.4 billion) in supplier deals at the PIF Private Sector Forum, locking in 45 % localization ahead of its 2026 model debut.

- February 2025: Masarat Mobility Park unveiled a 2 million m² automotive cluster at King Abdullah Economic City to attract component, testing, and mobility-service tenants.

Saudi Arabia Automobile Market Report Scope

| Two-Wheeler |

| Three-Wheeler |

| Passenger Cars |

| Commercial Vehicle |

| Off-Highway Vehicles |

| Internal Combustion Engine |

| Hybrid Vehicle |

| Electric Vehicle |

| Personal |

| Commercial |

| Public Transport |

| Industrial Use |

| Individual Ownership |

| Fleet Ownership |

| Subscription-Based |

| Shared Mobility |

| OEM Dealers |

| Independent Dealers |

| Online Platforms |

| Direct-to-Consumer |

| By Vehicle Type | Two-Wheeler |

| Three-Wheeler | |

| Passenger Cars | |

| Commercial Vehicle | |

| Off-Highway Vehicles | |

| By Propulsion Type | Internal Combustion Engine |

| Hybrid Vehicle | |

| Electric Vehicle | |

| By Application | Personal |

| Commercial | |

| Public Transport | |

| Industrial Use | |

| By Ownership Model | Individual Ownership |

| Fleet Ownership | |

| Subscription-Based | |

| Shared Mobility | |

| By Sales Channel | OEM Dealers |

| Independent Dealers | |

| Online Platforms | |

| Direct-to-Consumer |

Key Questions Answered in the Report

How large is the Saudi Arabia automobile market in 2026?

The sector is valued at USD 50.33 billion in 2026 and is projected to reach USD 67.55 billion by 2031.

Which vehicle type sells the most in Saudi Arabia?

Passenger cars command 76.55 % of 2025 registrations, supported by multi-car households and rising female mobility needs.

What is driving electric vehicle uptake?

Purchase incentives, expanding EVIQ charging stations, and local production from Lucid and Ceer combine to push EVs toward a 6.32 % CAGR through 2031.

How are online sales platforms changing car buying?

Sites like Syarah and Motor Souq integrate digital financing and nationwide delivery, helping the online channel grow at 6.18 % CAGR.

Which region sees the highest automotive demand?

Riyadh leads due to its economic scale and infrastructure projects, with Jeddah and the Eastern Province following closely.

What challenges limit market growth?

Import-based supply chains, premium EV pricing, and margin pressure from aggressive Chinese entrants act as key headwinds.

Page last updated on: