Saudi Arabia Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

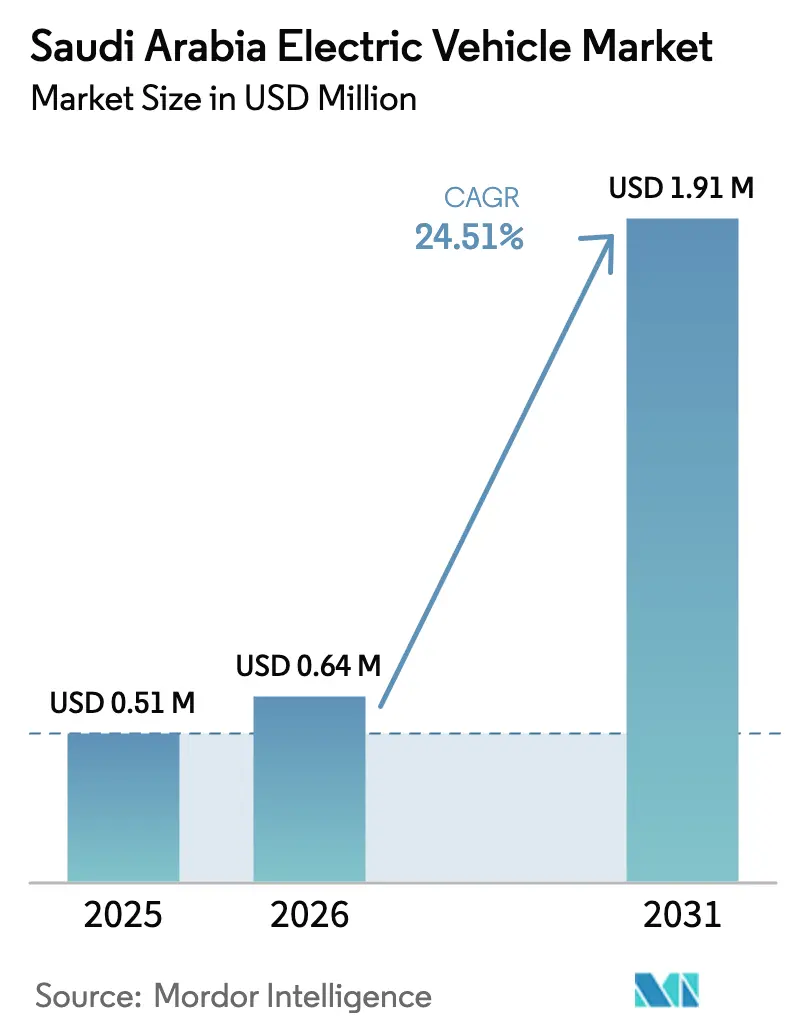

| Base Year Market Size (2025) | USD 0.51 Million |

| Market Size (2026) | USD 0.64 Million |

| Market Size (2031) | USD 1.91 Million |

| Growth Rate (2026 - 2031) | 24.51% CAGR |

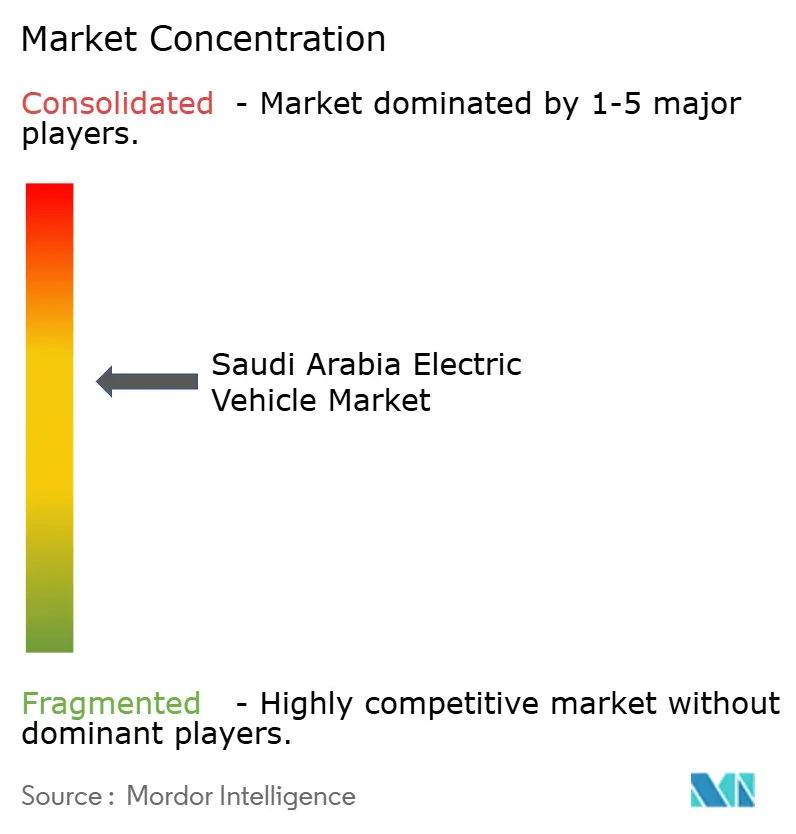

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Electric Vehicle Market Analysis by Mordor Intelligence

The Saudi Arabia electric vehicle market size is expected to grow from USD 0.51 million in 2025 to USD 0.64 million in 2026 and is forecast to reach USD 1.91 million by 2031 at a 24.51% CAGR over 2026–2031. Vision 2030’s mandate that most of Riyadh’s vehicles run on electric power, sovereign capital deployed through the Public Investment Fund (PIF), and a 10-year government purchase commitment for up to 100,000 Lucid units combine to compress the adoption curve. Passenger-car buyers continue to dominate volumes, yet fleet electrification quotas for ride-hailing and state entities accelerate commercial-vehicle uptake. Battery-electric offerings remain the preferred technology in 2025, but hydrogen fuel-cell vehicles gain momentum as the Kingdom leverages its low-cost green-hydrogen plans. Charging build-out, local battery-materials projects in Yanbu, and vertically integrated manufacturing clusters at King Abdullah Economic City anchor a competitive advantage even as extreme summer temperatures and subsidized gasoline temper retail demand.

Key Report Takeaways

- By vehicle type, passenger cars held 76.81% of the Saudi Arabia electric vehicle market share in 2025, while commercial vehicles are forecast to expand at a 24.53% CAGR through 2031.

- By fuel type, battery-electric vehicles captured 55.47% share of the Saudi Arabia electric vehicle market size in 2025, and fuel-cell electric vehicles are projected to register the fastest 24.61% CAGR to 2031.

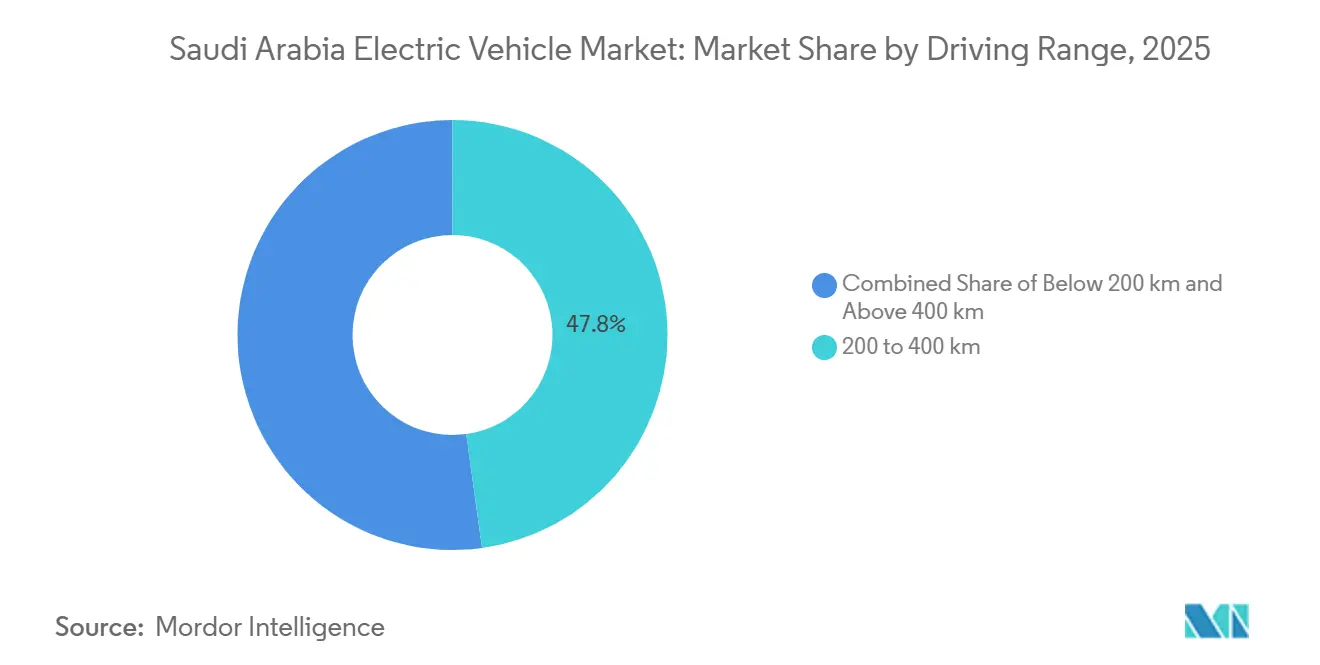

- By driving range, the 200–400 km segment led with 47.83% of the Saudi Arabia electric vehicle market share in 2025; models exceeding 400 km are poised to grow at a 24.63% CAGR.

- By power output, the 100–200 kW band accounted for 45.33% share of the Saudi Arabia electric vehicle market size in 2025, whereas vehicles above 200 kW should advance at a 24.55% CAGR.

- By region, Riyadh commanded 38.73% of 2025 sales, and Jeddah is projected to post the highest 24.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-2030 EV Incentives | +5.2% | National, concentrated in Riyadh, Jeddah, KAEC | Medium term (2-4 years) |

| Rapid Public-Private Charging Build-Out | +4.8% | Riyadh, Jeddah, Dammam; highway corridors to NEOM | Short term (≤ 2 years) |

| Battery-Pack Cost Decline | +4.1% | Global supply chains; Yanbu industrial zone | Long term (≥ 4 years) |

| Mandatory Fleet-Electrification Quotas | +3.9% | Riyadh, Jeddah, Mecca, Medina | Short term (≤ 2 years) |

| PIF-Backed Domestic OEM Launches | +3.7% | King Abdullah Economic City, Riyadh | Medium term (2-4 years) |

| Cross-GCC Green-Mobility Corridors | +2.8% | NEOM, Red Sea Project; UAE-Saudi border zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 EV Incentives & Manufacturing Funds

Sovereign capital fuels localization efforts in Saudi Arabia. The Public Investment Fund (PIF) has committed significant incentives to Lucid and additional funding to its joint venture with Hyundai, effectively mitigating risks associated with OEM capital expenditures. A purchase agreement from the Ministry of Finance ensures the offtake of a substantial number of units [1]Ministry of Finance, “Budget 2025 – Transportation & Infrastructure Allocation,” mof.gov.sa . Concurrently, the Saudi Industrial Development Fund is co-financing factories, and the Human Resources Development Fund is subsidizing labor costs, leading to a considerable reduction in payroll expenses. Furthermore, local-content regulations, endorsed at the 2025 Private Sector Forum, are solidifying supply-chain investments, facilitating a transition from import reliance to domestic manufacturing.

Rapid Public-Private Charging Build-Out

Backed by the Public Investment Fund (PIF) and the Saudi Electricity Company, EVIQ is setting its sights on significantly expanding its fast charger network over the next few years. The momentum is evident with the planned debut of the inaugural highway station along the Riyadh–Qassim corridor in early 2025. Furthermore, Electromin's battery-integrated chargers are paving the way for installations in areas with grid constraints. In Riyadh, an R&D lab is making strides by testing systems at extremely high temperatures, achieving a notable reduction in heat-related charging speed loss by a considerable margin [2]Saudi Electricity Company, “EVIQ Deployment Update,” se.com.sa .

Battery-Pack Cost Decline & Local Cell Projects

In Yanbu, EV Metals is investing USD 905 million to construct a lithium-hydroxide complex, catering to local cell lines [3]BloombergNEF, “Battery Price Survey 2025,” bloomberg.com . Priced at USD 81/kWh, lithium-iron-phosphate chemistries, known for their thermal stability, are well-suited to the Gulf's climate. This not only reduces range degradation but also bolsters the long-term cost advantage of Saudi Arabia's electric vehicle market.

Mandatory Fleet-Electrification Quotas (Ride-Hailing & Government)

Riyadh’s EV target by 2030 translates into binding fleet quotas. Lucid’s government agreement allocates thousands of vehicles annually to official agencies, while Hyundai’s PIF venture is integrated into public procurement pipelines. These mandates generate sizable fleet demand regardless of consumer sentiment, accelerating the Saudi Arabia electric vehicle market’s volume base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Fast-Charging Outside Tier-1 Cities | -3.4% | Rest of Saudi Arabia (excluding Riyadh, Jeddah, Dammam) | Short term (≤ 2 years) |

| Extreme Ambient Temperatures | -2.9% | National, most acute in interior desert regions | Medium term (2-4 years) |

| Persistently Subsidised Gasoline | -2.6% | National | Long term (≥ 4 years) |

| Shortage of EV-Trained Service | -2.1% | National, concentrated in secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sparse Fast-Charging Outside Tier-1 Cities

EVIQ’s initial rollout left secondary cities such as Mecca, Taif, and Abha dependent on home charging, fragmenting the network and limiting intercity travel. Apartment dwellers face steep installation costs, while a 950 km Riyadh–Jeddah corridor remains a “charging desert,” curbing utilization rates for ride-hailing fleets.

Extreme Ambient Temperatures Degrading Battery Life

Research from the University of Michigan reveals that traditional lithium-ion batteries experience a significant capacity loss with every rise in temperature. This leads to a noticeable reduction in performance during the sweltering summers of Saudi Arabia. While innovative liquid-cooling systems have managed to reduce this capacity penalty to a minimal level, they come at a steep price, increasing vehicle costs substantially and subsequently driving up insurance premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Shift Growth Trajectory

Commercial vehicles represented a smaller base in 2025, yet their 24.53% forecast CAGR outpaces the Saudi Arabia electric vehicle market size. Passenger cars retained a 76.81% Saudi Arabia electric vehicle market share due to early adopter households and government sedans. Commercial gains stem from ride-hailing quotas and logistics demand, with BYD light vans undercutting diesel rivals on five-year TCO. Hydrogen truck pilots aim to overcome payload losses from lithium-ion batteries, while depot-based e-buses serve NEOM and the Red Sea complex.

Fleet economics tilt adoption: centralized overnight charging reduces peak-tariff exposure, warranty management is streamlined, and kilometer accumulation accelerates parity with subsidized gasoline. SUVs dominate passenger uptake because higher ground clearance and cabin space suit desert terrain. Conversely, luxury sports models such as Lucid Air remain niche status symbols that showcase Saudi manufacturing capability rather than volume drivers.

By Fuel Type: Hydrogen Emerges as Strategic Hedge

Battery-electric vehicles commanded a 55.47% share in 2025, supported by global supply chains and pack costs that dipped to USD 99/kWh. Fuel-cell electric vehicles are projected to log a 24.61% CAGR, the fastest among propulsion options, as Saudi Arabia couples abundant renewable power with green-hydrogen production. BYD’s agreement with Saudi Aramco anchors technology localization, while Hyundai plans a hydrogen ecosystem with Air Products Qudra.

FCEVs’ three-minute refuels appeal to freight operators, yet public hydrogen stations remain absent, restricting current deployments to captive fleets. Plug-in hybrids continue as a transitional choice, though their relative economics fade as fast-charging spreads. The Saudi Arabian electric vehicle industry thus positions hydrogen as insurance against lithium volatility and foreign cell supply shocks.

By Driving Range: Long-Range Models Gain Favor

The 200–400 km class led the Saudi Arabia electric vehicle market in 2025 at 47.83%, balancing price and daily-use practicality. Vehicles above 400 km range should expand at 24.63% CAGR as intercity corridors open and buyers seek a buffer against minimal heat-related capacity loss. Lucid’s 883 km flagship proves long-range feasibility, but mass-market makers target 400–500 km at sub-USD 40,000.

A 200 km regulatory minimum limits micro-EVs, pushing OEMs toward larger packs. Highway-charger scarcity still curtails sub-400 km models for cross-regional travel, yet growing villa ownership of home chargers fuels urban commuting. BYD’s Seal and Han, both with above 400 km range, illustrate how competitive pricing can scale long-range adoption.

By Power Output: Performance Tier Accelerates

Models in the 100–200 kW band held 45.33% of Saudi Arabia electric vehicle market share in 2025, fitting typical family SUVs. Outputs above 200 kW are poised to climb at 24.55% CAGR, buoyed by luxury entrants such as Porsche Taycan and Mercedes-Benz EQS. Ceer’s planned sedans will straddle the 100–200 kW sweet spot, while Lucid’s 828 kW halo product demonstrates the ceiling of local engineering prowess.

Cultural preference for high-horsepower vehicles sustains demand for dual-motor configurations capable of maintaining 120 km/h cruise speeds across long highways. Conversely, sub-100 kW offerings remain marginal because they underperform on high-speed roads and carry limited resale appeal.

Geography Analysis

Riyadh’s dominant 2025 position stems from ministry fleets and high-income households with a share of 38.73% in 2025, yet the city’s sprawl demands thousands of additional public chargers to meet an EV target by 2030. EVIQ’s R&D center in the capital validates heat-resilient hardware, and Tesla’s 2025 launch highlights local appetite for software-defined mobility. However, apartment dwellers lacking dedicated parking slow penetration.

Jeddah’s marine gateway status propels it to the fastest-growing regional node, with a robust CAGR of 24.57% till 2031. The KAEC manufacturing base attracts tier-1 suppliers, while Red Sea zero-emission mandates create captive demand for buses, service vehicles, and guest transport. BYD’s rapid showroom expansion taps coastal affluence and tourist flows to Mecca and Medina.

Outside the top two metros, Dammam anchors the Eastern Province, but Taif, Abha, and interior towns await charging infrastructure. A UAE–Saudi grid interconnect due in Q4 2027 will lower cross-border range anxiety. NEOM’s car-free model, powered entirely by renewables, offers demonstrator data that can shorten rollout timelines in conventional cities.

Competitive Landscape

Saudi Arabia's electric vehicle market is moderately fragmented. Hyundai, supported by a significant joint venture with PIF, capitalizes on its long-standing relationships with dealers. BYD, offering competitively priced sedans and vans in the affordable segment, collaborates with Aramco to produce localized batteries. Lucid has secured a substantial governmental order, while Ceer, leveraging Foxconn's manufacturing expertise, aims to achieve a high level of local content.

Chinese players XPeng and NIO, with their software-focused designs, grapple with limited service reach. Today's competition among OEMs hinges more on gaining access to sovereign capital, forging charging partnerships, and adhering to SASO standards than on mere product differentiation.

As the industry converges on range and power outputs, battery thermal management and autonomous driving technologies emerge as pivotal battlegrounds.

Saudi Arabia Electric Vehicle Industry Leaders

Nissan Motor Corporation

Tesla Inc.

BMW AG

Lucid Group

Hyundai Motor Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hyundai, in collaboration with PIF, has commenced construction on a USD 500 million plant. The plant aims to assemble 50,000 vehicles each year, and production is slated to kick off in 2026.

- April 2025: Saudi Aramco Technologies Company (SATC), a subsidiary of Aramco, has signed a Joint Development Agreement with BYD to develop technologies aimed at improving efficiency and environmental performance in new energy vehicles.

- February 2025: Ceer Motors secured USD 1.5 billion in local partnerships to finance the production start-up in 2026.

- January 2025: Tesla confirmed entry into Saudi Arabia within months, promising Supercharger deployment to support customers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Saudi Arabia electric vehicle (EV) market covers every new road-worthy automobile that is propelled wholly or partly by electricity stored on board; this includes battery electric, plug-in hybrid, hybrid, and fuel-cell models sold or assembled inside the Kingdom. Vehicles with off-road, two-wheeler, or aftermarket conversion kits are outside this frame.

Scope exclusion: rebuilt or retro-fitted internal-combustion cars do not enter our market size.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Sedan & Hatchback

- SUV and Crossover

- Luxury and Sports

- Commercial Vehicles

- Light Commercial Vans and Pick-ups

- Medium and Heavy Trucks

- Buses & Coaches

- Passenger Cars

- By Fuel Type

- Battery Electric Vehicle (BEV)

- Plug-in Hybrid Electric Vehicle (PHEV)

- Hybrid Electric Vehicle (HEV)

- Fuel-Cell Electric Vehicle (FCEV)

- By Driving Range

- Below 200 km

- 200 to 400 km

- Above 400 km

- By Power Output

- Below 100 kW

- 100 to 200 kW

- Above 200 kW

- By Region

- Riyadh

- Jeddah

- Mecca

- Medina

- Rest of Saudi Arabia

Detailed Research Methodology and Data Validation

Primary Research

We interviewed charger installers, franchised dealers, provincial regulators, and fleet managers across Riyadh, Eastern, and Makkah provinces. Discussions clarified shadow-import volumes, fast-charger rollout pace, and average transaction prices, enabling us to refine model assumptions and challenge early desk findings.

Desk Research

Our analysts first mapped the demand pool using public datasets such as Saudi Transport General Authority new-registration files, ZATCA customs import codes, Saudi Central Bank consumer-credit bulletins, and Vision 2030 infrastructure dashboards. Global references, IEA Global EV Outlook, UN Comtrade battery trade tables, and peer-reviewed SAE papers on desert climate battery degradation helped benchmark local ratios. Select paid repositories like D&B Hoovers and Dow Jones Factiva supplied company revenue splits that anchored pricing spreads. These sources illustrate our inputs and are not exhaustive; many additional publications supported data checks.

Market-Sizing & Forecasting

The base year value derives from a top-down reconstruction of provincial new-vehicle registrations, adjusted by verified EV penetration rates, then converted to revenue through surveyed average selling prices. Supplier roll-ups and sample dealer channel checks offer a selective bottom-up view that validates totals. Key variables tracked include charger density per 100 km of highway, average battery pack cost per kWh, Vision 2030 adoption quotas, import duty schedules, and Riyadh household disposable income. A multivariate regression that links these drivers to historical uptake informs the 2025-2030 forecast, while scenario analysis handles policy or price shocks. Gaps where bottom-up evidence is thin are bridged with conservative midpoint estimates reviewed by regional experts.

Data Validation & Update Cycle

Outputs pass variance screens against independent signals such as electricity-demand growth, lithium-ion import tonnage, and OEM financial disclosures. Findings move through two analyst reviews before sign-off. We refresh the model annually and issue interim revisions whenever material events, policy shifts, tax changes, or major plant openings occur.

Why Mordor's Saudi Arabia Electric Vehicle Baseline Commands Reliability

Published estimates often diverge because firms define "market" differently, apply varied pricing ladders, or refresh at contrasting cadences.

Key gap drivers include whether components like chargers or aftermarket parts are bundled, if hybrid vehicles are counted as full EVs, and whether cross-border GCC sales inflate domestic totals. Mordor reports only in-country new vehicle sales at end-buyer prices and updates figures each year, which limits double counting and currency drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.62 million (2025) | Mordor Intelligence | - |

| USD 2,343.7 million (2024) | Global Consultancy A | Includes chargers, batteries, and commercial two-wheelers within headline value |

| USD 560 million (2024) | Industry Databook B | Uses ex-factory shipment prices and excludes government fleet orders |

| USD 9.25 billion (2023) | Regional Consultancy C | Aggregates wider GCC sales and counts future plant investment outlays as current revenue |

The comparison shows that once inconsistent scopes and pricing bases are stripped away, Mordor's disciplined, annually refreshed approach delivers a transparent starting point that executives can trace to clear variables and replicate with confidence.

Key Questions Answered in the Report

What is the projected 2031 value of the Saudi Arabian electric vehicle market?

The market is expected to reach USD 1.91 million by 2031 under a 24.51% CAGR.

Which segment is growing fastest in the Kingdom’s EV mix?

Commercial vehicles are forecast to register a 24.53% CAGR, outpacing passenger cars through 2031.

How large is Riyadh’s contribution to national EV demand?

Riyadh accounted for 38.73% of 2025 sales and targets 30% electric-vehicle penetration by 2030.

Why are hydrogen fuel-cell vehicles gaining attention?

Fuel-cell models hedge against lithium supply risks and can refuel in 3–5 minutes, making them attractive for long-haul fleets.

What are the main barriers to wider EV adoption beyond major cities?

Limited fast-charging outside tier-1 metros, extreme summer heat, subsidized gasoline prices, and a shortage of trained technicians.

Which local projects anchor Saudi EV manufacturing?

Lucid’s AMP-2 plant, Ceer’s 1 million m² complex, and the Hyundai–PIF joint venture at KAEC form the industrial backbone.

Page last updated on: