Saudi Arabia Bus Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 629.68 Million |

| Market Size (2030) | USD 851.84 Million |

| Growth Rate (2025 - 2030) | 6.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Bus Market Analysis by Mordor Intelligence

The Saudi Arabia bus market size is estimated at USD 629.68 million in 2025, and is expected to reach USD 851.84 million by 2030, at a CAGR of 6.23% during the forecast period (2025-2030). Driven by Vision 2030’s urban-mobility funding, the Saudi Green Initiative’s emissions goals and rising congestion in Riyadh and Jeddah. Extensive investment in integrated metro-bus networks, battery-electric charging corridors and hydrogen production capacity is reshaping fleet specifications and stimulating local assembly commitments. Seasonal Hajj and Umrah peaks keep fleet utilization high, while mandatory corporate-shuttle rules create a dependable base of private demand. Competitive intensity is rising as SAPTCO’s public contracts face liberalized intercity licensing that allows Chinese, European and local challengers to target the same tenders. Infrastructure roll-outs, subsidy programs and autonomous-shuttle pilots are positioning the Saudi Arabia bus market as a testbed for next-generation mobility solutions despite structural headwinds such as high e-bus capex and consumer preference for cars.

Key Report Takeaways

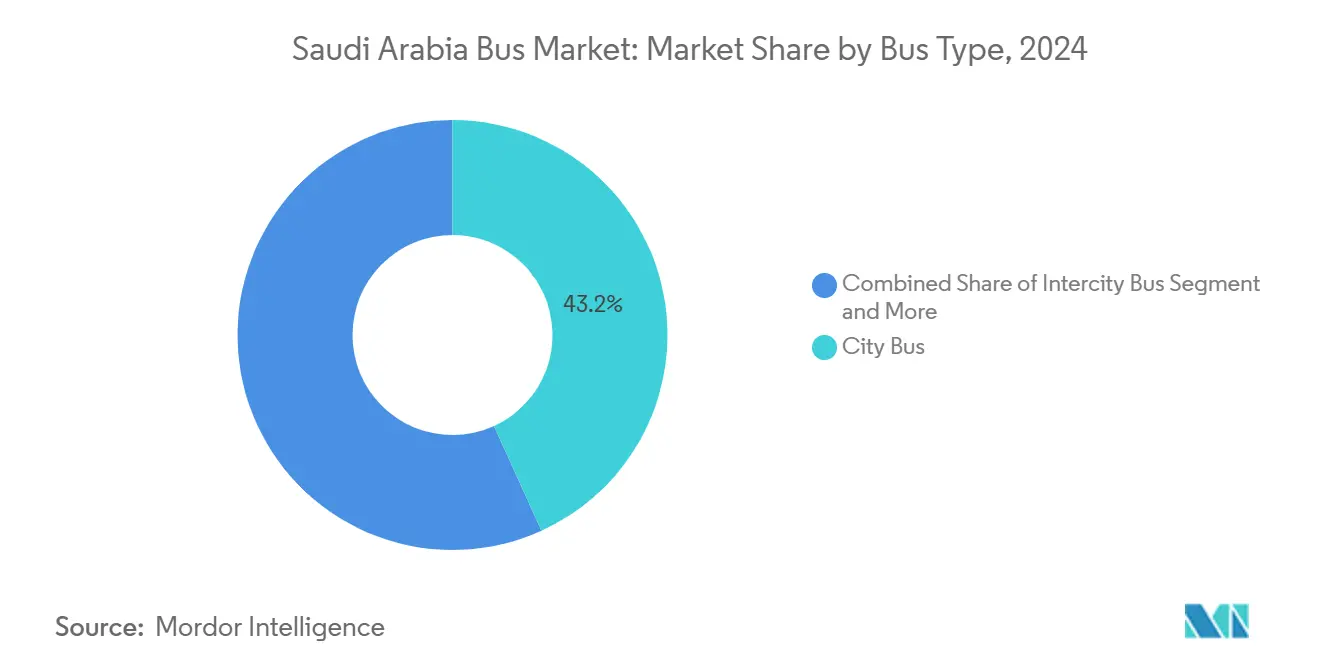

- By bus type, city buses held 43.18% of the Saudi Arabia bus market share in 2024; shuttle buses are projected to expand at a 6.25% CAGR through 2030.

- By propulsion, internal-combustion vehicles retained 77.81% share in 2024, whereas battery-electric buses are advancing at a 6.37% CAGR to 2030.

- By application, public transport accounted for 56.71% of the Saudi Arabia bus market size in 2024 and corporate shuttles are forecast to post a 6.27% CAGR.

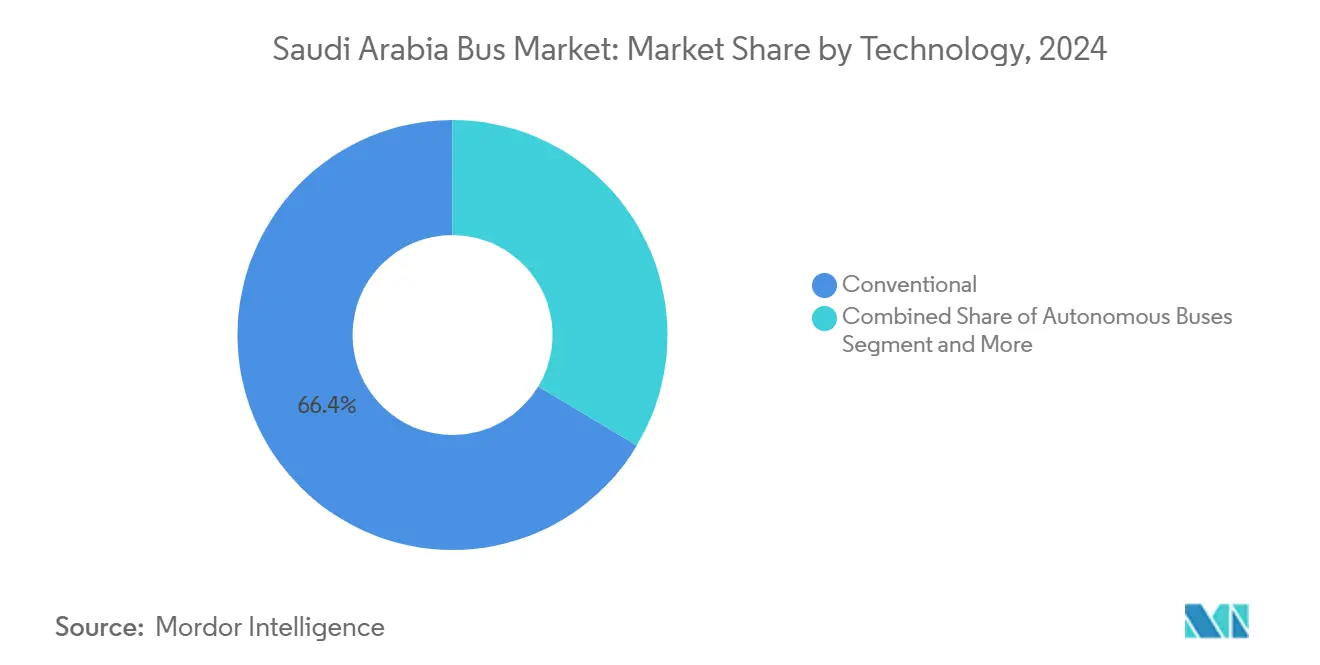

- By technology, conventional platforms dominated with 66.37% share in 2024; autonomous buses deliver the quickest growth at a 6.31% CAGR.

- By seating capacity, the 31–50 seat class captured 53.42% share in 2024, while sub-30-seat models are on track for a 6.33% CAGR through 2030.

Saudi Arabia Bus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Urban-Mobility Investments | +1.8% | National, with concentrated impact in Riyadh, Jeddah, Madinah | Long term (≥ 4 years) |

| Saudi Green Initiative Emissions Targets | +1.2% | National, with priority deployment in NEOM, major cities | Medium term (2-4 years) |

| Rising Urban Congestion | +0.9% | Riyadh metropolitan area, Jeddah urban core | Short term (≤ 2 years) |

| Mandatory Large-Employer Staff-Bus Rules | +0.7% | Industrial clusters, business districts nationwide | Medium term (2-4 years) |

| Hajj/Umrah Capacity Expansion | +0.6% | Makkah, Madinah, connecting transport corridors | Short term (≤ 2 years) |

| NEOM Autonomous-Shuttle Deployments | +0.4% | NEOM megacity, potential spillover to other smart cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Urban-Mobility Investments

Vision 2030 earmarks for public-transport projects, making state funding the single biggest catalyst for fleet renewal. The King Abdulaziz Project integrates six metro lines with an 842-bus grid and 80 routes that guarantee multi-year procurement pipelines for OEMs. SAPTCO’s contracts in Al-Ahsa, Tabuk and Madinah illustrate how provincial tenders mirror capital-city standards, encouraging suppliers to invest in local knock-down assembly and driver-training subsidiaries. Madinah’s BRT plan targets close to 500 stations and up to four-fifths area coverage by 2030, creating predictable volume for chassis, bodywork and telematics vendors. This infrastructure-first policy underpins the Saudi Arabia bus market by aligning fiscal outlays, emissions mandates and economic-diversification targets[1]Vision 2030 Secretariat, “Public Transport Projects Overview,” Vision2030.gov.sa.

Saudi Green Initiative Emissions Targets

The Saudi Green Initiative’s 2060 net-zero pledge compels operators to pivot from diesel to electric and hydrogen platforms. NEOM Green Hydrogen Company will deliver 600 t/day of renewable H₂ by 2026, a scale that supports intercity fuel-cell buses. EVIQ’s plan to install 5,000 DC fast chargers by 2030 removes range anxiety for electric fleets on major corridors. Yutong supplied the first battery-electric bus to Jeddah’s public network in 2023, validating technology performance in harsh climates and opening the door for wider fleet bids. Regulatory alignment, such as SASO’s adoption of IEC standards for high-voltage components, further de-risks investment for international suppliers. These measures accelerate the Saudi Arabia bus market transition even as legacy diesel assets remain dominant[2]Saudi Green Initiative, “Net-Zero Pathways,” SGI.gov.sa.

Rising Urban Congestion in Riyadh & Jeddah

Average arterial saturation in Riyadh jumped from one-tenth in 1996 to two-thirds in 2021, pushing economic losses from traffic delays slightly in a year. Similar patterns in Jeddah raise the urgency for high-capacity city-bus lines and dedicated BRT lanes. Health impacts from PM10 and SO₂ exposure are prompting local authorities to pair congestion relief with low-emission fleet mandates. Smart-signal prioritization and real-time passenger information systems are making public transit more reliable, but academic evidence shows socio-economic factors still outweigh service quality in modal choice. Consequently, policy makers bundle road-pricing studies and parking-scarcity initiatives with bus-network expansion to shift commuter behavior more decisively[3]Royal Commission for Riyadh City, “Riyadh Transport Factsheet 2025,” RCRC.gov.sa.

Mandatory Large-Employer Staff-Bus Rules

Regulations obligate companies above defined workforce thresholds to provide commuter shuttles, generating price-inelastic demand across Riyadh’s business districts and Eastern-Province industrial zones. Corporate fleets are shifting from cost-compliance to employee-experience tools, equipping buses with Wi-Fi, reclining seats and route-optimization software. The rules underpin the fastest-growing application segment at a robust CAGR and support the Saudi Arabia bus industry by smoothing cash-flow profiles for operators who might otherwise rely solely on volatile public tenders. Telematics suppliers likewise benefit as employers insist on punctuality and safety metrics for ESG reporting compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex For E-Bus | -1.1% | National, with acute impact in budget-constrained municipalities | Medium term (2-4 years) |

| Sparse Charging / H₂ Infrastructure | -0.8% | Rural corridors, secondary cities with limited grid capacity | Short term (≤ 2 years) |

| Lengthy Government-Tender Cycles | -0.6% | National procurement processes, municipal contracts | Short term (≤ 2 years) |

| Cultural Bias Toward Private Cars | -0.4% | Urban centers, particularly Riyadh and Jeddah | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for E-Bus & Fuel-Cell Fleets

Electric and hydrogen buses cost 2-3 times diesel models, stretching municipal budgets and dampening tender volumes outside flagship projects. Total cost of ownership calculations improve with fuel subsidies and maintenance savings, yet residual-value uncertainty still deters leasing firms. Fuel-cell platforms add complexity through cryogenic storage, technician re-skilling and specialized depots. Vision 2030 funding offsets some pain, and battery prices have fallen by one-tenth annually since 2018, but until local content rules spur scalable production the capex gap remains the most material brake on the Saudi Arabia bus market.

Sparse Charging / H₂ Infrastructure

As of 2025, EVIQ’s network clusters around Riyadh, Jeddah and the Dammam corridor, with rural grids lacking capacity for overnight depots. Hydrogen infrastructure is scarcer still; SAT’s single H₂ pilot route shows technical feasibility yet no commercial break-even. The timing mismatch between bus procurement and charger deployment pushes operators toward plug-in hybrids or diesel until corridor coverage matures. Grid upgrades, solar-plus-storage micro-stations and green-hydrogen hubs in NEOM will ease constraints mid-decade, but operators outside mega-projects must bridge the infrastructure gap alone, tempering near-term electrification.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bus Type: City Buses Lead Urban Transformation

City buses represented 43.18% of the Saudi Arabia bus market share in 2024 due to Riyadh, Jeddah and Dammam network build-outs under Vision 2030. The Riyadh Bus grid alone deploys 840 vehicles across 80 routes, demonstrating scale economics that favor standard 12-meter low-floor platforms with EURO VI or battery-electric drivelines. Fleet renewal aligns with air-quality mandates and congestion-pricing pilots that tilt travel demand toward high-frequency trunk lines. Tourist districts and mixed-use mega-projects embed dedicated busways in their master plans, further locking in demand for urban models.

Shuttle buses post the fastest 6.25% CAGR to 2030 in response to employer-transport obligations. Compact wheelbases, 25-seat layouts and luxury interiors cater to staff mobility in petrochemical zones and techno-parks. Seasonal pilgrim shuttles during Hajj and Umrah also employ high-utilization shuttle sub-fleets, supported by real-time dispatch and geofencing to manage security cordons. Intercity coaches benefit from Transport General Authority licensing reforms that open profitable routes such as Riyadh-Abha to private bids, diluting SAPTCO’s legacy share but expanding overall supply.

By Propulsion Type: Electrification Accelerates Despite ICE Dominance

Internal-combustion platforms held 77.81% share in 2024, underscoring entrenched depot infrastructure and technician skill sets. Yet battery-electric models grow at 6.37% CAGR as charger density, procurement subsidies and carbon-pricing pilots improve economics. The NEOM test fleet validates 350 km range with air-conditioning loads in 45 °C summers, easing performance doubts. Saudi Arabia bus market size for battery-electric units is poised to triple by 2030 as EVIQ’s highway fast-chargers connect Riyadh-to-Dammam corridors.

Fuel-cell buses remain in pilot stage; however, NEOM’s green-hydrogen output could support 1,200 long-haul coaches annually by 2028. Plug-in hybrids serve as stop-gap solutions for secondary cities where partial electrification satisfies emissions quotas without grid upgrades. The propulsion mix gradually tilts cleaner but preserves diesel for remote mining and defense deployments where refueling infrastructure is scarce.

By Application: Public Transport Drives Core Demand

Public networks absorbed 56.71% of the Saudi Arabia bus market size in 2024 as state budgets financed fleet replacements, smart-ticketing and bus-priority lanes. Integrated fare media across metro, tram and bus improve ridership stickiness, while digital-twin asset management optimizes maintenance windows. Hajj and Umrah pilgrim shuttles leverage identical telematics, enabling asset redeployment once peak season ends.

Corporate shuttles expand at 6.27% CAGR, propelled by Ministry of Transport compliance audits and HR departments viewing commute quality as a retention lever. Fleets adopt reclining seats, USB charging and 4G routers, blurring lines between fixed-route buses and on-demand vans. School operations migrate toward GPS safety monitoring, while tourism circuits in AlUla and Diriyah commission specialty coaches with panoramic glazing and all-terrain suspensions.

By Technology: Smart Systems Gain Traction

Conventional drivetrains plus basic CAN-bus diagnostics still dominate 66.37% of 2024 fleet count, but every new tender specifies remote condition monitoring, over-the-air updates and passenger Wi-Fi. Smart buses integrate predictive maintenance that enhances uptime by up to one-fifth in pilot data from SAPTCO’s Madinah depot. In-vehicle infotainment combined with MaaS-platform APIs improves occupancy forecasting, reducing dead-heading.

Autonomous shuttles clock a 6.31% CAGR to 2030, beginning with restricted-speed campus loops in NEOM and AlUla. L4-capable LiDAR stacks handle dust storms and high solar glare, while fleet-as-a-service contracts transfer capex risk from transit authorities to tech vendors. The Saudi Arabia bus industry is laying cybersecurity frameworks such as ISO 21434 to safeguard connected fleets, anchoring long-run confidence in driverless operations.

By Seating Capacity: Mid-Size Dominance with Small-Bus Growth

The 31–50 seat bracket captured 53.42% of deliveries in 2024, balancing aisle circulation with capacity targets on core city lines. Uniform body specifications support parts commonality and technician cross-training, lowering total cost of ownership. Double-door layouts speed boarding and align with Riyadh’s all-door ticket-validation pilots.

Sub-30-seat buses grow at 6.33% CAGR, driven by last-mile loops around metro stations and private-compound shuttles. Flexible platform lengths from 7 m to 9 m negotiate narrow heritage-district streets while achieving four-fifths average load factors. Larger >50-seat coaches serve the Riyadh-Makkah-Jeddah pilgrimage trunk where density peaks warrant articulated models.

Geography Analysis

Riyadh dominates volumes through the King Abdulaziz Project, which targets 4.5 million daily riders via six metro lines and 840 feeder buses. Its traffic-congestion economic cost of SAR 21 billion annually underpins public willingness to allocate budget for premium low-floor electrics and BRT lanes. Smart-card adoption jumped to four-fifths of trips in 2025, further solidifying bus patronage.

Jeddah follows with a port-anchored economy and its gateway role for Makkah pilgrims. Seasonal traffic compels operators to lease up to 5,000 extra buses each Ramadan, straining maintenance depots yet offering revenue spikes that offset low-season slack. The city’s Red Sea coastal climate necessitates corrosion-resistant body materials, influencing OEM selection criteria. The Eastern Province clusters petrochemical plants and military bases around Dammam and Jubail, producing stable commuter flows handled mainly by corporate shuttles. Electrification prospects hinge on EVIQ’s highway fast chargers that will bridge 400 km to Riyadh by 2027, opening the door for intercity BEV coaches.

NEOM, although nascent, shapes perception by field-testing autonomous, complete renewable mobility under desert extremes. Suppliers treat pilot orders as reference sites to win mainstream municipal bids later. Secondary cities such as Madinah, Tabuk and Al-Ahsa leverage SAPTCO contracts to mirror Riyadh’s service standards but at lower ridership densities, requiring mixed fleets of 9-m, 12-m and articulated models. Rural routes lag in alternative-fuel uptake due to grid constraints, sustaining diesel penetration above four-fifths of active fleet. Nevertheless, solar-powered micro-depots and mobile hydrogen dispensers trialed in Al-Qassim hint at a step-change once technology costs subside. Nationally, more than four-fifths urbanization concentrates demand geographically, enabling efficient parts logistics but leaving remote regions underserved until subsidy programs expand.

Competitive Landscape

SAPTCO retains the largest fleet and workshop footprint, holding multi-year operating contracts in Riyadh, Madinah and intercity corridors. Its vertical-integration push through driver-training and maintenance subsidiaries raises entry barriers for nascent operators. Yet liberalization allows companies such as Thakher Makkah, RATP Dev and Al-Qassim Transport to contest specific routes, diluting SAPTCO’s revenue share to near half in 2024.

Chinese OEMs BYD, Yutong and King Long target public tenders with aggressive pricing and turnkey charging packages. Yutong’s first electric bus for Jeddah in 2023 proved high-temperature battery performance, unlocking follow-up orders in 2025. European stalwarts Daimler, Volvo and Scania compete on lifecycle cost, emphasizing 600,000 km power-train warranties and digital maintenance platforms. Daimler’s eCitaro trials with SAPTCO highlight localized climate-control adaptations such as high-capacity rooftop HVAC units.

Strategic alliances shape competitive outcomes: EVIQ partners BYD on joint charging corridors; SAPTCO collaborates with RATP Dev on autonomous-shuttle pilots; NEOM awards hydrogen-bus trials to a Daimler-Yutong consortium. Local content requirements of up to two-fifths encourage knock-down assembly proposals near Jeddah Port, with employment creation targets factored into bid scoring. Cyber-security, battery end-of-life recycling and MaaS integration emerge as new frontiers where technology firms can differentiate beyond hardware.

Saudi Arabia Bus Industry Leaders

Daimler Buses

Volvo Buses

Scania

BYD Auto

SAPTCO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Alstom finished design for a 20-tram, battery-powered, catenary-free system in AlUla, integrating HealthHub predictive maintenance for desert operations.

- January 2025: Arabian Contracting Services secured a SAR 563.2 million 10-year deal from the Royal Commission for Riyadh City to monetize interior advertising across metro and bus assets.

- January 2025: SAPTCO appointed Bakr A. Al-Muhanna as Chairman and Eng. Khalid A. Al-Huqail as Managing Director to steer regional growth plans.

Saudi Arabia Bus Market Report Scope

| City Bus |

| Intercity Bus |

| School Bus |

| Tour Bus |

| Shuttle Bus |

| Double-Decker Bus |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Public Transportation |

| Private Fleet |

| School Transport |

| Tourism |

| Corporate Shuttle |

| Conventional |

| Smart / Connected Buses |

| Autonomous Buses |

| Below 30 Seats |

| 31–50 Seats |

| Above 50 Seats |

| By Bus Type | City Bus |

| Intercity Bus | |

| School Bus | |

| Tour Bus | |

| Shuttle Bus | |

| Double-Decker Bus | |

| By Propulsion Type | Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Fuel Cell Electric Vehicle (FCEV) | |

| By Application | Public Transportation |

| Private Fleet | |

| School Transport | |

| Tourism | |

| Corporate Shuttle | |

| By Technology | Conventional |

| Smart / Connected Buses | |

| Autonomous Buses | |

| By Seating Capacity | Below 30 Seats |

| 31–50 Seats | |

| Above 50 Seats |

Key Questions Answered in the Report

What is the projected value of Saudi Arabia’s bus sector by 2030?

Forecasts place the sector at USD 851.84 billion in 2030, reflecting a 6.23% compound annual growth rate from 2025.

Which bus category leads sales in Saudi Arabia and why?

City buses captured 43.18% of 2024 deliveries because Riyadh, Jeddah and Dammam expanded high-frequency urban routes under Vision 2030.

How fast are battery-electric buses growing in Saudi fleets?

Battery-electric units are advancing at a 6.37% CAGR through 2030 as charging corridors and green-energy incentives narrow lifecycle-cost gaps.

What factors are driving demand for corporate shuttle services in the Kingdom?

Mandatory employer transport rules, dense industrial clusters and a focus on employee experience are pushing corporate shuttles toward a 6.27% CAGR.

Which obstacles still hamper large-scale adoption of zero-emission buses?

High capital costs and uneven charging or hydrogen infrastructure remain the biggest hurdles, especially for cash-constrained municipalities and rural corridors.

How competitive is the supplier landscape for buses in Saudi Arabia?

SAPTCO still fields the largest fleet, yet liberalized licensing enables Chinese and European OEMs to win tenders, keeping supplier concentration at moderate levels.

Page last updated on: