Saudi Arabia Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

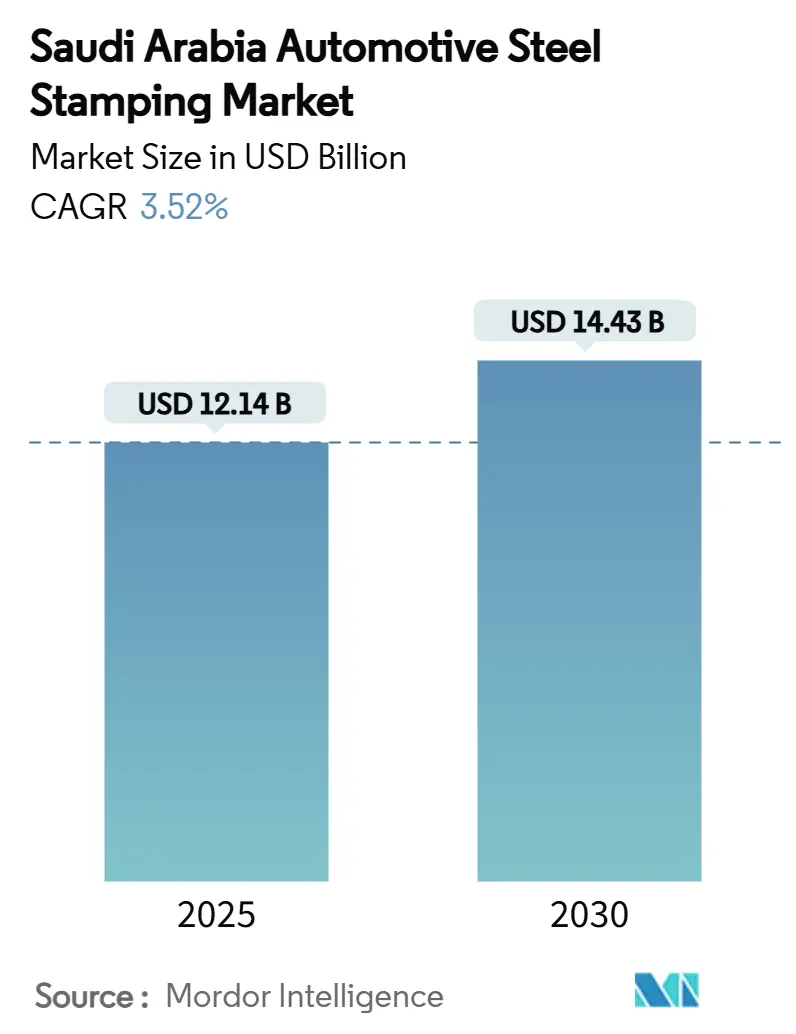

| Market Size (2025) | USD 12.14 Billion |

| Market Size (2030) | USD 14.43 Billion |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Automotive Steel Stamping Market Analysis by Mordor Intelligence

The Saudi Arabia automotive steel stamping market size stands at USD 12.14 billion in 2025 and is projected to reach USD 14.43 billion by 2030, expanding at a 3.52% CAGR during the forecast period. This trajectory reflects the Kingdom’s Vision 2030 push for manufacturing self-sufficiency, a surge of Public Investment Fund (PIF)-backed original-equipment-manufacturer (OEM) investments, and rising localization mandates that anchor production volumes. Blanking continues to dominate technology choices because it underpins most body-in-white panel production, yet hot stamping is gaining strategic ground as OEMs incorporate advanced high-strength steel (AHSS) to meet fuel-efficiency and crash-safety targets. Regional demand is concentrated around Riyadh’s King Salman Automotive Cluster, but Eastern Province facilities enjoy access to competitively priced feedstock through SABIC Hadeed and global seaborne steel flows. Headwinds persist, chiefly volatile steel input costs and price competition from Asian imports, but rising EV output from Lucid and Ceer provides a new demand anchor for precision hot-stamped battery housings and lightweight structures.

Key Report Takeaways

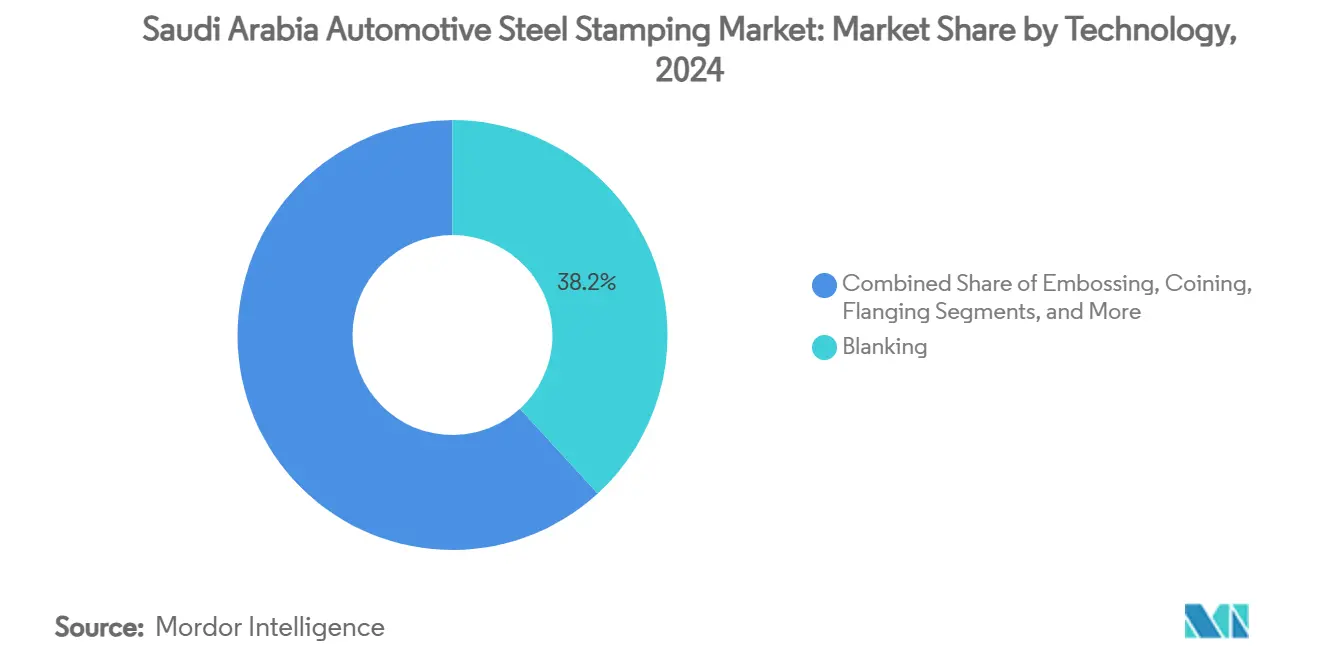

- By technology, blanking led with 38.15% of the Saudi Arabia automotive steel stamping market share in 2024, while embossing is on track to record a 4.65% CAGR through 2030.

- By process, sheet metal forming accounted for 29.44% of the Saudi Arabia automotive steel stamping market size in 2024, whereas hot stamping is forecast to expand at a 5.22% CAGR to 2030.

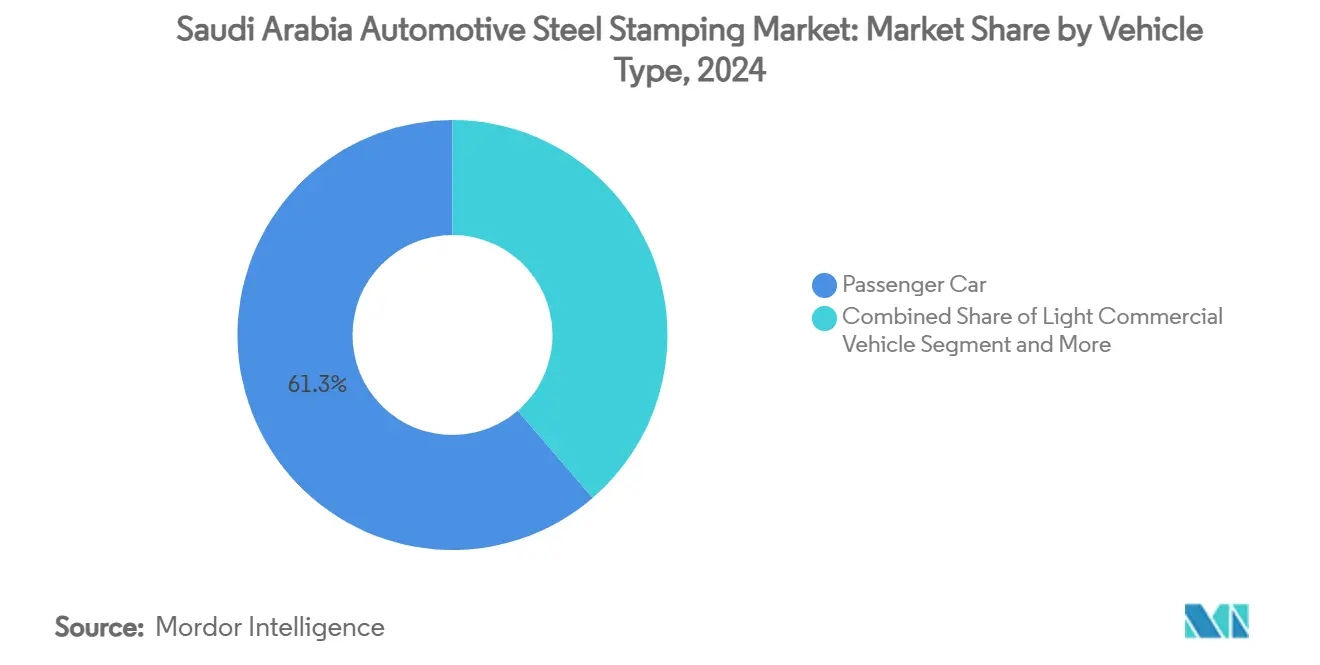

- By vehicle type, passenger cars captured 61.25% of demand in 2024, and are forecast to grow with a 3.96% CAGR through 2030.

- By propulsion, the internal combustion engine accounted for 75.63% of the Saudi Arabia automotive steel stamping market size in 2024, while electric vehicles are advancing at a 5.16% CAGR through 2030.

- By province, the Central Region held 39.72% share of the Saudi Arabia automotive steel stamping market size in 2024, but the Eastern Region is projected to grow at 5.54% CAGR to 2030.

Saudi Arabia Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Incentive-led Localization Under Vision 2030 | +0.8% | National (Central and East) | Long term (≥ 4 years) |

| Post-Pandemic Rebound in Passenger Cars | +0.7% | Nationwide and GCC spillover | Medium term (2-4 years) |

| Shift to Lightweight AHSS and Hot Stamping | +0.6% | Central early adoption | Medium term (2-4 years) |

| PIF-backed Lucid and Ceer Capacity Build-up | +0.5% | Central and Western hubs | Long term (≥ 4 years) |

| Industry 4.0 Smart Press Lines Adoption | +0.4% | Central leading, Eastern following | Long term (≥ 4 years) |

| Mandated Local-Content Thresholds | +0.3% | National, IKTVA-aligned suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Incentive-led localization under Vision 2030

Backed by manufacturer incentives, Vision 2030 and the National Industrial Development and Logistics Program set a target of achieving around 50% localized vehicle production by 2030. This initiative aims to boost domestic manufacturing capabilities, reduce reliance on imports, and foster economic growth within the automotive market[1] “National Industrial Strategy,”, Vision 2030,vision2030.gov.sa. Special Economic Zones deliver tax relief and simplified regulations that cut operational costs for qualifying press-shop investments. This protective framework reshapes competition by tilting procurement toward domestic stampers, though success still pivots on volume scalability and timely infrastructure roll-out.

Post-pandemic rebound in passenger car demand

Vehicle registrations rose considerably in 2024 as pent-up demand and improved financing revived the auto retail channel [2]“Apparent Steel Consumption in the Middle East 2024,” eurofer.eu. Steel consumption mirrored the trend, growing steadily after a sharp drop in 2023, which restored utilization rates at existing press lines. As consumers increasingly gravitate towards larger SUVs, the demand for additional structural reinforcements rises. These reinforcements are essential to enhance vehicle safety, durability, and performance, significantly boosting the tonnage of stamped parts used per vehicle.

Shift to lightweight AHSS and hot stamping adoption

Vehicle manufacturers are increasingly shifting to lightweight Advanced High-Strength Steel (AHSS) and adopting hot stamping techniques to enhance vehicle performance, improve fuel efficiency, and meet stringent environmental regulations. This transition aligns with the global automotive industry's focus on reducing vehicle weight while maintaining safety and durability standards.

By leveraging AHSS, automakers can achieve tensile strengths of up to 2,000 MPa while optimizing weight reduction by 20-30% [3]“AHSS Adoption in Automotive,” ssab.com. Saudi plants are utilizing thermoforming presses to effectively reduce springback and enable the production of intricate geometries, offering advantages over traditional cold lines.

PIF-backed OEM entrants

Saudi Arabia is making waves in the electric vehicle (EV) sector, underscoring its commitment to economic diversification. The Kingdom has poured substantial investments into EV production and battery supply chains. Notably, Saudi Arabia invested a significant USD 3.4 billion in Lucid Motors, enabling the production of 155,000 EVs annually. Additionally, a USD 5.6 billion agreement with Human Horizons further cements the Kingdom's strategy, drawing in global automakers and fostering a competitive manufacturing landscape.

Ceer is charting an ambitious course for the next decade. The company aims to attract over USD 150 million in foreign direct investment, with a goal of creating around 30,000 jobs, both directly and indirectly. Furthermore, Ceer targets a 45% localization rate for its product content and projects a direct contribution of USD 8 billion to Saudi Arabia’s GDP by 2034. Additionally, as long-run visibility aligns with stamping demand curves, contracts related to tooling, die-design, and material handling become pivotal. When quality benchmarks are achieved, these contracts act as catalysts for supply-chain localization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Global Steel Prices | −0.6% | Global feedstock costs (all regions) | Short term (≤ 2 years) |

| Limited Domestic OEM Volumes | −0.4% | National assembly hubs | Medium term (2-4 years) |

| Influx of Cheaper Asian Panels | −0.3% | National, the highest at Eastern Region ports | Short term (≤ 2 years) |

| Uncertain EV Tooling ROI | −0.2% | Central and Western EV-production clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile global steel prices

As global steel prices fluctuate, Saudi Arabia's automotive steel stamping market may face mounting challenges. These price swings might elevate production costs, destabilize supply chains, and shift market dynamics, potentially hindering growth during the forecast period. The volatility in steel pricing impacts manufacturers' operational efficiency and creates uncertainty in long-term planning and investment decisions. Furthermore, the unpredictable nature of steel pricing complicates operations for manufacturers, putting their competitive pricing strategies and ability to meet demand at risk. Such hurdles influence the market's direction throughout the study period.

In addition, the country's reliance on imports for some of its specialty grades heightens its vulnerability to freight disruptions and geopolitical tensions. This dependency increases the risk of supply shortages, which could further strain production timelines and market stability. While hedging contracts and quarterly price adjustments offer some relief, they fall short of fully alleviating the pressure, especially since OEMs are hesitant to pass on price changes frequently.

Limited domestic OEM volumes

Saudi Arabia targets an ambitious production goal of 500,000 electric vehicles (EVs). However, it risks falling short of this benchmark, a critical threshold for ensuring global cost competitiveness in the coming years. This constrained output forces local manufacturers to either operate below capacity or depend on simpler component imports from Asia, stunting their manufacturing growth. Such import dependence not only hampers cost efficiency but also slows establishing a strong local supply chain.

Moreover, without the development of regional export channels, this underproduction could hinder further capital-intensive growth, curtailing the nation's pursuit of economies of scale and its competitive stance in the global arena.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Blanking Underpins Volume, Embossing Scales Up

Blanking generated 38.15% of the Saudi Arabia automotive steel stamping market size in 2024 because it delivers the flat and contoured panels every vehicle architecture needs. Embossing is outpacing at 4.65% CAGR, propelled by EV battery-shield applications that command premium unit margins. Suppliers upgrade blanking lines with progressive-die sets and laser–hybrid trimming, achieving 15-20% material-yield gains. Coining protects dimensional tolerances on seat-belt anchors and roof-rail inserts, while hydroforming and roll hemming inhabit the “other technologies” bucket that now captures bespoke SUV panel geometries. These technology mixes highlight how the Saudi Arabia automotive steel stamping market evolves from volume-based blanks to value-added multi-step modules across the forecast horizon.

OEM directives for body-panel flatness and skin-quality drive continuous improvement in press-shop environmental control and tool steel metallurgy. Domestic suppliers partner with European die makers to localize tool maintenance, compressing lead times by nearly four weeks and supporting Vision 2030 employment objectives. As the digital twin model wears, predictive re-grinding schedules uplift uptime significantly, an essential KPI for the Saudi Arabia automotive steel stamping market.

By Process: Sheet Metal Forming Stays Core, Hot Stamping Ramps

Sheet metal forming retained 29.44% of the Saudi Arabia automotive steel stamping market share in 2024, owing to its installed press capacity and workforce familiarity. Yet hot stamping will post a 5.22% CAGR, reflecting AHSS content escalation in EV crash zones and B-pillars. Furnace-to-press transfer robots, integrated quench dies, and multi-zone cooling help Saudi plants target cycle times under 10 seconds, closing on European benchmarks. Investment is co-financed by the Industrial Development Fund, which covers most of the machinery costs for ventures meeting localization benchmarks.

Roll forming fulfils long-rail and rocker-panel demand in commercial vans, offering continuous cost efficiencies for extended linear parts. Metal fabrication sub-assemblies, spot welding, clinching, and adhesive bonding are spread throughout EV underbodies, providing envelope-resilient rigidity with fewer SKUs.

By Vehicle Type: Passenger Cars Dominate, Commercial Fleets Diversify

Passenger cars delivered 61.25% of Saudi Arabia automotive steel stamping market demand in 2024 and are slated for a 3.96% CAGR to 2030 on the back of favourable credit and demographic dynamics. Sedans and SUVs generate continuous panel tonnage, while premium crossover models lift per-vehicle AHSS intensity. Light commercial vehicles answer booming e-commerce logistics, stimulating demand for tailored load-floor stampings and reinforced door frames.

Heavy commercial vehicles, though numerically smaller, require thicker gauges for chassis cross-members, adding disproportionate tonnage per unit. Government megaprojects from NEOM to Qiddiya mandate bus and truck fleets that will pull specialized press work at lower but steady volumes. Suppliers streamlining die-change intervals below 20 minutes retain agility to service mixed vehicle programs without idle press downtime, a decisive capability in the Saudi Arabia automotive steel stamping market.

By Propulsion: ICE Still Rules, EV Panels Accelerate

Internal-combustion-engine (ICE) models commanded a 75.63% share in 2024, yet electric vehicles logged the fastest 5.16% CAGR as PIF funding compressed EV plant ramp-ups. Battery enclosures need multi-hit hot-stamped trays resistant to puncture and thermal runaway, diverting investments to thicker manganese-boron blanks. Gigacasting threatens certain underbody pressings, yet upper-body and safety-critical segments remain stamping strongholds through 2030.

Adaptive press tools capable of switching between HV-battery frames and ICE tunnel reinforcements future-proof capacity, ensuring utilization even if EV adoption growth plateaus temporarily.

Geography Analysis

Riyadh’s Central Region captured 39.72% of 2024 volume due to the King Salman Automotive Cluster, PIF-backed OEM headquarters, and streamlined regulatory access. Government procurement criteria, including mandatory IKTVA scoring, reward plants within a one-day trucking radius of final assembly lines. Expansion projects target twin-press halls with 1,600-t to 2,500-t capacity and cross-bar servo transfers that raise strokes per minute to 18 for outer panels. Workforce pipelines draw from automotive curricula at Princess Nourah University, closing skills gaps in die-maintenance and metrology.

Eastern Province claims the fastest 5.54% CAGR outlook by blending existing petrochemical and steel ecosystems with King Salman Energy Park (SPARK) logistics. Ready access to SABIC Hadeed slabs, Jubail-based coil processors, and Ras al-Khair port cuts transit times for imported AHSS coils. The Ministry of Investment reports that 87.2% of 2022 FDI landed in Eastern manufacturing projects, underscoring investors’ preference for mature infrastructure. Asian panel imports funnel through Dammam but also sharpen competitive pressure; local press shops respond by emphasizing short-lead custom runs and defensive sourcing partnerships with ArcelorMittal’s DRI-based low-carbon sheet offerings.

The Western Region, encompassing Makkah and Madinah, functions as an assembly and export bridge to Red Sea shipping lanes. Lucid’s coastal site links efficiently to European parts logistics, and Ceer’s supplier park in King Abdullah Economic City co-locates hot-stamping and axle machining. Northern and Southern provinces remain emergent but show potential; Qiddiya’s transport-themed entertainment complex and southern mining road networks call for commercial fleets, spurring future regional press capacity. National rail corridors will further equalize inbound coil transport costs, making distributed stamping feasible once volumes warrant.

Competitive Landscape

In Saudi Arabia's automotive steel stamping market, international giants vie for dominance against agile local players. The competition heats up, especially in EV sub-assemblies, including battery boxes, skateboard platforms, and high-ductility side-sills. Suppliers adept in 3rd-generation steel forming and mixed-material bonding command a premium, whereas commodity outer-skin blanks grapple with shrinking margins due to an influx from Asia. Meeting IKTVA thresholds has become as crucial as piece-price metrics in award decisions, compelling global entities to invest in local die workshops or miss out on lucrative high-volume bids.

Additionally, the market is witnessing a shift toward advanced manufacturing technologies, with players focusing on automation and precision engineering to enhance production efficiency and meet evolving quality standards. This trend aligns with the broader push for localization and sustainability, as companies aim to reduce dependency on imports and align with Saudi Arabia's Vision 2030 objectives.

Saudi Arabia Automotive Steel Stamping Industry Leaders

Gestamp Automoción

Magna International (Cosma)

SABIC Hadeed

ThyssenKrupp AG

ArcelorMittal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Slovenian Steel Group (SIJ) signed a €1.5 billion memorandum with WAHAJ to build electro-steel and premium hot-strip lines in Ras Al-Khair, anchoring feedstock for regional auto stampers.

- May 2024: Ceer invited contractor bids for an automotive supplier park adjacent to its King Abdullah Economic City EV plant, including hot stamping and axle facilities to secure vertically integrated metal parts.

Saudi Arabia Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Car |

| Light Commercial Vehicle |

| Heavy Commercial Vehicle |

| Internal Combustion Engine (ICE) |

| Electric Vehicle |

| Central Region (Riyadh) |

| Western Region (Makkah and Madinah) |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicle | |

| Heavy Commercial Vehicle | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric Vehicle | |

| By Province | Central Region (Riyadh) |

| Western Region (Makkah and Madinah) | |

| Eastern Region | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

How large is Saudi Arabia’s automotive steel stamping activity in 2025?

It is valued at USD 12.14 billion, with a 3.52% CAGR projected to lift it to USD 14.43 billion by 2030.

Which technology currently generates the highest revenue?

Blanking leads with 38.15% share because it produces the base panels required across nearly every vehicle platform.

What growth rate is forecast for hot stamping through 2030?

Hot stamping is set to rise at a 5.22% CAGR, driven by AHSS adoption for lighter, safer body structures.

Why is Riyadh’s Central Region critical for stampers?

The King Salman Automotive Cluster, proximity to government contracting, and PIF-backed OEM headquarters give the region 39.72% of 2024 demand.

What short-term challenges will suppliers face?

The key hurdles are volatile steel input prices that can cut margins, and cheaper Asian panel imports that pressure local pricing.

Page last updated on: