Saudi Arabia Car Rental And Leasing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

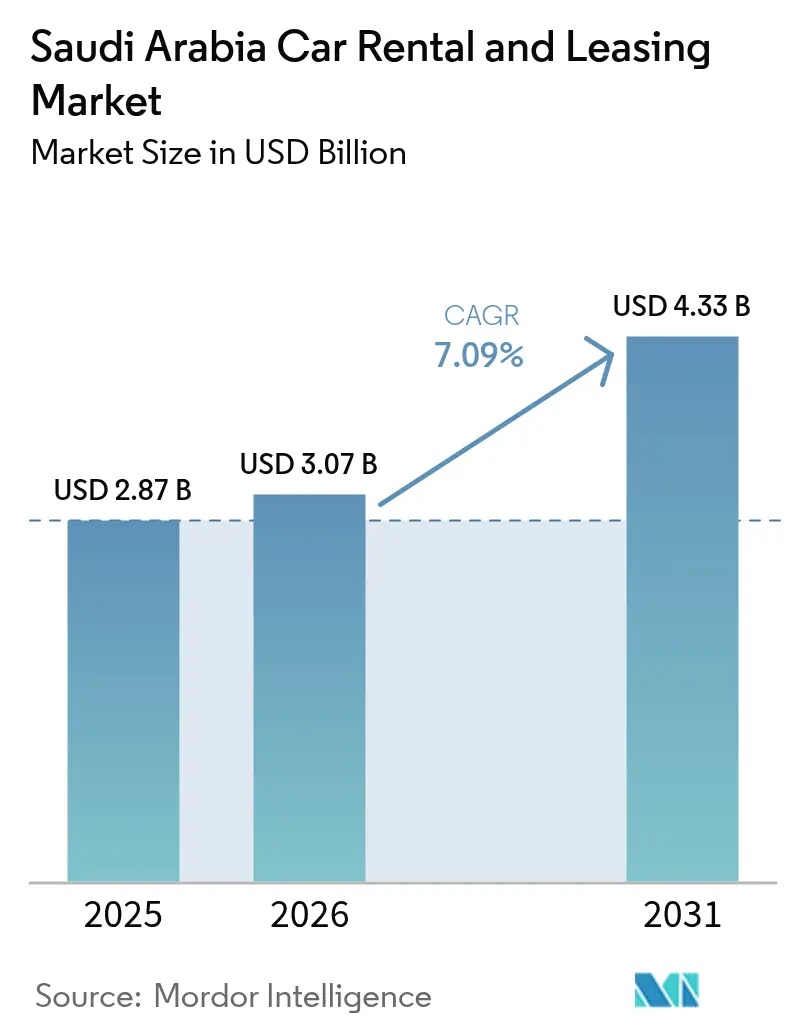

| Base Year Market Size (2025) | USD 2.87 Billion |

| Market Size (2026) | USD 3.07 Billion |

| Market Size (2031) | USD 4.33 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

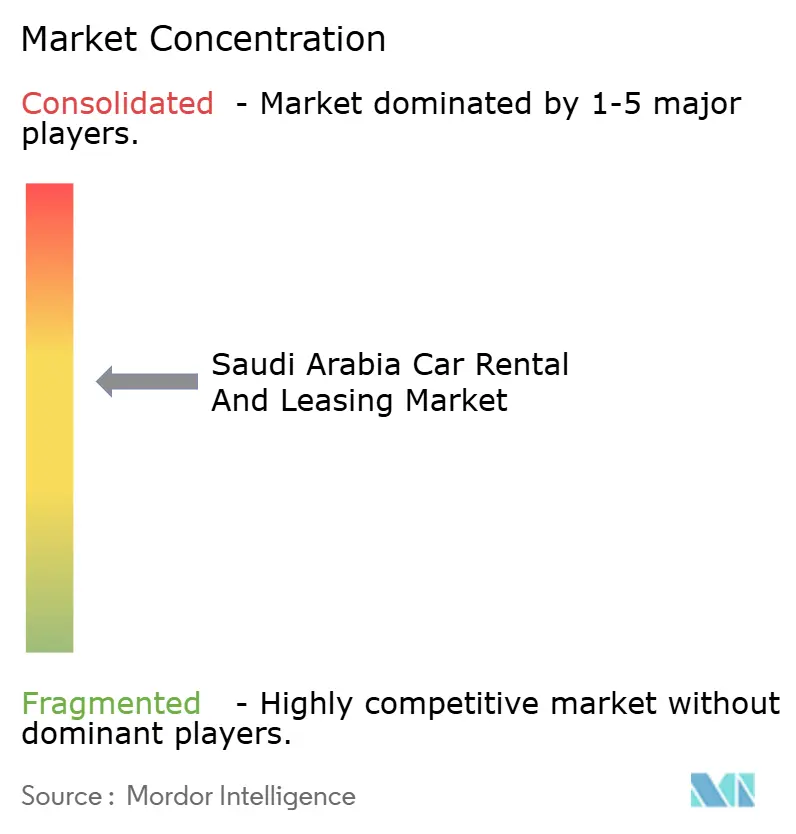

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Car Rental And Leasing Market Analysis by Mordor Intelligence

The Saudi Arabia Car Rental And Leasing Market size in 2026 is estimated at USD 3.07 billion, growing from 2025 value of USD 2.87 billion with 2031 projections showing USD 4.33 billion, growing at 7.09% CAGR over 2026-2031. Rising tourism, corporate fleet outsourcing, and Vision 2030 infrastructure commitments underpin steady demand expansion as the Kingdom transitions toward a diverse service economy. Online booking platforms, continue to streamline transactions and widen customer reach, while self-drive preferences, anchor consumer autonomy trends. Short-term rentals still lead overall volumes; however, corporate cost-optimization pushes long-term leasing to outpace the broader Saudi Arabia car rental and leasing market. Consolidation among large operators, coupled with technology-driven platforms such as SHIFT, intensifies competitive differentiation centered on digital convenience, predictive maintenance, and fleet electrification readiness.

Key Report Takeaways

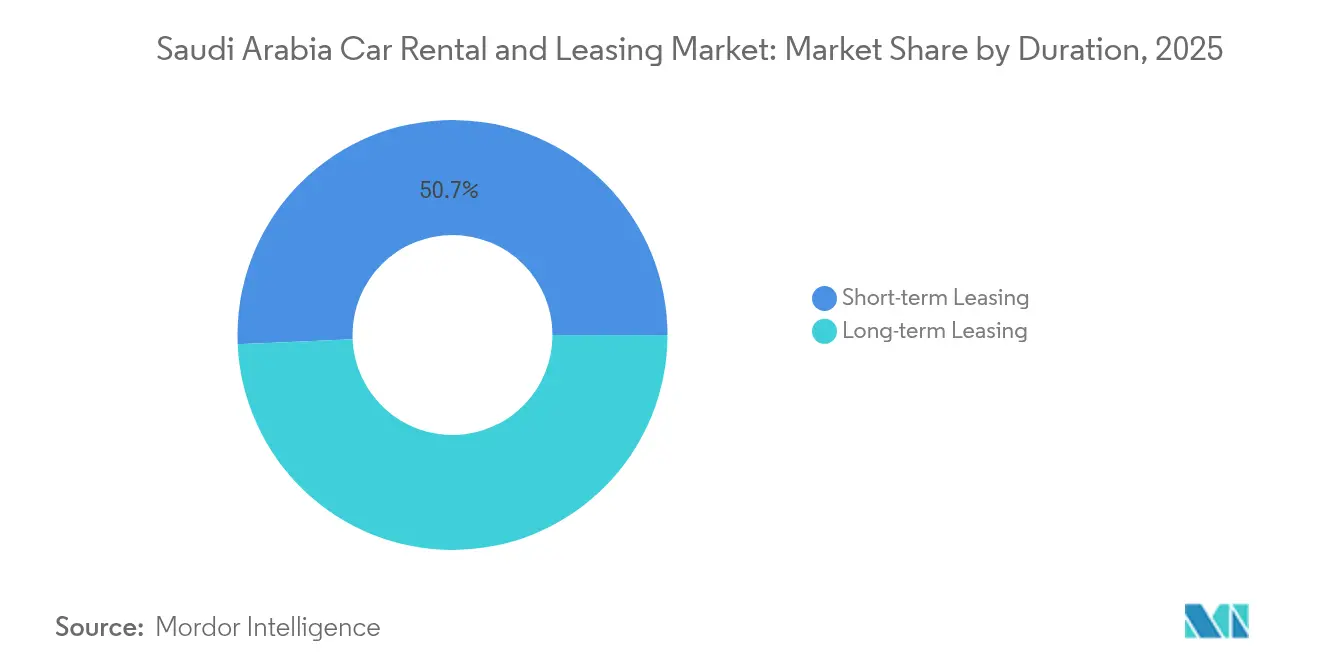

- By duration, short-term leasing held 50.68% of the Saudi Arabia car rental and leasing market share in 2025,long-term leasing is advancing at an anticipated 7.22% CAGR through 2031.

- By vehicle type, economy and budget cars commanded 62.85% share of the Saudi Arabia car rental and leasing market size in 2025, the premium and luxury segment is on track for 7.34% CAGR between 2026 and 2031.

- By body type, sedans accounted for 45.12% of the Saudi Arabia car rental and leasing market share in 2025; SUVs are projected to register a 7.36% CAGR through 2031.

- By booking type, online channels captured 71.05% of the Saudi Arabia car rental and leasing market share in 2025; online reservations are forecast to expand at 7.21% CAGR to 2031.

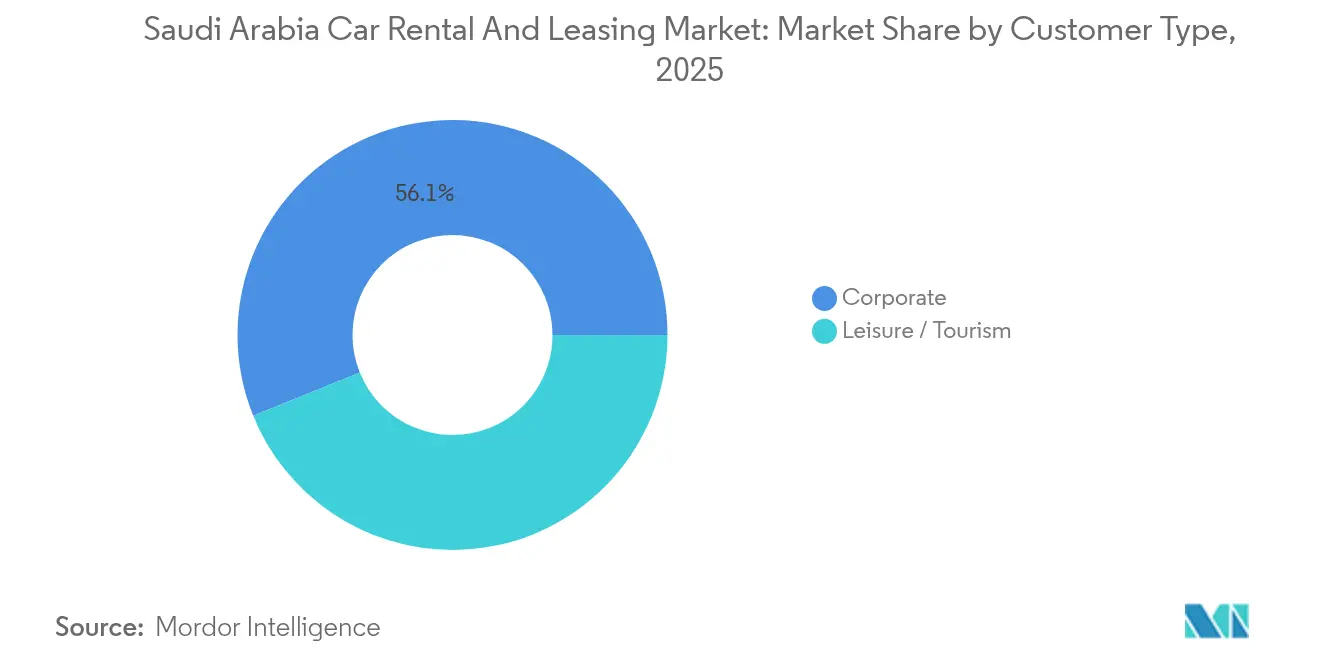

- By customer type, corporate accounts captured 56.12% revenue share of the Saudi Arabia car rental and leasing market in 2025, leisure and tourism demand is projected to expand at 7.17% CAGR to 2031.

- By rental mode, self-drive arrangements held 76.98% of the Saudi Arabia car rental and leasing market share in 2025; chauffeur-driven services are set to record the highest 7.15% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Car Rental And Leasing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Leisure & Religious Tourism | +1.8% | National, with peaks in Mecca, Medina, Riyadh | Long term (≥ 4 years) |

| Vision 2030 Entertainment Mega-Projects | +1.5% | NEOM, Qiddiya, Red Sea Project regions | Long term (≥ 4 years) |

| Surge In Logistics and E-Commerce Demand | +1.2% | National, concentrated in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Government Fleet-Outsourcing Mandates | +1.0% | National, government sector focus | Medium term (2-4 years) |

| Electrification Incentives | +0.8% | Urban centers, Riyadh priority | Long term (≥ 4 years) |

| AI-Based Predictive Maintenance Cuts TCO | +0.6% | National, technology-enabled fleets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion Of Leisure & Religious Tourism

Religious pilgrimages generate predictable but intense spikes, prompting dynamic pricing and fleet redeployment strategies around Mecca and Medina. Vision 2030 targets 30 million pilgrims yearly, boosts year-round utilization, and reduces seasonality risk[1]“Transport and Communications in Vision 2030,” Ministry of Transport, my.gov.sa. Leisure travelers pursuing desert, coastal, and heritage itineraries extend rental durations and favor premium SUVs. Simplified International Driving Permit processing expands self-drive adoption among foreign visitors. Integrated service models now package insurance, navigation, and multilingual assistance to capture tourist loyalty.

Vision 2030 Entertainment Mega-Projects

NEOM’s car-free blueprint compels operators to innovate with feeder services and mobility-as-a-service collaborations outside the core city limits[2]“NEOM, the world’s first smart city,” AtkinsRealis, atkinsrealis.com. Once attractions launch, Qiddiya and the Red Sea Project fuel demand for commercial vehicles during construction and upscale rentals. Incoming expatriate workforces rely on long-term leasing for reliable personal transportation under flexible contracts. Proximity-based service hubs reduce response times and enable premium vehicle availability for high-income tourists. Aggregated project zones offer predictable returns that justify fleet expansions and specialized vehicle acquisitions.

Surge In Logistics & E-Commerce Demand

Commercial vehicle leasing accelerates as e-commerce turnovers climb and delivery surges reach three-fifths during Hajj and Ramadan peaks. Logistics firms prefer long-term contracts that avoid capital outlays, facilitate quick fleet scaling, and ensure compliance with emission rules. Seasonal volatility pushes operators toward flexible rental terms that balance utilization with cost control. Government support for digital commerce and last-mile infrastructure widens the customer base for refrigerated vans and parcel trucks. Fleet managers leverage telematics to optimize routing, minimize idle time, and enhance vehicle turnaround efficiency.

Government Fleet-Outsourcing Mandates

State agencies increasingly replace owned vehicles with service contracts that guarantee uptime, standardized maintenance, and transparent costs. Standardized leasing templates expedite procurement while enforcing fuel-efficiency and safety benchmarks. Performance-linked contracts favor providers with digital fleet management and predictive maintenance capability. Long tenures and fixed monthly payments stabilize cash flows, enabling operators to invest in telematics. EV pilots, Public sector outsourcing has bolstered Budget Saudi’s long-term revenue visibility following its AutoWorld acquisition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-Driven Cost Escalation | -1.3% | National, affecting operational costs | Short term (≤ 2 years) |

| High Fleet-Financing Interest Rates | -0.9% | National, capital-intensive operators | Medium term (2-4 years) |

| Lagging EV-Charging Infrastructure | -0.6% | Urban centers, highway corridors | Medium term (2-4 years) |

| Strict Traffic-Violation Penalties | -0.4% | National, enforcement concentration in cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Inflation-Driven Cost Escalation

Fuel, parts, and insurance premiums climb faster than headline inflation and compress margins Unpredictable fuel pricing complicates multi-year contract negotiations, prompting hedging or surcharges Global semiconductor shortages extend vehicle delivery lead times and elevate acquisition costs, delaying fleet refresh cycles Higher accident rates lift insurance premiums, particularly for luxury and commercial vans Operators respond with bulk procurement, preventive maintenance, and telematics-guided driving behavior analytics to mitigate expenses.

Lagging EV-Charging Infrastructure

The planned deployment of thousands of chargers covers urban cores yet underserved intercity corridors. Range anxiety restricts tourism and business uptake of electric rentals despite incentives. Slow rollout of fast-charging technology prolongs vehicle turnaround times, reducing fleet utilization. Operators weigh early adoption advantages against residual value uncertainty and infrastructure delays. Until highway coverage improves, large-scale electrification of rental fleets remains constrained, postponing total cost-of-ownership benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Duration: Long-Term Gains Momentum

Short-term arrangements retained 50.68% of the Saudi Arabia car rental and leasing market share in 2025 by catering to tourism surges and business travel recovery. The Saudi Arabia car rental and leasing market size attributable to long-term contracts is forecast to double between 2023 and 2025 under Budget Saudi’s expansion roadmap. Integrated digital portals allow clients to pivot between daily and multi-year plans without administrative friction. Long-term contracts contributed 7.22% CAGR, nearly matching overall Saudi Arabia car rental and leasing market growth, as corporations and government agencies prioritize predictable monthly expenses over outright purchases.

Shift in payment preferences shapes asset-light supply chains, permitting rapid fleet rightsizing during demand volatility Corporate sustainability aims also push for low-emission vehicles, which are easier to pilot under long-term leases than outright purchases The Saudi Arabia car rental and leasing market benefits from tax deductions tied to service contracts, encouraging businesses to extend contract tenures Tourism-led short-term volumes still contribute cash-flow peaks, especially during Hajj and entertainment events.

By Vehicle Type: Premium Segment Accelerates

Thanks to competitive pricing, economy vehicles captured 62.85% of the Saudi Arabia car rental and leasing market share in 2025. Yet the premium category, growing at 7.34% CAGR, records above-average revenue per day as customers pursue elevated travel experiences. Corporate executives and high-end tourists gravitate toward technology-rich sedans and SUVs furnished with connectivity features.

Digital booking engines showcase premium inventory with transparent upgrade pricing, nudging customers toward higher categories Rising disposable incomes, coupled with luxury hospitality growth along the Red Sea coast, reinforce demand for prestige marques The Saudi Arabia car rental and leasing market size for premium vehicles is projected to grow exponentially by 2031 as operators expand brand-specific fleets Loyalty programs and chauffeur add-ons lock in repeat clientele and lift utilization ratios.

By Body Type: SUV Demand Surges

By body type, sedans accounted for 45.12% of the Saudi Arabia car rental and leasing market share in 2025. SUVs are clocking the fastest 7.36% CAGR, propelled by family travel, desert tourism, and perceived safety advantages. Sedans still hold more than two-fifths of volume share due to cost efficiency for corporate mobility. Enhanced road infrastructure encourages off-city adventures, boosting SUV rentals.

Telematics analytics reveal higher retention among SUV renters, prompting operators to adjust procurement toward crossover and midsize SUV categories. The Saudi Arabia car rental and leasing market size attached to SUVs is predicted to grow exponentially by 2031 under sustained tourism traffic. Seasonal package promotions bundle GPS, camping gear, and extra insurance for off-road journeys, increasing ancillary revenue.

By Booking Type: Digital Dominance Continues

Online reservations constitute 71.05% of the Saudi Arabia car rental and leasing market share in 2025, and expand at 7.21% CAGR as consumers seek frictionless comparison and instant confirmations. Algorithms refine dynamic pricing to maximize occupancy and revenue per vehicle.

Legacy walk-in channels persist for institutional contracts where personalized negotiation remains integral The Saudi Arabia car rental and leasing market gains operational savings from paperless processes, including e-payments and mobile key handoffs. Bilingual chatbots and AI-powered support accelerate resolution times, raising net promoter scores among domestic and foreign clients.

By Customer Type: Leisure Tourism Momentum

Corporate users provided 56.12% of the Saudi Arabia car rental and leasing market share in 2025, yet leisure demand, expanding at 7.17% CAGR, is closing the gap under Vision 2030 tourist inflows. Packages catered to pilgrims combine extended mileage, inclusive insurance, and flexible drop-off points across Mecca and Medina.

Season-pass bundles encourage repeat leisure rentals among domestic travelers frequenting coastal resorts. If visitation targets hold, the Saudi Arabia car rental and leasing market size drawn from leisure customers could top by 2031. Cross-selling of Wi-Fi hotspots and child-safety seats raises ancillary revenue margins.

By Rental Mode: Self-Drive Preferences Persist

Self-drive options control 76.98% of the Saudi Arabia car rental and leasing market share in 2025, mirroring cultural preference for privacy and autonomy. Chauffeur services, growing at a 7.15% CAGR, gain traction with luxury tourists, senior citizens, and female travelers seeking convenience and safety assurances.

Post-2018 female licensing reforms unlocked a new self-drive demographic, elevating weekday utilization rates. Autonomous-vehicle pilots slated for 2025-2026 may spawn hybrid models, combining self-drive flexibility with AI-supervised safety features. The Saudi Arabia car rental and leasing market positions driver training and background checks as service differentiators for chauffeur segments.

Geography Analysis

Riyadh, Jeddah, and Dammam collectively generate roughly three-fifth of nationwide rentals, anchored by governmental, commercial, and industrial activities that demand predictable mobility solutions Riyadh, the administrative and financial nucleus, leads absolute volume, supported by a dense network of business travelers and expatriate residents Jeddah merges commercial logistics with a gateway role for religious tourism, driving dual-purpose vehicle demand that blends corporate reliability with extended pilgrim itineraries.

The Northern region contributes more than half of Lumi Rental’s revenue, highlighting efficiency gains from hub-and-spoke deployments concentrated near mega-project sites. Dammam capitalizes on cross-border energy trade, maintaining steady corporate leasing and specialized documentation services for GCC travel. The Saudi Arabia car rental and leasing market sees average daily rental durations stretch in the Eastern Province due to project-based expatriate assignments.

Emerging destinations like NEOM, Qiddiya, and Amaala shift future demand poles as construction peaks and operational phases commence. Operators prepare satellite depots and flexible fleets to serve car-free urban cores and resort logistics perimeters The Saudi Arabia car rental and leasing market size attributable to these growth corridors is set to rise notably post-2026, diversifying geographic revenue distribution beyond the traditional three-city axis.

Competitive Landscape

More than 600 licensed firms compete, yet consolidation is accelerating. Budget Saudi’s acquisition of AutoWorld elevated its share significantly and unlocked millions in annual synergies. Lumi, Theeb, and Yelo invest in telematics and branch networks to dispute market leadership, while international brands such as Hertz and Avis sustain premium niches via global loyalty integration.

Technology shapes differentiation: SHIFT’s mobile-only interface and automated pick-up kiosks yield higher customer satisfaction and lower labor overhead. AI-enabled predictive maintenance cuts fleet downtime and supports government procurement standards on uptime ratios. The Saudi Arabia car rental and leasing market rewards data-rich platforms that forecast demand, optimize pricing, and steer fleet mix decisions.

Capital allocation focuses on electrification pilots and SUV procurement to align with user preference data. Operators pursue strategic partnerships with EV-charging suppliers to secure infrastructure near high-traffic branches. Franchise agreements and co-branding with hospitality chains embed rental desks at hotels and airports, extending distribution reach and capturing impulse bookings.

Saudi Arabia Car Rental And Leasing Industry Leaders

Hertz Corporation

Hanco Automotive

Budget Rent a Car

Theeb Rent A Car

Lumi Car Rentals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Merak Capital invested SAR 310.8 million in SHIFT to scale a 12,000-vehicle fleet across 57 cities with fully digital rental journeys.

- June 2024: United International Transportation Co. (Budget Saudi) finalized the AutoWorld acquisition, targeting a fleet expansion to surpass 65,000 units by 2028 while capturing SAR 30–50 million in cost synergies

Saudi Arabia Car Rental And Leasing Market Report Scope

Car leasing is the process by which a person uses a vehicle for a set period of time in exchange for timely rental payments.

The Saudi Arabian car leasing market is segmented by duration, vehicle type, body type, and booking type. By duration, the market is segmented into short-term leasing and long-term leasing. By vehicle type, the market is segmented into economy/budget and premium/luxury. By body type, the market is segmented into hatchback, sedan, and multi utility vehicle and sports utility vehicle. By booking type, the market is segmented into online and offline. The report offers market size and forecasts for all the abovementioned segments in value terms (USD).

| Short-term Leasing |

| Long-term Leasing |

| Economy / Budget |

| Premium / Luxury |

| Hatchback |

| Sedan |

| Multi-Utility Vehicle |

| Sports Utility Vehicle |

| Online |

| Offline |

| Corporate |

| Leisure / Tourism |

| Self-drive |

| Chauffeur-driven |

| By Duration | Short-term Leasing |

| Long-term Leasing | |

| By Vehicle Type | Economy / Budget |

| Premium / Luxury | |

| By Body Type | Hatchback |

| Sedan | |

| Multi-Utility Vehicle | |

| Sports Utility Vehicle | |

| By Booking Type | Online |

| Offline | |

| By Customer Type | Corporate |

| Leisure / Tourism | |

| By Rental Mode | Self-drive |

| Chauffeur-driven |

Key Questions Answered in the Report

How large is the Saudi Arabia car rental and leasing market in 2026?

It stands at USD 3.07 billion, expanding toward USD 4.33 billion by 2031.

Which rental duration category is growing fastest?

Long-term leasing, advancing at 7.22% CAGR on the back of corporate and government outsourcing.

What portion of bookings take place online?

Digital platforms account for 71.05% of all reservations, a share that is still climbing.

Which vehicle body type is seeing the strongest demand lift?

SUVs, growing at 7.36% CAGR due to tourism and family travel preferences.

How intense is competition among leading rental companies?

The top five firms control significant revenue, signaling moderate consolidation with active M&A and digital differentiation.

Page last updated on: