Saudi Arabia Heavy Duty Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

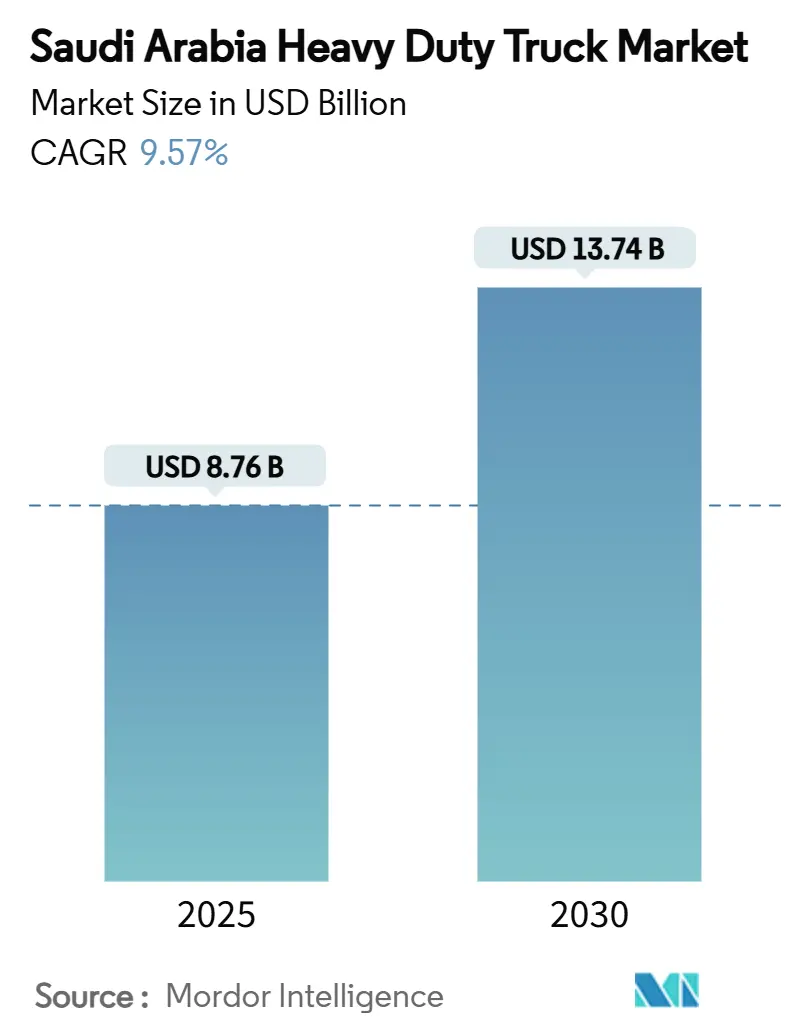

| Market Size (2025) | USD 8.76 Billion |

| Market Size (2030) | USD 13.74 Billion |

| Growth Rate (2025 - 2030) | 9.57% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Heavy Duty Truck Market Analysis by Mordor Intelligence

Saudi Arabia heavy duty truck market size stands at USD 8.76 billion in 2025 and is forecast to reach USD 13.74 billion by 2030, registering a 9.57% CAGR over the period. Robust public spending on roads, ports, and giga-projects under Vision 2030 anchors demand as construction, mining, and long-haul logistics expand. Specialized trucks above 40 t GVW post the fastest growth because NEOM, Qiddiya, and Arabian Shield mines require high-capacity haulage. An import age cap of five years accelerates fleet renewal, pushing operators toward newer, fuel-efficient models. Meanwhile, electric and hydrogen pilots introduce low-emission alternatives in a market still dominated by diesel. Persistent diesel price volatility and driver shortages temper margins, but generous manufacturing incentives broaden the local assembly base, lowering lead times and reinforcing after-sales support.

Key Report Takeaways

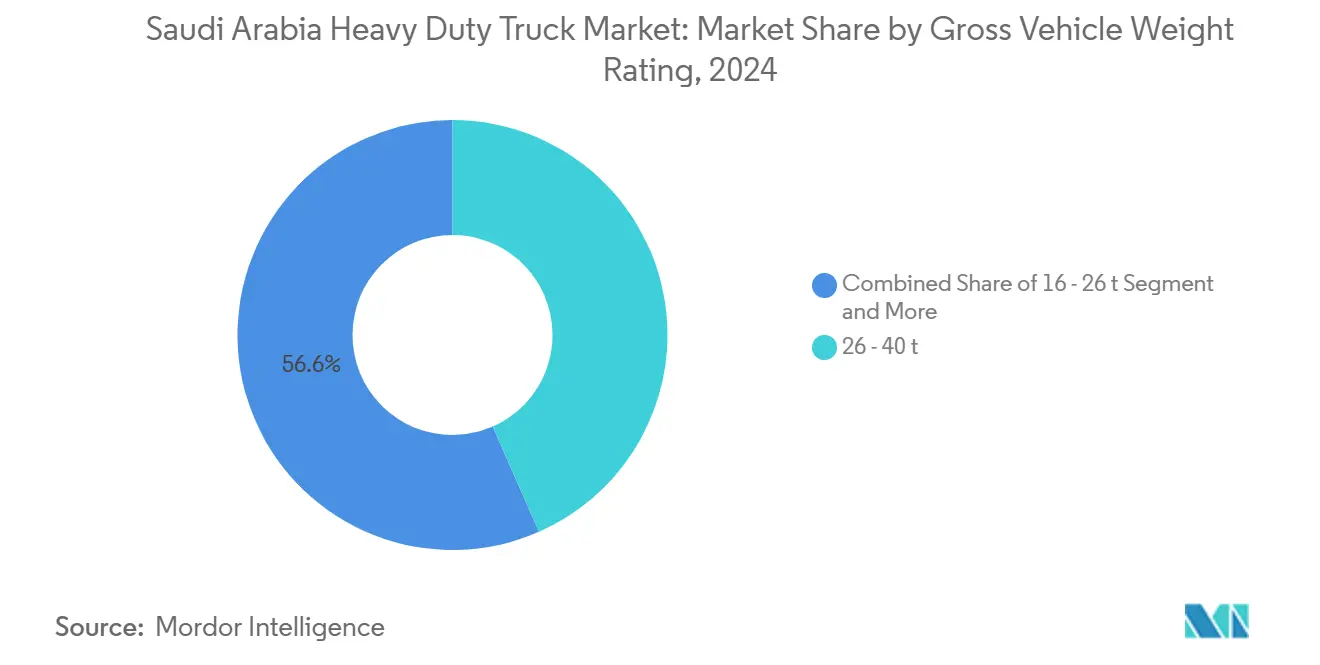

- By gross vehicle weight, the 26–40 t class led the Saudi Arabia heavy-duty truck market with 43.41% of the share in 2024, while the above-40 t segment is projected to record the fastest 10.29% CAGR through 2030.

- By propulsion, internal combustion engines retained 91.87% share of the Saudi Arabian heavy-duty truck market size in 2024; the electric segment is forecast to expand at a 13.26% CAGR between 2025 and 2030.

- By axle type, 6×4 configurations commanded 46.54% share of the Saudi Arabia heavy-duty truck market size in 2024, whereas 6×2 models are expected to rise at an 8.82% CAGR to 2030.

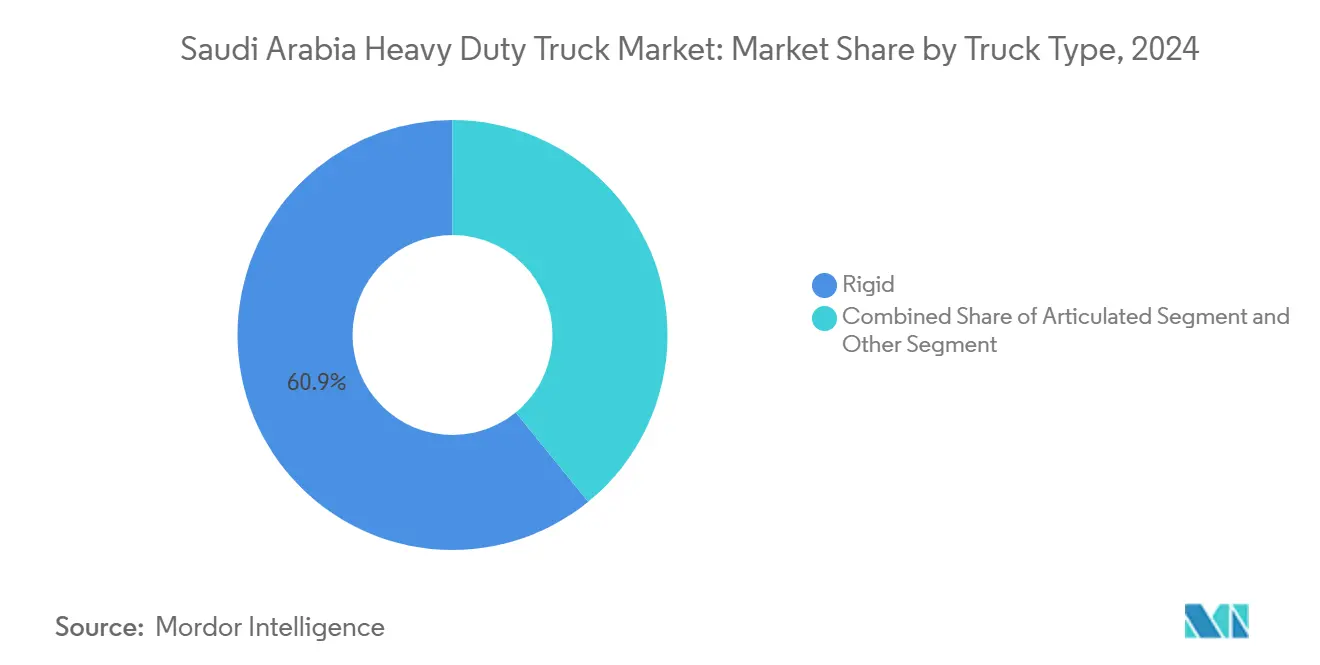

- By truck type, rigid bodies accounted for 60.88% of Saudi Arabia's heavy-duty truck market share in 2024, and articulated tractors are advancing at a 9.78% CAGR through 2030.

- By application, construction and mining captured 43.28% of Saudi Arabia's heavy-duty truck market size in 2024; freight and logistics represent the fastest-growing use case with a 9.28% CAGR to 2030.

- By geography, the Eastern Province held 31.25% of Saudi Arabia heavy duty truck market share in 2024 and is projected to grow at a 7.68% CAGR through 2030.

Competitive positioning in Saudi arabia includes both locally based firms and those operating across multiple regions. The market landscape in the global heavy duty trucks industry research shows how these players are arranged internationally.

Saudi Arabia Heavy Duty Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Builds | +2.1% | National; NEOM, Riyadh, Eastern Province | Long term (≥ 4 years) |

| E-com Freight and Ports | +1.8% | Eastern Province ports; Riyadh hubs | Medium term (2–4 years) |

| Age-cap Renewal Rule | +1.5% | Nationwide | Short term (≤ 2 years) |

| Assembly Incentives | +1.2% | KAEC; industrial zones | Medium term (2–4 years) |

| Hydrogen Corridors | +0.9% | NEOM route; major highways | Long term (≥ 4 years) |

| Mining Boom Above 40 t | +0.7% | Northern and central mining regions | Medium term (2–4 years |

| Source: Mordor Intelligence | |||

Vision 2030 Infrastructure Mega-Projects Pipeline

NEOM’s USD 500 billion smart city covers 26,500 km² and requires 40 t-plus dumpers, low-bed trailers, and articulated haulers to shuttle steel, precast concrete, and turbines. Parallel tourism hubs like the Red Sea Project and Qiddiya spark demand corridors from port gateways to desert sites. Fifty-nine logistics centers, twenty-one already under build-out, add construction phases that peak between 2026 and 2028[1]“Saudi Arabia – Transportation Infrastructure,”, International Trade Administration, trade.gov. This staggered timeline keeps procurement steady through 2030, with a visible spike ahead of the 2034 FIFA World Cup preparations.

E-Commerce-Led Freight & Port-Expansion Demand

Warehouses need high-capacity shuttles to ferry pallets between fulfillment centers and last-mile depots; each new 10,000 m² shed typically contracts two to three 26–40 t units for intracity moves. King Abdulaziz and Jeddah ports are dredging deeper channels and installing new ship-to-shore cranes. The 950 km Landbridge rail line links these ports, but rather than cannibalizing road freight, it multiplies short-haul truck moves at intermodal yards as containers switch from rail to road.

Mandatory Truck-Age Cap & Fleet Renewal Rules

Enforced in early 2024, the five-year age ceiling on imported trucks over 3.5 t forced thousands of Euro 3 and Euro 4 units off Saudi roads[2]“Regulations on Heavy Truck Imports,”, Saudi Standards, Metrology and Quality Organization, saso.gov.sa. Operators face a binary decision: scrap or upgrade. Scrappage drives a sharp, front-loaded buying cycle that favors brands with ready inventory and financing. The rule dovetails with energy-efficiency standards that penalize fuel-hungry engines, pushing fleets toward Euro 6 or equivalent models that cut diesel consumption. Because imported used vehicles accounted for nearly one-third of the historical supply, the policy shifts demand firmly to new-build units, compressing the standard seven-year replacement window into three to four years.

Arabian Shield Mining Boom (Above 40 t Tipper Demand)

Ma’aden’s phosphate, gold, and copper expansions across northern zones require continuous haulage of overburden and ore. Single pit operations deploy up to 200 super-heavy tippers each, driving the above-40 t segment’s 10.29% CAGR. Rough terrain demands double-frame chassis, reinforced suspension, and torque-rich powertrains, pushing average selling prices well above standard on-road units. Mine-to-port chains stretch 400 km on average, often on private haul roads, producing high annual kilometer accrual that compels quicker replacement.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel-Price Volatility | −1.4% | National | Short term (≤ 2 years) |

| Imported Chassis Supply-chain Bottlenecks | −0.8% | Major ports; assembly zones | Medium term (2–4 years) |

| Saudization Driver Shortage | −0.6% | National; acute in Eastern Province | Medium term (2–4 years) |

| Rail Freight Weight Limits | −0.4% | Landbridge corridor; connecting highways | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Diesel-Price Volatility After Subsidy Reforms

Aramco raised the pump price to SAR 1.66 per liter (USD 0.44) in January 2025, an increase of 44% year on year[3]“Saudi Diesel Price Reforms,”, Middle East Economic Survey, mees.com. Fleets operating older Euro 3 engines consume 8–10 % more fuel than Euro 6 models, turning price hikes into a competitive wedge. Smaller owner-operators running three to five trucks struggle to secure hedging, forcing higher freight rates or route rationalization. Margin compression spurs interest in LNG and hybrid units, yet infrastructure for those fuels remains thin outside urban hubs.

Imported Chassis Supply-Chain Bottlenecks

Semiconductor shortages have eased, but forged axle housings and aluminum wheels remain sporadically scarce due to European energy costs and Asian shipping delays. Lead times for specific 6×4 configurations stretched to nine months in 2024, slowing deliveries as the age-cap rule spurred demand. CKD assembly should offset risk, yet ramp-up to 50,000 units per year at the first Hyundai-PIF plant will not occur until late 2026, leaving a temporary capacity gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gross Vehicle Weight Rating: Mining Drives Super-Heavy Demand

Saudi Arabia's heavy-duty truck market size for the 26–40 t class stood at USD 3.81 billion in 2024, accounting for 43.41% of deliveries. The above-40 t group, while smaller, is forecast to post a 10.29% CAGR through 2030, fueled by NEOM bulk earthworks and Arabian Shield pit expansions. Vision 2030’s portfolio ensures a continuous pipeline of concrete, steel, and aggregate shipments, positioning super-heavy tippers and low-bed trailers as the fastest-moving inventory. Operators value the higher payloads and reduced cycle counts, which lower per-ton haul costs even after factoring in higher unit prices.

The 16–26 t band remains the backbone for regional distribution and municipal projects, benefitting from road-freight growth tied to e-commerce fulfilment. Its steady 6–7% CAGR reflects balanced demand across construction, retail, and light industrial sectors. OEMs targeting fleet conversions in this range emphasize driver comfort and telematics to reduce downtime and extend service intervals.

By Propulsion: Electric Transition Accelerates Despite ICE Dominance

Internal combustion engines represented 91.87% of Saudi Arabia's heavy-duty truck market share in 2024, but electrified alternatives are gaining traction as capital projects specify lower-emission fleets. The government’s target of 5,000 fast chargers by 2030 underpins confidence in battery-electric adoption for city and regional duty cycles. PepsiCo’s 4 t Quantron pilot in Riyadh demonstrated 200 km daily coverage with overnight depot charging, proving viability for short-haul beverage delivery.

Natural-gas engines ride on abundant domestic reserves, offering 15–20% fuel cost savings versus diesel. Hybrid and plug-in hybrid variants bridge the range gap until public fast-charging becomes ubiquitous. Fuel-cell electric trucks, though nascent, benefit from NEOM hydrogen output and Aramco’s station roll-out along the Dhahran–Tabuk corridor, positioning them for heavy long-haul once cost parity improves.

By Axle Type: Multi-Axle Configurations Gain Traction

Six-by-four models held 46.54% of shipments in 2024, balancing traction with cost for mixed on- and off-road work. Construction fleets standardize on this layout to negotiate sand, gravel, and unfinished roads. The 6×2 configuration’s 8.82% CAGR reflects highway haulers chasing lower rolling resistance and tire wear. Operators moving containers or fuel tankers between ports and inland depots favor 6×2 tractors paired with tri-axle trailers to optimize payload under national weight limits.

Specialist 8×8 chassis serve military, oil-field, and extreme mining roles. Although volumes are modest, elevated unit values make them a profitable niche for OEMs equipped with heavy-duty driveline technology. Demand clusters around NEOM’s mountainous sections and remote gold mines where conventional road access is limited.

By Truck Type: Articulated Growth Reflects Long-Haul Expansion

Rigid trucks commanded 60.88% of units in 2024, covering construction dumpers, concrete mixers, refuse collectors, and municipal tankers. Their ubiquity in city streets and project sites ensures a stable baseline demand. Articulated tractors, however, are forecast to grow at a 9.78% CAGR as Saudi Arabia integrates into global trade lanes. The Landbridge rail link and 21 new logistics centers feed containerized traffic that favors tractor-trailer combinations for rapid swap-out at yards.

Special bodies in the “Others” segment, such as truck-mounted cranes, see their order books tied directly to mega-project phases. While volumes do not surge like tractor sales, specialized bodies command higher margins, attracting domestic builders that can localize superstructure fabrication

By Application: Construction Leads, Logistics Accelerates

Construction and mining absorbed 43.28% of Saudi Arabia's heavy-duty truck market size in 2024, with spending anchored by a USD 70.33 billion sector outlay. Massive cement, aggregate, and pre-cast flows translate into continuous tipper and mixer rotations. Though smaller today, freight and logistics are projected to grow at a 9.28% CAGR as container throughput and e-commerce volumes rise. Warehouse-to-hub shuttles and intercity parcel linehaul demand medium-haul tractors that cycle up to 250,000 km annually.

Municipal services, oil-field support, and utilities form a stable third leg. These buyers prioritize reliability over cutting-edge tech, extending equipment life with rigorous maintenance, yet they gradually shift toward cleaner powertrains as corporate sustainability mandates tighten.

Geography Analysis

Eastern Province led with 31.25% of deliveries in 2024 because petrochemical hubs at Jubail and Ras Al-Khair generate constant inbound raw-material and outbound product flows. King Abdulaziz Port handles the highest container volume nationwide, spawning dense drayage corridors that soak up new 6×4 tractors. With a 7.68% CAGR to 2030, the region continues to anchor growth through refinery upgrades and the rollout of alternative-fuel corridors serving hydrogen and LNG trucks.

Riyadh Province thrives as the political and commercial heartland. Its inland dry port and the convergence of north-south and east-west highways funnel goods to a population of more than 8 million. Here, 26–40 t distribution trucks dominate, moving retail and FMCG loads from suburban fulfillment centers to urban stores. Logistics players leverage Riyadh’s geographic midpoint to backhaul containers arriving from both Gulf and Red Sea gateways.

Makkah Province stands third, propelled by religious tourism and Jeddah Islamic Port’s box traffic. Seasonal peaks during Hajj lift spot truck rates, compelling operators to maintain flexible capacity. The remaining provinces grow off lower bases but benefit from decentralization policies and infrastructure upgrades, especially the northwestern Tabuk region as NEOM scales. Improved road links and industrial clustering redistribute future fleet deployments beyond the traditional east–west axis.

Mordor Intelligence tracks the heavy duty trucks market across other major regions such as Europe and Africa, with additional country-level coverage spanning United States and Mexico, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

European and Japanese manufacturers retain entrenched share through long-standing dealerships, yet Chinese entrants and local joint ventures intensify rivalry. Mercedes-Benz surpassed 44,000 cumulative Actros deliveries by 2024, leveraging keyed-in service networks. Volvo and Scania follow with strong mining and oil-field portfolios. Hyundai’s 70:30 venture with the Public Investment Fund will assemble 50,000 vehicles annually, granting cost and lead-time advantages once production begins in 2026.

Chinese maker FAW eyes 10,000 annual sales region-wide, using aggressive pricing and lighter cab-over designs to entice smaller fleets. Tata Daewoo’s planned plant positions Indian engineering against incumbent European brands, targeting government tender preferences for locally built units. UD Trucks’ switch to Zahid Tractor boosts after-sales reach, a critical differentiator in desert operating conditions where downtime translates directly into lost site hours.

Electrification strategy forms the newest battleground. Daimler Truck’s battery-electric eActros line headlines regional demos, while Volvo taps pilot hydrogen routes. Companies with ready zero-emission line-ups gain an edge in mega-projects that stipulate carbon budgets. Simultaneously, parts localization under iktva guidelines determines bid success for oil-and-gas haulage contracts, nudging foreign OEMs to deepen Saudi content.

Saudi Arabia Heavy Duty Truck Industry Leaders

Daimler Truck

Volvo Trucks

MAN Truck & Bus

Isuzu Motors

Hino Motors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hyundai Motor Manufacturing Middle East broke ground on a USD 500 million plant in King Abdullah Economic City to build 50,000 vehicles annually from Q4 2026.

- May 2025: FAW Trucks announced a target of 10,000 annual Middle East sales, spotlighting Saudi Arabia as a primary growth market.

- March 2025: PIF and Hyundai Motor Company signed a joint venture to manufacture internal-combustion and electric vehicles domestically.

Saudi Arabia Heavy Duty Truck Market Report Scope

| 16 - 26 t |

| 26 - 40 t |

| Above 40 t |

| Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG / LNG) | |

| Electrified | Battery-Electric (BEV) |

| Hybrid & Plug-in Hybrid (HEV & PHEV) | |

| Fuel-Cell Electric (FCEV) |

| 4x2 |

| 6x4 |

| 6x2 |

| 6x6 |

| 8x6 |

| 8x8 |

| Others |

| Rigid |

| Articulated |

| Others |

| Construction & Mining |

| Freight & Logistics |

| Long-Haul |

| Other Applications |

| Riyadh Province |

| Makkah Province |

| Eastern Province |

| Asir Province |

| Medina Province |

| Rest of Saudi Arabia |

| By Gross Vehicle Weight Rating | 16 - 26 t | |

| 26 - 40 t | ||

| Above 40 t | ||

| By Propulsion | Internal-Combustion (ICE) | Diesel |

| Natural Gas (CNG / LNG) | ||

| Electrified | Battery-Electric (BEV) | |

| Hybrid & Plug-in Hybrid (HEV & PHEV) | ||

| Fuel-Cell Electric (FCEV) | ||

| By Axle Type | 4x2 | |

| 6x4 | ||

| 6x2 | ||

| 6x6 | ||

| 8x6 | ||

| 8x8 | ||

| Others | ||

| By Truck Type | Rigid | |

| Articulated | ||

| Others | ||

| By Application | Construction & Mining | |

| Freight & Logistics | ||

| Long-Haul | ||

| Other Applications | ||

| By Geography | Riyadh Province | |

| Makkah Province | ||

| Eastern Province | ||

| Asir Province | ||

| Medina Province | ||

| Rest of Saudi Arabia | ||

Key Questions Answered in the Report

What is the current value of the Saudi Arabia heavy duty truck market?

Saudi Arabia heavy duty truck market size is USD 8.76 billion in 2025 with a projected rise to USD 13.74 billion by 2030.

Which segment is growing fastest by gross vehicle weight?

Trucks above 40 t GVW are growing quickest at a 10.29% CAGR due to mining and giga-project demand.

How dominant are diesel engines today?

Internal combustion models hold 91.87% of 2024 deliveries, though electric variants are advancing at 13.26% CAGR.

Why is the Eastern Province the largest regional market?

It hosts major petrochemical complexes and port infrastructure, giving it 31.25% share of national heavy truck demand in 2024.

When will local truck manufacturing start?

Hyundai and PIF plan to roll out the first locally built units in late 2026, with capacity scaling to 50,000 vehicles annually.

Page last updated on: