Saudi Arabia Forklift Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

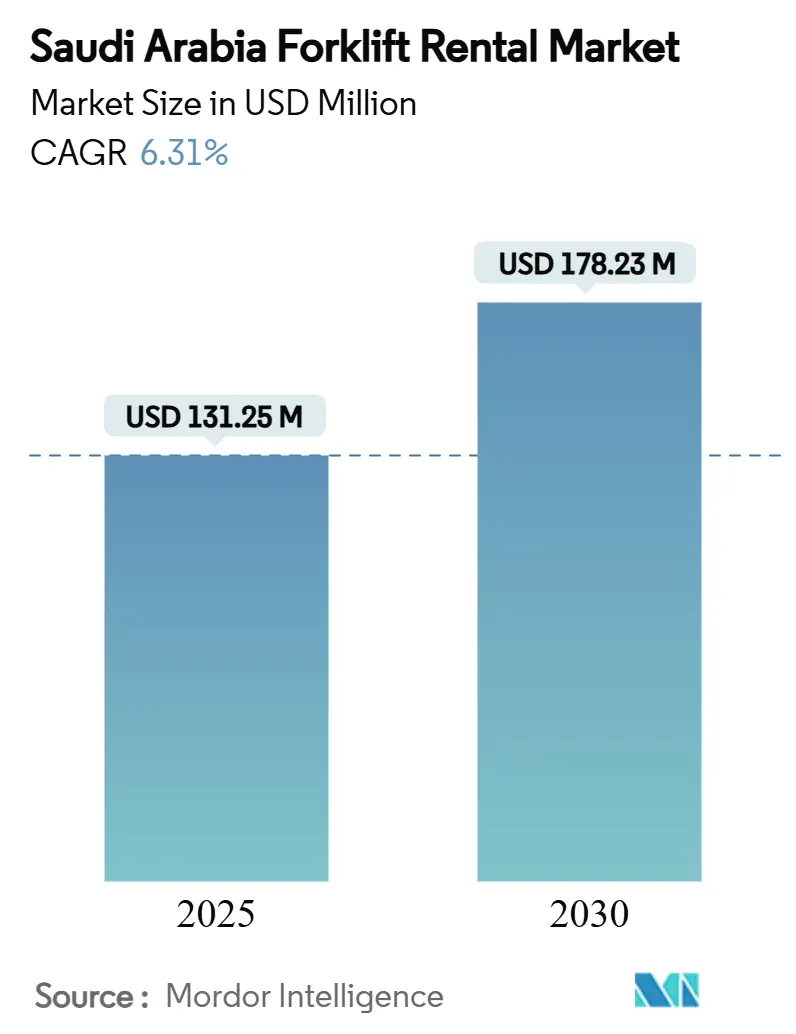

| Market Size (2025) | USD 131.25 Million |

| Market Size (2030) | USD 178.23 Million |

| Growth Rate (2025 - 2030) | 6.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Forklift Rental Market Analysis by Mordor Intelligence

The Saudi Arabia forklift rental market size is poised to reach USD 131.25 million in 2025 and is forecast to climb to USD 178.23 million by 2030, advancing at a 6.31% CAGR over the period. Current growth is supported by Vision 2030 capital programs that privilege logistics over ownership, by widening e-commerce networks and by the steady pivot toward battery-powered trucks. Contract lengths are becoming longer, fleet electrification is accelerating, and demand is spreading from the Eastern petrochemical belt to the mega-projects on the western seaboard. Competitive positioning is now defined by nationwide coverage, compliance expertise and the ability to supply smart, high-capacity units on demand.

Key Report Takeaways

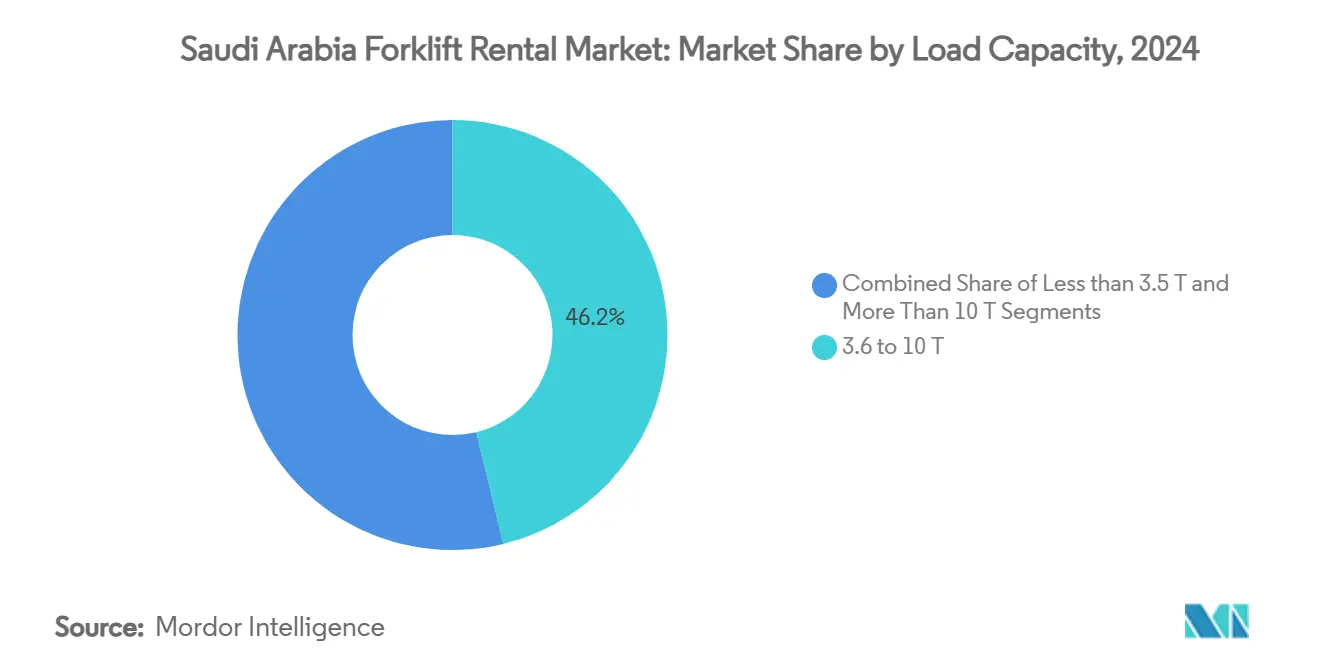

- By load capacity, the 3.6 to 10 ton class led with 46.25% of Saudi Arabia forklift rental market share in 2024, while units above 10 tons are on track for a 9.63% CAGR through 2030.

- By rental duration, mid-term contracts captured 42.10% of the 2024 value; long-term leases are projected to expand at an 8.76% CAGR to 2030.

- By power source, electric forklifts held 55.30% of % Saudi Arabia forklift rental market share in 2024 and will advance at a 12.18% CAGR through 2030.

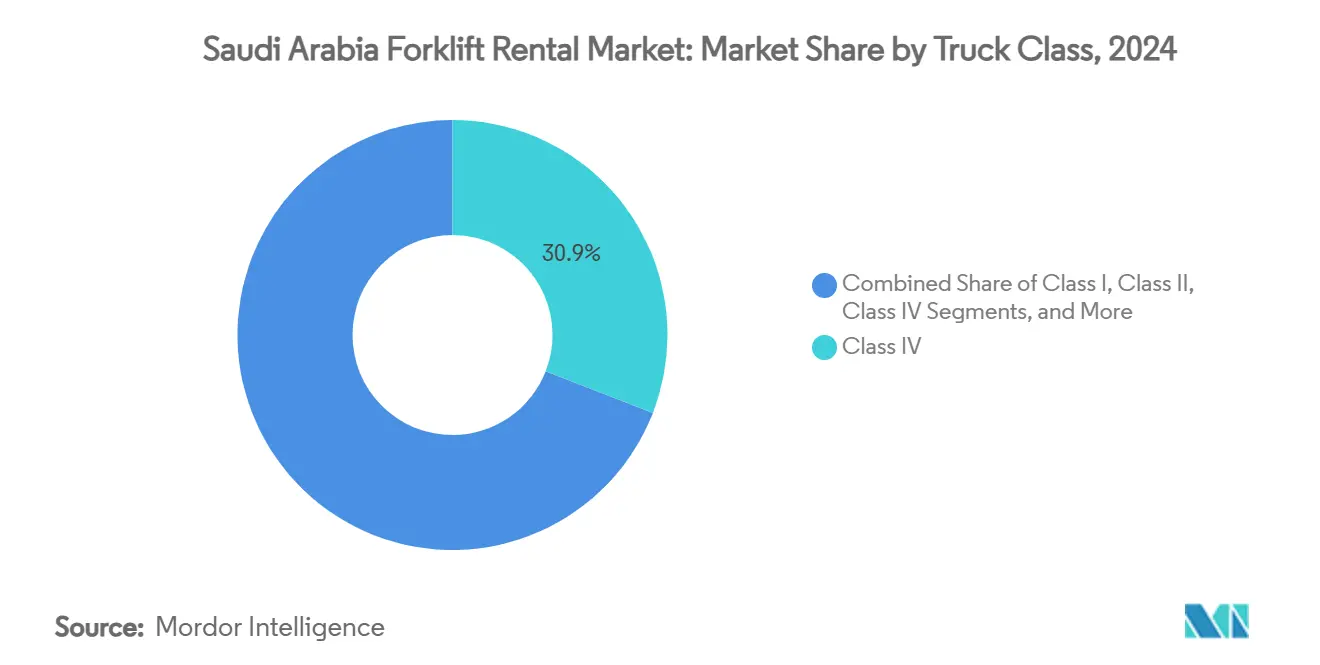

- By truck class, Class IV units accounted for 30.95% of the 2024 Saudi Arabia forklift rental market size, whereas Class I is the fastest-growing at 10.07% CAGR.

- By end-use industry, warehousing and logistics contributed 39.85% of 2024 revenue; the e-commerce warehousing slice is set to rise at 13.48% CAGR to 2030.

- By geography, the Eastern Province supplied 33.90% of 2024 rentals; the Western Province is forecast to post the quickest rise at 11.36% CAGR.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Saudi arabia. The forklift rental market share in our global report expresses these relative weights.

Saudi Arabia Forklift Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Logistics Build-Out | +2.1% | National, concentrated in Eastern and Western Provinces | Long term (≥ 4 years) |

| E-Commerce Warehouse Boom | +1.8% | National, with early gains in Riyadh, Jeddah, Dammam | Medium term (2–4 years) |

| Mega-Projects (NEOM, Red Sea, Qiddiya) | +1.6% | Western Province primary, spill-over to Northern Region | Long term (≥ 4 years) |

| Cap-Ex Shift to Rental Model | +0.9% | National, accelerated in industrial zones | Short term (≤ 2 years) |

| Green-Hydrogen Forklift Pilots | +0.7% | Eastern Province industrial complexes, NEOM development | Medium term (2–4 years) |

| Localization Tax Incentives on E-Forklifts | +0.5% | National, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Logistics Build-Out Transforms Equipment Demand

Saudi Arabia's USD 267 billion logistics sector investment through 2030 fundamentally reshapes forklift rental demand patterns, with 59 planned logistics centers covering over 1 billion square feet, creating sustained equipment requirements[1]Nadin Hassan, "Saudi Arabia to invest $267bn in logistics to become global hub by 2030," Arab News, arabnews.com.. The Kingdom's logistics market expansion from USD 27.6 billion in 2020 to a projected USD 38.8 billion by 2026 at a 5.85% CAGR demonstrates the sector's strategic importance beyond oil revenues[2]Lara Albertina Rebello, "Make way for the Middle East: UAE, KSA's ambitious drive to become global integrated logistics hubs," Maersk, maersk.com. . The Saudi Port Authority's USD 4.5 billion investment in 2024 for port infrastructure development directly drives forklift rental demand at maritime logistics hubs, particularly the USD 240 million DP World-Mawani logistics park at Jeddah Islamic Port, featuring 390,000 pallet positions. This infrastructure buildout creates predictable, long-term rental contracts that stabilize market revenues while reducing traditional cyclical volatility. The Special Integrated Logistic Zone (SILZ) in Riyadh, covering 32 million square feet, offers VAT exemptions and customs duty suspensions that incentivize logistics companies to establish operations requiring substantial material handling equipment fleets.

E-Commerce Warehouse Boom Drives Rental Acceleration

E-commerce infrastructure expansion creates the fastest-growing forklift rental subsegment at 13.48% CAGR through 2030, as digital commerce platforms establish fulfillment networks across Saudi urban centers. The warehousing sector's projected growth to USD 13.2 billion by 2030 reflects last-mile delivery infrastructure requirements that demand flexible, scalable material handling solutions. CEVA Logistics and Almajdouie Logistics' October 2024 joint venture, employing 2,000 people with 2,000+ assets, positions among the Kingdom's top 5 logistics players and demonstrates international operators' commitment to Saudi e-commerce infrastructure. DHL Supply Chain and Aramco's February 2024 ASMO joint venture integrates AI, data analytics, and blockchain technologies into supply chain operations, creating demand for smart, connected material handling equipment that supports digital logistics transformation. The shift toward automated warehouse operations requires rental companies to invest in electric, IoT-enabled forklifts that integrate with warehouse management systems, driving premium rental rates and longer contract durations.

Mega-Projects Create Sustained Industrial Equipment Demand

NEOM, Red Sea Development, and Qiddiya mega-projects generate concentrated forklift rental demand exceeding USD 1.25 trillion in total project value, with construction output projected to reach USD 181.5 billion by 2028. The Port of NEOM's 2026 Terminal 1 launch features Saudi Arabia's first automated remote-controlled cranes, indicating the project's advanced logistics infrastructure requirements that extend to material handling equipment throughout the development. Byrne Equipment Rental's expansion strategy targets explicitly the Red Sea and NEOM regions, with the company's 5,000+ unit fleet positioned to serve remote off-site camps and specialized project requirements[3]"Pursuing expansion opportunities in Saudi Arabia," Oil Review Middle East, oilreviewmiddleeast.com.. The King Salman Energy Park (SPARK) targets 100,000 job creation and USD 6 billion annual economic dividend by 2035, with 80% of the first phase allocated to industrial investors representing over USD 2 billion in commitments. These mega-projects require specialized heavy-duty forklifts with a capacity of above 10 tons, driving the segment's 9.63% CAGR through 2030 as standard equipment proves insufficient for large-scale industrial operations.

Cap-Ex Shift to Rental Model Optimizes Cash Flow

Saudi industrial companies increasingly prefer rental arrangements over equipment purchases to preserve capital for core operations, with this preference accelerated by the Kingdom's 54% surge in industrial investments to SAR 1.5 trillion in 2024 following expatriate fee waivers. The GCC construction equipment market's growth from 73,280 units in 2023 to a projected 102,039 units by 2029 at 5.67% CAGR reflects regional preference for flexible equipment access over ownership. Saudi Arabia's USD 160 billion infrastructure investment in 2024 across 1,000 projects creates demand spikes that rental models serve more efficiently than permanent equipment purchases, particularly for companies managing multiple simultaneous projects. The Regional Headquarters (RHQ) program requiring multinational companies to establish Saudi operations by January 2024 creates additional rental demand as international firms avoid large capital commitments while establishing local presence. Material handling equipment rental provides operational flexibility that aligns with project-based revenue cycles, allowing companies to scale equipment capacity dynamically without balance sheet impacts that could affect debt covenants or investment ratios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-Price Investment Cyclicality | -0.8% | National, concentrated in Eastern Province industrial zones | Short term (≤ 2 years) |

| Skilled-Operator Shortage | -0.6% | National, acute in Northern and Southern Regions | Medium term (2–4 years) |

| Saudization Cost Pressures | -0.4% | National, varying by company size and sector | Medium term (2–4 years) |

| Spare Parts Supply Chain Delays | -0.3% | Western and Central logistics corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Oil-Price Investment Cyclicality Affects Industrial Spending

Oil price volatility continues influencing Saudi industrial investment cycles despite Vision 2030 diversification efforts, with petroleum revenues still governing public spending patterns that cascade through equipment rental demand. Academic research demonstrates oil price uncertainty consistently shows negative impact on Saudi stock market returns, indicating broader economic sensitivity to energy price fluctuations that affect capital equipment decisions. The Eastern Province's 33.90% market share in 2024 reflects concentrated petrochemical and energy infrastructure that remains vulnerable to commodity price cycles, though mega-project investments provide countercyclical demand stability. Oil sector CAPEX projections of USD 730 billion by 2030 create substantial equipment demand, but quarterly variations in crude prices generate investment timing uncertainties that rental companies must navigate through flexible contract structures. The Kingdom's economic diversification progress reduces oil dependency gradually, with non-oil sectors contributing increasing portions of GDP growth that stabilize equipment rental demand patterns over time.

Skilled-Operator Shortage Constrains Market Growth

The Saudization policy's 2025 updates create skilled operator shortages that constrain forklift rental market expansion, as companies struggle to meet mandatory Saudi national employment quotas while maintaining operational efficiency. PwC identifies skilled labor shortage as a key logistics sector challenge, with workforce development initiatives struggling to match rapid infrastructure expansion pace. The Nitaqat classification system's increased stringency affects equipment rental companies' operational costs, as higher Saudi national employment requirements increase labor expenses that must be absorbed through rental rate adjustments or margin compression. Regional Headquarters (RHQ) programs offer Saudization quota exemptions for qualifying multinational companies, creating competitive advantages for international rental firms that can navigate regulatory requirements effectively. Training programs for Saudi women in high-tech logistics roles, as implemented at the Port of NEOM, represent long-term solutions to operator shortages, though immediate market constraints persist through the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Load Capacity: Heavy-Duty Demand Accelerates Industrial Growth

The 3.6 to 10 ton segment commands 46.25% market share in 2024, reflecting broad industrial applications across warehousing, construction, and manufacturing sectors that require moderate lifting capacity for standard operations. Heavy-duty forklifts above 10 tons emerge as the fastest-growing segment at 9.63% CAGR through 2030, driven by mega-project requirements and industrial complex expansions that demand specialized material handling capabilities. The King Salman Energy Park (SPARK) and similar industrial developments require heavy-duty equipment for petrochemical processing and large-scale manufacturing operations, creating sustained demand for high-capacity units. Light-duty units under 3.5 tons serve niche applications in retail and small-scale logistics operations, maintaining steady demand but limited growth potential as the market shifts toward larger-scale industrial applications.

Komatsu's March 2024 launch of electric forklifts powered by sodium-ion batteries represents a technological advancement in the heavy-duty segment. These forklifts offer rapid charging and extended cycle life, reducing operational costs for industrial users.Saudi Arabia's USD 160 billion infrastructure investment across 1,000 projects in 2024 creates concentrated demand for heavy-duty material handling equipment that standard forklifts cannot accommodate, driving rental companies to expand their high-capacity fleet offerings.

By Rental Duration: Long-Term Contracts Gain Strategic Preference

Mid-term rentals (1 to 12 months) capture 42.10% market share in 2024, aligning with construction project timelines and seasonal demand fluctuations that characterize Saudi industrial activity patterns. Long-term leases (3-5 years) grow fastest at 8.76% CAGR through 2030, reflecting companies' strategic shift toward predictable operational expenses and equipment modernization cycles that rental arrangements facilitate more effectively than ownership. The 59 logistics centers planned under Vision 2030 create multi-year equipment requirements that favor long-term rental contracts, providing revenue stability for equipment providers while offering cost predictability for logistics operators. Short-term spot rentals maintain relevance for emergency replacements and peak season capacity augmentation, though their market share contracts as companies optimize equipment planning processes.

The Regional Headquarters (RHQ) program's requirement for multinational companies to establish Saudi operations creates demand for flexible rental arrangements that accommodate business development uncertainties while maintaining operational capabilities. CEVA Logistics and Almajdouie Logistics' October 2024 joint venture demonstrates how strategic partnerships require long-term equipment commitments to support integrated logistics operations across multiple facilities. The shift toward longer rental durations reflects equipment users' preference for operational flexibility without capital commitment, particularly as technological advancement accelerates equipment obsolescence cycles.

By Power Source: Electric Dominance Reflects Sustainability Mandates

Electric forklifts command 55.30% market share in 2024 while maintaining the fastest growth at 12.18% CAGR through 2030, driven by sustainability mandates and operational cost advantages in warehouse environments. Internal combustion engines (diesel/LPG) serve outdoor applications and heavy-duty operations where electric alternatives face performance limitations, though their market share contracts as battery technology advances. Saudi Arabia's green logistics implementation study identifies environmental awareness and technological readiness as key factors driving electric equipment adoption, though financial considerations and infrastructure requirements create adoption barriers. Hybrid solutions occupy a transitional market position, offering operational flexibility while companies evaluate full electric conversion strategies.

The Port of NEOM's automated operations and renewable energy integration create demand for electric material handling equipment that aligns with the project's sustainability objectives. DP World and Mawani's USD 240 million Jeddah logistics park features a 20 MW rooftop solar plant, demonstrating infrastructure development that supports electric forklift operations through renewable energy integration. The Kingdom's photovoltaic electric vehicle charging infrastructure development, as demonstrated in Hail City case studies, indicates broader electrification trends that extend to material handling equipment across industrial facilities. Rental companies increasingly invest in electric fleets to meet customer sustainability requirements while capturing premium rental rates for advanced technology equipment.

By Truck Class: Versatile Class IV Leads Market Applications

Class IV forklifts hold 30.95% market share in 2024, reflecting their versatility across indoor and outdoor applications that serve diverse industrial requirements from warehousing to construction sites. Class I units emerge as the fastest-growing segment at 10.07% CAGR through 2030, driven by warehouse automation trends and electric vehicle adoption that favor counterbalanced electric forklifts for indoor operations. The global lift truck industry's 8% revenue growth to USD 58.2 billion in 2024 demonstrates strong demand for materials handling equipment, with electric trucks and automation driving technological advancement. Class II and Class III units serve specialized warehouse applications with narrow aisle requirements, maintaining steady demand in high-density storage facilities.

DHL Supply Chain and Aramco's ASMO joint venture integration of AI, data analytics, and blockchain technologies creates demand for smart, connected forklifts that support digital logistics transformation across multiple truck classes. Class V units serve rough terrain applications in construction and outdoor industrial sites, with demand linked to mega-project development timelines and infrastructure construction phases. The Special Integrated Logistic Zone (SILZ) in Riyadh's 32 million square feet requires diverse forklift classifications to serve varied logistics operations from air cargo handling to distribution center management. Rental companies optimize fleet composition across truck classes to serve diverse customer applications while maximizing equipment utilization rates.

By End-Use Industry: E-Commerce Drives Warehousing Transformation

Warehousing and logistics applications dominate with 39.85% market share in 2024, though e-commerce warehousing subsegments accelerate at 13.48% CAGR through 2030 as digital commerce infrastructure scales rapidly across Saudi urban centers. Construction sector demand remains substantial, supported by USD 181.5 billion projected construction output by 2028 and mega-project developments that require sustained material handling equipment deployment. Automotive sector applications benefit from an industrial investment surge, with 54% growth in industrial investments to SAR 1.5 trillion in 2024, creating expanded manufacturing capacity that requires material handling support. Food and beverage, aerospace and defense, and other retail and pharmaceutical sectors maintain steady demand patterns linked to economic diversification initiatives.

The Saudi logistics market's expansion from USD 27.6 billion in 2020 to projected USD 38.8 billion by 2026 at a 5.85% CAGR demonstrates sector-wide growth that benefits forklift rental demand across multiple end-use industries. Arabian Machinery & Heavy Equipment Co. (AMHEC) serves major clients, including Saudi Aramco and SABIC, with over 300 light equipment units, demonstrating established relationships between rental companies and key industrial end-users. The 59 planned logistics centers covering over 1 billion square feet create diversified end-use demand that reduces rental companies' dependence on single industry cycles while providing growth opportunities across multiple sectors.

Geography Analysis

The Eastern Province, home to Saudi Aramco and SABIC clusters, anchors one-third of 2024 revenue for the Saudi Arabia forklift rental market. Unique Group opened a 2,000 m² service hub in Dammam during February 2025 to shorten response times for offshore suppliers. SPARK’s freight village drives high-capacity diesel rentals and specialized explosion-proof electric models.

The Western Province will be the fastest riser. DP World’s new logistics park and NEOM’s automated port together inject multi-year volume with a tilt toward electrics powered by on-site renewables. Qiddiya entertainment district adds seasonal peaks that are ideally met through rental rather than ownership.

Riyadh’s central corridor benefits from the Special Integrated Logistic Zone, which waives duties on imported parts and positions the capital as an e-commerce gateway. Northern and Southern corridors account for a modest share today yet stand to grow as the national rail network links to Jordan, Yemen and Oman, extending the spatial footprint of the Saudi Arabia forklift rental market.

Mordor Intelligence examines the forklift rental market across diverse other regional markets as well, including North America, while also offering granular country-level perspectives for United Arab Emirates, United States, Indonesia, South Korea, and Brazil and more.

Competitive Landscape

Competition is moderate, with international OEM-backed dealers and independent local renters active. Abdul Latif Jameel Machinery Trading Co., Ltd has one of the largest branded fleets, along with key OEM distributors such as Alkhorayef Group and Al-Jomaih Equipment. Kanoo Machinery, Zahid Group (EJAR), anchors regional distribution and field service.

Byrne Equipment Rental's 5,000+ unit fleet and 20% UAE market share demonstrate the scale advantages required to serve major industrial clients, while the company's strategic focus on Red Sea and NEOM regions indicates geographic specialization strategies. White-space opportunities emerge in specialized applications, including green hydrogen forklift pilots and automated warehouse integration, where technology adoption creates premium rental segments with higher margins and longer contract durations.

Regulatory compliance through SASO’s Saber certification favors incumbents with documented safety records. Suppliers that add lithium-ion or hydrogen fuel-cell models plus predictive-maintenance analytics are achieving price premiums and multi-year renewals. No single participant controls more than 25% of spend, keeping pricing rational but not restrictive.

Saudi Arabia Forklift Rental Industry Leaders

-

Abdul Latif Jameel Machinery Trading Co., Ltd

-

Kanoo Machinery

-

Alkhorayef Group

-

Zahid Group (EJAR)

-

Al-Jomaih Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: CEVA Logistics and Almajdouie Logistics finalized creation of their joint venture in Saudi Arabia, named CEVA Almajdouie Logistics, employing around 2,000 people and operating a fleet of over 2,000 assets. The partnership positions the venture among the top 5 logistics players in the country, leveraging CEVA's global network and Almajdouie's local infrastructure to meet growing logistics demand.

- June 2024: DP World and the Saudi Ports Authority (Mawani) broke ground on a USD 240 million logistics park at Jeddah Islamic Port, set to become the largest integrated logistics hub in Saudi Arabia. The facility covers 415,000 square meters with 185,000 square meters of grade-A warehouse space and over 390,000 pallet positions, featuring a 20 MW rooftop solar plant for renewable energy generation.

- January 2024: Unique Group expanded operations in Saudi Arabia with a new 2,000 square meter facility in Dammam, featuring equipment available for sale and rental to support local market needs. The expansion aligns with Saudi Vision 2030 and includes partnerships with major players like Aramco and NEOM, demonstrating growing demand for specialized equipment services in the Kingdom's evolving industrial landscape.

Saudi Arabia Forklift Rental Market Report Scope

| Less than 3.5 T |

| 3.6 to 10 T |

| More Than 10 T |

| Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) |

| Long-term Lease (3 to 5 years) |

| Electric |

| Internal Combustion (Diesel/LPG) |

| Hybrid |

| Class I |

| Class II |

| Class III |

| Class IV |

| Class V |

| Warehousing and Logistics |

| Construction |

| Automotive |

| Food and Beverage |

| Aerospace and Defense |

| Others (Retail, Pharma, etc.) |

| Central Region (Riyadh) |

| Eastern Province (Dammam, Jubail) |

| Western Province (Jeddah, Makkah) |

| Northern Region |

| Southern Region |

| By Load Capacity | Less than 3.5 T |

| 3.6 to 10 T | |

| More Than 10 T | |

| By Rental Duration | Short-term/Spot (Less than 1 month) |

| Mid-term (1 to 12 months) | |

| Long-term Lease (3 to 5 years) | |

| By Power Source | Electric |

| Internal Combustion (Diesel/LPG) | |

| Hybrid | |

| By Truck Class | Class I |

| Class II | |

| Class III | |

| Class IV | |

| Class V | |

| By End-use Industry | Warehousing and Logistics |

| Construction | |

| Automotive | |

| Food and Beverage | |

| Aerospace and Defense | |

| Others (Retail, Pharma, etc.) | |

| By Region | Central Region (Riyadh) |

| Eastern Province (Dammam, Jubail) | |

| Western Province (Jeddah, Makkah) | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

How large is the Saudi Arabia forklift rental market today?

The Saudi Arabia forklift rental market size stood at USD 131.25 million in 2025 and is forecast to reach USD 178.23 million by 2030.

Which forklift segment is growing the fastest?

Rentals of units above 10 tons are projected to post the quickest rise at 9.63% CAGR thanks to mega-project demand.

Why are battery forklifts gaining ground in Saudi warehouses?

Zero-emission mandates, lower running costs, and new solar-powered charging hubs are pushing electric models to a 12.18% CAGR through 2030.

What rental duration is most common?

Mid-term contracts of 1-12 months held 42.10% share in 2024, yet long-term leases are growing faster as logistics centers lock in multi-year agreements.

Which region offers the highest growth potential?

The Western Province, home to NEOM and Red Sea Project, will advance at 11.36% CAGR, the quickest regional pace through 2030.

Who are the leading suppliers?

Toyota Material Handling, KION Group, Hyster-Yale, Kanoo Machinery, Zahid Tractor and Al-Jomaih Equipment top the list, with no single firm exceeding one-quarter of revenue.

Page last updated on: