Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

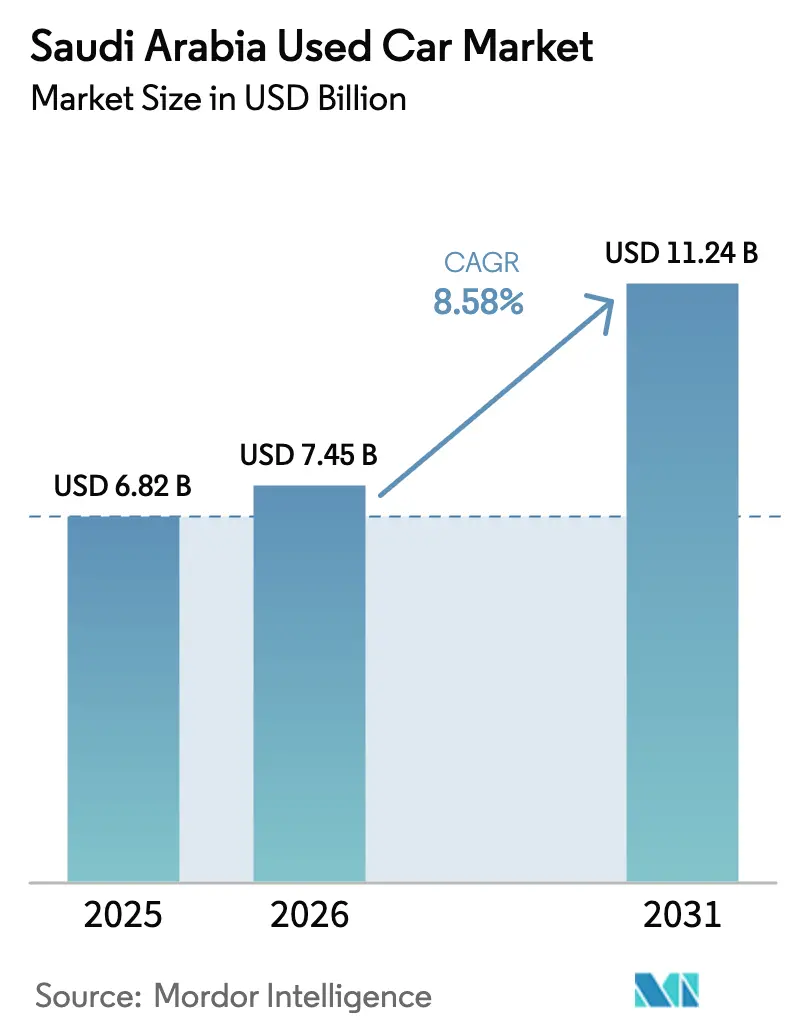

| Base Year Market Size (2025) | USD 6.82 Billion |

| Market Size (2026) | USD 7.45 Billion |

| Market Size (2031) | USD 11.24 Billion |

| Growth Rate (2026 - 2031) | 8.58% CAGR |

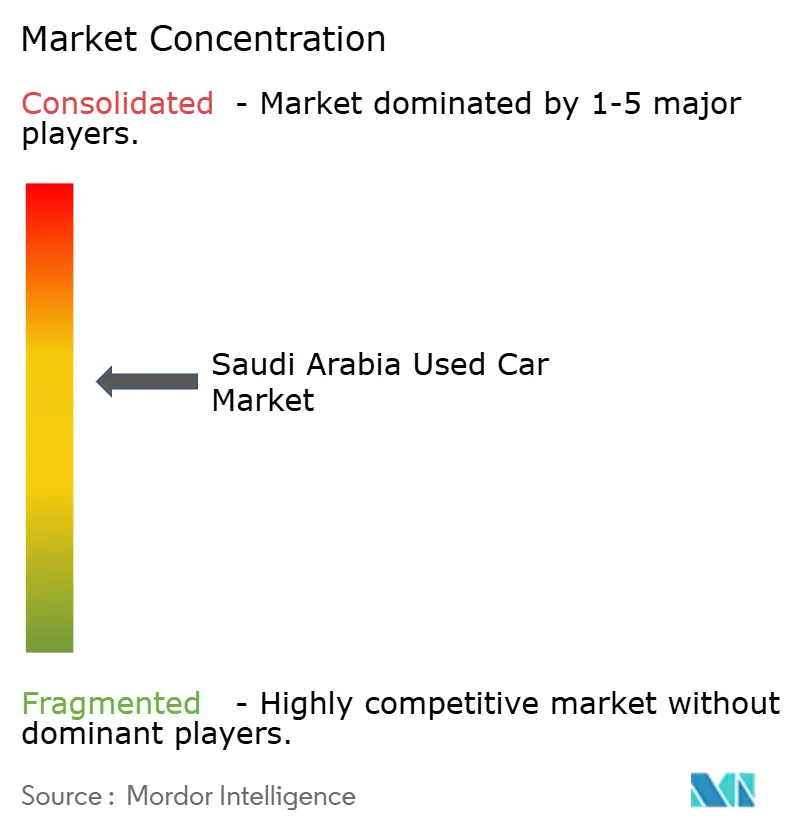

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Used Car Market Analysis by Mordor Intelligence

The Saudi Arabia used car market size is expected to grow from USD 6.82 billion in 2025 to USD 7.45 billion in 2026 and is forecast to reach USD 11.24 billion by 2031, registering an 8.58% CAGR over the forecast period (2026-2031). Robust population growth, stricter import rules, and mandatory comprehensive insurance are pushing many households toward certified pre-owned vehicles that bundle warranties with inspection reports. Online platforms are shortening listing-to-sale cycles and raising price transparency, while ride-hailing drivers and metro-linked commuters keep everyday sedans and compact SUVs in steady demand. Larger families are shifting to sport-utility vehicles that offer third-row seating and heat-resilient cooling systems, and this preference is widening resale premiums for models with complete service histories. Fuel economics still favor gasoline engines; however, the gradual rollout of charging stations and technician training is beginning to support a small but expanding battery-electric resale market. Competitive intensity remains high because roadside lots require little capital, but scale efficiencies are accruing to organized vendors that integrate financing, warranty, and logistics into a single transaction flow.

Key Report Takeaways

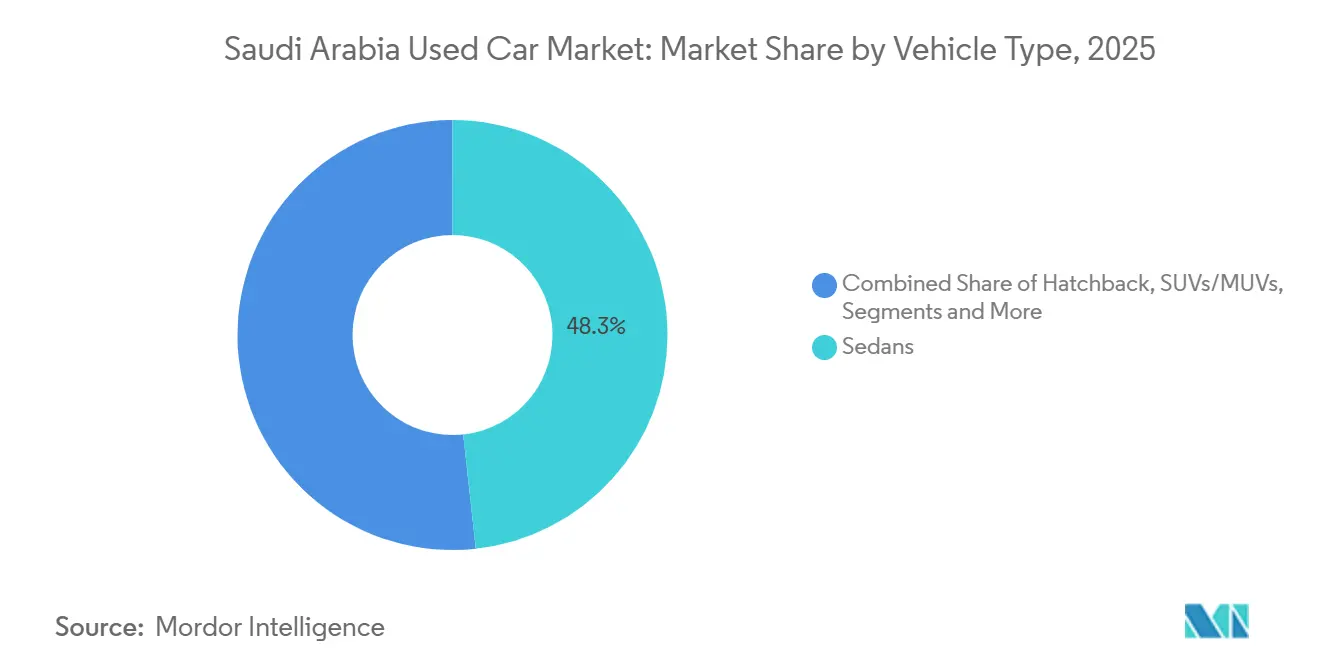

- By vehicle type, sedans led the Saudi Arabia used car market share in 2025, with 48.28%, while sport-utility vehicles are expected to expand at a 10.16% CAGR through 2031.

- By fuel type, gasoline powertrains accounted for 90.16% of the Saudi Arabia used-car market share in 2025, and battery-electric vehicles are projected to register the fastest growth, with a 16.24% CAGR, through 2031.

- By vehicle age, the three-to-five-year band captured 39.42% of the Saudi Arabia used-car market share in 2025, whereas the sub-three-year inventory is growing at a 11.91% CAGR over the same horizon.

- By mileage band, units with 40,000–80,000 kilometers held 35.32% of the Saudi Arabia used-car market share in 2025, and the sub-40,000-kilometer group is projected to grow at a 9.63% CAGR through 2031.

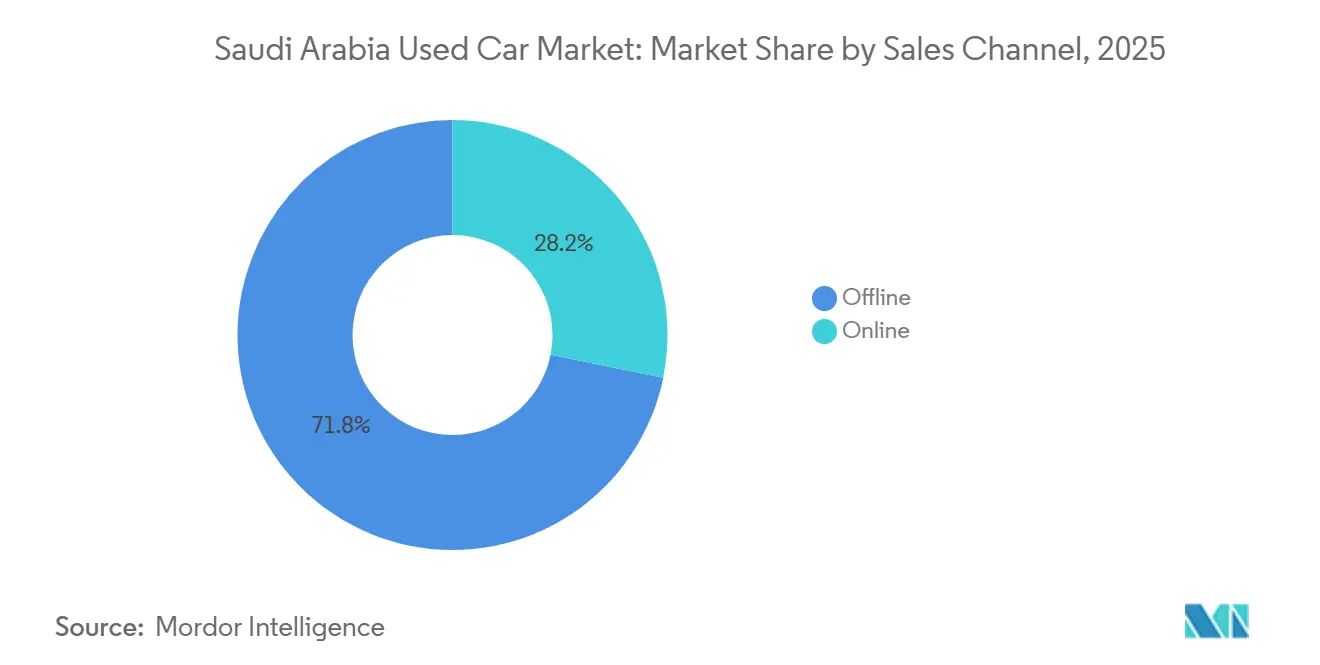

- By sales channel, offline dealers accounted for 71.82% of the Saudi Arabia used-car market share in 2025, while online platforms are expected to grow at a 13.61% CAGR through 2031.

- By vendor type, unorganized players accounted for 59.31% of the Saudi Arabia used car market share in 2025, while organized vendors are expected to expand at a 14.2% CAGR through 2031.

- By region, the Western region led with 34.43% of the Saudi Arabia used car market share in 2025, whereas the Central region is projected to post the fastest growth, with a 9.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Adoption Boosting Online Sales | +2.4% | National, led by Riyadh and Jeddah, expanding to secondary cities | Short term (≤2 years) |

| Certified Pre-Owned Demand From Confidence Programs | +2.1% | National, strongest in urban centers (Riyadh, Jeddah, Dammam) | Medium term (2–4 years) |

| Rising Insurance Costs Driving Used Purchases | +1.8% | National, with concentration in Central and Western regions | Medium term (2–4 years) |

| Riyadh Metro Expansion Fueling Car Demand | +1.3% | Central region, with spillover to Eastern province | Short term (≤2 years) |

| Scrappage Incentives Adding Sedans To Resale Pool | +0.6% | Central and Western regions, concentrated in Riyadh, Jeddah, and Makkah | Long term (≥4 years) |

| Expat Repatriations Creating Seasonal Supply Spikes | +0.5% | National, with peaks in Eastern region (oil sector) and Western region (commercial hubs) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Digital Platforms Compress Transaction Friction and Lift Online Share

Refurbishment centers, processing thousands of vehicles each year, are now matching e-commerce speeds on the showroom floor. With return windows and AI-driven pricing engines, these centers are revolutionizing the vehicle sales landscape. Same-day inspection slots, in-app financing, and instant insurance quotes have significantly reduced the typical negotiation cycle. The online share of vehicle sales is experiencing steady growth, driven by the adoption of electronic invoicing and VAT compliance. Furthermore, transparent condition reports and standardized warranties are successfully attracting price-sensitive buyers, shifting them away from informal roadside markets and toward more formal channels of trade.

Certified Pre-Owned Programs Build Post-Warranty Confidence

Original-equipment manufacturers are rolling out multi-point inspection schemes that combine roadside assistance with guarantees of varying durations. Volkswagen's comprehensive checklist and Audi's Approved Plus inspections have redefined retail benchmarks [1]“Certified Pre-Owned Program Details,” Volkswagen Middle East, volkswagen-me.com. Nissan's Intelligent Choice provides coverage for a specified period, while Toyota's Hybrid Extra Care focuses on battery concerns for its electrified models. Land Rover, aiming to attract premium SUV buyers, offers transferable warranties with extended durations. Digital marketplaces are adopting these high standards, recognizing the increasing buyer expectation for factory-level assurance even in second-hand purchases.

Escalating Insurance Premiums Shift Buyers to Pre-Owned Stock

Motor insurance revenue experienced significant growth, driven by increased prices across all segments after loss ratios exceeded acceptable levels [2]“Insurance Sector Financial Stability Report 2025,” Saudi Central Bank, sama.gov.sa. The introduction of mandatory comprehensive policies further raised annual premiums for new car buyers. Mid-income households, constrained by deductible caps, are now focusing on sedans and SUVs within a more affordable price range, where premiums are comparatively lower. Certified pre-owned warranties help mitigate maintenance concerns, making these vehicles attractive to first-time owners and ride-hailing drivers. This shift in purchasing behavior is reflected in the growing number of bank applications for used-car loans at the maximum loan-to-value ceiling.

Riyadh Metro Expansion Fuels Central-Region Commuter Demand

Riyadh Metro's Phase I debuted, featuring numerous stations spanning a significant distance, designed to accommodate a large number of daily passengers. Despite ongoing population inflows to the capital under Vision 2030, a notable percentage of residents find themselves outside a convenient walking distance to these stations. This gap has bolstered the demand for affordable sedans and compact SUVs, which are increasingly seen as essential for first- and last-mile transportation. Inventory turnover for dealers in Riyadh has improved, highlighting a swift absorption of certified stock. Additionally, financing packages tailored for ride-hailing drivers have further boosted sales in the affordable price range.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictive LTV Ratios Limiting Used-Car Loans | -1.2% |

National, acute for households earning |

Medium term (2–4 years) |

| Harsh Climate Accelerating Vehicle Depreciation | -0.7% | National, most severe in Central region (Riyadh) and interior provinces | Long term (≥4 years) |

| Import Rules Cutting Grey-Market Salvage Supply | -0.9% | National, strongest impact on luxury and sports-car segments in Eastern and Western regions | Long term (≥4 years) |

| Lack Of EV Technicians Weakening Resale Confidence | -0.4% | National, concentrated in urban centers with EV adoption (Riyadh, Jeddah, Dammam) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Restrictive Loan-to-Value (LTV) Rules Curbing Mid-Segment Purchases

The Saudi Central Bank limits auto-loan tenors to five years and caps salary deductions at one-third of gross income, shrinking credit headroom for families earning under SAR 15,000 per month. Banks typically finance a smaller percentage of a used car's price compared to new vehicles, while interest rates remain relatively high. Combined with higher comprehensive insurance costs, these monthly expenses either discourage potential buyers or lead them to opt for older, riskier models. As a result, auto finance accounts for a small portion of non-mortgage lending portfolios, with lenders remaining cautious due to concerns over fluctuations in residual values.

Tightened Import Rules Curtail Grey-Market Supply of Luxury and Sports Cars

Recent regulations prohibit imports of older vehicles and ban left-hand-drive conversions and salvage titles. Non-compliant vehicles face significant penalties based on their assessed value. These measures have effectively closed a channel that previously supplied discounted German sedans and Japanese performance cars from the UAE. As a result, affluent buyers are now turning to authorized dealer programs, which come with premium price tags. Meanwhile, platforms are shifting their focus towards mid-market SUVs and sedans, despite the narrower profit margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUV Momentum Adds Volume Outside Traditional Sedan Core

Sedans accounted for 48.28% of 2025 sales in the Saudi Arabia used car market, reflecting the country’s deep installed base of midsize Japanese and Korean models that cycle into the three-to-five-year resale band. Sport-utility and multi-utility vehicles are expanding at a 10.16% CAGR through 2031, as families seek cabin space, third-row seating, and cooling systems designed for desert heat. In the GCC, SUVs equipped with specialized cooling packages are valued higher than similarly aged and mileage sedans. With the introduction of strong new SUV models, including several from Toyota's upcoming lineup, the certified stock is expected to increase. Dealers note that SUVs are selling at a faster rate than the overall market average.

This trend aligns with rising affluence, growth in suburban housing, and periodic flooding in coastal cities, which favors vehicles with higher ground clearance. While fuel-economy challenges exist, they are mitigated by low domestic gasoline prices and the availability of improved hybrid options. Luxury sports cars are losing market share due to restrictions on salvaged imports and left-hand-drive conversions. Meanwhile, hatchbacks, preferred mainly by expatriates for urban parking convenience, remain a niche choice. As the vehicle mix increasingly shifts toward high-roof profiles, SUVs are expected to dominate the Saudi Arabia used car market in the coming years.

By Fuel Type: Gasoline Dominates While Early EV Signals Strengthen

Gasoline engines accounted for 90.16% of the Saudi Arabian used car market share in 2025, underscoring decades of reliance on internal-combustion technology and a refueling network that spans even small towns. Battery-electric resale volumes are currently small, but are expected to compound at a 16.24% CAGR through 2031, as charging points increase and technician training expands. As diesel passenger cars phase out, hybrids have emerged as a viable alternative, supported by warranty programs that protect key battery components.

Nonetheless, challenges remain: public chargers are limited and primarily concentrated in major cities, such as Riyadh, Jeddah, and Dammam, creating disparities in the prices of used EVs across smaller cities. The Technical and Vocational Training Corporation currently has a limited number of certified EV mechanics. Still, its new diploma program, in partnership with Lucid and KAUST, aims to address this shortage. Additionally, domestic production under the CEER brand is expected to expand its service networks and improve battery warranty transferability. These developments are likely to boost residual values and foster long-term confidence in Saudi Arabia's used car market.

By Vehicle Age: Three-to-Five-Year Sweet Spot Balances Price and Warranty

Units aged three to five years captured 39.42% of the Saudi Arabian used car market share in 2025, offering discounts of 35%–45% off new-car sticker prices while often retaining partial factory warranties. Sub-three-year stock is gaining fastest at 11.91% CAGR through 2031, driven by leasing returns and OEM buybacks that feed certified channels. Above-five-year segments draw budget-sensitive households and ride-hailing drivers willing to assume higher maintenance risk. Extreme ambient heat accelerates depreciation, making documented cooling-system service a decisive differentiator.

Regulatory loan maturities align seamlessly with the economic lifespan of cars, enabling banks to stay within safe value-recovery limits. Vehicles in the GCC, equipped with enhanced radiators and heat-resistant seals, hold a competitive edge over their parallel import counterparts. These dynamics position mid-age units as the foundational volume drivers of Saudi Arabia's used car market, a trend expected to persist through the decade's close.

By Mileage Band: Urban Driving Patterns Center on 40,000–80,000 Kilometers

Odometer readings between 40,000 and 80,000 kilometers covered 35.32% of the Saudi Arabian used car market share in 2025, correlating with three to five years of metropolitan commuting at roughly 13,000 kilometers a year. The sub-40,000-kilometer group is projected to rise at a 9.63% CAGR through 2031. Lower-mileage supply is expanding as corporate fleets rotate vehicles sooner, while the 80,000–120,000-kilometer bracket serves as replacements for taxis and rural buyers.

Mileage verification remains a challenge because the kingdom lacks a centralized database of historical records. Odometer fraud persists among informal lots despite SASO regulations. Digital vendors counter with encrypted service-record uploads and electronic odometer audits, a transparency layer that justifies their price premium. The Saudi Arabia used car market therefore sees growing consumer preference for fully traceable mileage ranges, pushing unverified high-kilometer units toward steeper discounts.

By Sales Channel: Online Platforms Chip Away at Legacy Offline Strongholds

Offline outlets retained 71.82% of the Saudi Arabian used car market share in 2025, but are conceding ground to e-commerce sites that integrate inspection, financing, and logistics. At the same time, the online platform is expected to grow at a CAGR of 13.61% through 2031. Listing-to-sale times on leading platforms fell from 45 days in early 2024 to 30 days by mid-2025 as AI-driven valuations narrowed the scope for price haggling. Reverse-logistics hubs now refurbish vehicles to a single industry standard, addressing buyer concerns about mechanical integrity.

Physical showrooms still dominate transactions above SAR 100,000, where test drives and third-party checks are non-negotiable. Yet, mandatory e-invoicing and VAT compliance under Vision 2030 are increasing back-office costs for unlicensed roadside traders, tilting the momentum toward tech-enabled models. These trends point to steady online share gains, potentially lifting the digital channel above one-third of the Saudi Arabia used car market by 2031.

By Vendor Type: Organized Players Gain Trust Through Warranty and Compliance

Unorganized vendors controlled 59.31% of the Saudi Arabian used car market share in 2025, reflecting low capital entry barriers and a cash-based bargaining system. Organized outfits—OEM-certified lines and venture-backed marketplaces—are growing at a 14.2% CAGR through 2031, driven by bank partnerships that favor standardized appraisal forms and verified service histories.

Import restrictions have cut grey-market inflows, further steering consumers toward authorized dealers. Extended warranties, transparent pricing, and buy-back guarantees anchor buyer confidence, while informal sellers feel margin pressure because they seldom provide return windows or VAT invoices. As Vision 2030 enforcement tightens, the organized cohort is on track to surpass 50% share of the Saudi Arabian used car market before the next decade.

Geography Analysis

The Western region, home to Jeddah, Makkah, and Madinah, accounted for 34.43% of transactions in the Saudi Arabia used-car market in 2025. Seasonal pilgrimage movements steered fleet operators to refresh sedans and vans every 3 to 5 years, feeding a steady flow of well-maintained units into local lots. Mazda operates eight showrooms across Jeddah, demonstrating a dense dealer network that supports a confident resale market. Commercial transport operators managing nearly 20,000 buses also channel support vehicles into the second-hand market, ensuring a steady supply of high-mileage vehicles for budget buyers.

The Central region, anchored by Riyadh, is expanding at a 9.46% CAGR through 2031, the fastest across the kingdom. Vision 2030 megaprojects and the newly opened metro draw migrants who still rely on private cars for first- and last-mile mobility, as more than one-third of residents live beyond easy station reach. Abdul Latif Jameel Finance programs aimed at ride-hailing drivers further reinforce demand for dependable compact sedans priced below SAR 50,000. Inventory turnover now stands at 45 days, five days faster than the national average, which underpins premium pricing for popular models.

The Eastern corridor, led by Dammam and Khobar, benefits from oil-sector salaries yet shows a smaller resale footprint because corporate fleet policies stretch retention periods. Southern and Northern provinces, such as Asir or Tabuk, are emerging catch-up markets where infrastructure spending raises disposable income, though dealer density remains thin. Import restrictions have particularly affected the Eastern region, which was once the gateway for grey-market luxury cars from the United Arab Emirates, prompting affluent consumers to opt for certified programs and mitigating volatility in the high-end supply. Digital listings are compressing regional price disparities, yet transport costs keep most sub-SAR 30,000 deals local, preserving provincial micro-markets within the broader Saudi Arabia used car market.

Competitive Landscape

The Saudi Arabia used car market is witnessing a diverse range of players. While unorganized roadside dealers and private sellers dominate, certified programs from Abdul Latif Jameel Motors, Al-Futtaim Automotive, and Al-Tayer Motors are rapidly gaining ground, driven by standardized warranties and factory-grade refurbishments. Digital platforms like Syarah and Kayishha are transforming the market by integrating appraisal, financing, and logistics into a seamless mobile experience, drawing tech-savvy buyers away from traditional dealerships. These organized entities are steadily increasing their market share.

Economies of scale are benefiting companies that combine physical infrastructure with data-driven strategies. Syarah operates a reconditioning hub that enhances customer confidence by offering return policies, narrowing the assurance gap between new and used car purchases [3]“Corporate Press Release: Series C Funding,” Syarah, syarah.com. Supported by the Public Investment Fund, Kayishha is expanding its network of buying centers to cater to sellers seeking quick transactions and immediate cash. Meanwhile, Dubizzle uses AI-driven algorithms to streamline inspections, improving efficiency and reducing operational costs.

The resale market for electric vehicles (EVs) remains underdeveloped—a limited number of EV-certified technicians nationwide hampers aftermarket confidence. Companies that can ensure battery health and provide transferable warranties are well-positioned to gain an early advantage. Additionally, policy changes requiring e-invoicing and VAT submissions are increasing compliance costs for informal dealers, driving market consolidation. This is likely to result in a two-tier structure, with nationwide platforms dominating high-volume certified inventory and regional specialists focusing on price-sensitive segments within the broader Saudi used car market.

Saudi Arabia Used Car Industry Leaders

-

Al-Futtaim Automotive (AutoTrust)

-

Al-Tayer Motors

-

Al-Nabooda Automobiles

-

Arabian Auto Agency

-

YallaMotor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Cartea introduced a complimentary car-selling service for GCC users, offering a secure and user-friendly platform for online car listings and buyer connections.

- September 2024: Syarah, a Saudi-based company, clinched USD 60 million in Series C funding, aiming to broaden its marketplace for both new and used cars.

- May 2024: Dubizzle Motors acquired Drive Arabia to integrate AI-driven valuation tools that reduce inspection times below 30 minutes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Saudi Arabia used-car market as the value of all previously registered passenger vehicles, ex-rental, fleet returns, imports, and consumer trade-ins, re-sold through online platforms or physical dealerships during the calendar year.

Scope Exclusions: vehicles written off by insurers or dismantled for parts are left outside the definition to keep comparability intact.

Segmentation Overview

-

Vehicle Type

- Hatchback

- Sedans

- Sports Utility Vehicles and Multi-purpose Vehicles

- Luxury and Sports Cars

-

By Fuel Type

- Gasoline

- Diesel

- Hybrid-Electric (HEV)

- Battery-Electric (BEV)

- Other Fuel Type (CNG, LPG, etc.)

-

By Vehicle Age

- Less Than 3 Years

- 3 – 5 Years

- 6 – 8 Years

- Over 8 Years

-

By Mileage Band

- Less Than 40,000 km

- 40,000 – 80,000 km

- 80,000 – 120,000 km

- Over 120,000 km

-

By Sales Channel

- Online

- Offline

-

By Vendor Type

- Organized

- Unorganized

-

By Region

- Central (Riyadh)

- Western (Jeddah, Makkah, Madinah)

- Eastern (Dammam, Khobar)

- Southern (Asir, Jazan)

- Northern (Tabuk, Hail)

Detailed Research Methodology and Data Validation

Primary Research

Discussions with Riyadh and Jeddah showroom managers, online platform product heads, inspection-center owners, and vehicle finance officers allow us to verify stock rotation cycles, typical discount ladders, and emerging EV premiums. Follow-up surveys with recent buyers across Western, Central, and Eastern regions close data gaps and fine-tune age-band assumptions.

Desk Research

Mordor analysts begin with Saudi General Authority for Statistics registrations, Zakat & Customs import tallies, and Saudi Central Bank auto-loan data to size the available pool, then layer prices quoted by the Ministry of Commerce's weekly used-car bulletin. Macro variables such as GDP per capita trends from the World Bank and Brent crude movements help us gauge consumer purchasing power swings. To refine segment splits, we consult open access trade sites such as Bestsellingcarsblog for model-wise turnover, KAPSARC fuel-economy papers for drivetrain mix, and peer-reviewed studies on desert climate wear patterns; company filings and local press provide transaction benchmarks, while D&B Hoovers supplies dealer revenue checks for spot validation. This list is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction starts from annual transfers, imports, and scrappage to derive the available stock, which is then filtered through observed turnover rates and average selling prices. Select bottom-up roll-ups, sample dealer volumes multiplied by verified ASPs, provide a reasonableness check. Key fingerprints include first-ownership transfer ratio, online share of transactions, bank loan-to-value ceilings, female-driver licensing growth, and BEV penetration. Forecasts employ a multivariate regression where unit demand is explained by real household income, new-car CPI, and fuel-price differentials; scenario analysis tests swings in Vision 2030 incentives. Data gaps in rural provinces are bridged using calibrated mileage-band proxies.

Data Validation & Update Cycle

Outputs pass three layers of analyst review. Outliers trigger re-contacts with respondents, and every figure is reconciled with independent signals such as quarterly bank loan books. Reports refresh annually, with mid-cycle updates after material regulatory or taxation shifts.

Why Mordor's Saudi Arabia Used Car Baseline Commands Reliability

Published values often diverge because studies vary in scope, price assumptions, and refresh timing.

Key gap drivers include whether nearly-new imports are counted, if fleet auctions are annualized, the aggressiveness of ASP escalation, and frequency of model updates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.87 B | Mordor Intelligence | |

| USD 6.83 B | Regional Consultancy A | excludes online-only sales, undercounts EV premiums |

| USD 10.70 B | Global Consultancy B | folds fleet lease-backs and grey imports into retail universe |

| USD 37.91 B | Industry Journal C | aggregates wider GCC data and salvage resales into KSA totals |

The comparison shows how definition breadth and data discipline sway outcomes. By anchoring numbers to verifiable registrations and live dealer inputs, Mordor delivers a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

How big is the Saudi Arabia used car market today?

The Saudi Arabia used car market size reached USD 7.45 billion in 2026 and is on course to hit USD 11.16 billion by 2031.

Which segment holds the largest share of sales?

Sedans dominate with 48.28% of 2025 volume, reflecting the large installed base of midsize passenger cars.

Which region is growing fastest for used-car sales?

The Central region, led by Riyadh, is expanding at a 9.46% CAGR thanks to metro-driven migration and ride-hailing demand.

What impact do stricter import rules have on buyers?

New regulations have curtailed grey-market supply of luxury and sports cars, steering buyers toward certified programs and raising average transaction prices.

Are electric vehicles important in the resale market?

EV volumes remain small but are the fastest-growing fuel segment, supported by new charging infrastructure and technician training initiatives.

Page last updated on: