India Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

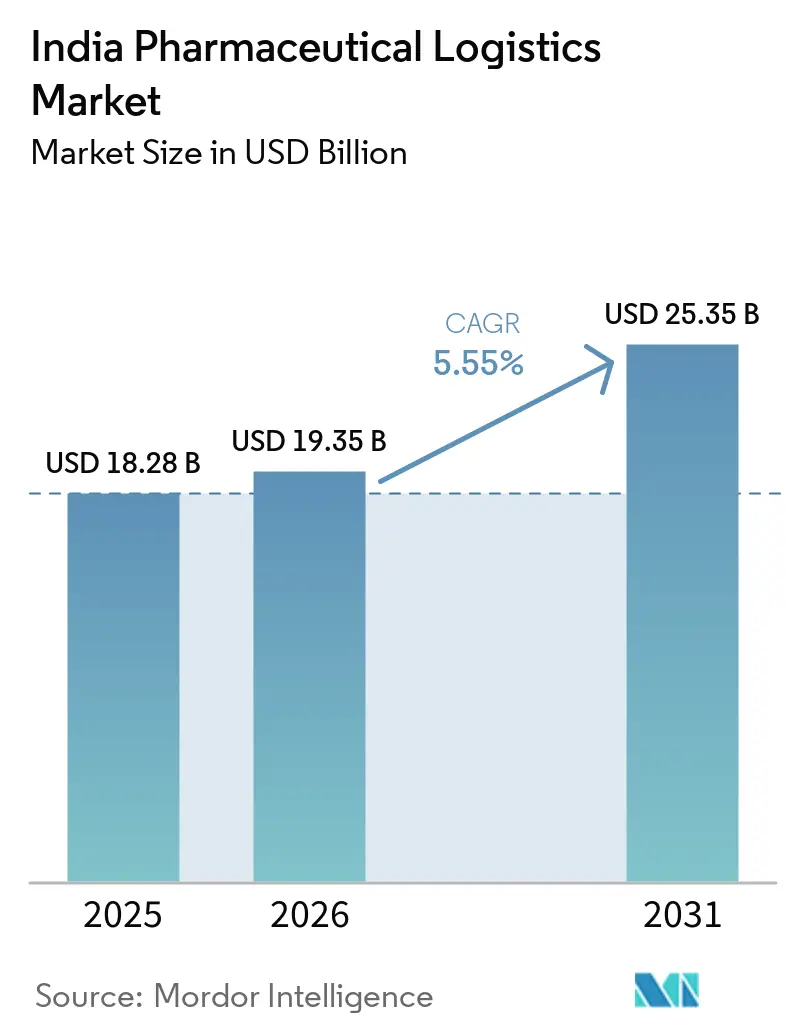

| Base Year Market Size (2025) | USD 18.28 Billion |

| Market Size (2026) | USD 19.35 Billion |

| Market Size (2031) | USD 25.35 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

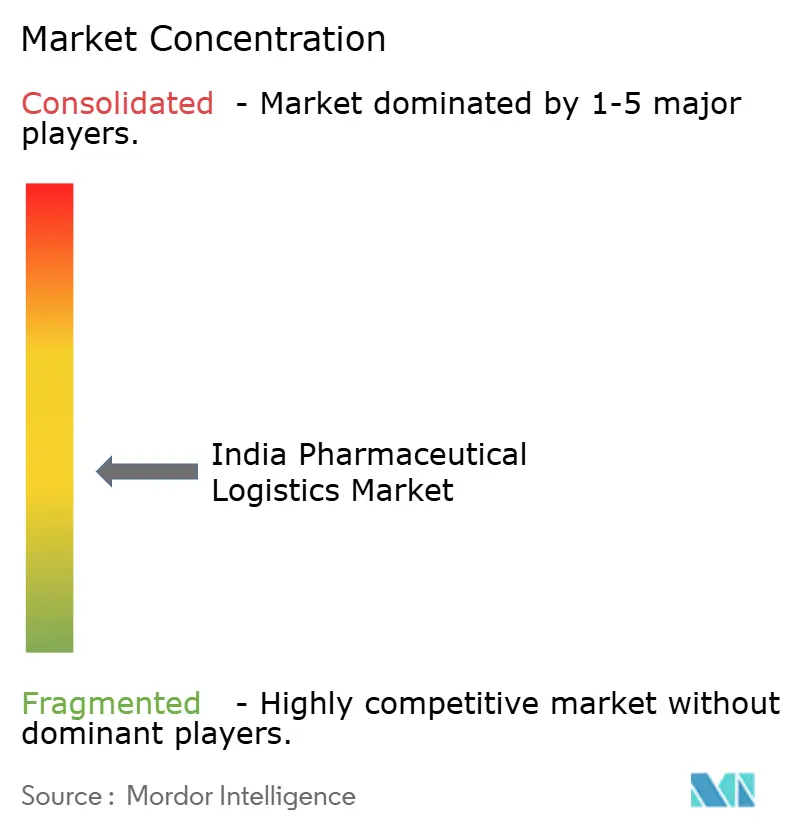

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The India pharmaceutical logistics market size is expected to increase from USD 18.28 billion in 2025 to USD 19.35 billion in 2026 and reach USD 25.35 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

India’s role as the world’s largest supplier of generic medicines, accounting for 20% of global generic drug exports by volume, continues to expand the scale and complexity of domestic and export distribution flows. Pharmaceutical exports reached USD 30.5 billion in FY2025, while the domestic pharmaceutical business stood at USD 60 billion, keeping demand active across factory dispatch, cold storage, line haul, and last-mile delivery. The market is also being reshaped by a shift toward biologics, vaccines, specialty injectables, and more tightly regulated product flows, which raises the value of temperature control, traceability, and GDP-compliant handling. Competitive pressure is rising as multinational operators expand pharma-grade assets in major hubs, while domestic specialists defend their positions through local reach, reefer capacity, and multi-temperature operations. The strongest opportunity over the forecast period lies with operators that can pair compliant cold-chain infrastructure with digital visibility, as pharma manufacturers reduce vendor counts and place more business with a smaller group of qualified partners.

Key Report Takeaways

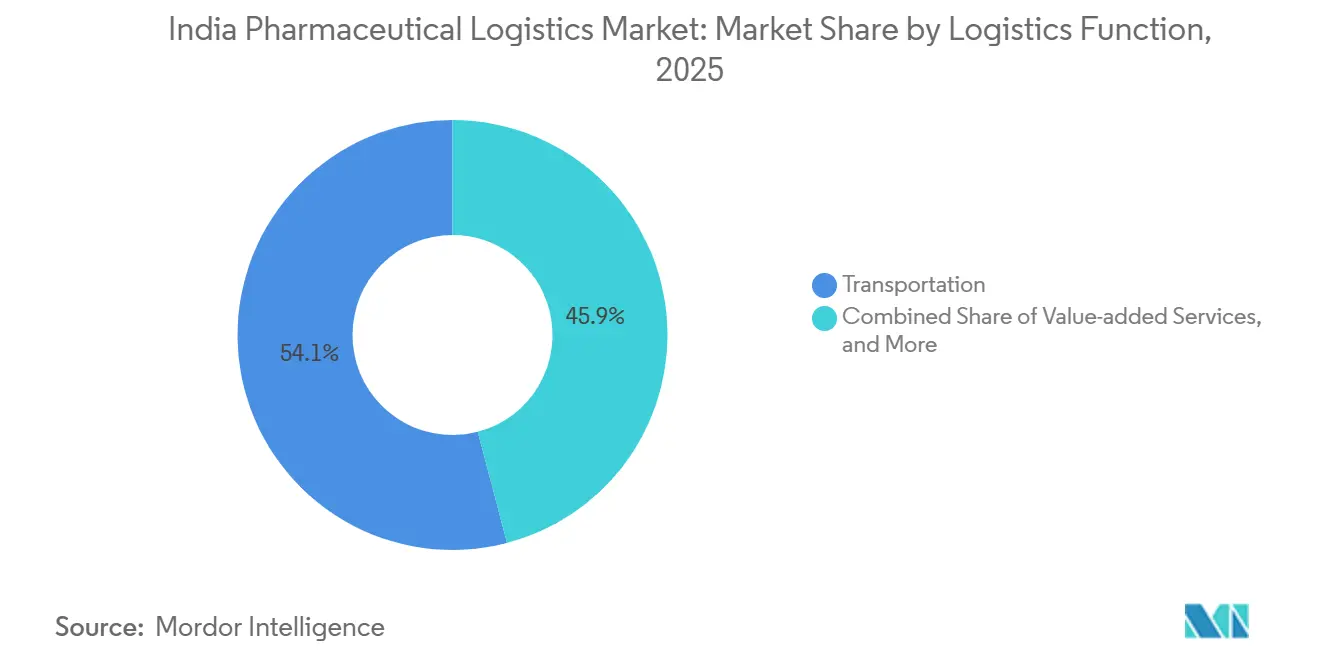

- By logistics function, transportation accounted for 54.07% of the India pharmaceutical logistics market share in 2025, while value-added services are forecast to expand at a 8.38% CAGR through 2031.

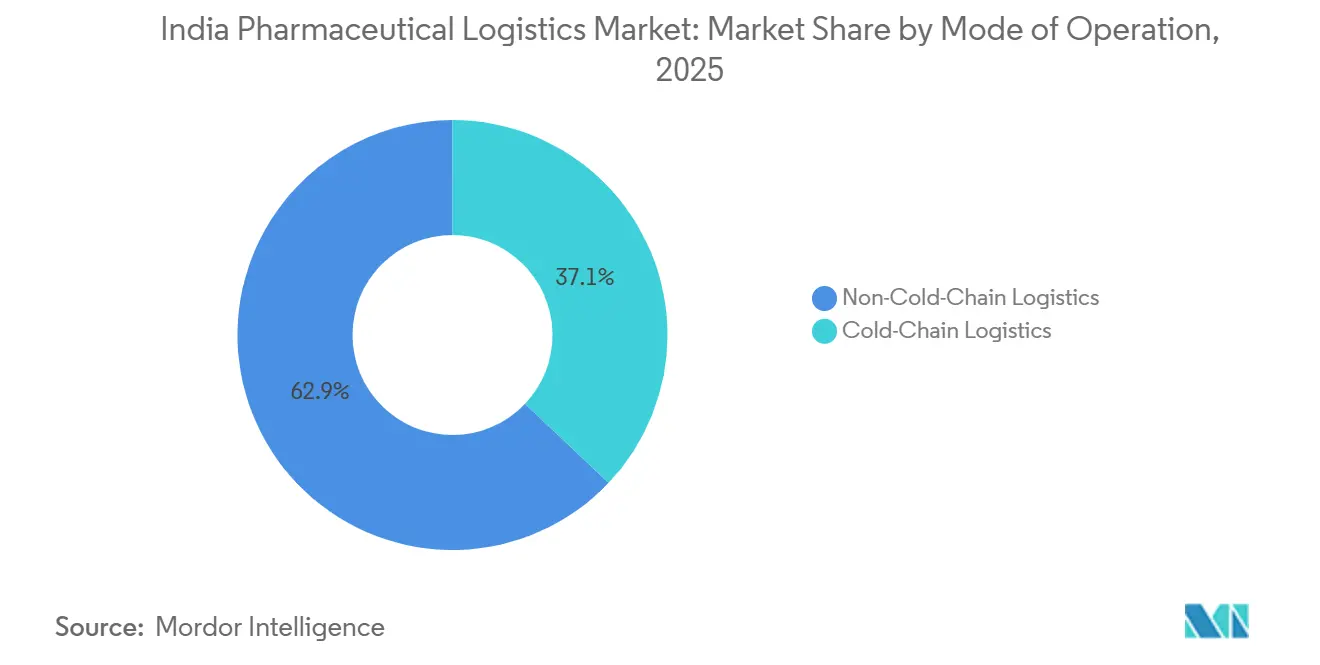

- By mode of operation, non-cold-chain logistics held 62.93% of the India pharmaceutical logistics market share in 2025, while cold-chain logistics is projected to grow at 7.55% CAGR through 2031.

- By product type, prescription drugs accounted for 46.12% of the market share in 2025, while cell and gene therapies are expected to grow at a 8.69% CAGR through 2031.

- By region, West India held 29.84% of the India pharmaceutical logistics market share in 2025, while South India is projected to grow at 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Temperature-Controlled Biologics and Vaccines | +1.5% | National, with concentration in Hyderabad, Pune, Bengaluru, and Ahmedabad pharma clusters | Short term (≤ 2 years) |

| Government Production-Linked Incentive Schemes Driving Manufacturing Scale-Up | +1.3% | National, early-stage gains in Gujarat, Telangana, Himachal Pradesh, and Andhra Pradesh | Medium term (2-4 years) |

| Growth of Domestic Pharmaceutical Manufacturing Clusters | +0.8% | Maharashtra, Gujarat, Telangana, Tamil Nadu, Andhra Pradesh | Medium term (2-4 years) |

| Expansion of E-Pharmacy and D2C Drug Distribution | +0.9% | National, with outsized gains in Tier 1 and Tier 2 metros | Short term (≤ 2 years) |

| RFID-Based Track-and-Trace Mandates by CDSCO | +0.5% | National, with early compliance gains in pharma export hubs | Medium term (2-4 years) |

| Surge in Reverse Logistics Due to Expiry-Date Compliance Mandates | +0.4% | National, spill-over to state-level distribution networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Production-Linked Incentive Schemes

India pharmaceutical logistics market demand is rising with the scale-up created by the pharmaceutical and bulk drug PLI programs. As of December 2025, cumulative investment under these schemes reached INR 41,943 crore (USD 4.66 billion), more than double the initial commitment target of INR 17,275 crore (USD 1.92 billion). Cumulative sales under both schemes reached INR 3,35,036 crore (USD 37.28 billion) across 1,988 products, including exports worth INR 2,15,248 crore (USD 23.95 billion), indicating that production-linked incentives are already driving higher logistics volumes across domestic and export channels. The more important shift is in the product mix, as the program favors biopharmaceuticals, complex generics, and autoimmune therapies that require tighter thermal and handling controls than conventional oral solids. Union Budget 2026-27 also backed the Biopharma SHAKTI initiative with INR 10,000 crore (USD 1.11 billion) over 5 years and a target of more than 1,000 accredited clinical trial sites, which points to a longer cycle of specialized transport and compliant warehousing demand[1]“India’s Pharmaceuticals in Global,” Government of India, pib.gov.in.

Rising Demand for Temperature-Controlled Biologics and Vaccines

India's pharmaceutical logistics market is being driven by a faster shift toward temperature-sensitive medicines. India supplies 60% of UNICEF's global vaccine procurement and meets 40%-70% of global demand for DPT and BCG vaccines, keeping vaccine handling capacity central to logistics planning. At the same time, the patent cliff for more than 40 major branded drugs between 2026 and 2030 is steering Indian manufacturers toward biologics, GLP-1 analogs, and specialty injectables that usually require 2 °C-8 °C control. This is putting pressure on a cold chain built primarily for bulk oral solids rather than for sensitive therapies. Kuehne+Nagel added HealthChain-certified cross-docks in Bengaluru in December 2025 and in Hyderabad in May 2026 to support API and vaccine exporters, indicating that providers are redesigning assets around this new mix.

Expansion of E-Pharmacy and D2C Drug Distribution

India pharmaceutical logistics market requirements are also changing because online fulfillment has very different operating needs from traditional wholesale distribution. Tata 1mg achieved EBITDA profitability across its established businesses in FY2026, suggesting the format is moving toward sustainable scale rather than solely customer acquisition. This raises demand for split-case picking, cold-bag last-mile delivery, serialization-linked order tracking, and tighter service windows inside cities. Quick-commerce expansion by platforms such as Blinkit and Zepto is pushing medicine delivery to sub-2-hour contracts, while pending online pharmacy rules mean future compliance demands will sit atop an already fast-growing delivery base.

RFID-Based Track-and-Trace Mandates by CDSCO

The competition in India pharmaceutical logistics market is shifting toward providers that can deliver end-to-end visibility and scan-based compliance. CDSCO’s push toward QR-based traceability is already moving manufacturers and service providers toward batch-level authentication on primary and secondary packaging, and a broader proposal covering vaccines, antimicrobials, anticancer medicines, and narcotics was published for consultation in October 2025. Once traceability rules expand, warehouse systems, sortation points, and cross-docks will need scanning capability across inbound, storage, and outbound movements. This raises the value of operators that can deliver real-time dashboards along with physical shipment handling. Providers that fail to upgrade risk losing pharmaceutical contracts, as manufacturers are pushing serialization and audit discipline throughout the supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Cold-Chain Infrastructure Beyond Metros and Tier 1 Pharmaceutical Hubs | -0.7% | Pan-India, pronounced in eastern states, central India, and rural Tier 2/3 corridors | Short term (≤ 2 years) |

| High Compliance Cost of Evolving GDP Audit Frameworks and Revised Schedule M Requirements | -0.5% | National, disproportionately impacting MSME logistics operators and smaller 3PLs | Medium term (2-4 years) |

| Scarcity of Rail-Side Pharma-Grade Warehouses and Temperature-Controlled Rail Infrastructure | -0.3% | National, particularly affecting central and eastern rail corridors | Long term (≥ 4 years) |

| Prospective Carbon Tax on Diesel Reefer Fleets Limiting Cost-Efficient Last-Mile Cold-Chain Delivery | -0.2% | National, with higher exposure in high-volume road freight corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Cold-Chain Infrastructure Beyond Metros

India pharmaceutical logistics market expansion is still limited by the uneven spread of compliant cold infrastructure. The network remains concentrated in a small group of metros and manufacturing hubs, while Tier 2, Tier 3, and rural corridors stay underserved for temperature-controlled transport and storage. More than 3,500 cold-chain operators exist in India, yet only 8%-10% meet WHO-GDP standards, leaving a large share of the network below the quality level required for sensitive pharmaceutical handling[2]“India’s Pharma Logistics Faces the Patent Cliff Head-On,” ITLN, itln.in. Blue Dart’s National Operations Head stated in 2026 that temperature-controlled transport and storage remain limited across Tier II, Tier III, and rural regions, even as biologics, insulin, and vaccines move beyond urban demand centers. Smaller regional operators often cannot absorb the cost of validation, backup power, and continuous monitoring systems, which slows network quality improvement outside the main corridors.

High Compliance Cost of Evolving GDP Audits

The India pharmaceutical logistics market formalization is also raising the cost base for operators that serve pharmaceutical customers. Schedule M implementation became fully effective in January 2026, and the related GDP discipline is pushing logistics providers toward more frequent audits, stricter SOPs, excursion management records, and qualified personnel across handling points. A 2026 study of MSME pharmaceutical firms found that more than 70% identified quality control and compliance as the biggest cost driver, and some projected infrastructure spending of over INR 20 crore (USD 2.22 million) to meet revised requirements. Those cost pressures spill into logistics contracts because compliant transport and storage now require more documentation, more trained staff, and better hardware. The burden is heavier for smaller 3PLs in secondary distribution markets, and this is likely to push more share toward larger certified operators over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Road Networks Anchor Volume, Value-Added Services Define Margin

Transportation accounted for 54.07% of the India pharmaceutical logistics market share in 2025, which confirms that road freight remains the core movement layer for domestic pharmaceutical distribution. Trucks remain essential because India’s 6.3 million km of road network supports deliveries to more than 750 districts, where direct reach matters more than modal substitution. Air freight carries lower volume but earns much higher revenue per kilogram for biologics, clinical trial materials, and urgent API shipments, especially on export lanes to the United States, Europe, and ASEAN markets. Sea and inland waterways remain limited for pharmaceutical use because long transit windows make temperature control and monitoring harder to sustain at the required standards.

Value-added services are projected to record the fastest growth at 8.38% CAGR, which shows that the India pharmaceutical logistics industry is moving beyond pure transport and storage contracts. Pharmaceutical customers are increasingly combining packaging, kitting, serialization support, reverse logistics, and documentation management inside integrated agreements. Warehousing and distribution is also becoming more active because humidity control, batch segregation, temperature mapping, and GDP-compliant SOP execution are now part of routine operations rather than optional services. Rail remains small, but the weekly Maersk-CONCOR reefer corridor from Hyderabad to Nhava Sheva launched in May 2026 shows that dedicated pharma rail routes can work where shipment density is high enough.

By Mode of Operation: Cold Chain Accelerates As Non-Cold Chain Stabilizes

Non-cold-chain logistics held 62.93% of the India pharmaceutical logistics market size in 2025 because prescription generics, OTC medicines, and many medical devices still move as ambient products. This large share reflects the volume profile of Indian pharmaceutical production, which is still anchored by oral solids, standard formulations, and broad domestic distribution. Even so, the balance is changing as vaccines, biologics and specialty therapies take a larger role in export flows[3]“Changing Dynamics of Indian Pharma Supply Chain,” IPA India, ipa-india.org. That means non-cold-chain growth is likely to remain steadier than the colder, more specialized parts of the network.

Cold-chain logistics is projected to grow at 7.55% CAGR within the India pharmaceutical logistics market through 2031, making it the fastest-expanding operating model. Snowman Logistics expanded capacity in FY2026 across Kolkata, Krishnapatnam, Kundli, and Jaipur, which shows that operators are adding footprint in both established and underserved corridors. The operating model is also changing as providers move from storage-heavy setups toward network orchestration, monitoring, and more integrated control layers. Compliance with the revised Schedule and WHO-GDP standards is becoming a key selection factor, meaning cold-chain operators are increasingly judged on audit readiness and data quality as much as on geographic reach.

By Product Type: Prescription Drug Volumes Conceal Cell and Gene Therapy’s Strategic Importance

Prescription drugs held 46.12% of the India pharmaceutical logistics market share in 2025, supported by the scale of generic formulations, injectables, and API shipments moving from major manufacturing states into nationwide distribution. This segment benefits from steady, high-frequency dispatch patterns that connect production sites in Gujarat, Himachal Pradesh, and Telangana with distributors and hospitals across the country. OTC medicines continue to add volume through consumer health demand, while biologics and biosimilars are gaining ground as Indian manufacturers increase output for domestic and regulated export markets. Clinical trial materials are also becoming increasingly relevant as India strengthens its role in later-stage trials under the Biopharma SHAKTI push.

Cell and gene therapies are expected to post the fastest growth at 8.69% CAGR in the India pharmaceutical logistics market size through 2031, even though the current base remains small. Their logistics profile is very different because transport can require ultra-low temperatures from -80 °C to -196 °C, highly validated containers, dedicated courier protocols, and chain-of-identity documentation. India’s developing CAR-T and advanced therapy activity at institutions such as Tata Memorial and AIIMS is creating early domestic demand for these services. DHL’s healthcare network expansion, which highlighted end-to-end visibility for cell and gene therapies and named India as a priority expansion market, points to higher-value logistics work emerging from this niche.

Geography Analysis

The West region remained the largest geography in 2025, with 29.84% of the India pharmaceutical logistics market share, and its lead stems from the combined strengths of Gujarat manufacturing and Maharashtra's export infrastructure. Ahmedabad, Vadodara, and Bharuch support dense manufacturing flows, while Mumbai airport and Nhava Sheva port handle a large share of regulated shipments moving to the United States and the European Union. FedEx’s upcoming automated hub at Navi Mumbai adds more support for premium air freight and time-sensitive cargo in this corridor. Western operators are also ahead on compliance investment because the region handles a higher share of export-linked pharmaceutical movement that demands stronger audit readiness.

The South region is projected to expand at 6.93% CAGR in the India pharmaceutical logistics market size through 2031, and this growth is centered on Hyderabad, Visakhapatnam, and Chennai-linked corridors. Genome Valley remains the most visible growth engine because its concentration of vaccine, biotech, and life sciences activity creates dense demand for specialized storage and export handling. Maersk and CONCOR launched a weekly reefer rail link from Hyderabad to Nhava Sheva in May 2026, providing the corridor with a scalable cold-chain route to port. Kuehne+Nagel also opened its Hyderabad temperature-controlled facility in May 2026 after the Bengaluru site in December 2025, which shows continued investment in South India origin points. Andhra Pradesh and Tamil Nadu add a different advantage because their port access and industrial land pipelines support both export routing and domestic distribution scale.

North India does not lead the India pharmaceutical logistics market by value, but it remains critical because Delhi NCR and the Baddi-Nalagarh belt supply large volumes of oral solids into national distribution channels. TCI Supply Chain’s Gurugram cold-chain facility reflects growing demand for compliant storage as biologics volumes rise in the region. The Central region remains under-served for temperature-controlled distribution and still depends heavily on road-based ambient movement. CONCOR’s December 2025 shipment from Dewas to Singapore shows that Central India can develop multimodal cold-chain links when export demand is consolidated. East India is still the smallest region, yet it is becoming more relevant as operators add facilities in Kolkata and Patna to address long-standing vaccine and insulin handling gaps.

Competitive Landscape

The India pharmaceutical logistics market remains moderately fragmented, but consolidation is becoming clearer at the higher end of compliant and temperature-controlled services. More than 3,500 operators are active nationally, and only 8%-10% are aligned with WHO Good Distribution Practice standards, which means compliant capacity is still limited relative to total market presence. Multinational groups such as DHL Group, Kuehne+Nagel, DSV, and CEVA are targeting this gap with GDP-certified infrastructure, digital control tools, and wider network coverage. Domestic specialists such as Snowman Logistics, ColdEx Logistics, Crystal Logistic Cool Chain, TCI Supply Chain Solutions, and Mahindra Logistics still hold an advantage in regional knowledge, domestic route density, and local execution.

The India pharmaceutical logistics market is increasingly separating into premium compliant networks and a large tail of smaller operators with weaker standardization. One clear strategic move came from DSV, which completed its EUR 14.3 billion (USD 15.8 billion) acquisition of DB Schenker in April 2025 and created a larger platform for healthcare freight and contract logistics in India. Another came from DHL Group, which announced a EUR 1 billion (USD 1.17 billion) India investment by 2030 and included a health logistics excellence center in Mumbai with similar centers planned for Chennai, Delhi NCR, and Hyderabad. Kuehne+Nagel has also expanded its position through new healthcare facilities in Bengaluru and Hyderabad that serve pharmaceutical and vaccine exporters under its HealthChain standard. These moves show that network breadth, compliance, and digital visibility are now more decisive than simple freight pricing in winning larger pharmaceutical accounts.

The India pharmaceutical logistics market still leaves room for domestic challengers because Tier 2 and Tier 3 distribution remains under-built and uneven in quality. Operators that can bring GDP-compliant cold rooms, reefer reach, batch traceability, and stable service economics into secondary cities are likely to gain from vendor rationalization by drug makers. Technology is also becoming basic rather than optional because real-time temperature monitoring, IoT dashboards, and scan-linked audit trails are increasingly expected in tenders. This keeps the field fragmented at the bottom, while the compliant premium layer continues to consolidate around better-capitalized providers[4]“The Resilience at Risk, Structural Vulnerabilities and Strategic Pathways in the Indian Pharmaceutical Supply Chain,” Indian Journal of Pharmaceutical Sciences, ijpsjournal.com.

India Pharmaceutical Logistics Industry Leaders

Blue Dart Express Pvt. Ltd.

FedEx

TCI Express

Mahindra Logistics, Ltd.

Snowman Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Maersk and CONCOR launched weekly reefer rail corridor from Hyderabad to Nhava Sheva. The dedicated service provides temperature-controlled rail transport for pharmaceutical exporters from Hyderabad's API and vaccine manufacturing cluster to Nhava Sheva Port, expected to reduce greenhouse gas emissions by approximately 3,000 tons annually compared with road equivalents. This represents the first commercially scalable, scheduled pharma reefer rail link in India, with implications for reducing freight costs and diversifying modes across the pharmaceutical supply chain.

- March 2026: Kuehne+Nagel opened a healthchain-certified airfreight cross-dock in Hyderabad. The 248 sqm facility operates across temperature zones of +2 °C to +8 °C and +15 °C to +25 °C and is the company's second GDP-compliant healthcare facility in India, following its Bengaluru Cool Zone. The Hyderabad site targets API and vaccine exporters and sets a GDP-compliance benchmark at the origin point for international shipments.

- March 2026: FedEx breaks ground on INR 2,500 crore (USD 278.24 million) automated air cargo hub at Navi Mumbai International Airport. The 300,000 sq ft facility, developed in partnership with Adani Airport Holdings, targets pharmaceutical and time-sensitive cargo, embedding India into FedEx's international routing for Southeast Asia, the Middle East, Europe, and the United States.

- February 2026: DHL Group expanded its dedicated pharma airfreight cold chain network with a EUR 2 billion (USD 2.35 billion) investment. The expanded global network, anchored by a Brussels-Cincinnati Boeing 777 freighter route with India among the priority expansion markets, delivers end-to-end visibility for temperature-sensitive medicines, vaccines, and cell & gene therapies. India is among eight countries prioritized for additional Airfreight Cold Chain Network routes.

India Pharmaceutical Logistics Market Report Scope

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing and Distribution | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics and Biosimilars |

| Vaccines and Blood Products |

| Clinical Trail Materials |

| Cell and Gene Therapies |

| Medical Devices and Diagnostics |

| Veterinary Medicine |

| Others |

| North |

| Central |

| West |

| East |

| South |

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing and Distribution | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics and Biosimilars | ||

| Vaccines and Blood Products | ||

| Clinical Trail Materials | ||

| Cell and Gene Therapies | ||

| Medical Devices and Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Region | North | |

| Central | ||

| West | ||

| East | ||

| South |

Key Questions Answered in the Report

What is the current size of pharmaceutical logistics in India?

The India pharmaceutical logistics market is estimated at USD 19.35 billion in 2026 and is forecast to reach USD 25.35 billion by 2031 at a 5.55% CAGR.

Which logistics function leads pharmaceutical movement across India?

Transportation was the largest function with 54.07% share in 2025, reflecting the continued dominance of road freight in nationwide pharmaceutical distribution.

Why is cold-chain demand rising faster than ambient pharmaceutical handling?

Cold-chain logistics is projected to grow at 7.55% CAGR because biologics, vaccines, biosimilars, and specialty injectables require validated temperature control and tighter compliance.

Which region offers the strongest growth outlook through 2031?

South India is expected to grow the fastest at 6.93% CAGR, supported by Hyderabad’s Genome Valley, Andhra Pradesh’s pharma build-out, and Tamil Nadu’s logistics expansion.

What is the main compliance challenge for logistics operators serving drug companies?

A large share of operators still lacks WHO-GDP alignment, and revised Schedule M requirements are increasing audit, documentation, staffing, and infrastructure costs.

Which product segment creates the highest specialized handling opportunity?

Cell and gene therapies are forecast to grow at 8.69% CAGR and require ultra-low-temperature movement, validated packaging, and chain-of-identity controls, making them a high-value service area.

Page last updated on: