Saudi Arabia Cross-Border Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

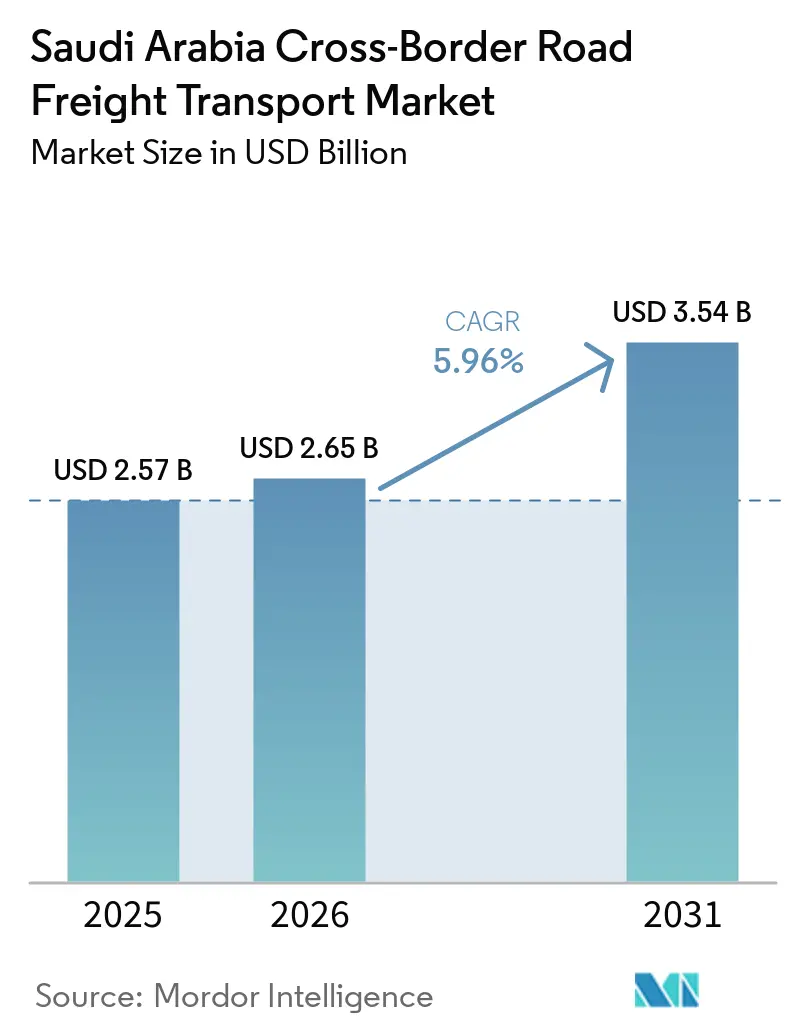

| Base Year Market Size (2025) | USD 2.57 Billion |

| Market Size (2026) | USD 2.65 Billion |

| Market Size (2031) | USD 3.54 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cross-Border Road Freight Transport Market Analysis by Mordor Intelligence

The Saudi Arabia cross-border road freight transport market size was valued at USD 2.57 billion in 2025 and is estimated to grow from USD 2.65 billion in 2026 to reach USD 3.54 billion by 2031, at a CAGR of 5.96% during the forecast period (2026-2031).

Diversification under Vision 2030, the four-laning of the Batha–Al Ghuwaifat corridor, and near-universal two-hour electronic customs clearance via the FASAH system are shrinking transit times and spurring volume gains.[1]Zakat Tax and Customs Authority, “Regulating Controls for Customs Procedures,” zatca.gov.sa Digital freight platforms, joint-venture consolidation, and multimodal rail links launched by Saudi Arabia Railways in 2026 further enhance capacity and reliability. Massive investments in highway networks, automated border ports, and specialized logistics zones are positioning the Saudi Arabia as a tri-continental transit hub, accelerating intra-GCC cargo movement.

Key Report Takeaways

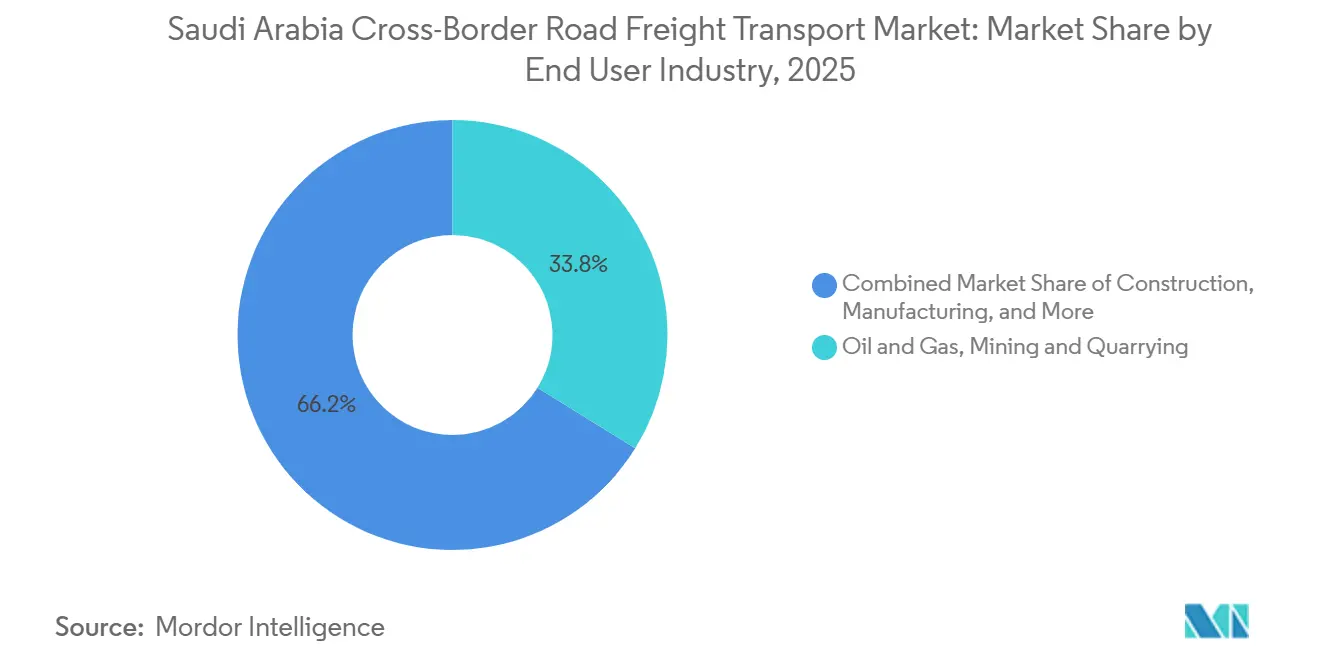

- By end-user industry, oil and gas, mining, and quarrying led with 33.83% of Saudi Arabia's cross-border road freight transport market share in 2025, while wholesale and retail trade is projected to advance at a 7.61% CAGR through 2031.

- By truckload specification, full-truck-load captured 73.11% share of the Saudi Arabia cross-border road freight transport market size in 2025, whereas LTL is forecast to grow at a 7.73% CAGR to 2031.

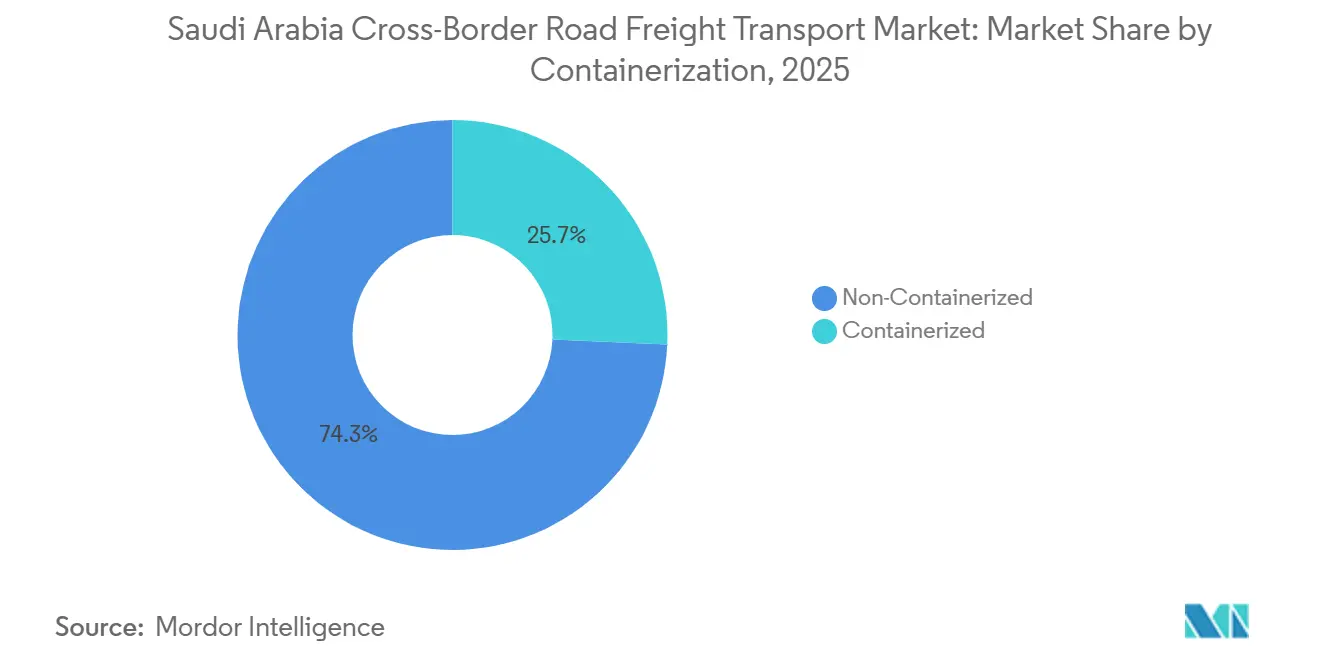

- By containerization, non-containerized cargo dominated with 74.3% of Saudi Arabia's cross-border road freight transport market share in 2025; containerized freight is the fastest-growing segment at a 7.89% CAGR over 2026-2031.

- By distance band, long-haul routes accounted for 67.72% of Saudi Arabia's cross-border road freight transport market size in 2025, while short-haul corridors are set to expand at a 6.44% CAGR through 2031.

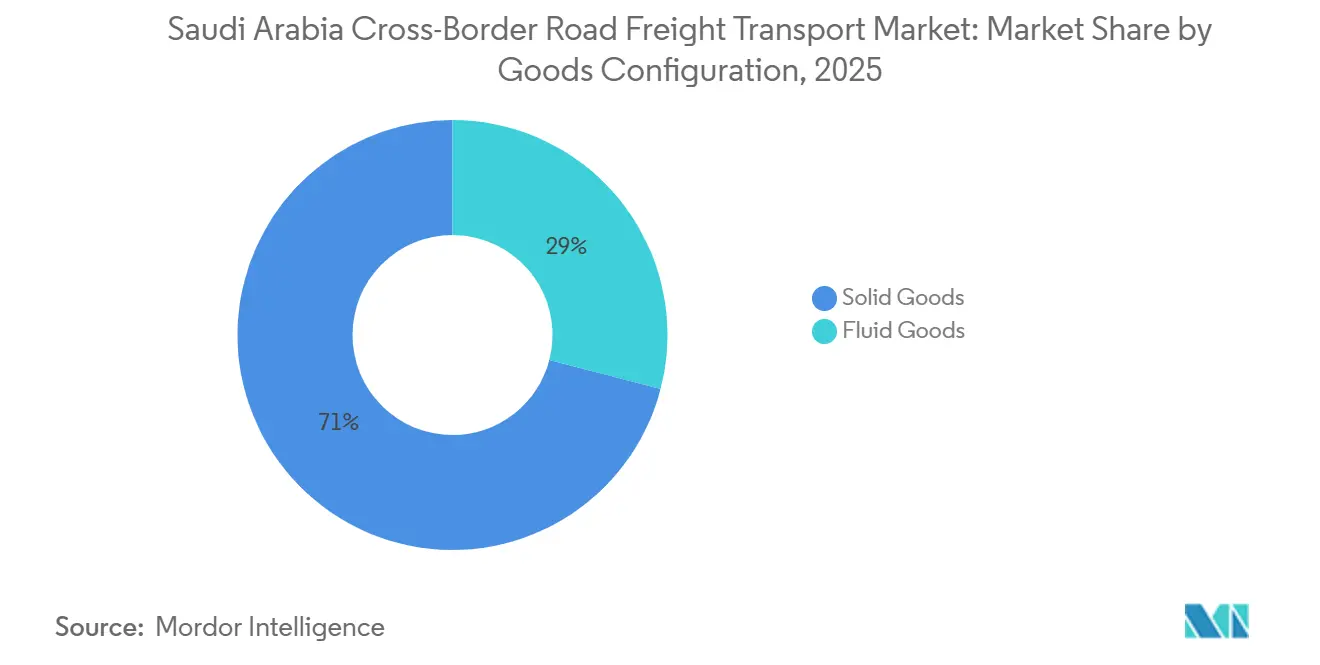

- By goods configuration, solid goods routes accounted for 70.96% of Saudi Arabia's cross-border road freight transport market size in 2025, while fluid goods is set to expand at a 6.78% CAGR through 2031.

- By temperature control, non-refrigerated held 89.07% of Saudi Arabia's cross-border road freight transport market share in 2025; yet temperature-controlled freight is advancing at a 9.57% CAGR, the steepest among all segments.

- By country, United Arab Emirates (UAE) held 47.47% of Saudi Arabia's cross-border road freight transport market share in 2025; yet Qatar is advancing at a 7.79% CAGR, the steepest among all segments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Cross-Border Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 giga-project pipeline fuels multi-year heavy-haul demand | +1.2% | National, especially NEOM (Tabuk) and Qiddiya (Riyadh) | Long term (≥ 4 years) |

| Rapid e-commerce growth elevates LTL and last-mile cross-border flows | +1.0% | National, spillover to UAE, Kuwait, Qatar, Bahrain | Medium term (2-4 years) |

| Industrial localization and SME clusters near borders | +0.8% | Eastern Province, Northern Borders, Riyadh | Medium term (2-4 years) |

| GCC customs digitalization cuts border dwell times | +0.7% | GCC-wide, early gains at Batha, Al Riggi, Jadidat Arar | Short term (≤ 2 years) |

| Saudi-UAE “twin-hub” Batha–Al Ghuwaifat corridor being four-laned | +0.5% | Eastern Province to the UAE | Medium term (2-4 years) |

| Oxagon automated logistics park creating early-adopter demand for smart cross-border trucking | +0.3% | NEOM, routes to Jordan and Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Giga-Project Pipeline Fuels Multi-Year Heavy-Haul Demand

Mega-projects such as NEOM, the Red Sea Project, and Qiddiya are generating sustained demand for oversize and overweight shipments that cannot shift to rail or container modes. Port of NEOM received its first automated cranes in June 2025, and Terminal 1 will open in 2026 with 1.5 million TEU capacity, anchoring inbound flows of steel and prefab modules. Saudi Arabia Railways added five rail-linked inland yards in April 2026, yet project cargoes still rely on specialized heavy-haul trailers for final-mile moves. Freight forwarders with hydraulic axle lines, escort services, and route-survey capability now command pricing power on Tabuk and Makkah corridors. As construction peaks through 2028, the Saudi Arabia cross-border road freight transport market should enjoy a structural freight floor set by giga-project material demand.[2]Ministry of Transport and Logistic Services, “National Transport and Logistics Strategy,” MOTLS Portal, mot.gov.sa

Rapid E-Commerce Growth Elevates LTL and Last-Mile Cross-Border Flows

Boston Consulting Group recorded a surge in Saudi online transactions during 2024-2025, with many parcels shipped overnight from UAE fulfillment hubs. Digital brokers such as TruKKer aggregate small consignments across 60,000 trucks and provide highly reliable tender acceptance, thereby shrinking empty backhaul ratios. FedEx’s nonstop Memphis-Riyadh freighter launched in September 2025 feeds a planned regional hub at King Salman International Airport, enabling air-road hybrid service within 24-48 hours to GCC addresses. Together, platform liquidity and express gateways are transforming cross-border freight from palletized bulk to box-level movements, raising demand for high-turn LTL capacity in the Saudi Arabia cross-border road freight transport market.

Industrial Localization and SME Manufacturing Clusters Near Borders

Vision 2030 incentives are luring small and medium manufacturers to zones near Dammam, Jubail, Arar, and Riyadh. The USD 1.14 billion SAL Logistics Zone north of Riyadh spans 1.5 million m² of grade-A space and opens in phases from 2025, cutting lead times for component imports. Agility’s USD 163 million Jeddah park offers six multi-tenant warehouses, 11 km from the port. These hubs allow just-in-time cross-border sourcing, boosting trucking frequency and stabilizing month-to-month load factors. As machinery and electrical parts already make up 23.2% of non-oil exports, localized assembly lines will deepen two-way flows of semi-finished goods, sustaining the Saudi Arabia cross-border road freight transport market.

GCC Customs Digitalization Cuts Border Dwell Times

Saudi Arabia’s FASAH system now clears most declarations within two hours, and Abu Dhabi Customs’ pre-arrival module enables document submission before trucks reach Al Ghuwaifat. Saudi–Kuwait connectivity was completed in June 2024, and a Saudi–Omani certificate-of-origin pact in October 2025 further streamlined paperwork. Average dwell time at Batha has fallen despite 88,000-truck peaks, improving asset turns and enabling tighter delivery windows. These efficiencies translate directly into capacity gains equivalent to hundreds of additional trucks without new vehicle purchases, lifting effective supply in the Saudi Arabia cross-border road freight transport market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortages intensified by Saudization wage rules | -0.8% | Kingdom-wide, acute in Eastern Province and Northern Borders | Short term (≤ 2 years) |

| Congestion and single-lane choke-points at key land borders | -0.4% | Batha, Jadidat Arar, Al Riggi | Short term (≤ 2 years) |

| Fragmented carrier base limits temperature-controlled reliability | -0.2% | National, notably UAE and Oman pharma lanes | Medium term (2-4 years) |

| ESG-linked cap-ex for fleet decarbonization raises operating costs | -0.1% | Major logistics hubs in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortages Intensified by Saudization Wage Rules

Transport General Authority data show 500,000 registered trucks but a tight pool of licensed Saudi heavy-goods vehicle drivers, forcing wage premiums that smaller fleets struggle to absorb. The Human Resources and Social Development Skills Framework lists commercial driving as a priority occupation, yet training enrollment trails demand. Carriers extend vehicle age limits and cross-hire expatriate drivers, but compliance audits are tightening. Until vocational pipelines scale, labor scarcity will cap near-term capacity growth in the Saudi Arabia cross-border road freight transport market.

Congestion and Single-Lane Choke-Points at Key Land Borders

Batha processed over 41,000 trucks in just 25 days during March 2026, underscoring limited buffer capacity despite pre-clearance gains. Jadidat Arar saw a 81.3% jump in truck movements in 2024, triggering QR code verification glitches that slowed flows. These bottlenecks inflate transit buffers, raise fuel burn during idling, and erode service reliability for the Saudi Arabia cross-border road freight transport market.[3]Zakat, Tax and Customs Authority, “Transit Customs Procedures and Regulations,” ZATCA Portal, zatca.gov.sa

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Wholesale and Retail Trade Gains Momentum

Oil and gas, mining and quarrying captured 33.83% of Saudi Arabia cross-border road freight transport market share in 2025, reflecting the prevalence of petrochemical exports and inbound mining equipment. Wholesale and retail trade is forecast to expand at a 7.61% CAGR to 2031, the quickest among all end users, fueled by e-commerce parcels moving overnight from UAE fulfillment centers. This structural pivot is visible in daily LTL consolidations at Batha, where consumer goods now fill return legs that once ran empty toward Riyadh. Manufacturing localization adds steady, two-way flows of machinery parts, often palletized for rapid cross-docking at Jeddah logistics parks.

The Saudi Arabia cross-border road freight transport market, attached to discretionary consumer goods, therefore broadens the customer base and reduces dependence on volatile commodity cycles. Retailers exploit electronic pre-clearance to reduce border dwell time to under 2 hours, enabling leaner inventories in Eastern Province warehouses. Petrochemical shippers, in contrast, continue to rely on full-truck-load (FTL) tankers that dominate import-export gates at Ras Al Khair, preserving baseline volumes even when consumer sentiment weakens. The coexistence of bulk energy cargoes and fast-cycling retail freight underpins year-round equipment utilization for carriers active in the Saudi Arabia cross-border road freight transport market.

By Truckload Specification: Digital Platforms Tip the Scale Toward LTL

Full-truck-load accounted for 73.11% of the Saudi Arabia cross-border road freight transport market share in 2025, anchored by petrochemicals and project cargo that require dedicated equipment. Less-than-Truck-Load volumes are projected to grow at a 7.73% CAGR through 2031 as digital brokers such as TruKKer leverage vast network liquidity across 60,000 vehicles to match capacity and reliably shrink empty-mile ratios. This aggregation on routes like the Riyadh–Dubai lane lets carriers monetize smaller lots that once moved by parcel networks. FedEx’s nonstop Memphis–Riyadh freighter injects time-critical imports that feed LTL feeders toward Kuwait and Bahrain within 48 hours.

The Saudi Arabia cross-border road freight transport market, tied to platform-driven LTL, already absorbs a widening array of electronics and apparel boxes. Carriers retrofit trailers with load bars and e-seals so mixed consignments can clear customs under a single manifest, trimming paperwork cost. Regulators encourage the shift by publishing the Logisti guide, which aligns truck categories with permissible cargo lists and streamlines market entry for small fleets. As more shippers adopt day-definite delivery promises, FTL dominance will erode gradually, though heavy industries still anchor baseline demand in the Saudi Arabia cross-border road freight transport market.

By Containerization: Standard Boxes Close the Gap

Non-containerized freight held 74.3% share in 2025, underpinned by oversize steel structures and bulk chemicals that bypass ports for direct yard deliveries. Containerized cargo is set to grow at a 7.89% CAGR between 2026 and 2031, propelled by 1.5 million TEU capacity coming online at the Port of NEOM in 2026. Railroad landbridges launched by Saudi Arabia Railways now shuttle boxes from Jeddah to Gulf states, shaving days off Suez routings. Standardized packaging enables sealed transfers across borders, reducing inspection and damage risks.

Rising container penetration is boosting the Saudi Arabia cross-border road freight transport market, as unitized loads translate into faster turnaround and more trips per tractor. Maersk’s April 2026 road–sea product from Jeddah to the UAE gains traction among electronics importers seeking Suez Canal alternatives. Logistics parks in Jeddah and Riyadh offer near-dock stuffing stations where SMEs consolidate exports into 40-foot containers, enabling access to global routes without investing in scale. As e-commerce warehouses demand carton-level traceability, container workflows provide the visibility backbone that bulk trailers lack.

By Distance Band: Short-Haul Corridors Accelerate

Long-haul routes accounted for 67.72% of Saudi Arabia cross-border road freight transport market share in 2025, dominated by Riyadh–Dubai and Dammam–Muscat trips spanning 1,000 km or more. Short-haul lanes are forecast to register a 6.44% CAGR to 2031, catalyzed by the June 2024 opening of the Al Riggi crossing with capacity for 2,000 trucks daily. Next-day delivery pledges for consumer goods fuel tighter milk-run circuits between Dammam and Manama, while petrochemical backhauls sustain reverse utilization.

The Saudi Arabia cross-border road freight transport market size for short-haul routes benefits from lower fuel costs per revenue day because tractors return to home bases nightly, aiding driver retention under Saudization rules. Transport General Authority now permits empty refrigerated Gulf trucks to enter Saudi Arabia to collect food loads, cutting deadhead mileage and boosting cold-chain density. Four-laning of Batha–Al Ghuwaifat will further compress Riyadh–Abu Dhabi transit to under six hours on light-traffic nights, shrinking order-to-delivery cycles for high-value electronics.

By Goods Configuration: Fluids Steady, Solids Diversify

Solid goods accounted for 70.96% of Saudi Arabia's cross-border road freight market share in 2025, encompassing machinery, packaged food, and building materials. Fluid cargo, chiefly chemicals and refined products, is projected to expand at a 6.78% CAGR as Jubail producers target downstream buyers in Oman and the UAE. Specialized stainless-steel tankers with GPS temperature probes fetch rate premiums and face fewer port bottlenecks than bulk vessels.

For solids, the Saudi Arabia cross-border road freight transport market size is widening beyond construction staples to include flat-packed furniture and white goods that demand gentle handling and sensor-equipped straps. Fluid haulers upgrade insulation and adopt electronic braking systems to meet stricter ADR hazardous-goods codes, elevating entry barriers for new players. The ongoing development of major mixed-use logistics complexes, such as the 80,000 m² Arcapita/Flow facility in Riyadh, which features dedicated hazardous-materials capacity, helps centralize last-mile distribution and reduces multi-stop risk for chemical shippers.

By Temperature Control: Cold Chain Scales Up Rapidly

Non-refrigerated freight controlled 89.07% of Saudi Arabia cross-border road freight transport market share in 2025, yet temperature-controlled lanes are primed for a 9.57% CAGR through 2031, the fastest among all splits. Pharmaceutical imports arriving at Dammam airport now ride GDP-certified reefers to Bahrain within six hours, leveraging empty-back permits for GCC trucks. Summer highs above 45 °C compel operators to install auxiliary chillers and solar roof panels to extend reefer runtime without engine idling.

Expanding cold capacity lifts the Saudi Arabia cross-border road freight transport market size by unlocking higher-margin lanes and boosting trailer utilization in what was once a highly seasonal niche. Consolidation moves, such as DHL’s 2025 minority stake in AJEX, integrate massive regional fleets of over 1,200 vehicles, significantly boosting network density and accelerating the rollout of temperature-capable assets across the Kingdom. Upcoming mixed-use parks in Riyadh and Jeddah promise blast-freezer chambers that let produce from Oman reach Saudi retailers within 24 hours, reducing spoilage risk and expanding product variety for consumers.

Geography Analysis

The United Arab Emirates dominated flows in 2025 with a 47.47% share of the Saudi Arabia cross-border road freight transport market, anchored by the Batha–Al Ghuwaifat corridor, which cleared over 41,000 trucks in 25 days during March 2026 after Abu Dhabi Customs activated pre-arrival filing. Four-laning work now shortens Riyadh–Dubai transit to under 14 hours on light-traffic weekends, supporting just-in-time delivery of electronics, apparel, and petrochemicals. Riyadh’s March 2026 logistics initiatives, which included extending the life of commercial trucks to 22 years, further reduced operating costs along this route. As a result, carriers schedule two round-trips per week instead of one, boosting asset productivity within the Saudi Arabia cross-border road freight transport market.

Qatar continues to leverage its reopened land gateway and is forecast to grow at a 7.79% CAGR through 2031, the fastest among country lanes, because importers now bypass sea detours when sourcing perishables and spare parts. Oman’s mutual recognition of certificates of origin with Saudi Arabia lifted Omani industrial exports to the Kingdom by 39% through July 2025 and cut inspection times at the Empty Quarter crossing. Kuwait-linked corridors, such as the Al-Raq'e post, smoothed Riyadh–Kuwait City loops to under ten hours door-to-door. Together, these shorter hauls diversify revenue and reduce reliance on long-haul routes for fleets active in the Saudi Arabia cross-border road freight transport market.

Iraq, Jordan, and Egypt represent smaller but strategic corridors. Egypt approved European truck transit across Safaga in April 2026, enabling reefers to reach NEOM via Ro-Pax ferry and continue onward to Kuwait within two days. Saudi Arabia Railways’ five new inland yards provide alternate sea-rail-road options that siphon part of the oversize flow away from congested roads. Yet the added intermodal nodes still feed last-mile trucking legs, keeping the Saudi Arabia cross-border road freight transport market expanding.[4]Transport General Authority, “Regulations Governing the Transport of Goods by Heavy Trucks,” TGA Portal, tga.gov.sa

Competitive Landscape

More than 500,000 licensed trucks operate nationwide, indicating a fragmented competitive landscape, but merger activity is quickening. DSV accelerated the integration of DB Schenker’s Saudi road assets in February 2026, combining networks and creating scale on petrochemical corridors to the UAE and Oman. DHL eCommerce's minority purchase of AJEX in August 2025 integrated a fleet of 1,200 vehicles that focus heavily on e-commerce parcel and LTL skids, illustrating the strategic push toward high-frequency consumer freight.

Digital platforms disrupt traditional brokerage. TruKKer, armed with USD 15 million in July 2025 debt funding, matches 60,000 trucks to real-time tenders and delivers highly reliable acceptance rates on the Riyadh–Dubai lanes. Wajeeh offers free software, credit lines, and port-drayage integration, which lures small fleets into an aggregated capacity pool that yields instant spot quotes. WiseTech Global and Elm aim to knit customs, telematics, and warehouse data into one Arabic interface so shippers see highly accurate predictive arrival times. These technology plays raise service benchmarks across the Saudi Arabia cross-border road freight transport market.

Investment is flowing into specialized facilities. Arcapita and Flow will build an 80,000 m² mixed-use logistics hub in Riyadh that features dedicated cold and hazardous-goods capacity, closing the GDP-certified gap that still forces pharmaceutical importers to dual-source carriers. Agility opened a USD 163 million park in Jeddah in November 2025, giving small and medium exporters grade-A bays eleven kilometers from the port. Saudi Global Ports committed USD 933 million to expand Dammam terminals, which will generate fresh drayage demand once rail-truck transload ramps are complete in 2029. As large integrators stitch together door-to-door networks and investors bankroll cold-chain real estate, smaller local hauliers face rising compliance and technology thresholds to stay active in the Saudi Arabia cross-border road freight transport market.

Saudi Arabia Cross-Border Road Freight Transport Industry Leaders

Almajdouie Logistics

Bahri Integrated Logistics

Aramex

NAQEL Express

Gulf Agency Company (GAC Saudi Arabia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Saudi Arabia Railways launched five multimodal logistics routes linking Gulf and Red Sea ports with inland yards, aiming to remove thousands of trucks from roads.

- March 2026: Riyadh introduced an integrated GCC logistics package that extends truck life to 22 years and waives 60-day storage fees at Dammam, easing carrier cost pressure.

- March 2026: Qatar activated a special digital land transit route via its Saudi border utilizing the TIR system to secure continuous goods flow amid regional transport disruptions.

- February 2026: DSV reported rapid progress on the integration of DB Schenker’s Saudi trucking operations, actively unifying networks ahead of a targeted late-2026 global completion date.

Saudi Arabia Cross-Border Road Freight Transport Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

| Containerized |

| Non-Containerized |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperature Controlled |

| Temperature Controlled |

| United Arab Emirates (UAE) |

| Kuwait |

| Qatar |

| Oman |

| Iraq |

| Rest of Countries |

| By End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| By Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| By Containerization | Containerized |

| Non-Containerized | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Country | United Arab Emirates (UAE) |

| Kuwait | |

| Qatar | |

| Oman | |

| Iraq | |

| Rest of Countries |

Key Questions Answered in the Report

What is the current size and forecast growth of Saudi Arabia cross-border road freight?

The sector was valued at USD 2.57 billion in 2025 and is projected to reach USD 3.54 billion by 2031, advancing at a 5.96% CAGR over 2026-2031.

Which end-user industry ships the most freight across Saudi borders?

Oil and gas, mining and quarrying led with 33.83% share in 2025, largely through petrochemical exports to the United Arab Emirates.

Which customer group is expanding fastest?

Wholesale and retail trade is expected to post a 7.61% CAGR through 2031 due to e-commerce that routes parcels from UAE fulfillment hubs,

What lane handles the bulk of cross-border traffic?

The Batha–Al Ghuwaifat Saudi–UAE corridor accounted for nearly half of all trucked freight in 2025 and continues to grow following capacity upgrades.

How quickly is temperature-controlled freight growing?

Cold-chain volumes are forecast to grow at a 9.57% CAGR through 2031, as pharmaceutical imports and perishables surge, outpacing all other segments.

Who are the leading logistics players in this market?

Multinationals such as DSV, CEVA Almajdouie, DHL-AJEX, and digital broker TruKKer headline the competitive field, yet, combined, they still hold under 30% of the revenue share, indicating fragmentation.

Page last updated on: