Saudi Arabia Last Mile Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

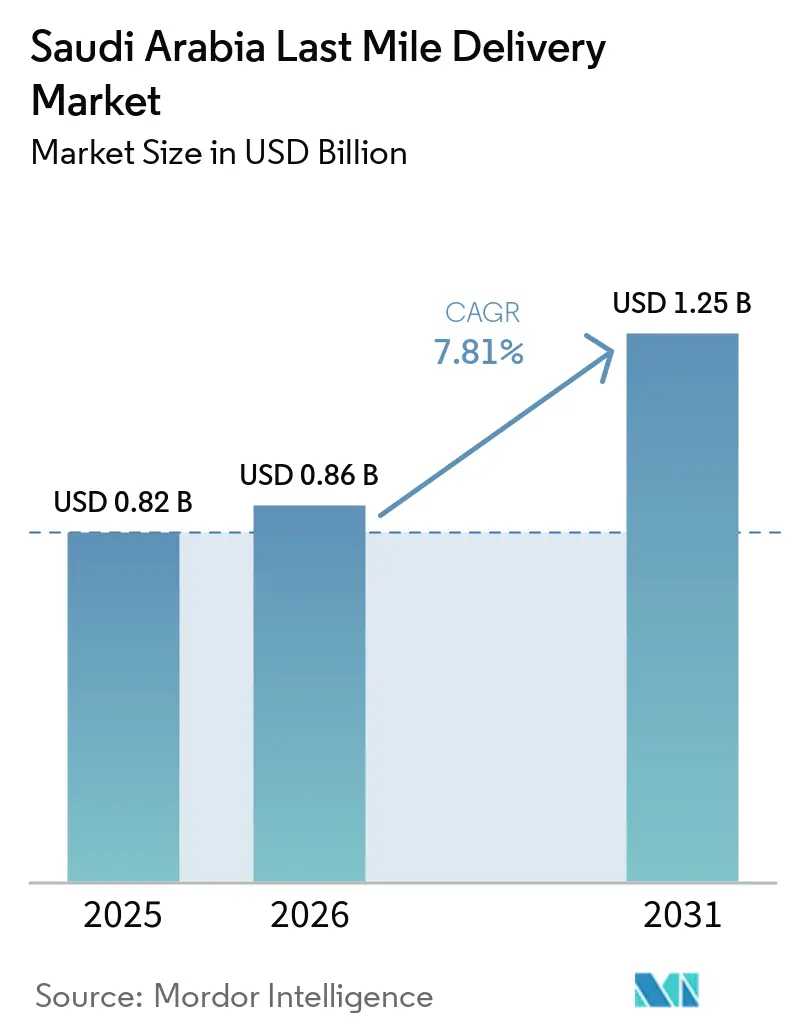

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.86 Billion |

| Market Size (2031) | USD 1.25 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

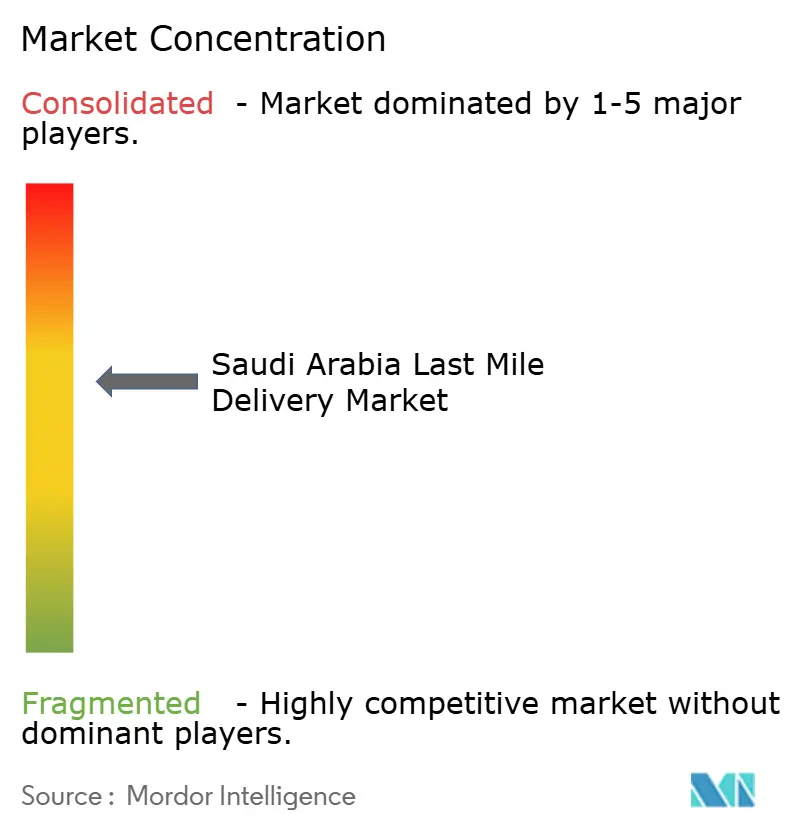

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Last Mile Delivery Market Analysis by Mordor Intelligence

The Saudi Arabia last mile delivery market size is projected to be USD 0.82 billion in 2025, USD 0.86 billion in 2026, and reach USD 1.25 billion by 2031, growing at a CAGR of 7.81% from 2026 to 2031.

The robust outlook mirrors Vision 2030’s commitment to invest SAR 280 billion (USD 74.6 billion) in transport and logistics corridors, digital customs platforms, and special economic zones. Escalating e-commerce volumes: 118 million transactions in Q1 2026, up 49% year-on-year, with daily parcel growth, with Riyadh alone generating 44% of orders. April 2024 courier-licensing reforms formalized 37 operators, channeling gig deliveries into compliant networks and raising service standards. International integrators, domestic specialists, and quick-commerce platforms now compress delivery windows through AI-enabled hubs, while unresolved address-standardization outside tier-1 cities keeps first-attempt failure rates high.

Key Report Takeaways

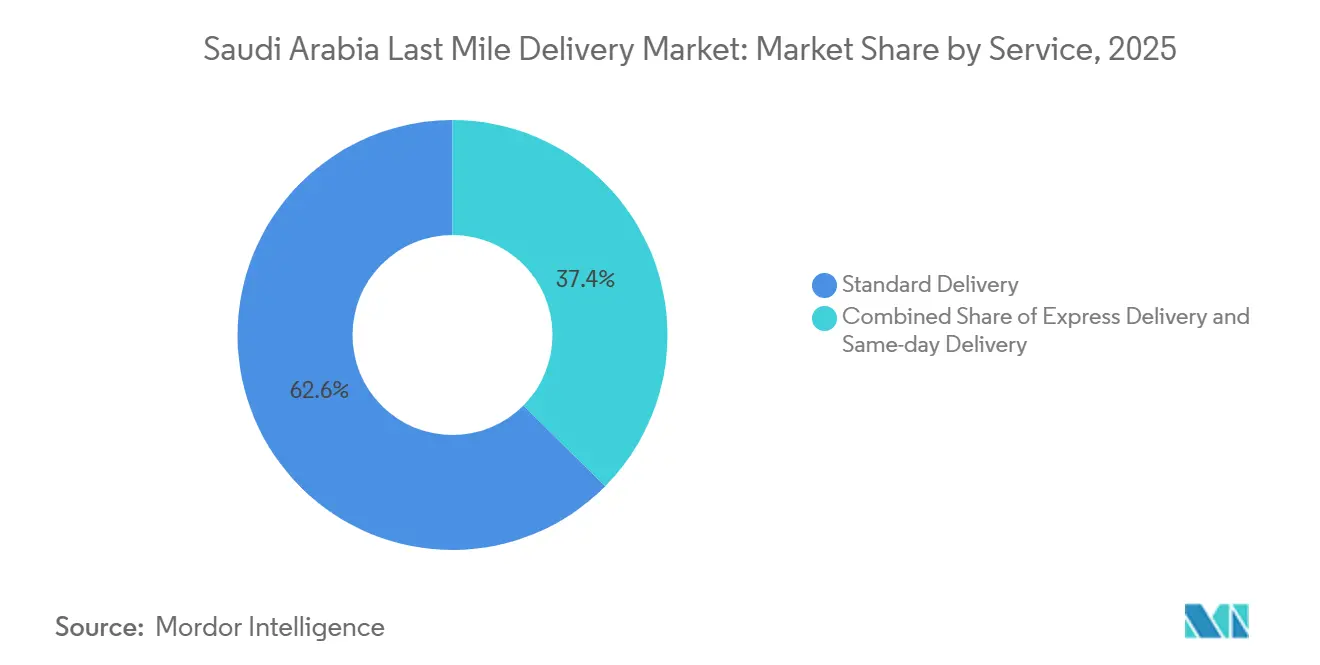

By service, standard delivery captured 62.57% of the Saudi Arabia last-mile delivery market share in 2025, whereas same-day delivery is projected to expand at a 9.46% CAGR through 2031.

By business model, B2C flows commanded 71.6% of the Saudi Arabia last-mile delivery market size in 2025, while C2C logistics records the fastest 9.58% CAGR on the back of recommerce platforms.

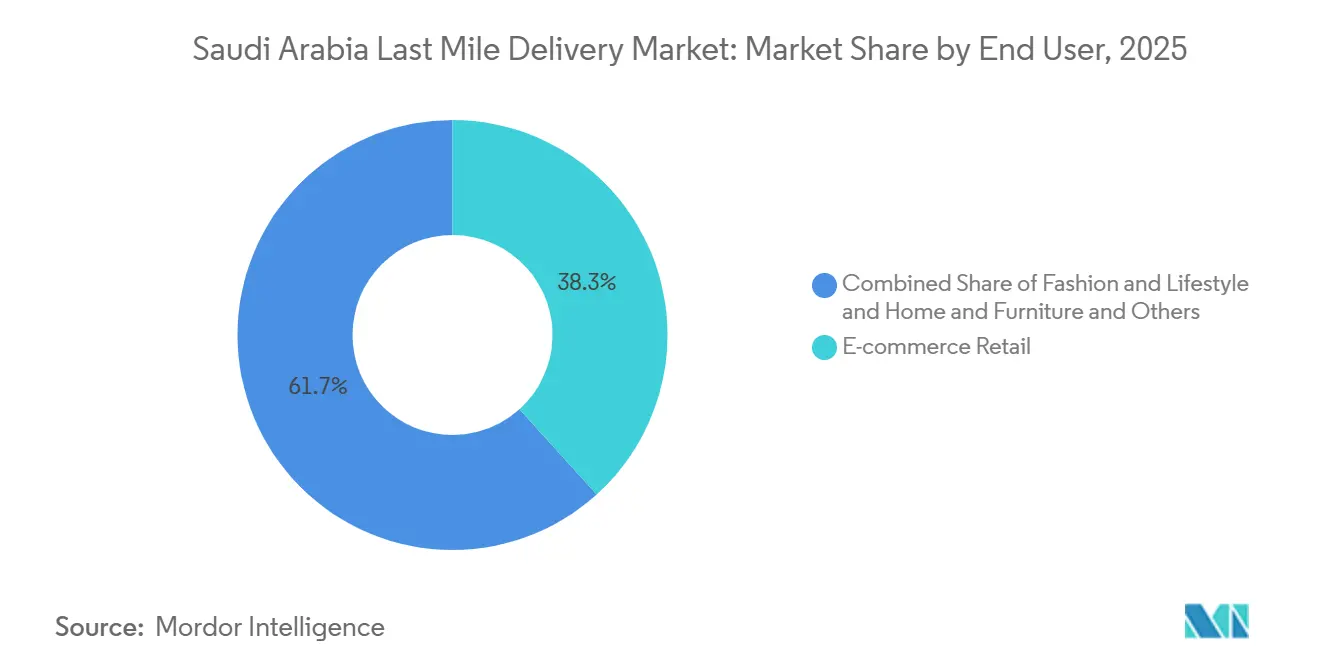

By end user industry, e-commerce retail led with 38.25% revenue share of the Saudi Arabia last-mile delivery market size in 2025, healthcare and medical supplies are advancing at a 9.74% CAGR to 2031.

By region, the Central region accounted for 45.76% of deliveries in 2025, while the Western corridor is the fastest-growing geography, with an 8.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid E-Commerce Penetration Post-COVID | +2.1% | National, with concentration in Riyadh (44%), Makkah (22%), Eastern Province (16%) | Short term (≤ 2 years) |

| Vision-2030 Logistics Infrastructure Push | +1.8% | National, with priority in SILZ zones (Riyadh, Jeddah, Dammam) and the Haramain corridor | Long term (≥ 4 years) |

| Rising Consumer Demand for Same/Next-Day Delivery | +1.5% | Central and Western regions, expanding to Eastern Province | Medium term (2-4 years) |

| Omni-Channel Expansion by Large Retailers | +0.9% | Tier-1 cities (Riyadh, Jeddah, Dammam, Khobar), gradual tier-2 rollout | Medium term (2-4 years) |

| Female Workforce Growth Lifting Daytime Parcel Density | +0.7% | Urban centers with Vision 2030 employment programs (Riyadh, Jeddah, Eastern Province) | Medium term (2-4 years) |

| AI-Driven Route Optimization Increasing Capacity and Margins | +0.6% | National, led by tech-enabled carriers in Central and Western regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid E-Commerce Penetration Post-COVID

E-commerce orders climbed 49% year-on-year to 118 million in Q1 2026, sustaining the single biggest demand shock to the Saudi Arabia last-mile delivery market. Digital payments now account for 79% of transactions, and 96% of point-of-sale interactions are contactless, eliminating the historical friction of cash-on-delivery[1]Saudi Central Bank, “Payment Systems Report 2025,” sama.gov.sa. Riyadh’s dominance generates dense routes but forces carriers to install neighborhood-level micro-fulfillment to meet same-day promises. Quick-commerce alliances such as Noon Minutes within the Jahez app are pushing the expectation of 15- to 30-minute drop-offs into smaller cities. As mobile-first shoppers expand outside tier-1 zones, e-commerce becomes the default retail entry point for SMEs in fashion, electronics, and grocery.

Vision-2030 Logistics Infrastructure Push

Government spending of SAR 280 billion (USD 74.6 billion) targets 18 special integrated logistics zones with 50-year tax holidays and 100% foreign ownership to attract multinationals. DHL broke ground on a EUR 130 million (USD 152.6 million), 78,000 m² hub in Riyadh in 2026, cementing the capital’s gateway status. Customs digitalization via Fasah now clears compliant imports inside 24 hours, slicing 3-5 days off cross-border lead times. Air cargo throughput rose 34% in 2025 as FedEx added six nonstop flights into King Salman International Airport. While hard assets mature over the long term, immediate throughput gains already elevate the Saudi Arabia last-mile delivery market.

Rising Consumer Demand for Same/Next-Day Delivery

Same-day services will grow at a 9.46% CAGR, redefining cost structures inside the Saudi Arabia last-mile delivery market. SMSA Express operates 150-plus micro-hubs within 5 km of dense clusters, and Aramex’s robotic sorter in Jeddah processes 4,000 parcels per hour[2]SMSA Express, “Corporate Overview 2025,” smsa.com. Amazon and Al Othaim launched two-hour grocery delivery in 2025 using AI inventory tools. Yet last-mile expenses still exceed 50% of total logistics cost, and heat over 45 °C makes refrigerated fleets mandatory in summer, inflating capex by 15-20%. Route-optimization systems that lift stops to 80-plus per round are now essential to preserve margins.

Omni-Channel Expansion by Large Retailers

Brick-and-mortar chains convert stores into forward nodes, turning physical inventory into same-day delivery assets that shrink reliance on suburban mega-centers. Carrefour’s Riyadh site can pack 5,000 orders daily and has 150 refrigerated trucks in rotation. Sharaf DG guarantees 30-minute click-and-collect or waives the fee, raising the bar for electronics service. Locker specialist RedBox installed 1,800 smart units, cutting failed deliveries by 15%. These models favor retailers with dense footprints, putting pure-play e-commerce on the defensive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Delivery Cost in Low-Density Areas | -0.8% | Northern (Al-Jouf, Arar) and Southern (Asir, Jazan, Najran) regions | Long term (≥ 4 years) |

| Labor and Visa Constraints on Gig Couriers | -0.6% | National, acute in cities with high expatriate courier populations | Medium term (2-4 years) |

| Ramadan and Hajj Volume Spikes Strain Capacity | -0.5% | Western region (Makkah, Medina), spillover to Jeddah logistics hubs | Short term (≤ 2 years) |

| Poor Address Standardization Outside Tier-1 Cities | -0.4% | Tier-2 and tier-3 cities, rural areas across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Delivery Cost in Low-Density Areas

Al-Jouf, Arar, Asir, Jazan, and Najran account for fewer than 10% of national e-commerce orders, forcing carriers onto 200-km spokes with single-digit stops. Climate-controlled vans add 15-20% to capex, and surcharge bands of SAR 10-20 (USD 5.33) per parcel further depress demand. With SILZ incentives clustered in Riyadh, Jeddah, and Dammam, rural gaps persist until public-service obligations or multi-operator asset sharing emerge.

Labor and Visa Constraints on Gig Couriers

The April 2024 decree ended non-Saudi self-employment, pushing drivers into 37 licensed firms and adding uniform plus biometric costs of SAR 500-800 (USD 133.33-213.33) per head. Unified wage contracts and stiff penalties lift compliance overhead just as seasonal peaks surge. Autonomous trials of Aramex drones for banking in 2026 remain pre-commercial while regulators tackle beyond-visual-line-of-sight safety[3]Ministry of Human Resources & Social Development, “Labor Law Amendments 2025,” hrsd.gov.sa .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Same-Day Delivery Redefines Premium Tiers

Standard delivery retained 62.57% of the Saudi Arabia last-mile delivery market share in 2025. Same-day, however, will outpace all categories with its 9.46% CAGR, moving the Saudi Arabia last-mile delivery market size toward high-velocity fulfillment zones clustered inside 5 km rings of demand. In dense Riyadh boroughs, carriers now design networks on 1-hour promise maps rather than postal codes. Aramex’s 4,000-parcel-per-hour sorter and 120 autonomous robots exemplify the capex incumbents wield, shutting smaller rivals out of urban premium lanes.

Express delivery holds a vital mid-speed niche for cross-border volumes, as customs delays render same-day delivery unfeasible. Yet route planners integrate express runs into same-day nets where density allows, blending premium SKUs with standard loads to amortize cost. JD Logistics’ JoyExpress and RedBox locker pick-ups illustrate hybrid tactics that push the Saudi Arabia last-mile delivery market share of premium services higher without wholesale network rebuilds. Standard delivery will remain dominant for palletized B2B and rural deliveries, but its share will shrink steadily as consumers internalize immediate-delivery norms.

By Business Model: Recommerce Fuels C2C Momentum

B2C flows accounted for 71.6% of the Saudi Arabia last-mile delivery market size in 2025, anchored by fashion, grocery, and electronics majors. C2C, however, is projected to grow at a CAGR 9.58% by 2031 as Haraj’s 50 million visitors list 50,000 items daily. Sellers with no packaging expertise or address accuracy strain pickup algorithms, yet escrow payments and same-day doorstep collection reduce friction and lure volume from informal handoffs. Mstaml’s Tap Payments rollout across 15 markets and uRecycle’s AI resale pilot attest to rising VC confidence.

B2B still underpins industrial supply chains, but its share declines as consumer parcels proliferate. Ostool, LMC Logistics, and Loadly specialize in palletized freight, pharmaceuticals, and spare parts, often sharing line-haul legs with parcel carriers to sweat assets. Operators that blend C2C pickups into retail return loops unlock incremental stops, a tactic becoming table stakes as the Saudi Arabia last-mile delivery market tilts toward individualized shipping.

By End User Industry: Cold-Chain Healthcare Accelerates

E-commerce retail led the Saudi Arabia last-mile delivery market with a 38.25% share in 2025. Yet, healthcare will post the fastest CAGR of 9.74% thanks to the Saudi Food and Drug Authority's Good Distribution Practice mandates. NAQEL’s 14 GDP-compliant offices and Four Winds’ 10,000 m² cold warehouse anchor a nascent network ready for biologics. Oncology drugs, vaccines, and insulin are shipped under 2-8 °C protocols that require real-time temperature telemetry[4]Saudi Food and Drug Authority, “Annual Report 2025,” sfda.gov.sa .

Fashion retains large baskets but faces 20-30% returns, ballooning reverse logistics. Beauty and personal-care SKUs require ambient conditions of 18-25 °C, with Quiqup offering 2-hour cold-chain cosmetic drops. Furniture calls for white-glove assembly, while electronics layer warranty installations services that few gig fleets can provide at scale. Healthcare’s structural rise aligns with Vision 2030’s plan to localize biopharma, permanently expanding cold-chain share in the Saudi Arabia last-mile delivery market.

Geography Analysis

The Central region accounts for 45.76% of parcels in 2025, housing the largest fulfillment clusters and DHL’s under-construction 78,000 m² regional hub, due in 2027. Suburban sprawl forces couriers to deploy micro-hubs that cut dwell times yet raise facility rent.

The Western corridor of Makkah, Medina, Jeddah, Tabuk, and Al-Bahah will expand at an 8.29% CAGR to 2031, the fastest nationwide. Hajj 2026 fielded 3.1 million seats and 12,000 flights, compressing six weeks’ throughput into 24-hour operations. Haramain High-Speed Railway carried 1.7 million passengers during Ramadan 1447, boosting the density of station-adjacent locker and courier services. Masar Makkah’s SAR 50 billion (USD 13.33 billion) retail zone will add 2,500 outlets with built-in logistics corridors.

The Northern and Southern regions remain underpenetrated, accounting for less than 10% of the national e-commerce volume. Sparse populations, long hauls, and heat spikes inflate costs, preserving standard-delivery dominance. Until SILZ incentives or universal-service subsidies extend beyond tier-1 cities, geographic disparity will persist within the Saudi Arabia last-mile delivery market.

Competitive Landscape

Roughly 37 licensed courier firms and 100 light-transport operators handle more than 200 million annual deliveries, rendering the Saudi Arabia last-mile delivery market moderately fragmented. FedEx, DHL, UPS, and Aramex chase premium express lanes, while SMSA, Saudi Post, and Zajil lean on Arabic customer care and government contracts. Quick-commerce players Jahez, Mrsool, and Talabat operate captive fleets, bypassing traditional carriers but grappling with drag on asset utilization.

Technology adoption is emerging as the primary differentiator in this evolving landscape. Logistics platforms like Receipts and Omniful are enabling operators to reduce operational costs by up to 40% through route optimization, real-time tracking, and warehouse automation, giving digitally mature players a clear margin advantage. Strategic investments are also signaling a shift toward consolidation and scale-building, exemplified by DHL’s EUR 500 million (USD 587.9 million) minority stake in AJEX to strengthen domestic coverage.

Despite increasing competition, significant white spaces remain, particularly in reverse logistics, rural last-mile connectivity, and SFDA-compliant cold chain delivery, where early entrants can establish strong footholds before the market transitions toward consolidation and higher entry barriers.

Saudi Arabia Last Mile Delivery Industry Leaders

Saudi Post (SPL)

Aramex

SMSA Express

DHL Express

Fedex Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: DHL International announced a SAR 150 million (USD 40 million) investment to expand its electric vehicle fleet for last-mile deliveries across Saudi Arabia.

- October 2025: Jahez and Noon integrated grocery quick-commerce with 50,000 restaurants across 100+ cities.

- October 2025: Amazon and Al Othaim launched same-day fresh-food delivery in Riyadh and Jeddah with AI stock tools.

- September 2025: FedEx began six weekly nonstop US flights into King Salman International Airport, shaving 1-2 days off transit.

Saudi Arabia Last Mile Delivery Market Report Scope

| Same-day Delivery |

| Express Delivery |

| Standard Delivery |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

| Central (Riyadh, Al-Qassim, and Hail) |

| Eastern (Ash-Sharqiyah) |

| Western (Al-Bahah, Makkah, Medina, and Tabuk) |

| Northern (Al-Jouf and Arar) |

| Southern (Asir, Jazan, and Najran) |

| By Service | Same-day Delivery |

| Express Delivery | |

| Standard Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End User Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By Region | Central (Riyadh, Al-Qassim, and Hail) |

| Eastern (Ash-Sharqiyah) | |

| Western (Al-Bahah, Makkah, Medina, and Tabuk) | |

| Northern (Al-Jouf and Arar) | |

| Southern (Asir, Jazan, and Najran) |

Key Questions Answered in the Report

What is the current Saudi Arabia last mile delivery market size and projected CAGR to 2031?

The market stood at USD 0.82 billion in 2025 and is forecast to reach USD 1.25 billion by 2031, advancing at a 7.81% CAGR

Which delivery tier is expanding the fastest in Saudi Arabia?

Same-day services lead growth at a 9.46% CAGR through 2031 as consumers demand sub-24-hour fulfillment.

How large is Riyadh’s share of national e-commerce shipments?

The capital generates about 44% of all online orders, creating the country’s densest parcel routes.

What 2024 regulation reshaped courier gig work?

The Transport General Authority banned non-Saudi self-employment for delivery drivers, requiring them to join one of 37 licensed firms within 14 months.

Why are healthcare and medical supplies deliveries accelerating?

Saudi Food and Drug Authority GDP rules and investment in cold-chain hubs are pushing healthcare parcels to a 9.74% CAGR through 2031.

Which technology most improves delivery margins?

AI route-optimization platforms that lift stops per route to 80-plus and cut fuel use by roughly 35% are now the key cost lever for carriers.

Page last updated on: