Saudi Arabia Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

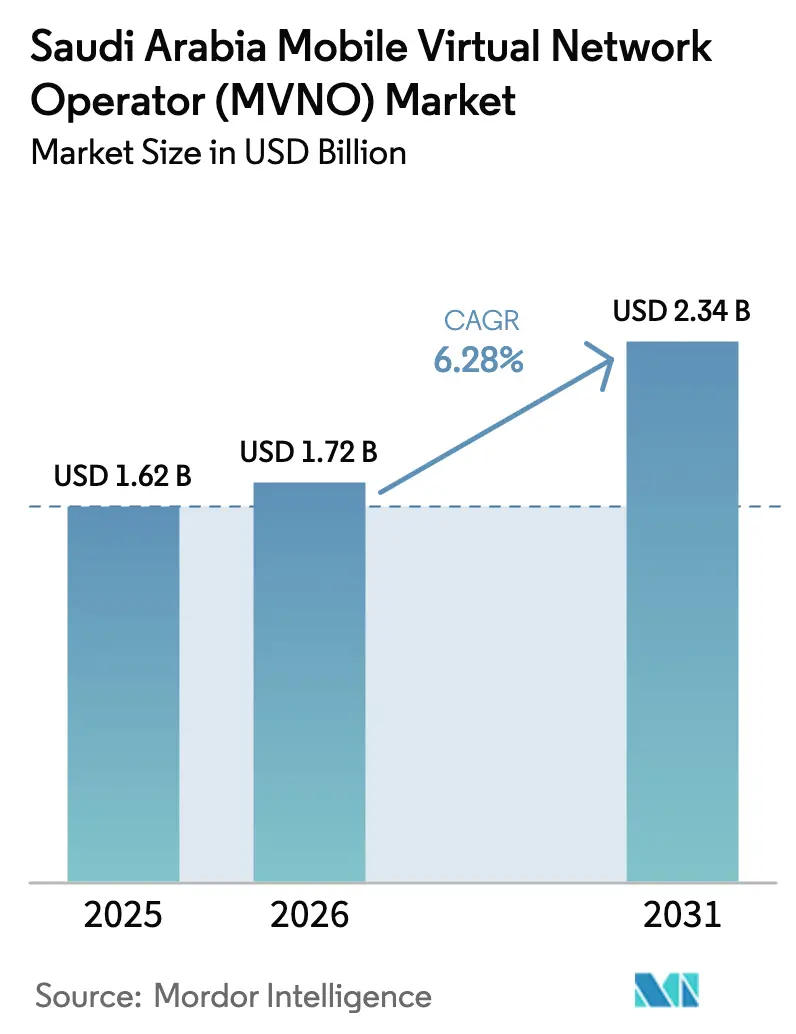

| Base Year Market Size (2025) | USD 1.62 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

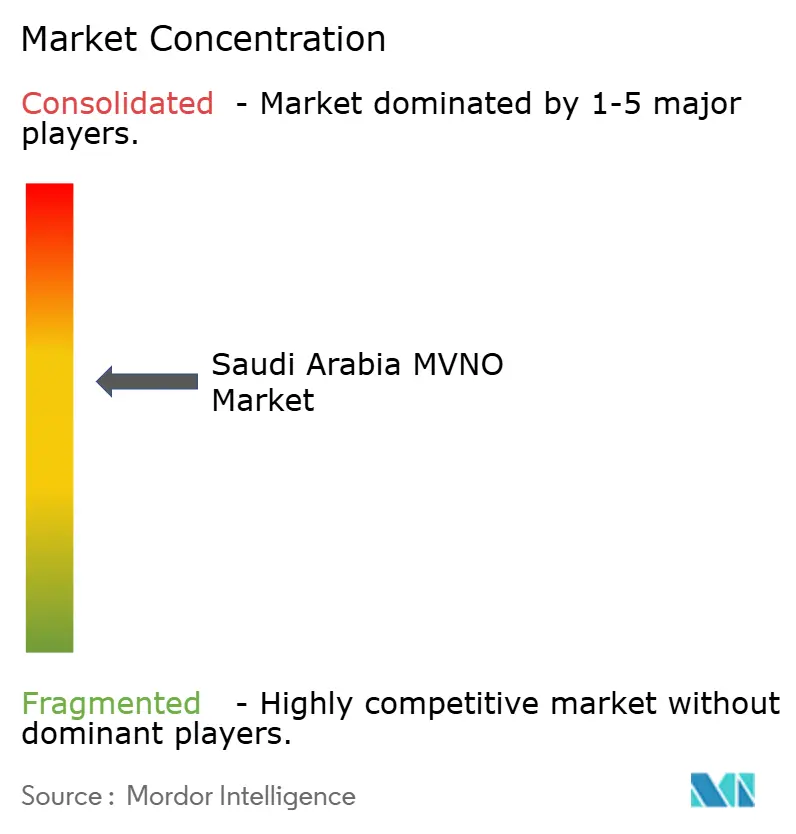

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

Saudi Arabia MVNO Market size in 2026 is estimated at USD 1.72 billion, growing from 2025 value of USD 1.62 billion with 2031 projections showing USD 2.34 billion, growing at 6.28% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 3.17 million subscribers in 2025 to 4.25 million subscribers by 2030, at a CAGR of 6.08% during the forecast period (2025-2030). Consolidated 5G coverage that now exceeds 87% of major cities, government‐mandated digital-inclusion targets under Vision 2030, and a wholesale‐friendly regulatory framework have converged to create sustained demand for virtual operators that address niche consumer, enterprise, and IoT connectivity needs. Incumbent mobile network operators (MNOs) have responded by opening wholesale portals and signing multi-year hosting deals that monetize dormant capacity while enriching the Saudi Arabia MVNO market with differentiated brand propositions. Cloud-native business support systems are lowering capex barriers, enabling rapid launch cycles, and intensifying service innovation, while eSIM provisioning and digital identity integration are shortening customer onboarding to minutes. At the same time, satellite/non-terrestrial network (NTN) breakthroughs are extending coverage beyond terrestrial limits, positioning the Saudi Arabia MVNO market to serve remote industries and disaster-recovery applications.

Key Report Takeaways

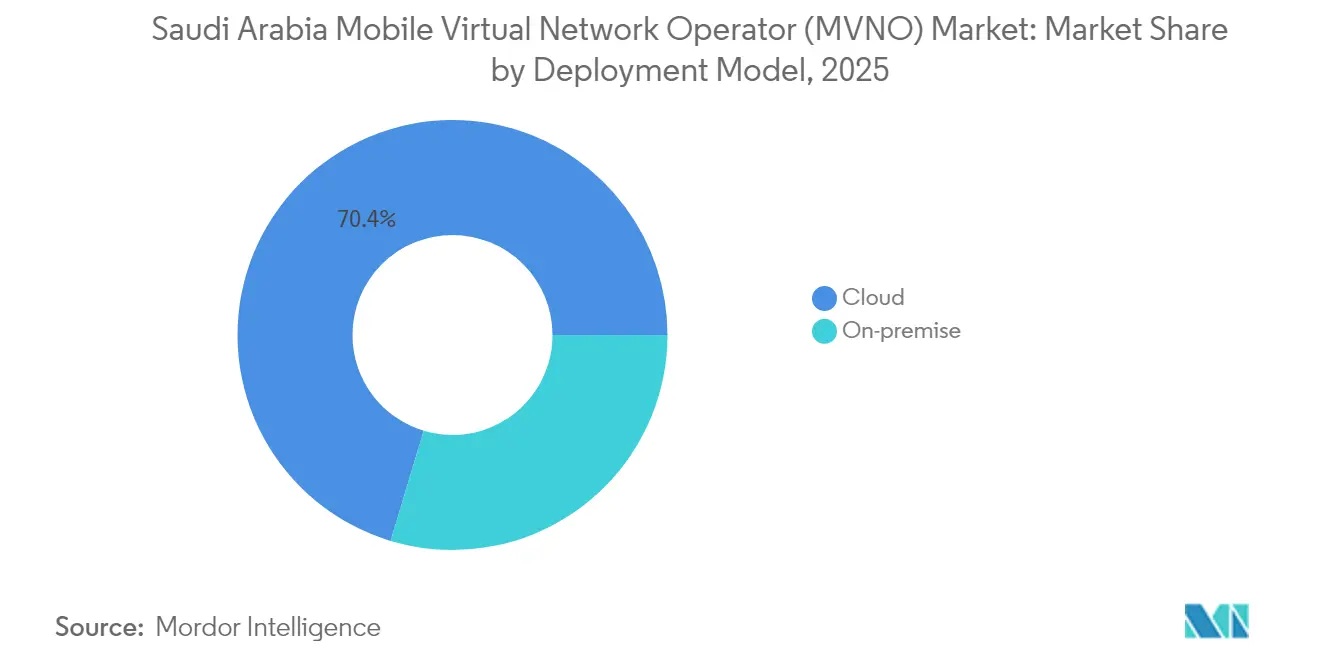

- By deployment model, cloud solutions held 70.35% of Saudi Arabia MVNO market share in 2025 and are growing at an 11.24% CAGR through 2031.

- By operational mode, full MVNOs are projected to expand at a 24.10% CAGR to 2031, while the consumer resellers/light/brand MVNO retained 53.10% of the Saudi Arabia MVNO market share in 2025.

- By subscriber type, IoT-specific services are rising at a 25.80% CAGR, while the consumer segment retained 82.05% of Saudi Arabia MVNO market share in 2025.

- By application, other application segments held 41.30% of the Saudi Arabia MVNO market share in 2025, while cellular M2M accounted for 20.95% CAGR growth potential between 2026-2031, eclipsing the broader applications category.

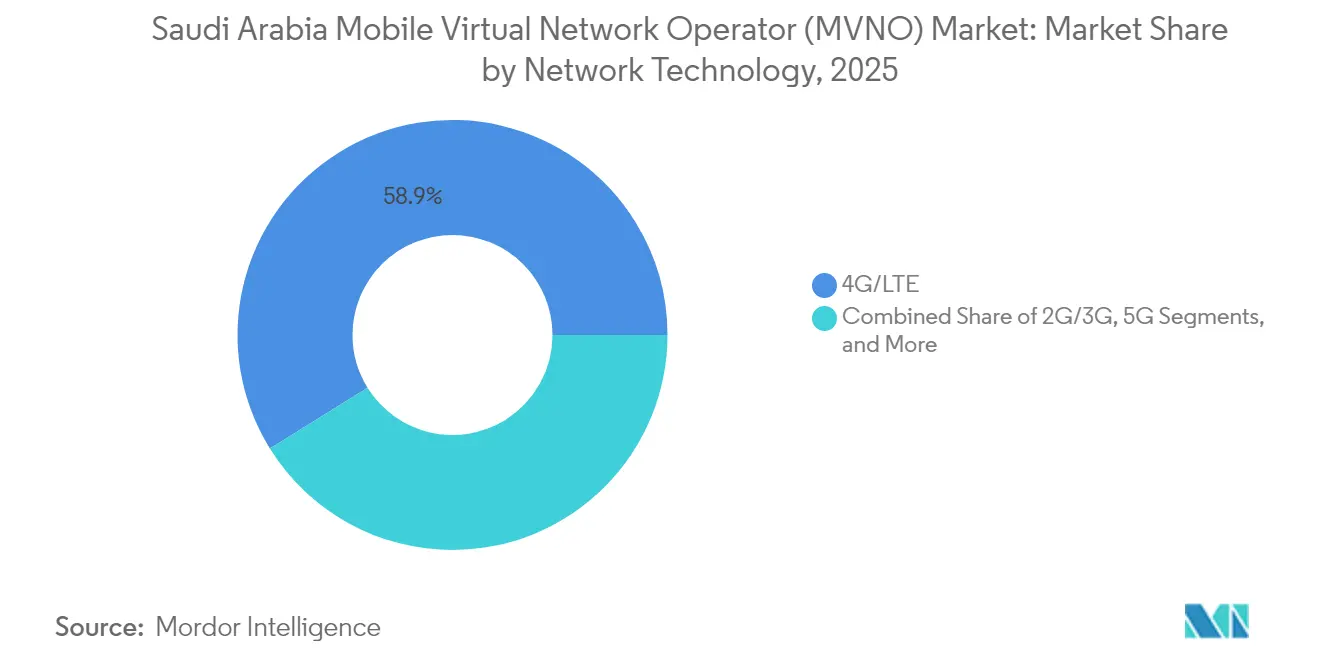

- By network technology, 4G/LTE segments held 58.85% of the Saudi Arabia MVNO market share in 2025, while satellite/NTN services are forecast to surge at a 96.40% CAGR through 2031, driven by new-generation LEO initiatives.

- By distribution channel, online/digital-only channel held 57.60% of Saudi Arabia MVNO market share in 2025 and is growing at a 9.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-5G wholesale spectrum availability | +1.8% | National | Medium term (2-4 years) |

| Vision 2030 digital-inclusion mandates | +1.5% | Major metros | Long term (≥ 4 years) |

| Growing price-sensitive youth segment | +1.2% | Urban centers | Short term (≤ 2 years) |

| eSIM-enabled digital onboarding | +0.9% | National | Medium term (2-4 years) |

| Pilgrimage-season capacity off-loading via sub-brand MVNOs | +0.7% | Makkah, Madinah | Short term (≤ 2 years) |

| IoT manufacturers seeking Saudi eUICCs under data-localization law | +1.1% | National and GCC spill-over | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-5G Wholesale Spectrum Availability Accelerates MVNO Deployment

Three nationwide 5G networks now deliver average download speeds of 261.5 Mbps, freeing ample wholesale capacity at cost-oriented tariffs enforced by regulators [1]stc KSA, “mywholesale portal,” stc.com.sa. Self-service wholesale portals automate contracting and usage monitoring, enabling small MVNO entrants to scale without bespoke negotiations. The regulated requirement for non-discriminatory access protects service quality while letting MNOs monetize underused spectrum, creating a virtuous cycle for the Saudi Arabia MVNO market. Competitive hosting deals, such as Mobily’s six-year Red Bull Mobile agreement, demonstrate how incumbents convert excess capacity into stable wholesale revenue. With further spectrum releases slated for 2026, price pressure is expected to persist, reinforcing MVNO cost competitiveness.

Vision 2030 Digital-Inclusion Mandates Drive Enterprise MVNO Opportunities

Government programs have already generated SAR 180 billion in ICT market value, opening new enterprise connectivity niches [2]Communications, Space & Technology Commission, “Communications, Space & Technology Commission,” CST.gov.sa . Mega-city projects such as NEOM and New Murabba demand sector-specific service-level agreements that generic retail plans cannot meet. Dedicated MVNO licences allow tailored private networks for utilities, public safety, and smart-mobility services. Host MNOs benefit by wholesaling specialized network slices rather than investing in vertical-specific capex themselves. The policy preference for Saudi ownership further motivates local MVNO ventures, ensuring compliance with Saudization quotas while anchoring high-skilled jobs inside the Kingdom.

Price-Sensitive Youth Segment Fuels Digital-First MVNO Models

Individuals below 35 constitute 67% of the population, and credit-card penetration remains below 30%, establishing fertile ground for prepaid, app-centric propositions [3]HSBC, “Silicon Kingdom: Saudi's digital leap opens doors for global business,” business.hsbc.com. Virgin Mobile has built a 3.5 million-strong subscriber base by bundling music streaming and gaming credits into data packages that never expire. In-app Direct Carrier Billing, launched with TIMWETECH, allows micro-transactions for premium content without bank cards, aligning perfectly with youth spending patterns. Social-influencer marketing further reduces acquisition costs, enabling aggressive pricing that still preserves margins because of low digital-only overheads. This demographic reality will keep digital-first MVNOs at the forefront of Saudi Arabia MVNO market growth.

eSIM-Enabled Digital Onboarding Reduces Operational Complexity

GSMA-compliant eSIM provisioning now comes baked into host-operator wholesale catalogs, eliminating physical SIM logistics and shrinking activation time from days to minutes. Zain’s Yaqoot lets customers authenticate via the national digital ID app and download profiles instantly, driving near-zero-touch fulfillment. For IoT MVNOs, remote profile swaps facilitate lifecycle management across thousands of devices without truck rolls, directly enhancing profitability. Lower friction accelerates customer acquisition and churn-free switching, positioning eSIM as a structural catalyst for the Saudi Arabia MVNO market. As Apple and Samsung extend eSIM-only handset portfolios, physical SIM demand will decline sharply, embedding digital onboarding as the new norm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wholesale access tariffs | -1.4% | National | Medium term (2-4 years) |

| Incumbent MNO dominance limits differentiation | -0.8% | Rural zones | Long term (≥ 4 years) |

| Lag in portable IIN allocation for IoT SIMs | -0.6% | National | Medium term (2-4 years) |

| Saudization quotas raise OPEX for lean MVNOs | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Wholesale Access Tariffs Constrain MVNO Margin Structures

Spectrum auction costs and rapid 5G rollout have driven MNO capex higher, pushing wholesale rates upward despite cost-orientation rules. With just three wholesale suppliers, MVNOs have limited leverage in contract negotiations, and arbitration mechanisms remain slow. Premium data bundles for youth or migrant workers, therefore, require razor-thin retail pricing, compressing margins. New entrants often offset the cost hurdle through aggressive digital customer acquisition and value-added services, yet sustained profitability hinges on deeper regulatory scrutiny of wholesale charge structures. Unless tariff transparency improves, smaller MVNOs may struggle to remain solvent beyond initial funding rounds.

Incumbent MNO Dominance Limits Service Differentiation Opportunities

STC, Mobily, and Zain collectively control nationwide coverage, multi-access edge compute, and fintech ecosystems, leaving little white space for generic voice-and-data resellers. Their own sub-brands, Jawwy and Yaqoot, already target digital natives, squeezing lifestyle MVNO propositions. In IoT, host operators bundle connectivity with device management, cybersecurity, and cloud, raising the innovation bar for stand-alone virtual players. Outside mega-cities, rural coverage maps depend exclusively on incumbent footprints, curbing MVNO geographic expansion. To survive, challengers must specialize in vertical solutions such as logistics telematics, satellite backhaul, or religious tourism capacity offload, niches that require both regulatory savvy and technical depth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Operational Agility

Cloud-based enablement platforms accounted for 70.35% of Saudi Arabia MVNO market share in 2025, and this slice is advancing at an 11.24% CAGR, markedly ahead of on-premise models. The cost avoidance of data centers, signaling nodes, and billing stacks allows start-ups to launch nationwide service for a fraction of legacy capex, directly reshaping the Saudi Arabia MVNO market economics. Host MNO APIs expose policy control, network slicing, and subscriber management functions, letting cloud MVNOs roll out new plans in hours rather than quarters.

On-premise deployments persist where data-sovereignty laws or ultra-low-latency use cases prevail, especially in defense, utilities, and critical national infrastructure. For these customers, the Saudi Arabia MVNO market size at the on-prem layer benefits from government procurement cycles tied to Vision 2030 megaprojects. Yet even within restricted environments, private clouds and virtualization are replacing bare-metal stacks, blurring the line between true cloud and traditional infrastructures. Over the forecast horizon, hybrid models are expected to dominate as enterprises demand public-cloud agility behind sovereign firewalls.

By Operational Mode: Full MVNOs Emerge Despite Infrastructure Complexity

Reseller and brand MVNOs held a 53.10% share in 2025 because they require minimal technical assets, but full MVNOs are projected to post a 24.10% CAGR, the fastest within the Saudi Arabia MVNO market. Growing subscriber bases eventually justify investments in core-network elements that grant control over roaming, policy, and user data, unlocking higher margins and bespoke service logic.

Service-operator models bridge the gap by operating their own OSS/BSS while leasing radio access, delivering moderate differentiation without heavy capex. For lifestyle brands such as Red Bull Mobile, the light model remains optimal because marketing, not network quality, drives customer value. However, industrial IoT providers favor full control to meet stringent service-level agreements. The evolutionary path thus mirrors market maturation: successful resellers reinvest profits to graduate into service operators and, ultimately, full MVNOs.

By Subscriber Type: IoT-Specific Services Drive Exponential Growth

The consumer base still represented 82.05% of 2025 connections, yet IoT-specific services are scaling at a 25.80% CAGR as Saudi Railways, Aramco, and smart-city programs demand machine connectivity. Saudi Arabia MVNO market size for enterprise and IoT will therefore expand at twice the overall pace by 2031.

Enterprise MVNOs exploit IoT device management, edge analytics, and secure private APNs to differentiate from consumer-centric brands. Global equipment vendors comply with data-localization law by embedding Saudi eUICCs, channeled through MVNO partners that offer regulatory shelter. As government procurement mandates grow stricter on local content, domestically owned IoT MVNOs gain preference in tenders, reinforcing the pivot toward industrial connectivity.

By Application: Cellular M2M Applications Accelerate Industrial Transformation

The other application segment remained the largest revenue bucket at 41.30% in 2025, combining content, tourism, and expatriate plans. Yet Cellular M2M outperforms with a 20.95% CAGR because factories, ports, and utilities integrate millions of sensors for predictive maintenance. Saudi Arabia MVNO market size for M2M will therefore widen its footprint across oil pipelines, autonomous mining vehicles, and renewable-energy farms.

Discount and business-application sub-segments continue to attract migrant workers and SMEs, but ARPU lags compared to mission-critical M2M connections with ten-year lifespans. MVNOs that master ruggedized SIMs, over-the-air firmware updates, and zero-touch provisioning will capture a disproportionate share of this high-growth pocket.

By Network Technology: Satellite/NTN Services Achieve Breakthrough Growth

4G/LTE still dominated at 58.85% in 2025, but Satellite/NTN services are tearing ahead with a 96.40% CAGR to 2031, the highest in the Saudi Arabia MVNO market. Direct-to-device trials proved smartphones can latch onto LEO satellites for text and low-rate data, removing coverage gaps across the Empty Quarter desert and the Red Sea corridor.

5G macro and small-cell rollouts continue to densify urban cores, supporting AR/VR, autonomous transport, and massive IoT. Legacy 2G/3G sunsets will re-farm spectrum toward 5G NR-Light and NB-IoT, gradually phasing out low-bandwidth applications. For aviation, maritime, and emergency services, NTN MVNOs promise ubiquitous reach without costly terrestrial towers.

By Distribution Channel: Digital-Only Channels Dominate Market Evolution

Online and app-based activations secured 57.60% of 2025 sign-ups and climbed at a 9.88% CAGR, the highest among distribution avenues. Saudi Arabia MVNO market share shifts toward self-service because 97% of adults own smartphones, and in-app identity verification eliminates SIM forms.

Physical retail persists for handset bundling and expatriate corridors but faces erosion as eSIM eliminates the need for plastic. Carrier sub-brand outlets serve dual roles as experience centers and last-mile distribution, especially during Hajj and Umrah when temporary prepaid demand spikes. Third-party wholesalers extend reach into convenience stores and logistics depots, yet their relevance will diminish as digital inclusion spreads to rural provinces.

Geography Analysis

Riyadh’s central region captured the lion’s share of gross additions in 2024, buoyed by multi-billion-dollar government ICT contracts and smart-city pilots . Jeddah-Makkah-Madinah in the west is the fastest-growing corridor, as religious tourism drives seasonal capacity and Red Sea giga-projects demand seamless roaming. The Eastern Province leverages proximity to hydrocarbon complexes and industrial ports to anchor IoT MVNO adoption, especially for real-time logistics and safety monitoring.

Northern and southern hinterlands traditionally lagged, but new rail fiber backbones and subsidies for rural coverage are enticing MVNOs to pilot community Wi-Fi and satellite backhaul solutions. Cross-border spill-over into GCC states further widens addressable volumes as eUICC-compliant SIMs allow single-SKU regional deployments. Overall, urban density remains the primary revenue driver, yet Vision 2030 infrastructure rollouts will progressively equalize digital access across provinces.

Competitive Landscape

The Saudi Arabia MVNO industry is semi-consolidated: three host MNOs support a dozen active MVNO brands while launching their own digital sub-labels. Jawwy and Yaqoot exemplify internal cannibalization strategies that let operators segment markets without ARPU dilution. Virgin Mobile amplifies youth appeal through endless validity data coins, whereas Red Bull Mobile fuses lifestyle branding with adventure sports perks.

IoT Squared and other enterprise specialists are rising on the back of government procurement that insists on local ownership and cybersecurity compliance. Satellite-enabled aspirants such as SKYFive Arabia threaten to bypass terrestrial wholesale altogether, inserting new dynamics into host-MVNO bargaining. Strategic moves center on platform partnerships, TIMWETECH for billing, MATRIXX for real-time charging, and MAVOCO for device management, highlighting how software ecosystems now dictate competitive advantage more than radio spectrum.

M&A chatter remains muted because national ownership caps restrain foreign buy-outs, but wholesale joint ventures flourish as incumbent operators monetize towers, dark fiber, and edge nodes. Over the next five years, sustained value migration toward enterprise and NTN niches will reward MVNOs that master regulatory complexity, security certification, and multi-access orchestration.

Saudi Arabia Mobile Virtual Network Operator (MVNO) Industry Leaders

Virgin Mobile Saudi Arabia LLC

Lebara Mobile KSA

Jawwy by STC (Etihad Jawraa Mobile Services Company)

Yaqoot (Zain KSA sub-brand)

Salam Mobile (Integrated Telecom Mobile Company (ITC Mobile))

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Beyond ONE partnered with TIMWETECH to deploy Direct Carrier Billing across Virgin Mobile Saudi Arabia and FRiENDi Oman, enabling 3.5 million subscribers to purchase premium content with mobile wallets.

- February 2025: The Communications, Space and Technology Commission issued INR 1 billion equivalent in new spectrum and carrier licenses at LEAP25, including NTN rights for SKYFive Arabia.

- January 2025: Saudi Telecom Company won a USD 8.7 billion government infrastructure contract, significantly boosting wholesale backhaul capacity for MVNO partners.

- November 2024: Viasat completed the Kingdom’s first 3GPP Rel-17 direct-to-device satellite messaging test, validating NTN feasibility for commercial MVNO offerings.

Saudi Arabia Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller / Light / Brand MVNO |

| Service Operator |

| Full MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller / Light / Brand MVNO |

| Service Operator | |

| Full MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

How large is the Saudi Arabia MVNO market in 2026?

It is valued at USD 1.72 billion and is set to grow at a 6.28% CAGR during 2026-2031.

Which segment grows fastest in Saudi MVNO services?

Satellite/NTN services register the highest 96.40% CAGR through 2031, driven by new-generation LEO initiatives.

Why are cloud deployment models dominant?

Cloud platforms cut capex, accelerate launch cycles, and already account for 70.35% of 2025 deployments.

What drives interest in satellite/NTN MVNOs?

Direct-to-device trials and LEO investments produce a 96.40% CAGR outlook for satellite-enabled services.

Where is geographic growth most rapid?

The Jeddah-Makkah-Madinah corridor leads, supported by pilgrimage traffic and Red Sea developments.

Page last updated on: