Kenya Mobile Virtual Network Operator (MVNO) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

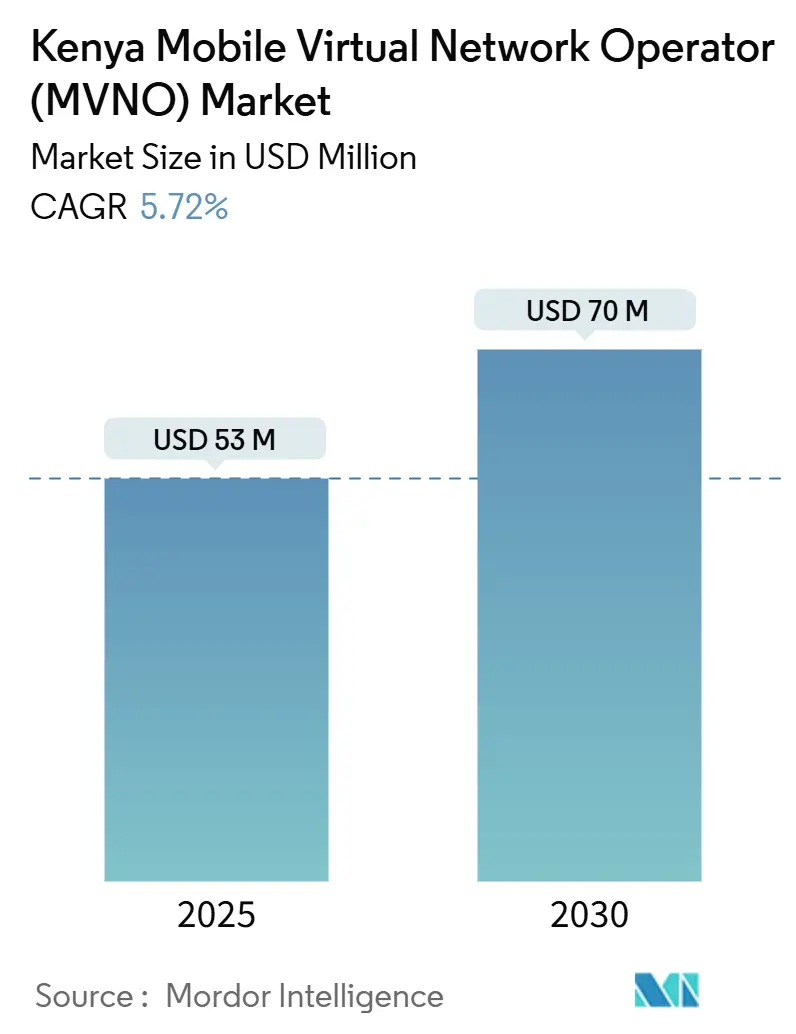

| Market Size (2025) | USD 53 Million |

| Market Size (2030) | USD 70 Million |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

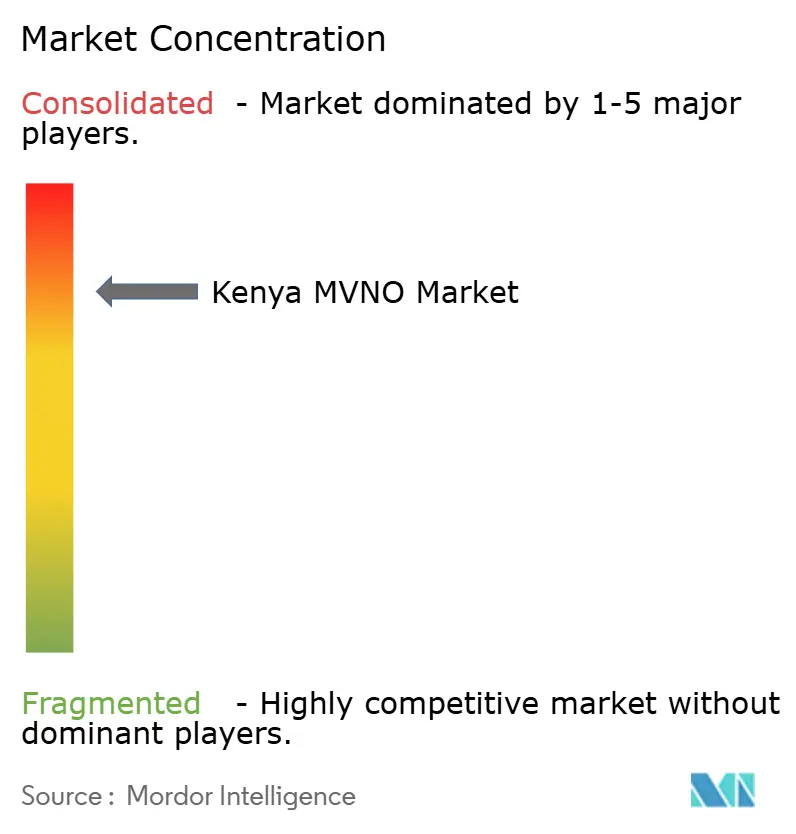

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Mobile Virtual Network Operator (MVNO) Market Analysis by Mordor Intelligence

The Kenya Mobile Virtual Network Operator Market size is estimated at USD 53 million in 2025, and is expected to reach USD 70 million by 2030, at a CAGR of 5.72% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 0.94 million subscribers in 2025 to 1.26 million subscribers by 2030, at a CAGR of 6.06% during the forecast period (2025-2030).

Sustained growth reflects rising mobile subscriptions, a sharp 29% cut in voice and SMS termination charges, and rapid 4G-to-5G coverage gains that reduce wholesale barriers for virtual operators. Aggressive spectrum refarming, device affordability, and mobile-money interoperability further propel the Kenya MVNO market by opening fintech-telecom cross-selling opportunities, especially in urban corridors. Competitive differentiation hinges on cloud-native deployments, discount pricing strategies, and emerging IoT-centric service bundles that target agriculture, logistics, and smart-city projects. At the same time, Safaricom’s 65.9% subscriber dominance and lingering wholesale quality-of-service gaps on alternative host networks act as structural checks on MVNO expansion.

Key Report Takeaways

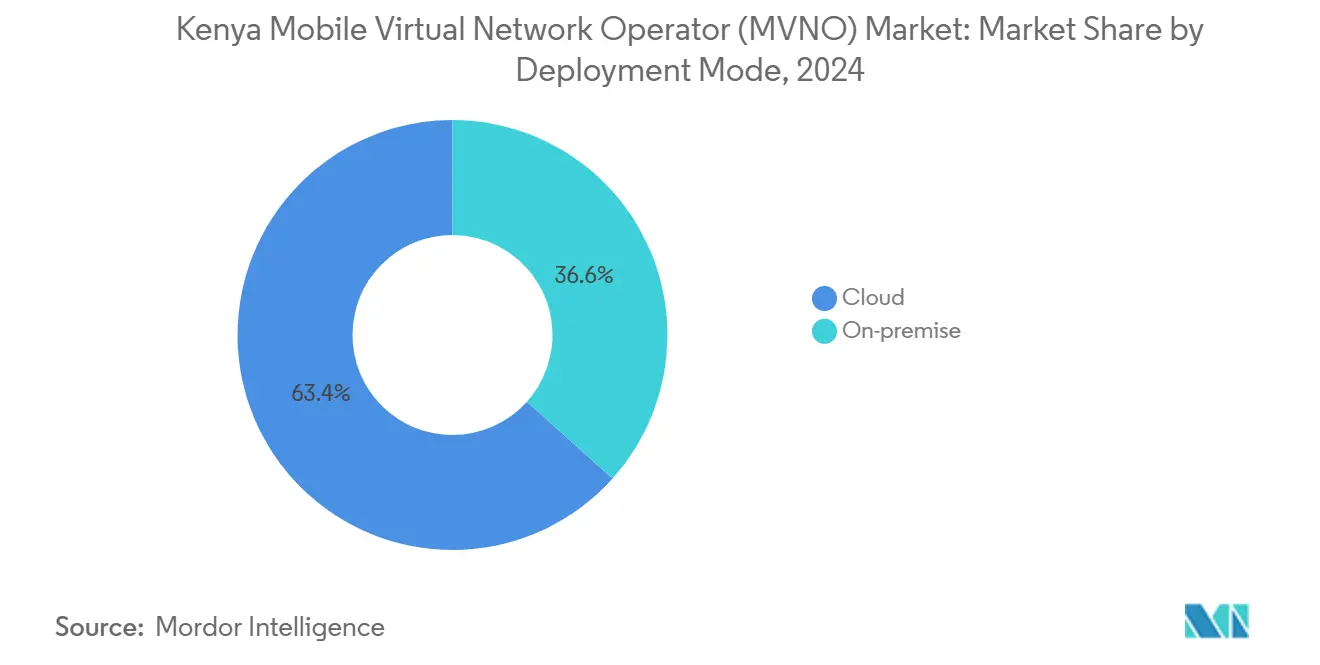

- By deployment model, cloud infrastructure led with 63.36% of the Kenya MVNO market share in 2024; on-premise deployments are projected to expand at an 11.46% CAGR to 2030.

- By operational mode, reseller & light MVNOs held 68.94% share of the Kenya MVNO market size in 2024, while full MVNOs record the highest projected CAGR at 29.81% through 2030.

- By subscriber type, the consumer segment accounted for 85.70% of the Kenya MVNO market size in 2024 and IoT-specific subscriptions are advancing at a 27.59% CAGR to 2030.

- By application, discount services captured 46.72% of the Kenya MVNO market share in 2024; cellular M2M applications are set to grow at 29.28% CAGR through 2030.

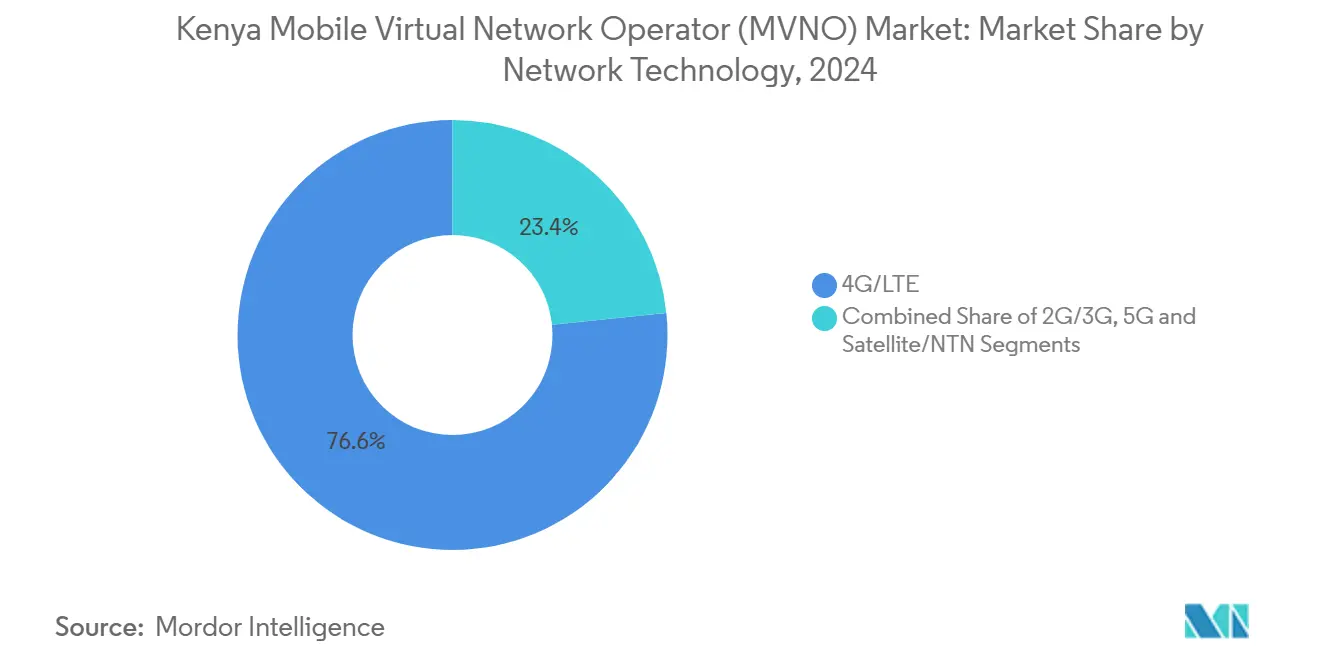

- By network technology, 4G/LTE delivered 76.64% of deployments in 2024, whereas 5G services are scaling at a 38.48% CAGR to 2030.

- By distribution channel, online and digital-only platforms commanded 51.69% share of the Kenya MVNO market size in 2024, with digital channels forecast to rise at 9.49% CAGR to 2030.

Kenya Mobile Virtual Network Operator (MVNO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing mobile-money penetration & interoperability mandates | +1.2% | National; strongest in urban centers and rural banking deserts | Medium term (2-4 years) |

| Aggressive MTR cuts slashing voice/SMS costs | +0.8% | National; benefits all MVNO models | Short term (≤ 2 years) |

| Rapid 4G/5G rollout on refarmed spectrum | +1.1% | National; priority in major cities | Medium term (2-4 years) |

| Regulatory “test-lab” for fintech-telco convergence | +0.9% | Pilot programs in Nairobi & Mombasa | Long term (≥ 4 years) |

| Starlink-enabled satellite backhaul opening rural niches | +0.7% | Northern Kenya & border regions | Medium term (2-4 years) |

| Surge in travel-eSIM adoption among diaspora & tourism | +0.5% | Airports and tourist destinations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Mobile-Money Penetration and Interoperability Mandates

Kenya hosts 42.3 million mobile-money wallets, equivalent to 78.9% penetration, giving MVNOs a ready base for bundling telecom and financial services. Airtel Money’s 2025 integration with Google Play via dLocal highlights how wallet interoperability now extends into digital commerce. [1]Finextra, “dLocal Adds Airtel Money to Google Play,” finextra.com Cross-network mandates cut friction, so MVNOs can build payment-enabled offerings without proprietary rails. Regulatory sandboxes allow pilots under the Data Protection Act 2019, lowering compliance barriers. These conditions let MVNOs bridge banking gaps for under-served users in both urban and rural settings. [2]Ministry of ICT, “Digital Economy Blueprint Progress Update,” ict.go.ke

Aggressive MTR Cuts Slashing Voice/SMS Costs

The Communications Authority’s March 2024 cut of mobile termination rates from KSh 0.58 to KSh 0.41 per minute slashed interconnect outlays by 29%, flipping voice economics in favor of virtual operators. Lower costs enable price-focused MVNOs to undercut incumbent bundles yet keep sustainable gross margins across the consumer base that forms 85.70% of subscribers. Volume elasticity also benefits host networks, aligning interests for wholesale partnerships. Coupled with mandated tower sharing, the Kenya MVNO market gains a cost baseline that accelerates prepaid voice recovery.

Rapid 4G/5G Rollout on Refarmed Spectrum

Safaricom now runs 1,114 5G sites across Kenya’s 47 counties, while Airtel increased sites from 690 to roughly 1,690 by late-2024. Spectrum refarming has lifted data throughput and reduced latency, making premium wholesale tiers viable for MVNOs. Equitel’s February 2024 5G launch—Africa’s first by an MVNO with 370 live cells—proves advanced network access is no longer the preserve of full MNOs. Open-RAN pilots and tower-sharing deepen wholesale capacity, a prerequisite for IoT MVNOs that depend on near-real-time links.

Regulatory “Test-Lab” for Fintech-Telco Convergence

Flexible licensing lets banks, SaaS vendors, and fintechs embed mobile connectivity. Equity Bank’s thin-SIM powered Equitel showcases seamless banking-telco fusion with 9 million active users. Sandboxes foster experimentation in micro-insurance, nano-loans, and digital ID, lowering entry hurdles. International accelerators—like Safaricom’s program with Sumitomo Corporation—channel capital and know-how into Kenya’s telecom-fintech mesh. [3]Sumitomo Corporation, “Safaricom and M-PESA Africa Launch Spark Accelerator,” sumitomocorp.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High on-net/off-net imbalance favoring Safaricom | -1.8% | Urban zones with heavy Safaricom usage | Long term (≥ 4 years) |

| Limited wholesale QoS SLAs on Airtel / Telkom | -1.1% | National; affects MVNO service quality | Medium term (2-4 years) |

| Low ARPU segments sensitive to KYC friction | -0.7% | Rural & informal settlements | Short term (≤ 2 years) |

| Delayed NUM for IoT SIMs | -0.4% | National; impacts M2M deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High On-Net/Off-Net Imbalance Favoring Safaricom

Safaricom’s 65.9% subscriber share consolidates network effects, as on-net calls cost less and often deliver better quality. Combined with 99% population coverage and an embedded M-Pesa ecosystem, churn barriers swell. MVNOs thus struggle to lure users whose social graphs sit on Safaricom. Even with 2024 MTR cuts, perception gaps remain. To compete, MVNOs must push value-added services or niche positioning rather than simple price plays.

Limited Wholesale QoS SLAs on Airtel / Telkom

Alternative hosts lack robust SLA frameworks, leaving MVNOs exposed on metrics such as call completion, data speed, and latency. The risk is acute for IoT MVNOs slated to grow at 27.59% CAGR, where downtime disrupts mission-critical telemetry. Monitoring overlays and customer-care investments become obligatory overheads, dampening margin upside. Progress on infrastructure-sharing regulations may ease constraints, yet a near-term service-quality gap persists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Scalability

Cloud deployments accounted for 63.36% of the Kenya MVNO market in 2024, underscoring operators’ preference for opex-light, elastic infrastructure. The Kenya MVNO market size for cloud deployments is projected to climb at an 11.46% CAGR through 2030 as virtual operators spin up services without owning core network hardware. Equitel’s 5G rollout validated the model by orchestrating nationwide coverage while managing workloads across distributed data centers. The shift dovetails with state-backed digital agendas that champion cloud adoption and codify data-protection norms, giving investors compliance clarity.

On-premise solutions persist, especially for enterprises bound by data-sovereignty or ultra-low-latency demands. Hybrid models emerge where core functions remain on-prem while value-added services run in public clouds. Rural initiatives benefit from cloud economics: Starlink’s USD 15 rental kits feed satellite backhaul into virtual cores, allowing MVNOs to sidestep tower construction costs. As cost curves fall, smaller brands enter, widening the Kenya MVNO market and challenging incumbent pricing.

By Operational Mode: Full MVNOs Gain Momentum

Reseller and light MVNOs captured 68.94% of 2024 subscriptions given minimal CAPEX and fast onboarding. Yet the full-MVNO cohort now registers a 29.81% CAGR, signaling maturing appetites for deeper network control and richer margins. Full licensees manage their own HLR/HSS, IMS, and billing, unlocking differentiated QoS and bespoke bundles for SMEs and verticals. The Kenya MVNO industry leans on cloud-native MVNE platforms that flatten entry costs, so fintechs and content providers can leapfrog straight to full-MVNO status.

Service-operator models secure niches in hospitality and transport, bundling Wi-Fi offload or transit ticketing. Regulatory schemes permit step-up licensing, enabling resellers to graduate as scale builds. Growing full-MVNO presence injects negotiating power into wholesale talks, potentially easing SLA bottlenecks on smaller host networks. Over time, operational-mode diversity strengthens competition and fuels consumer choice within the Kenya MVNO market.

By Subscriber Type: IoT Upswing Challenges Consumer Dominance

Consumers made up 85.70% of lines in 2024, reflecting prepaid-heavy dynamics and 135.8% SIM penetration. Nonetheless, IoT subscriptions—1.8 million as of September 2024—are sprinting at 27.59% CAGR on the back of agritech sensors, fleet telematics, and smart-city pilots. The Kenya MVNO market size attached to IoT endpoints rises as enterprises seek managed connectivity, data analytics, and device-lifecycle services packaged in one invoice.

Enterprise voice and data lines grow steadily, driven by remote-work and branch-connectivity needs. MVNOs woo SMEs with flat-rate bundles, MDM consoles, and API-ready billing. IoT growth diversifies revenue away from price-war-prone consumer arenas, cushioning ARPU drift. Regulatory clearance on IPv6 device numbering and streamlined KYC for low-data SIMs should further unlock scale.

By Application: Cellular M2M Outpaces Discount Voice

Discount voice still held 46.72% share in 2024 as price-sensitive users hunt deals. Yet cellular M2M lines, now at 29.28% CAGR, become the chief growth lever, paralleling Kenya’s digital-agriculture and logistics transformation. The Kenya MVNO market size for M2M services benefits from bundled sensor, platform, and connectivity offerings that deliver predictable margins. Business-application MVNOs cater to SMEs with secure VPNs, call-center integrations, and bulk SMS.

Other niche applications—gaming, edtech, health-monitoring—surface as 5G and edge compute reach scale. MVNOs leveraging cloud APIs spin up rapid pilots, testing uptake before committing spend. Such agility expands service diversity and stokes overall market competitiveness.

By Network Technology: 5G Adoption Escalates

4G/LTE commanded 76.64% of active lines in 2024, furnishing the baseline for mobile broadband and VoLTE. The Kenya MVNO market share of 5G lines, though embryonic, is climbing at a blistering 38.48% CAGR as device costs drop and coverage widens. High-bandwidth wholesale tiers allow MVNOs to pitch cloud gaming, 4K streaming, and low-latency industrial IoT. Legacy 2G/3G is sunset gradually, freeing spectrum for enhanced Mobile Broadband and NB-IoT overlays.

Satellite and NTN links complement terrestrial gaps; Starlink recorded over 10,000 Kenyan users by July 2024, illustrating latent rural demand. MVNOs bundle dual-profile eSIMs that shift between cellular and satellite, ensuring ubiquitous reach for agri-monitoring and humanitarian missions.

By Distribution Channel: Digital First Wins

Digital-only portals captured 51.69% of 2024 gross adds thanks to 72.6% smartphone penetration and widespread mobile-money fluency. App-based onboarding trims SIM logistics and supplies instant KYC. Physical retail survives via agent networks in rural markets where handset literacy lags. Hybrid pop-up kiosks at bus stops and malls extend reach during peak travel seasons.

Carrier sub-brand stores provide one-stop prospects but need careful channel-conflict management with host MNO branches. Third-party distributors, from agro-dealers to ride-hailing fleets, embed SIM sales, widening the Kenya MVNO market in hard-to-serve locales. eSIM uptake among diaspora travelers streamlines activation, cementing digital as the distribution channel of choice.

Geography Analysis

Nairobi, Mombasa, and Kisumu collectively generate the lion’s share of Kenya MVNO market revenues, buoyed by dense populations, 4G/5G saturation, and relatively high ARPU. Urban smartphone penetration tops 80%, fostering rapid adoption of fintech-enabled bundles. Safaricom and Airtel’s aggressive 5G rollouts have brought ultra-fast broadband to all 47 counties, flattening the traditional urban-rural digital divide.

In peripheral counties, satellite backhaul is bridging last-mile gaps. Starlink’s low-Earth-orbit nodes serve pastoral communities in Turkana and Marsabit, creating a testbed for hybrid terrestrial-satellite MVNO propositions. Government-driven digital village projects invite public-private tie-ups where MVNOs supply subsidized data and e-government access. Cross-border corridors with Uganda and Tanzania offer roaming-like-home propositions for traders and truck fleets, using shared numbering plans and zero-rated mobile-money transfers.

Kenya’s seaboard access to subsea cables enhances international bandwidth, favoring MVNOs focused on diaspora traffic. Travel-eSIM uptake spikes at Jomo Kenyatta and Moi airports as incoming tourists activate short-term voice-data bundles. Such geographic diversification mitigates urban saturation, enabling the Kenya MVNO market to chart multi-pronged expansion paths.

Competitive Landscape

The market hosts roughly a dozen active brands, yet top players hold meaningful scale. Equitel marries Equity Bank’s 9 million banking customers to telco services, leveraging integrated payment rails and, from 2024, 5G connectivity. Lycamobile Kenya positions for diaspora traffic, promising low international rates backed by a planned GBP 250 million Africa investment pipeline. Faiba Mobile focuses on unlimited data packs riding on Telkom’s 700 MHz spectrum.

Moderate entry barriers persist due to Safaricom’s infrastructure heft and M-Pesa lock-in, but wholesale-access mandates and cloud MVNE offerings dilute capex hurdles. Fintech entrants experiment with embedded-SIM lending, while agritech startups bundle sensor kits and data plans. Strategic alliances with cloud hyperscalers, satellite operators, and content studios diversify revenue streams beyond price plays, fostering a more dynamic Kenya MVNO market.

Wholesale negotiations increasingly revolve around differentiated SLAs for IoT and enterprise traffic. Host networks court MVNOs to monetize excess spectrum and shore up rural utilization. Regulatory vigilance on fair-competition keeps doorways ajar for fresh entrants, preserving healthy, innovation-driven rivalry.

Kenya Mobile Virtual Network Operator (MVNO) Industry Leaders

Equitel

Faiba Mobile

Lycamobile Kenya

JamboPay

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lycamobile announced a GBP 250 million Africa expansion plan, including Kenya.

- January 2025: Government proposed 10× fee hikes for satellite ISPs, raising cost-structure uncertainty.

- December 2024: Safaricom reported 44.7 million customers with 99% population coverage.

- September 2024: Kenya’s IoT subscriptions hit 1.8 million, up 1.2% QoQ.

Kenya Mobile Virtual Network Operator (MVNO) Market Report Scope

| Cloud |

| On-premise |

| Reseller |

| Service Operator |

| Full MVNO |

| Light / Brand MVNO |

| Consumer |

| Enterprise |

| IoT-specific |

| Discount |

| Business |

| Cellular M2M |

| Others |

| 2G/3G |

| 4G/LTE |

| 5G |

| Satellite/NTN |

| Online/Digital-only |

| Traditional Retail Stores |

| Carrier Sub-brand Stores |

| Third-Party/Wholesale |

| By Deployment Model | Cloud |

| On-premise | |

| By Operational Mode | Reseller |

| Service Operator | |

| Full MVNO | |

| Light / Brand MVNO | |

| By Subscriber Type | Consumer |

| Enterprise | |

| IoT-specific | |

| By Application | Discount |

| Business | |

| Cellular M2M | |

| Others | |

| By Network Technology | 2G/3G |

| 4G/LTE | |

| 5G | |

| Satellite/NTN | |

| By Distribution Channel | Online/Digital-only |

| Traditional Retail Stores | |

| Carrier Sub-brand Stores | |

| Third-Party/Wholesale |

Key Questions Answered in the Report

What is the current value of the Kenya MVNO market?

The Kenya MVNO market size is USD 53 million in 2025.

How fast is the Kenya MVNO market expected to grow?

It is projected to post a 5.72% CAGR, reaching USD 70 million by 2030.

Which deployment model leads among Kenyan MVNOs?

Cloud infrastructure leads, accounting for 63.36% of deployments in 2024.

What segment is growing fastest within Kenyan MVNO subscriptions?

IoT-specific lines are expanding at a 27.59% CAGR through 2030.

How significant is 5G adoption for Kenyan MVNOs?

5G lines are rising rapidly at a 38.48% CAGR as coverage and device affordability improve.

Which company launched Africa’s first MVNO-led 5G service?

Equitel introduced a 5G offering in February 2024 across 370 Kenyan sites.

Page last updated on: