Saudi Arabia Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

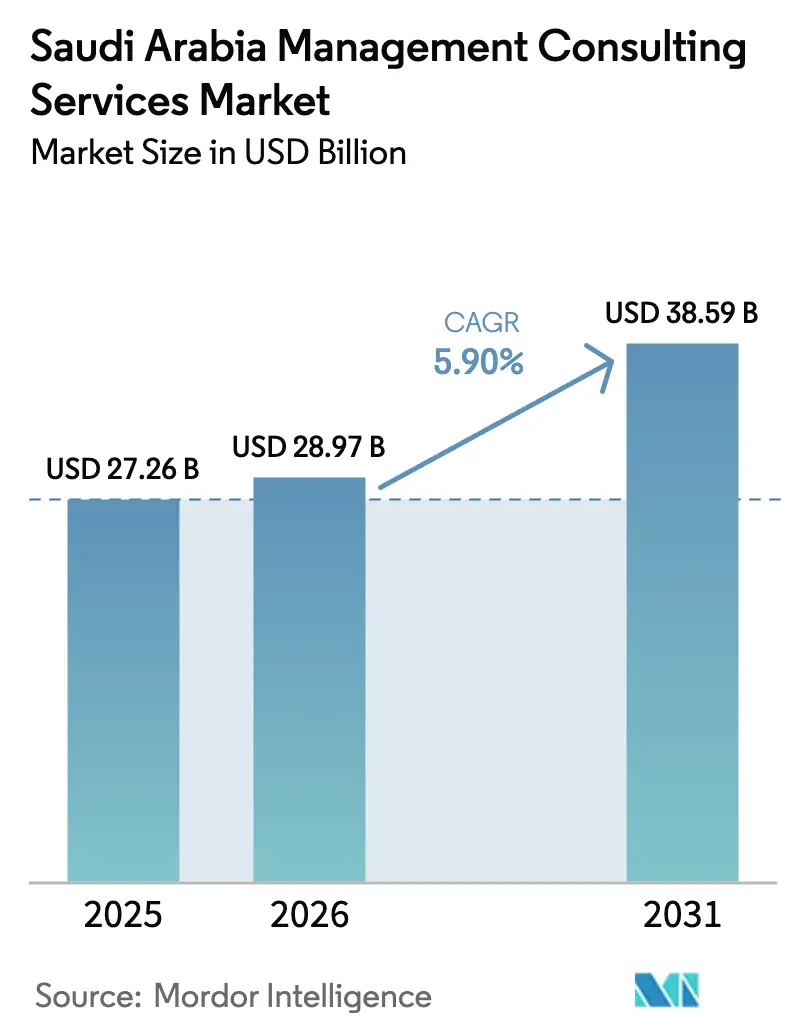

| Base Year Market Size (2025) | USD 27.26 Billion |

| Market Size (2026) | USD 28.97 Billion |

| Market Size (2031) | USD 38.59 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Management Consulting Services Market Analysis by Mordor Intelligence

The Saudi Arabia management consulting services market size was valued at USD 27.26 billion in 2025 and estimated to grow from USD 28.97 billion in 2026 to reach USD 38.59 billion by 2031, at a CAGR of 5.9% during the forecast period (2026-2031). Robust advisory demand stems from the Kingdom’s USD 1.3 trillion Vision 2030 investment plan, a 40% Saudization mandate that is redrawing talent pipelines, and giga-projects such as NEOM and Qiddiya that require integrated strategy, operations, and technology input. Heightened digital-transformation spending by ministries and state-owned enterprises is accelerating technology-consulting uptake, while procurement reforms that redirect at least 40% of personnel budgets to Saudi nationals are reshaping commercial models. International tier-one firms still capture 60% of fees, yet local champions are scaling quickly through public-private partnerships and acquisitions that unlock Category A digital-government contracts. The market continues to balance cyclical oil revenue headwinds with persistent diversification tailwinds, underpinning steady mid-single-digit growth rather than the boom-bust patterns seen a decade ago.

Key Report Takeaways

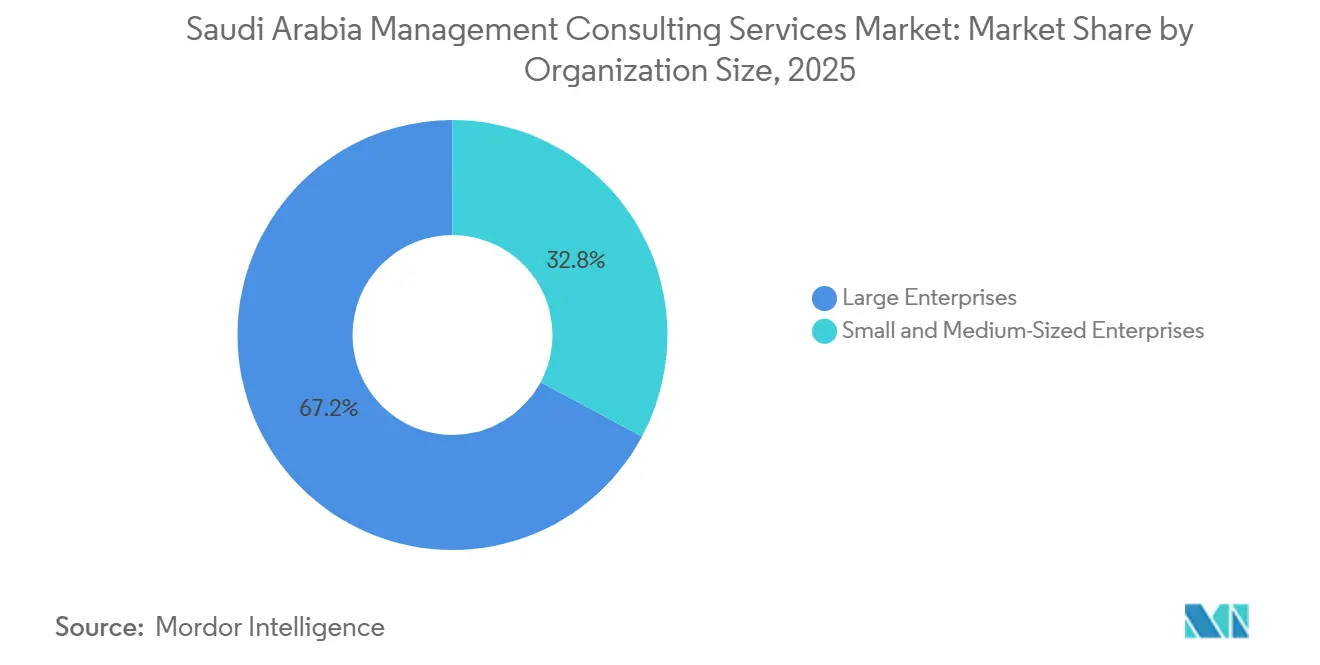

- By organization size, large enterprises led with 67.17% of the Saudi Arabia management consulting services market share in 2025, whereas SMEs are projected to expand at a 6.47% CAGR to 2031.

- By service type, strategy consulting held 28.43% revenue share in 2025, while technology consulting is forecast to grow at a 6.49% CAGR through 2031.

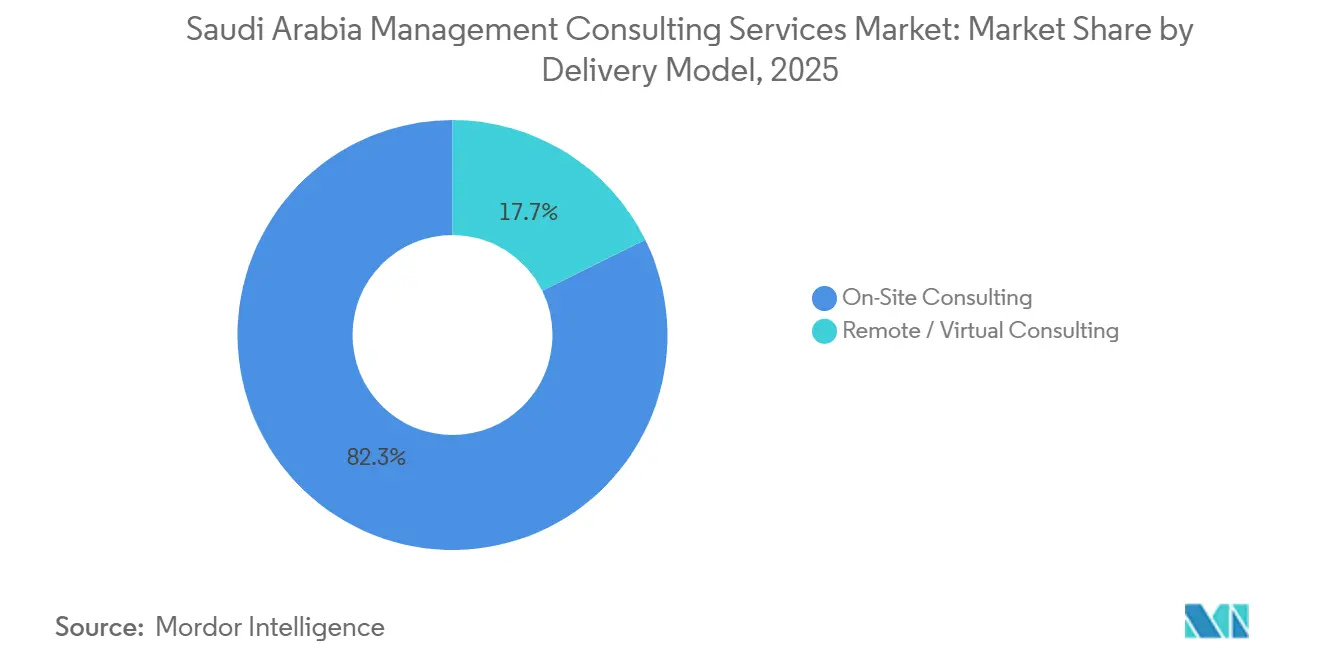

- By delivery model, on-site engagements accounted for 82.31% of the Saudi Arabia management consulting services market size in 2025, yet remote and virtual workstreams are advancing at a 6.71% CAGR between 2026-2031.

- By end-user industry, government and public-sector clients commanded 19.62% share in 2025, whereas esports and gaming is the fastest-rising vertical at a 6.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Diversification Spree Boosts Consulting Budgets | +1.80% | National, with concentration in Riyadh, Makkah, and Eastern Province | Long term (≥ 4 years) |

| Accelerated Digital Transformation and Cloud Adoption Across Sectors | +1.50% | National, with early gains in Riyadh and Jeddah | Medium term (2-4 years) |

| Mega-Project Pipeline (NEOM, Red Sea, Qiddiya) Driving Project-Based Advisory | +1.30% | Tabuk (NEOM), Makkah (Red Sea), Riyadh (Qiddiya) | Long term (≥ 4 years) |

| Liberalized Foreign-Ownership Rules Attract Global Entrants Needing Advice | +0.70% | National, with early entry via Riyadh and Jeddah | Medium term (2-4 years) |

| Saudization Compliance Complexity Raises HR and Operations Consulting Demand | +0.40% | National | Short term (≤ 2 years) |

| Emergence of Esports and Gaming Sector Needing Strategy and Market-Entry Support | +0.20% | Riyadh, with spillover to Jeddah and Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Diversification Spree Boosts Consulting Budgets

The government increased public-spending allotments to USD 342 billion in 2025, channelling funds into tourism, digital government, and infrastructure programs that require multi-year advisory mandates.[1]Ruth Steen, “MEcon | December 2025 Edition,” Deloitte Middle East, deloitte.com PIF, stewarding more than USD 700 billion in assets, added 30 new portfolio companies between 2024-2025, driving continuous demand for board design, governance, and market-entry support. Non-oil GDP outpaced oil growth at 4.6% YoY in Q2 2025, pushing ministries to seek external expertise for sector-specific policy frameworks. Faster foreign-investment licensing compresses set-up times to six months yet heightens the complexity of tax and local-content structuring, locking in tier-one firms that offer integrated legal, fiscal, and operating-model guidance. Quality-of-life initiatives such as a five-year Riyadh rent freeze add ancillary real estate advisory opportunities, broadening the consulting addressable spend.

Accelerated Digital Transformation and Cloud Adoption Across Sectors

Saudi Arabia’s ICT sector hit SAR 180 billion (USD 48 billion) in 2024 and is slated to grow another 50% by 2030, stimulating demand for cloud-migration, cyber-security, and AI-road-map projects.[2]Dunya Hassanein, “Foreign Business Setup in Saudi Arabia’s Consulting Sector: Guide for 2025,” Setup in Saudi, setupinsaudi.com SDAIA’s HUMAIN program aims to embed AI in 200 public-sector use cases by 2027, pushing agencies to engage firms for data-governance and change-management know-how.[3]Reem Walid, “Saudi Arabia’s Localization Plan Is Reshaping Consultancy Sector,” Arab News, arabnews.com Mandatory ISO 27001 certification for critical infrastructure by end-2026 has created a cybersecurity-consulting backlog among energy, healthcare, and finance operators. Category A PPP accreditation allows solutions by stc to migrate 50 government entities to the cloud by 2027, firming a template other are racing to replicate.[4]solutions by stc, “Annual Report 2024,” solutions.com.sa AI’s forecast USD 135 billion GDP uplift remains contingent on scaling pilots into enterprise deployment, underscoring the advisory void in data-to-value translation.

Mega-Project Pipeline (NEOM, Red Sea, Qiddiya) Driving Project-Based Advisory

NEOM awarded more than USD 10 billion in construction contracts during 2024-2025, necessitating master planning and program-management counsel. The Red Sea Project opened its first 16 hotels in 2024 and expands to 50 by 2030, bringing sustainability frameworks and hospitality workforce planning to the fore. Qiddiya’s USD 8 billion first phase broke ground on Six Flags Riyadh and a gaming hub, prompting revenue-stream modelling, visitor-experience design, and PPP structuring services. Diriyah Gate’s USD 64 billion cultural district likewise awarded heritage-preservation advisory contracts. As giga-projects scale, SMEs in their supply chains request strategic, operational, and leadership support via programs such as Aramco’s Taleed, which has already assisted more than 2,900 suppliers.

Liberalized Foreign-Ownership Rules Attract Global Entrants Needing Advice

From 2024, 100% foreign ownership in consulting removed the necessity for local equity partners, accelerating market entries and subsidiary upgrades. Fragomen’s second Saudi office exemplifies rising immigration-advisory work linked to the Regional Headquarters program. However, a 40% Saudization quota forces entrants to build talent pipelines via university alliances and internal academies, boosting HR and organization-transformation engagements for domestic specialists. M&A activity is accelerating solutions by stc’s 40% acquisition of Devoteam Middle East forged a top-tier digital-consulting platform consolidating nearly 25% local IT-consulting share.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened Procurement Scrutiny and PwC Advisory Ban Curb Spending | -0.60% | National, with concentration in Riyadh (central government) | Short term (≤ 2 years) |

| Rapid Build-Up of In-House Strategy Units Reducing External Spend | -0.50% | National, with early impact in Riyadh and Eastern Province | Medium term (2-4 years) |

| Chronic Shortage of Bilingual Saudi Consulting Talent Inflates Costs | -0.30% | National | Medium term (2-4 years) |

| Volatile Oil Revenues Trigger Budget Cyclicality for Consulting Projects | -0.20% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened Procurement Scrutiny and PwC Advisory Ban Curb Spending

An advisory ban on PwC for certain government work in 2024 extended tender cycles to nine months and raised bid-preparation expenses by up to 30%, as ministries now demand granular subcontractor disclosures and outcome metrics. The Expenditure and Project Efficiency Authority audits consulting contracts above SAR 10 million, compelling firms to tie fees to measurable benefits. While big-four peers absorbed much of PwC’s displaced pipeline, mid-tier players captured niche mandates, reshaping competitive allocations in the short run. Heightened scrutiny favours ISO 9001-certified firms with robust compliance functions, leaving smaller boutiques exposed to cost and legal burdens.

Rapid Build-Up of In-House Strategy Units Reducing External Spend

PIF’s 200-person internal strategy desk cut external advisory outlays by 30-40% year-on-year, while Aramco’s expanded corporate-planning division had a similar dampening effect. Saudi Telecom Company established an internal transformation office in 2024, shifting demand from holistic roadmaps to niche execution modules such as AI-model validation. Although total spend contracts in the near term, demand pivots to specialized skills that complement resident teams, forcing consultancies to differentiate through proprietary analytics tools and global benchmarking assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Enterprises Anchor Demand, SMEs Accelerate

Large enterprises captured 67.17% of the Saudi Arabia management consulting services market in 2025, principally through multi-year mandates exceeding USD 5 million that bundle strategy, operations, and technology work. Engagement intensity is highest among ministries implementing Vision 2030 roadmaps and PIF portfolio companies professionalizing governance structures. The Saudi Arabia management consulting services market size attributable to SMEs is expanding at a 6.47% CAGR, buoyed by 1.68 million active registrations and USD 15.7 billion in Tomouh funding.

SME advisory contracts average USD 50,000-500,000 over three to six months, focusing on digital go-to-market, access-to-finance, and supply-chain localization. Monsha’at’s support centers funnel thousands of firms from free guidance to paid consulting each year, while Aramco’s Taleed program signposts strategy, leadership, and market-access gaps for more than 2,900 suppliers. As a result, specialized boutiques with modular offerings are emerging to serve SME needs at scale.

By Service Type: Technology Consulting Outpaces Strategy Amid AI Push

Strategy retained 28.43% revenue share in 2025, underpinned by Vision 2030 sector-transformation roadmaps and PIF deal support. However, technology consulting will be the principal growth engine, expanding at 6.49% CAGR to 2031 as enterprises transition pilots into full-scale AI deployments. The Saudi Arabia management consulting services market share for operations consulting hovered near 20%, reflecting supply-chain and procurement-optimization programs across manufacturing and industrial clients.

Cloud-migration programs for 50 government entities, mandatory ISO 27001 certification, and the HUMAIN AI initiative together fuel multiyear technology-consulting pipelines. Sustainability advisory is surfacing as an adjacent hotspot as regulators prepare Scope 1-3 disclosure rules aligned with TCFD. Fee models are shifting to value-sharing structures, typified by solutions by stc’s ten-year smart-parking PPP that links consulting income to usage revenues.

By Delivery Model: Remote Consulting Gains Ground Despite On-Site Dominance

On-site engagements represented 82.31% of 2025 revenue as giga-projects and cultural norms require in-person workshops and program oversight. Yet remote and virtual delivery is moving up the curve at a 6.71% CAGR, enabled by collaboration tools and talent shortages that make fully on-premises staffing uneconomic. The Saudi Arabia management consulting services market size for remote work benefits from Digital Government Authority programs that legitimize virtual support and slash travel overheads.

Remote uptake exceeds 50% in cloud-migration and cybersecurity assignments, whereas strategy and HR remain around 20-30% virtual because stakeholder alignment still demands physical co-location. Hybrid models are emerging as the market norm, balancing cost efficiency with requirements for local presence under Saudization and data-sovereignty rules.

By End-User Industry: Government Anchors, Esports Surges

Government and public-sector entities absorbed 19.62% of 2025 consulting spend, linked to cloud-enablement mandates and the formation of 30 new PIF portfolio companies. The Saudi Arabia management consulting services market size tied to esports is on track for a 6.88% CAGR, catalysed by Savvy Games Group’s USD 38 billion war chest and the Esports World Cup’s successful debut in 2024.

IT and telecom held about 18% share, with Saudi Telecom Company rolling out digital wallets and 5G enterprise solutions that require architecture and cyber-resilience advisory. Financial services contributed roughly 16% as banks pursue open-banking and Islamic-fintech propositions. Healthcare, manufacturing, energy, and real estate round out the demand picture, each supported by sector-specific policy shifts and giga-project spillovers.

Geography Analysis

Riyadh Province commanded 39% of consulting activity in 2025, propelled by central-government ministries, PIF headquarters managing USD 700 billion in assets, and the 176-kilometer Riyadh Metro build-out. Category A public-private partnerships, such as solutions by stc’s smart-parking concession, provide recurring revenue streams that anchor firms in the capital. Stable office rents under a five-year freeze entice multinational headquarters, expanding advisory work on entity structuring and Saudization compliance.

Makkah Province accounted for 17% of 2025 spend, centered on the USD 28 billion Red Sea tourism corridor and Jeddah’s role as the country’s import-export gateway. Consulting demand spans sustainability certification, destination marketing, and Hajj-specific crowd-management systems for 30 million annual pilgrims. Eastern Province captured 16%, driven by Aramco’s energy-transition roadmaps and the 80-million-ton throughput at King Fahd Industrial Port, which requires logistics-optimization services.

The rest of Saudi Arabia, including Tabuk’s NEOM, absorbed the remaining 28%. NEOM alone issued USD 10 billion in contracts over 2024-2025, creating project-management offices and procurement-advisory mandates. Aseer’s USD 3.9 billion Soudah Development adds tourism-consulting opportunities. While Riyadh and Makkah will remain budget gatekeepers, consulting work is migrating toward emerging provinces as giga-projects move from design into execution.

Competitive Landscape

International tier-one firms McKinsey, BCG, Bain, Deloitte, EY, KPMG, Accenture jointly control roughly 60% of fee pools, but local players such as solutions by stc, Elm, and Pure Consulting are scaling fast through acquisitions and Category A digital-government accreditations. PwC’s 2024 advisory ban redistributed pipeline into competitors’ hands, temporarily tightening capacity and boosting day rates in specialized areas like forensic accounting.

Strategies split three ways: global majors localize talent via academies and secondments to hit 40% Saudization, domestic champions add capabilities through M&A evident in solutions by stc’s Devoteam deal and boutiques pick vertical niches such as gaming or ESG. Technology-led differentiation is rising; Deloitte’s Riyadh Digital Center lets clients co-create AI solutions on-site, whereas Elm’s planned 40% stake in Smart National Solutions widens systems-integration reach.

Price pressure persists as ministries adopt outcome-based contracts, rewarding firms that assume delivery risk through revenue-sharing. Simultaneously, internal strategy units at PIF, Aramco, and stc poach mid-career consultants with higher salaries and nation-building narratives, forcing consultancies to offer equity, global mobility, and cutting-edge toolkits to defend retention.

Saudi Arabia Management Consulting Services Industry Leaders

Deloitte Touche Tohmatsu Ltd. (Monitor Deloitte)

Ernst & Young Global Ltd. (EY-Parthenon)

McKinsey & Company Inc.

Accenture plc

PricewaterhouseCoopers (PWC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Monsha’at inked a strategic pact with LinkedIn to upskill high-growth enterprises and bolster SME talent pipelines.

- October 2025: Aramco’s Taleed program won World Economic Forum recognition after assisting 2,900 SMEs and launching 17 new ventures.

- January 2025: A USD 600 billion cooperation package with the United States accelerated AI-zone creation and business-licensing reforms, opening new consulting niche.

- December 2024: EY launched the EY Academy to train finance, data, and sustainability professionals, supporting Vision 2030 talent goals.

Saudi Arabia Management Consulting Services Market Report Scope

The Saudi Arabia Management Consulting Services Market Report is Segmented by Organization Size (Large Enterprises, Small and Medium-Sized Enterprises), Service Type (Strategy Consulting, Operations Consulting, HR Consulting, Technology Consulting, Other Service Types), Delivery Model (On-Site Consulting, Remote/Virtual Consulting), End-User Industry (IT and Telecommunications, Healthcare and Life Sciences, Financial Services, Manufacturing and Industrial, Energy and Utilities, Government and Public Sector, Real Estate and Construction, Retail and Consumer Goods, Media Entertainment and Sports, Hospitality and Travel, Other End-User Industries), and Geography (Riyadh Province, Makkah Province, Eastern Province, Rest of Saudi Arabia). The Market Forecasts are Provided in Terms of Value (USD).

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-Site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other End-User Industries |

| Riyadh Province |

| Makkah Province |

| Eastern Province |

| Rest of Saudi Arabia |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-Site Consulting |

| Remote / Virtual Consulting | |

| By End-User Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other End-User Industries | |

| By Geography | Riyadh Province |

| Makkah Province | |

| Eastern Province | |

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How big will consulting spend in Saudi Arabia be by 2031?

It is forecast to reach USD 38.59 billion, advancing at a 5.9% CAGR from 2026-2031.

Which segment grows fastest in advisory demand?

Technology consulting is projected to post a 6.49% CAGR through 2031 as cloud and AI programs scale.

Why are SMEs attracting more consulting attention now?

Monsha'at financing and programs like Tomouh fuel SME growth, pushing SME advisory revenues up at a 6.47% CAGR.

How does the Saudization policy affect consulting firms?

A 40% national-talent quota compels firms to build local academies, influencing HR consulting and staffing strategies.

What is driving remote-delivery uptake?

Hybrid models cut travel costs and mitigate talent shortages, helping remote engagements grow at 6.71% CAGR.

Page last updated on: