Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Saudi Arabia Data Center Processor Market Report Segments the Industry Into Processor Type (GPU, CPU, FPGA, AI Accelerator), Application (Advanced Data Analytics, AI/ML Training and Inferences, and More), Architecture (x86, Non-X86 (ARM, Power and Other Processors)), Data Center Type (Enterprise, Colocation, Cloud Service Providers). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

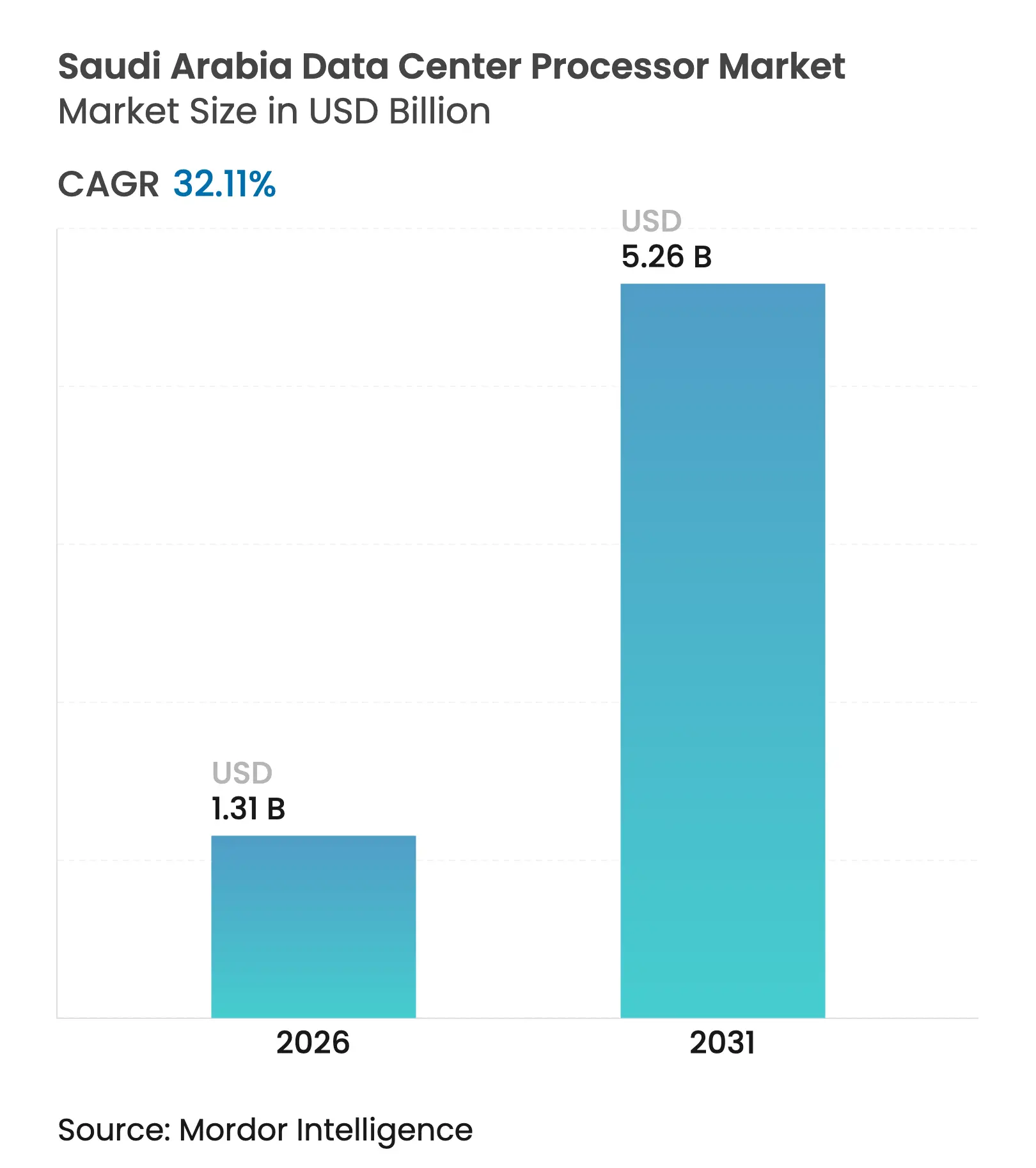

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 32.11 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

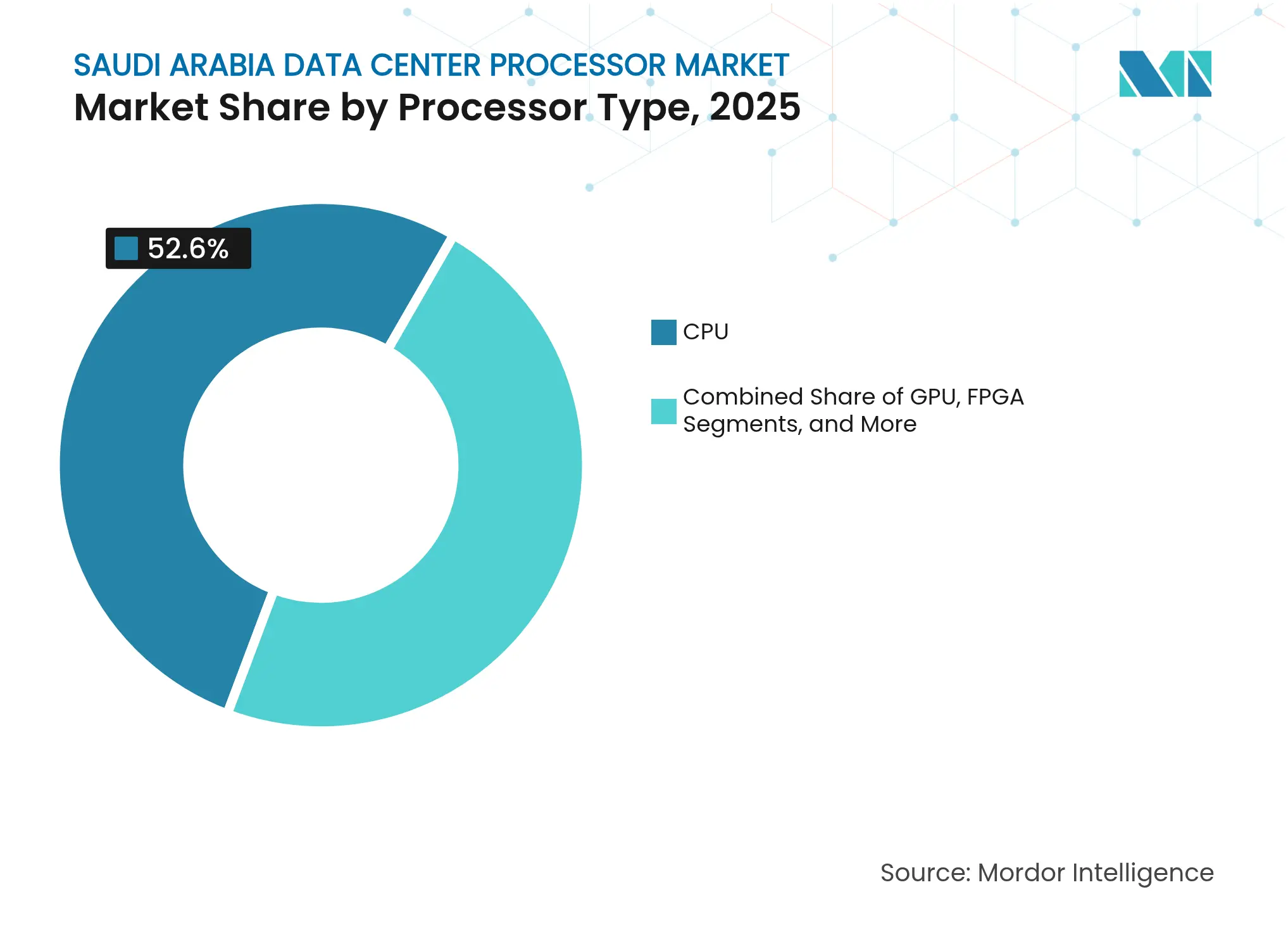

The Saudi Arabia data center processor market size was valued at USD 0.99 billion in 2025 and estimated to grow from USD 1.31 billion in 2026 to reach USD 5.26 billion by 2031, at a CAGR of 32.11% during the forecast period (2026-2031). Processor demand in the Kingdom is expanding from traditional enterprise workloads toward AI training, real-time inference and hyperscale computing as Vision 2030 turns the country into a regional digital infrastructure hub. Surging capital commitments exceeding USD 21 billion from hyperscale operators, combined with government cloud-first mandates, keep the procurement curve steep. Large single-order deals—such as HUMAIN’s purchase of 18,000 NVIDIA Blackwell GB300 GPUs for its planned 500 MW AI campus—demonstrate how specialized silicon now dominates new build-outs. CPUs continued to contribute the bulk of revenue at a 53.2% 2024 share, yet AI accelerators are advancing at a 36.4% CAGR as operators seek domain-specific throughput. Competition is intensifying: cloud service providers already account for 46.3% of 2024 revenue and are scaling at a 36.8% CAGR on the back of sovereign data localization plus massive AI cluster roll-outs.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Vision

2030 Cloud-First Policy accelerating digital infrastructure spend

Vision

2030 Cloud-First Policy accelerating digital infrastructure spend

| +8.5% | National, concentrated in Riyadh, Jeddah, NEOM | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:

+8.5%

|

Geographic

Relevance

:

National,

concentrated in Riyadh, Jeddah, NEOM

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Hyperscale

and colocation build-outs from AWS, Microsoft and stc

Hyperscale

and colocation build-outs from AWS, Microsoft and stc

| +7.2% | National, with focus on major urban centers | Short term (≤ 2 years) | |||

AI

factories ordering >200k GPUs spur processor demand

AI

factories ordering >200k GPUs spur processor demand

| +9.8% | NEOM, Riyadh, emerging tech zones | Medium term (2-4 years) | |||

Subsidised

power and tax incentives inside CCSEZ

Subsidised

power and tax incentives inside CCSEZ

| +3.1% | CCSEZ zones, industrial cities | Long term (≥ 4 years) | |||

Draft

Global AI Hub Law enables "data embassies"

Draft

Global AI Hub Law enables "data embassies"

| +2.7% | National, with international data sovereignty focus | Long term (≥ 4 years) | |||

Local

fab initiative (ALAT) to secure advanced nodes <7 nm

Local

fab initiative (ALAT) to secure advanced nodes <7 nm

| +1.9% | National, technology development zones | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Vision 2030 Cloud-First Policy Accelerating Digital Infrastructure Spend

Government agencies must prefer cloud over on-premises IT, driving hyperscalers to deploy sovereign regions and thereby multiplying processor installations across the Saudi Arabia data center processor market. The Cloud Computing Regulatory Framework obliges data localization and has already stimulated foreign direct investment while nudging private firms toward cloud-native adoption.[1]Cloud Computing Regulatory Framework, Middle East Institute (MEI), mei.edu Expanding multi-tenant footprints boosts demand for CPUs with strong virtualization support as well as GPUs tuned for scalable AI services. Localization clauses push providers to offer bespoke silicon stacks tuned to Saudi security rules, tightening competition around low-latency performance.

Hyperscale and Colocation Build-outs from AWS, Microsoft and stc

AWS has earmarked USD 5.3 billion to open multiple availability zones by 2026, Microsoft has finalized three sites, and stc now operates 16 facilities totaling 125 MW.[2]AWS to invest USD 5.3 billion in Saudi Arabia, aws.amazon.com; stc expands data centers to 125 MW, ec-mea.com Each new campus refreshes processor fleets faster than enterprise budgets can match, prompting vendors to fast-track product launches tailored to high-core-count, multi-socket nodes. Colocation providers are differentiating through heterogeneous compute pods—CPU, GPU and FPGA—in one rack, appealing to tenants that need flexible AI acceleration without moving entirely to public cloud.

AI Factories Ordering Greater than 200k GPUs Spur Processor Demand

NEOM’s USD 5 billion, 1.5 GW AI factory illustrates a new class of ultra-dense compute that centers on GPU clusters for sovereign language models.[3]NEOM announces net-zero AI factory, neom.com Such environments still rely on high-thread CPUs for input preprocessing and cluster control, creating blended demand for both categories inside the Saudi Arabia data center processor market. The national plan to train 20,000 AI professionals by 2030 further multiplies requirements for educational and research compute, including network processors and storage controllers that can feed large tensor jobs at line rate.

Subsidised Power and Tax Incentives Inside CCSEZ

The CCSEZ lowers power tariffs and offers tax breaks, driving TCO down for operators installing 500 W-plus GPUs. The zone’s quick-clearance import regime helps tenants adopt the newest silicon instead of sweating older assets. Its security-first charter draws companies requiring hardware security modules, fostering adoption of processors with embedded encryption engines.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

power and cooling OPEX for 300-W+ TDP chips

High

power and cooling OPEX for 300-W+ TDP chips

| -4.8% | National, particularly in desert regions | Short term (≤ 2 years) | (~) %

Impact on CAGR Forecast:

-4.8%

|

Geographic

Relevance

:

National,

particularly in desert regions

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

US

export controls on high-end GPUs/HBM stacks

US

export controls on high-end GPUs/HBM stacks

| -6.2% | National, affecting AI and HPC deployments | Medium term (2-4 years) | |||

Shortage

of advanced-node design and operations talent

Shortage

of advanced-node design and operations talent

| -2.9% | National, concentrated in tech hubs | Long term (≥ 4 years) | |||

Water

scarcity tightening liquid-cooling permits

Water

scarcity tightening liquid-cooling permits

| -3.1% | National, severe in inland regions | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Power and Cooling OPEX for 300-W+ TDP Chips

Summer temperatures above 50 °C push PUE above 2.0, inflating operating expenses for AI-class silicon inside the Saudi Arabia data center processor market. Processors such as Intel Xeon 6980P exceed 500 W TDP, necessitating liquid cooling investments that add both capital cost and skills gaps. Facilities now compare lifetime energy outlays as closely as purchase prices, encouraging interest in immersion and direct-to-chip approaches that require vendor-validated thermal designs.

US Export Controls on High-End GPUs/HBM Stacks

Commerce Department licenses can delay shipments of top-tier AI GPUs for months, creating procurement uncertainty for Saudi projects. Restrictions on high-bandwidth memory have encouraged some builders to pivot to European or Asian accelerators, even if raw performance lags. Stockpiling approved SKUs has become common, generating volatile demand spikes that ripple through the Saudi Arabia data center processor market.

By Processor Type: AI Accelerators Drive Next-Generation Workloads

CPUs retained 52.60% revenue share in 2025 as they remain central to orchestration, virtualization and general compute. However, AI accelerators are racing ahead with a 35.85% CAGR, reflecting the country’s preference for dedicated matrix engines. The Saudi Arabia data center processor market size for AI accelerators is projected to expand from a mid-three-digit-million baseline in 2026 alongside sovereign model build-outs. GPUs bridge graphics and training needs, while FPGAs cover telecom and edge workloads that prize deterministic latency.

Heterogeneous racks are becoming the norm. Groq’s language processing unit posts 25-fold faster inference versus legacy GPU servers, signalling how domain-specific chips can reset performance curves. Intel’s Gaudi 3 shows 50% better inference throughput and 40% energy savings compared to NVIDIA H100, sharpening competition. Architectural choices increasingly hinge on Arabic NLP efficiency, not just peak FLOPS, changing purchasing criteria across the Saudi Arabia data center processor market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Advanced Analytics Reshape Infrastructure Requirements

AI/ML workloads commanded 32.40% of 2025 revenue and continue to shape data-center design, followed by high-growth advanced analytics at 35.20% CAGR through 2031. The Saudi Arabia data center processor market share for advanced analytics will climb as ministries and enterprises ingest streaming data for real-time insights. HPC, security and network functions persist but now demand specialized cryptographic and programmable cores.

Processor metrics are shifting from GHz and core counts to tensors-per-second and memory bandwidth. Managing 8,700 national datasets calls for silicon optimized for rapid ETL and mixed-workload concurrency. CCSEZ’s cyber focus boosts demand for chips with integrated crypto accelerators. Hybrid applications that blend inference with database calls pressure vendors to supply balanced CPU-GPU packages.

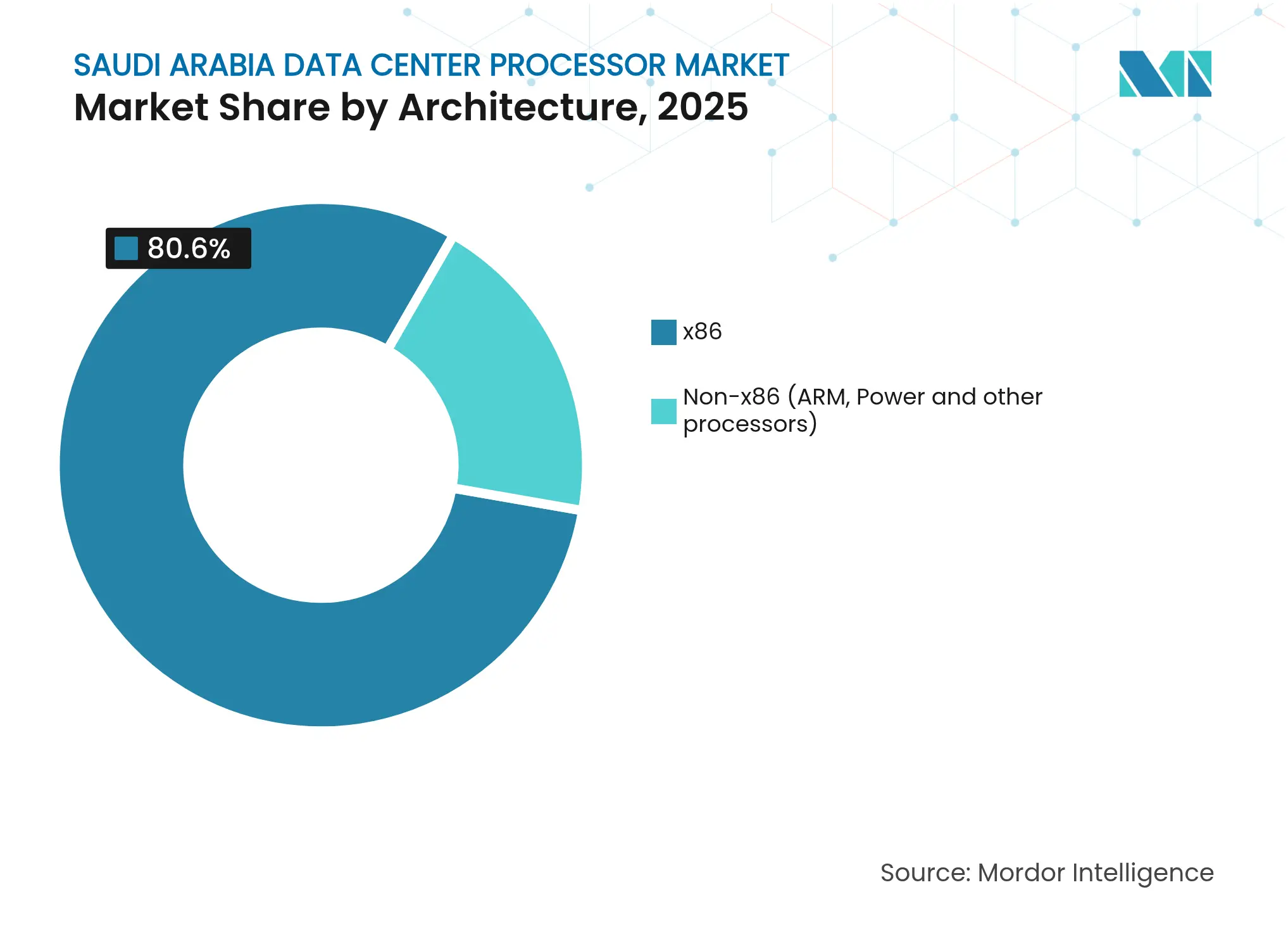

By Architecture: Non-x86 Gains Momentum Through Specialized Workloads

x86 maintained 80.60% share in 2025 by virtue of its mature software ecosystem. Yet non-x86 designs are advancing at 36.90% CAGR as ARM and AI-centric architectures promise higher performance-per-watt. A fast-growing slice of the Saudi Arabia data center processor market size will flow to ARM Neoverse platforms that offer better density for cloud-native services. Power11 remains in niche enterprise roles, while early RISC-V pilots test open-source viability.

AmpereOne’s 256-core CPU delivers 2.5 times the power efficiency of classic x86, suiting inference nodes where energy caps are strict. ALAT’s ambitions at sub-7 nm could let local players pair advanced lithography with novel core designs. Architecture choice is now workload-first, infrastructure-second across the Saudi Arabia data center processor market.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Cloud Providers Lead Infrastructure Modernization

Cloud operators held 46.10% revenue in 2025 and are growing at 36.43% CAGR, thanks to attractive economics from shared resource pools. Their aggressive refresh cadence means that freshest silicon often debuts in the cloud before appearing on enterprise price lists. The Saudi Arabia data center processor market share for enterprise facilities is slipping even though absolute spending still climbs; many organizations adopt hybrid topologies to balance latency, sovereignty and cost.

Microsoft’s trio of Saudi facilities will open by 2026, bringing multi-zone redundancy and new demand for top-bin CPUs and GPUs microsoft.com. Colocation specialists lure tenants with pre-cabled liquid loops and accelerator-dense racks, eliminating upfront capex hurdles. Edge-tier micro-data centers near industrial sites are another frontier, requiring low-power CPUs combined with AI inference engines for sub-10 ms response.

Riyadh and Jeddah currently anchor most capacity thanks to fiber density and proximity to major customers. Combined, the two hubs host well over half of all installed processors inside the Saudi Arabia data center processor market. The Kingdom’s geographic position allows sub-25 ms reach to one-third of the global population, making it a preferential latency node for regional AI services. NEOM is emerging as the flagship next-generation zone, with a planned 1.5 GW, net-zero, AI-centric campus engineered for renewable energy. Such green targets elevate demand for energy-frugal processors and rack-scale liquid cooling.

Economic zones like CCSEZ offer subsidized utilities that tilt TCO math toward processor-intensive deployments. Dammam and the Eastern Province extend reach into industrial digitization projects, fueling purchases of processors suited for industrial IoT workloads that integrate OT and IT stacks. Sovereignty rules sometimes mandate that sensitive government workloads stay within certain metro areas, guiding hardware placement.

Vision 2030 calls for distributed compute beyond major cities; new smart-city projects are budgeting edge clusters that need low-power, high-reliability silicon. Inland sites wrestle with limited water rights, leading investors to favor coastal or renewable-powered locales for GPU-dense builds. Renewable energy corridors support carbon-aware service-level agreements, positioning energy-efficient architectures as a competitive lever throughout the Saudi Arabia data center processor market.

Market Concentration

Market concentration is moderate but shifting. Intel and AMD still supply the bulk of CPU sockets, yet NVIDIA, Groq, Cerebras and emerging ARM providers capture outsized mindshare for AI compute. Vendors differentiate on domain-specific acceleration, package-on-package memory and total system cost rather than clock speed alone. Broadcom’s 3.5D chiplet packaging for AI accelerators underscores the industry’s race to compress more compute per watt and per rack unit.

The Saudi Arabia data center processor market is now an arena for strategic partnerships. HUMAIN aligned with NVIDIA for Blackwell GPUs, while DataVolt inked a USD 20 billion supply deal with Supermicro to secure liquid-cooled racks. Local chip design programs supported by the National Semiconductor Hub aim to attract 50 fabless firms, focusing on Arabic AI IP blocks and energy-efficient edge chipsets. Disruptors such as Groq show 18-fold inference speed-ups, proving that specialized architectures can leapfrog incumbents.

MandA activity around AI silicon start-ups is expected to accelerate as global suppliers seek regional footholds. Cloud providers negotiate directly with chip vendors for customized SKUs. With export-control risk still present, alternative suppliers from Europe and Asia are being evaluated. These dynamics collectively reshape vendor stakes inside the Saudi Arabia data center processor market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SEGMENTATION

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Data centers house and manage critical applications and data, using computing and storage networks for efficient delivery. Processors—GPUs, CPUs, and TPUs—are central to their operation. GPUs handle multitasking, excelling in graphics rendering and AI tasks. CPUs, with multi-core architecture, support parallel processing. TPUs, designed for machine learning, stand out from GPUs, which have transitioned from graphics to AI applications.

Saudi Arabia Data Center Processor Market is Segmented by Processor Type (CPU, GPU, FPGA, AI Accelerators), by Application (Advanced Data Analytics, AI/ML Training and Inferences, High Performance Computing, Security and Encryption, Network Functions, and Others), by Architecture (x86 and Non-x86 (ARM, Power and other processors), and by Data Center Type (Enterprise, Colocation and Cloud Service Providers). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.