Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

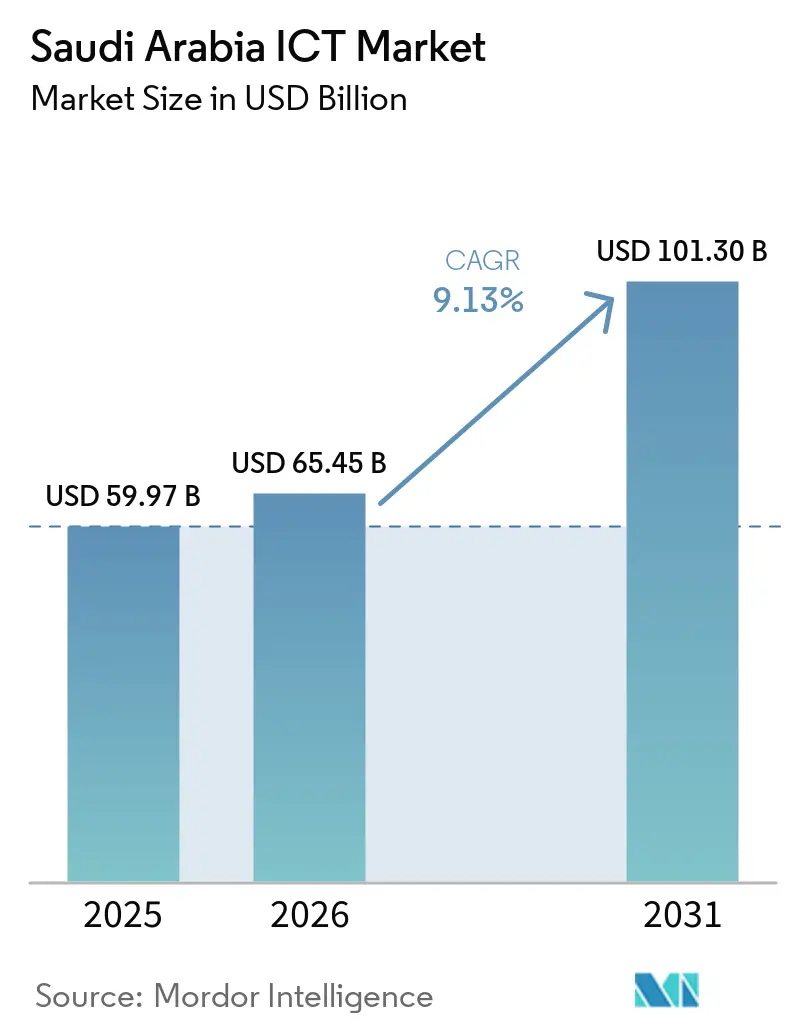

| Base Year Market Size (2025) | USD 59.97 Billion |

| Market Size (2026) | USD 65.45 Billion |

| Market Size (2031) | USD 101.30 Billion |

| Growth Rate (2026 - 2031) | 9.13% CAGR |

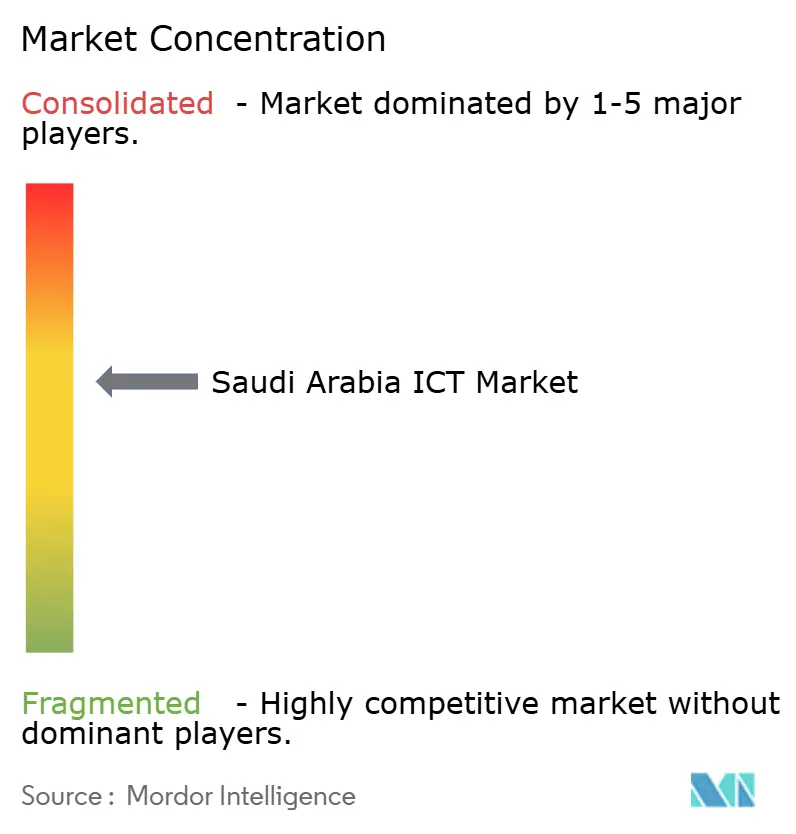

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia ICT Market Analysis by Mordor Intelligence

The Saudi Arabia ICT market size was valued at USD 59.97 billion in 2025 and estimated to grow from USD 65.45 billion in 2026 to reach USD 101.3 billion by 2031, at a CAGR of 9.13% during the forecast period (2026-2031). Vision 2030’s digital-first mandate, sovereign-cloud regulations, and hyperscale investments underpin this expansion, while 5G rollouts, public-sector e-government projects, and mega-projects such as NEOM sustain long-term demand. Cloud deployments already handle close to one-half of enterprise workloads, and data-center capacity is rising as CST imposes strict data-residency rules that carry fines up to SAR 25 million for non-compliance. Meanwhile, talent shortages and local-content rules act as speed bumps, but large-scale upskilling programs and managed-service outsourcing temper the impact. Competitive intensity is increasing as hyperscalers, telecom incumbents, and AI start-ups converge on software-defined services, reshaping revenue pools across the Saudi Arabia ICT market.

Key Report Takeaways

- By type, telecommunication services led with 31.78% of Saudi Arabia ICT market share in 2025; IT Software is projected to expand at a 9.53% CAGR through 2031.

- By end-user enterprise size, large enterprises accounted for 70.62% of the Saudi Arabia ICT market size in 2025, while SMEs record the highest projected CAGR at 10.58% through 2031.

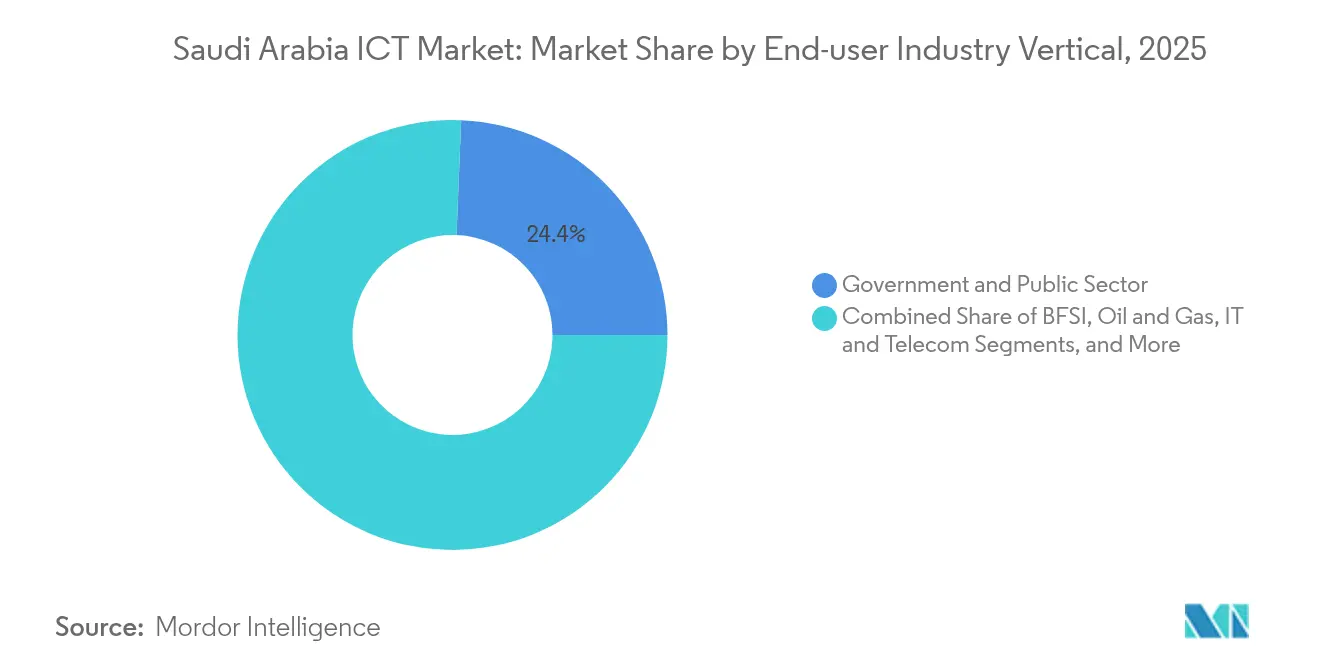

- By end-user industry vertical, government and public sector captured 24.36% share in 2025; Healthcare is advancing at a 13.45% CAGR to 2031.

- By deployment model, cloud captured 43.43% share of the Saudi Arabia ICT market size in 2025 and is forecast to grow at 14.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 public-sector digitization | +2.8% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| 5G network rollout and monetization | +2.1% | Major urban centers | Short term (≤ 2 years) |

| Accelerated cloud and SaaS adoption by SMEs | +1.9% | Industrial cities nationwide | Medium term (2-4 years) |

| IoT-enabled industrial modernization | +1.4% | Eastern Province, expanding nationwide | Long term (≥ 4 years) |

| NEOM and giga-projects’ hyperscale demand | +0.7% | Northwestern regions, national spillover | Long term (≥ 4 years) |

| Sovereign-cloud mandates | +0.3% | Riyadh and Dammam data-center hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Public-Sector Digitization Programs

Saudi Arabia’s climb to 4th in the UN Digital Services Index illustrates rapid e-government progress, with agencies targeting 90% uptake of premium services by 2025 [1]Saudi Press Agency. "Saudi Arabia Attends Preparatory Meeting for World Telecommunication Development Conference." April 17, 2025.. This public-sector push is the single largest catalyst for the Saudi Arabia IT services market. Platforms ranging from blockchain-based identities to AI chatbots drive steady demand for software, sovereign cloud, and cybersecurity. Unified charging-port rules effective 2025 likewise showcase how regulation can immediately redirect ICT spending, saving consumers SAR 170 million (USD 45.3 million) annually while cutting 2.2 million e-waste units [2]Communications, Space & Technology Commission. "Communications, Space & Technology Commission." Accessed February 15, 2025. . Vendors that align with mandated standards secure long-term contracts, reinforce interoperability, and influence procurement norms across the Saudi Arabia ICT market.

5G Network Rollout and Subscriber Monetization

stc Group, Mobily, and Zain KSA collectively lit up nationwide 5G, enabling premium consumer plans and private-network solutions for factories, ports, and energy fields. stc’s brand value reached USD 16.1 billion in 2024, reflecting strong 5G monetization. Spectrum auctions, 60% foreign-ownership caps, and infrastructure-sharing rules keep deployment costs manageable, while edge-computing nodes and slicing APIs open new enterprise revenue. Saudi Arabia’s telecom revenue base is now forecast to hit USD 22.22 billion by 2029, largely on 5G-linked services.

NEOM and Giga-Projects’ Hyperscale Demand

The USD 20 billion DataVolt-Supermicro agreement for AI data centers in NEOM represents the single largest ICT infrastructure order ever booked in the Kingdom. LEAP 2025 alone unveiled USD 20 billion in fresh AI commitments, spurring orders for liquid-cooling racks, edge fabrics, and quantum-grade security modules. Submarine cables and regional IX points follow, feeding workloads into Riyadh and Eastern Province data hubs. Domestic telecoms have responded; Mobily earmarked USD 905 million for cables and campuses, while stc lifted its data-center outlay to USD 266 million.

Accelerated Cloud and SaaS Adoption by SMEs

SMEs long underserved by enterprise IT become the fastest-growing buying group as sovereign cloud and Vision 2030 grants cut cost and complexity. Google’s new cloud region in Dammam trims latency and satisfies data-residency rules, making SaaS viable even for micro-retailers. Government programs subsidize migration assessments and offer tax credits on software spend. stc reported engagements with 665 SMEs in 2023, illustrating rising traction for marketplace bundles that package IaaS, cyber tools, and finance software. The pattern widens the revenue base for the Saudi Arabia ICT market, reducing over-reliance on oil-and-gas majors.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced ICT talent shortage and Saudization | -1.8% | Acute in Riyadh and Eastern Province | Long term (≥ 4 years) |

| Cyber-security skills deficit | -1.2% | Highest in finance and government sectors | Medium term (2-4 years) |

| Local-content hosting rules | -0.9% | Nationwide | Medium term (2-4 years) |

| Hardware supply-chain volatility | -0.6% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Advanced ICT Talent and Saudization Gap

A 20% talent gap persists in security operations, AI engineering, and cloud architecture, inflating project costs and timelines. Korn Ferry estimates wage inflows of USD 33.6 billion by 2030 as companies outbid each other for scarce skills. Saudization rules require local headcount, yet only 18.6% of private-sector IT posts are held by nationals, forcing heavy spend on academies and managed services. The National Cybersecurity Authority now demands in-house Saudi expertise for all critical-infrastructure audits, driving urgent but slow upskilling programs.

Local-Content and Hosting Rules Limiting Foreign Cloud Entrants

CST’s Essential Cybersecurity Controls lock sensitive workloads inside Saudi borders and levy fines up to SAR 25 million (USD 6.6 million) for breaches. International providers must invest in domestic facilities, perform security audits locally, and commit to knowledge transfer. While the measures spur data-center construction, they also elongate time-to-market for newcomers and limit feature rollouts pending certification. The net effect tempers competitive pricing pressure within the Saudi Arabia ICT market, preserving margins for incumbent players but potentially slowing innovation cadence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Acceleration Drives Diversification

Telecommunication Services retained 31.78% Saudi Arabia ICT market share in 2025 as 5G subscriber monetization ramped. Yet IT Software leads growth at 9.53% CAGR, supported by SDAIA’s effort to train 20,000 AI specialists and Vision 2030’s goal of USD 135.2–235.2 billion GDP uplift from AI. Enterprise application suites, middleware, and security stacks displace proprietary hardware, while SaaS models unlock cash-flow advantages for SMEs. The Saudi Arabia ICT market size attributable to software platforms is forecast to nearly double by 2030 as organizations modernize legacy stacks and meet cybersecurity mandates. Hardware demand remains steady for edge routers and data-center builds, but value is shifting to orchestration layers, APIs, and analytics engines.

Meanwhile, end-user device vendors tackle the 2025 USB-C deadline that standardizes charging ports, trimming SKU complexity yet pushing firmware redesigns. Network-equipment orders mirror 5G rollout phases and metro fiber densification. Managed IT services flourish because customers outsource technical debt remediation to system integrators that can guarantee compliance and uptime. As such, software’s rising share rebalances vendor revenue models away from capex-heavy, low-margin hardware toward subscription-led recurring streams across the Saudi Arabia ICT market.

By End-user Enterprise Size: SME Digitization Momentum

Large Enterprises commanded 70.62% of Saudi Arabia ICT market size in 2025 owing to multi-billion-dollar budgets in oil, gas, and public administration. However, SMEs exhibit a 10.58% CAGR through 2031, rapidly narrowing the digital-gap. Fiscal incentives, low-touch SaaS provisioning, and pay-as-you-grow cloud bundles pull micro-retailers and manufacturing clusters into formal ICT consumption. Google’s AI hub near Dammam specifically tailors language models and analytics to Arabic SME workflows, compressing deployment cycles and cost.

Large-cap entities such as Saudi Aramco still anchor spend with AI-driven field optimization and mega data-lake initiatives. Yet their procurement cycles favor mature vendors able to meet Tier-IV uptime and stringent national-security criteria. Conversely, SMEs tolerate standard SLAs but demand local payment gateways and Arabic interfaces, a niche now addressed by emerging start-ups. The two-tier dynamic balances stability and growth in the Saudi Arabia ICT market, fostering diversified revenue portfolios for service providers.

By End-user Industry Vertical: Healthcare Digital Transformation

Government and Public Sector represented 24.36% Saudi Arabia ICT market share in 2025 on the back of e-services, smart-card IDs, and national cloud contracts. Healthcare posts the fastest 13.45% CAGR, catalyzed by Seha Virtual Hospital, which handled 255,765 patients via teleconsultations, and the Sehhaty app’s 1.6 million sessions. Electronic medical records, AI triage engines, and wearables integrate into a secured, sovereign cloud that satisfies patient-data mandates.

BFSI drives security-tech uptake as open-banking and instant-payment platforms go live. Oil and Gas continues heavy spend on IIoT sensors, predictive analytics, and digital twins Aramco attributes a 15% output lift at Khurais to such systems. Retail and E-commerce adds omnichannel engines and last-mile robotics. Collectively, these verticals diversify demand streams, buffering the Saudi Arabia ICT market against sector-specific shocks.

By Deployment Model: Cloud Sovereignty Drives Growth

Cloud captured 43.43% of Saudi Arabia ICT market size in 2025 and is projected to grow at 14.16% CAGR, propelled by AWS’s USD 5.3 billion build and Equinix’s USD 1 billion interconnection hub. Sovereign cloud rules require critical workloads to stay in-country, aligning hyperscaler roadmaps with telecom landlords who offer power, land, and government relations. Hybrid architectures emerge as the default for regulated sectors, combining on-premise appliances for secret data tiers with burst-to-cloud economics for AI training.

On-premise remains indispensable in defense and central-bank cores, where air-gapped resilience trumps cost. Meanwhile, edge mini-clouds proliferate in factories and wind farms, keeping latency-sensitive analytics local while syncing summaries to regional data lakes. Tencent Cloud’s USD 150 million commitment affirms foreign appetite despite compliance hurdles, broadening service choice and pressuring prices across the Saudi Arabia ICT market.

Geography Analysis

Riyadh dominates spending and policy formulation, housing ministries, regulators, and most headquarters. Major banks, oil majors, and government cloud nodes cluster here, ensuring a baseline of high-bandwidth connectivity and continuous ICT procurement cycles. The capital’s data-center footprint now exceeds 250 MW, with additional campuses under construction as sovereign-cloud mandates intensify capacity needs.

The Eastern Province leverages industrial heft refineries, petrochem, and logistics to accelerate IIoT deployments. Google’s Dammam region cuts latency for factory-floor AI, while edge gateways tie into 5G private networks at Jubail and Ras Al-Khair ports. Supply-chain modernization across Dhahran and Al-Khobar introduces blockchain tracking and predictive-maintenance dashboards, widening addressable spend within the Saudi Arabia ICT market.

NEOM’s northwestern zone forms an emerging tech corridor that will host the Kingdom’s largest AI compute clusters, powered by renewables and sea-water cooling. DataVolt’s hyperscale campus seeds a regional mesh connecting submarine cables landing on Red Sea shores to Riyadh cores. Government offers unified licenses to expedite spectrum and fiber build-outs, attracting start-ups and global vendors chasing first-mover advantage. Together, these geographies position the Saudi Arabia ICT market as a central hub for MENA digital traffic while balancing growth across regions.

Competitive Landscape

Three incumbent telcos stc Group, Mobily, and Zain KSA control last-mile access and most towers, yet cloud hyperscalers and AI start-ups erode traditional silos. stc reinforces its moat via USD 266 million mega-data-center builds and minority stakes in fintech and gaming studios, seeking cross-sell synergies. Mobily’s USD 905 million undersea-cable push adds wholesale bandwidth and enterprise interconnects, diversifying away from consumer ARPU volatility. Zain KSA upgrades 5G Standalone to carve private-network niches in oil fields and smart cities, leveraging recent spectrum refarming.

Regulatory compliance stands out as a differentiator. Firms with Tier-III+ facilities certified by CST and the National Cybersecurity Authority enjoy fast-track procurement. Domestic integrators partner with global vendors to navigate localization rules e.g., Alat (PIF’s tech manufacturing arm) aims to domestically assemble servers for hyperscalers, lowering import dependency. SaaS specialists focusing on Arabic NLP, health informatics, and fintech APIs fill white spaces, often incubated through Vision 2030 funds.

Investment flows mirror strategic priorities. PIF dedicates USD 100 billion to advanced-tech plays through Alat, while venture-capital funds target AI diagnostics, OT-security software, and supply-chain SaaS. The inflow of foreign direct investment from AWS, Google, Tencent, and Equinix intensifies competition but also widens the partner ecosystem, raising the capability ceiling across the Saudi Arabia ICT market.

Saudi Arabia ICT Industry Leaders

-

IBM Corporation

-

DELL Technologies INC.

-

Palo Alto Networks Inc.

-

Amazon Web Services Inc. (AMAZON.COM INC.)

-

NYBL MIDDLE EAST FZ‑LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DataVolt signed a USD 20 billion deal with Supermicro for AI data centers in NEOM.

- February 2025: Tencent Cloud committed USD 150 million to launch Saudi operations with local data centers.

- October 2024: The Public Investment Fund and Google agreed to build an AI hub near Dammam to support SME cloud adoption.

- March 2024: AWS pledged USD 5.3 billion for Saudi data-center infrastructure with 2026 go-live.

Saudi Arabia ICT Market Report Scope

Information and Communication Technologies or ICT is a broader term for Information Technology (IT). It refers to all communication technologies, such as wireless networks, the internet, computers, cell phones, software, videoconferencing, middleware, social networking, and other media applications and services enabling users to store, access, transmit, retrieve, and manipulate information in a digital form.

The Saudi Arabia ICT market is segmented by type (hardware, software, IT services, and telecommunication services), size of the enterprise (small and medium Enterprise and large enterprises), industry vertical (BFSI, IT and telecom, government, retail and E-commerce, manufacturing, and energy and utilities), and geography (North, East, West, South). The market size and forecasts regarding value (USD) are provided for all the above segments.

By Type

| Hardware | Data-center Hardware |

| Networking Equipment | |

| End-user Devices | |

| Software | Enterprise Applications |

| Operating Systems and Middleware | |

| Security Software | |

| IT Services | Managed Services |

| Professional and Consulting Services | |

| Telecommunication Services |

By End-user Enterprise Size

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

By End-user Industry Vertical

| BFSI |

| Government and Public Sector |

| Oil and Gas |

| IT and Telecom |

| Retail and E-commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare |

| Other End-user Industry Vertical (Transportation, Education, Hospitality) |

By Deployment Model

| On-premise |

| Cloud |

| Hybrid |

| By Type | Hardware | Data-center Hardware |

| Networking Equipment | ||

| End-user Devices | ||

| Software | Enterprise Applications | |

| Operating Systems and Middleware | ||

| Security Software | ||

| IT Services | Managed Services | |

| Professional and Consulting Services | ||

| Telecommunication Services | ||

| By End-user Enterprise Size | Small and Medium-sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By End-user Industry Vertical | BFSI | |

| Government and Public Sector | ||

| Oil and Gas | ||

| IT and Telecom | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Healthcare | ||

| Other End-user Industry Vertical (Transportation, Education, Hospitality) | ||

| By Deployment Model | On-premise | |

| Cloud | ||

| Hybrid | ||

Key Questions Answered in the Report

How big is the Saudi Arabia ICT market in 2026?

The Saudi Arabia ICT market size is USD 65.45 billion in 2026 and is forecast to grow at a 9.13% CAGR to 2031.

Which segment grows fastest between 2026 and 2031?

IT Software leads expansion with a 9.53% CAGR, driven by cloud, AI, and cybersecurity deployments.

Why are SMEs important for ICT demand?

SMEs show a 10.58% CAGR because Vision 2030 incentives and new cloud regions reduce cost and complexity for small businesses.

How do sovereign-cloud rules affect foreign providers?

CST mandates local data hosting for critical workloads, so hyperscalers must build domestic data centers and pass cybersecurity audits.

What role does NEOM play in ICT spending?

NEOM’s USD 20 billion AI data-center build is the Kingdom’s largest single ICT investment, boosting demand for hyperscale infrastructure and edge connectivity.

Page last updated on: