Saudi Arabia Managed Security Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

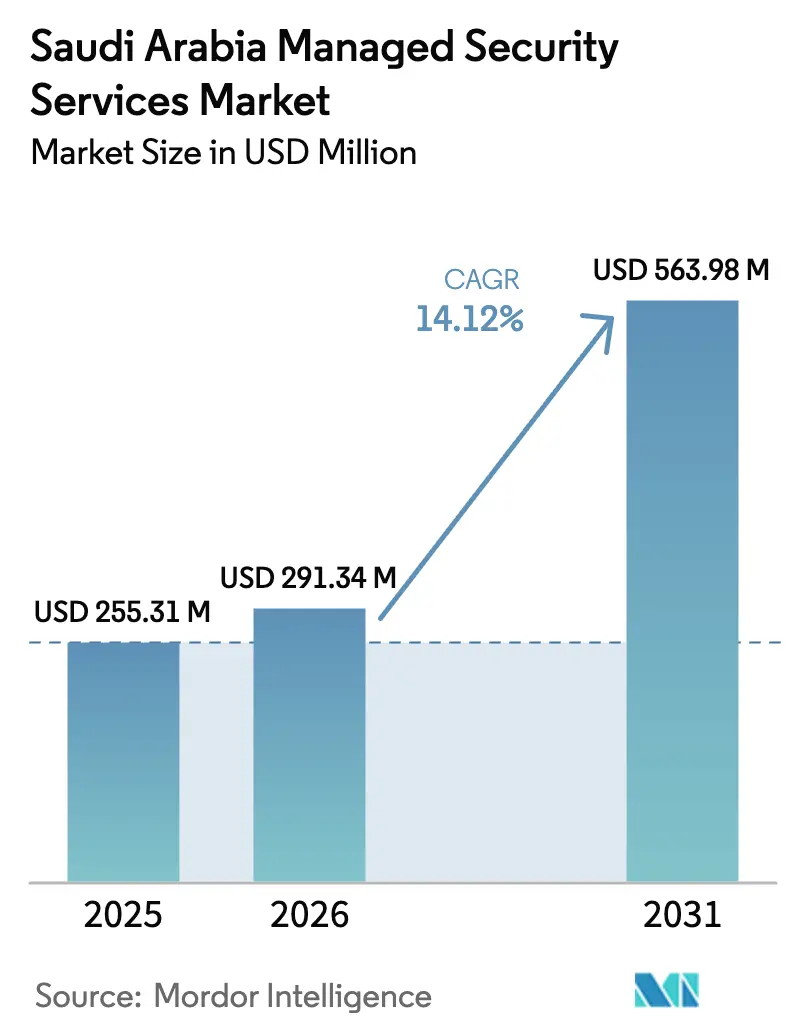

| Base Year Market Size (2025) | USD 255.31 Million |

| Market Size (2026) | USD 291.34 Million |

| Market Size (2031) | USD 563.98 Million |

| Growth Rate (2026 - 2031) | 14.12% CAGR |

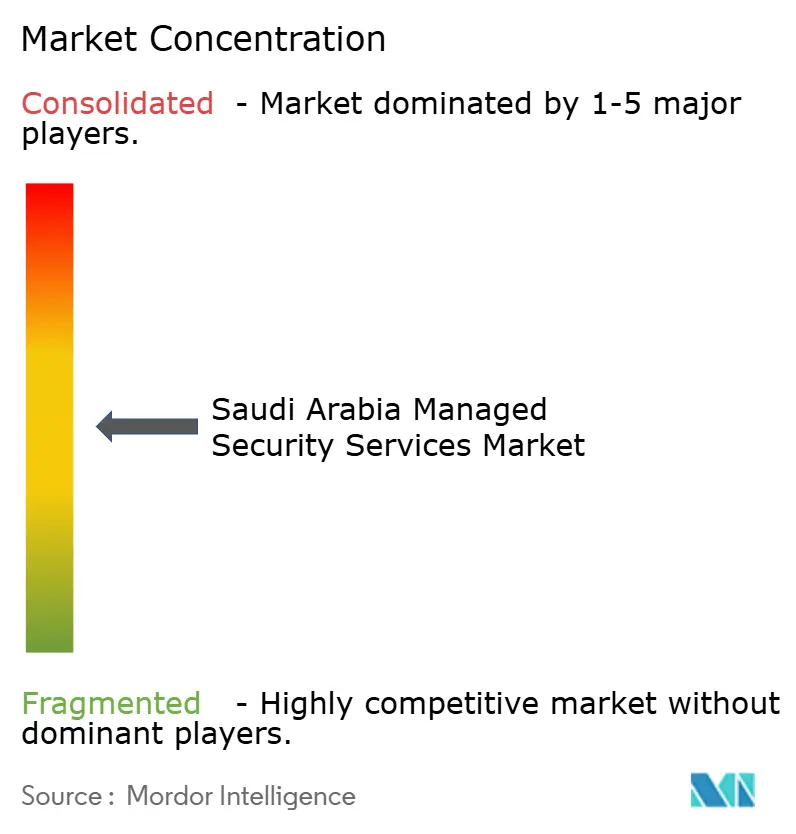

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Managed Security Services Market Analysis by Mordor Intelligence

The Saudi Arabia managed security services market size is expected to grow from USD 255.31 million in 2025 to USD 291.34 million in 2026 and is forecast to reach USD 563.98 million by 2031 at 14.12% CAGR over 2026-2031. Mandatory compliance with the National Cybersecurity Authority’s Essential Cybersecurity Controls 2024 (ECC-2), hyper-scale cloud investments exceeding USD 11 billion, and fast-tracking of Vision 2030 digital projects are the primary demand catalysts. Rapid rollout of Operational Technology Cybersecurity Controls (OTCC) across energy and industrial zones, combined with the Kingdom’s USD 40 billion AI program, has enlarged the national attack surface and moved buyers toward outsourced, 24x7 threat-hunting models. Data-residency mandates under the Personal Data Protection Law (PDPL) now favour providers with local infrastructure, while a domestic talent shortage is elevating managed security services to a board-level procurement priority. Competitive intensity is rising as global vendors open Riyadh bases to meet localization rules and to align with the cloud-first policy. [1]Amazon Web Services, “AWS to Launch an Infrastructure Region in the Kingdom of Saudi Arabia,” press.aboutamazon.com

Key Report Takeaways

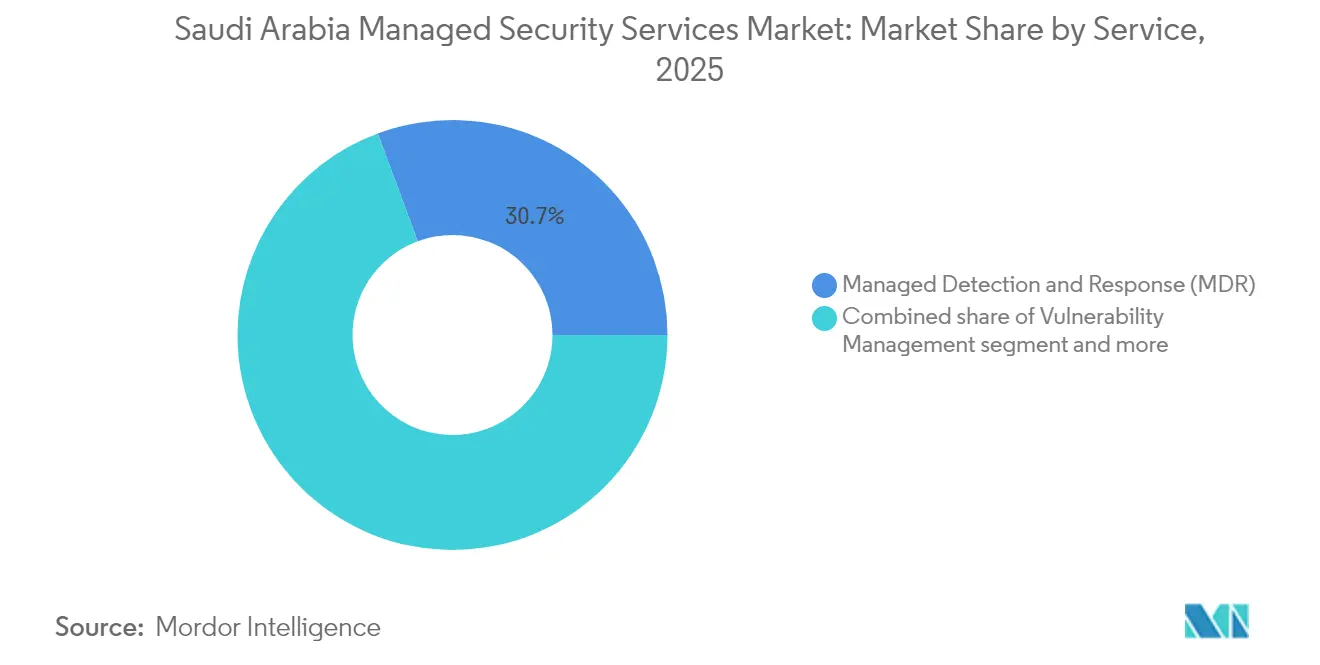

- By service, Managed Detection and Response captured 30.65% of Saudi Arabia managed security services market share in 2025 and is projected to grow at a 21.36% CAGR to 2031.

- By enterprise size, large enterprises held 63.40% of the Saudi Arabia managed security services market share in 2025; SMEs record the fastest CAGR at 18.22% through 2031.

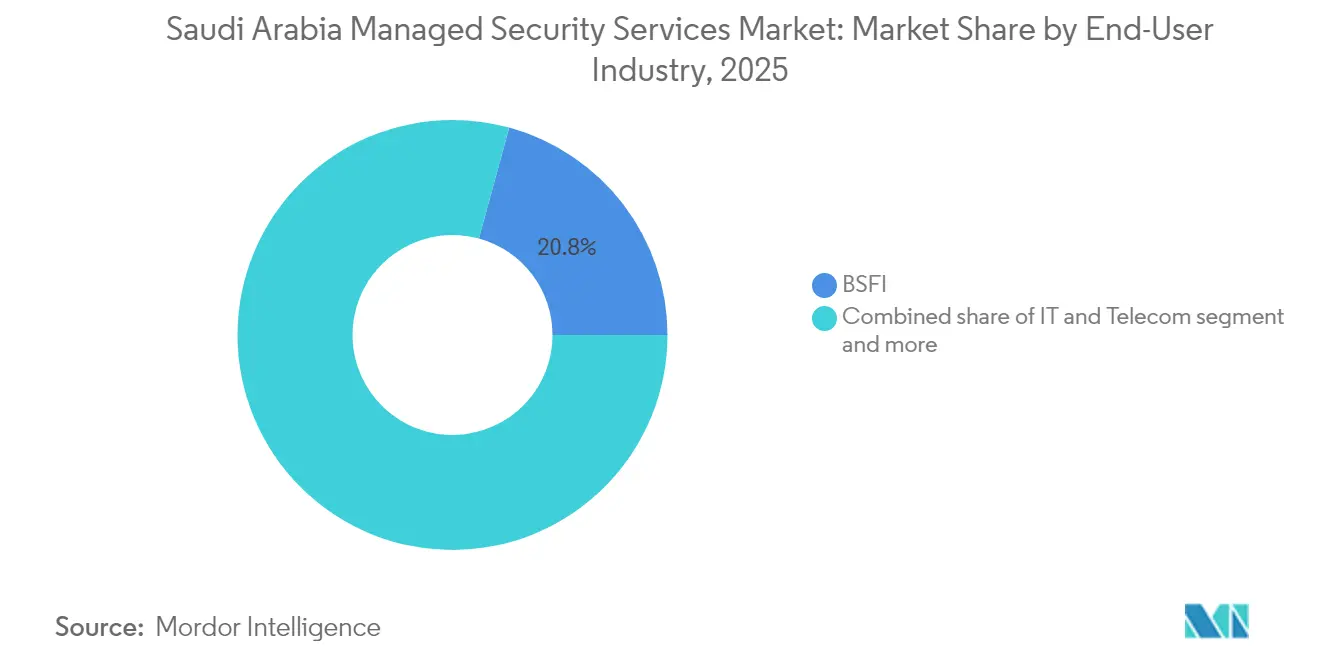

- By end-user industry, BFSI led with 20.75% revenue share in 2025, while retail and e-commerce are forecast to expand at a 18.86% CAGR to 2031.

- By delivery mode, cloud-based solutions accounted for 55.20% of the Saudi Arabia managed security services market size in 2025 and are advancing at a 22.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Managed Security Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanded attack surface from Vision 2030 digital-economy projects | 3.20% | National, with concentration in Riyadh, Jeddah, and NEOM | Medium term (2-4 years) |

| Mandatory NCA ECC-2 localization and Saudization quotas | 2.80% | National, affecting all sectors | Short term (≤ 2 years) |

| Hyper-growth of cloud SOC build-outs by telcos and hyperscalers | 2.10% | National, with primary hubs in Riyadh and Jeddah | Medium term (2-4 years) |

| Surge in OT-security spend across energy and industrial clusters | 1.90% | Eastern Province, Jubail, and Yanbu industrial cities | Long term (≥ 4 years) |

| AI-driven analytics reducing SOC false-positive cost burden | 1.50% | National, with early adoption in large enterprises | Short term (≤ 2 years) |

| Hyperscaler data center investments creating local infrastructure demand | 1.20% | Riyadh, Jeddah, with expansion to secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanded Attack Surface from Vision 2030 Digital-Economy Projects

The Vision 2030 portfolio—ranging from NEOM’s cognitive city to the National Gaming and Esports Strategy—connects millions of new endpoints that require continuous monitoring. Tonomus has already deployed AI engines in NEOM capable of inspecting millions of security events per second, illustrating the volume of telemetry flowing into Security Operations Centers. Each digital initiative is tightly inter-linked, so a breach propagates laterally, incentivizing enterprises to outsource detection and response functions to providers with extended attack-surface visibility. [2]NEOM, “Changing the Future of Technology & Digital,” neom.com

Mandatory NCA ECC-2 Localization and Saudization Quotas

ECC-2, released in 2024, cuts the number of controls to 108 but imposes Saudization for every cybersecurity role. Companies unable to source local analysts are turning to managed security services that already meet localization checks. Providers boasting ≥70% Saudi headcount now command premium rates, whereas foreign-staffed firms face prolonged licensing cycles.

Hyper-Growth of Cloud SOC Buildouts by Telcos and Hyperscalers

AWS’s USD 5.3 billion Riyadh region and Microsoft’s trio of data-center campuses have removed latency barriers and supplied sovereign-cloud zones for security log storage. STC Group’s sirar subsidiary is pairing its telecom backbone with these facilities to stand up cloud-native SOCs, giving buyers an on-shore, low-latency alternative to offshore monitoring.

Surge in OT-Security Spend Across Energy and Industrial Clusters

The OTCC framework now covers refineries, petrochemical plants and desalination units. Aramco’s Eye on AI program adds advanced analytics to industrial control systems, triggering demand for OT-specific threat modelling and managed incident response. Service providers with energy domain expertise can charge higher premiums and enjoy longer contract tenures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortfall of 6,000 qualified cyber analysts despite Saudization | -2.10% | National, with acute shortages in Riyadh and Eastern Province | Medium term (2-4 years) |

| Hidden cost of data-residency mandates on foreign MSSPs | -1.80% | National, affecting international service providers | Short term (≤ 2 years) |

| Fragmented compliance overlap (ECC-2, OTCC, SCyWF) raising onboarding friction | -1.30% | National, with complexity varying by sector | Long term (≥ 4 years) |

| High implementation costs constraining SME adoption rates | -1.00% | National, with greater impact in secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortfall of 6,000 Qualified Cyber Analysts Despite Saudization

IBM’s Himmah program will train 200 professionals a year, but total vacancies exceed 6,000, creating wage inflation and leaving many SOC seats unfilled. Outsourced models therefore shift from optional to mandatory for enterprises lacking bench strength.

Hidden Cost of Data-Residency Mandates on Foreign MSSPs

PDPL Standard Contractual Clauses require onshore processing or encrypted “data embassy” hosting, which adds localization capex of about 15% to a foreign provider’s first-year budget. Native firms with in-Kingdom data centers face no such uplift, gaining price and compliance advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: MDR Dominance Drives Market Evolution

MDR held 30.65% of the Saudi Arabia managed security services market share in 2025. The segment is forecast to expand at 21.36% CAGR as enterprises migrate from log aggregation to active threat hunting. Saudi Arabia managed security services market size for MDR is projected to reach USD 249.8 million by 2031, driven by the new Managed Security Operations Centre licensing regime.

Steady SIEM demand stems from continuous-monitoring clauses in ECC-2, while managed IAM rises with zero-trust adoption in BFSI. Vulnerability management remains compliance-driven, yet cloud-security posture management shows early momentum as multi-cloud estates proliferate. Providers increasingly bundle these functions into unified service portals, enabling cross-selling.

By Enterprise Size: SME Acceleration Reshapes Market Dynamics

Large enterprises commanded 63.40% revenue in 2025 by virtue of complex regulatory obligations and bigger threat surfaces. Saudi Arabia managed security services market size attributable to this tier is expected to expand at 11.74% CAGR through 2031.

SMEs, however, are the volume growth engine, posting an 18.22% CAGR as cloud-SOC platforms lower entry costs. Monsha’at data show 1.3 million registered SMEs at end-2024, each newly subject to PDPL audits. Consumption-based pricing and packaged incident-response retainers align with SME cash-flow profiles, accelerating adoption.

By End-User Industry: BFSI Leadership with Retail Disruption

BFSI secured 20.75% market share in 2025, underpinned by central-bank mandates for AI-based fraud analytics and 24x7 monitoring. Saudi Arabia managed security services market share within BFSI is expected to remain above 20% through 2031 as banks expand Open Banking APIs.

Retail and e-commerce are the fastest climber at 18.86% CAGR. A 34% year-on-year rise in online transactions in 2024 has heightened payment-data theft risk, steering merchants to cloud-based SOC subscriptions. Construction mega-projects such as The Line require integrated physical-cyber monitoring, adding diverse demand pockets.

By Delivery Mode: Cloud-First Policy Accelerates Transformation

Cloud-based offerings captured 55.20% revenue in 2025 and are projected to grow at a 22.02% CAGR, reflecting the sovereign-cloud narrative and hyperscaler roll-outs. Saudi Arabia managed security services market size for cloud delivery could top USD 464.6 million by 2031 as additional regions from Tencent Cloud and Oracle go live.

Hybrid models persist in public sector entities balancing on-prem and cloud workloads, while pure on-prem services show single-digit growth limited to critical infrastructure. The Cloud Computing Special Economic Zone’s tax incentives further tilt new deployments toward cloud resilience architectures.

Geography Analysis

Riyadh anchors demand at federal ministries, telco HQs and financial regulators, accounting for an estimated 42.60% of Saudi Arabia managed security services market revenue in 2025. Jeddah follows with port, logistics and retail business. AWS’s Jeddah CloudFront edge launched in January 2025 enhances low-latency log ingest for Red Sea enterprises.

The Eastern Province hosts energy majors in Dhahran, Jubail and Yanbu. OT-centric engagements here average 20% higher deal value than IT-only contracts due to control-system complexity. DataVolt’s net-zero AI factory inside NEOM widens the geographic footprint and demands always-on SOC coverage for AI workloads.

Mega-projects spread across the northwest (NEOM), west coast (Red Sea Project) and central corridors draw global engineering firms that outsource security to comply with ECC-2 during construction. Upcoming USD 21 billion in multi-city data-center builds will decentralize log storage and create new SOC nodes, ensuring nationwide service availability.

Competitive Landscape

The market shows moderate concentration: the five largest players hold about 55% combined revenue. STC Group’s sirar leads domestic share, leveraging telecom channels and onshore cloud zones. IBM committed USD 200 million in 2024 to expand its Riyadh Cybersecurity Center, keeping pace with Palo Alto Networks, which integrated QRadar cloud analytics into its Cortex XSIAM stack in 2025.

Global entrants pair with local infrastructure owners to satisfy data-sovereignty clauses. Tencent Cloud’s USD 150 million region ride-shares with Saudi telco fiber loops to shorten deployment cycles. Energy-grade MSS is becoming a niche battleground, with SLB-Palo Alto Networks and Honeywell-Nozomi Networks alliances tailoring OT threat suppression.

AI differentiation is now central. Providers embedded large-language models into playbooks that cut false positives by 30%, lifting analyst productivity at a time of acute talent scarcity. Post-quantum encryption pilots from SEALSQ and WISeKey target future regulatory mandates, signaling new competitive vectors beyond classic SOC metrics. [4]Palo Alto Networks, “SLB and Palo Alto Networks Expand Collaboration to Strengthen Cybersecurity for the Energy Sector,” paloaltonetworks.com

Saudi Arabia Managed Security Services Industry Leaders

STC Group

International Business Machines Corporation

Cisco Systems, Inc.

Saudi Information Technology Company (SITE)

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Tencent Cloud confirmed a USD 150 million Saudi cloud region, opening H2 2025.

- February 2025: NCA issued the licensing framework for Managed Security Operations Centre services.

- February 2025: DataVolt and NEOM signed a USD 5 billion deal for a net-zero AI factory.

- January 2025: AWS activated a CloudFront Edge region in Jeddah

Saudi Arabia Managed Security Services Market Report Scope

The Saudi managed security services market is defined based on the revenues generated from the sale of various managed security services such as managed detection and response (MDR), security information and event management (SIEM), managed identity and access management (IAM), and vulnerability management, deployed in various end-user industries to manage and monitor the security aspects of the customers’ IT infrastructure in Saudi Arabia (KSA). The analysis is based on the market insights captured through secondary research and the primaries. The report also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The Saudi managed security services market is segmented by service (managed detection and response (MDR), security information and event management (SIEM), managed identity and access management (IAM), vulnerability management, other services), size of enterprises (large enterprises, small and medium-sized enterprises (SMEs)), end-user industry (IT and telecom, BFSI, retail and e-commerce, construction and real estate, government and defense, energy, oil, and gas, other end-user industries). The report offers market forecasts and size in terms of value in USD for all the above segments.

| Managed Detection and Response (MDR) |

| Security Information and Event Management (SIEM) |

| Managed Identity and Access Management (IAM) |

| Vulnerability Management |

| Other Services |

| Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) |

| IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Retail and E-commerce |

| Construction and Real Estate |

| Government and Defense |

| Energy, Oil and Gas |

| Other Industries |

| Cloud-based MSS |

| Hybrid MSS |

| On-premise MSS |

| By Service | Managed Detection and Response (MDR) |

| Security Information and Event Management (SIEM) | |

| Managed Identity and Access Management (IAM) | |

| Vulnerability Management | |

| Other Services | |

| By Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises (SMEs) | |

| By End-User Industry | IT and Telecom |

| Banking, Financial Services and Insurance (BFSI) | |

| Retail and E-commerce | |

| Construction and Real Estate | |

| Government and Defense | |

| Energy, Oil and Gas | |

| Other Industries | |

| By Delivery Mode | Cloud-based MSS |

| Hybrid MSS | |

| On-premise MSS |

Key Questions Answered in the Report

What is the current size of the Saudi Arabia managed security services market?

The market stands at USD 291.34 million in 2026.

How fast is the market growing?

Revenue is forecast to rise at a 14.12% CAGR, reaching USD 563.98 million by 2031.

Which service type leads the market?

Managed Detection and Response holds the largest share at 30.65% in 2025 and grows fastest at 21.36% CAGR.

Why are cloud-based managed security services expanding quickly?

The Kingdom’s cloud-first policy, hyperscaler data-center investments, and sovereign-cloud compliance drive a 22.02% CAGR for cloud delivery.

What regulatory changes are shaping demand?

ECC-2 Saudization quotas, PDPL data-residency rules, and OTCC standards are pushing organizations toward outsourced, compliant security operations.

How severe is the cybersecurity talent gap in Saudi Arabia?

The country lacks around 6,000 qualified analysts, making managed security services a primary solution for many firms.

Page last updated on: