Saudi Arabia Data Center Server Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

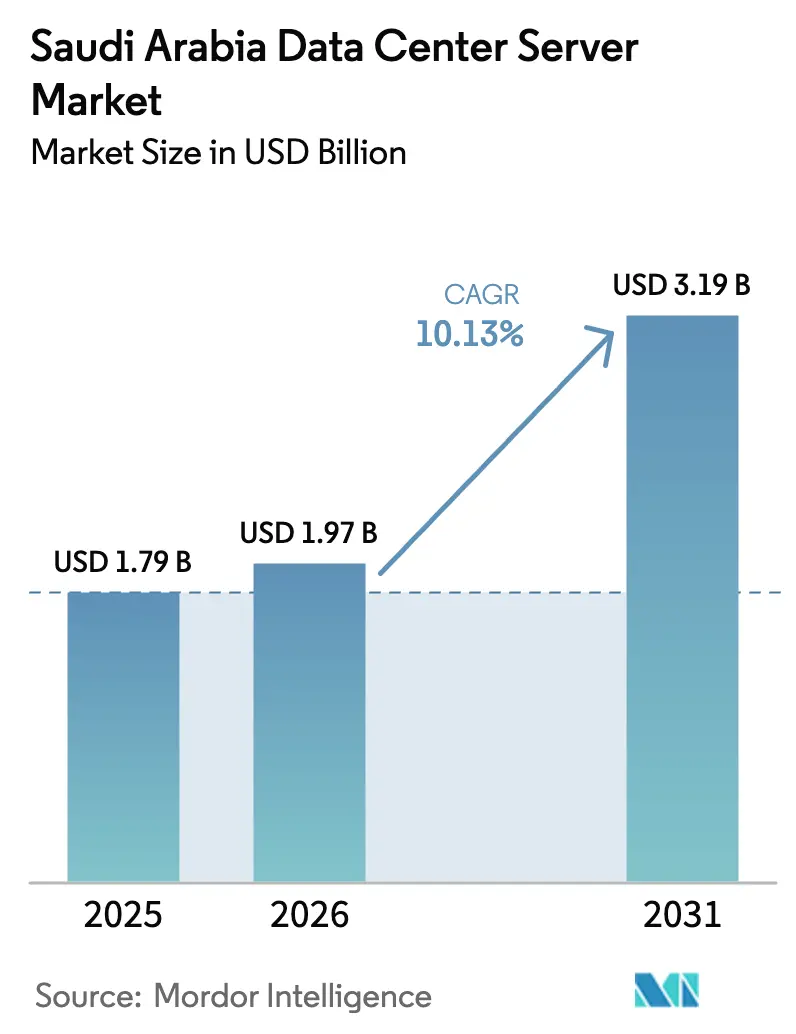

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 10.13% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Data Center Server Market Analysis by Mordor Intelligence

Saudi Arabia data center server market size in 2026 is estimated at USD 1.97 billion, growing from 2025 value of USD 1.79 billion with 2031 projections showing USD 3.19 billion, growing at 10.13% CAGR over 2026-2031. Sustained growth is anchored in Vision 2030, which positions the Kingdom as the Gulf’s digital hub; mandatory data-residency rules and large-scale hyperscale capital commitments continue to accelerate demand for locally deployed servers. Rising AI projects, sovereign cloud mandates, and green energy incentives in Special Economic Zones are combining to reshape procurement patterns toward high-density, liquid-cooled systems. Hyperscale operators that entered the market only recently are now outspending traditional telco-dominated data center operators, shifting revenue toward rack-scale GPU platforms. Meanwhile, talent shortages and supply-chain gaps for advanced cooling components temper near-term deployment velocity but do not alter the longer-term expansion outlook of the Saudi Arabia data center server market.

Key Report Takeaways

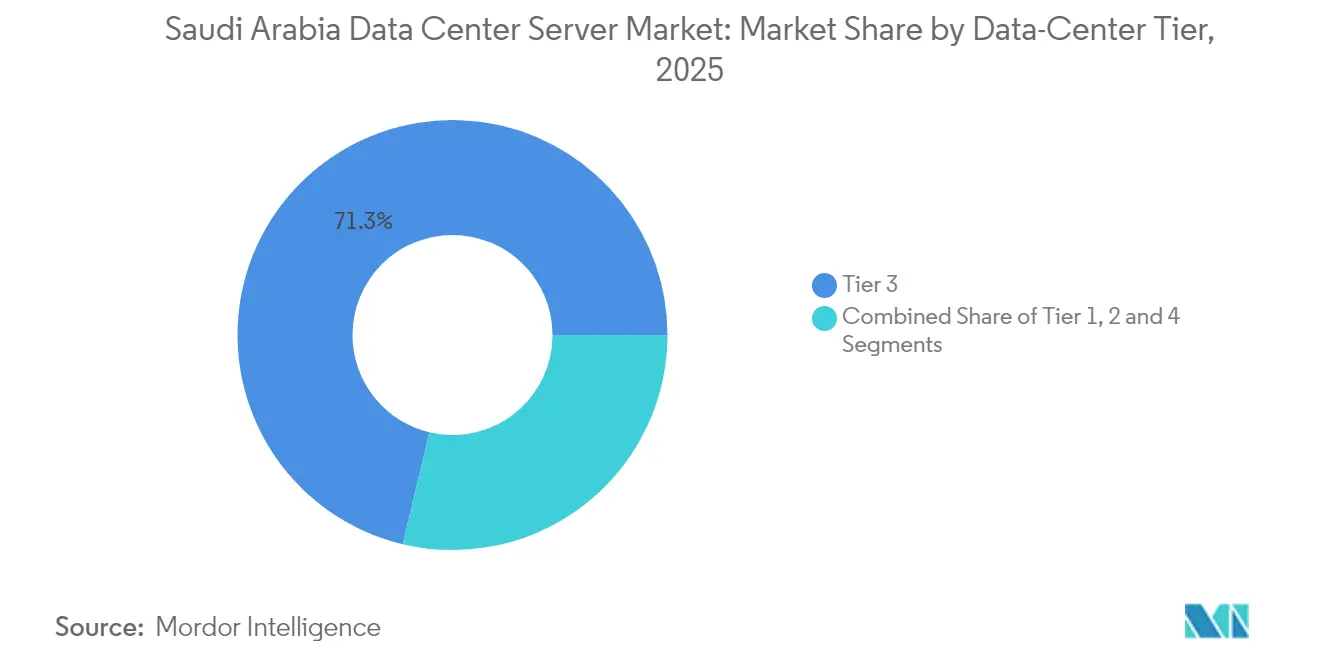

- By data-center tier, Tier 3 installations commanded 71.28% of the Saudi Arabia data center server market share in 2025; Tier 4 is the fastest-growing tier, advancing at a 12.08% CAGR.

- By form factor, half-height blades accounted for 62.74% of the Saudi Arabia data center server market size in 2025, whereas quarter-height and micro-blade servers are growing at a 10.36% CAGR.

- By application, AI/ML workloads occupied 36.42% of market revenue in 2025; virtualization and private cloud workloads show the highest forecast CAGR at 10.56% to 2031.

- By data-center type, colocation facilities led with 53.62% revenue share in 2025, while hyperscale providers are projected to expand at a 11.74% CAGR through 2031.

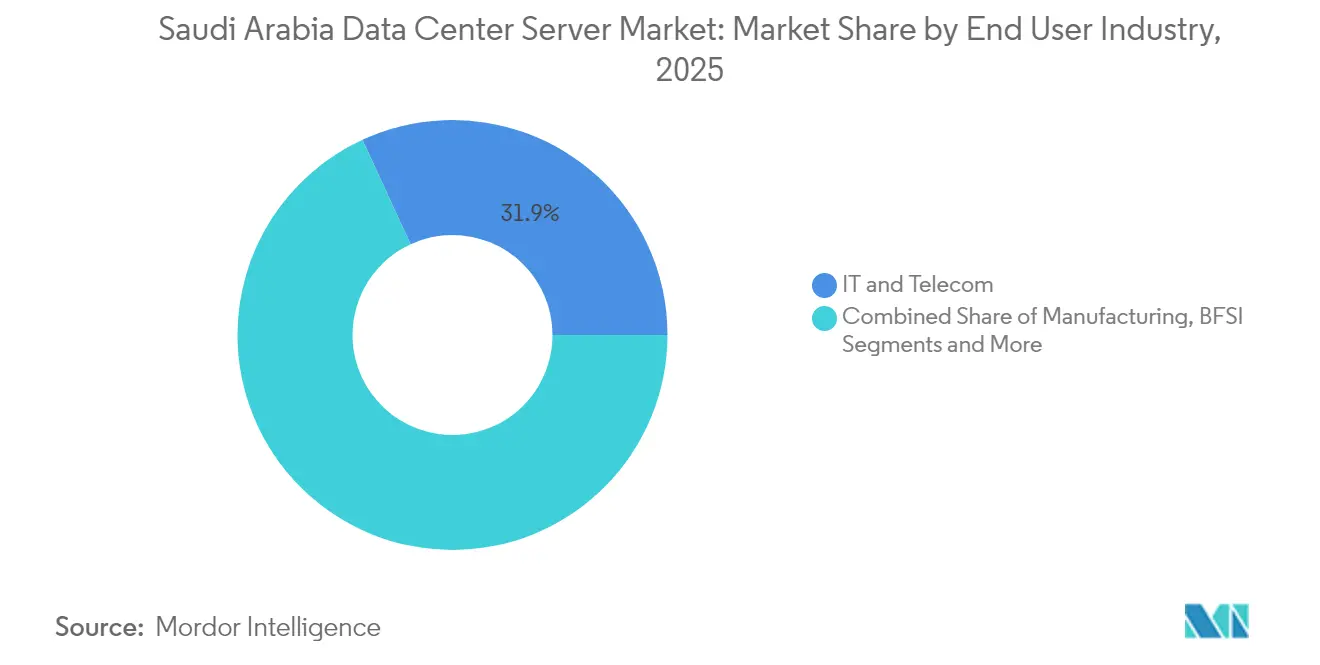

- By end-use industry, IT & telecom retained 31.88% share in 2025, while manufacturing and Industry 4.0 workloads are projected to grow at an 10.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in Saudi arabia many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide data center server market outlook by Mordor Intelligence brings these expectations together.

Saudi Arabia Data Center Server Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating hyperscale cloud provider investments | +2.8% | National, concentrated in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Government-backed digital transformation (Vision 2030 & smart cities) | +2.1% | National, with early gains in NEOM, Red Sea Project | Long term (≥ 4 years) |

| Rapid growth in 5G and IoT traffic | +1.7% | Urban centers, expanding to rural areas | Short term (≤ 2 years) |

| Rising demand for AI/ML & HPC workloads | +2.4% | National, with concentration in Riyadh tech corridors | Medium term (2-4 years) |

| Mandatory local data-residency regulations | +1.8% | National, particularly government and BFSI sectors | Short term (≤ 2 years) |

| Green-energy pricing incentives in SEZs | +0.9% | Special Economic Zones, NEOM, industrial cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Hyperscale Cloud Provider Investments

Hyperscale commitments have redrawn the capital map of the Saudi Arabia data center server market. AWS allocated USD 5.3 billion to new cloud zones, Microsoft partnered with Aramco Digital on sector-specific clouds, and Google Cloud sealed local partnerships that require rack-scale liquid-cooled GPU clusters.[1]Armada,"Aramco, Armada, and Microsoft Collaborate to Deploy World’s First Industrial Distributed Cloud," armada.aiThese deployments favor micro-blade and quarter-height architectures to maximise compute density and drive down watts-per-teraflop. Cost-recovery models centre on economies of scale, putting pressure on legacy vendor margins even as overall unit demand rises. Competitive entrance of multiple global platforms is therefore simultaneously enlarging and commoditising hardware supply.

Government-backed Digital Transformation (Vision 2030 & Smart Cities)

Vision 2030 embeds digital infrastructure across every megaproject, from NEOM’s USD 5 billion net-zero AI factory to nationwide cloud-first directives. The Saudi Data and AI Authority enforces data-sovereignty rules that guarantee steady domestic server demand. Edge nodes placed along Riyadh and Jeddah smart-traffic corridors handle high-volume camera streams and public-safety analytics, while 100,000 nationals are enrolled in government-funded ICT upskilling to staff new facilities. As a result, the Saudi Arabia data center server market now prioritises edge-hardened, renewable-powered designs that can operate in desert climates without compromising compute density. NEOM's USD 5 billion AI factory partnership with DataVolt exemplifies how megaprojects are creating demand for specialized server configurations that integrate renewable energy systems with high-performance computing clusters. [2]NEOM,' DataVolt and NEOM to develop regions first net-zero AI factory." neom.com

Rapid Growth in 5G and IoT Traffic

Telecommunications operators deploy ruggedised micro-blades to support autonomous vehicle telemetry, industrial automation, and AR/VR services that demand sub-20 ms latency. Manufacturing plants leveraging Industry 4.0 produce sensor floods that must be processed locally for predictive maintenance. The Saudi Arabia data center server market therefore sees rising demand for small-footprint, high-core-count units capable of operating in non-traditional data-hall environments.

Rising Demand for AI/ML & HPC Workloads

Sovereign AI spending shapes server configurations across the Kingdom. HUMAIN procured 18,000 NVIDIA Blackwell GPUs, while Aramco’s Dammam-7 supercomputer delivers 55.4 petaflops for reservoir simulation. New Arabic LLM initiatives require petascale clusters fitted with direct liquid cooling. Healthcare AI for imaging and BFSI AI for fraud detection intensify the need for GPU-dense servers with ultralow latency. The Saudi Arabia data center server market is consequently tilting toward power-hungry, accelerator-rich racks that necessitate facility-wide electrical and cooling upgrades.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing number of data-security breaches | -0.8% | National, particularly affecting government and BFSI sectors | Short term (≤ 2 years) |

| High CAPEX for next-gen server hardware | -1.2% | National, with greater impact on SME deployments | Medium term (2-4 years) |

| Shortage of bilingual (Arabic/English) DC talent | -0.9% | National, acute in specialized AI and HPC roles | Long term (≥ 4 years) |

| Supply-chain delays for liquid-cooling components | -0.7% | National, affecting hyperscale and AI-focused deployments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Number of Data-Security Breaches

Rising cyber incidents prompt the Saudi Arabian Monetary Authority to mandate hardware-level security modules and encrypted drives. Compliance adds 15–20% to server bill-of-materials and elongates procurement cycles because only a handful of global vendors meet EAL4+ certification thresholds.[3]Saudi Arabian Monetary Authority,"Cyber Security Framework Saudi Arabian Monetary Authority," sama.govAir-gapped configurations demanded for critical national infrastructure further swell capital outlays as redundant clusters are provisioned to maintain isolation.

High CAPEX for Next-Gen Server Hardware

GPU-accelerated nodes cost up to 5× more than legacy x86 servers. When coupled with 25–30% additional spend for liquid cooling and high-density power distribution, many firms—especially SMEs—delay refresh cycles. The pricing gap drives some enterprises toward OPEX-based public cloud, moderating direct hardware demand and affecting the slope of the Saudi Arabia data center server market growth curve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data-Center Tier: Mission-Critical Workloads Drive Tier 4 Adoption

Tier 3 facilities captured 71.28% of 2025 shipments, giving the Saudi Arabia data center server market size a dominant mid-tier profile. Enterprises appreciate concurrent maintainability without the premium of full fault tolerance. Yet Tier 4 racks, essential for AI training pipelines and high-value transactions, are growing 12.08% annually. Government policy mandating 99.995% availability for national AI services accelerates this shift. Over the forecast window, Tier 4 clusters inside hyperscale campuses and financial data centers are expected to erode the Tier 3 share as service-level agreements tighten.

Continued migration away from Tier 1 and Tier 2 is evident: legacy web-hosting workloads are being re-platformed into multitenant Tier 3 halls, while low-risk dev-test environments increasingly spin up in public cloud. The Saudi Arabia data center server industry therefore pays closer attention to future-proofing Tier 4 designs with recycled water loops and grid-interactive UPS systems that align with net-zero mandates

By Form Factor: Micro-Blades Gain Traction in Edge Deployments

Half-height blades owned 62.74% revenue in 2025, underscoring their versatility across mixed enterprise loads. Nevertheless, quarter-height and micro-blade nodes are projected to grow at 10.36% CAGR as telecom operators and smart-city integrators deploy compute at the edge. These smaller blades shorten the distance between sensor and inference, crucial for traffic analytics and industrial controls. The Saudi Arabia data center server market size for edge-class micro-blades is therefore forecast to rise alongside 5G densification.

Supermicro’s rack-scale partnership with DataVolt pairs chassis-level liquid cooling with 100 kW racks, illustrating how form-factor evolution aligns with thermal management innovation. Full-height blades remain relevant for single-server peak-performance tasks but are niche compared with density-optimised micro-blade designs.

By Application/Workload: AI/ML Leads Despite Virtualization Growth

AI/ML workloads already command 36.42% share of deployed compute in 2025. This share should persist until 2031 because sovereign AI factories and language-model research consume multi-node GPU clusters. In parallel, virtualization and private-cloud workloads expand at 10.56% CAGR as medium-sized enterprises modernise infrastructure, leveraging abstraction to boost utilisation. This dual dynamic supports stable demand across both accelerator-rich and CPU-centric SKUs, further diversifying the Saudi Arabia data center server market.

High-performance computing (HPC) remains concentrated in energy and academia, while storage-heavy archival nodes grow to satisfy regulatory retention rules.

By Data Center Type: Hyperscalers Challenge Colocation Dominance

Colocation held 53.62% share in 2025, benefiting from enterprises that want control without building proprietary sites. Hyperscale footprints, however, are rising at 11.74% CAGR as global clouds roll out kingdom-specific regions, absorbing the lion’s share of next-generation GPU orders. This evolution directly lifts the Saudi Arabia data center server market share for ODM-style white-box suppliers who cater to cloud specifications.

Enterprise and edge micro-data centers remain niche yet strategically important where latency or sovereignty prohibits shared infrastructure. Telcos now reposition their mega halls as carrier-neutral hubs, bundling managed cloud and interconnect services to fend off hyperscale encroachment.

By End-Use Industry: Manufacturing Emerges as Growth Leader

IT and telecom organisations still occupy 31.88% of 2025 shipments, but manufacturing and Industry 4.0 workloads accelerate at an 10.96% CAGR as Aramco and NEOM embed predictive maintenance, robotics, and quality-control AI. These deployments require deterministic latency and rugged design, pulling specialised server SKUs into factory floors. The Saudi Arabia data center server industry thus gains a diversified demand base, less reliant on pure IT refresh cycles.

BFSI adoption benefits from open-banking regulations and faster payment rails, spurring GPU-enabled fraud-detection clusters. Healthcare digitisation adds imaging-specific accelerators, while government and defence prioritise hardened, sovereign nodes with dedicated key-management hardware.

Geography Analysis

Riyadh anchors major share of national server-rack shipments, housing ministry data centers, fiscal headquarters, and the majority of hyperscale cloud zones. Jeddah leveraging international subsea cables and logistics-driven demand that extends into hospitality and pilgrimage-supporting smart-city projects. Dammam and the Eastern Province represent the industrial heartland, where petrochemical and energy HPC clusters run subsurface modeling and refinery optimisation simulators.

NEOM introduces a northern pole of growth with its USD 5 billion DataVolt AI factory. Once operational, this plant alone will lift the Saudi Arabia data center server market size materially, particularly for liquid-cooled GPU sleds powered by on-site renewables. Secondary cities such as Al-Khobar, Taif, and Medina begin to adopt mini-hubs as digitisation policies trickle outward, although share remains capped by limited power redundancy and talent pools.

Regional distribution is therefore evolving from a Riyadh-centric topology to a multi-hub network that aligns with submarine cable landings, industrial corridors, and smart-city clusters. This dispersion creates new edge-node opportunities, extending the Saudi Arabia data center server market into non-traditional localities.

Mordor Intelligence's coverage of the data center server market extends across other regions including Africa, North America, and Americas, while country-specific intelligence is also available for Italy, Norway, Canada, United States, Japan, and Germany, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The Saudi Arabia data center server market exhibits moderate concentration. Chinese vendors Huawei and Inspur challenge incumbents with price-competitive, vertically integrated platforms. ODM suppliers—Supermicro, Quanta, and Wiwynn—expand rapidly by fulfilling hyperscale custom SKUs, often bypassing traditional distributors.

Strategy is tilting toward verticalisation; vendors develop energy-sector-specific cabinets certified for hazardous zones, or fintech-grade blades with hardware roots-of-trust. DataVolt’s USD 20 billion order for Supermicro’s rack-scale GPU systems exemplifies this pivot, giving rise to locally headquartered system integrators capable of bridging global supply chains with compliance know-how. Meanwhile, the shortage of bilingual engineers drives joint academies between vendors and universities to safeguard future talent intake.

Regulatory uncertainty around forthcoming Global AI Hub Law may alter competitive rules by permitting “data embassies” that operate under foreign jurisdiction. Vendors able to guarantee sovereign enclaves without contravening residency law will secure differentiated positioning in the Saudi Arabia data center server market.

________________________________________

Saudi Arabia Data Center Server Industry Leaders

-

Dell Technologies

-

Hewlett Packard Enterprise

-

IBM Corporation

-

Lenovo Group Ltd

-

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Supermicro and DataVolt launched a USD 20 billion collaboration covering GPU platforms cooled via direct liquid loops and powered by renewable energy.

- May 2025: NVIDIA shipped 18,000 Blackwell GPUs to HUMAIN under a USD 10 billion AI data-center build-out targeting 500 MW capacity.

- May 2025: Qualcomm signed an MoU with HUMAIN to co-develop data-center AI silicon and announced a Riyadh design office.

- March 2025: Aramco scaled Dammam-7 to process 10 billion data points daily and partnered with Groq on an inferencing centre.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Saudi Arabia data center server market encompasses every new, factory-built rack-mount, blade, or micro-blade compute node installed within commercial colocation, hyperscale cloud, enterprise, or government facilities in the Kingdom and delivering mission-critical workloads to downstream users. Servers shipped only as part of integrated storage or networking appliances are excluded.

Scope exclusion: Refurbished or gray-market servers and micro edge sites below ten racks do not fall within this study.

Segmentation Overview

-

By Data-Center Tier

- Tier 1 and 2

- Tier 3

- Tier 4

-

By Form Factor

- Half-height Blades

- Full-height Blades

- Quarter-height / Micro-blades

-

By Application / Workload

- Virtualisation and Private Cloud

- High-Performance Computing (HPC)

- Artificial Intelligence/Machine Learning and Data Analytics

- Storage-centric

- Edge / IoT Gateways

-

By Data Center Type

- Hyperscalers/Cloud Service Provider

- Colocation Facilities

- Enterprise and Edge

-

By End-use Industry

- BFSI

- IT and Telecom

- Healthcare and Life-Sciences

- Manufacturing and Industry 4.0

- Energy and Utilities

- Government and Defence

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews with facility operators, cloud architects, and procurement heads across Riyadh, Jeddah, and Dammam validated utilization rates, refresh cycles, and price dispersion that desk sources could only approximate. Follow-up surveys with regional distributors helped us align import tallies with on-ground shipments before final triangulation.

Desk Research

Our analysts began with trade statistics from Saudi Customs and UN Comtrade that quantify x86 server imports, then overlaid local shipment splits from the Communications, Space & Technology Commission. Trend articles from Saudi Data Center Association, GCC IDC white papers, and peer-reviewed IEEE journals on hyperscale architecture helped us benchmark workload mixes. Company 10-Ks, IPO prospectuses, and investor decks disclosed capex, rack density, and average selling prices. Paid intelligence from D&B Hoovers and Dow Jones Factiva supplied recent contract values and headline project announcements. This list is illustrative, not exhaustive; many other sources informed baseline verification.

Market-Sizing & Forecasting

The top-down build starts with import-adjusted server revenue, which is reconciled against installed rack counts and typical server density to cross-check volumes. Select bottom-up roll-ups of large facility purchase orders and sampled ASP × unit data provide a reasonableness check, and gaps are prorated across segments using workload penetration and tier-mix ratios. Key variables like hyperscale capex plans, Vision 2030 project timelines, rack-power envelopes, AI/ML server ASP drift, and GDP-linked IT spend feed a multivariate regression that projects demand to 2030. ARIMA overlays capture cyclical refresh peaks.

Data Validation & Update Cycle

Before sign-off, Mordor analysts run variance screens against public capacity announcements, consult a second senior reviewer, and re-contact sources if deviations exceed preset thresholds. The dataset is refreshed annually, with interim adjustments when material events such as new cloud region launches occur.

Why Mordor's Saudi Arabia Data Center Server Baseline Commands Reliability

Published estimates often diverge because firms mix entire data center stacks, use differing currency years, or apply untested refresh assumptions.

Key gap drivers include whether storage and network hardware are bundled with servers, if hyperscale self-builds are counted in investment rather than revenue terms, and the cadence at which ASP erosion is modeled. Mordor's study reports server-only revenue in 2025 US-dollar terms and refreshes every twelve months, which reduces scope creep and currency slippage.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.79 B (2025) | Mordor Intelligence | - |

| USD 1.50 B (2024) | Regional Consultancy A | Includes electrical & mechanical infrastructure, not server-only |

| USD 0.50 B (2025) | Trade Journal B | Counts enterprise refresh orders only, excludes hyperscale imports |

| USD 4.51 B (2024) | Global Consultancy C | Values total data center market; bundles software & services |

These comparisons show that once scope, currency, and refresh cadence are aligned, Mordor's disciplined variable selection and transparent steps provide the most dependable baseline for strategic planning in the Kingdom.

Key Questions Answered in the Report

What is the current size of the Saudi Arabia data center server market?

The market is valued at USD 1.97 billion in 2026 and is projected to reach USD 3.19 billion by 2031.

Which server workload segment holds the largest share?

AI/ML workloads lead with 36.42% of 2025 revenue, driven by sovereign AI initiatives and large GPU deployments.

Which data-center tier is expanding the fastest?

Tier 4 facilities show the highest growth, advancing at a 12.08% CAGR through 2031 as fault tolerance becomes critical.

Why are micro-blade servers gaining popularity in Saudi Arabia?

Edge computing for 5G, smart-city applications, and industrial IoT demands compact, high-density form factors that micro-blades provide.

Page last updated on: