Malaysia IT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

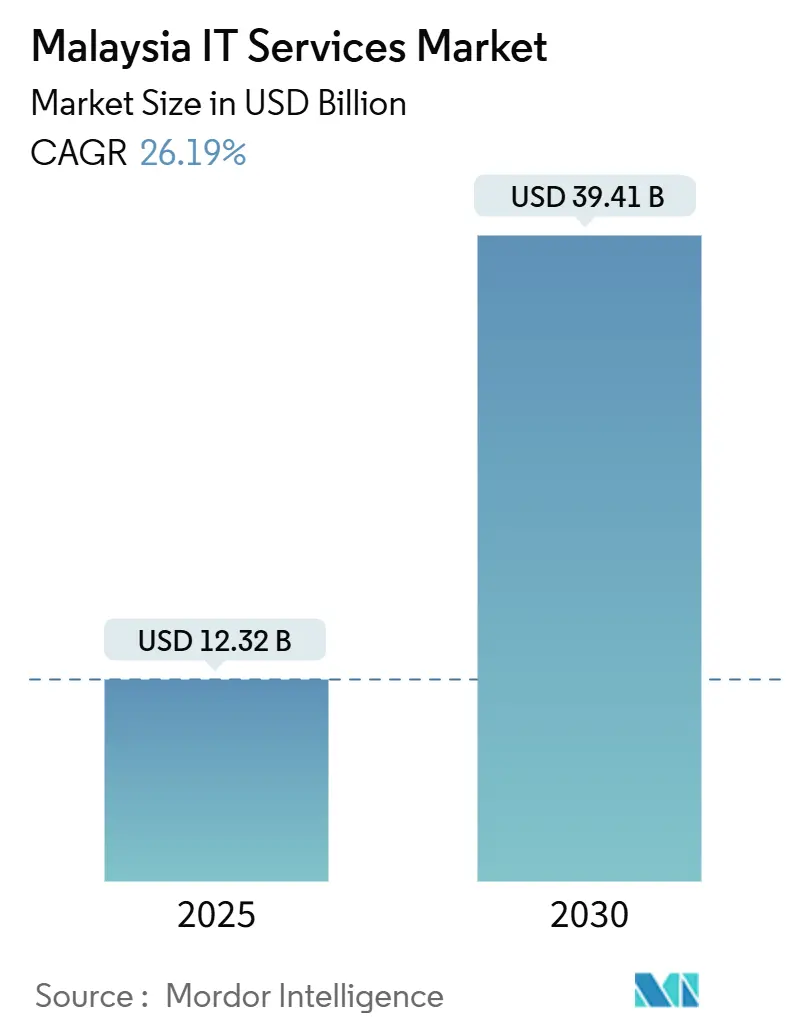

| Market Size (2025) | USD 12.32 Billion |

| Market Size (2030) | USD 39.41 Billion |

| Growth Rate (2025 - 2030) | 26.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia IT Services Market Analysis by Mordor Intelligence

The Malaysia IT services market size stands at USD12.32 billion in 2025 and is projected to touch USD39.41 billion by 2030, translating to a robust 26.19% CAGR over the forecast period. Several converging factors propel this expansion: the government’s MYR21 billion MyDIGITAL blueprint, a surge of hyperscale data-center investments, fast-tracked Islamic digital-bank launches, and expanding tax incentives under MSC Malaysia. Together, these initiatives shorten technology refresh cycles, push enterprises toward cloud-first architectures, and draw international vendors that view Malaysia as an ASEAN springboard. New ESG-reporting mandates also widen the revenue pool for carbon-accounting platforms, while bilingual Malay–Arabic talent attracts GCC outsourcing contracts that were once routed to the Gulf states. Competitive intensity is gradually tilting in favor of providers able to pair local regulatory fluency with deep cloud partnerships, raising the barrier to entry for smaller system integrators.

Key Report Takeaways

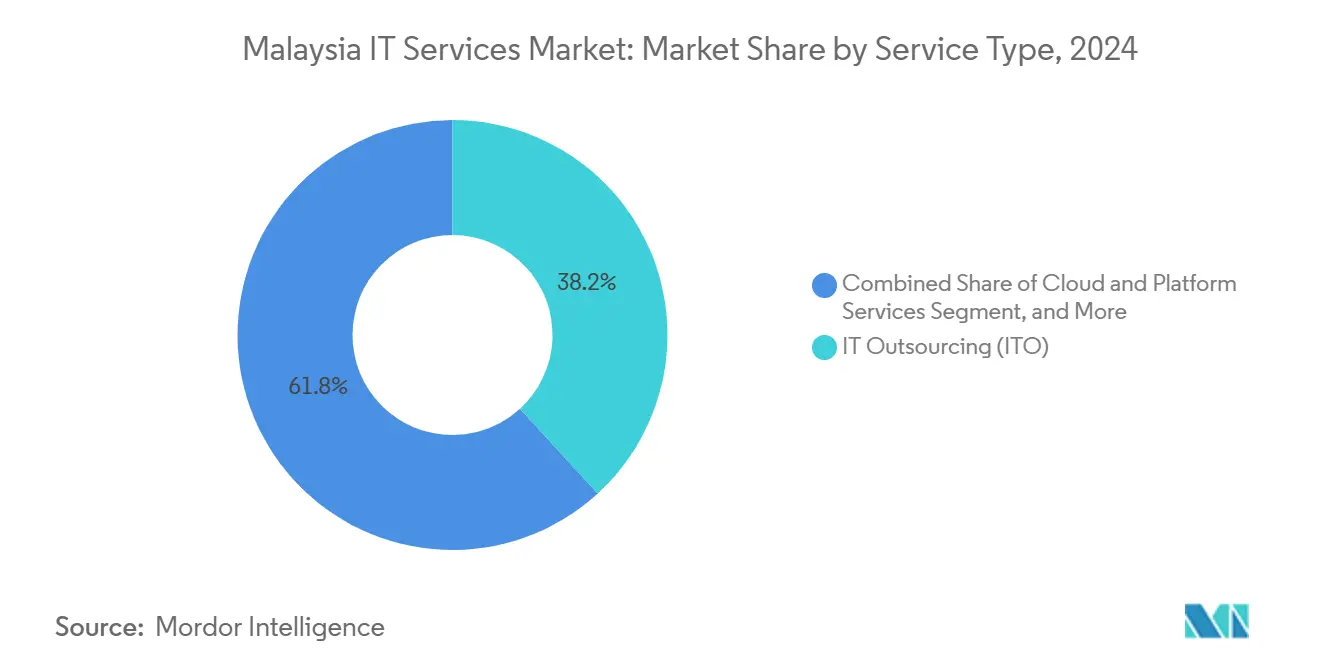

- By service type, IT outsourcing led with 38.2% of the Malaysia IT services market share in 2024, whereas cloud and platform services are on track for a 27.9% CAGR to 2030.

- By end-user enterprise size, large enterprises held 67.3% of the Malaysia IT services market size in 2024, while small and medium enterprises are advancing at a 28.5% CAGR through 2030.

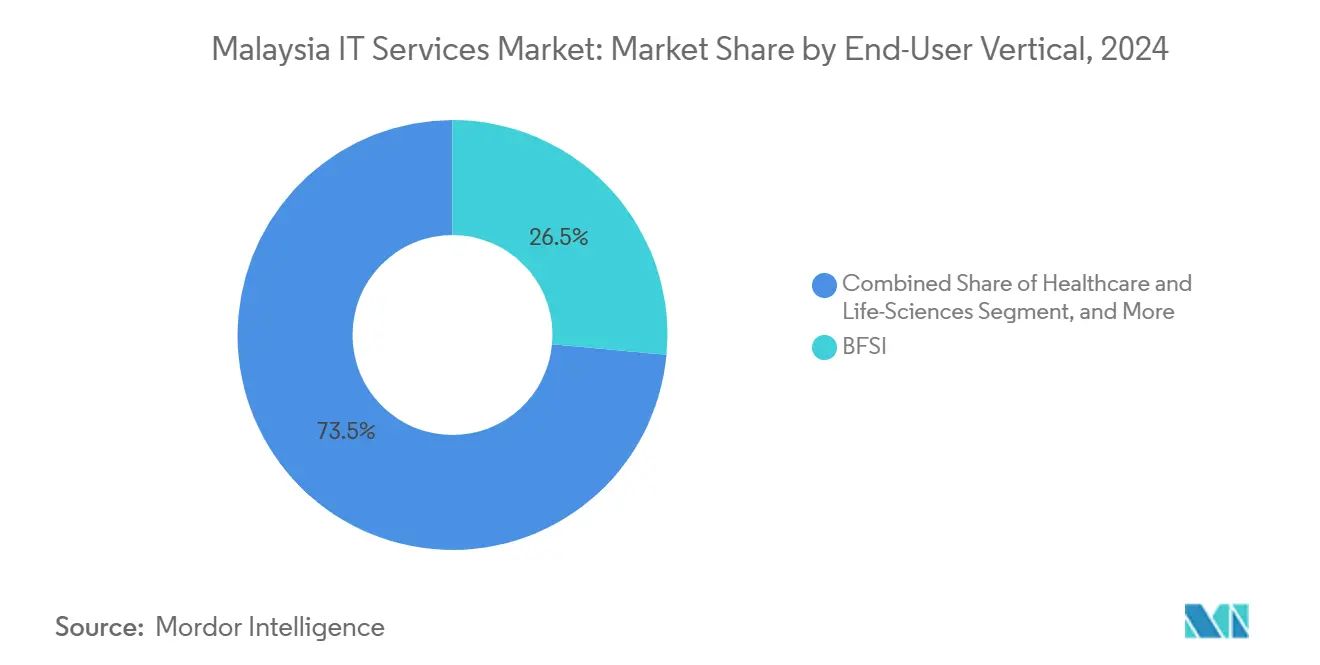

- By end-user vertical, BFSI captured 26.47% revenue share of the Malaysia IT services market in 2024; healthcare and life sciences are accelerating at a 28.1% CAGR through 2030.

Malaysia IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MyDIGITAL blueprint accelerates enterprise IT spending | +6.2% | Klang Valley, Cyberjaya | Medium term (2-4 years) |

| Hyperscale cloud data centers spur migration and modernization | +8.1% | Selangor, Johor | Long term (≥4 years) |

| Islamic digital-bank licenses drive managed-services demand | +4.3% | Urban centers nationwide | Short term (≤2 years) |

| MSC Malaysia tax incentives fuel outsourcing uptake | +3.7% | MSC-designated locations | Medium term (2-4 years) |

| ESG-reporting rules create need for carbon-accounting solutions | +2.1% | Manufacturing hubs | Short term (≤2 years) |

| Bilingual Malay-Arabic talent attracts GCC contracts | +1.8% | Kuala Lumpur | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

MyDIGITAL blueprint accelerates enterprise IT spending

The blueprint shifts public procurement away from one-off hardware buys toward outcome-based partnerships that reward integrators able to modernize legacy workflows. With MYR21 billion earmarked through 2025, ministries now mandate open APIs and citizen-centric digital services, compelling suppliers to harden cloud architectures, refine mobile UX, and ensure seamless data interchange across agencies. For the Malaysia IT services market, this translates into multi-year integration roadmaps rather than discrete projects, widening the total contract value per customer. International vendors pilot advanced e-governance modules in Kuala Lumpur before rolling them out across ASEAN, reinforcing Malaysia's role as a regional testbed. [1]Ministry of Digital, “Vantage Data Center’s New KUL2 Data Centre to Solidify Malaysia’s Role as Hub for Larger Hyperscale Data Centres,” digital.gov.my

Hyperscale cloud data centers spur migration and modernization

Vantage Data Centers’ 256 MW Cyberjaya campus and Microsoft’s USD2.2 billion cloud buildout together inject unprecedented capacity that trims latency for Southeast Asian workloads. Enterprises migrating to these facilities turn to local partners for discovery, re-platforming, and post-migration optimization, lifting high-value consulting billings. Submarine cable upgrades such as Southeast Asia–Japan 2 enhance cross-border throughput, encouraging multinationals to repatriate compute from Singapore. Edge nodes located near manufacturing clusters now support IoT analytics, fostering new managed-services streams for the Malaysia IT services market. [2]Vantage Data Centers, “Vantage Data Centers Breaks Ground on 256 MW Cyberjaya Campus,” vantage-dc.com

Islamic digital-bank licenses drive managed-services demand

Bank Negara Malaysia’s five newly authorized digital banks must honor Shariah tenets while delivering real-time digital experiences, a dual challenge that heightens reliance on external service providers. Demand spikes for DevOps pipelines embedding automated compliance checks, analytics platforms that flag interest-bearing activities, and secure API gateways that isolate prohibited instruments. As Shariah-compliant robo-advisory services gain traction, providers with both fintech tooling and Islamic governance know-how enjoy first-mover advantage, reinforcing Malaysia’s aspiration to be an Islamic fintech nucleus.

MSC Malaysia tax incentives fuel outsourcing uptake

The 100% investment tax allowance and 10-year pioneer status remain compelling, yet recent rule changes accelerate decision-making for projects involving artificial intelligence, cybersecurity, and blockchain. Kyndryl’s ASEAN Mainframe Modernization Center illustrates how global players centralize legacy-to-cloud expertise in Kuala Lumpur to serve regional clients. Streamlined work visa processing under MSC allows firms to plug skill gaps quickly, while knowledge-transfer clauses ensure local capability buildup, improving project throughput across the Malaysia IT services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity talent shortage and skill gaps | -3.4% | Kuala Lumpur, Cyberjaya | Short term (≤2 years) |

| Data-sovereignty concerns over foreign hyperscale providers | -2.8% | Government, BFSI | Medium term (2-4 years) |

| Ringgit volatility inflates USD-denominated cloud costs | -1.9% | Nationwide | Short term (≤2 years) |

| Fragmented state procurement rules limit federal consolidation | -1.6% | State agencies | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity talent shortage and skill gaps

Malaysia needs 26,430 cybersecurity professionals by 2025, but counts only 15,248 qualified experts today, creating a 43% shortfall. Scarcity inflates salaries, stretches project timelines, and compels providers to turn down work or import talent, eroding margins. The pinch is most acute in 24/7 security operations centers, where cloud security architects and threat hunters remain in limited supply. CyberSecurity Malaysia’s certification tracks aim to bridge the gap, but typical training cycles run 18-24 months, keeping supply tight in the near term.

Data-sovereignty concerns over foreign hyperscale providers

The Personal Data Protection Act and Bank Negara residency rules restrict where sensitive citizen and financial data may physically sit. Agencies and banks pursuing AI workloads must juggle compliance with the appeal of advanced American hyperscale services. Many settle on hybrid or sovereign-cloud constructs, adding architectural complexity that slows adoption and raises costs. Local clouds still lag in ML tooling, so performance trade-offs remain a sticking point.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Cloud Platforms Drive Digital Transformation

Cloud and platform services contribute the fastest growth, expanding at a 27.9% CAGR and reshaping spending priorities within the Malaysia IT services market. Enterprises executing lift-and-shift programs quickly graduate to refactoring and managed container-platform engagements, producing multiyear annuity streams for service partners. In 2024, IT outsourcing retained 38.2% revenue dominance thanks to enduring demand for application maintenance and business-process support. These engagements often evolve into phased modernization roadmaps, keeping incumbent outsourcers entrenched even as consumption models tilt toward hyperscale clouds. Hybrid-integration work that spans legacy mainframes, private clouds, and containers now commands premium pricing, underscoring the shift from labor arbitrage toward expertise arbitrage.

The Malaysia IT services market size for managed security services is climbing as newly launched SOCs, such as Kyndryl–LifeTech’s in-country facility, promise data-residency compliance and 40% cost reductions, enticing highly regulated industries. Business-process outsourcing extends into finance, HR, and omnichannel support, capturing foreign captive centers keen to rebalance away from the Philippines. Consulting and implementation partners bundle change-management frameworks with agile delivery, shortening time-to-value for government projects under MyDIGITAL. Collectively, these dynamics reinforce Malaysia’s transition from a low-cost coding shop to a full-stack digital-solutions hub.

By End-User Enterprise Size: SMEs Accelerate Digital Adoption

Large enterprises still account for 67.3% of 2024 spending, but SMEs are compounding at 28.5% annually, cementing their role as the fastest-expanding buyer cohort in the Malaysia IT services market. Government grants under the DigitalSME program subsidize up to 50% of eligible tech investments, dramatically lowering entry barriers to SaaS ERP and CRM modules. Cloud marketplaces offering pay-as-you-go billing resonate with SMEs that shun capex commitments, allowing them to deploy e-commerce storefronts, accounting suites, and e-invoicing stacks within days.

The Malaysia IT services market size for large-enterprise engagements nevertheless grows as banks, telcos, and utilities modernize decades-old cores while hardening cybersecurity postures. Complexities in multi-jurisdictional compliance, especially for regional conglomerates, demand specialist advisory and managed-governance layers that smaller integrators cannot easily match. As both spectrums gravitate to cloud solutions, providers that engineer modular service catalogs—scalable from startup to Fortune 500—enjoy cost efficiencies and higher wallet share.

By End-User Vertical: Healthcare Leads Digital Health Revolution

Healthcare and life sciences are accelerating at a 28.1% CAGR, making it the quickest riser within the Malaysia IT services market. Post-pandemic telemedicine victories earned public trust, spurring hospital groups to digitize patient record management and explore AI-assisted imaging diagnostics. HeiTech Padu’s pilot for a national clinical-documentation module typifies the pivot toward integrated platforms that standardize care protocols across facilities.

BFSI keeps its 26.47% leadership due to continuous digital-banking rollouts and compliance spending. Islamic finance principles multiply architecture complexity, lifting the Malaysia IT services market share captured by boutique fintech specialists. Manufacturing stays vibrant as semiconductor and EMS players deploy IoT sensors and predictive-maintenance analytics inside Industry 4.0 programs. Government, retail, telecom, transport, and energy each deepen their digital transformation plays, underscoring a broadening client base that buffers service providers against sector-specific shocks.

Geography Analysis

Klang Valley, home to Kuala Lumpur and Selangor, generates about 60% of 2024 billings in the Malaysia IT services market. Its proximity to federal agencies, multinational headquarters, and Cyberjaya’s data-center cluster secures a flywheel effect: new hyperscale builds attract more integrators, which in turn entice additional enterprise tenants. Johor evolves as a secondary magnet following TM and Singtel’s Nxera joint venture for an AI-ready 200 MW campus, positioning the state to capture overflow workloads from Singapore. [3]TM, “TM and Singtel’s Nxera Form Joint Venture to Develop Next-Generation Data Centres,” tm.com.my

Penang’s electronics manufacturing heritage fuels steady demand for ERP rollouts and supply-chain analytics, while its talent pool lends itself to specialized firmware and embedded-software projects. Sarawak advances renewable-energy-powered data-center plans, leveraging ample hydroelectric resources to market carbon-neutral hosting, which is increasingly essential for ESG-minded clients.

Nationwide 5G coverage now surpasses 81.8% of populated areas, flattening historical infrastructure disparities and expanding addressable market pockets beyond metropolitan corridors. Submarine cables such as Asia Pacific Gateway reinforce Malaysia’s gateway status, enabling local providers to serve Indonesian and Philippine clients while satisfying Malaysian data-residency laws. Altogether, these geographic spreads reduce single-region dependency and distribute revenue more evenly across the Malaysia IT services market.

Competitive Landscape

The Malaysian IT services market shows moderate fragmentation. Telekom Malaysia and Axiata Digital Services wield entrenched public-sector relationships, while IBM, Accenture, and Kyndryl deliver global best practices and certified hyperscale expertise. Mid-tier contenders bridge language skills, cost advantages, and niche domain competencies to win specialized work such as Islamic fintech or carbon accounting.

Hyperscale alliances now constitute a critical differentiator. Kyndryl’s Mainframe Modernization Center funnels legacy-system conversions to a centralized Kuala Lumpur hub that serves broader ASEAN demand, underscoring Malaysia’s export-services potential. [4]Kyndryl, “Kyndryl Establishes Malaysia as ASEAN Hub for Mainframe Modernisation,” kyndryl.com Security operations offerings often hinge on data-residency guarantees, prompting joint ventures between foreign MSSPs and local cloud operators.

M&A activity is rising as providers seek breadth. Silverlake Axis’s SunGard Ambit acquisition extends retail-banking software reach, while Datasonic’s stake in Innov8tif fortifies e-KYC capabilities. Scale efficiencies and domain depth are becoming prerequisites as enterprise buyers favor vendors that can bundle consulting, implementation, and managed run services under a single SLA, gradually squeezing smaller pure-play resellers out of complex bids.

Malaysia IT Services Industry Leaders

Telekom Malaysia Berhad

Axiata Digital Services Sdn Bhd

IBM Malaysia Sdn Bhd

Accenture Solutions Sdn Bhd

HeiTech Padu Berhad

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HeiTech Padu signed a JV with Regal Orion to build a Tier IV data center in Shah Alam, targeting global tenants.

- May 2025: HeiTech Padu secured a RM28.61 million contract from the Health Ministry to pilot a clinical-documentation module.

- May 2025: Silverlake Axis purchased SunGard Ambit for USD12 million, adding core retail-banking solutions.

- April 2025: HeiTech Padu inked MOUs with Huawei Malaysia and Maiyue Technology to explore AI-powered smart-government services.

- March 2025: HeiTech Padu reaffirmed its capacity to deliver an RM902.96 million hydroelectric project for TNB Power Generation.

- February 2025: Kyndryl and LifeTech Group launched Malaysia’s first public-cloud SOC, promising 40% cost reductions.

- January 2025: Censof Holdings won a RM4.27 million mandate from KWAP to replace its accounting system.

Malaysia IT Services Market Report Scope

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-User Verticals |

| By Service Type | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| Healthcare and Life-Sciences | |

| Retail and Consumer Goods | |

| Telecom and Media | |

| Logistics and Transport | |

| Energy and Utilities | |

| Other End-User Verticals |

Key Questions Answered in the Report

How large is the Malaysia IT services market in 2025?

It is valued at USD12.32 billion and is forecast to reach USD39.41 billion by 2030.

What is the expected CAGR for Malaysia’s IT services through 2030?

The market is projected to expand at 26.19% annually over the 2025–2030 period.

Which service segment is growing the fastest?

Cloud and platform services is the fastest-expanding category, registering a 27.9% CAGR.

Why are SMEs adopting IT services more aggressively now?

Government grants under DigitalSME and pay-as-you-go cloud models lower up-front costs, enabling SMEs to implement ERP and CRM rapidly.

What restraint poses the greatest short-term risk?

A 43% shortage in cybersecurity professionals raises labor costs and could delay security-critical projects.

Which Malaysian region is emerging as a new data-center hotspot after Klang Valley?

Johor is quickly becoming a secondary hub following TM and Singtel’s Nxera 200 MW AI-ready campus initiative.

Page last updated on: