Saudi Arabia E-commerce Cosmetics and Fragrances Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

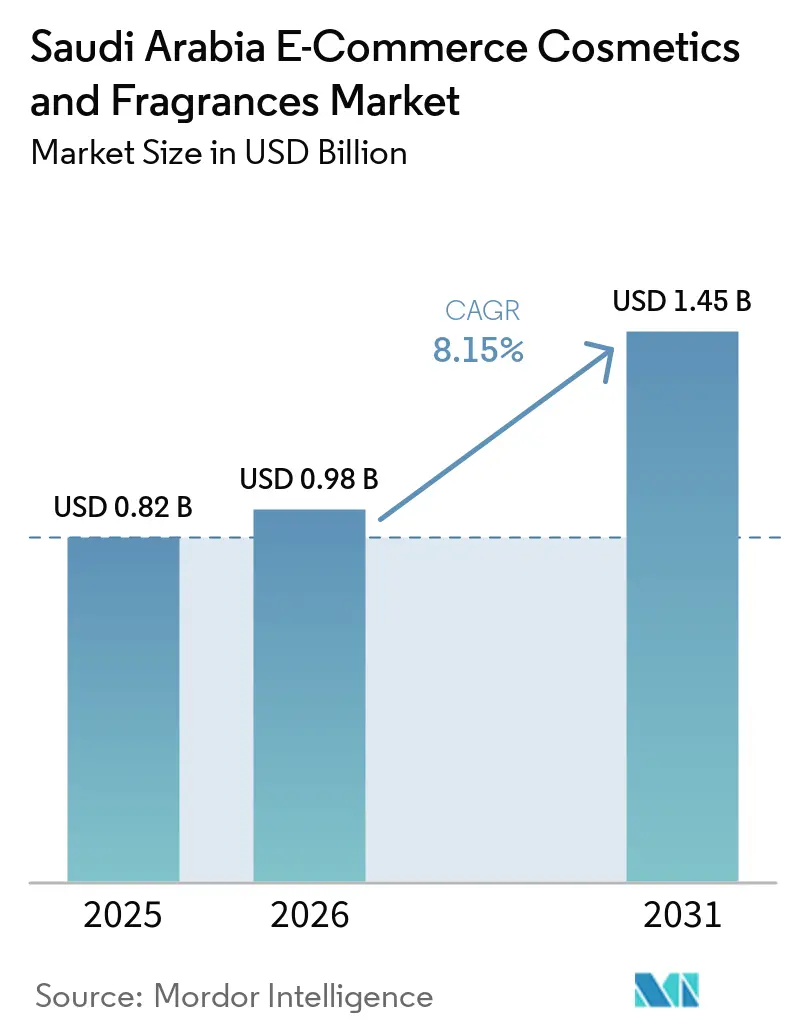

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

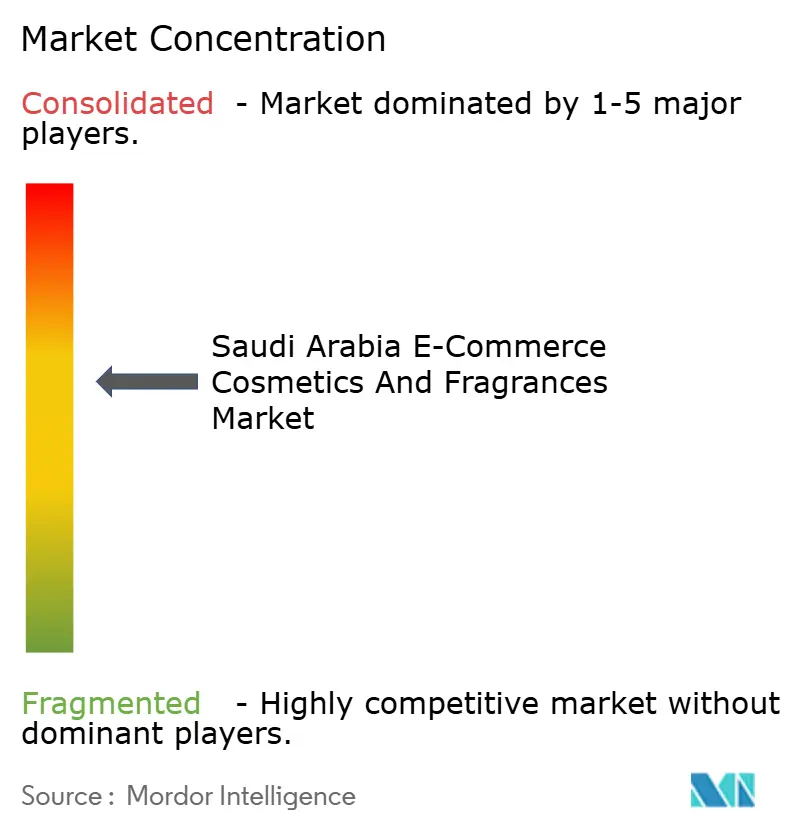

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia E-commerce Cosmetics and Fragrances Market Analysis by Mordor Intelligence

The Saudi Arabia E-commerce Cosmetics and Fragrances Market size is projected to grow from USD 0.82 billion in 2025 and USD 0.98 billion in 2026 to USD 1.45 billion by 2031, registering a CAGR of 8.15% between 2026 and 2031. This growth is driven by the nation's Vision 2030 initiative, which emphasizes digital transformation, alongside one of the highest internet penetration rates in the Gulf Cooperation Council (GCC). According to a 2024 report by the Communications, Space and Technology Commission (CST), internet penetration in Saudi Arabia has reached an impressive 99% [1]Source: Communications, Space, and Technology Commission, "CST Issued the Saudi Internet Report", cst.gov.sa. In the online shopping segment, skincare and makeup dominate, while fragrances, supported by the Kingdom's cultural preference for premium scents, are experiencing the fastest growth. Although mass-market products account for the largest share, there is a growing demand for premium and luxury lines, influenced by social media platforms like TikTok and Instagram. Younger, tech-savvy female consumers are driving this shift, with a notable preference for natural and organic products that align with health and sustainability trends. Global players like Sephora GCC and L’Oréal are actively leveraging strategies such as personalization and exclusive online product launches to enhance customer loyalty.

Key Report Takeaways

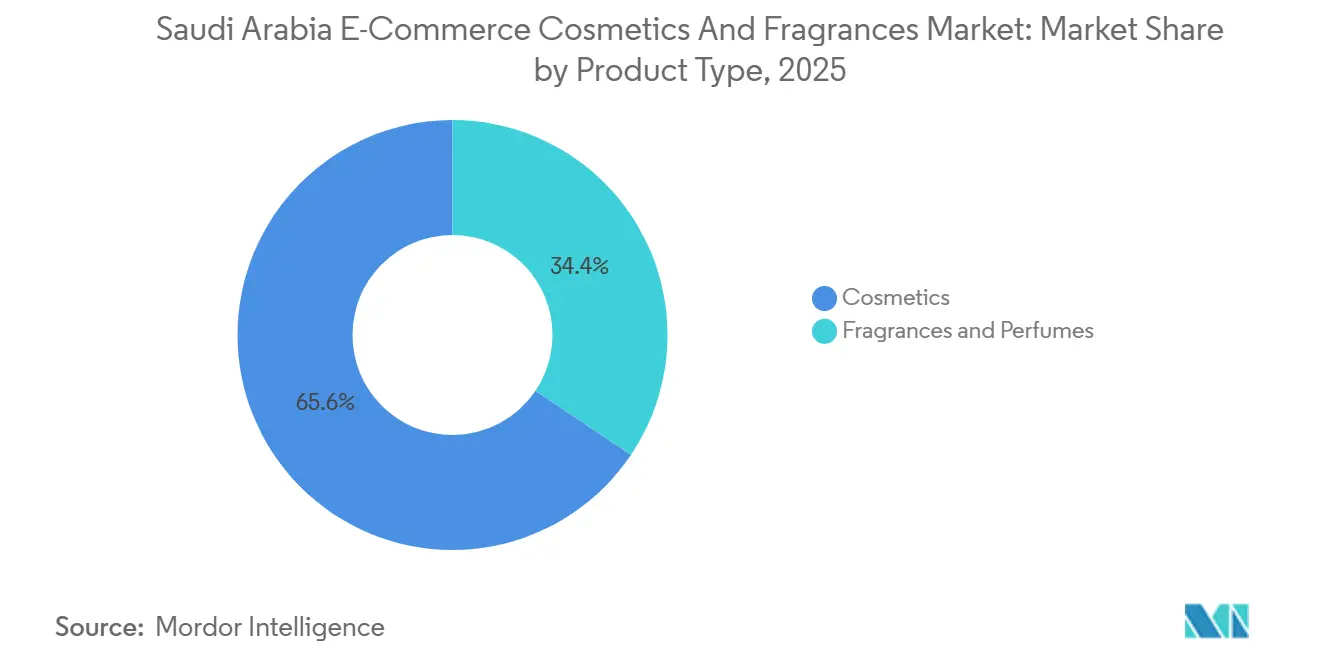

- By product type, cosmetics led with 65.58% of the Saudi Arabia E-commerce Cosmetics and Fragrances Market share in 2025, while fragrances and perfumes recorded the highest projected CAGR at 8.88% through 2031.

- By price range, the mass segment held 58.48% share of the Saudi Arabia E-commerce Cosmetics and Fragrances Market size in 2025, whereas premium/luxury offerings are forecast to expand at 9.86% CAGR to 2031.

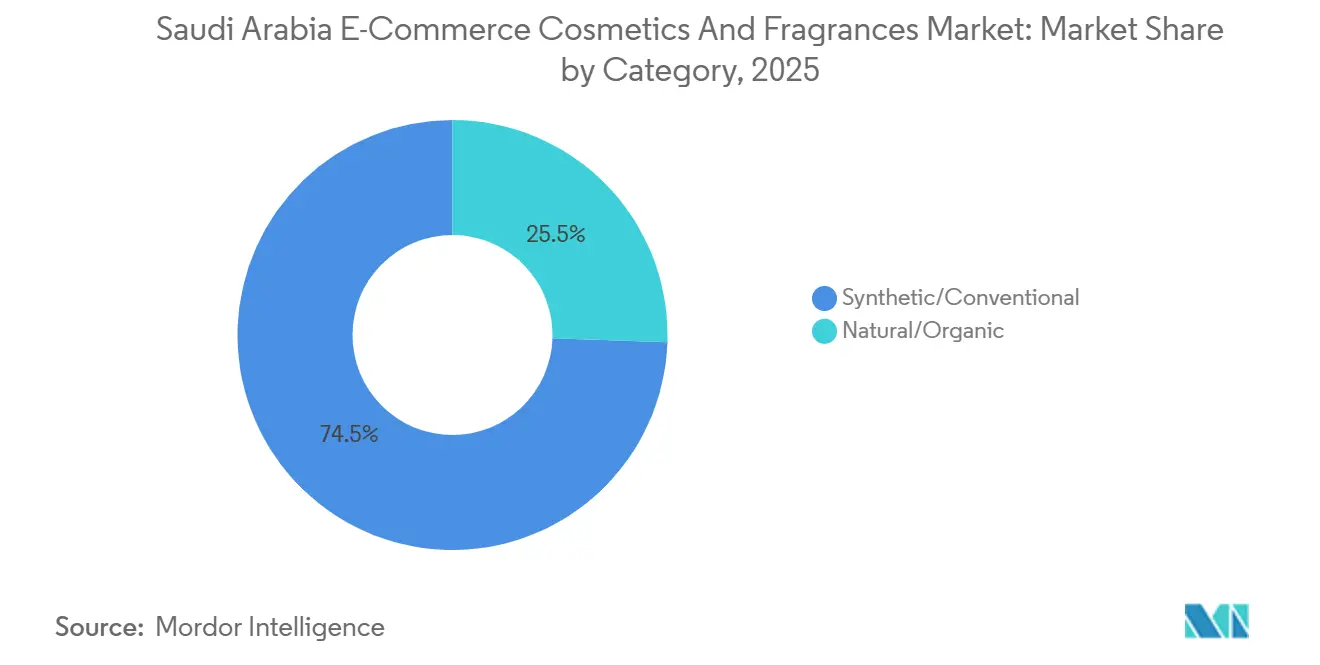

- By category, synthetic/conventional products accounted for 74.47% share in 2025, yet natural/organic lines are growing at 7.58% CAGR on halal-certified demand.

- By platform, third-party marketplaces commanded 96.18% share in 2025, while company-owned platforms show the fastest trajectory at 9.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia E-commerce Cosmetics and Fragrances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising internet penetration and digital adoption | +1.8% | National, with concentration in Riyadh, Jeddah, Dammam metropolitan areas | Short term (≤ 2 years) |

| Influence of social media and beauty influencers | +2.1% | National, with spillover to GCC via cross-border influencer reach | Medium term (2–4 years) |

| Preference for premium and luxury brands online | +1.5% | National, particularly urban centers (Riyadh, Jeddah, Eastern Province) | Medium term (2–4 years) |

| Cultural and gifting preferences for fragrances and cosmetics | +1.3% | National, peak demand in Ramadan/Eid periods across all regions | Short term (≤ 2 years) |

| Expansion of online retailers and platforms | +1.0% | National, led by Riyadh and Jeddah, expanding to secondary cities | Medium term (2–4 years) |

| Technological advancements, such as AI-driven personalized beauty suggestions | +0.8% | National, early adoption in major urban hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising internet penetration and digital adoption

Saudi Arabia's e-commerce market for cosmetics and fragrances is experiencing significant growth, driven by increasing internet penetration and rapid digital adoption. This growth positions the Kingdom as a leading digital market within the GCC. With widespread smartphone usage and near-universal connectivity, online beauty shopping has become highly accessible. Key features in demand include preferred payment options, user-friendly online stores and carts, and mobile-optimized shopping experiences, which are particularly important for cosmetics and fragrance purchases where convenience and personalization are essential. Global brands such as L’Oréal and Estée Lauder are enhancing consumer engagement through online exclusives and tailored campaigns. E-commerce platforms like Namshi and Noon are leading the market with diverse product offerings and competitive pricing. Supported by digital innovations, mobile-centric payment solutions, and a more connected consumer base, Saudi Arabia is undergoing a rapid transformation toward online beauty consumption.

Influence of social media and beauty influencers

In Saudi Arabia, social media and beauty influencers are transforming the e-commerce market for cosmetics and fragrances, reshaping how consumers discover and purchase products online. Platforms like TikTok and Instagram have become key channels for beauty engagement, where influencer-led tutorials, product reviews, and live shopping streams influence consumer decisions. Online retailers such as Golden Scent and Nice One collaborate with Saudi beauty creators to highlight exclusive launches and seasonal collections. Boutiqaat, a popular GCC platform, integrates influencers into its strategy, enabling consumers to shop directly from curated influencer "stores." These approaches resonate with younger audiences, particularly women, who view influencers as trusted voices in the beauty market. Partnerships with regional lifestyle influencers enhance the premium positioning of luxury products through aspirational narratives. Meanwhile, niche brands increasingly use micro-influencers to build authenticity and trust, especially in halal, clean, and sustainable beauty. With high social media penetration and a growing preference for shoppable content, influencer marketing is boosting brand visibility and streamlining the journey from discovery to purchase, solidifying online platforms as key destinations for cosmetics and fragrances in Saudi Arabia.

Preference for premium and luxury brands online

A strong preference for premium and luxury beauty brands is a significant growth driver for the Saudi Arabia E-commerce Cosmetics and Fragrances Market. Saudi consumers exhibit a clear inclination toward high-end fragrances, prestige makeup, and internationally recognized luxury brands, influenced by cultural values and increasing purchasing power. This trend is further shaped by the importance of personal grooming and appearance in Saudi culture, where luxury products are often associated with social status and sophistication. This growth is supported by robust consumer spending; data from the Capital Market Authority shows that total consumer expenditure in 2023 was approximately SAR 1.6 trillion, with projections to reach around SAR 2.3 trillion by 2030 [2]Source: Savola Group Company, "Savola Group Company prospectus", cma.gov.sa. Rising disposable incomes, a young and brand-conscious population, and growing female workforce participation are further driving demand for aspirational and status-oriented purchases. Additionally, the increasing penetration of digital platforms and the convenience of online shopping have made luxury products more accessible to a broader audience. E-commerce platforms are leveraging this trend by offering premium positioning, influencer-driven marketing, convenient payment options, and doorstep delivery, all of which enhance the luxury shopping experience.

Cultural and gifting preferences for fragrances and cosmetics

In Saudi Arabia, the e-commerce market for cosmetics and fragrances thrives on cultural and gifting traditions. Beauty and luxury products are integral to social customs and personal practices. Fragrances are culturally significant, essential for special occasions, social events, and religious ceremonies. Cosmetics and skincare products are also popular gifts during holidays, weddings, and festivals. E-commerce platforms leverage these preferences by offering curated gift sets, personalized packaging, and timely promotions. Brands like Arabian Oud, Ajmal Perfumes, Rasasi, Abdul Samad Al Qurashi, Golden Scent, and Nice One, operating within the MEA flavor and fragrance landscape cater to this demand with curated gift sets and luxury bundles featuring personalization and festive packaging. The younger, tech-savvy population blends traditional gifting practices with online shopping, driving demand for exclusive fragrances, designer makeup, and customized beauty bundles. By aligning offerings with cultural values and gifting occasions, local and international brands are boosting consumer loyalty and online sales in Saudi Arabia's growing beauty and fragrance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of physical consultation in cosmetics | -0.9% | National, more pronounced in secondary cities with limited retail infrastructure | Medium term (2–4 years) |

| High preference for in-store trial for fragrances | -1.2% | National, especially for premium oud and niche perfumes | Medium term (2–4 years) |

| Consumer trust issues with counterfeit products | -0.7% | National, with higher incidence in cross-border e-commerce channels | Short term (≤ 2 years) |

| Delays in order fulfillment for time-sensitive purchases | -0.6% | National, acute in remote areas and during peak seasons (Ramadan, Eid) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer trust issues with counterfeit products

Consumer trust continues to be a major challenge in the Saudi Arabia E-commerce Cosmetics and Fragrances Market, primarily due to the ongoing issue of counterfeit products. The Ministry of Commerce's interception of over five million counterfeit products underscores the magnitude of the problem and the regulatory efforts to address it [3]Source: Saudi Gazette, "Ministry of Commerce prevents over 5 million counterfeit products from reaching consumers", saudigazette.com.sa. Despite these measures, the prevalence of counterfeit cosmetics and fragrances, particularly through unauthorized online sellers and third-party marketplaces, has increased consumer skepticism regarding online beauty purchases. In segments such as fragrances and premium cosmetics, where authenticity, ingredient safety, and brand reputation are crucial, the risk of receiving counterfeit or diluted products significantly affects consumer confidence. Additionally, counterfeit beauty products pose potential health risks due to unregulated formulations, further deterring online purchases. Consequently, many consumers prefer physical retail stores or authorized brand websites, where product authenticity is guaranteed.

High preference for in‑store trial for fragrances

Counterfeit products pose a significant challenge in Saudi Arabia's e-commerce market for cosmetics and fragrances, undermining consumer trust and hindering growth. Major online platforms, particularly third-party marketplaces, often enable the sale of imitation products, making it difficult for consumers to verify authenticity. Luxury brands like Ghawali, Ajmal Perfumes, and Rasasi struggle to protect their online reputation as counterfeit versions of their products appear on unofficial websites and social media channels. This issue discourages first-time buyers, especially for high-value items where authenticity is critical. While platforms like Golden Scent and Boutiqaat have introduced measures such as verified seller programs and secure packaging, smaller e-commerce players often lack such controls. Without stronger regulatory enforcement and anti-counterfeit measures across all platforms, counterfeit products will continue to hinder the growth of Saudi Arabia's cosmetics and fragrance e-commerce market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fragrances Accelerate Despite Cosmetics Dominance

In 2025, cosmetics accounted for 65.58% of the market share, while fragrances and perfumes are projected to grow at a CAGR of 8.88% through 2031, surpassing the overall market growth rate of 8.15%. This growth highlights the Kingdom's cultural preference for oud and oriental scents. Within the cosmetics segment, facial makeup, eye makeup, and lip-and-nail products are gaining traction, driven by the popularity of influencer-led tutorials. The fragrance segment is categorized into eau de parfum, eau de toilette, eau de cologne, and specialty formats, with eau de parfum holding the largest share due to consumer preferences for higher concentration and longer-lasting scents. Consumers are willing to pay premiums exceeding SAR 500 (USD 133) per bottle for such products.

Brands such as Ghawali, Arabian Oud, and Ajmal Perfumes are leveraging online platforms to offer exclusive collections, limited editions, and subscription samples. These strategies aim to address the sensory limitations of digital fragrance shopping. Online platforms not only introduce consumers to traditional oud-based fragrances but also to global luxury scents, reflecting a blend of tradition and modernity. While fragrances remain a focal point, there is a growing demand for other categories, particularly halal and organic beauty products. Online platforms play a crucial role in enabling niche brands to target specific audiences and capitalize on the expanding e-commerce beauty market.

By Price Range: Premium Channels Outpace Mass Despite Smaller Base

Mass-market offerings accounted for a 58.48% market share in 2025, driven by affordability and extensive distribution through third-party marketplaces. However, the premium/luxury segments are experiencing a compound annual growth rate (CAGR) of 9.86% through 2031. E-commerce platforms play a significant role by enabling consumers to purchase beauty products at prices often lower than traditional retail markups. Brands such as Rasasi, Swiss Arabian, and Faces Cosmetics dominate the perfume category, while Max Factor, Maybelline, and L’Oréal Paris lead in makeup. These mass-market players are leveraging digital platforms to highlight product quality, ingredient benefits, and promotional offers. Additionally, by improving packaging and marketing strategies, they are actively working to build customer loyalty in an increasingly competitive market.

Premium brands like Ghawali, Arabian Oud, and Ajmal Perfumes, along with global names such as Tom Ford in fragrances and makeup leaders Huda Beauty, Farsali, and Lancôme, are utilizing e-commerce to enhance their market presence. These brands are not only selling products but also curating exclusive collections, offering personalized services, and creating direct-to-consumer experiences that justify their premium pricing. In Saudi culture, gifting holds considerable importance, with consumers often investing in high-end beauty products for special occasions. Online platforms have streamlined this process, enabling easy selection, personalization, and delivery of gifts. As the market shifts towards premiumization, mass-market brands are adopting digital innovations to remain competitive in the evolving landscape.

By Category: Natural and Organic Gain Traction Amid Halal Certification Demand

The Saudi Arabia E-commerce Cosmetics and Fragrances Market is primarily driven by synthetic/conventional formulations, which accounted for 74.47% of the total market share in 2025. This dominance is attributed to well-established manufacturing ecosystems, strong brand presence, extensive product availability, and relatively lower price points compared to premium natural alternatives. In the online channel, these products benefit from promotional strategies, bundled offers, and mass-market positioning that appeal to a wide consumer base. Established international and regional brands utilizing synthetic formulations maintain strong visibility on leading e-commerce platforms, supported by efficient supply chains and competitive pricing strategies.

Meanwhile, the natural/organic segment is emerging as a high-growth niche, projected to grow at a CAGR of 7.58% through 2031. This growth is driven by increasing ethical consumerism, heightened health consciousness, and rising demand for halal-certified and “tayyib” (pure and safe) products. A 2024 academic study involving 207 Saudi consumers revealed a significant positive correlation between halal and tayyib attributes and purchase intention, with brand trust and certification transparency identified as key purchase drivers. In the e-commerce space, where ingredient scrutiny and brand storytelling are easily accessible, this segment benefits from detailed product descriptions, certification labeling, and influencer-led education efforts.

By Platform: Company-Owned Channels Expand as Brands Pursue First-Party Data

Third-party platforms hold a dominant 96.18% market share, reflecting consumers' preference for variety, competitive pricing, and the convenience of accessing multiple brands in one place. Established platforms such as Noon and Amazon Saudi Arabia play a critical role by offering trusted payment systems and reliable fulfillment networks. These marketplaces provide beauty brands with immediate access to a large and engaged customer base while leveraging an established logistics infrastructure. This significantly reduces entry barriers for both international and regional brands, enabling them to enter the Saudi market without substantial upfront investments.

The company-owned platform segment, though currently smaller, is experiencing the fastest growth with a CAGR of 9.45%. Beauty brands are increasingly prioritizing direct-to-consumer relationships, leveraging the strategic benefits of first-party data collection, and gaining greater control over brand presentation and customer experience. Prominent brands such as Huda Beauty, Ghawali, Arabian Oud, and Ajmal Perfumes are investing in proprietary online stores and localized delivery solutions to strengthen their market presence. This shift is supported by advancements in digital payment systems, including STC Pay and Mada, which facilitate seamless transactions. Furthermore, the development of local logistics networks enables brands to offer competitive delivery services independently, signifying a notable evolution and diversification of Saudi Arabia’s e-commerce landscape.

Geography Analysis

Saudi Arabia is the leading market in the GCC's e-commerce cosmetics and fragrances industry, supported by a strong digital infrastructure, growing consumer demand, and robust regulatory frameworks. Urban centers such as Riyadh, Jeddah, and Dammam play a pivotal role, driven by advanced logistics networks, affluent populations, and high levels of social media engagement. These cities are key drivers of premium beauty purchases, with consumers expecting fast and efficient deliveries. Regulatory measures, including the SFDA's cosmetics safety protocols, ZATCA's e-invoicing requirements, and CITC's cybersecurity mandates, enhance consumer confidence. Additionally, strategic ports in Jeddah and Dammam improve the efficiency of cross-border beauty product imports.

The direct-to-consumer segment for premium and luxury beauty products is experiencing rapid growth, fueled by rising disposable incomes, aspirational purchasing trends, and increasing digital adoption in cities like Riyadh, Jeddah, and Dammam. Brands such as Ghawali, Arabian Oud, Ajmal Perfumes, and Huda Beauty are investing heavily in their online platforms, offering exclusive collections, personalized services, and unique gifting options. Collaborations with social media influencers, including Nora Bo Awadh, Shouq, and Yara Alnamlah, further enhance brand engagement, enabling these companies to deliver premium experiences that surpass those offered by third-party platforms.

While smaller cities and rural areas are witnessing gradual growth, challenges such as limited logistics infrastructure, lower population density, and niche market segments hinder rapid expansion. To address these issues, plans are underway to establish 59 logistics hubs by 2030, aiming to extend service coverage and integrate these regions into the e-commerce ecosystem. Furthermore, the Vision 2030 initiative is promoting local manufacturing, with new domestic hubs for perfumes and cosmetics being developed. This initiative not only ensures compliance with local regulatory standards and reduces reliance on imports but also increases the availability of high-quality beauty products in areas beyond major urban centers.

Competitive Landscape

Saudi Arabia's e-commerce cosmetics and fragrances market is moderately consolidated, with both international and regional players competing for market share through diverse product offerings, pricing strategies, and digital initiatives. Prominent global brands such as L’Oréal, Estée Lauder, and Lancôme leverage platforms like Sephora SA, Noon, and Amazon Saudi Arabia to showcase their extensive makeup and skincare ranges. These companies combine their global brand recognition with localized marketing strategies. On the other hand, regional leaders specializing in traditional scents, including Arabian Oud, Ajmal Perfumes, and Al Rehab, appeal to Saudi consumers by emphasizing culturally relevant narratives and exclusive product lines. These regional brands differentiate themselves by curating unique collections, offering limited editions, and providing personalized services, creating a distinct online shopping experience compared to mass-market alternatives.

Adopting advanced technology is essential for brands aiming to maintain a competitive edge. Brands like Huda Beauty and Ghawali enhance their websites with features such as augmented reality (AR) and virtual reality (VR) makeup try-ons, artificial intelligence (AI)-driven product recommendations, and interactive social commerce tools to increase customer engagement. To address the challenge of selecting fragrances online, many brands offer subscription boxes and sampling programs. Additionally, third-party marketplaces build consumer trust by providing secure payment options like STC Pay and Mada, efficient fulfillment services, and user review systems. These technology-driven approaches not only personalize the shopping experience but also encourage repeat purchases and improve customer satisfaction, particularly in a market where sensory engagement is limited online.

Market positioning in Saudi Arabia's e-commerce cosmetics and fragrances sector relies on strategic partnerships, collaborations, and platform diversification. Global players like L’Oréal invest in BeautyTech, collaborate with influencers, and develop exclusive online collections to strengthen their presence. In contrast, regional brands partner with platforms such as Noon and Sephora SA to expand their reach. Smaller brands utilize social media, targeted marketing campaigns, and niche offerings, including halal makeup and luxury fragrances, to establish their presence. Aligning with Vision 2030, emerging brands are increasingly exploring mergers, acquisitions, and local manufacturing initiatives to enhance supply chains, reduce dependency on imports, and drive growth.

Saudi Arabia E-commerce Cosmetics and Fragrances Industry Leaders

-

L'Oréal S.A.

-

The Estée Lauder Companies

-

Ajmal Perfumes

-

Huda Beauty LLC

-

Arabian Oud Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Malaysia’s JEONG FAMILY has entered into an exclusive agreement with Saudi beauty retailer Nice One to launch its kids’ beauty brand, ILY, in Saudi Arabia. Under this agreement, Nice One will act as the sole distributor for ILY across both online and offline channels. This marks the first introduction of a Malaysian-born, Halal-certified kids’ beauty brand to the Middle Eastern market.

- November 2024: The clean beauty brand Kosas has officially launched in Saudi Arabia, expanding its reach through Sephora Middle East. Founder Sheena Zadeh has highlighted that this expansion aligns with Saudi consumers’ growing demand for high-quality, skin-focused makeup products that emphasize nourishing ingredients and performance.

- September 2024: Saudi beauty brand Asteri Beauty has unveiled its “Proudly Saudi” campaign in celebration of Saudi National Day. The campaign highlights new products that honor Saudi heritage and women, including four new shades of the brand’s Legacy Lipstick. Each shade is named after influential Saudi women who have inspired founder Sara Al Rashid. These additions to the collection feature a rich, hydrating formula designed to keep lips soft and moisturized.

Saudi Arabia E-commerce Cosmetics and Fragrances Market Report Scope

Cosmetics are defined as items with mild action on the human body for the purpose of cleaning, beautifying, adding to attractiveness, altering the appearance, or keeping or promoting the skin or hair in good condition. These include facial cosmetics, eye cosmetics, lip and nail cosmetics, and hair styling and coloring products, to name a few.

The Saudi Arabian E-Commerce Cosmetics and Fragrances Market is Segmented by Product Type (Hair Care, Skin Care, Make-Up Products, Deodorants, and Fragrances), Category (Mass and Premium), and End User (Men, Women, And Unisex). The report offers market sizes and values (in USD million) during the forecast period for the above segments.

| Cosmetics | Facial Make-up |

| Eye Make-up | |

| Lip and Nail Make-up | |

| Fragrances and Perfumes | Eau de Parfum |

| Eau de Toilette | |

| Eau de Cologne | |

| Others |

| Mass |

| Premium/Luxury |

| Synthetic/Conventional |

| Natural/Organic |

| Third-Party Marketplace |

| Company-owned Platform |

| By Product Type | Cosmetics | Facial Make-up |

| Eye Make-up | ||

| Lip and Nail Make-up | ||

| Fragrances and Perfumes | Eau de Parfum | |

| Eau de Toilette | ||

| Eau de Cologne | ||

| Others | ||

| By Price Range | Mass | |

| Premium/Luxury | ||

| By Category | Synthetic/Conventional | |

| Natural/Organic | ||

| By Platform | Third-Party Marketplace | |

| Company-owned Platform | ||

Key Questions Answered in the Report

What is the forecast CAGR for e-commerce cosmetics and fragrances market in Saudi Arabia through 2031?

The Saudi Arabia E-commerce Cosmetics and Fragrances Market is projected to grow at 8.15% annually from 2026 to 2031.

Which product class is expanding faster than the wider market?

Fragrances and perfumes are advancing at 8.88% CAGR, outpacing cosmetics.

How dominant are third-party marketplaces today?

They captured 96.18% of 2025 value, though brand-owned platforms are growing at 9.45% CAGR.

Why are premium and luxury SKUs gaining share online?

High disposable income, halal-certified demand, and frictionless BNPL payments fuel a 9.86% CAGR for premium tiers.

Page last updated on: