Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

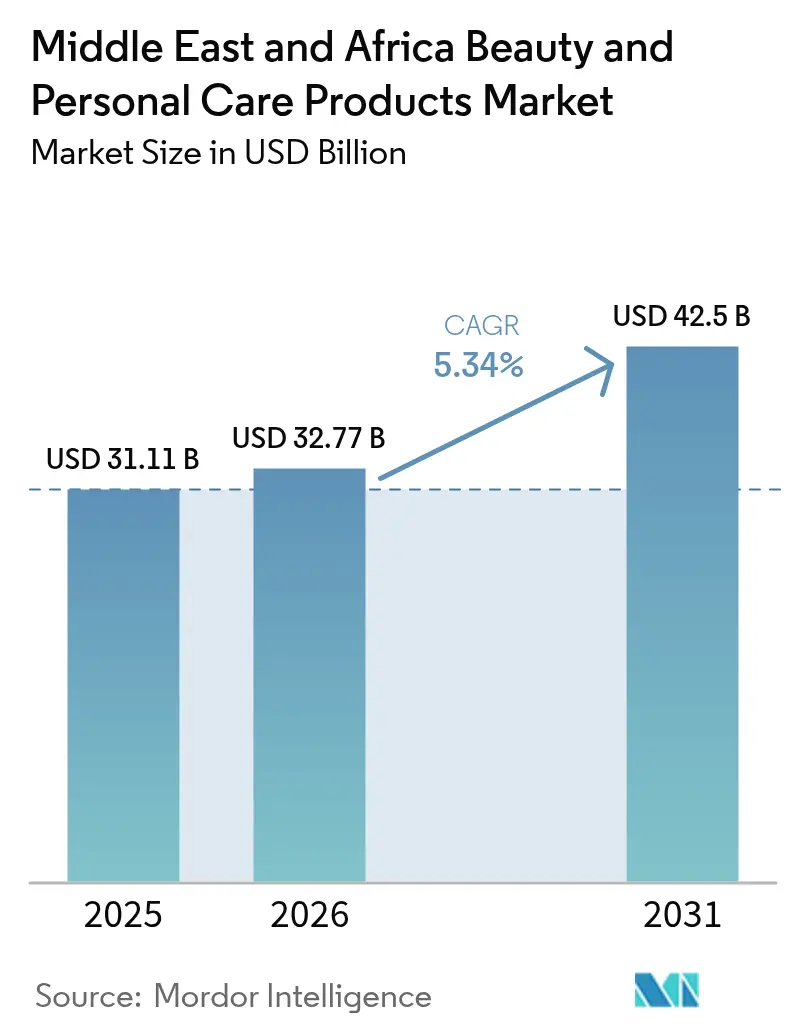

| Base Year Market Size (2025) | USD 31.11 Billion |

| Market Size (2026) | USD 32.77 Billion |

| Market Size (2031) | USD 42.5 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The Middle East and Africa beauty and personal care products market size in 2026 is estimated at USD 32.77 billion, growing from 2025 value of USD 31.11 billion with 2031 projections showing USD 42.5 billion, growing at 5.34% CAGR over 2026-2031. This growth is driven by evolving consumer preferences toward halal-certified and clean beauty formulations that align with regional cultural values and religious requirements. The market's momentum stems from the intersection of traditional beauty practices with modern digital commerce, where social media influence accelerates product discovery and purchase decisions across diverse demographic segments.

Key Report Takeaways

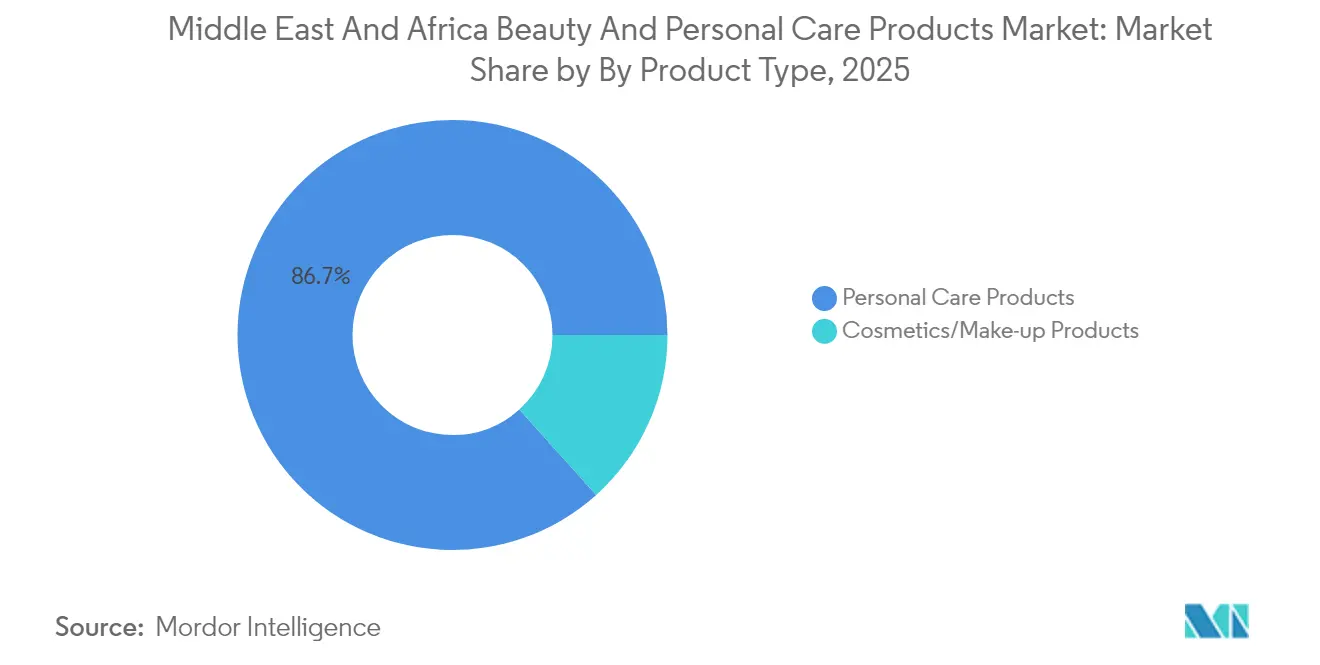

- By product type, personal care products commanded 86.65% of the 2025 revenue, whereas the cosmetics/make-up segment is expected to grow at a 6.62% CAGR from 2026 to 2031.

- By category, the mass tier held 57.10% share in 2025; premium/luxury offerings are forecast to grow at 7.05% through 2031.

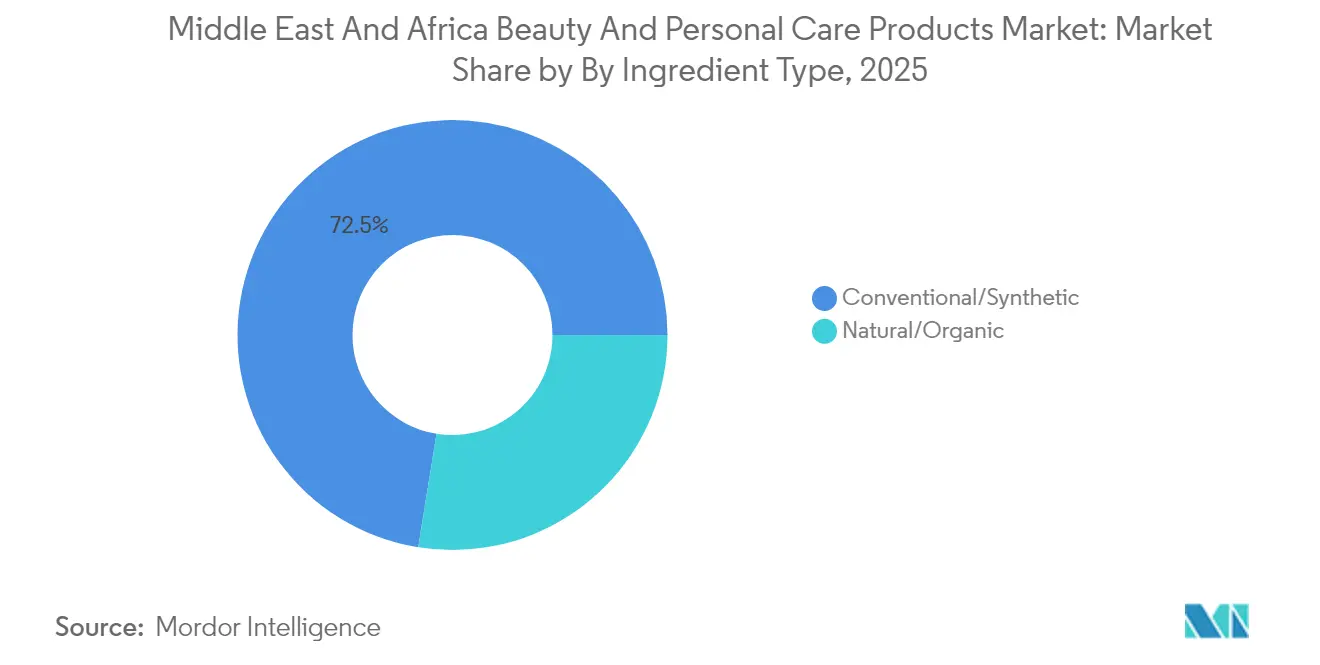

- By ingredient type, conventional/synthetic formulations held 72.45% of sales in 2025, yet natural/organic ranges are expanding at a 7.42% CAGR to 2031 owing to increasing clean-beauty adoption.

- By distribution channel, specialty stores led with 47.00% share in 2025, while online retail is advancing at an 7.78% CAGR to 2031, spearheading digital disruption across the region.

- By geography, Saudi Arabia accounted for the largest 25.20% share in 2025, whereas South Africa is poised to be the fastest-growing market, rising at 6.60% CAGR during the forcast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for clean/halal products | +1.2% | GCC, North Africa, with spillover to Nigeria, Egypt | Medium term (2-4 years) |

| Shift toward organic and natural products | +0.9% | United Arab Emirates, Saudi Arabia, South Africa | Long term (≥ 4 years) |

| Rising male grooming trends | +0.8% | Saudi Arabia, United Arab Emirates, Turkey, with expansion to Egypt, Morocco | Medium term (2-4 years) |

| Increasing social media and influencer marketing | +1.1% | Concentrated in Gulf states, urban South Africa | Short term (≤ 2 years) |

| Growing investments in advertisement, research and development, and marketing | +0.7% | Regional hubs: United Arab Emirates, Saudi Arabia, Egypt, South Africa | Long term (≥ 4 years) |

| Rising innovative and new product launches | +0.6% | Concentration in premium markets United Arab Emirates, Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preference for clean/halal products

The convergence of religious compliance and clean beauty positioning creates a unique value proposition that commands premium pricing across Muslim-majority markets. Halal certification requirements, governed by standards bodies like SMIIC (Standards and Metrology Institute for Islamic Countries), extend beyond ingredient sourcing to encompass entire manufacturing processes, creating barriers to entry that benefit established players with compliant facilities[1]Source: Standards and Metrology Institute for Islamic Countries, “Halal Product Certification,” smiic.org. This driver particularly influences the United Arab Emirates market, where Dubai Municipality's halal certification program has streamlined approval processes for international brands seeking regional distribution. The clean beauty intersection with halal requirements enables brands to capture both religious compliance and wellness-oriented consumer segments simultaneously. SGS and Cotecna provide third-party halal verification services, indicating institutional support for market expansion. The premium pricing power of halal-certified clean beauty products creates sustainable competitive advantages for brands that invest in compliant manufacturing and certification processes.

Shift toward organic and natural products

Consumer migration toward organic and natural formulations drives ingredient sourcing strategies that leverage Africa's biodiversity advantages, particularly shea butter from West Africa, argan oil from Morocco, and marula oil from Southern Africa. This trend creates vertical integration opportunities for brands seeking to control supply chains while building authentic storytelling around indigenous ingredients. Consumer willingness to pay premiums for perceived safety and efficacy benefits continues to drive growth in the organic segment, especially among educated urban populations throughout the region. Natural ingredient sourcing also aligns with sustainability narratives that resonate with younger demographics, creating brand differentiation opportunities in increasingly crowded market segments. The challenge lies in scaling organic ingredient supply chains while maintaining quality consistency and cost competitiveness against synthetic alternatives.

Rising male grooming trends

Male grooming market expansion reflects changing social attitudes and increased disposable income among young male demographics across oil-rich economies and urban centers. The trend gains momentum through social media influence and celebrity endorsements that normalize male beauty routines, particularly in traditionally conservative societies where such behaviors were previously discouraged. Pert Plus's relaunch of enhanced men's grooming ranges in the GCC, including 4-in-1 products, demonstrates how established brands adapt product portfolios to capture emerging male consumer segments. This demographic shift creates opportunities for specialized male grooming brands and forces traditional female-focused companies to develop gender-specific product lines and marketing strategies. The male grooming trend particularly benefits online retail channels, where privacy concerns about purchasing beauty products are minimized through discreet delivery options.

Increasing social media and influencer marketing

Social media platforms serve as primary product discovery and purchase decision channels, particularly among Gen Z consumers who represent 60% of Africa's population under 25 years old. Influencer marketing effectiveness stems from authentic cultural connections and local language content that resonates with diverse regional audiences across Arabic, French, and English-speaking markets. The Gulf states lead social media beauty engagement, with high smartphone penetration and disposable income creating ideal conditions for influencer-driven commerce. Digital marketing strategies must navigate cultural sensitivities while building authentic brand connections, requiring localized content creation and influencer partnerships that respect religious and social norms. The acceleration of social commerce creates direct-to-consumer opportunities that bypass traditional retail intermediaries while building deeper customer relationships through personalized engagement strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit and grey-market proliferation | -0.8% | Concentrated in Nigeria, Egypt, Morocco | Short term (≤ 2 years) |

| Stringent and fragmented regulation | -0.6% | United Arab Emirates, Saudi Arabia having streamlined processes | Medium term (2-4 years) |

| Cultural and religious sensitivities | -0.4% | Muslim-majority countries, conservative regions | Long term (≥ 4 years) |

| Underdeveloped local manufacturing ecosystem | -0.7% | Sub-Saharan Africa, with exceptions in South Africa, Egypt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of counterfeit and grey-market proliferation

Counterfeit product circulation across porous regional borders creates revenue leakage and brand reputation risks that particularly impact premium and luxury segments where authenticity commands significant price premiums. The UAE's enforcement initiatives through ESMA (Emirates Authority for Standardisation and Metrology) demonstrate regulatory responses to counterfeit proliferation, yet cross-border coordination remains limited across the broader region[2]Source: Emirates Authority for Standardization and Metrology, “Anti-Counterfeit Enforcement Updates,” esma.gov.ae. South African authorities have intensified anti-counterfeiting efforts, with customs seizures increasing in 2024, indicating both the scale of the problem and institutional responses to address it. Grey market distribution through unauthorized channels undermines official distributor networks and pricing strategies, forcing brands to invest heavily in supply chain monitoring and legal enforcement. The counterfeit challenge particularly affects online marketplaces, where consumer education about authentic product identification becomes critical for brand protection strategies.

Stringent and fragmented regulation

Regulatory complexity across diverse national frameworks requires significant compliance investments and delays market entry timelines for international brands seeking regional expansion. Saudi Arabia's SFDA streamlined cosmetic import procedures through the new GHAD system in 2024, requiring prior approval for shipments, demonstrating both regulatory evolution and ongoing complexity[3]Source: Saudi Food and Drug Authority, “SFDA Issues Certificates of Conformity for Beauty Sector Consignments via FASEH,” sfda.gov.sa. The fragmentation creates competitive advantages for established players with regulatory expertise while disadvantaging smaller brands lacking compliance resources. Different countries maintain varying standards for product registration, labeling requirements, and ingredient approvals, necessitating market-specific formulations and packaging adaptations. Regulatory compliance costs disproportionately impact emerging brands and local manufacturers, potentially limiting market competition and innovation while favoring multinational corporations with established regulatory affairs capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominance Faces Cosmetics Acceleration

Personal care products command 86.65% market share in 2025, reflecting fundamental consumer priorities around hygiene, skincare, and hair care across diverse climate conditions and cultural preferences throughout the Middle East and Africa region. The segment's dominance stems from essential product categories, including shampoos, body care, oral care, and deodorants that represent non-discretionary spending patterns regardless of economic conditions. Within Personal Care, hair care products benefit from climate-specific formulations addressing humidity and sun exposure challenges.

The cosmetics/make-up segment's superior 6.62% CAGR through 2031 signals evolving consumer behavior toward self-expression and social media-driven beauty standards, particularly among younger demographics in urban centers. The structural shift toward cosmetics reflects income growth and cultural liberalization, particularly in Gulf states, where expatriate populations introduce diverse beauty practices and product preferences. Facial cosmetics lead the makeup category, driven by social media influence and professional makeup application trends, while eye cosmetics gain traction through tutorial-driven learning and cultural acceptance of decorative products.

By Category: Mass Market Stability Enables Premium Acceleration

The mass market category holds a 57.10% share in 2025, providing market stability and volume growth. This segment serves price-conscious consumers in emerging economies, where limited disposable income is affected by economic volatility and currency fluctuations. Mass market dominance reflects the importance of accessible pricing strategies that accommodate diverse income levels while maintaining product quality and brand recognition across traditional retail channels.

The premium/luxury segment is expected to grow at a CAGR of 7.05% through 2031, driven by increasing consumer income in oil-rich economies and urban centers, where affluent consumers demand premium products and exclusive brand experiences. The premium segment benefits from aspirational purchasing behavior and social media influence that elevates luxury beauty consumption as status signaling among emerging middle-class populations. Premium segment growth particularly concentrates in Gulf states where high per-capita income and expatriate populations create demand for international luxury brands and exclusive product launches. The category segmentation creates opportunities for multi-tier brand strategies that capture both volume through mass market offerings and margin through premium positioning.

By Ingredient Type: Synthetic Dominance Challenged by Natural Innovation

Conventional/Synthetic ingredients hold a 72.45% market share in 2025, driven by their cost advantages, reliable supply chains, and established effectiveness in mass market production. These ingredients provide manufacturers with significant benefits, including lower production costs, standardized quality control processes, and proven performance metrics. The widespread use of synthetic ingredients enables manufacturers to maintain consistent product quality and shelf stability across their product lines. Additionally, synthetic ingredients support extended supply chain operations by offering predictable degradation rates, stable chemical compositions, and resistance to environmental factors that could compromise product integrity during storage and transportation in the region.

Natural/Organic ingredients' accelerated 7.42% CAGR through 2031 demonstrates consumer migration toward clean beauty propositions that align with health consciousness and environmental awareness, particularly among educated urban demographics willing to pay premiums for perceived safety benefits. The natural segment benefits from Africa's biodiversity advantages, including indigenous ingredients like shea butter, argan oil, and marula oil that create authentic storytelling opportunities and supply chain differentiation.

By Distribution Channel: Specialty Stores Leadership Faces Digital Disruption

Specialty Stores command 47.00% market share in 2025, leveraging product expertise, personalized service, and brand partnerships that create differentiated shopping experiences, particularly valued for premium and luxury beauty products. The channel's strength stems from trained staff capabilities, product demonstration opportunities, and brand storytelling that support complex purchase decisions and customer education across diverse product categories. Moreover, supermarkets/hypermarkets provide mass market accessibility and convenience purchasing that supports routine replenishment of essential personal care products, while their limited beauty expertise constrains premium product sales and brand differentiation opportunities.

Online Retail Channels' superior 7.78% CAGR through 2031 reflects digital transformation accelerated by COVID-19 behavioral changes and younger consumer preferences for convenience, privacy, and competitive pricing across traditional retail boundaries. The digital acceleration creates opportunities for direct-to-consumer strategies that bypass traditional retail intermediaries while building deeper customer relationships through personalized engagement and data-driven marketing.

Geography Analysis

Saudi Arabia leads the regional market share at 25.20% in 2025, driven by Vision 2030 economic diversification initiatives that promote local manufacturing and reduce import dependence while fostering a vibrant consumer economy. The kingdom's market leadership stems from high disposable income levels, a young demographic profile, and government support for beauty and personal care sector development through industrial investment incentives and regulatory streamlining. The Saudi market benefits from cultural acceptance of beauty products aligned with Islamic values, creating opportunities for halal-certified brands and clean beauty positioning.

South Africa exhibits the fastest regional growth at 6.60% CAGR through 2031, driven by expanding retail infrastructure, e-commerce penetration, and diverse population demographics that create demand for inclusive beauty products addressing varied skin tones and hair textures. The market benefits from established manufacturing capabilities and regulatory frameworks that support both local production and international brand entry strategies. Nigeria's market potential stems from Africa's largest population and growing urban middle class, yet infrastructure challenges and currency volatility create operational complexities for international brands seeking market entry.

The United Arab Emirates represents the region's premium beauty hub, leveraging Dubai's status as a regional commercial center and multicultural population that drives demand for diverse international brands and luxury products. The United Arab Emirates' market strength stems from a high expatriate population, tourism industry, and established retail infrastructure that supports both traditional and digital commerce channels. Egypt's market potential reflects its large population base and growing middle class, yet economic volatility and currency fluctuations create challenges for premium product positioning and import-dependent supply chains.

Competitive Landscape

The Middle East and Africa beauty and personal care products market exhibits moderate fragmentation with a concentration index of 5 out of 10, creating space for both multinational corporations and emerging local players to capture market share through differentiated positioning strategies. Established global players like Procter & Gamble, Unilever, and L'Oréal pursue localization strategies that combine international brand recognition with regional manufacturing capabilities and cultural adaptation, while emerging local brands leverage indigenous ingredients and authentic cultural connections to build competitive advantages.

The competitive intensity reflects strategic tensions between scale advantages that favor multinational corporations and cultural authenticity that benefits regional players with deep local market understanding. Technology adoption patterns reveal digital transformation as a key competitive differentiator, with brands investing in e-commerce capabilities, social media marketing, and data analytics to capture younger consumer segments and build direct customer relationships.

White-space opportunities emerge in male grooming, natural/organic formulations, and halal-certified products where consumer demand outpaces current market supply, creating entry points for specialized brands and product line extensions. The competitive landscape benefits from regulatory modernization initiatives, such as Saudi Arabia's SFDA streamlined approval processes, that reduce barriers to entry while maintaining quality standards that protect consumer interests and brand investments.

Middle East And Africa Beauty And Personal Care Products Industry Leaders

Unilever PLC

L’Oréal Group

Estée Lauder Companies

Beiersdorf AG

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Henkel Consumer Brands launched the Schwarzkopf Gliss Hair Care product line in GCC markets through an event at the Bvlgari Hotel & Resort, expanding the brand's presence in the Middle East personal care market.

- November 2024: Kosas, a clean beauty brand, launched in Saudi Arabia through Sephora Middle East. The company, founded by Sheena Zadeh, offers makeup products formulated with skin-nourishing ingredients. The brand's focus on skincare-infused cosmetics aligns with consumer preferences in the Saudi market.

- April 2024: Kay Beauty, a makeup brand founded by Katrina Kaif, expanded into the United Arab Emirates market. The brand has established an omnichannel retail presence through a partnership with retailer Nysaa. The brand's focus on developing products for diverse skin types aligns with the GCC region's multicultural consumer base, which spans various ethnicities, age groups, and genders.

Middle East And Africa Beauty And Personal Care Products Market Report Scope

Beauty and personal care are an art field that addresses the looks and health of someone's hair, nails, and skin.

The scope of the Middle East and Africa beauty and personal care products market includes segmentation of the market based on category, product type, distribution channel, and geography. By category, the market is segmented as mass, premium, and super-premium/luxury. By product type, the market is segmented as personal care products and cosmetics/make-up products. The personal care products are further segmented into hair care products, skincare products, bath and shower, oral care, men's grooming, and deodorants and antiperspirants. The hair care products are sub-segmented into shampoo, conditioners, hair styling and coloring products, and other hair care products. Skincare products are further sub-segmented into facial care products, body care products, and lip care products. The bath and shower segment is further sub-segmented into soaps, shower gels, and other bath and shower products. Oral care is further sub-segmented into toothbrushes and replacements, toothpaste, mouthwashes and rinses, and other oral care products. The cosmetics/make-up products are further sub-segmented into facial cosmetics, eye cosmetic products, and lip and nail make-up products. By distribution channel, the market is segmented as supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into the United Arab Emirates, Saudi Arabia, South Africa, and the Rest of Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Personal Care Products | Hair Care Products | Shampoo |

| Conditioners | ||

| Hair Colors | ||

| Hair Styling Products | ||

| Other Hair Care Products | ||

| Skin Care Products | Facial Care Products | |

| Body Care Products | ||

| Lip Care Products | ||

| Bath and Shower | Soaps | |

| Shower Gels | ||

| Other Bath and Shower Products | ||

| Oral Care | Toothbrushes and Replacements | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Other Oral Care Products | ||

| Men’s Grooming | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Make-up | |

| Eye Make-up | ||

| Lip and Nail Make-up Products | ||

By Category

| Mass |

| Premium/Luxury |

By Ingredient Type

| Conventional/Synthetic |

| Natural/Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Channels |

| Other Distribution Channels |

By Geography

| South Africa |

| Saudi Arabia |

| United Arab Emirates |

| Nigeria |

| Egypt |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Personal Care Products | Hair Care Products | Shampoo |

| Conditioners | |||

| Hair Colors | |||

| Hair Styling Products | |||

| Other Hair Care Products | |||

| Skin Care Products | Facial Care Products | ||

| Body Care Products | |||

| Lip Care Products | |||

| Bath and Shower | Soaps | ||

| Shower Gels | |||

| Other Bath and Shower Products | |||

| Oral Care | Toothbrushes and Replacements | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Other Oral Care Products | |||

| Men’s Grooming | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Make-up | ||

| Eye Make-up | |||

| Lip and Nail Make-up Products | |||

| By Category | Mass | ||

| Premium/Luxury | |||

| By Ingredient Type | Conventional/Synthetic | ||

| Natural/Organic | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Stores | |||

| Online Retail Channels | |||

| Other Distribution Channels | |||

| By Geography | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

How fast is the Middle East and Africa beauty and personal care products market expected to grow to 2031?

It is forecast to expand at a 5.34% CAGR, moving from USD 32.77 billion in 2026 to USD 42.5 billion by 2031.

Which product category shows the quickest growth momentum?

Cosmetics/make-up lines are climbing at 6.62% CAGR as social-media-driven self-expression gains regional traction.

Which country is poised for the fastest growth through 2031?

South Africa leads with a projected 6.60% CAGR owing to inclusive shade ranges and maturing e-commerce infrastructure.

What distribution channel is disrupting traditional retail most?

The online retail market is growing at a CAGR of 7.78%, driven by increased smartphone adoption and social media commerce through influencer marketing, especially in GCC countries.

Page last updated on: