Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

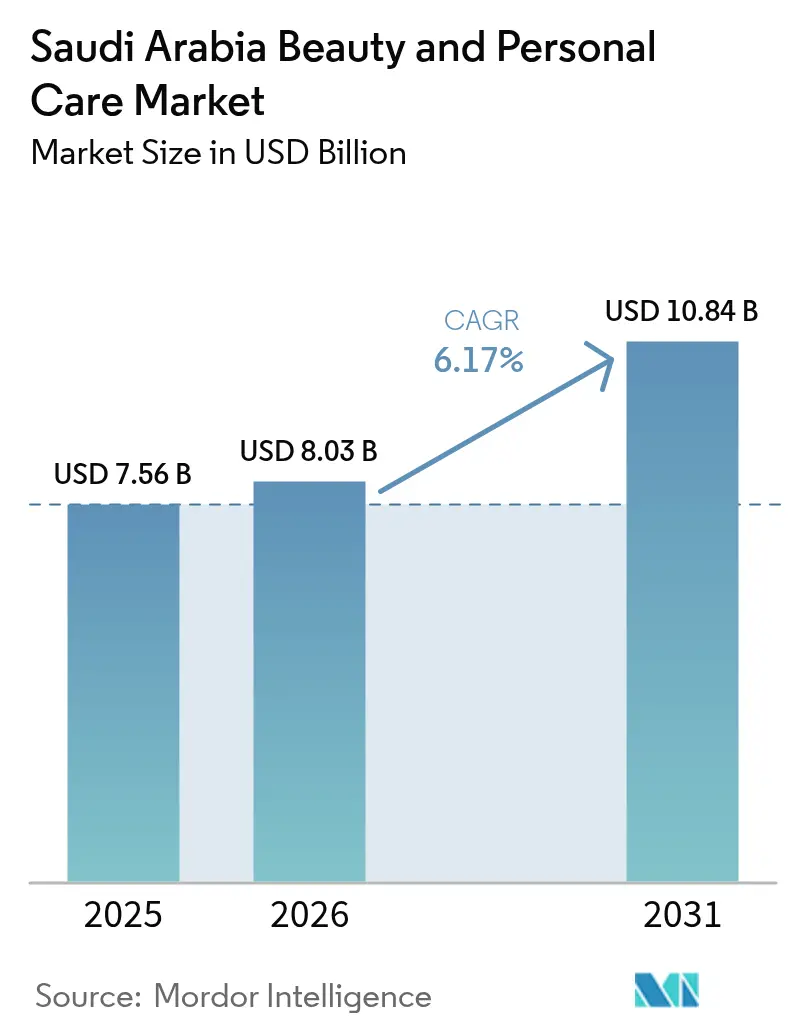

| Base Year Market Size (2025) | USD 7.56 Billion |

| Market Size (2026) | USD 8.03 Billion |

| Market Size (2031) | USD 10.84 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

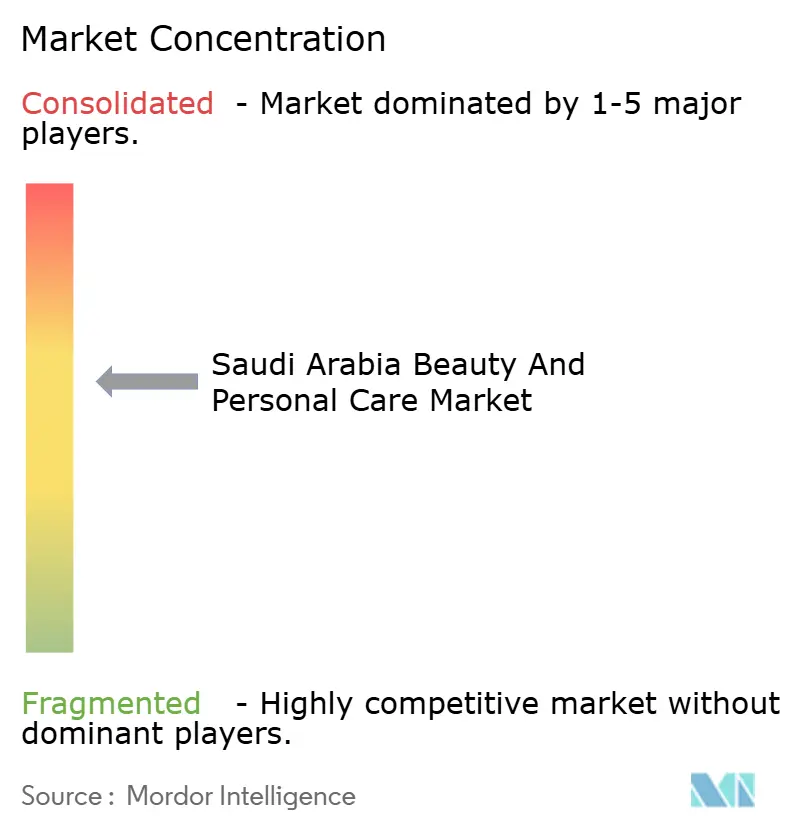

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Beauty And Personal Care Market Analysis by Mordor Intelligence

The Saudi Arabia beauty and personal care market size is expected to grow from USD 7.56 billion in 2025 to USD 8.03 billion in 2026 and is forecast to reach USD 10.84 billion by 2031 at 6.17% CAGR over 2026-2031. This trajectory reflects structural shifts in consumer behavior, regulatory modernization, and the Kingdom's Vision 2030 agenda, which has elevated female workforce participation from 17.4% in 2017 to 36% by the first quarter of 2023, surpassing the program's original 30% target[1]Source: Saudi Arabia 2030, "Saudi Vision 2030", vision2030.gov. Personal care holds the lion’s share of current spending, yet decorative cosmetics deliver the quickest volume gains as liberalizing social norms encourage broader makeup usage among working women. Higher female labor participation, stringent halal certification, and Vision 2030 tourism targets form a multi-layered demand engine that rewards brands offering both efficacy and cultural alignment. Clean-beauty labels are scaling fast because natural formulations satisfy halal, ethical, and skin-health criteria while desert-proof technologies keep texture performance intact. Competitive intensity sits at a moderate level because multinational incumbents dominate the shelf, yet local digital-native challengers exploit influencer networks and regulatory familiarity to carve profitable niches.

Key Report Takeaways

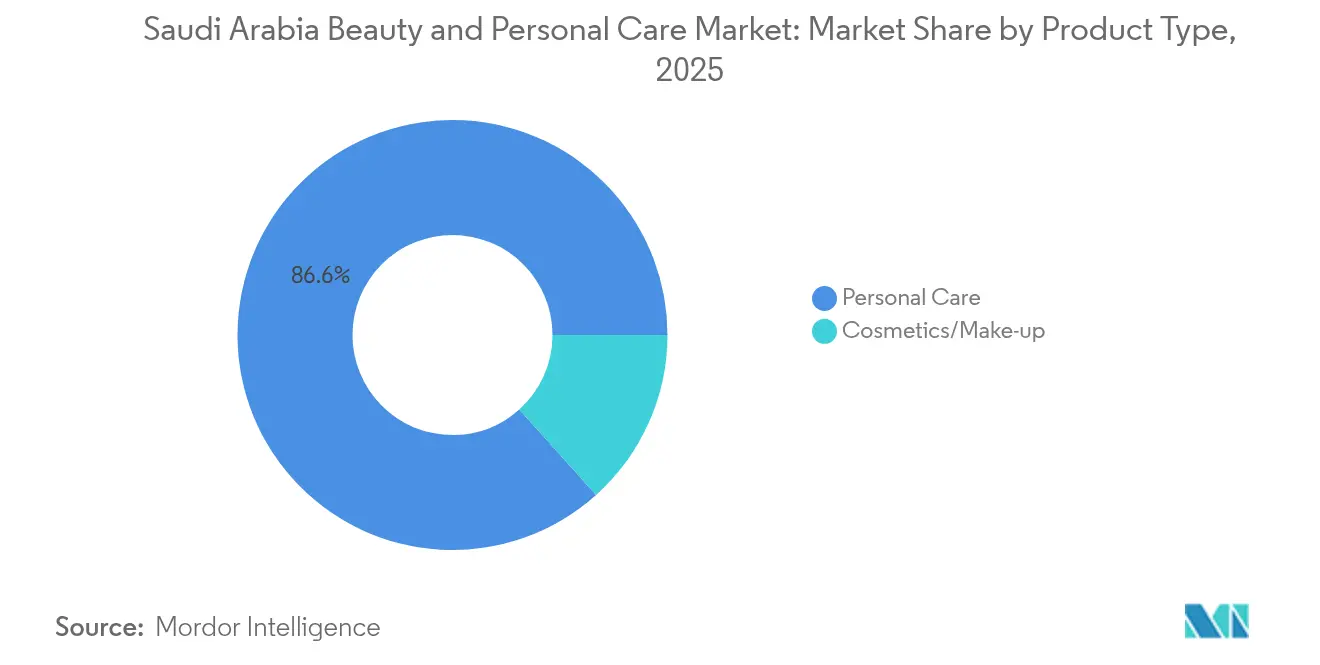

- By product type, personal care commanded 86.64% of the beauty and personal care market share in 2025, while cosmetics are expanding at a 6.61% CAGR through 2031.

- By category, the mass segment accounted for 60.78% of the beauty and personal care market size in 2025, whereas premium offerings are set to grow at a 6.62% CAGR to 2031.

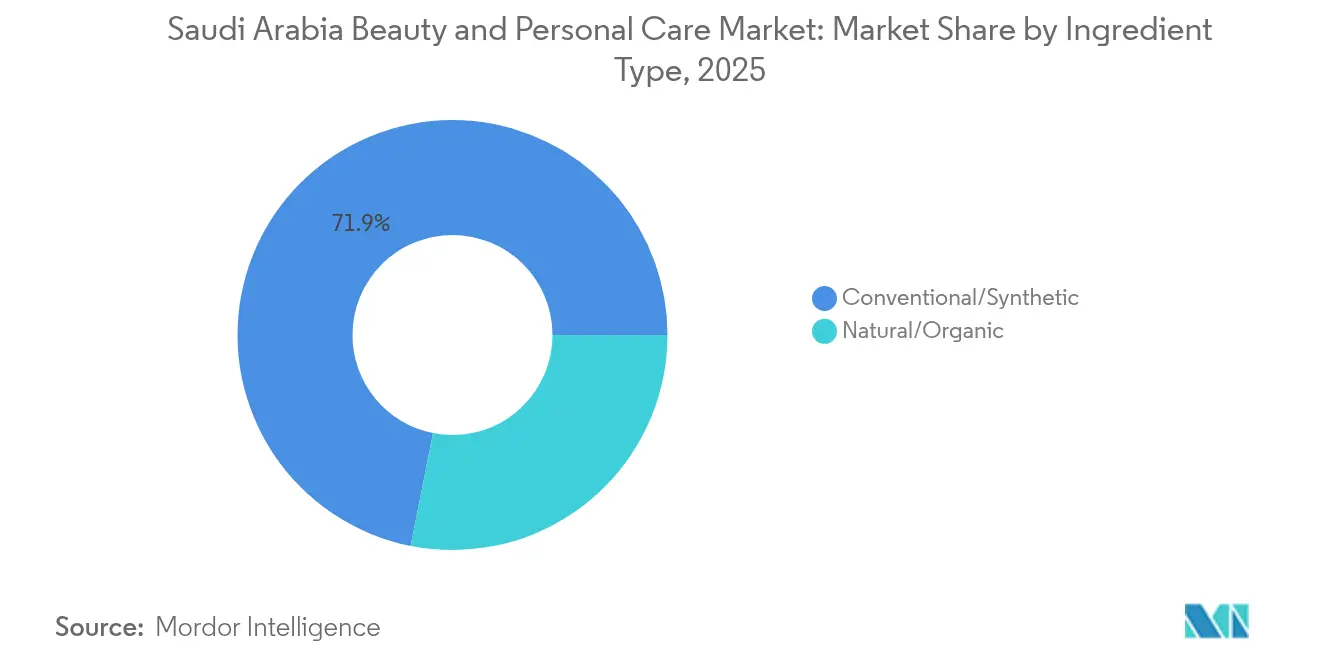

- By ingredient type, conventional formulations retained 71.88% share in 2025, and natural products are forecast to climb at a 6.72% CAGR over 2026-2031.

- By distribution channel, specialty retailers controlled 56.77% of 2025 sales, yet online retail is on track for the quickest rise at 7.65% CAGR through 2031.

- By gender focus, men’s grooming reached USD 802.35 million in 2023 and is anticipated to accelerate at a 6.08% CAGR to USD 1.29 billion by 2031 as social acceptance of male self-care widens.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Beauty And Personal Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High social-media influence on beauty trends | +1.2% | National, with concentration in Riyadh, Jeddah, and urban centers | Short term (≤ 2 years) |

| Rising demand for halal-certified cosmetics | +0.8% | National, with spillover to GCC markets | Long term (≥ 4 years) |

| Expanding men's grooming and personal care usage | +0.6% | National, with early adoption in Eastern Province and Jeddah | Long term (≥ 4 years) |

| Rising female workforce participation and grooming needs | +1.0% | National, with the highest gains in Riyadh and major employment hubs | Medium term (2-4 years) |

| Preference for premium, dermatologically tested products | +0.9% | National, skewed toward high-income urban consumers | Medium term (2-4 years) |

| Younger, digitally-savvy consumer base | +1.1% | National, driven by Gen Z and millennials (70% under 30) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Social-Media Influence on Beauty Trends

Instagram's penetration among Gen Z Saudi females has transformed product discovery into a real-time, influencer-mediated process that compresses brand-building cycles. TikTok and Snapchat amplify this effect, with online beauty purchases now originating from social or chat commerce channels such as WhatsApp and Instagram Shopping. L'Oréal's positioning of Saudi Arabia as a USD 2 billion market with significant internet penetration underscores the platform's role as a demand generator, not merely a marketing channel. Brands that fail to maintain daily content cadence or secure micro-influencer partnerships risk invisibility among the 60% of Gen Z consumers who cite skincare as their top purchase motivation. This dynamic favors agile digital-native brands over legacy players with slower go-to-market processes.

Rising Demand for Halal-Certified Cosmetics

SFDA's mandatory halal certification for certain product categories and the GCC Standardization Organization's GSO 1943:2024 standard create a compliance framework that differentiates Saudi Arabia from secular markets. Halal certification extends beyond ingredient sourcing to encompass manufacturing processes, supply-chain traceability, and packaging materials, raising entry barriers for international brands unfamiliar with Islamic jurisprudence [2]Source: SFDA Regulatory Guideline, " Islamic jurisprudence" sfda.gov.sa. Local brands such as AÏZA leverage heritage ingredients like AlUla Peregrina oil, featured in Cartier's fragrance collaborations- to signal authenticity, while multinational entrants must navigate certification timelines that can extend 6 to 12 months. Most of the Middle Eastern consumer preference for natural and botanical ingredients intersects with halal mandates, creating a sweet spot for clean-beauty formulations that meet both ethical and religious criteria.

Expanding Men's Grooming and Personal Care Usage

Saudi men's grooming market expansion reflects cultural recalibration around male self-care, accelerated by Vision 2030's emphasis on lifestyle diversification. Beiersdorf's 2024 launch of NIVEA MEN Deep Clean Face Wash in Saudi Arabia and Henkel's Schwarzkopf Professional salon product expansion signal multinational recognition of this segment's latent potential. The Eastern Province, with its expatriate-influenced consumer base, exhibits higher per-capita spending on male grooming than conservative inland regions, suggesting geographic segmentation strategies. However, the segment remains underpenetrated relative to female personal care, offering first-mover advantages to brands that localize messaging around modesty and functionality rather than vanity.

Rising Female Workforce Participation and Grooming Needs

Female economic participation's contribution of SAR 18 billion (USD 4.8 billion) to Saudi GDP in 2022 has created a professional-grooming category that barely existed a decade ago[3]Source: Saudi Ministry of Economy, "Female economic participation", mep.gov.sa. The workforce participation rate translates into demand for time-efficient, multi-functional products such as BB creams, tinted moisturizers, and express hair-care solutions. Saudi women's average use of 9 makeup products daily, versus 7 in Europe, and 4.7 products per facial routine, indicates a high-intensity grooming culture that professional obligations are amplifying rather than constraining. This demographic shift favors premium personal care over decorative cosmetics, as working women prioritize skincare maintenance and subtle enhancement over bold makeup looks that may clash with workplace norms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory requirements hinder growth | -0.5% | National, with uniform SFDA enforcement | Short term (≤ 2 years) |

| Risk of counterfeit and low-quality products undermining trust | -0.4% | National, with hotspots in Riyadh, Dammam, and Al-Khobar | Medium term (2-4 years) |

| Fragmented consumer preferences are hindering brand loyalty | -0.3% | National, with regional variations (Riyadh conservative, Jeddah cosmopolitan) | Medium term (2-4 years) |

| Logistic and import constraints for international brands | -0.4% | National, with port congestion at Jeddah Islamic Port and King Abdulaziz Port | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Requirements Hinders Growth

SFDA's FASEH system mandates pre-market notification for all cosmetics and personal care products, requiring manufacturers to submit ingredient lists, safety data, and manufacturing-site certifications before commercial distribution. The GCC Standardization Organization's GSO 1943:2024 and GSO 2528 standards impose additional labeling, packaging, and quality-control requirements that international brands must navigate alongside Saudi-specific halal certification. Compliance timelines range from 2 to 6 months for straightforward products but can extend to 12 months for novel ingredients or claims requiring clinical substantiation. The 5% customs duty on cosmetics and toiletries, combined with Certificate of Origin, Commercial Invoice, Packing List, and Bill of Lading documentation requirements, adds 2 to 4 weeks to import cycles, disadvantaging brands reliant on just-in-time inventory models. These frictions favor multinational incumbents with dedicated regulatory affairs teams and local manufacturing footprints, such as L'Oréal's Jeddah facility, which bypasses import bottlenecks entirely.

Risk of Counterfeit and Low-Quality Products Undermining Trust

The Saudi Ministry of Commerce's seizure of 6 million counterfeit products, including 400,000 cosmetics units, and subsequent 2019 raids netting 597,000 fake cosmetics in Riyadh retail chains and Dammam-Al-Khobar distribution networks reveal the scale of gray-market infiltration, according to the Saudi Ministry of Commerce. An 89% consumer self-reported purchase rate of counterfeit products in a study, though predating recent enforcement intensification, suggests trust erosion that legitimate brands must continuously combat through authentication technologies and consumer education. SFDA's closure of 35 perfume outlets and seizure of 192,398 perfume bottles during Riyadh inspections demonstrate regulatory vigilance, yet penalties of up to 3 years imprisonment and SAR 1 million (USD 266,667) fines have not eliminated the problem. Counterfeit proliferation disproportionately harms premium brands, as price-sensitive consumers may knowingly purchase fakes, while affluent buyers who unknowingly acquire counterfeits experience brand disillusionment that depresses repeat purchases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Anchors Volume, Cosmetics Drive Growth

Personal care's 86.64% share in 2025 reflects the segment's breadth, encompassing skincare, hair care, bath and shower, deodorants, and oral care, and its embeddedness in daily routines across all demographic cohorts. Cosmetics and makeup products, despite holding the remaining 13.36% share, are forecast to grow at 6.61% CAGR from 2026 to 2031, outpacing personal care's more modest expansion. This divergence stems from the low base effect in decorative cosmetics, where Saudi Arabia's cultural norms historically constrained usage, and the recent liberalization of social codes under Vision 2030, which has normalized makeup application in professional and social settings. Procter & Gamble's 2024 launch of Olay Regenerist Collagen Peptide 24 across the Middle East, including Saudi Arabia, exemplifies multinational's focus on anti-aging skincare within the personal care umbrella. Hair care benefits from the Kingdom's climate, which necessitates frequent washing and conditioning, while oral care maintains steady demand driven by public health campaigns. The cosmetics segment's acceleration is further propelled by social media tutorials that demystify application techniques, reducing the skill barrier that previously deterred novice users.

SFDA's cosmetovigilance system, which mandates adverse-event reporting for both personal care and cosmetics, ensures product safety but also imposes post-market surveillance costs that smaller brands struggle to absorb. Johnson & Johnson's 2024 expansion of its Neutrogena Hydro Boost line and launch of Aveeno Baby Eczema Therapy in Saudi Arabia illustrate how established players leverage regulatory compliance as a competitive moat. The personal care segment's maturity limits margin expansion opportunities, whereas cosmetics' premiumization potential, evidenced by Estée Lauder's Tom Ford Beauty launch, offers higher per-unit profitability. However, the instruction to minimize cosmetics content in this report aligns with personal care's dominant revenue contribution and its alignment with the market's utilitarian consumption patterns.

By Category: Mass Dominance Masks Premium's Momentum

The mass category's 60.78% share in 2025 underscores price sensitivity among Saudi Arabia's broad consumer base, yet the premium segment's 6.62% CAGR from 2026 to 2031 signals a wealth effect among the Kingdom's expanding affluent class. Premium products' appeal lies in their dermatological validation, prestige packaging, and association with international luxury brands that confer social status. Shiseido's USD 400-500 million acquisition of Dr. Dennis Gross Skincare in February 2024, explicitly targeting Middle East expansion, reflects strategic conviction in premium growth. Paris Gallery's 65+ stores across the GCC, with significant Saudi presence, serve as premium distribution anchors, offering curated assortments and personalized consultations that mass retailers cannot replicate. The mass segment's resilience stems from its accessibility through supermarkets, hypermarkets, and neighborhood stores, which serve price-conscious consumers and those in smaller cities lacking specialty retail infrastructure.

Unilever's Dove "Real Beauty" campaign in Saudi Arabia during 2024, partnering with Noon.com for distribution, illustrates how mass-market brands are adopting premium marketing tactics, emotional storytelling, and influencer partnerships to defend share against trading-up consumers. The category bifurcation creates strategic dilemmas for mid-tier brands, which risk being squeezed between mass players' scale economies and premium brands' aspirational positioning. Bath & Body Works' opening of a flagship store in Riyadh Park in 2024, with plans for 10+ Saudi locations by 2025, represents a mass-premium hybrid strategy targeting the "affordable luxury" segment. The premium segment's growth will likely concentrate in Riyadh and Jeddah, where per-capita incomes exceed national averages, while the mass category retains dominance in secondary cities and rural areas.

By Ingredient Type: Synthetic Leads, Natural Gains Ground

Conventional and synthetic ingredients' 71.88% share in 2025 reflects their cost efficiency, formulation stability, and decades of safety data that satisfy regulatory requirements. Natural and organic ingredients, commanding the remaining 28.12% share, are forecast to grow at a 6.72% CAGR from 2026 to 2031, driven by clean-beauty narratives and consumer perception, often scientifically unfounded, that "natural" equals "safer." Kosas' 2024 launch in Saudi Arabia via Sephora, positioning itself as clean and cruelty-free, taps into this sentiment, as do local brands Asteri (vegan, desert-proof) and AÏZA (heritage ingredients).

AlUla Peregrina oil, an indigenous Saudi ingredient featured in Cartier fragrance collaborations, exemplifies how natural ingredients can convey cultural authenticity and command premium pricing. However, natural formulations face stability challenges in Saudi Arabia's extreme heat, requiring advanced encapsulation technologies or cold-chain logistics that inflate costs. Conventional ingredients' dominance in hair care and oral care, categories where performance trumps ingredient origin, will likely persist, whereas skincare and body care present greater natural-ingredient penetration opportunities. SFDA's ingredient-approval process does not discriminate between natural and synthetic, requiring equivalent safety documentation, which levels the regulatory playing field but disadvantages small natural-beauty brands lacking toxicology budgets.

By Distribution Channel: Specialty Stores Hold, Online Surges

Specialty stores' 56.77% share in 2025 reflects their consultative selling model, product-trial opportunities, and curated assortments that reduce choice overload for consumers navigating thousands of SKUs. Online retail, despite a smaller current share, is forecast to grow at a 7.65% CAGR from 2026 to 2031, propelled by mobile commerce's share of digital transactions during peak shopping periods like Ramadan and Nice One Beauty's demonstration of pure-play e-commerce viability. The platform's 28,000+ products and 1,200+ brands offer selection breadth that physical stores cannot match, while user reviews and AI-driven recommendations replicate, and often surpass, in-store consultations. Supermarkets and hypermarkets serve as convenience channels for replenishment purchases of shampoo, toothpaste, and deodorants, but lack the ambiance and expertise to drive discovery in premium categories.

Saudi Arabia's e-commerce market expansion provides infrastructure tailwinds for online beauty retail. Social and chat commerce via WhatsApp, Instagram, and TikTok, driving a significant share of online purchases, blur the line between content and commerce, enabling impulse buying that specialty stores' appointment-based models cannot capture. However, online's inability to offer tactile product trials, critical for fragrances and color cosmetics, will preserve specialty stores' role in initial purchases, with online serving as a replenishment and discovery channel for established preferences.

Regulatory Landscape

Saudi Arabia regulates beauty and personal care mainly through the Saudi Food and Drug Authority (SFDA). Cosmetics must be notified/listed prior to importation or commercial trading via SFDA electronic systems, supported by defined documentation needed for customs clearance. In January 2025, SFDA guidance on cosmetic product notification and clearance conditions tightened procedural requirements around dossier completeness, safety substantiation, and supply-chain documentation, while maintaining alignment with GCC technical requirements applicable in the Kingdom.

On standards and ingredients, the compliance baseline builds on GCC standards, including GSO 1943:2024 and GSO 2528, and recognized GMP expectations such as ISO 22716. SFDA also applies controls on labeling and claims, alongside its maintained prohibited and restricted substances lists. SFDA issued an updated prohibited ingredients list in July 2026 and published Products Classification Guidance (Version 9) in January 2026, which increases the precision of category and claim interpretation for notifications and inspections and raises the operational importance of regulatory affairs capabilities for both importers and local manufacturers.

Competitive Landscape

The Saudi Arabia beauty and personal care market's moderate concentration reflects a competitive structure where multinational incumbents, L'Oréal, Unilever, Procter & Gamble, Estée Lauder, and Beiersdorf command significant share through brand portfolios spanning mass to prestige, yet face encroachment from digital-native disruptors and local brands exploiting cultural authenticity. Strategic patterns center on localization, with L'Oréal's USD 100 million Jeddah factory and its planned second Saudi facility in 2025 exemplifying a shift from import-dependent models to in-country manufacturing that compresses lead times, mitigates tariff exposure, and signals long-term commitment to regulators and consumers.

Omnichannel integration has become table stakes, as evidenced by Unilever's Dove partnership with Noon.com and Nice One Beauty's 95% mobile-app sales penetration, forcing specialty retailers like Paris Gallery to invest in digital storefronts and loyalty programs that bridge physical and online experiences. Opportunities cluster around men's grooming, where the market size suggests underpenetration relative to female personal care and clean beauty, where local brands Asteri, AÏZA, and Lora are carving niches that multinational mass-market portfolios have yet to address comprehensively. Emerging disruptors leverage social commerce and influencer partnerships to bypass traditional retail gatekeepers, a dynamic that Nice One Beauty's 2024 IPO, raising capital to expand its 1,200-brand, 28,000-product catalog, validates as a scalable model.

Technology deployment extends beyond e-commerce infrastructure to AI-driven personalization, virtual try-on tools for color cosmetics, and blockchain-based authentication to combat the counterfeit epidemic that saw 6 million fake products seized. Shiseido's February 2024 acquisition of Dr. Dennis Gross Skincare for USD 400-500 million, targeting Middle East expansion, illustrates how M&A serves as a fast-track to premium positioning and dermatological credibility that organic brand-building would require years to establish. However, the market's fragmented consumer preferences, Gen Z's skincare obsession versus millennials' brand loyalty versus older cohorts' mass-market orientation, create execution risk for one-size-fits-all strategies, rewarding brands that segment marketing and product development by age, income, and regional culture.

Saudi Arabia Beauty And Personal Care Industry Leaders

-

L'Oréal S.A.

-

Beiersdorf AG

-

Unilever PLC

-

The Procter & Gamble Company

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory tightening around notification, ingredient restrictions, and classification is creating actionable openings for brands that can treat compliance as a speed and trust advantage, particularly for clean and halal-aligned positioning where documentation, traceability, and manufacturing controls are central. The July 2026 SFDA update to the prohibited ingredients list and the January 2026 classification guidance support product renovation cycles, including reformulation, claim rework, and SKU rationalization. They also increase demand for locally knowledgeable authorized representatives, testing partners, and quality systems built to ISO 22716 and applicable GSO standards.

Beyond demand pull, localization and capability-building are emerging as practical opportunity themes. In May 2026, L'Oréal opened a new office in Jeddah and linked the expansion to workforce development through professional training partnerships with Saudi universities, signaling continued investment in local commercial execution and talent pipelines across beauty retail and salon ecosystems. In parallel, PIF-owned Halal Products Development Co. (HPDC) announced an investment in Believe in May 2024 that included relocating the company headquarters to Saudi Arabia and constructing a local manufacturing facility, which points to a pathway for in-Kingdom production and halal-oriented export platforms and reduces dependence on import lead times for fast-moving personal care ranges.

Recent Industry Developments

- May 2026: L'Oréal opened a new office in Jeddah and linked the expansion to local talent development, including a professional hairdressing academy initiative with Princess Nourah bint Abdulrahman University, Imam Abdulrahman Bin Faisal University, and Effat University. The move strengthens in-country commercial and training capabilities for professional and consumer beauty, supporting faster activation across retail and salon channels. It also reinforces localization in a market where regulatory compliance and speed-to-shelf shape competitiveness.

- November 2025: JEONG FAMILY partnered with Nice One to introduce the ILY brand in Saudi Arabia, positioning it with dermatologically tested, halal-ready formulations designed for young skin. The partnership uses a scaled local e-commerce platform to accelerate distribution and discovery, reflecting how digital-first routes can reduce reliance on physical shelf space while still meeting product positioning requirements. It also adds competitive pressure in clean and youth-focused skincare subsegments.

- February 2024: Shiseido acquired Dr. Dennis Gross Skincare for USD 400-500 million, with an explicit strategic focus on supporting expansion in the Middle East. The deal strengthens Shiseido's premium, dermatology-led skincare proposition and broadens the set of clinically positioned brands competing for high-value consumers in Saudi Arabia. It also signals continued M&A-led portfolio building aimed at credibility in performance skincare.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market represents the value of beauty and personal care products sold in Saudi Arabia across cosmetics and personal care, counted at the point of sale through major retail and online channels.

Scope exclusions: It excludes professional salon services and clinical procedures, and it also excludes devices that are not primarily sold as consumable beauty or personal care products.

Segmentation Overview

-

Product Type

- Personal Care

- Cosmetics/Makeup Products

-

Category

- Mass

- Premium

-

Ingredient Type

- Natural/Organic

- Conventional/Synthetic

-

Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set a consistent fact base and to align definitions with what is actually sold in Saudi Arabia. We first checked consumer and macro indicators from public sources such as the General Authority for Statistics (GASTAT), Saudi Central Bank releases, and World Bank and IMF datasets to understand income direction, inflation, and overall household spending.

To anchor category context, we also reviewed Saudi Food and Drug Authority communications on regulated product themes, UN Comtrade trade statistics for relevant HS-coded flows, and selected peer-reviewed journals that discuss hygiene, skincare, and cosmetics usage patterns in the region. Company annual reports, investor presentations, association websites, and reputable press coverage were then used to confirm channel expansion, brand launches, and pricing signals. In a few cases, paid subscriptions were used for company financials and for shipment-level import and export checks, so the model inputs stayed realistic. The desk sources mentioned here are illustrative only, and additional references were used across data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives value growth in Saudi Arabia, specifically mass versus premium mix shifts, discounting behavior, and channel margins across modern trade and e-commerce. We spoke with a balanced set of stakeholders such as brand and distributor teams, retail and online operators, and industry specialists, with coverage that reflects the main demand centers and shopper profiles in the country.

These conversations helped address gaps that do not show up in public datasets, and they were also used to pressure-test assumptions before finalizing the model outputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 13% | |

| Mid tier: 45% | Functional/Unit leaders: 36% | |

| Smaller Players: 16% | Managers: 51% |

Market-Sizing & Forecasting

Sizing started with a top-down build, translating Saudi Arabia consumer spend direction and retail sell-out signals into value pools for beauty and personal care. To keep the model practical, we used inputs such as population and urbanization trends, disposable income movement, women workforce participation signals, average selling price movement by category, and the share shift toward online retail.

The totals were then corroborated with selective bottom-up approximations, mainly by checking a sample of supplier and distributor revenue exposure to Saudi Arabia and by using sampled price points multiplied by likely consumption volumes for a few high-velocity categories. Where company disclosure was limited, gaps were handled by using interview-based channel mix ranges and then tightening them through follow-up checks.

For forecasting, scenario analysis was used to reflect different paths for inflation, premiumization, and channel mix, before settling on the most probable track supported by expert feedback. Assumptions were refreshed when multiple respondents pointed to a clear pricing reset or demand softening in a particular year.

Data Validation & Update Cycle

Validation was done through repeated cross-checks between the model output and independent signals such as import direction for key product groups, visible pricing behavior in mainstream shopping baskets, and channel growth narratives from retailers and distributors. When a value jump looked too high or too low, we traced the drivers back to the input level, and respondents were re-contacted if the variance could not be explained through desk checks.

Before sign-off, outputs go through multi-step internal review so category totals, growth rates, and implied pricing remain consistent across the set. The report is refreshed annually, and interim updates are triggered when material events occur, such as regulatory changes, major tax or pricing actions, or sharp shifts in consumer demand. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Saudi Arabia Beauty and Personal Care Market Size Compared Against Other Published Estimates

Published market values for Saudi Arabia beauty and personal care often do not match because different researchers do not count the same product lines, and they also make different assumptions on pricing and channel mix. Divergence is common when one estimate uses a narrow retail basket, and another includes a wider set of personal care categories and purchasing occasions.

Some sources restrict coverage to selected categories with clearer retail tracking, or they apply conservative price progression that keeps premium growth muted. Other published figures may fold in adjacent spend like salon services. For Mordor Intelligence, only packaged beauty and personal care products sold through specialty stores, supermarkets and hypermarkets, and online retail are counted, and salon services are kept out so the total stays tied to product sell-through.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.56 B (2025) | |

| Industry Research Publisher A | USD 4.80 B (2025) | Uses a narrower product basket and tends to emphasize selected categories, which can leave out sizable parts of everyday personal care sold through general retail. |

| Consultancy Report B | USD 6.80 B (2025) | Applies more conservative assumptions on ASP progression and premium mix, and it also uses a different channel split that can understate modern trade and online value. |

The table shows that most of the spread comes from scope and from how price and premium mix are treated in the base year. When inputs are kept linked to visible signals like category mix, channel shares, and realistic price ladders, it becomes easier to explain differences and to update the model when conditions change.

Key Questions Answered in the Report

How large is Saudi Arabia’s beauty and personal care market in 2026?

The beauty and personal care market size stands at USD 8.03 billion in 2026 and is forecast to hit USD 10.84 billion by 2031.

What is the expected growth rate of premium beauty products?

Premium products are projected to expand at a 6.62% CAGR between 2026 and 2031, outpacing mass lines.

Which distribution channel is growing fastest?

Online retail is set for the quickest ascent at a 7.65% CAGR thanks to 90% mobile-commerce penetration and social-commerce integration.

Why is halal certification important in the Saudi beauty sector?

SFDA and GCC standards mandate halal compliance for many categories, making certification essential for shelf access and consumer trust.

Page last updated on: