Gulf Cooperation Council Fragrances And Perfumes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

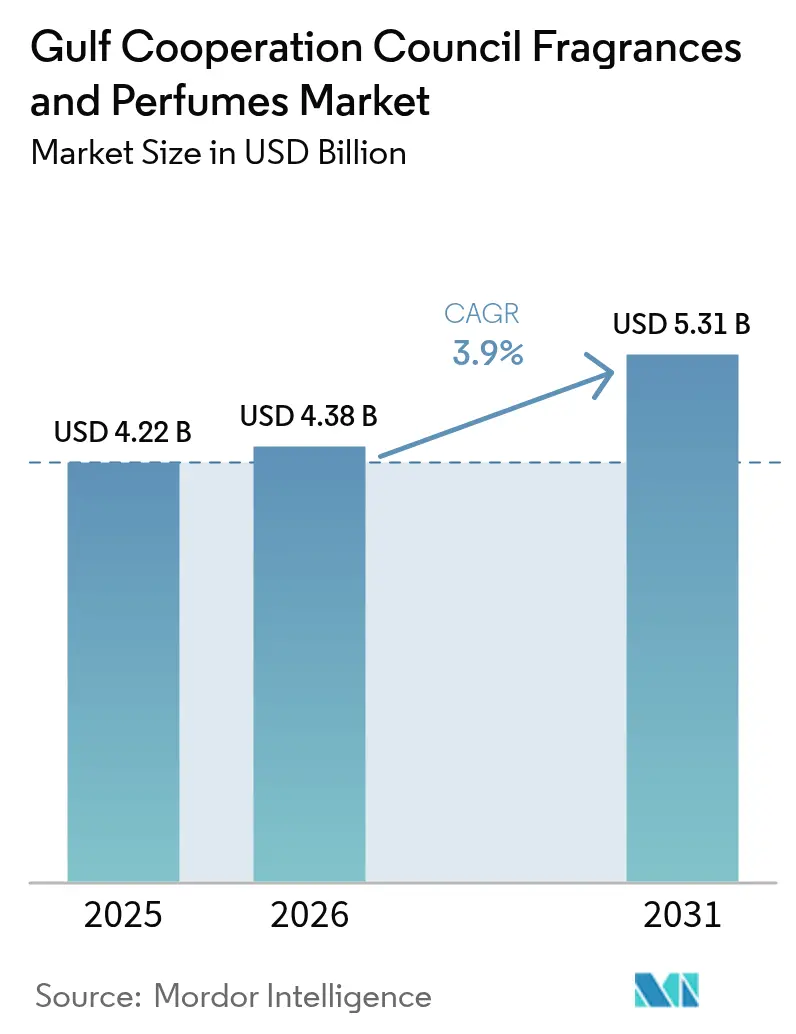

| Base Year Market Size (2025) | USD 4.22 Billion |

| Market Size (2026) | USD 4.38 Billion |

| Market Size (2031) | USD 5.31 Billion |

| Growth Rate (2026 - 2031) | 3.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gulf Cooperation Council Fragrances And Perfumes Market Analysis by Mordor Intelligence

The GCC fragrances and perfumes market size was valued at USD 4.22 billion in 2025 and estimated to grow from USD 4.38 billion in 2026 to reach USD 5.31 billion by 2031, at a CAGR of 3.90% during the forecast period (2026-2031). Rooted in cultural heritage, the Gulf Cooperation Council (GCC) fragrance market is now a canvas of modern luxury and innovation. Once dominated by traditional oriental scents, the region's perfume industry has seamlessly woven Eastern and Western influences, crafting unique signature fragrances. The market's structure underscores this evolution: while Arabian Oud remains a frontrunner, there's a clear nod to contemporary trends, showcasing a blend of tradition and modernity. Retail innovations and experiential marketing strategies are reshaping the market landscape. Take, for instance, Gucci's pop-up store at the iconic Burj Al Arab, where patrons are treated to an immersive luxury fragrance shopping journey. In a similar vein, the UAE's premium brand Lecmo unveiled 'The Blue' collection, merging traditional elements with a modern touch. As consumer preferences tilt towards premium and artisanal fragrances, there's a burgeoning demand for unique, personalized scent experiences. This trend was palpable at a major perfume exhibition in Riyadh, which showcased over 200 regional and international brands. The event served as a launchpad for new products and custom fragrance creations, underscoring the industry's pivot towards sophistication and personalization in response to evolving consumer tastes. Retail strategies are evolving, with celebrity collaborations taking center stage to bolster brand visibility and deepen consumer engagement. For example, Paris Hilton's "Ruby Rush" perfume debut at Debenhams in the Mall of the Emirates, where she made a personal appearance, signing units.

Key Report Takeaways

- By product type, Eau de Parfum led with 64.72% of the GCC fragrances and perfumes market share in 2025; Eau de Toilette is projected to post the fastest 4.62% CAGR through 2031.

- By category, luxury fragrances captured 80.78% of 2025 revenue, while the segment is expected to grow at a 4.95% CAGR to 2031.

- By end user, women’s scents held 56.95% of spend in 2025, and the unisex sub-segment is moving ahead at a 4.21% CAGR over the forecast timeframe.

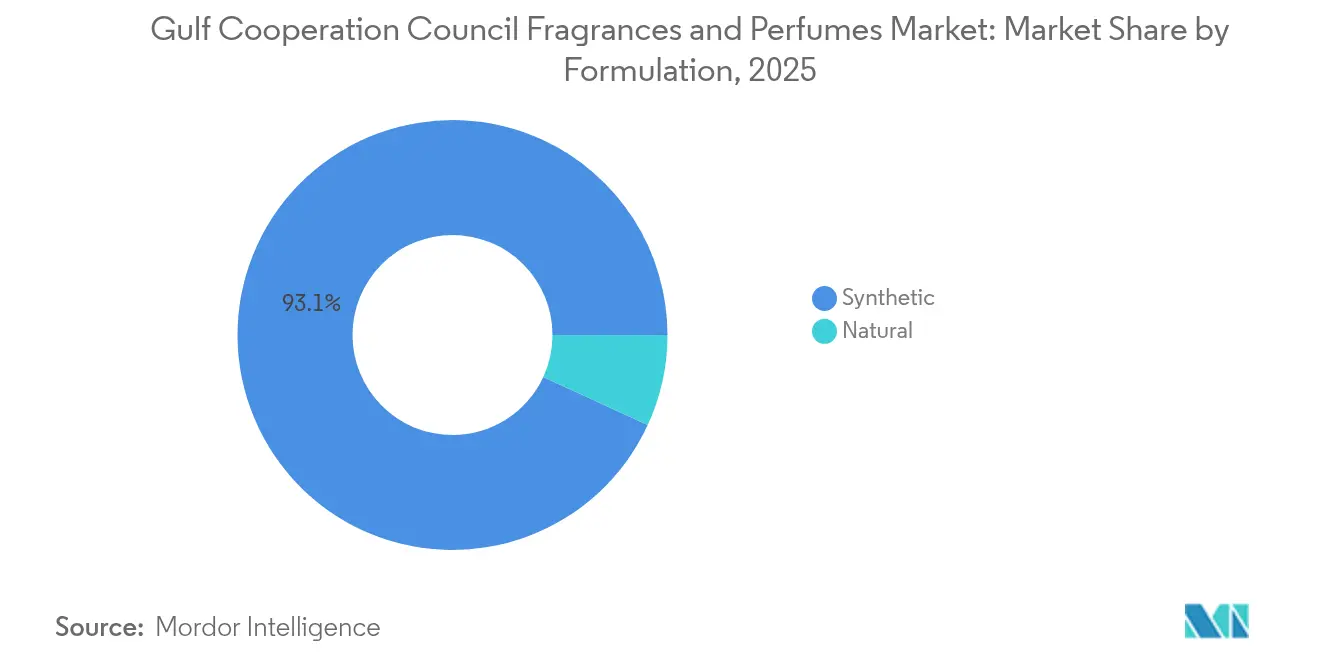

- By formulation, synthetic blends represented 93.12% of 2025 sales; natural formulations are forecast to expand at a 4.68% CAGR between 2026 and 2031.

- By distribution channel, specialty stores commanded 58.90% of turnover in 2025, whereas online retail is on course for a 5.88% CAGR up to 2031.

- By geography, Saudi Arabia generated 56.92% of the 2025 value, and Bahrain is poised for the highest 6.15% CAGR in the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Middle east representing one of the more structurally developed among them. The global report on fragrance and perfume market by Mordor Intelligence reflects how these regional layers combine into a single system.

Gulf Cooperation Council Fragrances And Perfumes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for halal, niche, artisanal, and traditional Arabian fragrances | +1.2% | Global, strongest in GCC, growing in Western markets | Medium term (2-4 years) |

| Aggressive marketing and strategic investments by key players | +0.8% | GCC core with spill-over to international markets | Short term (≤ 2 years) |

| Perfumes endorsed as gifting options | +0.9% | Global, peak during Eid and Ramadan | Medium term (2-4 years) |

| Increased demand for luxury and ultra-luxury perfumes | +1.1% | North America and Europe, strong GCC uptake | Long term (≥ 4 years) |

| Increase in tourism and duty-free shopping | +0.7% | GCC airports and travel hubs | Short term (≤ 2 years) |

| Growing demand for organic, natural, and sustainably sourced fragrances | +0.6% | Global, early gains in UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Halal, Niche, Artisanal, and Traditional Arabian Fragrances

The GCC fragrance market is witnessing a robust surge, fueled by a renewed appetite for halal, niche, artisanal, and traditional Arabian perfumes. This trend underscores a profound cultural affinity for scents, as consumers gravitate towards products that echo their heritage and personal identity. In 2024, FARIDAH, a brand spearheaded by Faridah F. Ajmal, made its debut in Dubai. The brand's ELEMENTS and Maktub collections spotlight natural ingredients, artisanal craftsmanship, and halal formulations. For example, the ELEMENTS line, inspired by Fire, Earth, Water, and Air, crafts unique scents that resonate with consumers seeking genuine and ethically sourced fragrances. This strategy highlights a pronounced shift towards products that mirror cultural and ethical values. In a similar vein, Saudi Arabian brand Al Dakheel Oud marries traditional perfumery with a contemporary twist. In 2024, it unveiled Abeek, a fragrance melding spicy notes with grapefruit, rose, incense, and cashmere wood. By engaging in regional showcases like the Kuwait International Perfume Exhibition, Al Dakheel Oud bolstered its presence in the GCC, appealing to consumers who cherish authentic Arabian scents with modern nuances. This heightened emphasis on halal, artisanal, and culturally attuned fragrances is redefining consumer preferences in the GCC.

Perfumes Endorsed as Gifting Options

In the GCC, the fragrances and perfumes market is witnessing a surge, largely driven by the trend of positioning perfumes as premium gifting options. Luxury perfumes, once seen as personal indulgences, are now increasingly viewed by consumers as thoughtful and prestigious gifts, especially during special occasions and celebrations. Brands and retailers are capitalizing on this shift, launching targeted campaigns and limited-edition releases to promote gifting. For example, My Perfumes unveiled special Eid collections with enticing promotional deals, directly catering to consumers in search of ready-made gifts. In a similar vein, Gallivant rolled out its Gulf Collection, explicitly branded for gifting, drawing in customers desiring regionally inspired premium gifts. V Perfumes, seizing the moment during cultural events like Youm Al-Otoor, presented exclusive gifts and promotions, encouraging purchases for loved ones. Such strategic moves not only bolster brand visibility but also broaden the market by tapping into the celebratory and gifting-driven consumption. By synchronizing product launches with pivotal cultural and social events, fragrance brands are not just creating opportunities for repeat purchases but are also reinforcing consumer loyalty. This emphasis on gifting is reshaping buying behaviors, transforming what were once seasonal demand spikes into consistent market growth opportunities.

Increased Demand for Luxury and Ultra-Luxury Perfumes

In the GCC, a pronounced shift is underway in the fragrance market, with consumers gravitating towards luxury and ultra-luxury perfumes. This pivot underscores a burgeoning appetite for exclusivity, quality, and tailored experiences. As a result, high-end fragrances are increasingly being perceived as emblems of status and sophistication. In May 2024, Amal Ameen Beauty unveiled its Sun Memories collection, drawing inspiration from Mediterranean locales such as Mykonos, Marrakesh, and Marbella. The launch was accentuated by an immersive perfume trunk show, underscoring the brand's commitment to experiential retail. These strategic launches underscore the potent influence of luxury and ultra-luxury offerings on consumer behavior, crafting aspirational experiences that not only spur higher spending but also foster brand loyalty. This trend gains momentum against a backdrop of escalating consumer expenditure in the region. According to the Capital Market Authority in 2023, Saudi Arabia's total consumer spending hit approximately 1.6 trillion Saudi riyals, with projections suggesting a rise to around 2.3 trillion by 2030 [1]Source: Capital Market Authority, “Prospectus of Savola Group,” cma.gov.sa . By aligning their products with the desires for exclusivity and personalization, fragrance brands are adeptly tapping into the region's surging purchasing power. This strategy not only propels growth in the high-end segment but also broadens the overall GCC fragrances and perfumes market.

Increase in Tourism and Duty-Free Shopping

Tourism and duty-free shopping are reshaping consumer habits and fueling the growth of the fragrances and perfumes market in the GCC. International travelers, often on the lookout for premium, travel-friendly products, increasingly view fragrances as both personal luxuries and valuable gifts. In response, brands are bolstering their presence in travel retail. In 2024, Ajmal Perfumes inaugurated a new boutique at Muscat Duty-Free, curating an immersive shopping experience that marries convenience with luxury. Highlighting this trend, Dubai Duty Free reported sales of AED 724.7 million (USD198.5 million) in May 2025, marking a 12.5% year-on-year surge and setting the year's peak monthly sales. These figures underscore the direct correlation between rising tourist numbers and fragrance sales, especially in the luxury and niche segments. With international visitors hitting 68.1 million in 2023, a 40% uptick from 2019, there's a pronounced inclination towards exclusive, high-quality scents, often for gifting [2]Source: GCC Statistical Center, “Tourism Report,”gccstat.org. By customizing store experiences, promotions, and product selections, brands are not just driving impulse buys but also cultivating brand loyalty. This synergy between tourism and duty-free shopping is reshaping buying patterns, leading to increased spending and a burgeoning GCC fragrances and perfumes market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High penetration of counterfeit perfumes | −0.9% | UAE and Saudi Arabia retail hubs | Short term (≤ 2 years) |

| Strict regulations and compliance requirements | −0.6% | GCC, affecting cross-border trade | Medium term (2-4 years) |

| Market saturation and intense competition | −0.7% | Core GCC markets | Long term (≥ 4 years) |

| Rising costs of raw materials and sustainable ingredients | −0.8% | Global sourcing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Penetration of Counterfeit Perfumes

Counterfeit perfumes are significantly hampering the growth of the GCC fragrances and perfumes market. These fakes not only erode consumer trust but also divert spending away from legitimate brands. When consumers encounter low-quality counterfeit products, they often mistakenly attribute issues like poor fragrance longevity or inconsistent scent profiles to premium brands. This misassociation discourages repeat purchases and diminishes overall market confidence. The challenge is especially pronounced in major retail hubs and online marketplaces, where counterfeit products are rampant. Recent enforcement actions highlight the magnitude of the problem. The Saudi Authority for Intellectual Property (SAIP) spearheaded a significant crackdown on counterfeit goods, targeting 61 businesses in Riyadh, Jeddah, and Dammam. They seized over 23,000 counterfeit cosmetics, perfumes, and fashion items [3]Source: Saudi Press Agency, “SAIP Launches Crackdown on Intellectual Property Infringement,” spa.gov.sa. Such interventions underscore the widespread nature of counterfeiting in the region. This not only diminishes legitimate market revenue but also compels brands to heavily invest in anti-counterfeit technologies, authentication measures, and consumer awareness campaigns. The rise of counterfeit perfumes is steering consumer behavior towards caution. This shift reduces the willingness to invest in high-end or niche fragrances, thereby limiting the growth potential of premium segments. Without stronger enforcement and heightened consumer education, the market's aspirations in the GCC remain stunted.

Market Saturation and Intense Competition

Market saturation and fierce competition are constraining the growth of the GCC fragrances and perfumes market, shaping consumer behavior in the process. An influx of both established and new brands has inundated consumers with choices, complicating efforts for individual brands to stand out and cultivate loyalty. This oversaturated market has led consumers to be more discerning, favoring brands that provide unique experiences, personalized offerings, or distinct scent profiles. Concurrently, the cutthroat competition has raised the bar, pushing consumers to expect more in terms of innovation, packaging, and engagement, whether in-store or online. The surge of online retail has further amplified this trend, enabling consumers to swiftly compare products, prices, and reviews, which in turn heightens the chances of brand switching and diminishes long-term loyalty. Consequently, to sway consumer choices in this challenging landscape, fragrance brands are channeling substantial investments into marketing, experiential retail, and digital engagement. Unless these brands can consistently deliver unique experiences that align with shifting consumer preferences, the constraints on the GCC fragrances and perfumes market's growth are likely to persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eau de Parfum Dominance Drives Premium Positioning

In 2025, Eau de Parfum dominates the market with a commanding 64.72% share, underscoring a clear consumer preference for its concentrated formulations. These offer enhanced longevity and sillage, particularly suited to the GCC's climate. Brands are keenly attuning their offerings to these regional tastes. For example, Floris London rolled out Middle East-exclusive Eau de Parfum variants, infusing amber, woody amber, and frankincense to amplify depth and longevity. In a similar vein, Ajmal Perfumes curates premium Eau de Parfum collections, delivering intense, enduring scents tailored for the region's luxury-seeking clientele.

Eau de Toilette is on the rise, charting the fastest growth with a projected 4.62% CAGR from 2026 to 2031. This surge is largely fueled by younger consumers gravitating towards lighter, versatile fragrances ideal for daily wear and layering. Meanwhile, categories like Eau de Cologne, along with traditional formats such as concentrated perfume oils (CPO) and attars, continue to cater to niche demands and cultural inclinations. Across these segments, product innovation is thriving, spotlighting hybrid formulations. These blends marry Western techniques with Arabian ingredients. A prime example is Gallivant’s Gulf Collection, which showcases citrus-enhanced and oud-vanilla accords, presenting contemporary takes on classic scents that resonate with both casual users and dedicated fragrance aficionados.

By Category: Luxury Segment Reinforces Premium Market Character

Luxury fragrances dominate the GCC fragrances and perfumes market with 80.78% share in 2025 and lead growth with a 4.95% CAGR (2026-2031), reflecting strong consumer preference for high-quality, prestigious scent experiences. Cultural values associating fragrance with status, hospitality, and personal identity drive sustained demand for premium and artisanal offerings. Brands are tailoring their portfolios to meet these expectations; for example, Chalhoub Group’s exclusive distribution of Roberto Cavalli fragrances across the UAE, Bahrain, Kuwait, Saudi Arabia, and Egypt highlights the alignment between global luxury houses and regional consumer demand. Similarly, Gallivant’s Gulf Collection and Ajmal Perfumes’ luxury lines provide long-lasting, signature scents, blending traditional Arabian ingredients with contemporary perfumery, catering to the region’s discerning clientele.

Mass-market fragrances maintain a presence through value-oriented SKUs and discovery sets, enabling trial and entry-level access while serving younger, price-conscious consumers exploring fragrance preferences. This segment focuses on lighter, versatile options suitable for daily wear, layering, and introductory experiences, allowing consumers to explore scents without committing to high-end products. Retailers leverage promotions, gift sets, and accessible packaging to drive adoption and trial among emerging consumers, supporting gradual market growth in this segment.

By End User: Women Lead While Unisex Gains Momentum

In 2025, women's fragrances capture a dominant 56.95% market share, with projections indicating a 3.78% CAGR from 2026 to 2031. This trend underscores a sustained consumer affinity for floral, fruity, and gourmand scents, alongside regional favorites like rose, jasmine, and other exotic blooms. Brands are honing in on this segment, employing gender-specific marketing and product strategies. They curate collections that echo traditional femininity. A case in point: Ajmal Perfumes tailors its women's lines to spotlight floral and oriental blends, catering to those who value both cultural authenticity and a touch of modern luxury.

On the other hand, the men's segment leans heavily on oud-forward, woody, and spicy scents, aligning closely with cultural masculinity and professional settings. Notable mentions include Rasasi’s La Yuqawam and Arabian Oud’s Kalemat, both of which offer enduring scents that resonate deeply with male consumers in the GCC. The unisex fragrance category, however, is witnessing a swift expansion, largely propelled by younger demographics, especially Gen Z and millennials, who gravitate towards versatile scents. Leading the charge are ByShams’ unisex collections and Maison Francis Kurkdjian’s Aqua Universalis. These fragrances artfully meld masculine notes like oud and amber with feminine touches such as florals and vanilla, transcending gender boundaries. Marketers are increasingly spotlighting this gender-neutral approach, emphasizing scent profiles, occasions, and emotional ties over traditional gender labels. Practical factors, like ease of travel and shared household use, further bolster this trend.

By Formulation: Synthetic Dominance with Natural Growth Acceleration

In 2025, synthetic formulations dominate the market with a commanding 93.12% share. Their edge lies in cost efficiency, consistent quality, regulatory compliance, and widespread availability, enabling mass production and stable pricing across a diverse product range. These formulations are particularly advantageous for manufacturers aiming to scale production without compromising on quality or affordability. The ability to meet stringent regulatory standards further enhances their appeal, ensuring compliance across various regions and industries. Brands catering to the mass market lean on these synthetic bases, ensuring their products are both reliable and value-driven for price-sensitive consumers. This widespread adoption underscores the pivotal role synthetic formulations play in maintaining affordability and accessibility in the market.

Natural formulations, however, are on a rapid ascent, boasting a projected 4.68% CAGR from 2026 to 2031. A growing consumer focus on wellness, sustainability, and a penchant for premium products fuels this surge. Initiatives like AlUla Peregrina Trading Company's commercialization of peregrina oil from Saudi Arabia underscore the potential of weaving local natural ingredients into high-end artisanal collections. They empower brands to strike a balance between performance, cost, and sustainability, all while catering to a consumer base that values authenticity and environmental responsibility. Furthermore, ingredients sourced through biotechnology and sustainable practices bolster consumer trust in these premium natural products, even as they navigate challenges posed by climate fluctuations in the supply chain.

By Distribution Channel: Specialty Stores Lead While Online Accelerates

In 2025, specialty stores dominate with a 58.90% market share, underscoring the significance of experiential retail, expert consultations, and scent testing in fragrance discovery and purchasing. Brands are tapping into these channels for immersive experiences. For example, Ajmal Perfumes’ flagship boutiques in the UAE and Oman offer personalized scent consultations, exclusive collections, and in-store events, catering to consumers desiring guidance and a premium shopping experience.

Online retail, witnessing a robust 5.88% CAGR from 2026 to 2031, is the fastest-growing segment. The allure of convenience, digital discovery, and broader access to niche and international brands fuels this surge. UAE's V Perfumes exemplifies this trend, seamlessly merging e-commerce with virtual consultations and curated gift offerings. This innovation empowers consumers to explore fragrances that were once elusive in traditional retail. Meanwhile, supermarkets, hypermarkets, and duty-free stores continue to cater to mass-market and impulse purchases. Emerging formats, such as subscription services and social commerce, are carving a niche by providing personalized selections and fostering interactive brand engagement.

Geography Analysis

In 2025, Saudi Arabia commands a dominant 56.92% share of the GCC fragrances and perfumes market. This stronghold is bolstered by robust consumer demand, a sizable population, increasing disposable incomes, and the Vision 2030 initiatives, which spotlight luxury consumption and tourism. The kingdom's established retail and travel infrastructure, highlighted by Al Waha Duty-Free Company capitalizing on the surging travel retail demand and brands like Arabian Oud proliferating their stores in major cities, further cements this dominance. Saudi consumers are gravitating towards premium, culturally resonant fragrances, with products like Arabian Oud’s Oud Kalemat and Ajmal Perfumes’ Signature collection witnessing robust sales in both domestic and regional arenas.

Bahrain is emerging as the region's fastest-growing market, boasting a projected CAGR of 6.15% from 2026 to 2031. This swift ascent is attributed to strategic tourism initiatives, a comparatively affluent populace, and a penchant for high-end fragrances. In response to the burgeoning demand for niche and artisanal products, brands are establishing boutique stores and forging luxury retail partnerships.

Other GCC nations, including the UAE, Qatar, Kuwait, and Oman, are experiencing steady growth, each driven by distinct dynamics. The UAE stands out as a manufacturing and export nexus, with Ahmed Al Maghribi Perfumes boasting over 180 stores and exports to upwards of 160 countries. Meanwhile, Qatar is bolstering its local production through enterprises like The Perfume Factory and S-Ishira. Oman, capitalizing on its rich frankincense heritage, showcases globally esteemed luxury brands like Amouage. Collectively, these markets enrich the region's diversity and foster niche market evolution, paving the way for specialized products and unique retail experiences.

Regulatory Landscape

Fragrances and perfumes in the GCC fall under cosmetics controls that combine Gulf Standardization Organization (GSO) technical standards with country-level registration and border-clearance requirements. A key anchor is GSO 1943:2024, which sets safety requirements for cosmetics and personal care products, and is used as a reference point for testing, labeling, and ingredient compliance across GCC markets.

Saudi Arabia and the UAE remain the main compliance gates for brands scaling across the region. In Saudi Arabia, the SFDA administers cosmetic product notification and clearance conditions, including continued updates to prohibited and restricted ingredients and transition timelines referenced by industry guidance (technical amendments applying to imported products from December 1, 2026, with a grace period for existing products until December 1, 2028). In the UAE, MoIAT enforces the Emirates Conformity Assessment Scheme (ECAS) for perfumes and cosmetics, issuing certificates of conformity typically valid for one year, with the Emirates Quality Mark (EQM) used by some manufacturers as a higher-assurance alternative for customs clearance.

Competitive Landscape

The GCC fragrances and perfumes market exhibits moderate consolidation, with established regional players maintaining significant shares while facing increasing competition from international luxury brands and emerging niche houses. Traditional Arabian manufacturers such as Rasasi, Ajmal, Al Haramain, and Swiss Arabian leverage cultural authenticity, deep local market knowledge, and established distribution networks to maintain loyalty and defend market positions against global entrants seeking to capitalize on Middle Eastern fragrance trends. Institutional confidence in the region is demonstrated through consolidation activities, including L’Oréal’s minority stake in Amouage and General Atlantic’s investment in Kayali, reflecting the growing attractiveness of regional fragrance assets.

Strategic differentiation is achieved through vertical integration, large-scale manufacturing, and technology adoption. For example, Swiss Arabian operates five manufacturing plants producing 35 million units annually for global export while partnering with international ingredient suppliers like Givaudan. Brands are also deploying AI-driven personalization, virtual consultations, and digital marketing to engage younger demographics and international consumers.

Opportunities exist in sustainable formulations, bespoke services, and hybrid retail concepts that combine traditional Arabian craftsmanship with modern consumer preferences for transparency, customization, and experiential engagement. Regulatory requirements, such as ECAS certification in the UAE and SFDA regulations in Saudi Arabia, act as entry barriers for smaller players, enabling established brands to leverage compliance expertise and sustain competitive advantages in the region’s complex operating environment.

Gulf Cooperation Council Fragrances And Perfumes Industry Leaders

Arabian Oud Company

Abdul Samad Al Qurashi Company Ltd.

Ajmal Perfumes LLC

Mahmood Saeed Group

Rasasi Perfumes Industry LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational automation and local capability build-out are creating whitespace for suppliers and brand owners to shorten lead times, improve batch consistency, and document compliance. A concrete signal is the April 2026 Mohammed Bin Rashid Innovation Fund (MBRIF) credit guarantee (AED 7.2 million) supporting Fragrance Delivery Technologies to upgrade its Jebel Ali Free Zone facility with Industry 4.0-oriented automation, which reinforces opportunities for GCC-based contract manufacturing, packaging, and formulation support aligned to premium and export-grade requirements.

Sustainability-led differentiation is also shifting from marketing claims to operations, creating room for ingredient and manufacturing partners that can demonstrate environmental controls and supply chain discipline. Eurofragance has referenced cutting over 5.5 tons of CO2 in its UAE operations through supply chain emission controls, supporting demand for measurable sustainability practices alongside luxury positioning. Travel retail and experiential formats remain a key activation channel for premiumization in the GCC, with duty-free performance indicators already visible in the region (for example, Dubai Duty Free reported AED 724.7 million in sales in May 2025), which creates room for brands with travel formats, gifting bundles, and compliant assortments tailored to airport retail constraints.

Recent Industry Developments

- April 2026: Mohammed Bin Rashid Innovation Fund (MBRIF) provides a credit guarantee of AED 7.2 million to Fragrance Delivery Technologies to upgrade its Jebel Ali Free Zone facility with Industry 4.0-oriented automation. The upgrade strengthens GCC contract manufacturing, packaging, and formulation capabilities targeted at premium and export-grade requirements. It signals a push toward digitalized, locally embedded fragrance production in the UAE.

- February 2025: L'Oreal took a minority position in Amouage, strengthening its exposure to Middle East luxury fragrance assets. The investment highlights international strategic interest in GCC-rooted premium fragrance brands and can accelerate capability transfer in distribution and brand building.

- May 2024: Amal Ameen Beauty launched the Sun Memories collection and supported it with an immersive perfume trunk show format. Experience-led launches like this raise the bar for premium retail engagement and encourage higher-value discovery and gifting-driven purchases in the region.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of fragrances and perfumes sold in GCC countries across retail and online channels, counted at end-market selling prices and tracked in USD.

Scope exclusions: We exclude non-fragrance personal care items like soaps, shampoos, and generic body lotions unless they are primarily positioned and priced as fragrance products.

Segmentation Overview

- By Product Type

- Eau de Parfum

- Eau de Toilette

- Eau de Cologne

- Others

- By Category

- Mass

- Luxury

- By End User

- Women

- Men

- Unisex

- By Formulation

- Natural

- Synthetic

- By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Others

- By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Oman

- Kuwait

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping GCC fragrance spending demand and retail flows, then aligning them with a practical product definition used by brands and retailers. We reviewed public releases and datasets such as GCC national statistics portals, central bank consumer price and inflation bulletins, UN Comtrade trade statistics, World Bank macro indicators, and selected WHO publications where relevant as consumption proxies.

To keep the model grounded, we also used company annual reports, audited financial statements, investor presentations, and major retailer and duty-free announcements for category direction and pricing ranges. An import and export shipment-level database was referenced selectively to verify trade movements and flag unusual spikes that required follow-up. These desk sources are illustrative only, and we relied on other public references as well for cross-checks, clarification, and validation.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk sources cannot show clearly, especially mix shifts between luxury and mass, the role of gifting, and how online retail affects pricing and volumes. We spoke with manufacturers, distributors, retailers, and category specialists across the GCC so assumptions on pricing, promo intensity, and channel splits could be aligned before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 48% | Functional/Unit leaders: 37% | |

| Smaller Players: 21% | Managers: 49% |

Market-Sizing & Forecasting

Sizing followed a top-down build that reconstructs GCC fragrance demand using country-level consumption signals, trade flows, and category spending patterns, then converts them into value using typical price ladders by product type. To keep totals realistic, we corroborated them with selective bottom-up checks, such as sampled average selling price (ASP) times estimated unit volumes from channel checks, along with sanity checks using supplier and distributor revenue ranges where disclosure existed.

Key inputs used in the model included GCC population and income trends, tourism and travel retail direction, perfume import values and re-export patterns, product mix shares across Eau de Parfum and Eau de Toilette, and channel mix (specialty retail, supermarkets and hypermarkets, and online). Where direct volume evidence was thin, we used bounded ranges from interviews and narrowed them using observable indicators such as price inflation and trade movements.

For forecasting, scenario analysis was used, with base, conservative, and faster-growth paths tied to variables interviewees could comment on with confidence, including premiumization pace, online discounting behavior, and expected travel retail recovery patterns. The final forecast selection was the one that stayed consistent with both macro direction and on-the-ground category feedback.

Data Validation & Update Cycle

Outputs were checked in several steps so unusual jumps could be explained before sign-off. We compared results against independent signals like import trends, retail category commentary, and known pricing inflation, then re-ran the model when a mismatch crossed a pre-set tolerance.

A second analyst review is completed to test assumptions and calculations, and follow-up calls are triggered if critical inputs like ASP progression or channel mix are disputed by multiple respondents. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery review is done so clients receive the latest updated view.

Mordor Intelligence's Gcc Fragrance and Perfumes Market Size Compared With Other Published Estimates

Published estimates for GCC fragrances often vary because each publisher draws the market line differently and uses its own price and channel assumptions. Differences in whether travel retail is treated as local demand, how luxury price inflation is applied, and how re-exports are handled can shift the reported number by a meaningful amount.

The main gap comes from how GCC re-exports and travel retail sales are counted, where Mordor Intelligence only includes fragrance and perfume demand that can be tied back to GCC end buyers through channel and trade checks, instead of simply adding gross import values into consumption.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.22 B (2025) | |

| Regional Consultancy A | USD 3.10 B (2024) | Uses an earlier base year and a narrower product interpretation that tends to emphasize perfumes only, which can undercount adjacent fragrance formats and newer channel sales. |

| Trade Journal B | USD 3.01 B (2023) | Relies on older-period estimates and lighter validation of ASP and channel mix, so premiumization and online retail price dispersion are not fully reflected in the total. |

The spread in the table is largely explained by year choice and how the demand pool is constructed, rather than a simple math difference. By keeping the scope tied to end-market spending and checking it against trade and channel indicators, we can present a market value that is easier to trace and repeat when clients update assumptions.

Key Questions Answered in the Report

What is the current value of the GCC fragrances and perfumes market?

The market is valued at USD 4.38 billion in 2026, with growth expected to continue through 2031.

How fast is the market growing?

A 3.90% CAGR is projected for the 2026-2031 period, driven by luxury demand, tourism, and digital adoption.

Which product type dominates sales?

Eau de Parfum holds the largest share at 64.72% of 2025 revenue.

Which distribution channel is expanding quickest?

Online retail shows the fastest trajectory with a 5.88% CAGR forecast up to 2031.

Page last updated on: