Luxury Perfume Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

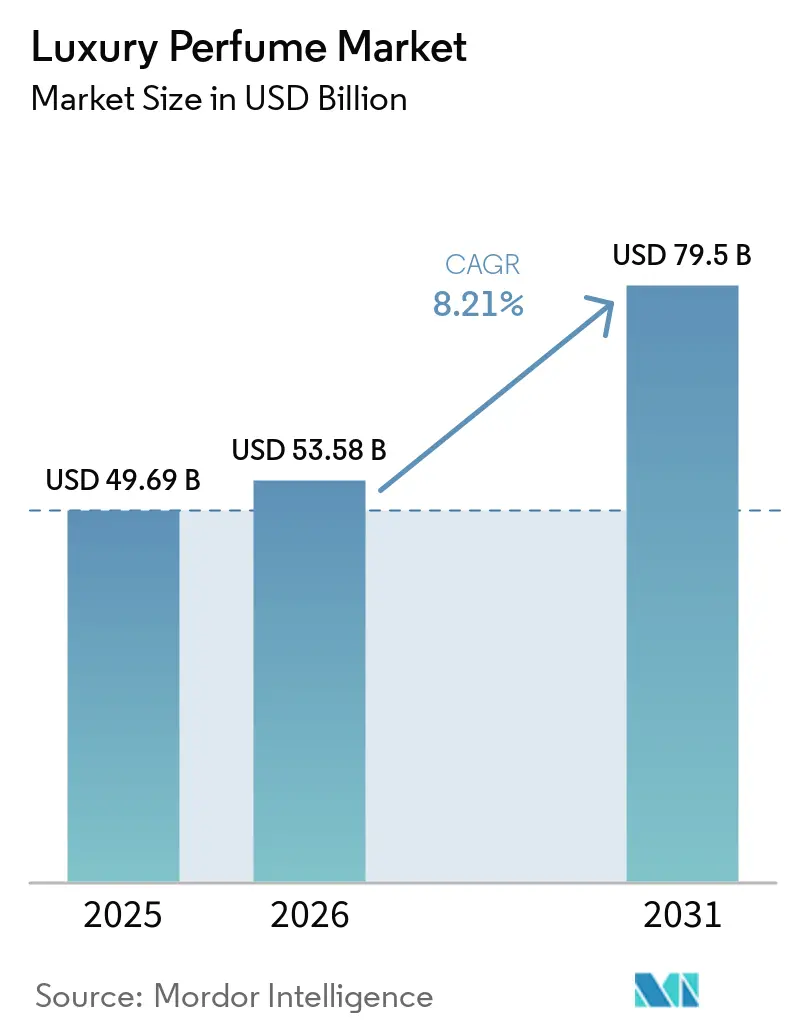

| Market Size (2026) | USD 53.58 Billion |

| Market Size (2031) | USD 79.5 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Perfume Market Analysis by Mordor Intelligence

The luxury perfume market size is estimated at USD 49.69 billion in 2025, USD 53.59 billion in 2026, and is expected to reach USD 79.50 billion by 2031, at a CAGR of 8.21% during the forecast period (2026-2031). This acceleration reflects a structural shift beyond traditional prestige channels, as consumers increasingly prioritize olfactory identity over brand heritage alone. Niche houses capturing wallet share from established maisons signal that fragrance provenance and ingredient transparency now rival logo recognition in purchase decisions. The pivot toward artisanal formulations and personalized scent profiles is reshaping competitive dynamics, compelling legacy players to either acquire indie labels or launch in-house ateliers that mimic boutique authenticity. Health-conscious buyers are also rewarding natural and biotech-derived formulas, a trend strengthened by stricter European allergen rules and U.S. disclosure guidance.

Key Report Takeaways

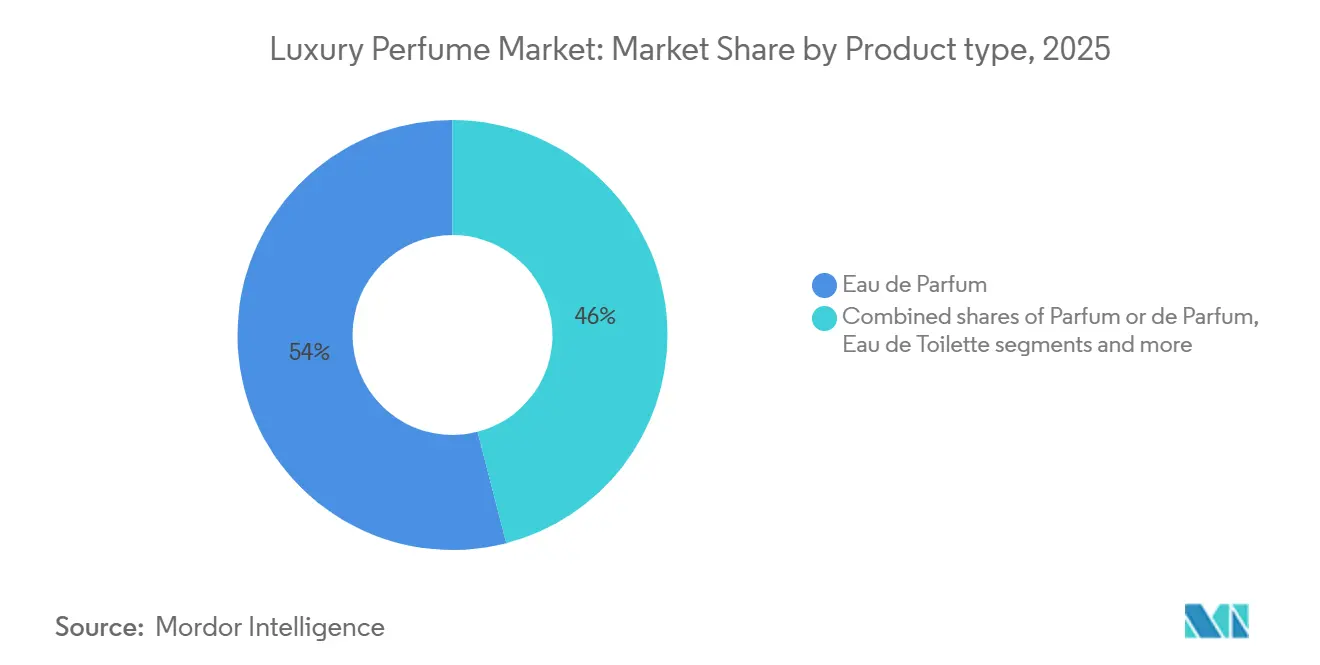

- By product type, Eau de Parfum led with 54.02% revenue share in 2025; Parfum or de Parfum is projected to expand at a 9.24% CAGR to 2031.

- By category, conventional and synthetic blends held 85.60% of the luxury perfume market share in 2025, while natural/organic formulations are advancing at a 12.49% CAGR through 2031.

- By end-user, women accounted for 64.58% of 2025 demand; unisex lines are growing at a 10.31% CAGR to 2031.

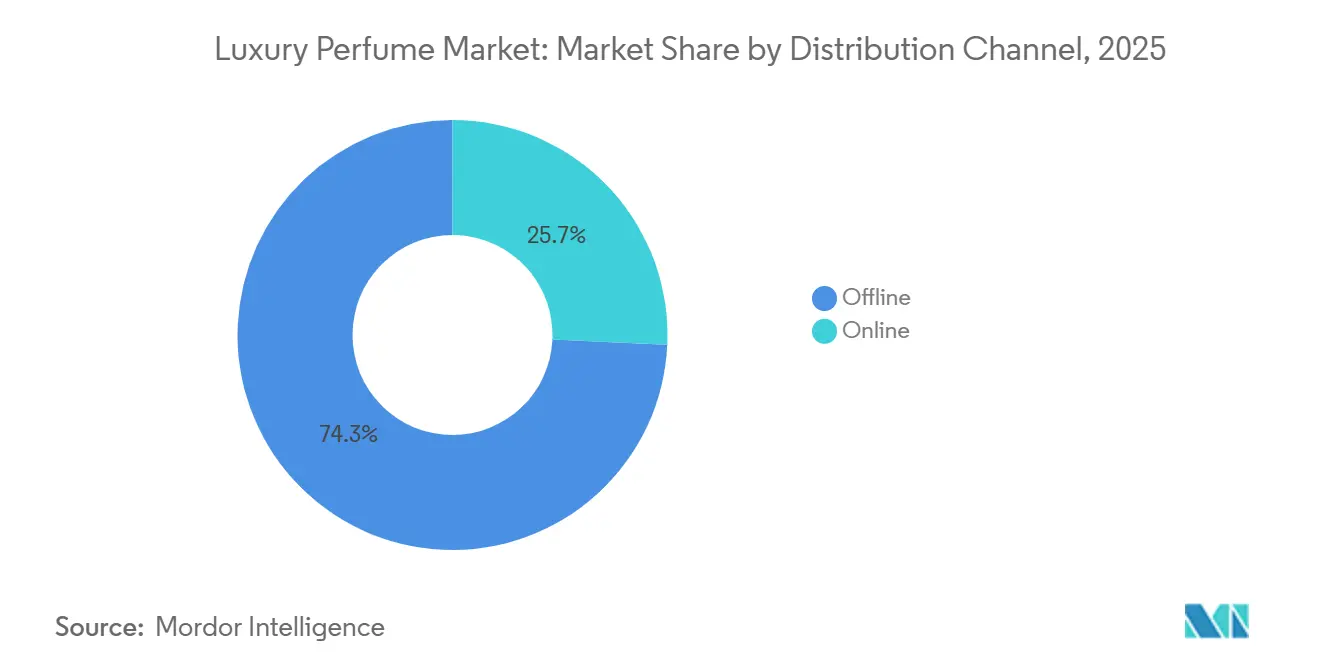

- By distribution channel, offline retained a 74.27% share in 2025, whereas online retail is rising at a 9.75% CAGR through 2031.

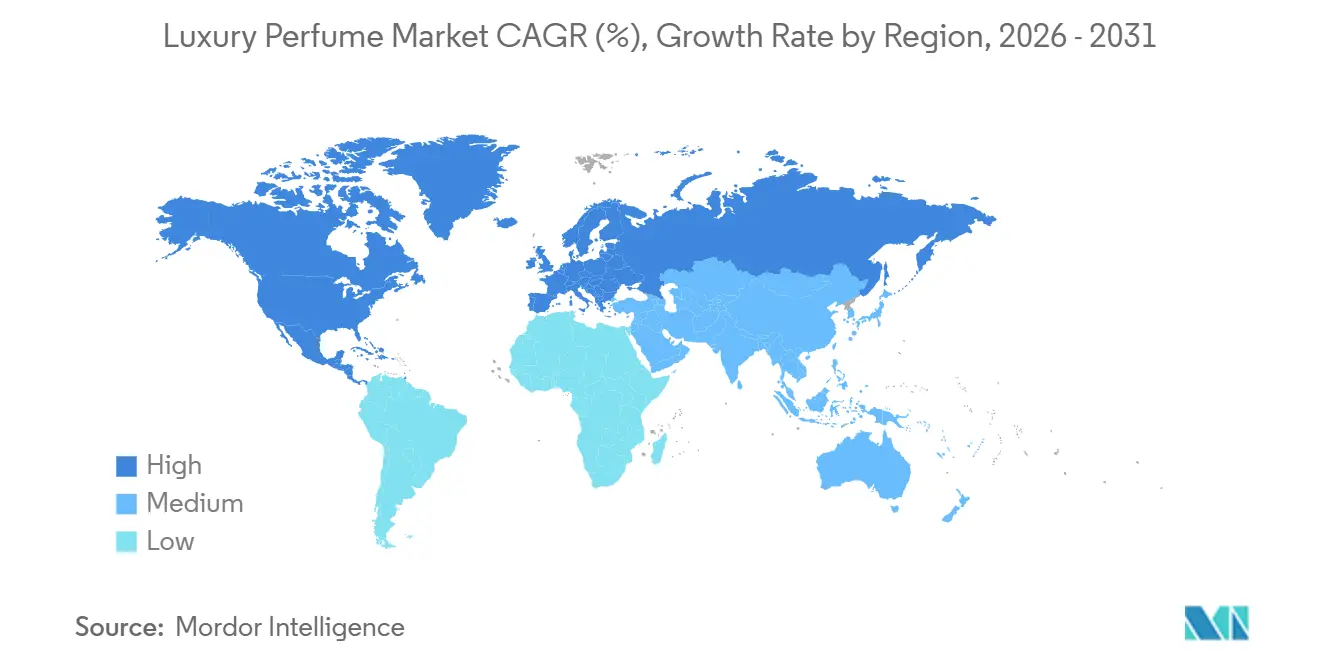

- By geography, Europe captured 40.06% of the 2025 value, while Asia-Pacific is set to progress at a 10.72% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Perfume Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Collaborations with designers and celebrities boost limited editions | +1.8% | Global, with strongest effect in North America and Europe | Short term (≤ 2 years) |

| Spike in demand for niche and artisanal fragrance | +1.2% | Europe, North America, with growing influence in Asia-Pacific | Medium term (3-4 years) |

| Expansion of travel retail and e-commerce | +1.5% | Global, particularly strong among Gen Z consumers | Short term (≤ 2 years) |

| Consumer inclination towards natural and organic products | +1.0% | Europe, North America, with emerging impact in Asia-Pacific | Long term (≥ 5 years) |

| Rising gift-giving culture is supporting the market | +0.9% | Global, with pronounced effect in Asia-Pacific and Middle East | Medium term (3-4 years) |

| Growing demand for personalized fragrances | +1.1% | North America, Europe, with emerging impact in high-income Asia-Pacific markets | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Collaborations with designers and celebrities boost limited editions

Designer and celebrity partnerships inject scarcity-driven urgency into product launches, converting casual browsers into committed buyers through time-bound availability and social-media amplification. In 2025, Coty's collaboration with Kim Kardashian's KKW Fragrance generated over USD 14 million in first-day sales, underscoring how influencer credibility can bypass traditional advertising spend. These limited-edition drops also enable brands to test unconventional scent profiles, such as gourmand-woody hybrids or vegan musks, without committing to full-line extensions, thereby reducing inventory risk. The strategy is particularly effective among Gen Z and millennial cohorts, who prioritize collectability and brand storytelling over heritage prestige. However, over-reliance on celebrity equity can backfire if the public figure's reputation deteriorates, as seen when certain endorsements were quietly discontinued following controversies. Brands are now diversifying by partnering with micro-influencers and niche designers who command loyal but smaller followings, spreading reputational risk while maintaining exclusivity appeal.

Spike in demand for niche and artisanal fragrance

Niche and artisanal houses are capturing share from mass-prestige incumbents by emphasizing raw-material provenance, small-batch production, and transparent ingredient sourcing that resonate with consumers skeptical of industrial formulations. Independent perfumers such as Byredo, Le Labo, and Diptyque have cultivated cult followings by offering scent narratives rooted in specific geographies or cultural moments, contrasting sharply with the generic floral-oriental templates of mainstream launches. This shift is quantifiable: niche brands collectively grew revenue in 2025, outpacing the broader market's expansion, according to data compiled from multiple company filings. The trend is further amplified by social-media fragrance communities, so-called "fragheads", who disseminate reviews and decant samples, effectively democratizing access to previously obscure labels. Retailers are responding by dedicating floor space to discovery zones where customers can explore 50-plus niche references, a format that drives higher basket values despite lower per-unit margins. The challenge for artisanal players lies in scaling production without diluting brand mystique, a balancing act that has prompted several to accept minority investments from conglomerates while retaining creative autonomy.

Rising gift-giving culture is supporting the market

Fragrance's role as a socially acceptable gift across age groups and occasions, from corporate incentives to wedding favors, underpins consistent demand spikes during holiday quarters and cultural festivals. In Asia-Pacific, gifting traditions tied to Lunar New Year, Diwali, and Mid-Autumn Festival drove an estimated significant growth of annual luxury perfume sales in 2025, with brands launching region-specific packaging and limited-edition coffrets to capitalize on seasonal purchasing. This cultural tailwind is reinforced by e-commerce platforms offering curated gift sets with personalized messaging and expedited delivery, lowering friction for last-minute buyers. Corporate gifting represents an underexploited channel: companies allocating budgets for client appreciation are shifting from generic hampers to bespoke fragrance selections that signal sophistication and attention to detail. However, the gift segment is price-sensitive; brands must balance premium perception with accessible entry points, often achieved through 30ml or 50ml formats priced below USD 100. The challenge lies in converting gift recipients into repeat purchasers, a metric that remains opaque but is increasingly tracked via loyalty programs that incentivize post-gift engagement.

Consumer Inclination towards natural and organic products

Consumers seek information about ingredient origins and prefer brands using eco-friendly and biodegradable packaging. Regulatory frameworks, including the EU's (European Union) Cosmetics Regulation (EC No 1223/2009), support this shift by requiring the elimination of harmful chemicals from cosmetics and perfumes, thereby strengthening consumer confidence in natural products [1]Source: European Commission, "Legislation", commission.europa.eu. In parallel, certifications such as COSMOS Organic and USDA (United States Department of Agriculture) Organic are becoming table stakes for premium positioning, as consumers cross-reference ingredient lists against databases like the Environmental Working Group's Skin Deep. Natural formulations command price premiums of 15% to 25% over synthetic equivalents, yet they introduce supply-chain complexity: sourcing sustainable sandalwood or vetiver requires multi-year contracts with cooperatives in India and Haiti, exposing brands to geopolitical and climate risks. Despite these hurdles, L'Oréal's Luxe division reported that its certified-organic fragrance lines grew 18% in 2025, outpacing synthetic counterparts. The shift also opens white space for biotech startups engineering lab-grown aroma molecules that replicate natural profiles without an agricultural footprint, a frontier that could redefine "natural" in the next decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -1.2% | Global, with highest impact in emerging markets | Medium term (3-4 years) |

| Health concerns over chemical ingredients | -0.8% | North America, Europe, with growing awareness in Asia-Pacific | Long term (≥ 5 years) |

| Complex supply chain management | -0.6% | Global, particularly affecting multi-market operations | Medium term (3-4 years) |

| High marketing costs associated with maintaining luxury brand positioning | -0.7% | Global, with strongest effect in saturated markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit Products

Counterfeit products pose significant challenges to the luxury perfume market by damaging brand value and consumer confidence. According to the U.S. Customs and Border Protection (CBP) report, perfumes rank as the fourth most seized counterfeit item, with 44,000 units confiscated[2]Source: Customs and Border Protection, "Intellectual Property Rights Seizure Statistics", cbp.gov. The increasing prevalence of counterfeit fragrances, particularly through online platforms, negatively impacts consumer trust. Luxury brands are deploying blockchain-based authentication systems and NFC-enabled packaging to verify product provenance, yet adoption remains uneven due to cost considerations and consumer awareness gaps. The challenge is compounded in emerging markets where price sensitivity drives consumers toward suspiciously discounted offerings, often unaware they are purchasing fakes. Regulatory enforcement varies widely: the European Union's customs authorities seized over 4 million counterfeit cosmetic items in 2024, yet jurisdictions with weaker intellectual-property frameworks struggle to interdict shipments.

Health concerns over chemical ingredients

Health concerns about chemical ingredients in luxury fragrances constrain market growth as premium brands adapt their formulation strategies and enhance transparency. Recent regulations, including Washington State's Toxic-Free Cosmetics Act (effective January 2025), prohibit certain chemicals in high-end cosmetics and fragrances, affecting product development and market entry[3]Source: Washington State Department of Ecology, "Toxic-Free Cosmetics Act (TFCA)", ecology.wa.gov. The high-end fragrance industry must balance traditional compositions with safety standards and consumer preferences. In parallel, the International Fragrance Association's 51st Amendment, effective January 2025, restricted or banned over 100 materials based on updated safety assessments, requiring brands to reformulate legacy bestsellers at costs ranging from USD 200,000 to USD 1 million per SKU. Consumer advocacy groups amplify these concerns through social media, often citing studies linking certain synthetics to endocrine disruption, though peer-reviewed evidence remains contested. Brands are responding by investing in green chemistry and biotechnology to develop safer alternatives, yet these substitutes often lack the performance characteristics, such as longevity and projection, of traditional ingredients, forcing trade-offs between safety perception and olfactory quality. The reputational risk is asymmetric: a single adverse study can trigger boycotts, whereas proactive reformulation garners limited consumer credit, creating a defensive rather than value-creating dynamic.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Concentration Drives Premiumization

Eau de Parfum captured 54.02% of market share in 2025, reflecting consumer preference for formulations that balance longevity, projection, and price accessibility, yet Parfum or de Parfum is accelerating at 9.24% CAGR as affluent buyers trade up to higher-concentration offerings that deliver 8 to 12 hours of wear and justify price points exceeding USD 300 per 50ml bottle. This premiumization trend is particularly pronounced in Middle Eastern markets, where cultural norms favor intense, long-lasting sillage, and in Asia-Pacific, where rising disposable incomes enable experimentation with ultra-luxury tiers. Eau de Toilette and Eau de Cologne, traditionally positioned as daytime or casual options, are experiencing slower growth as consumers consolidate fragrance wardrobes around fewer, higher-quality bottles rather than maintaining separate scents for different occasions. Other product types, including solid perfumes and fragrance oils, occupy niche segments appealing to travelers and consumers seeking alcohol-free alternatives, yet they remain marginal in revenue terms.

The shift toward higher concentrations is also driven by ingredient transparency: Parfum formulations typically contain 20% to 30% fragrance oils versus 10% to 15% in Eau de Parfum, allowing brands to showcase premium raw materials such as oud, iris, and natural musks that are diluted in lighter concentrations. Regulatory compliance under IFRA standards applies uniformly across concentration tiers, yet higher-concentration products face stricter scrutiny on allergen thresholds, requiring reformulation expertise that smaller brands may lack. The economic logic is compelling for brands: Parfum commands gross margins 10 to 15% points higher than Eau de Parfum, offsetting the elevated raw-material costs. However, the segment's growth is constrained by price sensitivity outside ultra-high-net-worth cohorts, limiting addressable market size and necessitating targeted distribution through flagship boutiques and duty-free channels where purchase intent is already elevated.

By Category: Natural Formulations Gain Momentum

Conventional and synthetic fragrances held 85.60% of market share in 2025, leveraging cost efficiencies and performance consistency that natural alternatives struggle to match, yet natural and organic formulations are expanding at 12.49% CAGR as consumers prioritize ingredient transparency, sustainability, and hypoallergenic profiles over the olfactory complexity that synthetics enable. This bifurcation reflects a broader tension in the luxury beauty industry: synthetics offer creative latitude, perfumers can engineer molecules that do not exist in nature, such as Iso E Super or Ambroxan, whereas naturals constrain the palette to plant-derived absolutes and essential oils, limiting avant-garde experimentation. Brands are responding by launching dual portfolios: conventional lines targeting mainstream consumers and certified-organic collections appealing to wellness-oriented buyers willing to accept shorter longevity and higher prices.

The natural segment's growth is underpinned by regulatory tailwinds, particularly in Europe, where the EU Ecolabel and COSMOS Organic certifications provide third-party validation that resonates with skeptical consumers. However, natural formulations introduce supply-chain complexity: sourcing certified-organic lavender or bergamot requires multi-year contracts with cooperatives in Provence and Calabria, exposing brands to agricultural variability and geopolitical risks. The challenge for natural brands lies in scaling production without diluting authenticity claims, a balancing act that has prompted several to accept minority investments from conglomerates while retaining creative and sourcing autonomy.

By Distribution Channel: Online Retail Disrupts Specialty Stores

Offline stores retained 74.27% of distribution share in 2025, benefiting from tactile discovery and expert consultation that remain difficult to replicate digitally, yet online retail channels are surging at 9.75% CAGR, propelled by virtual try-on tools, subscription discovery boxes, and direct-to-consumer models that bypass traditional wholesale margins. Subscription services such as Scentbird and Olfactif have democratized access to niche brands by offering monthly samples at USD 15 to USD 20, converting trial into full-bottle purchases at rates exceeding 25%, a conversion funnel that traditional retail struggles to match. Supermarkets and hypermarkets, though still relevant for mass-market fragrances, are losing share in the luxury segment as consumers prioritize curated assortments and brand storytelling over convenience.

The challenge for online channels lies in overcoming the sensory gap: fragrance is inherently experiential, and digital descriptors, such as "woody with citrus top notes," provide imperfect proxies for olfactory reality. Brands are deploying augmented reality and AI-powered recommendation engines that map consumer preferences to scent profiles, yet these tools remain nascent and prone to misalignment between expectation and delivery. Specialty stores are fighting back by offering experiential retail, such as scent-blending workshops and personalized consultations, that online channels cannot replicate, yet these activations require significant investment and are difficult to scale beyond flagship locations in major cities.

By End-User: Men's Fragrances Accelerate

Women accounted for 64.58% of end-user demand in 2025, reflecting entrenched purchasing habits and broader product assortments, yet unisex fragrances are growing at 10.31% CAGR, driven by grooming normalization, celebrity-endorsed unisex launches, and digital-native brands that bypass traditional retail gatekeepers to reach younger male cohorts. This acceleration is quantifiable: men's fragrance revenue grew in 2025, outpacing women's expansion, according to aggregated data from Estée Lauder, L'Oréal, and Coty investor presentations. The shift is particularly pronounced among Gen Z and millennial men, who view fragrance as an extension of personal branding rather than a special-occasion accessory, a mindset amplified by social-media influencers who position scent as integral to grooming routines. Brands are responding by launching woody-aromatic and citrus-spice profiles that appeal to male preferences while avoiding the overly masculine tropes, such as aggressive leather or tobacco, that alienate younger buyers seeking versatility.

Unisex fragrances, though not separately quantified in most market data, are blurring traditional gender boundaries and capturing share from both men's and women's segments. Labels such as Le Labo and Byredo have built reputations on gender-neutral positioning, a strategy that resonates with consumers rejecting binary categorization and seeking scents that reflect individual identity rather than societal norms. The challenge for brands lies in marketing: unisex positioning risks alienating core female buyers who associate fragrance with femininity, yet overly gendered campaigns can deter male experimentation. The solution is increasingly channel-specific messaging, gender-neutral storytelling on social media and e-commerce, paired with targeted campaigns in men's lifestyle publications, that allows brands to straddle both segments without diluting either.

Geography Analysis

Europe held 40.06% of market share in 2025, underpinned by centuries-old perfumery traditions in France, Italy, and the United Kingdom, yet the region's growth is moderating as mature consumer bases prioritize replacement purchases over wardrobe expansion, a dynamic that contrasts sharply with Asia-Pacific's 11.67% CAGR driven by rising affluence and cultural adoption of fragrance as a daily ritual. Within Europe, France remains the epicenter of luxury perfumery, home to heritage houses such as Chanel, Dior, and Hermès, as well as artisanal ateliers in Grasse that supply raw materials to global brands. Germany and the United Kingdom are significant markets for niche and natural fragrances, reflecting consumer preferences for transparency and sustainability, while Southern Europe, particularly Italy and Spain, exhibits strong demand for floral and citrus profiles aligned with Mediterranean sensibilities. Eastern European markets, including Poland and the Czech Republic, are emerging as growth pockets as disposable incomes rise and Western luxury brands expand distribution networks. The European Union's Cosmetics Regulation (EC) No 1223/2009, updated in 2024 to tighten allergen labeling, has accelerated reformulation cycles and elevated compliance costs, yet it also provides a competitive moat for established players with robust regulatory infrastructure.

Asia-Pacific is the fastest-growing region, fueled by China's expanding middle class, India's burgeoning luxury market, and Japan's sophisticated fragrance culture that prizes subtlety and craftsmanship. India's market is nascent but accelerating, driven by urbanization, rising female workforce participation, and the proliferation of modern retail formats that introduce fragrance to consumers previously reliant on traditional attars and essential oils. Japan represents a mature yet distinctive market, where consumers favor light, ephemeral scents and exhibit high brand loyalty, creating opportunities for niche labels that emphasize artisanal provenance. Southeast Asia, particularly Singapore, Thailand, and Indonesia, is emerging as a high-growth corridor, supported by travel-retail hubs and increasing digital penetration that facilitates the discovery of international brands.

North America, the Middle East, and South America collectively represent the remaining market share, each exhibiting unique growth drivers and challenges. North America, dominated by the United States, is characterized by high per-capita fragrance consumption and strong demand for celebrity-endorsed and niche brands, yet growth is moderating as the market matures and consumers consolidate purchases around fewer, higher-quality bottles. The Middle East, particularly Saudi Arabia and the United Arab Emirates, exhibits cultural affinity for intense, long-lasting oud-based fragrances, creating a distinct segment that Western brands are targeting through region-specific launches and partnerships with local distributors. South America, led by Brazil and Argentina, is recovering from economic volatility, with growth concentrated in urban centers where rising middle-class incomes support premiumization trends. Africa remains underpenetrated, yet South Africa and Nigeria are emerging as early-stage markets where international brands are establishing footholds through selective distribution and localized marketing campaigns.

Competitive Landscape

The luxury perfume market exhibits moderate concentration, as conglomerates such as LVMH, Estée Lauder, and Coty dominate mass-prestige and selective distribution channels, yet fragmented artisanal players carve defensible niches in ultra-premium and bespoke segments through agility, storytelling, and direct-to-consumer models that bypass traditional wholesale economics. Large groups leverage vertical integration; LVMH's ownership of rose and jasmine farms in Grasse secures supply for Dior and Givenchy, while Estée Lauder's scale in digital marketing amplifies reach for brands such as Jo Malone and Tom Ford, yet they struggle to replicate the authenticity and exclusivity that independent perfumers cultivate through limited-edition drops and founder narratives.

This bifurcation creates strategic tension: conglomerates acquire indie labels to access niche credibility, as seen in Puig's 2024 purchase of Byredo for an undisclosed sum, yet post-acquisition integration often dilutes the very attributes that made the target attractive, a risk that has prompted some founders to resist buyout offers despite lucrative valuations. Opportunities are emerging in personalization technology, biotech-derived ingredients, and circular-economy business models that address sustainability concerns without compromising olfactory performance.

Brands deploying AI-driven scent profiling and in-store blending stations are capturing high-net-worth individuals willing to pay premiums for bespoke formulations, while biotech startups engineering lab-grown aroma molecules, such as Ginkgo Bioworks' yeast-derived vanillin, are positioning themselves as sustainable alternatives to agricultural supply chains vulnerable to climate variability. Refillable packaging and take-back programs are gaining traction in Europe, where regulatory pressure and consumer activism are compelling brands to adopt circular models, yet adoption remains limited in other regions due to logistical complexity and consumer indifference. Technology is also reshaping competitive dynamics: augmented reality try-on tools and virtual consultations lower barriers to online discovery, enabling digital-native brands to compete with heritage houses that historically relied on in-store tactile experiences to justify premium pricing.

Luxury Perfume Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

The Estée Lauder Companies Inc.

-

Coty Inc.

-

Chanel SA

-

Kering S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Vera Wang launched a new fragrance, marking the brand's entry into the luxury fragrance segment. The fragrance combines floral notes with warm amber woods and vanilla, complemented by jasmine sambac and mandarin.

- August 2024: Balmain introduced its first beauty product line, a collection of eight gender-neutral fragrances called "Les Éternels de Balmain." The fragrance collection draws inspiration from Pierre Balmain's Parisian heritage and Olivier Rousteing's contemporary fashion influence.

- July 2024: Drip, an Indian luxury brand, introduced "Halo," a new perfume in the fragrance market. The product focuses on quality ingredients and detailed craftsmanship.

- May 2024: Fendi introduced a luxury perfume collection consisting of seven fragrances, developed in collaboration with perfumers Anne Flipo, Fanny Bal, and Quentin Bisch.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the luxury perfume market as retail and travel-retail sales of fragrance juices priced in the premium tier, spanning parfum, eau de parfum, eau de toilette, and extrait formats produced by prestige houses as well as independent niche brands. The scope captures finished juices sold through specialty stores, department stores, mono-brand boutiques, duty-free, and direct-to-consumer digital channels worldwide.

Scope exclusion: value estimates omit mass fragrances, private-label colognes, testers, and B2B concentrate sales.

Segmentation Overview

-

Product Type

- Parfum or de Parfum

- Eau de Parfum (EDP)

- Eau de Toilette (EDT)

- Eau de Cologne (EDC)

- Other Product Types

-

Category

- Conventional/Synthetic

- Natural/Organic

-

End-User

- Men

- Women

- Unisex

-

Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Others Distribution Channel

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview fragrance evaluators, duty-free buyers, raw-material suppliers, and boutique owners across Europe, North America, the Gulf, and East Asia. These dialogues validate average selling prices, refill adoption rates, and emerging demand for gender-neutral scents, which in turn sharpen assumptions drawn from secondary data.

Desk Research

We start with macro foundation blocks from sources such as UN Comtrade shipment codes for HS 3303, Eurostat retail indices, US Census Monthly Retail Trade, and industry notes from the International Fragrance Association. Company 10-Ks, investor decks, and patent libraries accessed through D&B Hoovers and Questel enrich brand pipeline visibility. Trade-press archives on Dow Jones Factiva and customs tariff updates supply timely event signals. This list is illustrative; many other public datasets inform benchmarking and sense-checks.

Market-Sizing & Forecasting

A top-down demand pool is built from premium personal-care expenditure per capita, tourist footfall in major travel hubs, and specialty retail floor space, which are then multiplied by fragrance penetration ratios. Bottom-up cross-checks, sampled brand ASP multiplied by volume scans and channel checks, refine totals. Key drivers modeled include disposable income growth, refill bottle uptake, counterfeit seizure trends, online luxury share, and new boutique openings. Multivariate regression, complemented by scenario analysis for price elasticity, projects values to 2030. Data voids in country splits are bridged through regional weighting tied to credit-card luxury spending indices.

Data Validation & Update Cycle

Outputs pass three-layer reviews, anomaly flags trigger re-contact of sources, and variances above two percentage points prompt recalibration. Reports refresh annually, with interim updates when exchange-rate shocks, blockbuster launches, or regulatory shifts materially reshape the baseline.

Why Our Luxury Perfume Baseline Commands Reliability

Published figures often diverge because each firm picks its own blend of channels, price bands, and inflation treatments. According to Mordor Intelligence, anchoring estimates to real sell-out flows and verified ASP ladders minimizes such drift.

Key gap drivers include whether artisanal labels and travel-retail sales are counted, the manner in which testers and gift sets are stripped out, currency conversion timing, and the frequency of refresh. Some providers rely on producer shipment data alone, which understates mark-ups, while others inflate totals by layering wholesale and retail values without reconciliation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 51.99 B (2025) | Mordor Intelligence | |

| USD 23.99 B (2024) | Global Consultancy A | Excludes niche brands and duty-free; uses conservative ASPs; older base year |

| USD 13.32 B (2024) | Industry Association B | Limits scope to prices above USD 200; omits online direct-to-consumer flows |

These contrasts show that Mordor's mixed top-down and bottom-up approach, refreshed every twelve months, delivers a balanced, transparent baseline that decision-makers can trace back to observable variables and repeatable steps.

Key Questions Answered in the Report

How large is the luxury perfume market in 2026?

The luxury perfume market size reached USD 49.69 billion in 2026 and is forecast to climb steadily on an 8.21% CAGR trajectory.

Which region is growing fastest for high-end fragrances?

Asia-Pacific is expanding at a 11.67% CAGR, driven by rising incomes in China, India, and Southeast Asia and by vibrant duty-free channels.

What segment leads by product concentration?

Eau de Parfum holds the largest share at 54.02%, while Parfum or de Parfum shows the fastest growth at 9.24% CAGR.

Why are natural formulations gaining traction?

Stricter allergen rules, wellness preferences, and third-party certifications are prompting consumers to trade up to natural and organic blends despite higher prices.

Page last updated on: