United Arab Emirates Beauty And Personal Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

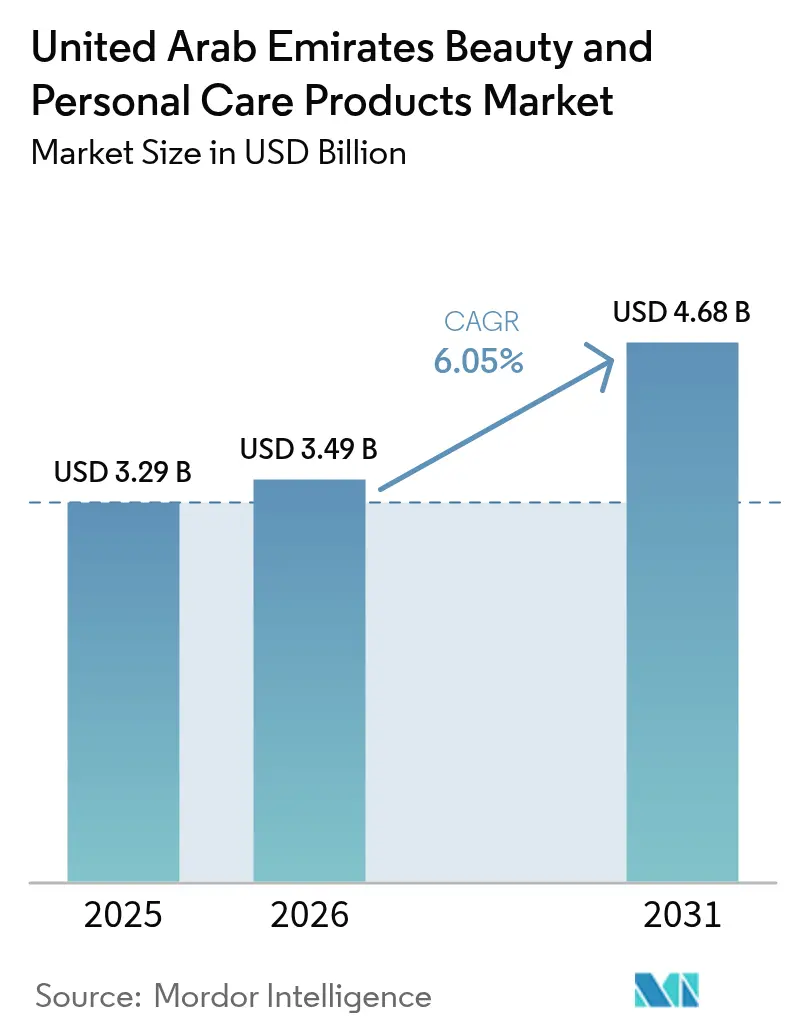

| Base Year Market Size (2025) | USD 3.29 Billion |

| Market Size (2026) | USD 3.49 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Arab Emirates Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The United Arab Emirates beauty and personal care products market size was valued at USD 3.29 billion in 2025 and estimated to grow from USD 3.49 billion in 2026 to reach USD 4.68 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Continuous tourist inflows, a digitally engaged population, and rising disposable incomes fuel steady demand for skin care, hair care, and color cosmetics. Season-linked passenger peaks at Dubai International Airport bolster duty-free fragrance sales, while government support for local manufacturing under the “Made in UAE” program strengthens domestic supply chains. Social media’s penetration level accelerates trend cycles and shortens product development timelines. However, counterfeit seizures and stringent halal certification rules temper expansion but simultaneously reward compliant brands that emphasize authenticity.

Key Report Takeaways

- By product type, personal care products commanded 88.72% revenue share in 2025, while cosmetics/makeup products are projected to expand at a 6.10% CAGR through 2031.

- By category, mass products held 67.10% of sales in 2025, whereas premium/luxury offerings are forecast to grow at a 5.52% CAGR to 2031.

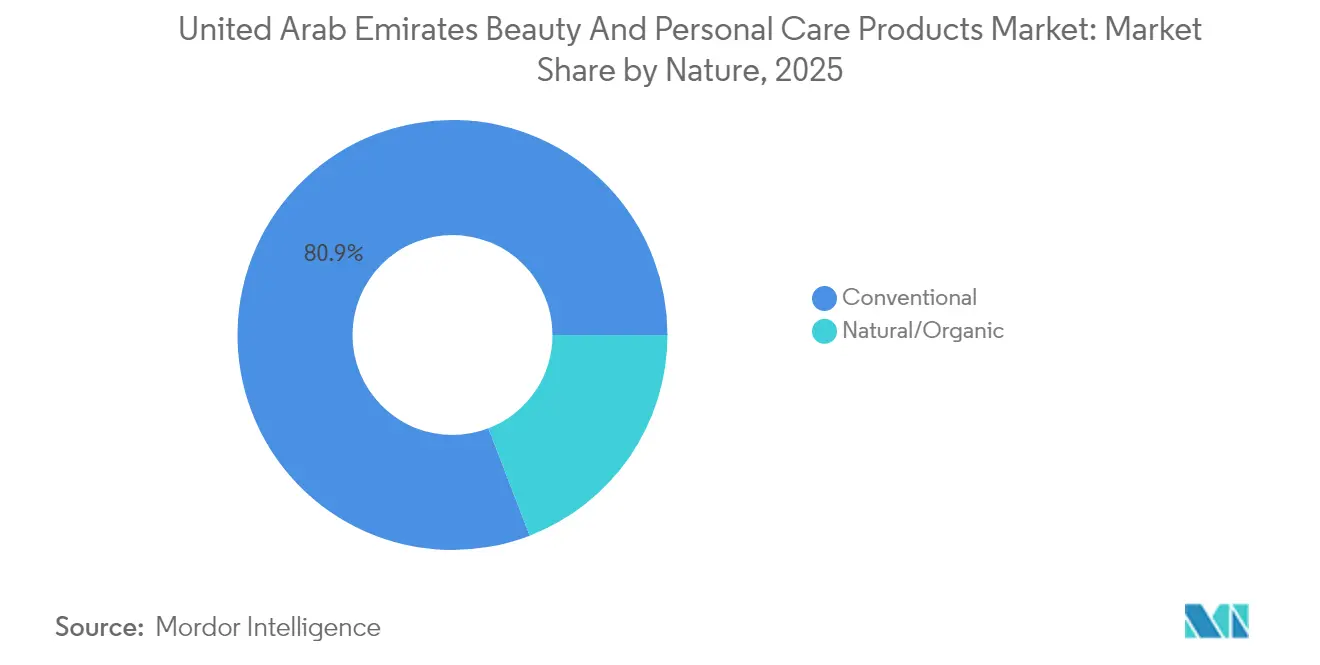

- By nature, conventional formulations captured 80.85% market share in 2025, yet natural and organic lines are advancing at a 5.79% CAGR through 2031.

- By distribution channel, health and beauty specialty stores led with 42.20% share in 2025, while online retail is rising at a 5.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong inbound tourism boosting duty-free and retail purchases | +1.8% | UAE nationwide, concentrated in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Increased awareness about personal grooming | +1.2% | UAE nationwide, stronger in urban areas | Medium term (2-4 years) |

| Rising impact of social media and beauty trends | +0.9% | UAE nationwide, particularly among millennials and Gen Z | Short term (≤ 2 years) |

| High demand for halal-certified and culturally relevant beauty products | +0.7% | UAE nationwide, spillover to broader GCC | Long term (≥ 4 years) |

| Government's "Made in UAE" initiative fostering local brands | +0.6% | UAE nationwide, manufacturing zones focus | Long term (≥ 4 years) |

| Brand expansion and product innovation | +0.5% | UAE nationwide, premium retail channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong inbound tourism boosting duty-free and retail purchases

Inbound tourism, a key driver of the UAE's economy, significantly fuels the beauty and personal care market, particularly in duty-free and retail purchases. In 2024, Dubai's international overnight visitors surged to 18.72 million, marking a 9% rise from the record 17.15 million in 2023, according to the Dubai Department of Economy and Tourism [1]Source: Government of Dubai, "City Focuses on Strategic Approach to Destination Growth as Upward Trajectory Continues", dubaidet.gov.ae. This tourism growth not only boosts personal beauty purchases but also amplifies gift-giving, especially for international travelers, heightening the demand for premium and travel-sized products. In 2024, the perfume category at Dubai Duty Free emerged as the primary growth driver, underscoring the influence of tourism on beauty consumption patterns. The diverse demographics of the emirate's visitors gravitate towards culturally neutral packaging. Yet, seasonal inventory challenges highlight the edge of companies adept in supply chain and inventory management. This intertwining of tourism and beauty bestows significant pricing power to premium brands. Boutiques of Chanel and Louis Vuitton at Dubai Duty Free’s terminal 3, for instance, consistently report growth. Additionally, the dynamics of travel retail lean towards compact, multifunctional products tailored for travelers, further cementing the UAE's sophisticated market and its pivotal role in the global personal care landscape.

Increased awareness about personal grooming

The UAE's expatriate-majority population, combined with dynamic social media influence, has significantly heightened personal grooming awareness, pushing standards well beyond traditional regional norms. This cultural shift manifests clearly in increased demand for specialized products, especially in hair care, skin care, and men's grooming categories, where consumers show willingness to invest in premium, multi-step skincare routines and professional-grade formulations. The labor force participation rate in the UAE stands at 54.1% for females and 89.6% for males as per the World Bank, 2024, underpinning a workforce increasingly attentive to workplace appearance and grooming expectations, amplified by corporate wellness programs across the service-oriented economy [2]Source: World Bank, "United Arab Emirates", genderdata.worldbank.org. Grooming has evolved from a mere daily habit to a valued form of self-expression and wellness, compelling brands to go beyond transactions by offering personalized consultation and educational content, which effectively differentiates them in a competitive market. This landscape benefits premium brands like L'Oréal Men and Nivea Men, which combine specialty product lines with digital engagement to capture discerning consumers. The growing grooming consciousness is further propelled by the rise of men-exclusive spas and wellness centers in the UAE, exemplified by venues such as 1847 Executive Grooming in Dubai. The convergence of a multicultural populace, social influence, and professional standards creates fertile ground for brands that deliver tailored, premium experiences aligned with evolving consumer sophistication, making personal grooming a key growth driver within the beauty and personal care products market in the UAE.

Rising impact of social media and beauty trends

Social media platforms, particularly Instagram and TikTok, are rapidly spreading beauty trends and influencing how consumers discover and purchase products in the UAE. Research underscores the pivotal role of Gulf female influencers in shaping the beauty landscape, especially among younger audiences who prioritize authentic user-generated content and peer endorsements, often valuing them more than traditional advertising. This evolution in marketing dynamics has led brands to invest heavily in local influencer collaborations and social commerce, aiming to tap into the swiftly changing trend-driven demand. The fast-paced nature of social media trends pushes beauty firms to embrace agile product development and inventive marketing tactics, allowing them to swiftly adapt to shifting consumer tastes. Brands such as The Body Shop are at the forefront, partnering with regional influencers to spotlight sustainability, a theme that resonates profoundly with the UAE's audience. These approaches cultivate genuine brand loyalty, surpassing the confines of traditional marketing and fostering a cycle of continuous engagement and innovation. In this landscape, companies boasting robust digital marketing skills and adaptability thrive, solidifying the UAE's status as a leading beauty market where social media and beauty trends are pivotal to industry expansion.

High demand for halal-certified and culturally relevant beauty products

The UAE’s Muslim-majority population, combined with its strategic position as a halal economy hub, significantly fuels demand for halal-certified beauty products, underpinned by the Emirates Authority for Standardization and Metrology (ESMA), which provides official certification frameworks ensuring compliance and authenticity. This demand transcends mere religious adherence, encompassing cultural preferences in ingredients, packaging, and marketing that deeply resonate with local values, enhancing consumer trust and loyalty. Halal certification introduces premium pricing due to the costs associated with verification and specialized sourcing, creating lucrative margin opportunities for brands adhering to these standards. The UAE’s role as a certification center additionally unlocks regional expansion potential, enabling halal-certified products to gain broader acceptance across GCC markets. Early investment in halal certification and culturally relevant product development helps companies build defensible competitive moats, limiting entry for non-compliant rivals. Brands like Amara Halal Beauty successfully leverage these dynamics by aligning product formulations and branding with halal principles and local cultural sensibilities. This ecosystem not only supports a sustainable premium segment but also strengthens the UAE’s standing as a regional leader in halal beauty, combining authenticity with commercial growth in its beauty and personal care products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit products | -0.8% | UAE nationwide, concentrated in traditional retail areas and free zones | Short term (≤ 2 years) |

| Regulatory barriers for new ingredient approvals or claims (esp. halal/natural) | -0.6% | UAE nationwide, affecting all distribution channels | Medium term (2-4 years) |

| Market saturation and intense competition | -0.7% | UAE nationwide, particularly in mass market segments | Medium term (2-4 years) |

| Public skepticism regarding product claims, especially for premium pricing | -0.5% | UAE nationwide, stronger impact in premium retail channels | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of counterfeit products

Dubai Customs seized counterfeit products valued at AED 42.195 million in the first quarter of 2025, highlighting the ongoing challenge counterfeit goods pose to the UAE's beauty and personal care market. As a global trade hub, the UAE inadvertently facilitates the circulation of counterfeit products, with beauty and cosmetics frequently topping the list. This undermines both consumer trust and safety. The issue hits hardest in premium segments, where authenticity commands a high price, and for smaller brands that often lack the resources for comprehensive anti-counterfeiting measures. In contrast, industry giants like L'Oréal leverage robust authentication systems and brand protection strategies, bolstering consumer confidence. While Federal Decree-Law No. 36 of 2021 on Trademarks imposes hefty penalties for counterfeiting, ranging from AED 100,000 to AED 1,000,000, enforcement faces challenges due to the UAE's extensive free trade zones and intricate supply chains. Despite a government-backed zero-tolerance stance and regular enforcement actions, counterfeiters adeptly navigate the emirate’s vast logistics infrastructure, revealing persistent vulnerabilities. In response, brands and authorities are ramping up investments in consumer education and cutting-edge authentication technologies. Yet, the scale and sophistication of counterfeit operations continue to pose significant challenges to market profitability and consumer safety in the UAE's beauty and personal care sector.

Regulatory barriers for new ingredient approvals or claims (esp. halal/natural)

Stringent regulatory barriers significantly influence the beauty and personal care market in the UAE, particularly in the approval of new ingredients and product claims. The Montaji system, managed by Dubai Municipality, enforces rigorous product registration and compliance checks, often leading to extended approval timelines and delaying product launches by several months. While this regulatory framework prioritizes consumer safety, it creates challenges for innovative formulations and novel ingredients lacking established safety profiles in the UAE. Demonstrating this regulatory vigilance, the Abu Dhabi Department of Health identified 41 unsafe products in early 2025, including cosmetics containing unauthorized ingredients such as hydroquinone and clobetasol propionate [3]Source: Department of Health Abu Dhabi, "Adulterated Products", doh.gov.ae. Successfully navigating this complex framework requires engagement with multiple authorities, including ESMA for standardization and various emirate-level bodies for distribution approvals. These regulatory intricacies tend to favor established multinational corporations, such as L’Oréal, which possess dedicated regulatory teams capable of efficiently managing compliance across products and regions. Conversely, smaller innovators may face slower rates of new product introductions. The UAE's regulatory landscape, aligned with Gulf Cooperation Council (GCC) standards like GSO 1943 and GSO 2528, emphasizes formula safety, transparent labeling, and substantiated claims. This environment aims to balance consumer protection with the demands of innovation, making it a critical consideration for businesses seeking growth in the UAE's evolving beauty and personal care sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominates Despite Cosmetics Acceleration

In 2025, personal care products account for 88.72% of the market share, highlighting the focus on essentials such as hair and skin care, oral hygiene, men's grooming, and fragrances. The segment's dominance is driven by consistent repurchase patterns and its broad demographic appeal, in contrast to the more discretionary nature of cosmetics purchases. However, cosmetics are experiencing rapid growth, with a projected CAGR of 6.10% through 2031. This growth is propelled by social media influence and the image-conscious younger population. The region's position as a beauty hub further accelerates this trend, with global trends quickly adopted through influencer marketing and premium retail channels.

Colgate-Palmolive is leading sustainability efforts in the personal care sector with the introduction of recyclable toothpaste tubes made from high-density polyethylene. Additionally, the company's global launch of the Optic White Whitening Pen in 2025, featuring advanced applicator technology and pressure venting systems, demonstrates its commitment to innovation in oral care. In the cosmetics segment, facial products are driving growth due to the climate-driven need for specialized foundations and concealers. Eye cosmetics are also thriving, supported by cultural preferences for bold eye makeup styles that align with both traditional and modern fashion trends.

By Category: Mass Market Stability Versus Premium Acceleration

In 2025, mass products command a 67.10% market share, reflecting price sensitivity among certain consumer segments and the widespread availability of these brands in hypermarkets and supermarkets. This stability in the mass segment ensures predictable revenue streams for industry giants like Unilever and Procter & Gamble, who adeptly use economies of scale to offer competitive prices. Meanwhile, premium/luxury products are on a growth trajectory, boasting a 5.52% CAGR through 2031. This surge is largely attributed to the UAE's affluent per capita income and its expatriate populace, many of whom are accustomed to elevated beauty standards from their native countries. As the premium segment expands, it opens doors for brands to enhance their profit margins by positioning themselves as luxury alternatives.

Partnerships and activations with beauty brands during the Dubai Shopping Festival highlight the advantages of premium positioning. These brands leverage experiential retail strategies, effectively justifying their elevated price points. Duty-free channels in the UAE present a particular boon for premium products. Here, global travelers actively seek out luxury brands and unique formulations, often unavailable in their home countries. Success in the mass market is increasingly tied to value-added features. These can range from sustainable packaging to specialized formulations tailored for the UAE's unique climate. On the other hand, premium brands carve their niche through exclusivity, innovative ingredients, and bespoke services, forging deeper emotional ties with the region's affluent consumers.

By Nature: Conventional Dominance With Organic Momentum

In 2025, conventional products account for 80.85% of the market share, reflecting established consumer preferences and the proven performance of traditional formulations across various skin types and climatic conditions in the UAE. Multinational companies, with significant investments in research and development, have tailored these products to endure the region's high temperatures and humidity. Meanwhile, natural/organic products are projected to grow at a 5.79% CAGR through 2031, driven by rising health consciousness and environmental awareness among younger consumers. This growth aligns with global clean beauty trends and the UAE's sustainability goals under its Net Zero by 2050 strategy.

In 2024, Kenvue launched its Aveeno Daily Moisturizing Cream, featuring prebiotic oat and shea butter, marketed as fragrance-free and paraben-free. This initiative highlights how established brands are leveraging natural positioning to capitalize on the expanding organic segment. Additionally, Kenvue's clinical study on 0.1% retinol, published in the Journal of Drugs in Dermatology, provides scientific validation for natural ingredient claims, addressing consumer skepticism regarding the efficacy of organic products. Dubai Municipality's regulatory framework, which mandates comprehensive ingredient disclosure, benefits transparent natural brands while posing compliance challenges for conventional products with complex chemical formulations.

By Distribution Channel: Specialty Stores Lead With Digital Disruption

Health and beauty specialty stores are projected to capture a 42.20% market share in 2025, driven by expert consultation services and curated product selections that resonate with quality-conscious consumers in the UAE. This channel's dominance highlights a strong consumer inclination toward personalized recommendations and the ability to test products before purchase, particularly in the color cosmetics and fragrance categories. Online retail stores are expected to grow at a 5.28% CAGR through 2031, supported by the UAE's position as the world's fastest-growing e-commerce market and a smartphone penetration rate exceeding 90%. This digital acceleration creates significant opportunities for direct-to-consumer brands and international players seeking cost-effective market entry strategies.

Ulta Beauty's partnership with Alshaya Group to enter the Middle East market in January 2025 exemplifies how international specialty retailers leverage local partnerships to establish a regional presence. This collaboration combines Ulta's beauty expertise with Alshaya's regional retail infrastructure, creating a hybrid model that bridges physical and digital channels. Supermarkets and hypermarkets play a complementary role by offering convenience for mass-market replenishment purchases, while independent pharmacies and salon channels cater to specialized professional products that require expert application guidance.

Geography Analysis

The beauty and personal care market in the UAE demonstrates distinct growth patterns, driven by the country's unique demographic composition and economic framework. The emirates of Dubai and Abu Dhabi dominate consumption, supported by their large expatriate populations, high disposable incomes, and extensive retail infrastructure, including duty-free operations catering to both residents and international travelers. While the northern emirates account for a smaller market share, they are experiencing increased consumption due to infrastructure development and population growth extending beyond traditional commercial hubs. Dubai's strategic position as a regional beauty hub leverages its location between European luxury brands and Asian manufacturing centers, offering pricing advantages and ensuring product availability across the UAE.

Tourism significantly influences consumption patterns, creating seasonal fluctuations that benefit retail channels concentrated in Dubai's commercial districts and airport facilities. Dubai Duty Free's AED 7.901 billion sales in 2024 highlight how tourism-driven demand complements resident consumption, fostering market dynamics that favor international brands with a strong duty-free presence. The UAE's expanding e-commerce infrastructure is enabling geographic growth beyond traditional retail centers, with online platforms providing access to beauty products across all emirates. Ministry of Economy data projects UAE e-commerce to grow from AED 27.5 billion in 2023 to AED 48.8 billion by 2028, showcasing how digital channels are reducing geographic barriers to product access.

The regulatory framework in the UAE, governed by Dubai Municipality's Montaji system and ESMA certification requirements, ensures standardized product safety and quality across all emirates, enhancing consumer confidence in beauty product purchases. Free trade zones in Dubai, Abu Dhabi, and Sharjah facilitate the entry of international brands and support local manufacturing operations. For instance, Epoch Cosmetics & Toiletries LLC operates production facilities in Umm Al Quwain to serve regional markets. The concentration of manufacturing and distribution infrastructure in the UAE's major emirates drives cost efficiencies, benefiting the entire market while aligning with the government's "Made in UAE" initiative to promote local production capabilities nationwide.

Competitive Landscape

The competitive landscape in the UAE's beauty and personal care market allows both global corporations and emerging local brands to establish distinct positions. Multinational leaders like L'Oréal, Unilever, and Procter & Gamble leverage extensive distribution networks and global brand equity to secure a strong presence. Simultaneously, local players such as Huda Beauty and Nabeel Perfumes capitalize on cultural relevance and regional market insights to build loyal customer bases. This dynamic highlights the necessity of integrating global scale with local expertise. For instance, L'Oréal’s 2025 sustainability partnerships with BinSina Pharmacy and Sephora address environmental concerns specific to the UAE.

Technological advancements are becoming critical for competitive differentiation, with companies heavily investing in e-commerce infrastructure, social media marketing, and personalized customer experiences to engage the UAE’s digitally savvy consumers. The rapid growth of online retail and the influence of social media have transformed traditional retail models, driving the need for agile digital strategies. Key opportunities exist in halal-certified premium products, men’s grooming specialization, and sustainable packaging that aligns with regulatory requirements and shifting consumer preferences. The Auréa-led consortium’s acquisition of The Body Shop highlights ongoing consolidation opportunities, while Huda Beauty's spin-off of Kayali to General Atlantic demonstrates how regional brands can achieve global scalability.

Regulatory compliance remains a critical factor in competitive positioning, with stringent standards such as Dubai Municipality’s Montaji system favoring companies with robust quality assurance operations. Henkel, for example, has enhanced its Dubai facility over the past decade with precision testing equipment to ensure packaging integrity and regulatory compliance, which are essential for building trust and maintaining market share. These market dynamics illustrate how global scale, local insights, technological innovation, and regulatory adherence collectively shape leadership in the UAE’s evolving beauty and personal care sector.

United Arab Emirates Beauty And Personal Care Products Industry Leaders

-

L’Oréal SA

-

Procter & Gamble Company

-

Unilever PLC

-

Coty Inc.

-

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: British beauty company UKLASH introduced UKHAIR, its first hair care product line, in the Middle Eastern market, including the UAE. The company, which had established recognition for its eyelash serum, developed a seven-product range comprising hair growth serum, shampoo, conditioner, repair mask, vitamins, and styling tools. The products focused on addressing hair thinning and improving scalp health. The paraben-free, sulfate-free formulations aligned with the Gulf region's increasing demand for vegan and cruelty-free beauty products.

- June 2025: TRUSS, a Brazilian professional haircare brand, launched in the UAE with its complete range of vegan products and a training academy for salon professionals. The brand's product line included the Infusion Line, Frizz Zero, Deluxe Prime sprays, and Curl collections, which were all vegan and cruelty-free. The company utilized biodegradable packaging that decomposed within eight years, reducing environmental impact.

- May 2024: Kay Beauty, founded by Katrina Kaif, expanded into the UAE market through the Nysaa store at City Centre Mirdif and nysaa.com. The brand's comprehensive makeup collection encompassed lip, eye, face, and nails products. The product line featured over 60 SKUs in the lips and face categories, and over 30 SKUs for nails and eyes, providing customers with a complete range of shades and colors for their makeup needs.

United Arab Emirates Beauty And Personal Care Products Market Report Scope

Color cosmetics are pigments that add color to make-up, skincare, hair care, personal hygiene, scents, and other personal care products. These cosmetics help give off a fresh and attractive look while improving the appearance, defining facial features, and covering blemishes and marks.

The United Arab Emirates color cosmetics market is segmented by Type into facial makeup, eye makeup, nail makeup, lip makeup, and hair color products. The market is segmented by distribution channel into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels.

The report offers market size and forecasts in value (USD million) for the above segments.

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colorant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Body Wash/Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men's Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Makeup Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Cosmetics | ||

| Mass Products |

| Premium/Luxury Products |

| Conventional |

| Natural/Organic |

| Supermarkets/Hypermarkets |

| Health and Beauty Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colorant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Body Wash/Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men's Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Makeup Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Cosmetics | |||

| By Category | Mass Products | ||

| Premium/Luxury Products | |||

| By Nature | Conventional | ||

| Natural/Organic | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Health and Beauty Specialty Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

Key Questions Answered in the Report

What is the current value of the United Arab Emirates beauty and personal care products market?

The market is valued at USD 3.49 billion in 2026 and is forecast to reach USD 4.68 billion by 2031.

Which product type contributes most to revenue?

Personal care items such as skin, hair, and oral-care products account for 88.72% of overall sales.

How fast is the premium segment expanding?

Premium and luxury products are advancing at a 5.52% CAGR between 2026 and 2031.

Which retail channel is growing the quickest?

Online platforms are increasing at a 5.28% CAGR, supported by high smartphone use and robust logistics.

Page last updated on: