Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

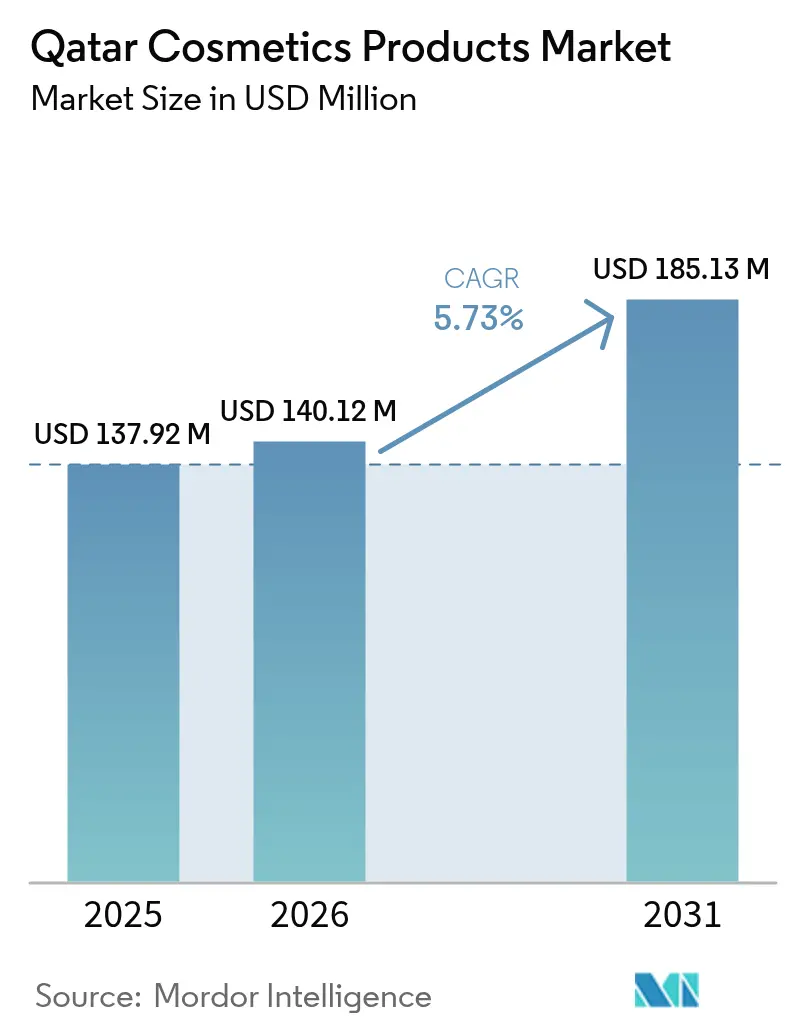

| Base Year Market Size (2025) | USD 137.92 Million |

| Market Size (2026) | USD 140.12 Million |

| Market Size (2031) | USD 185.13 Million |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

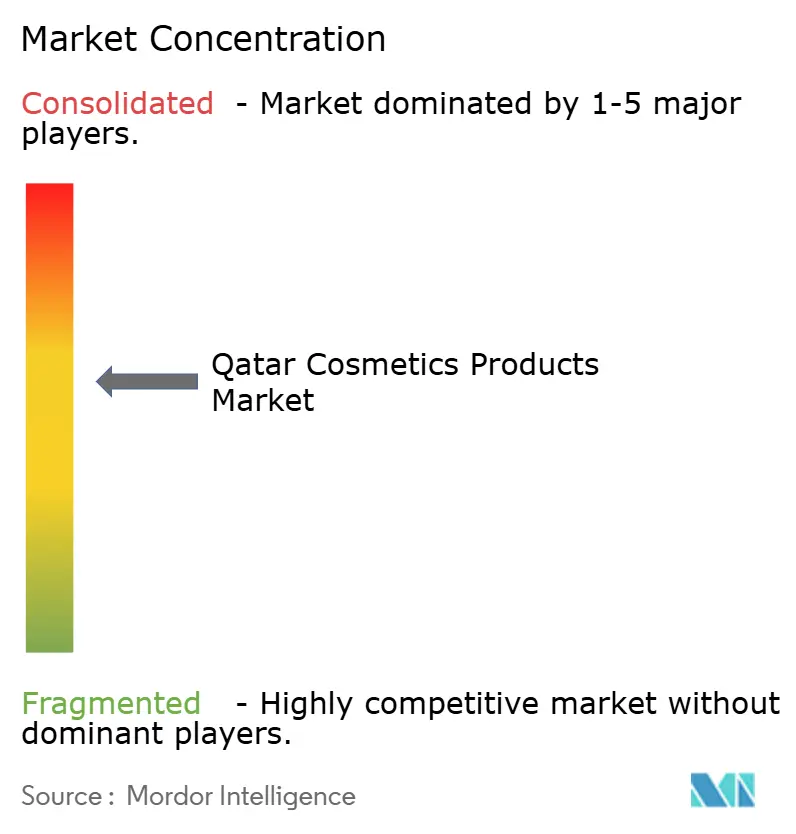

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Cosmetics Products Market Analysis by Mordor Intelligence

The Qatar cosmetics products market size is expected to increase from USD 137.92 million in 2025 to USD 140.12 million in 2026 and reach USD 185.13 million by 2031, growing at a CAGR of 5.73% over 2026-2031. Qatar’s highest GDP per capita in the GCC, premium-oriented retail infrastructure exceeding 2.3 million m², and duty-free hubs at Hamad International Airport provide a fertile launchpad for global beauty brands that seek affluent, experience-driven shoppers. Mandatory cosmetics registration by the Ministry of Public Health creates a compliance barrier that discourages the rapid influx of low-cost imports and indirectly protects pricing power for established players. Halal certification moved from niche differentiator to baseline expectation, allowing certified lines to command up to double-digit price premiums in a society where religious adherence and ingredient safety are intertwined. Experiential luxury venues, such as Lancôme Café De La Rose at the airport and Dolce & Gabbana Beauty inside Place Vendôme, blur retail, hospitality, and entertainment, extending dwell time and nurturing repeat purchases that reinforce the Qatar cosmetics products market’s premium skew.

Key Report Takeaways

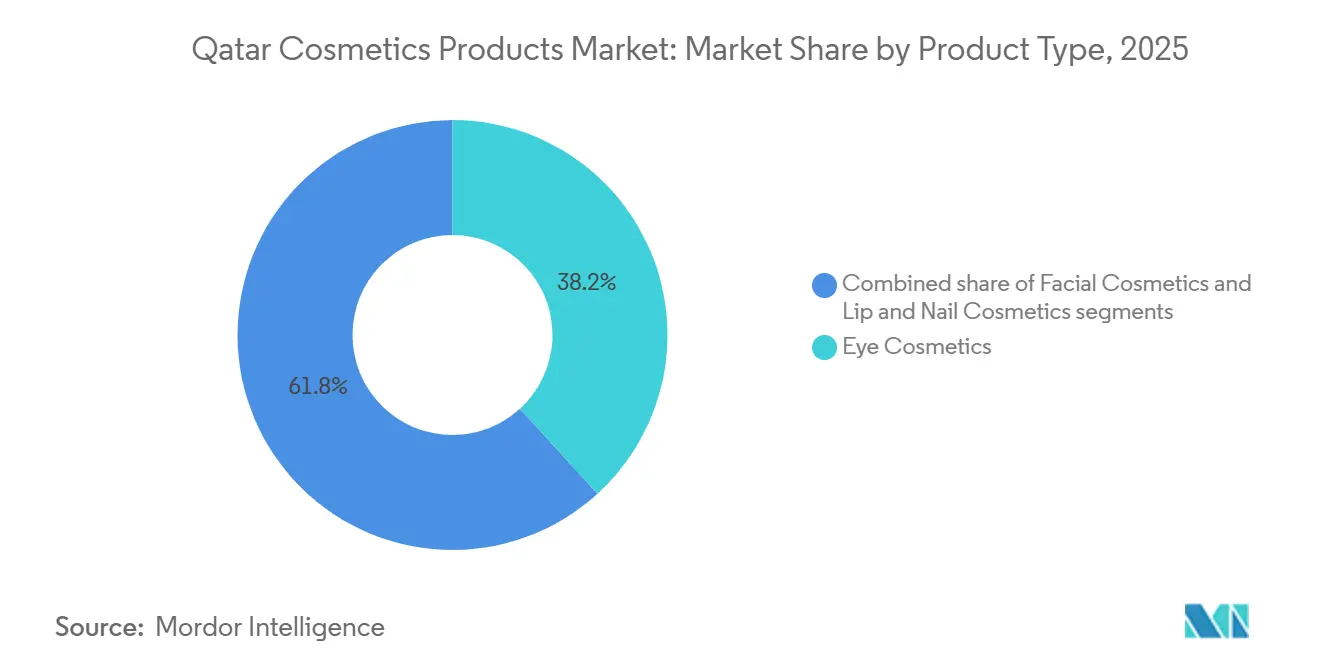

- By product type, eye cosmetics captured 38.21% of the Qatar cosmetics products market share in 2025, while facial cosmetics are advancing at a 7.08% CAGR through 2031.

- By category, mass-market lines held 56.45% of the Qatar cosmetics products market in 2025; premium offerings are expanding at a 8.21% CAGR to 2031.

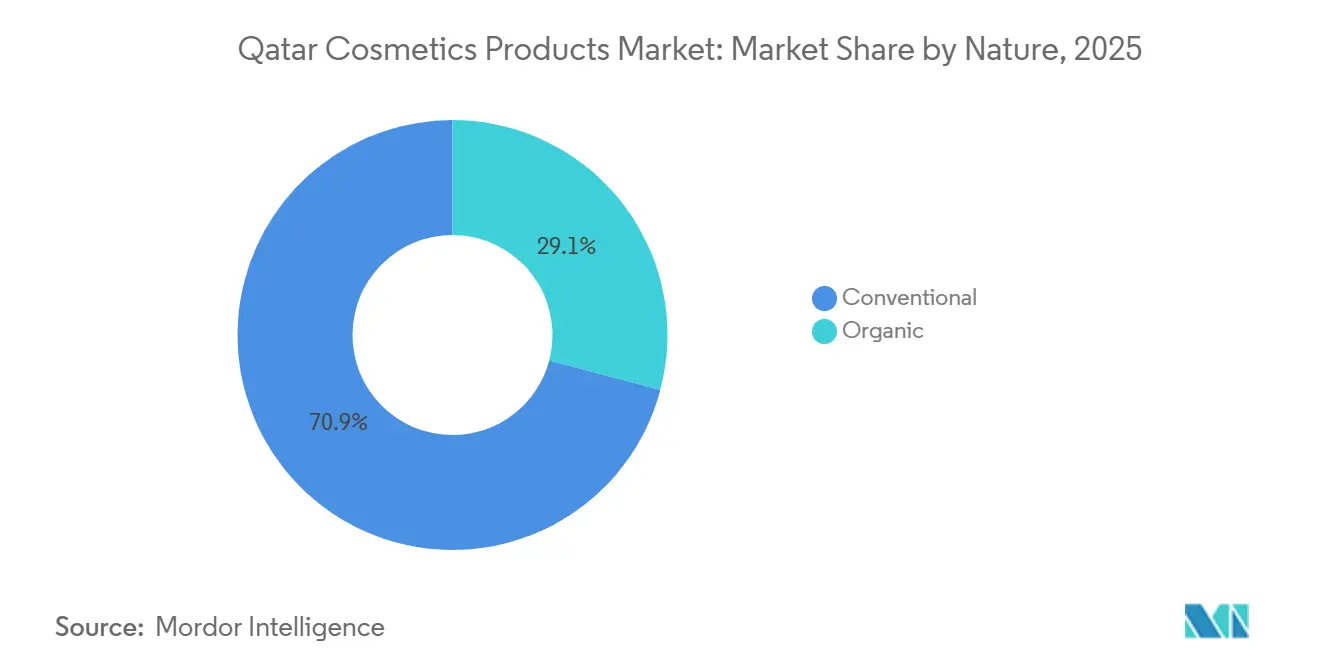

- By nature, conventional items accounted for 70.18% of the Qatar cosmetics products market size in 2025, while organic alternatives are on course for a 6.42% CAGR growth.

- By distribution channel, specialty beauty stores led with 40.22% revenue share in 2025, whereas online retail is projected to grow 7.50% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Cosmetics Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Halal, Clean, and Organic Offerings | +1.2% | Qatar (national), spillover to broader GCC | Medium term (2-4 years) |

| Surge in Male Grooming and Unisex Product Adoption | +0.9% | Qatar urban centers (Doha, Lusail), GCC-wide trend | Short term (≤2 years) |

| Expansion of Youthful, Fashion-Savvy Demographics | +1.1% | Qatar (63% of Saudi population under 30, similar youth cohort in Qatar) | Long term (≥4 years) |

| Social Media's Role in Fueling Market Expansion | +0.8% | Qatar (national), amplified in digitally connected urban areas | Short term (≤2 years) |

| Demand for Convenient, Multi-Functional Solutions | +0.7% | Qatar (national), particularly relevant in hot, humid climate zones | Medium term (2-4 years) |

| Influx from Tourism and Expat Populations | +0.6% | Qatar (Doha, Hamad International Airport catchment) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Halal, Clean, and Organic Offerings

Halal certification has shifted from being a simple compliance requirement to a significant competitive advantage, enabling brands to charge premium prices. Qatar's Ministry of Public Health requires halal compliance for all imported cosmetics, setting a regulatory standard that also raises consumer expectations. Notably, 38% of GCC consumers now prioritize natural ingredients over cost, while 28% place them above proven efficacy. This trend reflects a growing consumer preference for ingredient transparency, even at the expense of performance claims. Demonstrating the market's potential, OnePure LLC raised USD 50 million in Series B funding in April 2025. This investment highlights confidence in plant-based formulations that combine halal certification with sustainable packaging, targeting environmentally conscious Muslim consumers who view product origin as an extension of their ethical values. Additionally, AI-powered molecular authentication systems are being introduced to ensure the integrity of halal ingredients, addressing supply chain trust issues and reducing the risk of contamination that could compromise certification and lead to costly recalls.

Surge in Male Grooming and Unisex Product Adoption

Male grooming products, historically confined to basic skincare and fragrances, are expanding into color cosmetics and advanced skincare as younger Qatari men embrace grooming routines influenced by South Korean beauty trends and social media visibility. Chalhoub Group reported 20-25% annual growth in skincare at its FACES retail chain, with a notable uptick in male customers purchasing serums, sunscreens, and tinted moisturizers that deliver subtle coverage without overt makeup signaling. Unisex fragrances, which accounted for 49% of GCC beauty sales in 2024, reflect cultural preferences for oud-based scents that transcend gender binaries, yet this category's dominance masks an emerging opportunity in gender-neutral color cosmetics where brands like Huda Beauty's Kayali, separated from its parent in March 2025 to scale independently, are testing layerable, sheer formulations designed for diverse skin tones and application contexts. The Body Shop's interactive activist concept store in Doha, opened in 2022, introduced gender-neutral product merchandising and unisex packaging that resonated with Gen Z shoppers who reject traditional beauty aisle segmentation

Expansion of Youthful, Fashion-Savvy Demographics

From 2018 to 2023, Qatar's population grew at a 1.5% CAGR. Combined with a youthful demographic, 63% of whom are under 30, similar to Saudi Arabia, this has created a consumer base that views beauty purchases as a form of identity expression rather than a functional need. This fashion-conscious group quickly adopts trend-driven products. For example, e.l.f. Beauty strategically entered the GCC market through Sephora in November 2025, leveraging a 38% year-over-year increase in regional social media mentions. This digital momentum not only preceded their retail launch but also accelerated the traditional awareness-to-trial process. Additionally, Place Vendôme recorded a 64% rise in visitors in 2024, highlighting the demographic's preference for experiential retail. Beauty purchases in such environments often double as social media content, with stores featuring AR skin analyzers and 'magic mirrors' that turn transactions into shareable experiences. A survey conducted by Qatar University's SESRI found that Qatari consumers prioritize quality over price[1]Source: Qatar University SESRI, “Survey on Consumer Quality Priorities,” qu.edu.qa. This preference allows premium brands to introduce limited-edition collaborations and exclusive colorways, which command a 20-40% price premium over standard SKUs.

Social Media's Role in Fueling Market Expansion

In the GCC, social media platforms, particularly Instagram and TikTok, have become influential discovery engines. Beauty influencers now drive purchase decisions more effectively than traditional advertisements. GCC consumers, in particular, engage with AI-driven influencer campaigns 40% more than with static content. L'Oréal Travel Retail's YSL Beauty "Summer Mirage" activation at Hamad International Airport, held from July to October 2024, exemplified innovation. This campaign, in partnership with Qatar Airways, combined push notifications via the airline's app with personalized digital out-of-home ads. This pentarchy partnership, comprising the airline, airport, retailer, brand, and media, successfully increased foot traffic. By targeting passengers two hours before departure, the campaign offered tiered gifts based on loyalty status. Chalhoub Group's Layla AI chatbot, which processes 79% of its interactions in Arabic, highlights a key insight: localized digital assistants outperform English-language tools. They effectively address cultural nuances in beauty consultations, such as preferences for modest makeup and halal ingredient verification. E.l.f. Beauty's GCC market entry strategy demonstrates the value of social validation. By building social demand before physical distribution, the brand showcased how social listening and pre-launch campaigns can reduce market entry risks.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Hurdles and Elevated Compliance Expenses | -0.5% | Qatar (national), affecting all importers and manufacturers | Short term (≤2 years) |

| Proliferation of Counterfeit Goods | -0.4% | Qatar (national), concentrated in informal retail channels | Medium term (2-4 years) |

| Persistent Supply Chain Interruptions | -0.3% | Qatar (national), with spillover from global logistics disruptions | Short term (≤2 years) |

| Heavy Reliance on Imported Supplies | -0.2% | Qatar (national), affecting inventory management and pricing | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Hurdles and Elevated Compliance Expenses

Qatar's Ministry of Public Health requires all cosmetic products to undergo pre-market registration. This process involves submitting documentation such as ingredient lists, manufacturing certificates, and safety assessments, which can cost between USD 2,000 and 5,000 per SKU and delay product launches by 3 to 6 months[2]Source: Ministry of Public Health Qatar, “Cosmetics Registration,” moph.gov.qa. While this regulatory framework ensures consumer safety, it creates significant hurdles for smaller brands and indie labels. These companies often lack dedicated regulatory affairs teams or regional distribution partners, making it challenging to handle Arabic-language documentation and coordinate with government agencies. Additionally, the ministry's banned substances list, which includes lead-based kohl and certain preservatives commonly used in international formulations, forces brands to reformulate products specifically for the Qatari market. This reformulation increases development costs and reduces margins on lower-volume SKUs. Although halal certification is not legally required, it has become a practical necessity for market acceptance. Brands must secure approvals from recognized bodies and maintain segregated supply chains to avoid cross-contamination. For companies without existing halal infrastructure, this process can raise production costs by 10-15%. Compliance costs also extend to labeling requirements, where Arabic translations must accompany English text, and font sizes must meet minimum legibility standards. These requirements often necessitate packaging redesigns, increasing per-unit costs by USD 0.20-0.50, which is particularly burdensome for mass-market products with already narrow profit margins.

Proliferation of Counterfeit Goods

Counterfeit cosmetics, identified by OECD research as entering Qatar through informal channels, undermine brand equity and expose consumers to untested ingredients that can cause allergic reactions or long-term health effects[3]Source: OECD, “Trade in Counterfeit Goods and the Palestinian Territories,” oecd.org. Fake luxury beauty products, often sold at 30-50% discounts versus authentic items, target price-sensitive consumers who prioritize brand names over purchase channel verification, creating a parallel market that diverts revenue from authorized retailers and manufacturers. Qatar Customs has intensified enforcement actions, yet the sophistication of counterfeit packaging—including holographic seals, QR codes, and batch numbers that mimic genuine products—makes detection challenging without laboratory testing or brand authentication partnerships. The proliferation of counterfeit goods is particularly damaging in the premium segment, where brand perception depends on exclusivity and quality assurance; a single viral social media post exposing fake products purchased in Qatar can trigger regional reputation damage that requires costly marketing campaigns to remediate. E-commerce platforms, while offering convenience, inadvertently facilitate counterfeit distribution when third-party sellers list unauthorized products alongside genuine inventory, creating consumer confusion and eroding trust in online channels that are critical to the 7.50% CAGR projected for online retail distribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Eye Dominance Faces Facial Momentum

Eye cosmetics held a 38.21% Qatar cosmetics products market share in 2025, anchored by kohl and kajal’s cultural significance. Yet volume growth is plateauing as Gen Z gravitates toward minimal-makeup aesthetics and lightweight tubing mascaras that withstand 45 °C summers without smudging. Facial cosmetics are projected to notch the fastest 7.08% CAGR, and within that surge, BB creams and cushion foundations that fuse SPF, hydration, and coverage resonate with consumers who want one-step routines. E.l.f. Beauty’s region-wide launch demonstrates how data-backed shade assortments can challenge incumbents by marrying affordability with trend currency.

The eye segment’s innovation now hinges on vegan, water-permeable halal liners and lash serums that complement ablution practices, positioning local startups for niche capture. Facial players experiment with adaptive pigments and airless pumps that tolerate indoor-outdoor humidity swings, ensuring texture stability. As climate-ready skincare ingredients migrate into complexion products, the Qatar cosmetics products market size for hybrid facial lines is expected to expand steadily, creating cross-sell opportunities into primers and setting sprays formulated for high-UV locales.

By Category: Premium Ascends While Mass Retains Breadth

Mass products represented 56.45% of revenue in 2025, supported by Carrefour and Lulu shelf breadth and ticket sizes under QAR 75, yet premium lines outpace at 8.21% CAGR, propelled by ultra-luxury malls and duty-free exclusives. High disposable income allows Qatari shoppers to prioritize sensorial packaging, personalized engraving, and limited-edition drops, all of which mitigate price sensitivity. The premium tier benefits from Lancôme Café De La Rose’s food-and-beauty fusion that converts dwell time into sampling, reinforcing post-travel loyalty.

Mass brands, facing online price transparency, defend share with Korean-inspired multitaskers and private-label assortments. They integrate QR-code traceability to assure authenticity and speed line extensions by white-labeling proven regional shades. Even so, as more consumers equate ingredient safety with higher spend, the Qatar cosmetics products market size captured by premium players is forecast to stretch its lead, especially within skincare-centric cosmetics.

By Nature: Conventional Stronghold, Organic Gains Credibility

Conventional formulas accounted for 70.18% of the 2025 value, buoyed by stability, wider shade ranges, and aggressive promotion across specialty and mass channels. Organic SKUs, however, are progressing at a 6.42% CAGR, supported by OnePure’s capital injection and retailers’ education campaigns clarifying overlap and divergence between halal and organic labels. ECOCERT badges function as proof points for wellness-oriented buyers who accept shorter shelf life in exchange for perceived safety.

Conventional giants, mindful of reputation risk, are stripping parabens and talc from hero SKUs while launching vegan offshoots to retain loyalty. Packaging advances such as Estée Lauder’s refill pods satisfy sustainability expectations without sacrificing product aesthetics. Given climate stresses on formulation integrity, organic brands must master cold-chain logistics or deploy natural preservatives that withstand 35 °C warehouses. The Qatar cosmetics products market share for green labels will likely broaden once supply reliability matches consumer intent.

By Distribution Channel: Specialty Stores Anchor, Online Accelerates

Specialty beauty stores controlled 40.22% of sales in 2025 by offering diagnostics, sampling, and curated storytelling that justify premium tags. Yet online portals are accelerating at 7.50% CAGR as AI chatbots deliver Arabic consultations that mirror in-store advisory quality, proving digital convenience no longer compromises personalization. Hybrid journeys dominate: shoppers test fragrance strips at Sephora, then reorder duty-free minis through sephora.me to secure loyalty points and tax savings.

Hypermarkets sustain foot traffic among value seekers but risk share attrition if they cannot provide shade matching or ingredient transparency filters that e-commerce excels at. Omnichannel players like LETOILE capitalize by syncing stock visibility across app and store, ensuring click-and-collect within two hours. As payment gateways normalize buy-now-pay-later and cross-border fulfillment, the Qatar cosmetics products market size attributed to pure-play online specialists is set to climb, though experiential flagships will remain critical for prestige sampling.

Geography Analysis

In Doha, luxury corridors such as The Pearl, Doha Festival City, and Lusail Boulevard account for the majority of spending. These locations enhance the shopping experience with AR mirrors and concierge services, turning it into a form of entertainment. Duty-free revenues, driven by visitors attending MICE events or on layovers, reached USD 861.5 million. This success serves as an international platform for airport-exclusive product launches, which gain momentum on social media and later appear in downtown outlets. The city's diverse expatriate population broadens SKU requirements, prompting retailers to cater to varied preferences and formulation philosophies.

Secondary hubs like Al Rayyan and Al Khor are witnessing increased disposable incomes due to infrastructural developments following the FIFA World Cup. However, these areas remain underserved by prestige counters, creating an opportunity for omnichannel chains to introduce click-and-collect lockers. While rural areas see limited penetration due to low population density, next-day shipping from Doha warehouses ensures nationwide product availability. Regionally, Qatar should keep an eye on Saudi Arabia's manufacturing investments, which promise faster lead times and tariff-free supplies, potentially challenging Doha's pricing competitiveness if freight costs rise.

International tourism significantly contributes to Qatar's growth. In Q1 2025, the country welcomed 4.4 million visitors. Many of these tourists converted airport impulse purchases into cross-border e-commerce orders after returning home, expanding the online shopper base beyond residents. As Qatar shifts toward hosting year-round events, such as fashion weeks and art fairs, the spending geography may expand. Pop-up venues outside traditional malls could emerge, integrating the Qatari cosmetics market with the nation's hospitality and cultural sectors.

Competitive Landscape

The market demonstrates moderate concentration, with the top five portfolios accounting for just over 60% of the share. This reflects a balance between the strength of multinationals and the dynamism of local challengers. L’Oréal, Estée Lauder, and LVMH utilize their multi-brand strategies to penetrate duty-free, specialty, and mass markets, effectively mitigating risks across various price tiers. Meanwhile, Chalhoub’s FACES and SKIN CARE NATION leverage regional insights, emphasizing Arabic-first services and AI-driven personalization to strengthen their position against global e-commerce competitors.

Innovation distinguishes the leaders. Lancôme's Café De La Rose combines gastronomy with skincare, generating social media engagement and premium ticket upgrades, which traditional retailers struggle to replicate. Estée Lauder's refill initiative reduces packaging waste by 20%, appealing to environmentally-conscious consumers and easing regulatory pressures. E.l.f. Beauty employs data-driven color narratives to challenge premium pricing, pushing established brands to redefine their value propositions beyond heritage.

Local startups are focusing on authenticity. OnePure, offering halal and vegan products in compostable packaging, attracts ESG-focused investors and Muslim millennials seeking ethical luxury. Addoony Cosmetics targets Gen Z with Arabic pop-culture-inspired packaging. Meanwhile, biotech firm QatarBio is developing date-seed antioxidants, signaling the future of cosmeceuticals. While competition is intense in premium facial care and fragrances, opportunities remain in halal nail products and men's skincare, where brand recognition is still limited.

Qatar Cosmetics Products Industry Leaders

L'Oréal S.A

Coty Inc.

Shiseido Co. Ltd

The Estée Lauder Companies Inc.

Louis Vuitton Moët Hennessy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pinky Blush Beauty Lounge became the first in Qatar to introduce MANUCURIST Paris No-TPO Vegan Gel Polishes. This launch marked a significant step in offering eco-friendly and innovative nail care solutions to customers in the region.

- August 2025: Anthropologie announced the launch of its new beauty category, which debuted this month in its Qatar store. This expansion into the beauty segment was introduced in collaboration with Bassam Fattouh, a highly regarded figure in the regional makeup industry, aiming to enhance its product offerings and cater to diverse consumer preferences.

- December 2024: Chanel, in collaboration with Qatar Duty-Free, kicked off a three-month takeover at Hamad International Airport, dubbed "Chanel Winter Tale." This festive endeavor features interactive experiences, a handpicked assortment of exclusive and limited-edition products, personalized gifts and souvenirs, and fun activities for families.

- September 2024: Kosas announced its exclusive launch at Sephora across the Middle East. Known for its clinically backed, skin-friendly makeup, the brand became popular among celebrities like Hailey Bieber and Kylie Jenner, and expanded its reach to beauty enthusiasts in Qatar.

Qatar Cosmetics Products Market Report Scope

Cosmetics, composed of chemical compounds sourced from nature or synthesized, are applied to the human body for purposes like cleaning and beautifying.

The Qatari cosmetics market is categorized by product type and distribution channel. By product type, the market is divided into color cosmetics and hairstyling/coloring products. The color cosmetics category breaks down into facial, eye, and lip/nail makeup. Hairstyling/coloring further divides into hair colors and styling products. Distribution channels include hypermarkets/supermarkets, specialty stores, pharmacies and drug stores, online retail, and others.

Market sizing and forecasts for each segment are based on value (in USD).

By Product Type

| Facial Cosmetics |

| Eye Cosmetics |

| Lip and Nail Cosmetics |

By Category

| Mass |

| Premium |

By Nature

| Organic |

| Conventional |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Health and Beauty Stores |

| Online Retail Channels |

| Other Channels |

| By Product Type | Facial Cosmetics |

| Eye Cosmetics | |

| Lip and Nail Cosmetics | |

| By Category | Mass |

| Premium | |

| By Nature | Organic |

| Conventional | |

| By Distribution Channel | Supermarkets / Hypermarkets |

| Health and Beauty Stores | |

| Online Retail Channels | |

| Other Channels |

Key Questions Answered in the Report

How large is the Qatar cosmetics products market in 2026?

It is valued at USD 140.12 million, on track to reach USD 185.13 million by 2031.

Which product segment is growing the fastest?

Facial cosmetics are forecast to post a 7.08% CAGR through 2031, outpacing other categories.

Why are premium cosmetics outperforming mass lines?

Higher GDP per capita, experiential retail in luxury malls, and duty-free tax savings drive consumers to trade up despite higher prices.

What is the main distribution shift expected by 2031?

Online retail is projected to grow at 7.50% CAGR as AI-powered Arabic consultations narrow the service gap with specialty stores.

Page last updated on: