Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

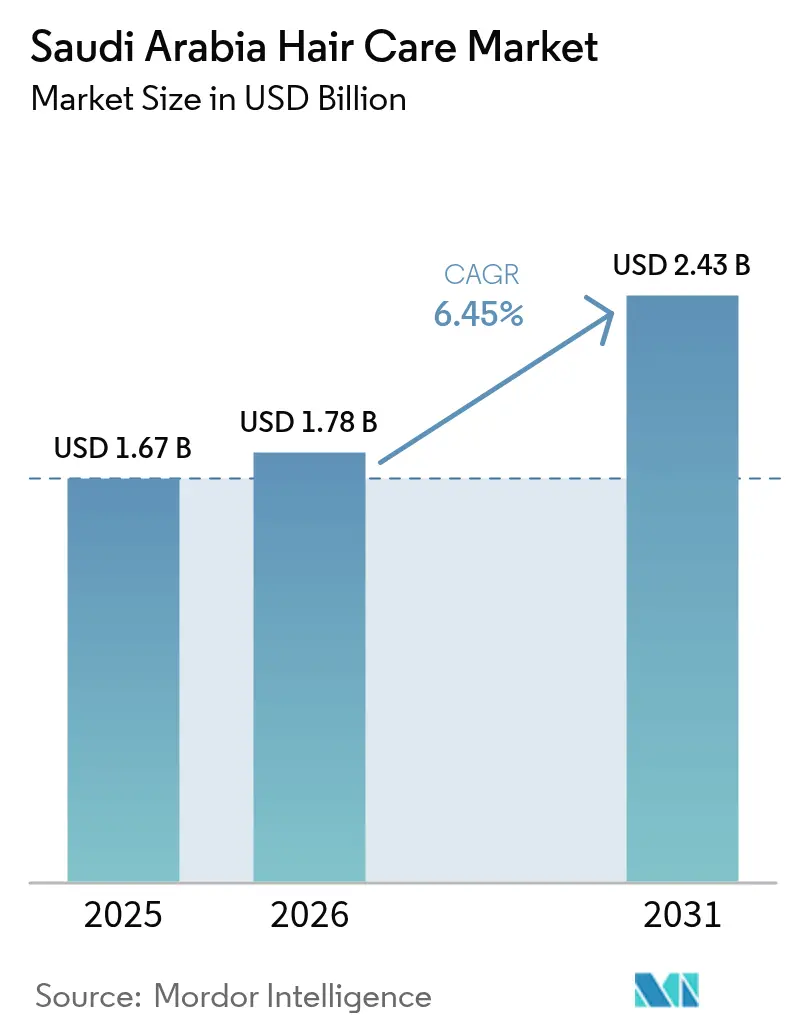

| Base Year Market Size (2025) | USD 1.67 Billion |

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

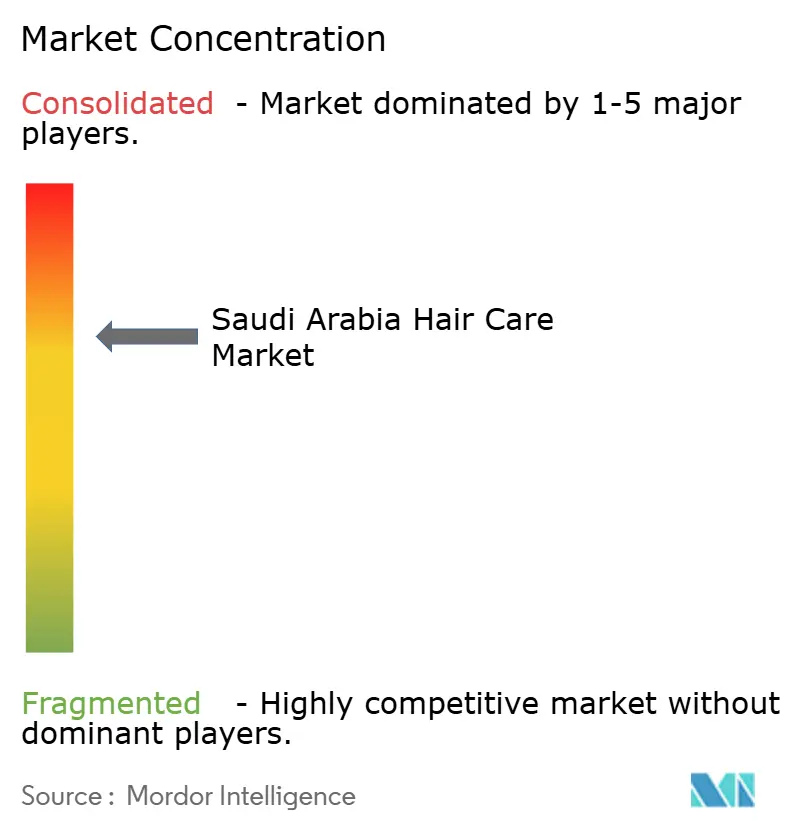

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Hair Care Market Analysis by Mordor Intelligence

Saudi Arabia Hair Care Market size in 2026 is estimated at USD 1.78 billion, growing from 2025 value of USD 1.67 billion with 2031 projections showing USD 2.43 billion, growing at 6.45% CAGR over 2026-2031. This growth trajectory positions Saudi Arabia as the largest and fastest-growing beauty market in the Gulf Cooperation Council, driven by a unique convergence of demographic dividends, digital transformation, and evolving cultural norms that are reshaping consumer behavior across personal care categories. The market's structural evolution reflects broader societal shifts, including increased female workforce participation and social reforms that have expanded women's public presence, directly translating into higher demand for professional grooming products.

Key Report Takeaways

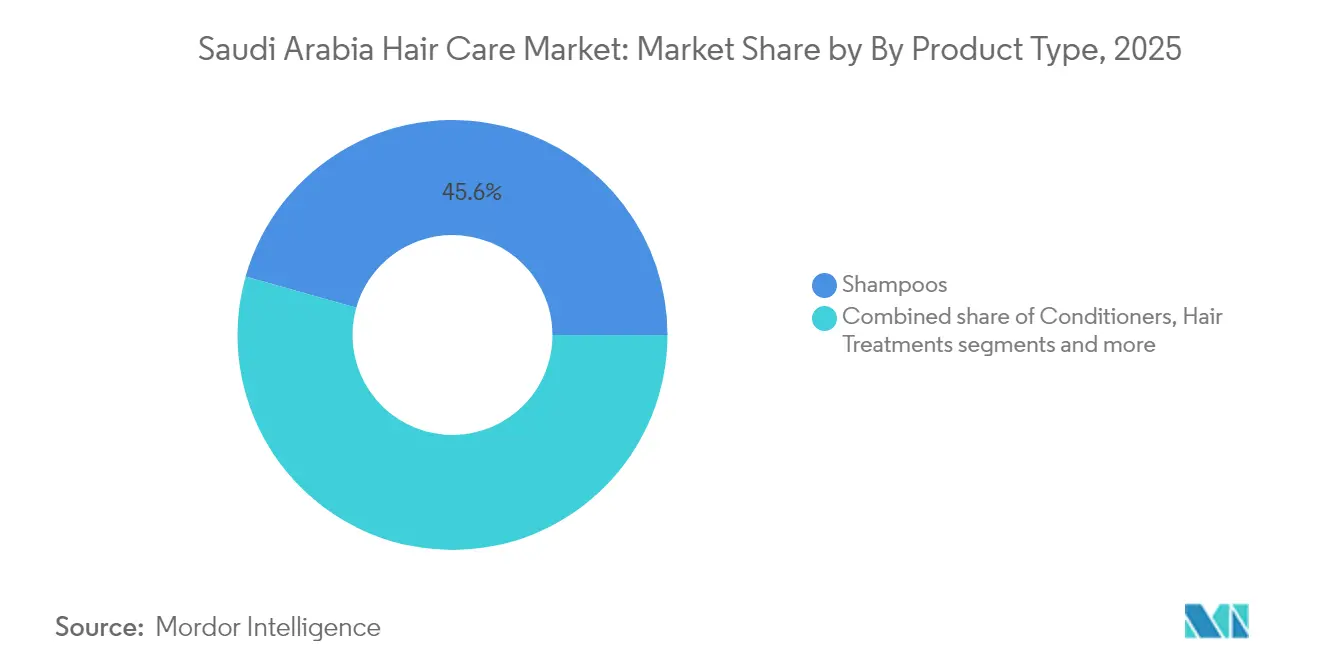

- By product type, shampoos held 45.62% of the Saudi Arabia hair care market share in 2025, while hair treatments are forecast to advance at a 7.02% CAGR between 2026-2031.

- By category, the mass segment captured 71.45% revenue in 2025; premium/luxury is positioned to expand at an 7.83% CAGR to 2031.

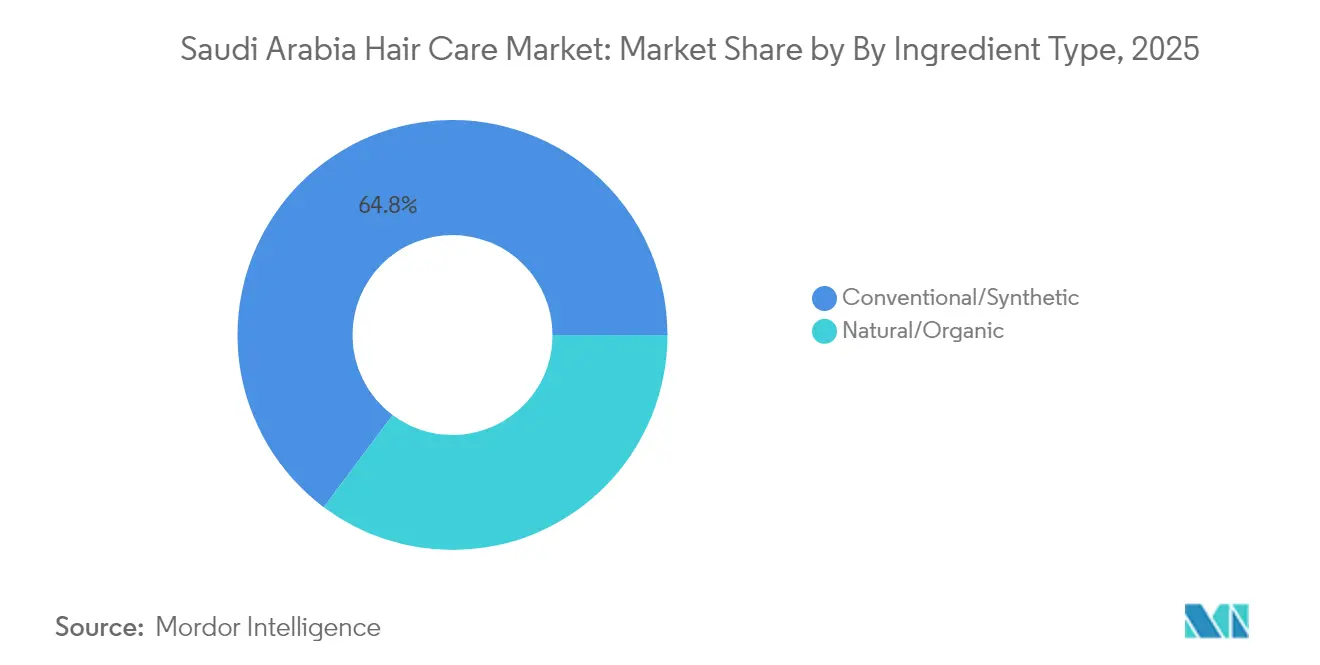

- By ingredient, conventional/synthetic accounted for 64.78% of the Saudi Arabia hair care market size in 2025, but natural/organic formulations are projected to grow at an 8.06% CAGR through 2031.

- By distribution, hypermarkets/supermarkets led with 39.85% share in 2025, whereas online retail stores post the highest expected channel CAGR of 8.11% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Emphasis on personal grooming and hygiene | +1.2% | National, concentrated in major cities | Medium term (2-4 years) |

| Influence of social media and beauty influencers | +1.8% | National, strongest in urban areas | Short term (≤ 2 years) |

| Preference for natural and organic formulations | +1.1% | National, premium segments | Long term (≥ 4 years) |

| Concerns around hair loss and scalp health | +0.9% | National, male-focused growth | Medium term (2-4 years) |

| Product innovation and customization | +0.7% | Urban centers, tech-savvy demographics | Long term (≥ 4 years) |

| Growing Male Grooming | +1.0% | National, accelerating in younger cohorts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Influence of social media and beauty influencers

Social media has become deeply embedded in Saudi Arabia's population, establishing powerful platforms that shape consumer behavior. Channels like TikTok and Instagram now play a pivotal role in how beauty products are discovered and purchased, driving unprecedented influence across the market. The phenomenon extends beyond traditional advertising, with online content now playing a dominant role in shaping consumer behavior. This shift has transformed how individuals in Saudi Arabia research and choose hair care products, making digital influence a key driver in purchase decisions. This digital transformation has enabled rapid trend propagation, with hair care brands leveraging short-form video content and influencer partnerships to drive product trials and brand switching. The cultural significance of this shift cannot be overstated, social media has democratized beauty expertise, allowing consumers to access professional-grade advice and product recommendations that were previously limited to salon visits.

Emphasis on personal grooming and hygiene

The convergence of cultural evolution and economic prosperity has elevated personal grooming from a basic necessity to a form of lifestyle expression. Saudi consumers are recognized globally for their significant investment in beauty and care products. This spending pattern reflects deeper societal changes, including increased female workforce participation and social reforms that have expanded women's public visibility, creating sustained demand for professional appearance maintenance. The grooming emphasis extends beyond traditional gender boundaries, with male consumers increasingly investing in hair care routines as part of broader wellness and self-care practices. Hair health has become intrinsically linked to overall wellness perception, particularly among Gen Z consumers who view hair care as essential to physical and mental well-being. The trend has been amplified by remote work adoption and video conferencing culture, where hair appearance directly impacts professional presentation, sustaining demand even during economic uncertainties.

Preference for natural and organic formulations

Consumer preference for natural and organic hair care formulations reflects both global clean beauty trends and deep-rooted cultural affinity for traditional remedies, with consumers preferring cleaner, natural ingredients. Research conducted in northwest Saudi Arabia identified 41 medicinal plants and 11 home remedies commonly used for hair and scalp care, with henna, coconut, and olive oil leading usage patterns. This cultural foundation provides natural ingredient brands with inherent consumer acceptance, especially when modern formulations integrate traditional elements like argan oil, which resonates strongly with consumers seeking natural hair care solutions. The trend has gained momentum through social media education, with platforms like TikTok driving awareness of the benefits and potential risks of ingredients and synthetic chemicals. Saudi Food and Drug Authority's (SFDA) updated restricted substances list has further reinforced consumer scrutiny of product formulations and heightened the demand for transparency in ingredient sourcing [1]Source: Saudi Food and Drug Authority, “LIST OF PROHIBITED SUBSTANCES IN COSMETIC PRODUCTS,” sfda.gov.sa.

Product innovation and customization

The hair care industry is experiencing a technological revolution centered on personalization and advanced delivery systems. The technology-driven customization trend is meeting the rising consumer demand for targeted solutions, particularly among Saudi Gen Z, who increasingly perceive themselves as knowledgeable about ingredient benefits and confident in making informed product choices. Innovation extends beyond diagnostics to formulation breakthroughs, as demonstrated by Kao Corporation's development of gel-like hair oil using stabilized high internal phase emulsion technology, creating products that are gel-like at rest but soften under application. The customization trend reflects broader consumer evolution toward "skinification" of hair care, where scalp health receives equal attention to hair aesthetics, driving demand for targeted treatments addressing specific concerns like dryness, oiliness, and hair loss prevention.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent SFDA registration and compliance timelines | -0.8% | National, affecting imports | Short term (≤ 2 years) |

| Rising concerns over counterfeit products | -0.6% | National, online channels | Medium term (2-4 years) |

| Preference for traditional and herbal remedies | -0.4% | Regional, rural areas | Long term (≥ 4 years) |

| Skepticism toward synthetic chemicals | -0.3% | Urban, educated segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent SFDA registration and compliance timelines

According to the Updated Personal Import Rules 2024 by the Saudi Food and Drug Authority, SASO's 2025 updates require Product Certificates of Conformity and Shipment Certificates of Conformity for all imports. This update eliminates the earlier provision of the Letter of Undertaking, which permitted self-declaration of compliance [2]Source: Saudi Food and Drug Authority, “Updated Personal Import Rules 2024,” sfda.gov.sa. Such regulatory changes create significant barriers for new market entrants and increase compliance costs for existing players, with processing timelines for herbal and health products extending to 155 working days for regular pathways. The regulatory tightening reflects Saudi Arabia's commitment to consumer protection and market quality improvement, but creates operational challenges for international brands seeking rapid market entry. Companies must now invest in comprehensive regulatory expertise and longer lead times for product launches, potentially slowing innovation cycles and increasing market entry costs.

Rising concerns over counterfeit product

Counterfeit product infiltration poses significant market disruption, with Saudi Arabia's Authority for Intellectual Property (SAIP) blocking 3,317 websites and confiscating more than 41 million counterfeit items in its enforcement campaign against intellectual property violations in 2023. These actions align with the country's efforts to protect intellectual property rights and strengthen its knowledge-based economy[3]Source: Saudi Authority for Intellectual Property, “Saudi Arabia: 3,317 Sites Blocked Over Intellectual Property Breaches,” saip.gov.sa. The counterfeit issue extends beyond traditional retail channels into e-commerce platforms, where regulatory fragmentation between SFDA, Ministry of Health, and Customs Authority creates enforcement gaps that allow uncertified products to enter the market. The proliferation of counterfeit products undermines consumer confidence in legitimate brands and creates unfair competition for compliant manufacturers who invest in proper formulation, testing, and regulatory approval processes. This challenge is particularly acute in online channels, where international discount retailers often operate without equivalent enforcement oversight, creating regulatory asymmetry that disadvantages local businesses sourcing SFDA-certified products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Treatments Drive Premium Evolution

Hair treatments segment leads growth projections with a 7.02% CAGR through 2031, significantly outpacing the traditional dominance of shampoos, which maintain 45.62% market share in 2025. This growth differential reflects the market's evolution toward specialized, problem-solving formulations that address specific hair concerns rather than basic cleansing needs. Hair treatments benefit from the "skinification" trend, where consumers increasingly view scalp health as fundamental to overall hair wellness, driving demand for targeted serums, masks, and leave-in treatments that deliver measurable results.

Conditioners and hair styling products represent mature segments with steady but modest growth. The premiumization of this segment aligns with consumer willingness to invest in efficacy-driven products, particularly those backed by clinical claims and ingredient transparency. Hair styling products are gaining traction among younger consumers influenced by professional salon trends and social media education. The segment evolution reflects broader consumer sophistication, where product selection is increasingly driven by specific hair goals rather than generic maintenance routines.

By Category: Premium Gains Despite Mass Dominance

The premium/luxury segment is expected to grow at 7.83% CAGR through 2031, while the mass category holds 71.45% of the market share in 2025. This market division shows value-conscious consumers remaining loyal to accessible brands, while affluent consumers shift toward premium products and specialized retail experiences. The premium segment's growth is driven by increasing disposable incomes among young professionals, social media influence on luxury beauty routines, and wider availability of premium brands through Sephora and specialty retail stores.

The premium segment's growth is further supported by the rise of A-beauty brands that combine traditional Middle Eastern ingredients with modern formulations, creating culturally resonant premium positioning that commands price premiums while delivering authentic regional identity. Mass market players face increasing pressure to innovate within price constraints, leading to the emergence of "masstige" positioning that bridges affordable pricing with premium-inspired formulations and packaging. The category evolution suggests a maturing market where consumers are willing to pay premiums for perceived value, efficacy, and brand prestige, creating sustainable growth opportunities for well-positioned premium players.

By Ingredient Type: Clean Beauty Momentum Accelerates

Natural/organic formulations are expected to grow at a CAGR of 8.06% through 2031, significantly exceeding the growth rate of conventional/synthetic alternatives, despite the conventional/synthetic products holding a 64.78% market share in 2025. This growth stems from the combination of traditional remedies and global clean beauty preferences. Research in northwest Saudi Arabia shows extensive use of natural hair care ingredients, particularly henna, coconut oil, and olive oil, indicating strong cultural acceptance of natural products.

The clean beauty movement gains momentum through social media education and ingredient transparency demands, with consumers preferring natural ingredients in hair care formulations. SFDA's comprehensive restricted substances list has heightened consumer awareness of synthetic chemical risks and increased scrutiny of product formulations. Conventional/synthetic formulations maintain market dominance through established distribution networks, proven efficacy, and competitive pricing, but face increasing pressure to reformulate with cleaner ingredients or risk market share erosion to natural alternatives. The ingredient evolution reflects broader consumer sophistication, where purchasing decisions increasingly incorporate safety, sustainability, and cultural authenticity considerations alongside traditional efficacy and price factors.

By Distribution Channel: Digital Commerce Reshapes Retail

Online retail stores are expected to grow at 8.11% CAGR through 2031, surpassing the growth of hypermarkets/supermarkets, which currently hold a 39.85% market share in 2025. This shift in retail channels indicates changing consumer preferences, as Saudi consumers increasingly adopt e-commerce platforms for their shopping needs. The growth of online retail, initially accelerated by the pandemic, continues due to the convenience, product selection, and competitive prices offered by digital platforms compared to traditional retail stores.

Pharmacy and drug stores maintain their competitive position through professional consultation services and immediate product availability. Community pharmacists in Saudi Arabia provide beauty product counseling to customers. Specialty stores compete with online retailers and mass retail channels by offering exclusive brands, professional services, and enhanced shopping experiences. The retail landscape is evolving with the integration of omnichannel capabilities, which are essential for business sustainability. Consumers expect seamless connections between online research, social media product discovery, and multiple fulfillment options, including same-day delivery and buy-online-pickup-in-store services.

Geography Analysis

Saudi Arabia represents the largest and most dynamic hair care market in the Gulf Cooperation Council, driven by unique demographic advantages and economic transformation initiatives that distinguish it from regional peers. The Kingdom’s youthful demographic creates a substantial consumer base characterized by rising disposable incomes and heightened beauty consciousness. The market benefits from high urbanization rates, concentrating purchasing power in major cities where modern retail infrastructure and digital commerce capabilities support premium product distribution and brand-building activities.

Cultural and regulatory factors create distinctive market characteristics that differentiate Saudi Arabia from other Middle Eastern markets. Social reforms and increased female workforce participation have expanded women's public presence, directly translating into higher demand for professional grooming products and premium beauty categories. Moreover, digital penetration reaches exceptional levels, enabling rapid trend propagation and direct-to-consumer brand building that bypasses traditional retail gatekeepers.

The Saudi market demonstrates unique consumption patterns that reflect both cultural heritage and modern aspirations, creating opportunities for brands that successfully navigate local preferences while delivering global quality standards. Traditional ingredient preferences, such as the widespread use of henna, coconut oil, and olive oil for hair care, offer natural brands inherent cultural acceptance. These preferences also create differentiation opportunities for international players that incorporate regional ingredients.

Competitive Landscape

The Saudi Arabia hair care market exhibits moderate consolidation, reflecting established multinational dominance tempered by emerging local competition and digital-native disruptors. Market leaders leverage extensive distribution networks, proven brand equity, and substantial marketing investments to maintain their position. Competitive dynamics are reshaping through technology adoption and regulatory enforcement, creating both opportunities and challenges for market participants.

Emerging white-space opportunities include scalp care specialization, male grooming expansion, and personalized formulations that address specific hair concerns prevalent in the regional population. The rise of beauty brands and local manufacturing initiatives, supported by Vision 2030 industrialization goals and PIF investments, suggests a structural shift toward domestic value creation that may challenge traditional import-dependent business models.

Technology integration, including advancements such as personalized diagnostics and advanced delivery systems, is becoming increasingly important for maintaining competitive differentiation. Personalized diagnostics enable tailored solutions by leveraging consumer-specific data, improving treatment outcomes and efficiency. Advanced delivery systems enhance the precision and effectiveness of therapeutic interventions, ensuring optimal delivery. These innovations are crucial as consumer sophistication rises and regulatory compliance requirements become more stringent, driving the need for continuous technological advancements.

Saudi Arabia Hair Care Industry Leaders

Johnson & Johnson

Dabur International

L’Oréal SA

Unilever

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: UKLASH, an award-winning beauty company, launched its first comprehensive hair care line, UKHAIR, in the Middle Eastern market. The British brand, recognized for its eyelash serum, introduced a seven-product collection targeting hair growth and scalp health. The product range includes a hair growth serum, conditioner, shampoo, repair mask, and styling tools.

- September 2024: FSN E-Commerce Ventures Ltd., the parent company of fashion e-retailer Nykaa, has incorporated a subsidiary in Saudi Arabia named Nysaa Trading LLC. The subsidiary, operating under the brand name "Nysaa KSA," will focus on online and offline sales of toiletries, cosmetics, perfumes, beauty products, soaps, and hair care items.

- July 2024: Henkel opened a beauty care production facility in Riyadh. The facility manufactures Pert brand products, including conditioners, shampoos, and other personal care items, to serve the Middle East market.

Saudi Arabia Hair Care Market Report Scope

Hair care is an overall term for hygiene and cosmetology involving the hair which grows from the human scalp and, to a lesser extent, facial and other body hair. Hair care products include Hair conditioner, Shampoo, Hair spray, Hair oil, Hair wax, Beard oil etc. The Saudi Arabian hair care market is segmented by product type into shampoo, conditioner, hair oil, and other product types. The market is segmented by distribution channel into hypermarkets/supermarkets, specialty stores, online stores, convenience stores, pharmacies/drug stores, and other distribution channels. The report offers market size and forecasts for the hair care market in value (USD million) for all the above segments.

By Product Type

| Shampoos |

| Conditioners |

| Hair Treatments |

| Hair Colorants |

| Hair Styling Products |

| Others |

By Category

| Mass |

| Premium/Luxury |

By Ingredient Type

| Conventional/Synthetic |

| Natural/Organic |

By Distribution Channel

| Hypermarkets/Supermarkets |

| Pharmacy and Drug Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Shampoos |

| Conditioners | |

| Hair Treatments | |

| Hair Colorants | |

| Hair Styling Products | |

| Others | |

| By Category | Mass |

| Premium/Luxury | |

| By Ingredient Type | Conventional/Synthetic |

| Natural/Organic | |

| By Distribution Channel | Hypermarkets/Supermarkets |

| Pharmacy and Drug Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large will Saudi Arabia’s hair care market become by 2031?

The Saudi Arabia hair care market size is projected to reach USD 2.43 billion by 2031, growing at a 6.45% CAGR.

Which product type is expanding the quickest?

Hair Treatments lead growth with a forecast 7.02% CAGR thanks to “skinification” trends that spotlight scalp health.

What share do premium brands hold today?

Premium/Luxury lines account for 28.55% of 2025 value and are outpacing mass with an 7.83% CAGR outlook.

How important is e-commerce to category growth?

Online Retail Stores are the fastest-growing channel, expected to post an 8.11% CAGR as Saudis are increasingly shopping online regularly.

Page last updated on: