Saudi Arabia Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

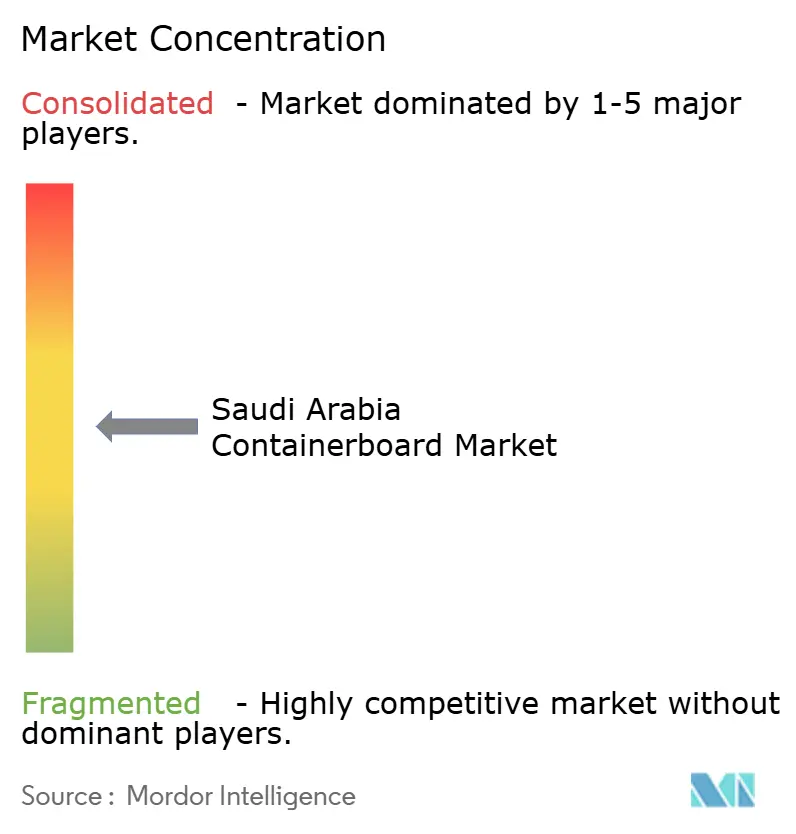

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Containerboard Market Analysis by Mordor Intelligence

The Saudi Arabia containerboard market size was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.21 billion in 2026 to reach USD 1.45 billion by 2031, at a CAGR of 3.69% during the forecast period (2026-2031). The Saudi Arabia containerboard market is being supported by steady demand from food processing, e-commerce logistics, and a broader manufacturing localization push under Vision 2030. Demand is also becoming more quality sensitive because more Saudi-made goods now move through longer domestic distribution chains and stricter export packaging channels. Import dependence still matters, which means domestic capacity additions can influence not only supply security but also pricing stability for corrugators. The March 2026 disruption in Gulf shipping routes showed that local mills can capture redirected orders quickly when imported board becomes harder to secure. Competition therefore remains shaped by a concentrated primary production base and a fragmented converter layer, where reliable board access matters as much as conversion capability.

Key Report Takeaways

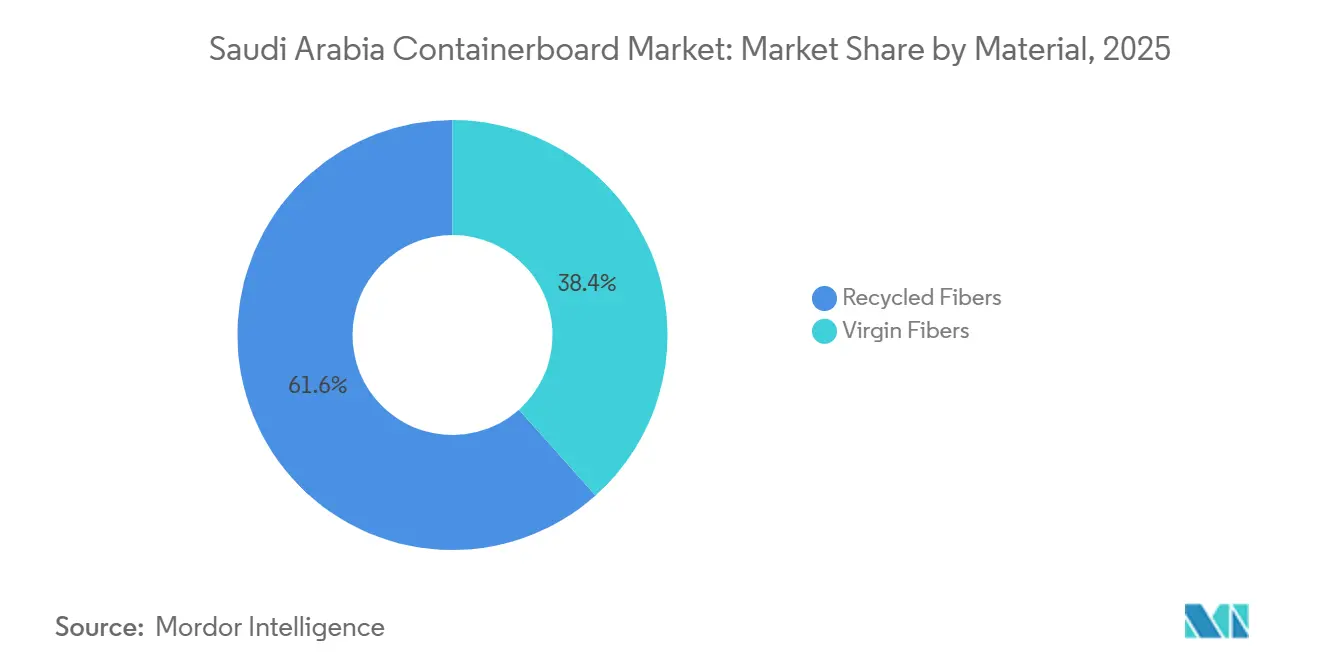

- By material, recycled fibers captured 61.59% of the Saudi Arabia containerboard market share in 2025.

- By product type, the Saudi Arabia containerboard market size for the kraftliners segment is forecast to advance at a 4.16% CAGR through 2031.

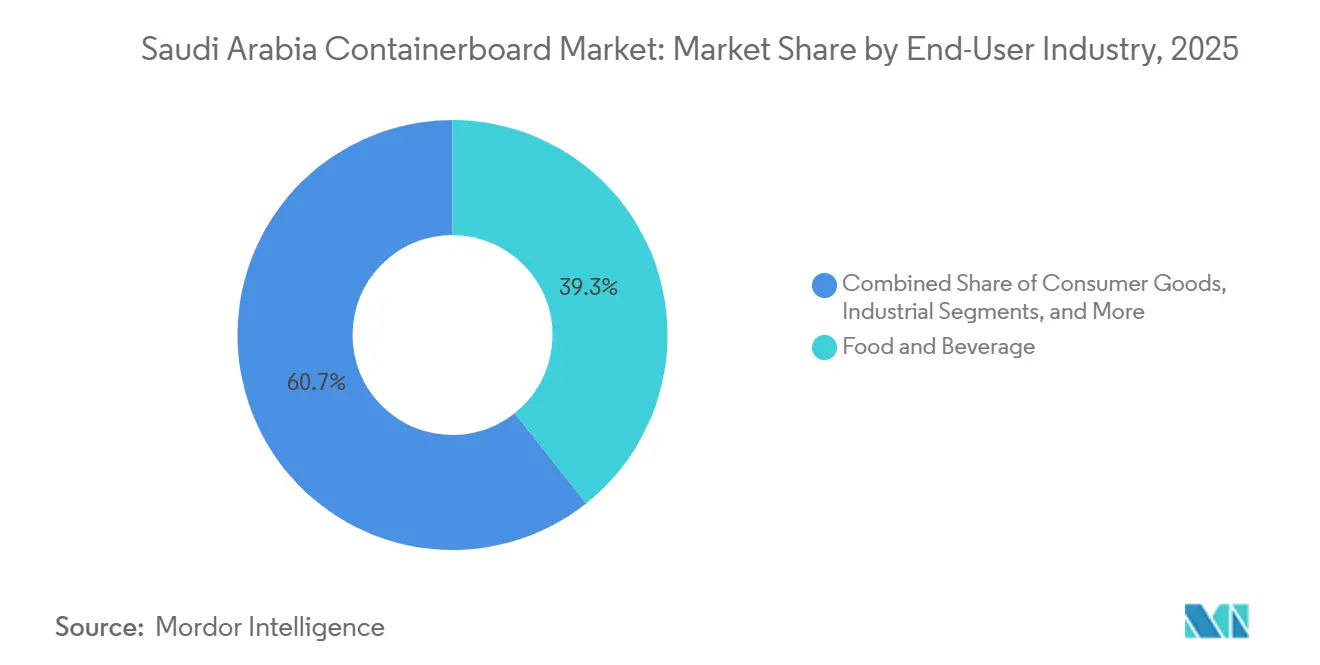

- By end-user industry, food and beverage captured 39.32% of the Saudi Arabia containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Processing Localization And Packaged Food Throughput Growth | +1.0% | National, with peak demand concentration in Riyadh and Jeddah food industrial clusters | Short term (≤ 2 years) |

| E-commerce Fulfillment And Omnichannel Transit Packaging Demand | +0.8% | National, with early gains in Riyadh and Jeddah last-mile delivery hubs | Short term (≤ 2 years) |

| Vision 2030 Manufacturing Localization And Export Packaging Needs | +0.7% | National, with strongest activity in MODON industrial cities across Riyadh, Dammam, and Yanbu | Medium term (2-4 years) |

| Sustainability Shift Toward Recycled Containerboard | +0.5% | National, aligned with MWAN waste governance framework and EPR provisions | Medium term (2-4 years) |

| Hajj And Umrah Peak-Season Beverage And Food Shipping Spikes | +0.3% | Makkah and Madinah regions, with logistics spillover to Jeddah and Riyadh distribution networks | Short term (≤ 2 years) |

| Date And Fresh-Produce Export Upgrading Toward Moisture-Resistant Corrugated Formats | +0.2% | Al-Qassim, Madinah, and Al-Ahsa date-producing provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food Processing Localization And Packaged Food Throughput Growth

Food processing localization remains the clearest demand engine for the Saudi Arabia containerboard market, as it combines policy support with steady packaging volumes. The Kingdom's food processing base included more than 1,300 registered companies in 2025, which sustained broad demand for corrugated transit cases and secondary packaging across domestic and export channels. The sector also had significant capital depth, with investment estimated at USD 60 billion, and food processing sales accounting for more than 75% of total sector revenues. Vision 2030 and the National Industrial Development and Logistics Program were designed to reduce food import dependence and expand domestic production capacity, thereby broadening the customer base for corrugated board and boxes.[1]Saudi Vision 2030, “2021-2025 National Industrial Development and Logistics Program Delivery Plan,” Saudi Vision 2030, vision2030.gov.sa This shift also underscores the need for double-wall and heavy-duty formats, as more locally processed foods now move across the Kingdom before reaching retail shelves or export pallets, keeping baseline box demand firm in the Saudi Arabia containerboard market.

E-commerce Fulfillment And Omnichannel Transit Packaging Demand

E-commerce fulfillment is lifting packaging intensity in the Saudi Arabia containerboard market because more orders are moving as individual parcels rather than as bulk wholesale shipments. This changes box demand in favor of right-sized corrugated packs, shorter production runs, and greater use of die-cut formats that better align with last-mile delivery economics than older bulk-transport cases. The operating effect is important because higher shipment fragmentation increases reorder frequency for corrugators, even when a single stock-keeping unit does not experience a large jump in unit sales. Seasonal retail peaks also intensify this pattern, since converters serving major urban hubs need faster turnaround and more flexible board availability during compressed ordering windows. That favors converters with stronger printing, inventory planning, and supply relationships, which means e-commerce is supporting volume growth while changing competitive behavior in the Saudi Arabia containerboard market.

Vision 2030 Manufacturing Localization And Export Packaging Needs

Vision 2030 is expanding the addressable manufacturing base for the Saudi Arabia containerboard market by pulling more production activity into the Kingdom. Saudi Arabia's local content score rose to around 50% in 2025 from around 33% in 2020, suggesting a broader domestic footprint for industries that require packaging for inbound materials and outbound finished goods. This matters because localized manufacturing increases packaging demand at all stages of the production cycle, not just at the final retail shipment stage. It also raises the share of demand tied to export-compliant corrugated formats, where better burst strength, print quality, and dimensional stability carry more weight than in purely domestic commodity applications. As a result, the Saudi Arabia containerboard market is seeing not just more volume from localization, but a gradual pull toward higher-spec testliner and kraft-faced corrugated suited to regulated and export-oriented supply chains.

Sustainability Shift Toward Recycled Containerboard

The sustainability shift toward recycled board is reinforcing existing production economics in the Saudi Arabia containerboard market rather than changing them from scratch. MEPCO's recycling platform, through its subsidiaries, handled around 500,000 tons of recovered paper annually as of 2025, helping secure feedstock for testliner and fluting production and confirming the scale of the domestic circular model already in place.[2]MEPCO Group, “Annual Report 2024,” MEPCO Group, mep.co Saudi Arabia is also building a stronger policy framework for waste management and producer responsibility, which supports the adoption of recycled-content packaging and the development of better formal collection systems over time. New investments such as Al-Jawdah Paper's recycled containerboard mill in Al-Qassim show that smaller domestic players are also committing capital to recycled board and organized OCC sourcing networks. Certification is adding another layer to this trend, since mills with FSC Chain of Custody and environmental management credentials are better placed to serve multinational accounts that want traceable and lower-impact packaging in the Saudi Arabia containerboard market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Fiber Quality And Supply Constraints | -0.9% | National, with concentration around Jeddah, Dammam, and Yanbu mill clusters | Short term (≤ 2 years) |

| Water And Energy Cost Pressure On Paper Mills | -0.6% | National, with highest exposure at energy-intensive Jeddah and Yanbu mill facilities | Medium term (2-4 years) |

| Grade-Mix Mismatch Between Domestic Recycled Output And Premium Virgin Kraft Requirements | -0.5% | National, export-oriented manufacturers across all industrial regions | Medium term (2-4 years) |

| Circular-Regulation Transition Risk For Packaging Compliance And Waste Traceability | -0.3% | National, with early compliance burden concentrated in Riyadh and Jeddah industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Fiber Quality And Supply Constraints

Recovered fiber quality remains the main structural restraint on the Saudi Arabia containerboard market, as most domestic mills are built around recycled inputs. That model works at a volume scale, but it becomes more vulnerable when several mills compete for the same OCC pool or when imported recovered paper becomes harder to source on time. The March-April 2026 disruption in Gulf shipping routes showed how quickly this pressure can feed into pricing, with the PIX Testliner GCC index rising 4.38% in one month as converters shifted orders toward local supply. Quality also matters because contamination and inconsistent moisture levels in locally collected OCC can make it harder to produce premium recycled grades with stable yields, especially for stronger liners and better print surfaces. With Al-Jawdah Paper, Red Sea Paper PM2, and MEPCO PM5 all increasing pressure on fiber sourcing across 2025-2027, raw material competition is likely to remain a margin constraint even as demand stays healthy in the Saudi Arabia containerboard market

Water And Energy Cost Pressure On Paper Mills

Water and energy input pressure is becoming more important for the Saudi Arabia containerboard market as subsidy reform and efficiency requirements mature. Large mill operators are already responding through internal efficiency programs rather than assuming past cost advantages will continue unchanged. MEPCO reported a 29% internal water recycling rate in 2024, which shows that resource management has become a core operating issue for local producers rather than a secondary sustainability measure. Mills with weaker recycling systems or less integrated energy management are more exposed if fuel and utility costs rise faster than selling prices, especially in competitive recycled grades. This does not change the long-run demand base, but it can limit margin expansion, slow smaller operators' investment plans, and widen the cost gap between leading and subscale suppliers in the Saudi Arabia containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead While Virgin Grades Gain Premium Demand

Recycled fibers held 61.59% of the Saudi Arabia containerboard market share in 2025, while virgin fibers are projected to expand at a 4.08% CAGR through 2031. That lead reflected the structure of local production, where domestic mills are centered on recovered-fiber technology and can supply commodity testliner and fluting at competitive cost. The segment's position is also reinforced by Saudi Arabia's lack of domestic wood pulp production, which keeps virgin containerboard linked to imported pulp, external freight, and global fiber price cycles. This cost and sourcing structure means recycled grades remain the natural fit for broad food, consumer goods, and industrial transit packaging across the Saudi Arabia containerboard market. It also explains why recycled board continues to dominate even though demand is becoming more quality-conscious in parts of the value chain.

Virgin fibers are still the fastest-growing material class because they serve the part of the demand that recycled grades cannot consistently satisfy. Export-oriented food shipments, pharmaceutical packaging, electronics applications, and multinational food processor requirements are all driving demand for kraft-faced corrugated with stronger moisture resistance and more consistent surface quality. MEPCO's PM5 project will add 450,000 TPA of recycled containerboard capacity in the 70-140 g/m² range, strengthening the recycled segment's volume share while also improving efficiency and grade capability.[3]MEPCO, “Investment Amounting to SAR 1.78 Billion Saudi Riyals in 5th Production Line to Boost Cardboard Paper Production Capacity Annually by 450 Thousand Tons,” MEPCO, mep.co Even so, the faster growth of virgin grades shows that some customers are buying performance rather than price alone, especially where packaging failure incurs higher compliance or export costs. This leaves the Saudi Arabia containerboard industry split between a scale-driven recycled base and a smaller premium kraft niche that is growing from a higher-value part of demand.

By Product Type: Testliners Hold The Base While Kraftliners Move Upmarket

Testliners accounted for 41.88% share of the Saudi Arabia containerboard market size in 2025, while kraftliners are projected to grow at a 4.16% CAGR through 2031. Testliners remain the volume backbone of the Saudi Arabia containerboard market because they align with the country's recycled-fiber production base and serve a wide range of food, consumer goods, and industrial applications at a workable cost. Domestic mills have long been better aligned with this grade family, which is why testliner keeps the largest share even as buyer expectations rise in selected end uses. Kraftliner is growing faster because export-grade packaging, stronger compression performance, and better moisture resistance are becoming more important for a part of Saudi demand. This shift is especially relevant for converters that need to meet stricter retailer or shipping requirements without taking on quality risk with recycled commodity grades.

The product mix is therefore moving in two directions at once rather than through a simple substitution story. Testliners will likely remain the broadest-volume grade because domestic supply, converter familiarity, and cost discipline still favor recycled liners for everyday transport applications. At the same time, domestic producers are moving toward white-top and more functional recycled grades, which narrows the quality gap with imported material and creates room for value-added product differentiation inside the Saudi Arabia containerboard market. Fluting continues to play a complementary role in volume because lightweight, high-stiffness board structures are useful in fast-turn delivery applications where dimensional efficiency matters. The result is a product portfolio that still depends on commodity grades for scale, while slowly building more local capability in performance-led formats

By End-User Industry: Food And Beverage Keeps Scale While Consumer Goods Gains Speed

Food and beverage accounted for 39.32% of the Saudi Arabia containerboard market in 2025, while consumer goods are projected to record the fastest CAGR at 4.24% through 2031. Food and beverage held the lead because its packaging needs are structural, not occasional, and span processing plants, distribution centers, retail channels, and export logistics.[4]U.S. Department of Agriculture Foreign Agricultural Service, “Retail Foods Annual, Saudi Arabia,” USDA GAIN, apps.fas.usda.gov The presence of more than 1,300 registered food companies kept corrugated demand broad-based across the Kingdom in 2025. Ordering patterns are also lifted by recurring seasonal cycles, and Fastmarkets reported stronger stock building by corrugators ahead of Hajj in 2026, which shows how pilgrimage-linked food and beverage logistics can compress purchases into shorter windows. This steady and recurring demand makes food and beverage the anchor end use for the Saudi Arabia containerboard market, even when growth is faster elsewhere.

Consumer goods are growing faster because more products now move through direct-to-consumer, organized retail, and higher-service distribution models that require individualized secondary packaging. Vision 2030 is widening that addressable demand by encouraging more local manufacturing and brand presence, which supports additional packaging needs across personal care, electronics, and household goods. Industrial users also remain important because building materials, machinery, chemicals, and project supply chains require stronger corrugated formats for multi-stage transport and storage. That combination gives the Saudi Arabia containerboard industry both a stable food-led demand base and a faster consumer goods lane that is changing format requirements over time. It also means that future growth in the Saudi Arabia containerboard market will depend on both consumption-linked packaging and manufacturing-linked logistics demand rather than on one end-use group alone

Geography Analysis

Saudi Arabia held 35.7% of the Middle East and Africa total in 2025, and domestic market value stood at USD 1.18 billion. The Saudi Arabia containerboard market size is projected to advance at a 3.69% CAGR through 2031, which is slightly ahead of the wider regional pace of 3.31%. That difference implies a gradual gain in regional weight as local capacity, manufacturing localization, and converter demand expand inside the Kingdom. The UAE remains important as a logistics platform and Turkey remains relevant as a source of virgin-fiber supply into the region, but Saudi Arabia combines scale of demand with rising local production capability. The partial closure of the Strait of Hormuz in March 2026 strengthened that position because converters that struggled to secure imported RCCM redirected orders toward Saudi mills, which highlighted the value of domestic supply in a disrupted regional trade setting.

The Saudi Arabia containerboard market is concentrated in the Riyadh, Jeddah, and Dammam corridors because industrial density and logistics throughput are highest in these areas. Riyadh is the strongest internal demand hub because it combines food manufacturing, consumer goods distribution, and a large localized industrial base. Jeddah and the wider Western corridor carry added importance because port activity, converter capacity, and pilgrimage-related food and beverage logistics sit in the same geography. Dammam remains strategically relevant because Eastern Province industrial activity and import handling support both board movement and downstream conversion demand. Demand therefore follows industrial cluster density and logistics intensity more closely than population distribution alone in the Saudi Arabia containerboard market.

Saudi Arabia's 35.7% share of the regional total is also supported by a multi-hub supply footprint rather than one production center. MEPCO's Jeddah base, WARAQ's Dammam presence, and Red Sea Paper's Yanbu location give the Saudi Arabia containerboard market broader port access and better supply resilience than many neighboring markets. Al-Qassim is becoming more relevant as a secondary node because it combines recycled containerboard investment with agricultural packing demand and organized OCC collection networks. Once PM5 enters commercial production in 2027, the Kingdom will be in a stronger position to serve domestic converters and nearby export markets from this spread of production locations.

Competitive Landscape

The Saudi Arabia containerboard market operates through a two-tier structure, with moderately concentrated primary production and a fragmented converting layer. MEPCO and Arab Paper Manufacturing Co. (WARAQ) supplied most domestically manufactured containerboard rolls in 2025, while more than 100 corrugators were active downstream across Riyadh, Jeddah, and Dammam. This creates a market where board access, fiber sourcing, and logistics reliability matter more at the mill level than the simple number of competitors. At the converter level, fragmentation remains high enough to keep pricing and service competition active across regions and applications. The Saudi Arabia containerboard market therefore looks concentrated upstream and dispersed downstream, which is why integration moves carry outsized strategic value.

UCIC stood out in 2025 with a 37-40% share of Saudi Arabia's corrugated carton market, supported by 5 facilities across Jeddah and Riyadh and a model built around scale economies and digital printing capability. That position shows how a well-covered converter can win business not only on price, but also on service speed, print flexibility, and national reach. On the supply side, MEPCO's PM5 remains the single most important strategic expansion because the Voith-supplied 450,000 TPA recycled containerboard line is expected to double the company's annual capacity from 425,000 to 875,000 tons when it starts up in Q4 2027. MEPCO has also indicated that PM5 will support a downstream move into corrugated box manufacturing, which would bring an upstream producer directly into the converter space and alter bargaining dynamics inside the Saudi Arabia containerboard market. That strategy mirrors the advantage already demonstrated by integrated and scale-backed converters, where reliable board supply can be as decisive as converting capacity itself.

Import dependence still leaves room for new entrants and specialized grades because Saudi Arabia imported around 30% of its containerboard needs in 2025. The clearest white spaces remain moisture-resistant fluting, coated white-top testliner, and higher-spec food and pharmaceutical corrugated formats that still rely heavily on imported supply. Certification is also becoming more important, since FSC Chain of Custody and ISO 14001:2015 credentials improve access to multinational food and consumer goods accounts that run tighter supply-chain audits. Smaller converters such as Gulf Carton Factory Company, Theeb Pack, and CADIS Packaging Solutions still serve regional and application-specific needs, but the Saudi Arabia containerboard market is likely to reward scale, supply security, and certification more than basic box-making capacity as domestic board supply expands.

Saudi Arabia Containerboard Industry Leaders

Middle East Paper Company

United Carton Industries Company

National Paper Products Company Ltd.

Gulf Carton Factory Company

Etihad Gate Industrial Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Saudi Arabia-based corrugators reported strong stock-building ahead of Hajj, estimated late May 2026, with Fastmarkets documenting that preparations for the pilgrimage season drove one of the strongest April corrugated demand readings in the Kingdom since 2024, with smaller corrugators facing imported RCCM shortages shifting business to larger domestic participants, GCC containerboard producers anticipated continued price firming through May on Hajj-driven demand and Middle East conflict supply disruptions.

- April 2026: The partial closure of the Strait of Hormuz following military action caused the PIX Testliner GCC index to reach USD 482.44/tonne, up 4.38% from USD 462.20 on March 3, and the PIX Fluting GCC index to reach USD 457.33/tonne, Saudi Arabia-based corrugators diverted import orders to local mills, generating a significant demand surge that directly benefited domestic containerboard producers.

- January 2026: Red Sea Paper Manufacturing Company formally began trial production on its PM2 in Yanbu, adding approximately 178,000 TPA of white-top testliner, gypsum board, and corrugating medium in the 75-150 g/m² range, the first domestic production of functional coated containerboard at scale in Saudi Arabia, directly challenging the premium import supply chain for retail-shelf corrugated.

- January 2026: Saudi Paper Manufacturing Company signed a Sharia-compliant credit facility agreement with Kuwait Finance House, Bahrain, for USD 40 million, encompassing 12-month renewable working capital facilities and 48-month medium-term financing with a 6-month grace period, structured to support raw material procurement, operational liquidity, and medium-term debt restructuring.

Saudi Arabia Containerboard Market Report Scope

The Saudi Arabia Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Saudi Arabia Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Saudi Arabia containerboard market in 2026?

The Saudi Arabia containerboard market stands at USD 1.21 billion in 2026 and is projected to reach USD 1.45 billion by 2031 at a 3.69% CAGR.

Which material type leads demand in Saudi Arabia containerboard?

Recycled fibers lead demand with 61.59% share in 2025 because domestic mills are primarily built around recovered-fiber technology and commodity board supply.

Why are virgin fibers growing faster than recycled fibers in Saudi Arabia?

Virgin fibers are projected to grow at 4.08% CAGR through 2031 because export packaging, pharmaceuticals, electronics, and premium food applications need stronger and more consistent kraft performance.

Which product category is the largest and which is growing fastest?

Testliners held the largest share at 41.88% in 2025, while kraftliners are projected to post the fastest growth at 4.16% through 2031.

Which end-user group drives the strongest box demand in the Kingdom?

Food and beverage is the largest end-user with 39.32% share in 2025, supported by more than 1,300 registered food companies and steady domestic distribution needs.

How is Vision 2030 affecting demand for containerboard in Saudi Arabia?

Vision 2030 is widening the local manufacturing base, lifting local content, and increasing demand for packaging used in inbound materials, domestic distribution, and export-ready finished goods.

Which companies matter most in the competitive landscape?

MEPCO and WARAQ matter most in primary production, while UCIC stands out downstream with a 37-40% share of Saudi Arabia's corrugated carton market in 2025.

Page last updated on: