Bahrain Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

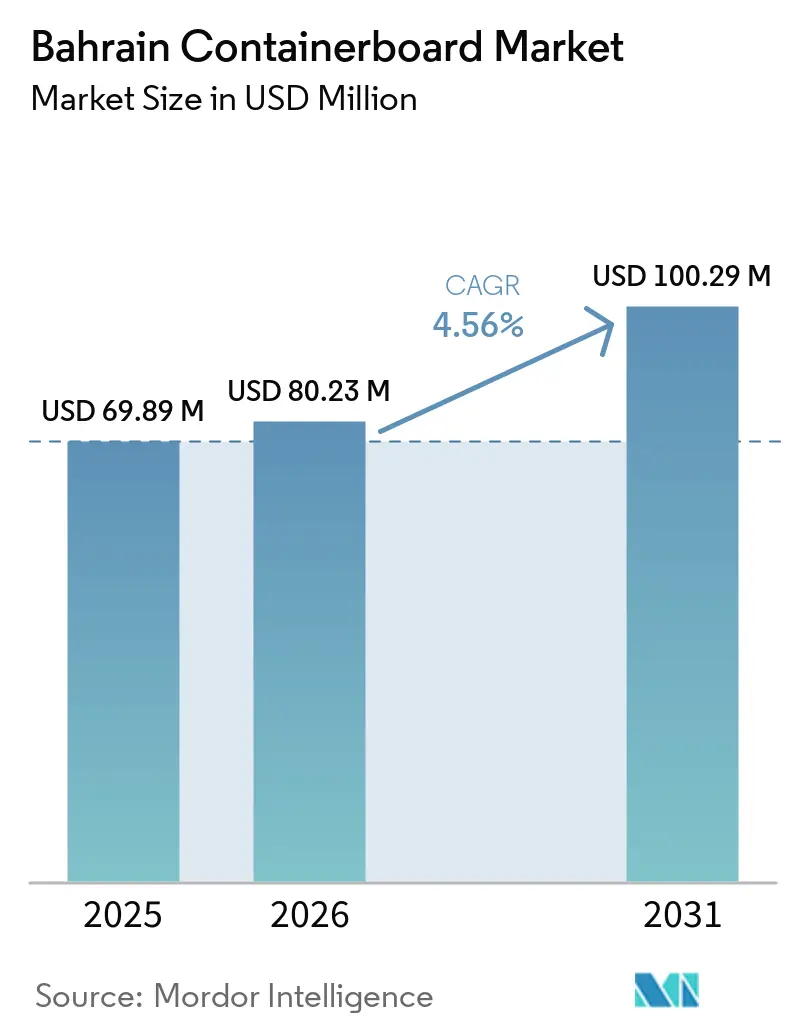

| Base Year Market Size (2025) | USD 69.89 Million |

| Market Size (2026) | USD 80.23 Million |

| Market Size (2031) | USD 100.29 Million |

| Growth Rate (2026 - 2031) | 4.56% CAGR |

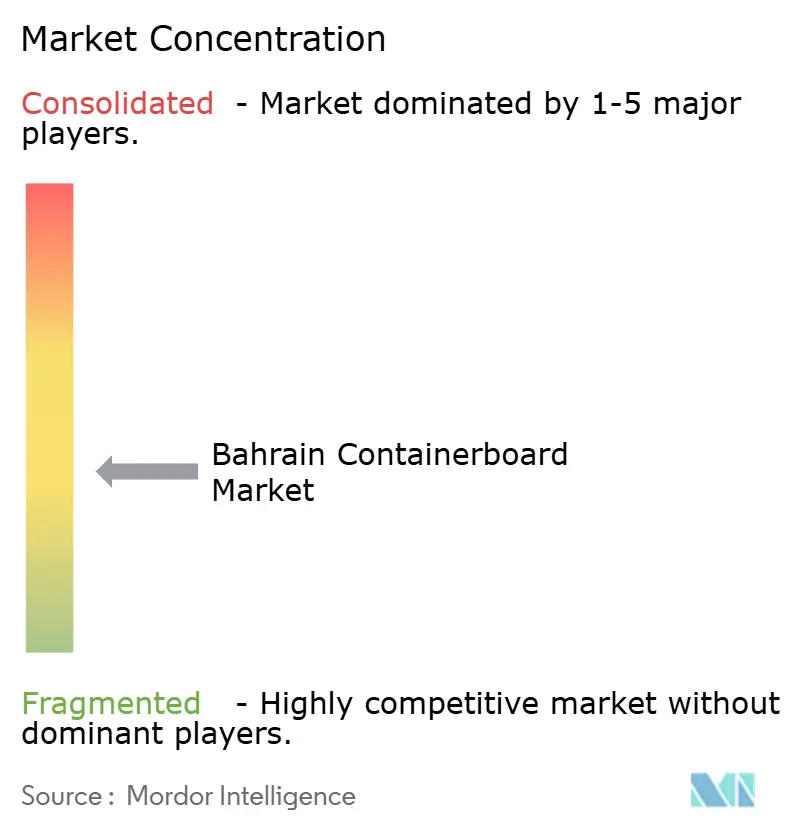

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain Containerboard Market Analysis by Mordor Intelligence

The Bahrain Containerboard Market size is projected to expand from USD 69.89 million in 2025 and USD 80.23 million in 2026 to USD 100.29 million by 2031, registering a CAGR of 4.56% between 2026 to 2031.

The Bahrain containerboard market reflects the country’s role as both a domestic converting base and a transit point for containerized goods moving across the northern Arabian Gulf. Recycled fibers shaped the structure of the Bahrain containerboard market in 2025 because they remained more cost-competitive than imported virgin kraftliner and aligned with stronger recovered paper collection systems across GCC markets. That advantage also left converters more exposed to OCC price swings, which tightened margins in a market where local players had limited room to pass on cost increases. Demand remained anchored by food and beverage packaging, while faster changes in e-commerce fulfillment and industrial packaging requirements started to alter grade mix and end-use specifications across the Bahrain containerboard market. The outlook for the Bahrain containerboard market remains supported by new regional recycled containerboard capacity and tighter plastic regulation, but the clearest gains are likely to favor converters that broaden sourcing options and reduce dependence on a single import channel.

Key Report Takeaways

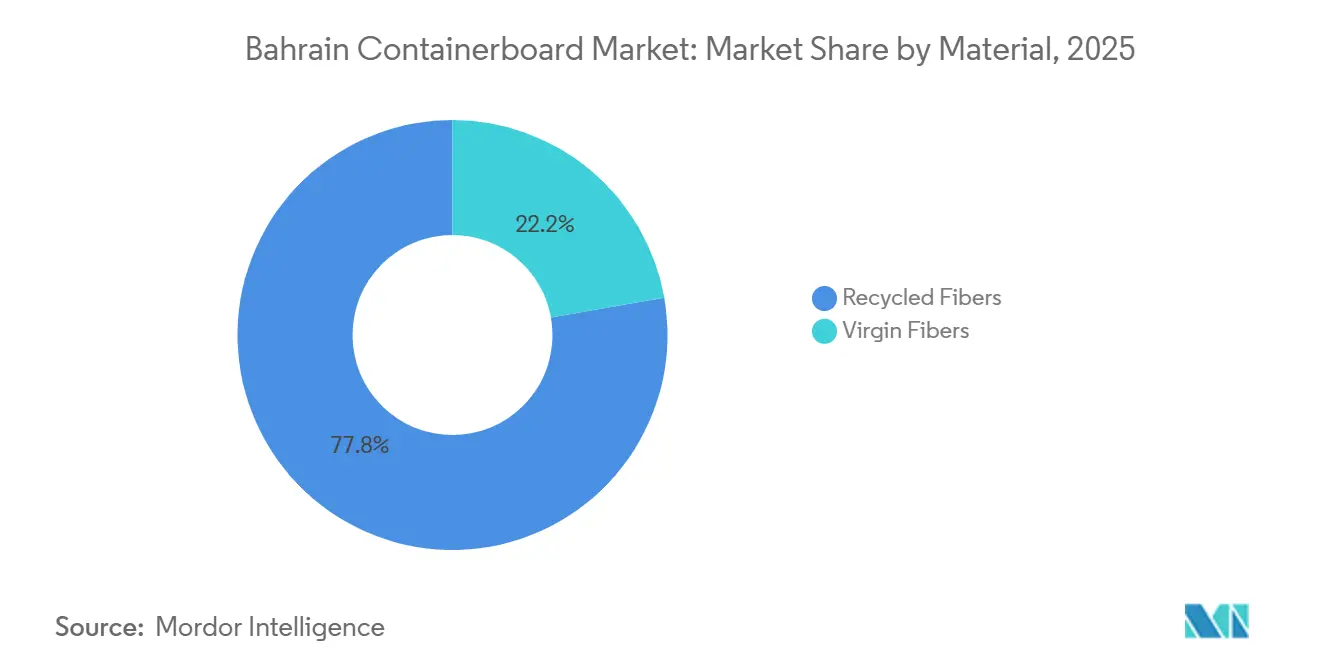

- By material, Recycled Fibers held 77.78% of the Bahrain containerboard market in 2025, while the same segment is also projected to record the fastest growth at a 3.41% CAGR through 2031.

- By product type, kraftliners accounted for 45.61% share in 2025, while flutings are forecast to expand at a 3.17% CAGR through 2031.

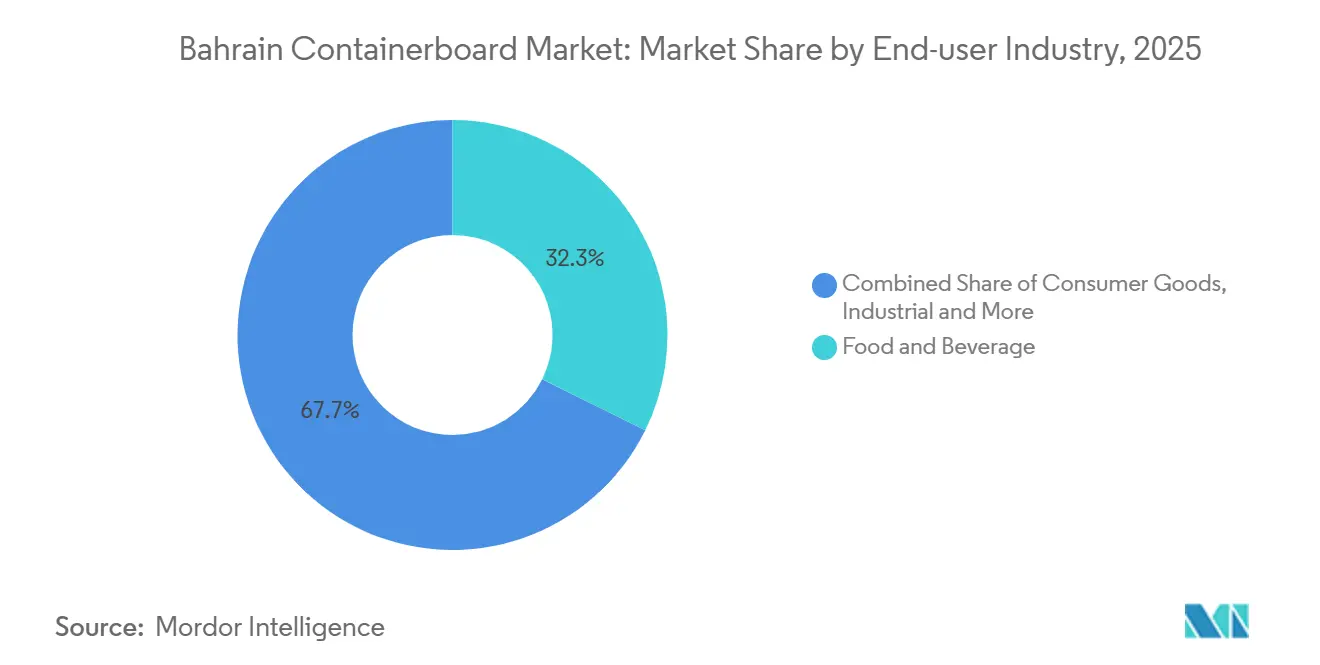

- By end-user industry, food and beverage retained the largest share at 32.31% in 2025, while industrial is projected to record the highest CAGR at 2.87% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bahrain Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Fulfillment And Parcel Box Demand | +1.5% | Bahrain-wide, concentrated in Manama metropolitan zone and Khalifa Bin Salman Port logistics corridor | Short term (≤ 2 years) |

| Shift From Single-Use Plastic Packaging Toward Fiber-Based Formats | +1.1% | Bahrain-wide, amplified by GCC-harmonized regulatory convergence | Medium term (2-4 years) |

| Food And Beverage Packaging Demand Expansion | +0.9% | Bahrain domestic manufacturing base and re-export routes to Saudi Arabia and Kuwait | Medium term (2-4 years) |

| Regional Recycled Containerboard Capacity Additions | +0.6% | GCC-wide, with direct supply-chain benefits for Bahrain-based importers | Medium term (2-4 years) |

| Bahrain Re-Export And Transshipment Packaging Intensity | +0.4% | Khalifa Bin Salman Port and King Fahad Causeway overland corridor | Long term (≥ 4 years) |

| Premium Food-Safe And Shelf-Ready Packaging Requirements | +0.3% | Bahrain food manufacturing exporters and GCC retail-channel converters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment And Parcel Box Demand

Bahrain’s digital commerce penetration reached 15-20% of total retail sales in 2025, which kept parcel-box demand active across short-run and high-frequency fulfillment cycles. This demand pattern matters because individual online orders consume more corrugated material than traditional shelf-replenishment shipments moving in palletized form. Corrugators therefore faced tighter production scheduling, narrower size tolerances, and more frequent substrate changeovers as order density increased across fulfillment stations. Quick-commerce operators in Manama also started testing right-sized packaging automation, which reduced void fill but increased annual board throughput per fulfillment cell. That shift supported greater use of lower-basis-weight corrugating medium rather than simply lifting demand evenly across all grades. It also helps explain why flutings are set to outpace the broader Bahrain containerboard market with a 3.17% CAGR through 2031.

Shift From Single-Use Plastic Packaging Toward Fiber-Based Formats

Bahrain has tightened its stance on single-use plastic packaging in stages since 2019, and that path became more important in February 2026 when Ministerial Decision (7) of 2026 banned the manufacture, import, and use of plastic bags under 57 microns.[1]Bahrain National News Agency, “Industry Minister: Ministerial Decision (7) Of 2026 Prohibits Single-Use Plastic Bags Less Than 57 Microns To Promote Sustainability,” Bahrain National News Agency, bna.bh Enforcement is being carried out through port controls and field inspections by the Ministry of Industry and Commerce, supported by the Supreme Council for Environment. The effect reaches beyond domestic retail because goods moving through Bahrain for re-export increasingly have to meet destination-market packaging expectations that favor fiber formats over thin plastic. That gives converters a reason to invest earlier in food-contact-certified fiber grades and stronger compliance processes. Players that stay with lower-grade recycled inputs alone are less likely to benefit from this shift in packaging specifications. The result is a durable demand tailwind for the Bahrain containerboard market rather than a short-lived substitution trend.

Food And Beverage Packaging Demand Expansion

Bahrain’s food and beverage processing base continues to support a stable flow of demand for single-wall corrugated transit cases used in biscuit, dairy, and confectionery shipments across GCC markets. Weekly distribution schedules into all 6 GCC countries keep order volumes recurring even during softer domestic economic periods. A second layer of demand is forming through halal-certified ready meals and snacks, where global brands have been using Bahrain’s industrial platform for Gulf operations. Packaging supplied into these channels must also meet food-contact performance requirements on moisture resistance, grease resistance, and migration control. That standard limits the use of lower-quality recycled inputs in some applications and preserves a clear role for virgin fiber grades where performance matters most. This combination of recurring shipment demand and stricter specification needs helps explain why food and beverage held the largest end-user share at 32.31% in 2025.

Regional Recycled Containerboard Capacity Additions

Regional supply conditions are changing as more recycled containerboard capacity comes onstream within practical shipping distance of Bahrain. Star Paper Mill inaugurated its USD 54.4 million recycled containerboard facility in KEZAD in May 2026, adding 135,000 tonnes per year of testliner and fluting and positioning Bahrain within its main GCC export corridor.[2]Trade Arabia, “USD 54.4m Recycled Containerboard Plant Opens In KEZAD,” Trade Arabia, tradearabia.com The plant also recycles up to 80% of domestically sourced UAE waste paper, which points to a more developed regional circular supply base for recycled grades. MEPCO’s PM5 line in Jeddah is scheduled for startup in Q4 2027 and will add 450,000 tonnes per year of lightweight testliner and corrugating medium, which materially changes the future supply balance for the GCC. For converters in Bahrain, nearer regional supply means shorter lead times, less need for precautionary inventory, and lower exposure to long-haul freight shocks. As these mills ramp up, European suppliers are likely to face more price pressure on standard grades, which should improve procurement leverage across the Bahrain containerboard market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Recovered Paper, Energy, And Freight Costs | -0.9% | GCC-wide, with acute pass-through exposure for Bahrain’s import-dependent converters | Short term (≤ 2 years) |

| Limited Domestic Recycling And Fiber Recovery Infrastructure | -0.6% | Bahrain-specific, compounded by small population base and commercial waste management gaps | Medium term (2-4 years) |

| Strait Of Hormuz And Red Sea Logistics Disruption Risk | -0.5% | Bahrain and all GCC states dependent on sea-borne containerboard imports and exports | Short term (≤ 2 years) |

| Desalinated-Water Cost Burden On Regional Paper Supply | -0.3% | Bahrain and broader GCC, most acute for energy-intensive papermaking at regional mills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In Recovered Paper, Energy, And Freight Costs

OCC prices fell to USD 44 per tonne by December 2025 and then rose to USD 62.50 per tonne by May 2026, which represented a 42% increase in 5 months and quickly changed the cost base for recycled containerboard grades. That volatility passed directly into pricing for GCC testliner and fluting because regional mills tie output economics to recovered paper and energy benchmarks. Saudi Arabia also raised diesel prices by 7.8% to SAR 1.79 per liter from January 1, 2026, which added more cost to board transported into Bahrain by land through the King Fahad Causeway. Converters in Bahrain could not fully recover that increase through box pricing without risking volume leakage to imported alternatives. The problem is structural because Bahrain has no meaningful domestic recovered paper base that would allow converters to hedge these cycles through local sourcing. As GCC energy subsidy reforms continue, regional papermaking costs are also likely to remain under pressure in the Bahrain containerboard market.

Limited Domestic Recycling And Fiber Recovery Infrastructure

Bahrain’s local fiber recovery base remains constrained by a small resident population, limited waste sorting capacity, and the absence of a large-scale recovered paper collection and baling system. This leaves the Bahrain containerboard market heavily dependent on imported recovered paper and imported finished board. Converters have tried to manage that exposure with inventory buffers, but the 2026 shipping disruptions showed those buffers were not sufficient when multiple trade routes were stressed at the same time. Port-side recovered paper volumes from Khalifa Bin Salman Port are too limited to support domestic papermaking at a meaningful scale. Without organized material recovery facilities handling commercial and retail waste streams, Bahrain’s circular packaging goals are harder to translate into actual fiber availability. The National Waste Management Strategy sets the policy direction, but mandatory collection targets for the paper value chain have not yet been codified in binding sector-specific rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Dominance Reshapes Input Sourcing

Recycled Fibers accounted for 77.78% of Bahrain containerboard market share by material in 2025, and they are also projected to grow at the fastest pace with a 3.41% CAGR through 2031. This shows that the Bahrain containerboard market is being shaped first by cost discipline and then by a broader regional supply shift toward recycled grades. The lead for recycled inputs is not only a price issue because GCC recovered paper systems are becoming more established and are narrowing the quality gap for standard transit-case applications. That makes recycled testliner and fluting more acceptable across a wider range of end uses in the Bahrain containerboard market.

Star Paper Mill’s KEZAD facility, commissioned in May 2026, reinforced that direction by recycling up to 80% of domestically sourced UAE waste paper into testliner and fluting for GCC-wide distribution. The project also signals a more practical regional circular model that matches Bahrain’s policy direction on waste and packaging. Virgin Fibers still hold a necessary place in food-contact, high-burst-strength, and pharmaceutical-adjacent applications where 100% recycled inputs cannot fully meet specification needs. That means recycled grades will keep leading volume, while virgin grades should retain a smaller but more performance-driven role. The Bahrain containerboard market is therefore likely to remain split between recycled-grade scale and virgin-grade specification premiums over the forecast period.

By Product Type: Kraftliners Lead Volume While Flutings Register Fastest Growth

Kraftliners held 45.61% of the Bahrain containerboard market share by product type in 2025, reflecting steady demand for stronger outer liners in food, beverage, industrial, and export transit cases. Their lead comes from the need for burst strength and transport durability in shipments that move across GCC routes and through re-export channels. Flutings, however, are forecast to post the fastest expansion, and the Bahrain containerboard market size for flutings is projected to grow at a 3.17% CAGR through 2031. That growth is closely tied to e-commerce and quick-commerce formats that need structural rigidity with lighter weight and tighter packaging efficiency.

Testliners continue to serve the middle ground of the product mix, especially in cost-sensitive general merchandise boxes where compression strength and printability matter more than maximum burst performance. A more important structural change is the rising demand for lightweight fluting grades below 90 g/m². MEPCO’s PM5 line is designed to target this space and is expected to introduce low-basis-weight paper at regional scale after its planned Q4 2027 startup. Once that capacity becomes available, Bahrain-based converters that adjust procurement early may be in a better position to manage landed costs and respond faster to changing order profiles. This keeps the Bahrain containerboard market centered on kraftliner today, while the next change in mix is likely to come from flutings.

By End-User Industry: Food And Beverage Anchors Demand, Industrial Segment Accelerating

Food and Beverage accounted for 32.31% of the Bahrain containerboard market in 2025, making it the largest end-user segment because of recurring demand from Bahrain’s GCC-serving food processing base. These plants supply biscuit, dairy, and confectionery products across the region on regular schedules, which keeps corrugated case demand stable even when domestic conditions are softer. Industrial is the fastest-growing end-user segment, with forecast growth of 2.87% through 2031, supported by Bahrain’s push into aluminium downstream activity, petrochemical packaging, and light manufacturing. This growth direction shows that the Bahrain containerboard market is not relying on food demand alone to support its next phase of expansion.

Consumer goods also remain relevant as organized retail expands and private-label as well as promotional carton runs become more common. Other end-user industries, including pharmaceuticals, personal care, and logistics packaging, add a smaller but growing stream of demand, especially in corrugated inserts used for temperature-sensitive shipments.

Geography Analysis

Bahrain’s containerboard demand is concentrated within a small island economy, but its role in GCC logistics gives the Bahrain containerboard market importance beyond its physical size. Khalifa Bin Salman Port recorded 428 vessel calls in H1 2025, up from 389 calls in H1 2024, which showed a clear recovery in Bahrain’s regional trade activity.[3]Ministry of Transportation and Telecommunications, Bahrain, “Khalifa Bin Salman Port,” Ministry of Transportation and Telecommunications, mtt.gov.bh In February 2025, Bahrain and APM Terminals signed a Letter of Intent to more than double port throughput by 2030. The planned investment also included new container-handling capacity, stronger Saudi connectivity, and an 11.5-megawatt solar project for the terminal. That port-led buildout supports packaging demand because goods moving through free-zone warehousing often need corrugated cases for storage, repacking, and onward distribution.

Bahrain’s location between Saudi Arabia and Gulf shipping lanes strengthens its position as a regional logistics and repackaging node. Non-oil re-exports reached BHD 165 million in Q1 2026, and the UAE as well as Saudi Arabia accounted for 66% of that value, which confirms Bahrain’s gateway role in regional trade flows. Re-export intensity directly lifts demand for kraftliner and recycled testliner because goods are frequently consolidated, repacked, or relabeled before they move onward. The dual disruption affecting the Strait of Hormuz and Red Sea from late February 2026 exposed how vulnerable this geography can become when multiple chokepoints are under pressure at the same time. Port calls were disrupted, imported board faced delays, and locally available corrugated stock saw short-term demand spikes during the same period. This mix of opportunity and exposure remains a defining feature of the Bahrain containerboard market.

Within the GCC, Bahrain remains a smaller demand center than Saudi Arabia and the UAE, but it benefits from flexible access to both overland and short-sea supply routes. The King Fahad Causeway and intra-Gulf services, including the MSC Gulf Shuttle connection from Dammam to Khalifa Bin Salman Port, give Bahrain options that many island markets do not have. Harmonized GCC standards also make it easier to procure certified grades from regional suppliers without facing repeated approval costs across borders. The medium-term path for the Bahrain containerboard market therefore looks steady, with port expansion and re-export activity offsetting the natural demand ceiling created by a resident population of around 1.7 million.

Competitive Landscape

The Bahrain containerboard market has a concentrated local converting structure because domestic output is handled by a small number of integrated corrugated-box producers. This pattern is reinforced by the capital intensity of box manufacturing and the limited scale of the local market. United Paper Industries BSC(C), trading as Bahrain Pack, remains one of the strongest domestic positions in corrugated-box converting, and its reach extends beyond Bahrain into Saudi Arabia, Kuwait, and other GCC destinations. Its location benefits from both port access and the direct overland route into Saudi Arabia, which supports export-oriented distribution. Even so, the Bahrain containerboard market still depends heavily on imported finished board because local paper production capacity remains very limited.

International suppliers compete in Bahrain mainly through trading relationships and distributor channels rather than through direct local conversion assets. Mondi opened its EUR 200 million, USD 216 million, recycled containerboard mill in Duino, Italy in December 2025, adding 420,000 tonnes per year of waste-based fluting and testliner that can serve export routes into Middle East markets.[4]Mondi Group, “Full-Year Results Announcement 2025, Integrated Report And Financial Statements,” Mondi Group, mondigroup.comThat move increases competitive pressure on standard grades entering GCC markets from Europe. Regional competition is also becoming stronger after Star Paper Mill commissioned its 135,000-tonne-per-year KEZAD facility in May 2026 and identified the GCC, including Bahrain, as a priority export corridor. MEPCO’s PM5 investment adds another strategic supply move that is likely to deepen regional competition once startup begins in Q4 2027.

The clearest white-space opportunities in the Bahrain containerboard market are in food-safe converting, certified sustainable packaging, and shelf-ready formats. GCC food exporters are placing greater value on FSC and PEFC documentation when packaging is meant for retail channels with stricter compliance requirements. Shelf-ready packaging also remains under-served because it requires cleaner print surfaces, tighter die-cut accuracy, and better score consistency than standard transit cases. Smaller converters are starting to respond by adding advanced die-cutting and digital printing capability so they can compete on turnaround speed and design flexibility rather than price alone. Over time, the Bahrain containerboard market is likely to reward converters that combine compliance, print quality, and sourcing resilience rather than relying only on scale.

Bahrain Containerboard Industry Leaders

United Paper Industries BSC(C)

Manama Packaging Industry W.L.L.

Middle East Paper Manufacturing and Production Company

Hotpack Packaging Industries LLC

Arabian Packaging Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Star Paper Mill inaugurated its USD 54.4 million, AED 200 million, recycled containerboard manufacturing facility at Khalifa Economic Zones Abu Dhabi, spanning 90,000 sq m with an annual production capacity of 135,000 tonnes of testliner and fluting jumbo reels. The plant recycles up to 80% of domestically sourced UAE waste paper, with the GCC, including Bahrain, designated as the primary export corridor, materially increasing available regional supply of recycled containerboard.

- May 2026: Simultaneous disruptions to the Strait of Hormuz and Red Sea shipping routes, following regional military escalation from February 28, 2026, created the GCC containerboard market’s most severe logistics disruption in modern history. Kpler Container Intelligence data through May 2026 showed 79% of the 53 container vessels initially trapped inside the Persian Gulf still waiting, and rerouting via the Cape of Good Hope added 10-14 days to transit times and significantly inflated freight surcharges on imported containerboard reaching Bahrain converters.

- February 2026: Bahrain’s Ministry of Industry and Commerce issued Ministerial Decision (7) of 2026, prohibiting the manufacture, import, and use of single-use plastic bags with a thickness of less than 57 microns under the National Waste Management Strategy, with a 6-month transitional period for inventory depletion and manufacturer compliance. The decision was coordinated with the Supreme Council for Environment and built on a regulatory escalation since Ministerial Decision (11) of 2019.

Bahrain Containerboard Market Report Scope

The Bahrain Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Bahrain Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast size of the Bahrain containerboard market?

The Bahrain containerboard market was valued at USD 69.89 million in 2025, stands at USD 80.23 million in 2026, and is projected to reach USD 100.29 million by 2031 at a 4.56% CAGR.

What is driving demand for containerboard in Bahrain?

The main demand drivers are e-commerce parcel box requirements, tighter regulation against thin plastic packaging, steady food and beverage shipments, and new regional recycled containerboard capacity.

Which material segment leads in Bahrain?

Recycled Fibers led with 77.78% share in 2025 and are also the fastest-growing material segment, with a projected 3.41% CAGR through 2031.

Which product type is growing the fastest?

Flutings are forecast to expand at a 3.17% CAGR through 2031, supported by e-commerce fulfillment, right-sized packaging, and demand for lighter corrugating medium.

What are the main risks for converters operating in Bahrain?

The biggest risks are OCC, energy, and freight cost volatility, limited domestic fiber recovery infrastructure, and shipping disruption through the Strait of Hormuz and Red Sea routes.

Why does Bahrain matter in GCC packaging supply chains?

Bahrain plays a logistics and re-export role through Khalifa Bin Salman Port and the King Fahad Causeway, which creates packaging demand beyond what its domestic population alone would generate.

Page last updated on: