Hybrid Terrestrial-Satellite Telecom Networks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

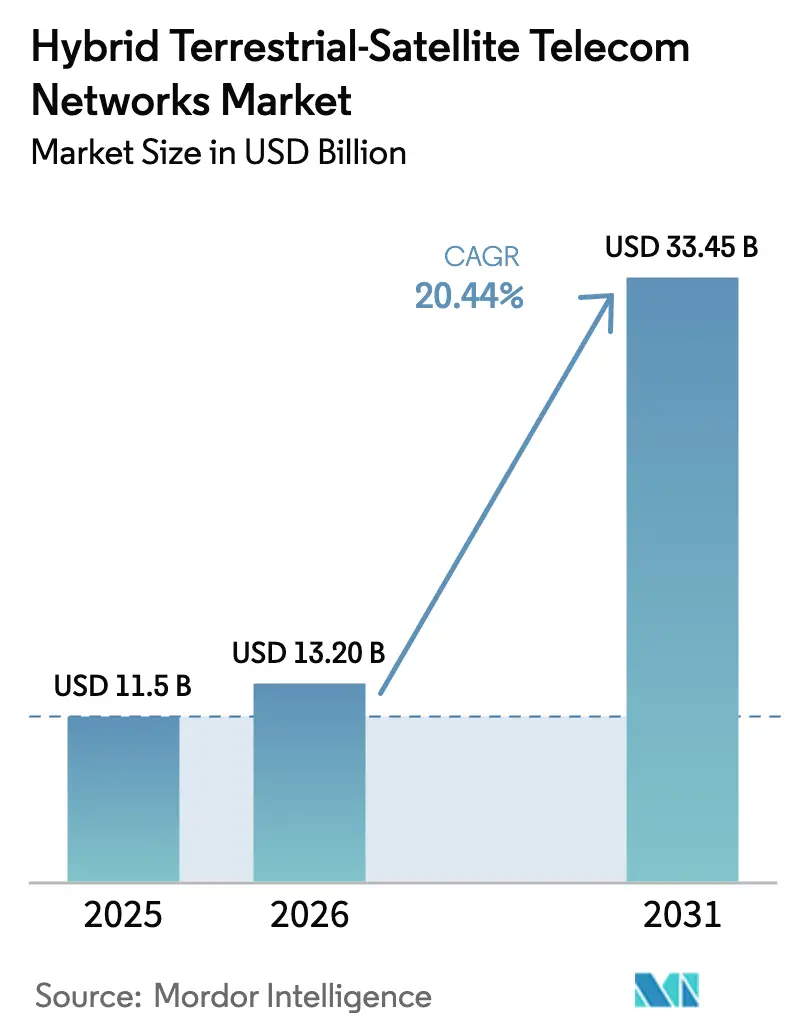

| Market Size (2026) | USD 13.20 Billion |

| Market Size (2031) | USD 33.45 Billion |

| Growth Rate (2026 - 2031) | 20.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hybrid Terrestrial-Satellite Telecom Networks Market Analysis by Mordor Intelligence

The Hybrid Terrestrial-Satellite Telecom Networks Market size is expected to grow from USD 11.5 billion in 2025 to USD 13.20 billion in 2026 and is forecast to reach USD 33.45 billion by 2031 at 20.44% CAGR over 2026-2031. Advancing 3GPP Release 17 non-terrestrial network (NTN) standards, dramatic launch-cost reductions of approximately 50% since 2024, and government-funded rural broadband mandates have converted satellite links from backup to integral 5G access, especially where fiber remains uneconomic. Mobile network operators now embed Kuiper, Starlink, and AST SpaceMobile capacity into their cores, ensuring seamless coverage that meets regulatory service-quality targets. Capital inflows have therefore shifted toward multi-orbit architectures, edge gateways, and AI-based traffic orchestration that lower the total cost of ownership and unlock new revenue pools. Operator enthusiasm translates into vigorous competition among vertically integrated hyperscalers, traditional GEO incumbents, and emerging LEO specialists. North America remains the test bed for spectrum-sharing and direct-to-device pilots, while Asia-Pacific records the fastest capital spending as China Mobile, NTT DOCOMO, and India’s state operators race to extend 5G footprints via satellites.

Key Report Takeaways

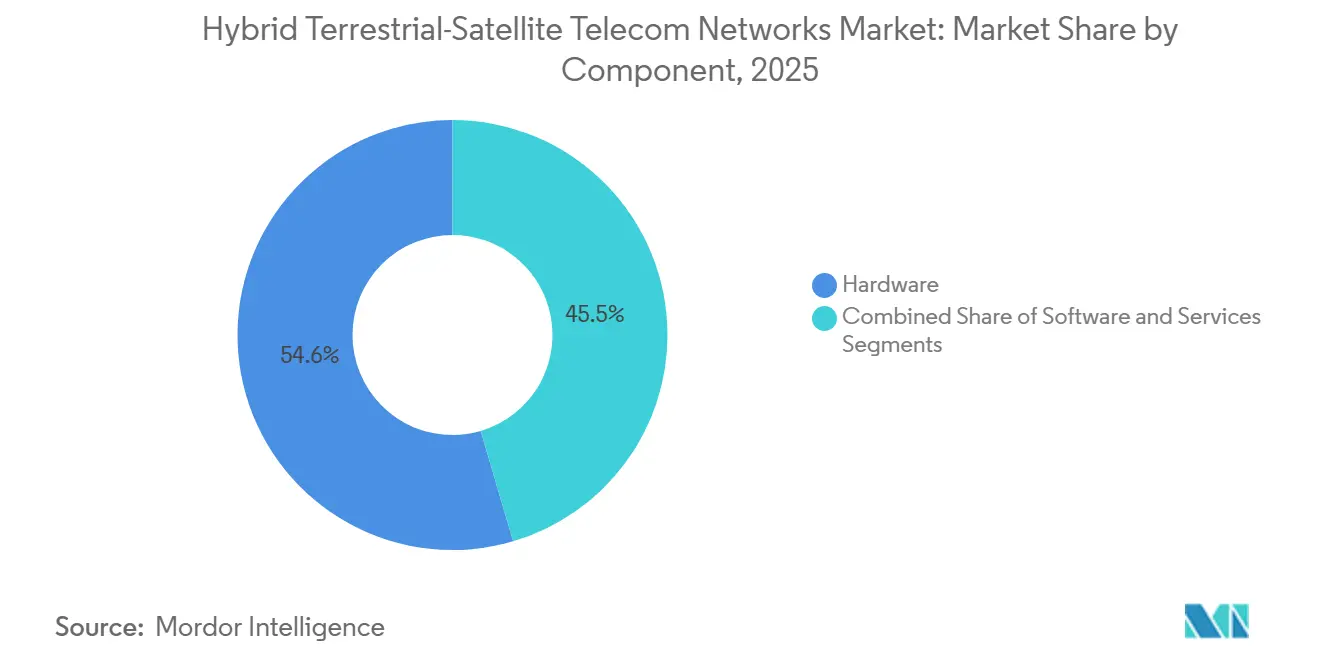

- By component, hardware led with 54.55% of the Hybrid Terrestrial-Satellite Telecom Networks market share in 2025, whereas software is projected to expand at a 24.50% CAGR through 2031.

- By platform, satellite constellations held a 38.97% share of the Hybrid Terrestrial-Satellite Telecom Networks market in 2025, while user equipment is advancing at a 27.82% CAGR through 2031.

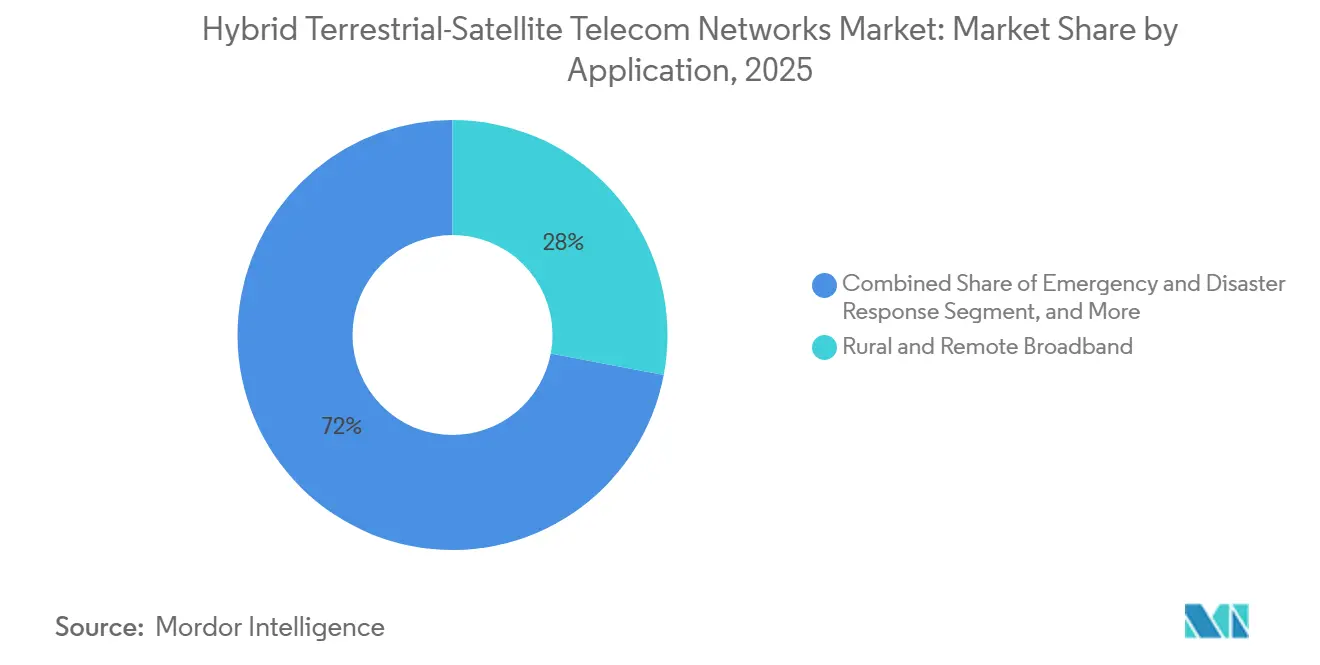

- By application, rural and remote broadband accounted for 27.98% of revenue share in 2025; Internet-of-Things use cases are forecast to grow at a 26.45% CAGR through 2031.

- By end-user, mobile network operators accounted for 31.32% of revenue in 2025, whereas the consumer direct-to-device segment is registering a 28.67% CAGR for 2026-2031.

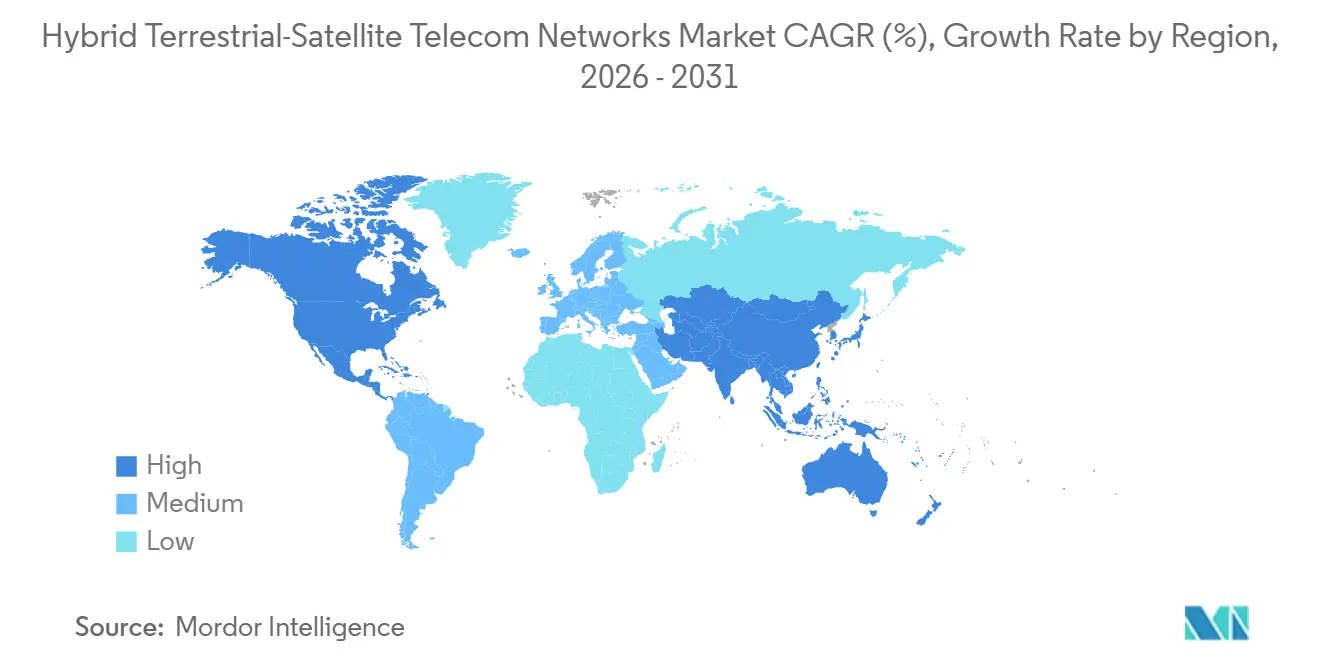

- By geography, North America commanded 35.70% of the revenue share in 2025, whereas Asia-Pacific is predicted to post the fastest regional CAGR of 25.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hybrid Terrestrial-Satellite Telecom Networks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 3GPP Rel-17 NTN Standardization | +4.2% | Global, early uptake in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government-Funded Rural Broadband Programs | +5.1% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Reusable Launch Vehicles Lowering Constellation CAPEX | +3.8% | Global, highest influence on North America and Asia-Pacific operators | Long term (≥ 4 years) |

| Demand for Resilient Disaster-Response Connectivity | +2.3% | North America, Asia-Pacific, South America | Short term (≤ 2 years) |

| AI-Driven Traffic-Steering for LEO/Terrestrial Hand-Off | +2.9% | Global, strongest where dense terrestrial grids exist | Medium term (2-4 years) |

| Spectrum-Trading Marketplaces for Idle Satellite Capacity | +1.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

3GPP Rel-17 NTN Standardization

Finalized air-interface rules let smartphones treat satellites as native radio nodes, eliminating bulky antennas and trimming modem complexity. More than 50 million Snapdragon X80 and Dimensity 9400 devices shipped by late 2025, proving consumer appetite for built-in satellite coverage. Release 18 pushes the capability to NB-IoT and LTE-M, lowering sensor power budgets below 1 watt and widening agricultural and maritime adoption. Interoperability tests certified in January 2026 show cross-operator roaming works, giving carriers confidence to expose services under common billing profiles.[1]GSMA, “NTN Roaming Profile Certification,” gsma.com As silicon vendors integrate NTN logic into commercial chipsets, production economies drive down handset premiums, accelerating penetration in mid-tier models.

Government-Funded Rural Broadband Programs

The United States BEAD program earmarked USD 42.45 billion and requires hybrid designs where fiber costs exceed USD 100,000 per mile. 18 states already qualified satellite-terrestrial bidders, turning LEO links into permanent infrastructure rather than temporary bridges. Europe’s EUR 6 billion IRIS2 constellation embeds sovereignty clauses that oblige traffic to remain on EU soil and interoperate with 5G cores. India’s mandate for satellite backhaul at new rural 5G sites compels operators to deploy NTN gateways, while China’s CNY 15 billion fund pilots integrations across Tibet and Xinjiang. Such policies convert latent demand into booked contracts, bolstering the revenue pipeline for constellation owners and terrestrial carriers alike.

Reusable Launch Vehicles Lowering Constellation CAPEX

Falcon 9 broke the 23-flight record in 2025, pushing launch prices to LEO toward USD 2,500 per kilogram, half the 2020 level.[2]SpaceX, “Starlink Direct to Cell,” spacex.com New Glenn and Vulcan Centaur lifts pushed Kuiper’s per-satellite cost below USD 1 million, enabling regional carriers and small nations to contemplate national micro-constellations.[3]Amazon, “Project Kuiper Updates,” aboutamazon.com AST SpaceMobile reported a 40% cut in BlueBird build-and-launch outlay versus 2023 prototypes, hastening its 20-satellite global grid. Faster, cheaper launches shrink payback periods and justify secondary replenishment cycles that keep average satellite age under five years, improving power-efficient payload design and throughput.

Demand for Resilient Disaster-Response Connectivity

Hurricanes Helene and Melissa in 2024 showed that terrestrial grids can fail for weeks. AT&T’s satellite-enabled FirstNet trucks restored priority links within 48 hours, 60% faster than fiber repair teams. Starlink terminals delivered hospital connectivity in Jamaica within three days, becoming a model for national disaster stockpiles. NOAA and Verizon now stream hurricane core video from drones using satellite backhaul, a practice adopted for wildfire monitoring, too. As climate events intensify, first-responder agencies insist on hybrid coverage in procurement specifications, driving predictable capacity bookings even outside peak consumer hours.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Dual-Mode Terminals and Gateways | -2.7% | Global, acute in Asia-Pacific and South America | Short term (≤ 2 years) |

| Complex Multi-Jurisdictional Licensing Regimes | -1.9% | Europe and Asia-Pacific | Medium term (2-4 years) |

| Doppler-Induced Latency Issues for 5G-URLLC | -1.4% | Global industrial and automotive users | Long term (≥ 4 years) |

| Power-Budget Limits on Battery IoT Nodes | -1.2% | Agriculture, logistics, maritime sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Dual-Mode Terminals and Gateways

Dual-mode smartphones still cost USD 150-300 more than terrestrial-only units, limiting uptake where average selling prices stay under USD 200. Gateway nodes, priced at USD 5-15 million each, must be installed every 500-1,000 kilometers to achieve sub-100-millisecond round-trip latency, stretching operator balance sheets. BlueBird alone will need more than USD 200 million in ground infrastructure to enable global roaming. Financing hurdles can delay commercial launches by a year, compressing first-mover advantages and slowing revenue recognition.

Complex Multi-Jurisdictional Licensing Regimes

A hybrid operator entering the EU must negotiate 27 national rules, a process that pushed Vodafone’s Satellite Connect Europe launch 9 months beyond plan. RSPG guidelines issued in 2025 harmonize core principles yet leave power-flux and device-type details to member states, leading Germany to approve by mid-2026 while Italy defers to 2027. In Asia-Pacific, India’s security clearances, Japan’s emergency-only restrictions, and China’s domestic-traffic routing mandate each impose distinct cost layers. Fragmentation forces constellation owners to tailor beams, encryption, and billing, eroding economies of scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Orchestration Drives Margin Expansion

Hardware accounted for 54.55% of total revenue in 2025, following heavy spending on satellites, launch services, and dual-mode devices. Software, however, is forecast to outpace all other layers at a 24.50% CAGR. This swing positions orchestration engines, slice controllers, and AI traffic directors as the core profit levers of the Hybrid Terrestrial-Satellite Telecom Networks market. Qualcomm’s modem firmware predicts satellite ephemeris ten seconds ahead, cutting handoff latency by 40% and improving voice continuity, an advantage operators monetize through premium service tiers.

Service revenues follow software’s trajectory as operators outsource constellation-to-core integration and 24/7 network operations. Nokia’s Network as Code platform allows enterprises to reserve on-demand satellite bandwidth through APIs, turning connectivity into a programmable resource. While antennas and power systems remain essential, much of the incremental value accrues to code that maximizes spectral reuse, compresses Doppler offsets, and ensures regulatory compliance in real time. As chipset prices fall, margin contribution tilts decisively toward algorithms and lifecycle support, reinforcing the strategic logic of hyperscalers bundling connectivity with cloud services.

By Platform: User Equipment Adoption Accelerates Direct-to-Device Shift

Satellite constellations took 38.97% of 2025 billings, yet growth now pivots to user equipment as chipset integration slashes entry barriers. Hybrid Terrestrial-Satellite Telecom Networks market size allocations show user equipment tracking a 27.82% CAGR through 2031, reflecting handset vendors embedding NTN functions for single-SIM behavior. MediaTek’s Dimensity 9400 adds satellite messaging at a bill-of-materials cost under USD 15, aligning cost structures with mid-tier consumer price points.

Terrestrial infrastructure still absorbs capital, particularly standalone 5G cores with slice-awareness that broker satellite capacity. Edge gateways capable of steering beams across LEO, MEO, and GEO orbits proliferate near fiber landing stations, shortening effective path length and mitigating Doppler distortion. Amazon’s Kuiper customer-premises terminal, priced at USD 299, halves the cost of historic GEO VSAT while bundling Wi-Fi 7, making residential adoption practical in sparsely populated counties. As direct-to-device capability becomes mainstream, differentiated performance will arise from how smartly devices and base stations swap orbits in sub-second intervals rather than from raw satellite counts.

By Application: IoT Overtakes Traditional Broadband Use Cases

Rural broadband still accounted for the largest slice at 27.98% of 2025 revenue, but IoT services now have the steepest trajectory. The Hybrid Terrestrial-Satellite Telecom Networks market will see IoT categories grow at a 26.45% CAGR, driven by 3GPP Release 18 optimizations that enable battery-powered sensors to transmit via satellite within a 1-watt budget. Asset-tracking for agriculture, oil pipelines, and rail logistics dominates massive-IoT volumes, whereas remote valve control and grid automation define critical-IoT demand.

Vodafone’s GEO-plus-LEO model charges per message, slashing ownership costs for distributors needing only sporadic status checks. Deutsche Telekom blends GEO, LEO, and terrestrial LTE-M to guarantee sub-1-second reaction times for industrial automation, validating that hybrid links can satisfy deterministic control loops. Maritime and aviation operators adopt multi-orbit bundles that balance latency and sky-view availability; SES’s O3b mPOWER delivers 100 Mbps per aircraft, enough for simultaneous 4K streaming and telemetry. Emergency-response agencies and defense networks round out demand, leveraging satellite resiliency to ensure command continuity in the event of fiber cuts or jamming.

By End-User: Consumers Drive Direct-to-Device Surge

Mobile network operators accounted for 31.32% of 2025 billings, owing to wholesale satellite capacity purchases and gateway rollouts. Consumer adoption is now accelerating, with a 28.67% CAGR, as leading smartphones embed satellite SOS, messaging, and, soon, voice. NTT DOCOMO’s fiscal 2026 launch will make Japan the first Asian market where everyday users access LEO coverage without hardware add-ons. T-Mobile already offers satellite texts at no extra cost to postpaid subscribers, framing the service as a resilience feature rather than a luxury.

Enterprises leverage bonded links for mining, oil, and agriculture to meet latency targets under 100 milliseconds, even in off-grid sites. Maritime majors such as Maersk optimize routes via always-on links, saving 3% fuel on Pacific crossings. Airlines equip cabins with phased arrays that promise 100 Mbps per passenger, converting connectivity into ancillary revenue and improving flight operations. Defense agencies integrate commercial LEO into encrypted architectures, expanding tactical bandwidth while hardening networks against single-orbit disruption.

Geography Analysis

North America accounted for 35.70% of revenue in 2025, anchored by FCC spectrum-sharing milestones and the USD 42.45 billion BEAD program that subsidizes hybrid deployments in high-cost counties. The United States serves as an innovation hub as AT&T bonds Kuiper backhaul with fiber, T-Mobile runs PCS-band direct-to-cell in beta, and Verizon uses satellite links for FirstNet emergency drones. Canada’s Telus and Bell invested in AST SpaceMobile to extend service across northern territories, while Mexico streamlined licensing to allow foreign constellations to sell direct without local partners, speeding Starlink's rural coverage.

Asia-Pacific leads growth, with a projected 25.41% CAGR through 2031. China’s CNY 15 billion fund compels state carriers to validate interoperability between domestic constellations and SA-5G cores by 2027. India’s directive requires every new remote 5G base station to support satellite backhaul, and Bharti Airtel’s OneWeb alliance underscores private carrier momentum. Japan’s early 2026 commercial launch by NTT DOCOMO positions consumers for nationwide direct-to-device coverage, while South Korea invests KRW 200 billion in indigenous gateway technology to reduce its reliance on foreign suppliers. Australia channels AUD 1.2 billion into regional connectivity, deploying Starlink backhaul for mining and indigenous communities.

Europe advances through policy harmonization yet remains staggered. RSPG guidelines published in 2025 set the blueprint for direct-to-device, but power-flux limits and device certification still differ per country, slowing pan-EU rollouts. The EUR 6 billion IRIS2 project guarantees sovereign routing and 5G core integration, sustaining domestic manufacturers and launch providers. Vodafone and AST SpaceMobile will activate service in Germany, Spain, and the United Kingdom by late 2026, proving commercial viability ahead of lagging markets. South America, plus the Middle East and Africa, are earlier in the curve, though Brazil’s regulator licensed Kuiper and Starlink in 2025, and Gulf Cooperation Council states negotiate with Thuraya and Inmarsat to blanket desert corridors.

Competitive Landscape

No entity controls more than 15% of global revenue, yielding a moderate level of fragmentation, yet mergers and acquisitions are accelerating. SES closed a USD 3.1 billion Intelsat purchase in 2025, combining 100 GEO satellites with 26 mPOWER MEO craft to market latency-selective bundles for aviation, maritime, and government users. Amazon’s vertically integrated Kuiper division counts 200 in-orbit satellites and will start commercial service in five countries by Q1 2026, leveraging AWS edge presence to cross-sell compute and storage.

AST SpaceMobile posted USD 54 million Q4 2025 revenue from pre-sold capacity to Vodafone, AT&T, and Rakuten, projecting USD 140 million in 2026 as it scales to 20 satellites. Spectrum strategy differentiates leaders. SpaceX co-opts existing PCS bands under tight FCC power flux density rules, granting rural coverage without new handset hardware.

Lynk Global contributes NB-IoT intellectual property to 3GPP, securing licensing revenue even if its constellation lags volume deployment. Legacy GEO operators retrofit software-defined payloads for elastic beam-forming, extending asset life and boosting revenue per hertz. Launch economics remain a wild card; should reusable heavy-lift costs drop another 30%, LEO stalwarts could triple spacecraft counts, diluting GEO operators’ price umbrella.

Hybrid Terrestrial-Satellite Telecom Networks Industry Leaders

Space Exploration Technologies Corp.

AST SpaceMobile, Inc.

Lynk Global, Inc.

Eutelsat S.A.

Intelsat S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Telus invested in AST SpaceMobile and pledged to launch Canadian direct-to-device services by late 2026.

- February 2026: NTT DOCOMO confirmed Starlink-powered direct-to-cell service for early fiscal 2026.

- December 2025: The seventh BlueBird satellite lifted, raising system throughput to 120 Mbps for unmodified smartphones.

Global Hybrid Terrestrial-Satellite Telecom Networks Market Report Scope

The Hybrid Terrestrial-Satellite Telecom Networks Market Report is Segmented by Component (Hardware, Software, and Services), Platform (Satellite Constellations, Terrestrial Infrastructure, User Equipment, and Edge Nodes and Gateways), Application (Emergency and Disaster Response, Maritime Connectivity, Aviation IFC and ATC Backup, Rural and Remote Broadband, Internet-of-Things (Massive IoT, Critical IoT), Defense and Security Networks, and Other Applications), End-User (Government and Defense Agencies, Maritime Operators and OEMs, Airlines and UAV Operators, Mobile Network Operators (MNOs), Enterprises and SMBs, Consumers (Direct-to-Device), and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Value (USD).

| Hardware |

| Software |

| Services |

| Satellite Constellations |

| Terrestrial Infrastructure (RAN and Core) |

| User Equipment (Handsets, CPE, IoT) |

| Edge Nodes and Gateways |

| Emergency and Disaster Response |

| Maritime Connectivity |

| Aviation IFC and ATC Backup |

| Rural and Remote Broadband |

| Internet-of-Things (Massive IoT, Critical IoT) |

| Defense and Security Networks |

| Other Applications |

| Government and Defense Agencies |

| Maritime Operators and OEMs |

| Airlines and UAV Operators |

| Mobile Network Operators (MNOs) |

| Enterprises and SMBs |

| Consumers (Direct-to-Device) |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | GCC Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Platform | Satellite Constellations | ||

| Terrestrial Infrastructure (RAN and Core) | |||

| User Equipment (Handsets, CPE, IoT) | |||

| Edge Nodes and Gateways | |||

| By Application | Emergency and Disaster Response | ||

| Maritime Connectivity | |||

| Aviation IFC and ATC Backup | |||

| Rural and Remote Broadband | |||

| Internet-of-Things (Massive IoT, Critical IoT) | |||

| Defense and Security Networks | |||

| Other Applications | |||

| By End-User | Government and Defense Agencies | ||

| Maritime Operators and OEMs | |||

| Airlines and UAV Operators | |||

| Mobile Network Operators (MNOs) | |||

| Enterprises and SMBs | |||

| Consumers (Direct-to-Device) | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | GCC Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is revenue growing for Hybrid Terrestrial-Satellite Telecom Networks?

The market’s revenue is projected to rise from USD 13.2 billion in 2026 to USD 33.45 billion by 2031, a CAGR of 20.44%.

Which region will add the most new users?

Asia-Pacific shows the steepest trajectory with a projected 25.41% CAGR, helped by operator trials in China, Japan, and India.

When will smartphones offer mainstream satellite messaging?

Chipsets integrated in late 2025 already support it, and mass-market handsets below USD 400 are expected to include the feature by 2027.

What share of 2025 revenue came from hardware?

Hardware captured 54.55% of 2025 revenue, reflecting satellites, launches, and dual-mode devices.

Which application is expanding fastest?

IoT services, spanning asset tracking to industrial automation, are forecast to grow at 26.45% CAGR through 2031.

Page last updated on: