Broadcast Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 8.02 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Broadcast Equipment Market Analysis by Mordor Intelligence

The Broadcast Equipment market size is expected to grow from USD 5.58 billion in 2025 to USD 5.93 billion in 2026 and is forecast to reach USD 8.02 billion by 2031 at 6.23% CAGR over 2026-2031.

This expansion in the Broadcast Equipment Market reflects the steady replacement of legacy, hardware-centric systems with software-defined, IP-native, and cloud-enabled architectures that cut capital costs and improve workflow agility. Intensifying direct-to-consumer streaming competition, surging demand for remote production, and ongoing digital switch-over mandates continue to steer purchasing decisions toward flexible equipment that supports multiple codecs, hybrid contribution networks, and real-time resource scaling. Established vendors strengthen their portfolios through R&D and selective acquisitions, while cloud-native entrants lower entry barriers with subscription models that convert upfront investment into predictable operating expenses. As broadcasters integrate artificial intelligence for content analysis and automated quality assurance, demand rises for compute-dense appliances and virtualized microservices that can be orchestrated both on premises and in hyperscale clouds.

Key Report Takeaways

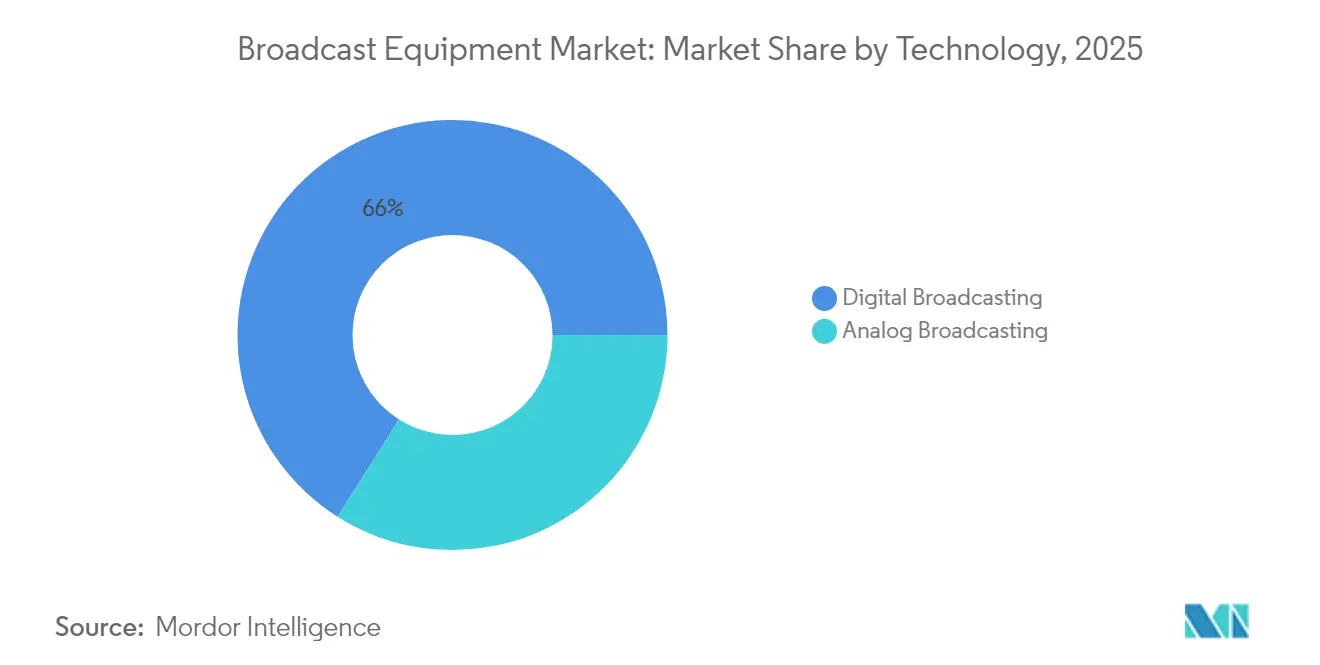

- By 2025, digital broadcasting had captured 66.02% of the broadcast equipment market share, and it is projected to grow at a 7.92% CAGR through 2031.

- By product, encoders held 24.42% of the broadcast equipment market share in 2025, and the segment is projected to grow at a 6.61% CAGR to 2031.

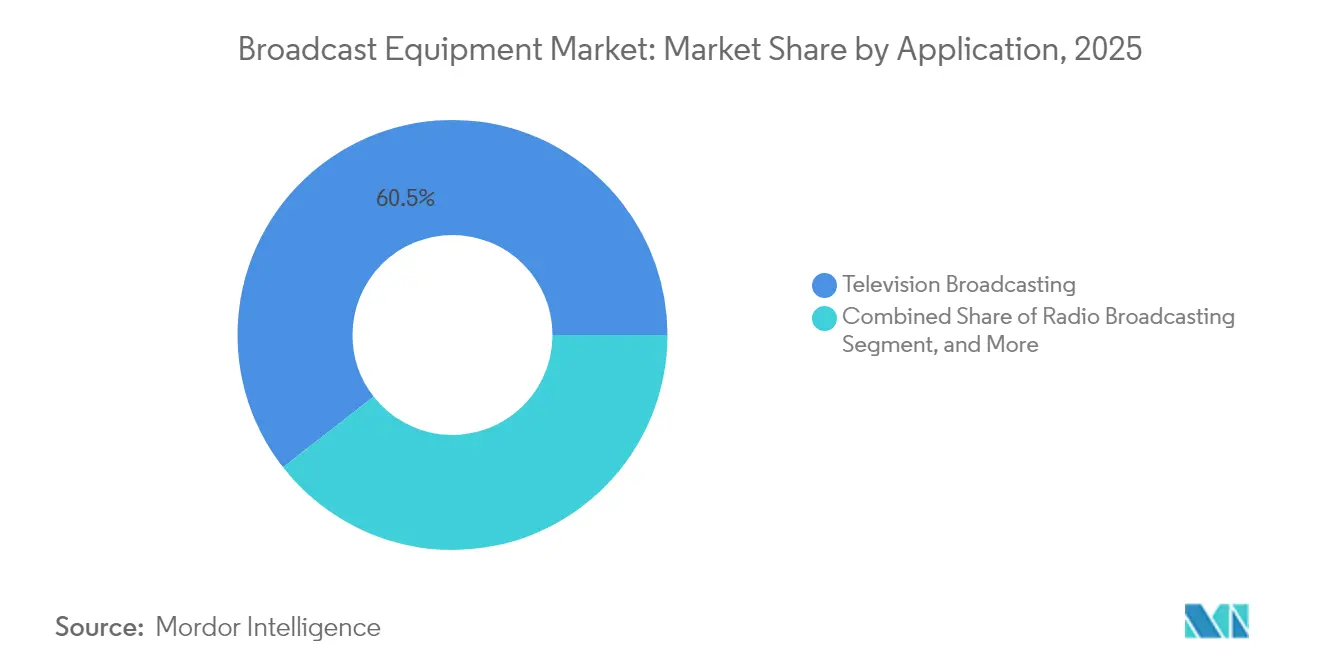

- By application, television broadcasting accounted for a 60.55% share of the broadcast equipment market size in 2025, whereas internet live streaming is advancing at a 7.18% CAGR.

- By end user, broadcasters commanded 53.12% of demand in 2025, while streaming service providers are projected to record the highest CAGR at 7.47% through 2031.

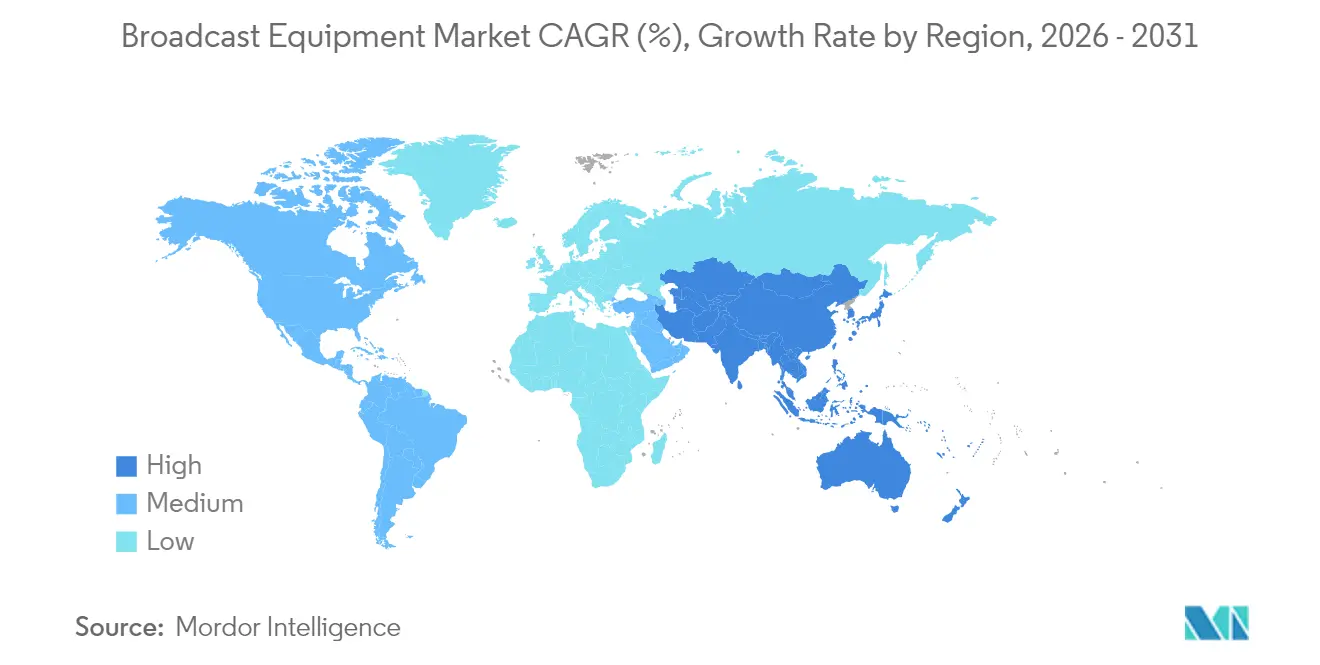

- By geography, North America led the broadcast equipment market with a 33.21% contribution in 2025, and the Asia-Pacific region is expected to be the fastest-growing at a 7.05% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Broadcast Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Encoders Supporting Multiple Codecs | +1.2% | Global-strongest in North America and Europe | Medium term (2-4 years) |

| Direct-To-Consumer OTT Expansion Accelerating Equipment Upgrades | +1.8% | Global-particularly Asia-Pacific and North America | Short term (≤ 2 years) |

| Rapid Transition to IP-Based Broadcasting Infrastructure | +1.5% | North America and Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Surge in Remote Production Workflows Post-Pandemic | +0.9% | Global-early adoption in North America and Europe | Short term (≤ 2 years) |

| Adoption of Cloud-Native SaaS Playout and Graphics | +0.8% | North America and Europe, expanding in Asia-Pacific | Medium term (2-4 years) |

| Government Mandates for Digital Switch-Over in Emerging Economies | +0.6% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Direct-To-Consumer OTT Expansion Accelerating Equipment Upgrades

Explosive subscriber growth at leading streaming services compels broadcasters to overhaul legacy plants so they can output pristine linear feeds and adaptive bitrate streams simultaneously. Netflix recorded 260 million global subscriptions in 2024, while Disney+ passed 150 million, prompting rights holders to demand delivery in HEVC for cable head-ends, AV1 for bandwidth-efficient streaming, and emerging VVC for 8K readiness.[1]Securities and Exchange Commission, “Company Filings and Reports,” sec.gov Multi-codec encoders, therefore, replace single-purpose appliances, triggering a new purchase cycle across newsrooms, sports networks, and regional stations. In parallel, the surge in original content budgets fuels the uptake of IP-backhaul kits that support distributed remote production and cloud post-production, ensuring that studios can fast-track global releases without relying on heavy on-site crews.

Rapid Transition to IP-Based Broadcasting Infrastructure

With SMPTE ST 2110 reaching critical mass, 78% of broadcasters budgeted IP infrastructure projects for 2024, accelerating the sunset of SDI routers and patch panels.[2]Society of Motion Picture and Television Engineers, “SMPTE Standards and Technology,” smpte.org Switching to commodity Ethernet fabrics slashes cabling complexity and reduces total cost of ownership as workflows migrate from dedicated baseband chains to software instances running on COTS servers. IP networks also simplify redundancy through seamless path protection, while native multicast enables operational scaling for pop-up channels or remote commentary positions. Crucially, IP backbones provide a direct bridge to public cloud services, enabling temporary compute bursts during marquee events without incurring permanent hardware costs, thereby further propelling the broadcast equipment market.

Growing Demand for Encoders Supporting Multiple Codecs

Eighty-five percent of facilities now require HEVC, H.264, and AV1 within the same encoder chassis to tailor content for legacy set-top boxes, smart TVs, and mobile streaming apps.[3]Alliance for IP Media Solutions, “IP Media Standards and Best Practices,” aims.tv Vendors respond with AI-optimized compression engines that deliver up to 40% bitrate reductions, freeing capacity on congested contribution links. Field-upgradable firmware enables operators to load VVC modules ahead of major sports tournaments, ensuring forward compatibility and protecting their investment. As 8K trials expand in Japan and South Korea, the need for software-defined, multi-codec pipelines becomes increasingly critical, sustaining encoder revenue growth within the broadcast equipment market.

Surge in Remote Production Workflows Post-Pandemic

The shift from truck-centric outside broadcasts to REMI workflows is now structural: adoption has jumped 340% between 2020 and 2024, and leading sports networks have trimmed on-site crews by up to 70% while preserving the quality of multi-camera storytelling. Low-latency encoders, secure bonded cellular uplinks, and IP-native switchers enable directors, replay operators, and graphics artists to collaborate from centralized hubs. Financial benefits include reduced travel costs, higher staff utilization, and faster venue turnaround, while environmental targets gain from lower logistical footprints. Consequently, demand intensifies for scalable IP routers, robust timing networks, and cloud-based replay engines, strengthening prospects for vendors that deliver integrated REMI toolkits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Lack of Global Standardization of Media Formats | -0.8% | Global-especially in cross-border distribution | Long term (≥ 4 years) |

| High Capital Expenditure for UHD and 8K Transmission Gear | -1.1% | Global-more pronounced in emerging markets | Medium term (2-4 years) |

| Spectrum Allocation Constraints in Urban Regions | -0.5% | Urban areas worldwide-North America and Europe visible | Long term (≥ 4 years) |

| Skills Gap in Operating IP and Cloud Broadcast Systems | -0.7% | Global-acute shortages in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for UHD and 8K Transmission Gear

Transitioning from HD to UHD and then to 8K multiplies network data rates and processing overhead, pushing equipment prices up to 3-7 times those of HD counterparts. Smaller stations and emerging-market operators struggle to align their payback horizons with such steep outlays, creating a two-speed adoption pattern where marquee channels upgrade first and regional players lag. Limited financing options and fast depreciation cycles exacerbate budget pressures, delaying wider rollouts and restraining the broadcast equipment market’s full revenue potential.

Persistent Lack of Global Standardization of Media Formats

The International Telecommunication Union logged more than 40 active video compression standards in 2024, fragmenting workflows and forcing broadcasters to maintain costly transcoding farms. Divergent regional preferences—from DVB-T2 in Europe to ISDB-T in parts of Latin America—complicate the exchange of multinational content and hinder economies of scale for manufacturers. Until regulators and standards bodies converge on fewer baseline profiles, interoperability expenses will continue to weigh on purchasing decisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Digital Broadcasting Deepens Its Hold

Digital platforms claimed 66.02% of 2025 revenue, and their 7.92% CAGR indicates relentless momentum as governments enforce analog switch-off deadlines. In parallel, many networks overlay IP fabrics on existing digital transmission, enabling self-provisioned contribution links and interactive services that drive advertising yield. The broadcast equipment market size for hybrid analog-digital solutions remains meaningful in rural pockets, yet sunset timetables narrow replacement windows, prompting brisk demand for combo transmitters that can be reconfigured through software updates.

Adoption also reflects the spectral efficiency of digital encoding, which allows multiplexing of secondary channels and data services within a single RF allocation. This agility fuels local language programming in the Asia-Pacific region and pop-up sports channels in Europe, expanding the addressable inventory for advertisers. Vendors that bundle spectrum-efficient modulators with IP-native monitoring dashboards secure repeat orders, reinforcing the primacy of digital technology within the broadcast equipment market.

By Product: Encoders Anchor Multi-Platform Workflows

Encoders generated 24.42% of 2025 turnover and maintain a 6.61% growth trajectory as every distribution path—terrestrial, satellite, cable, or OTT-depends on compression efficiency. AI-assisted algorithms now learn scene complexity and allocate bits adaptively, achieving 30-40% savings without picture degradation. These innovations lower CDN bills for streaming providers and free up transponder bandwidth for satellite operators, fueling a virtuous upgrade cycle that supports the broadcast equipment market's leadership share.

Video servers, switches, and transmitters remain indispensable, yet their design increasingly adopts modular, x86-based hardware wrapped in containerized software. As a result, customers focus on orchestration APIs and license flexibility rather than raw hardware specs. Dish antennas continue to serve remote contribution and disaster-recovery links, but growth lags IP terrestrial paths as 5G and fiber footprints widen. Vendors that package encoders with cloud transcoding and just-in-time packaging retain a competitive advantage across a converged broadcast equipment industry.

By Application: Television Retains Volume but Streaming Sets the Pace

Television broadcasting still delivered 60.55% of revenue in 2025, reflecting entrenched viewing habits and free-to-air mandates in many countries. Even so, internet live streaming’s 7.18% CAGR underscores shifting consumption toward mobile screens and connected TVs. Broadcasters address the overlap by simulcasting: linear content travels via ATSC 3.0 or DVB-T2 while synchronized OTT streams offer catch-up and personalization, demanding sophisticated origin servers and audience measurement tools.

Radio broadcasting remains crucial for local news and emergency alerts, especially in sparsely populated regions, but the incremental gains are modest. Satellite broadcasting secures specialized niches such as maritime broadband and in-flight entertainment, relying on high-power transponders and resilient uplink chains. Equipment manufacturers, therefore, refine converged playout engines that output SDI, IP, and satellite feeds concurrently, safeguarding investment as client priorities shift between traditional and streaming-first strategies in the broadcast equipment market.

By End User: Streaming Providers Propel Innovation

Broadcasters accounted for 53.12% of 2025 spending, while the fastest-rising budgets belonged to streaming service providers, with a 7.47% CAGR. These digital-native firms favor operational expenditure and microservices architectures, expecting elastic scale to millions of peak-time viewers without forklift upgrades. Consequently, vendors are pivoting toward SaaS modules for live channel origination, AI captioning, and ad insertion, bundled with consumption-based pricing to align with streaming revenue models.

Cable network operators modernize head-ends to mitigate cord-cutting, adding cloud DVR and IP gateways that ingest off-air signals and redistribute them as unicast streams. Production studios invest in virtual sets and cloud render farms to accelerate multi-platform content creation. Collectively, these shifts reward suppliers that deliver ultra-low-latency glass-to-glass chains and open APIs, reshaping competitive dynamics within the broader broadcast equipment industry.

Geography Analysis

North America led the broadcast equipment market with a 33.21% share in 2025 thanks to early IP adoption, NextGen TV incentives and heavy streaming investment. The Federal Communications Commission’s spectrum repack and ATSC 3.0 rollouts triggered facility rebuilds, while rights-holders poured capital into REMI studios supporting coast-to-coast sports coverage. Canada’s public-service mandates spurred procurements of multilingual captioning and rural transmitters, whereas Mexico’s completed analog switch-off supplied a final wave of transmitter orders.

Europe ranks second, buoyed by cross-border initiatives from the European Broadcasting Union that promote standardization and shared infrastructure. Germany and the United Kingdom spearhead UHD workflows and IP hub-and-spoke production, and France underpins demand with public broadcasting upgrades tied to cultural preservation funds. Southern and Eastern markets continue replacing DVB-T with DVB-T2 and adding HEVC encoders for HD tier expansion, sustaining steady equipment refresh cycles.

Asia-Pacific posts the fastest 7.05% CAGR as India’s nationwide digitization connects more than 200 million households and China’s 5G-based broadcast pilots showcase 8K and VR trials. Japan and South Korea retain technology leadership through immersive audio and 4K/8K satellite services, while Southeast Asian nations tap multilateral loans for infrastructure. Australia’s dispersed population drives demand for satellite uplinks and IP contribution to span vast geographies, rounding out regional growth drivers for the broadcast equipment market.

Competitive Landscape

The broadcast equipment market remains moderately fragmented, with the top five vendors controlling roughly 45% of the revenue, leaving ample room for specialists. Cisco Systems leverages its network heritage to dominate IP routers and multicast controllers, while Sony Group utilizes its imaging prowess in cameras and switchers. Panasonic and Grass Valley compete with end-to-end 4K live production suites, while Harmonic strengthens compression leadership after acquiring Ateme’s video delivery division in July 2024.

Cloud-native challengers such as AWS Elemental and Amagi disrupt by offering channel playout and ad insertion on an opex model, appealing to streaming entrants that prefer usage-based billing. Incumbents respond by containerizing flagship applications, launching subscription tiers, and integrating orchestration APIs for multicloud deployment. Patent filings exceeded 200 in 2024, centered on AI-assisted compression and IP timing, affirming sustained innovation despite maturing hardware margins.

Strategic differentiation gravitates toward unified workflows, as clients seek single-vendor stacks that bundle ingest, processing, graphics, automation, and delivery analytics. Consequently, merger activity intensifies as firms acquire niche talent in cloud playout, edge streaming, or low-latency transport to bridge portfolio gaps. The narrative positions integrators that can harmonize on-premises SDI islands with public cloud microservices as front-runners in the evolving broadcast equipment market.

Broadcast Equipment Industry Leaders

Cisco Systems Inc.

Telefonaktiebolaget LM Ericsson

EVS Broadcast Equipment SA

Grass Valley USA LLC

Harmonic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Sony Group Corporation allocated USD 200 million to build next-generation AI broadcast production systems that combine machine-learning-based content creation with live quality optimization, helping operators cut costs while sustaining premium output across every platform.

- August 2025: Cisco Systems finalized its USD 75 million purchase of cloud-native specialist StreamLabs Technologies, adding edge computing and AI-enhanced video processing to reinforce its leadership in IP-centric broadcast infrastructure.

- June 2025: Harmonic Inc. secured a USD 45 million contract from a leading European broadcasting consortium to deploy IP transmission networks across 12 countries, creating unified distribution standards and paving the way for the group’s direct-to-consumer expansion.

- March 2025: Ericsson opened a Broadcast Innovation Center in Singapore with a USD 30 million investment focused on 5G broadcast and edge-computing research, strengthening its foothold as Asia-Pacific demand for mobile-first video accelerates.

Global Broadcast Equipment Market Report Scope

Broadcasting is audio and video distribution to a broad audience using an electronic mass communication medium, usually radio waves. The broadcasting is done in a one-to-many format. Studio transmitter link, FM stereo generator, composite switcher, FM exciter, FM transmitter power amplifier, antenna combiner, antenna array, and antenna switcher are among the various broadcasting equipment required. They are used in news production, concerts, sports, and corporate conferences and are expected to be a critical factor in the growth of the broadcasting equipment market. The broadcast equipment market is segmented by technology (analog broadcasting, digital broadcasting), product (dish antennas, switches, video servers, encoders, transmitters, repeaters, and other products), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). Further, factors affecting the market's evolution in the near future, such as drivers and constraints, have been covered in the study. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

| Analog Broadcasting |

| Digital Broadcasting |

| Dish Antennas |

| Switches |

| Video Servers |

| Encoders |

| Transmitters and Repeaters |

| Other Products |

| Radio Broadcasting |

| Television Broadcasting |

| Internet Live Streaming |

| Satellite Broadcasting |

| Broadcasters |

| Cable Network Operators |

| Streaming Service Providers |

| Production Studios |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Analog Broadcasting | ||

| Digital Broadcasting | |||

| By Product | Dish Antennas | ||

| Switches | |||

| Video Servers | |||

| Encoders | |||

| Transmitters and Repeaters | |||

| Other Products | |||

| By Application | Radio Broadcasting | ||

| Television Broadcasting | |||

| Internet Live Streaming | |||

| Satellite Broadcasting | |||

| By End User | Broadcasters | ||

| Cable Network Operators | |||

| Streaming Service Providers | |||

| Production Studios | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the broadcast equipment market?

The broadcast equipment market size reached USD 5.93 billion in 2026.

How fast is demand for broadcast equipment expected to grow?

The market is projected to expand at a 6.23% CAGR between 2026 and 2031.

Which technology segment leads sales?

Digital broadcasting equipment commands 66.02% of revenue and grows at 7.92% CAGR.

Why are encoders so critical for broadcasters?

Encoders enable multi-codec delivery for linear, OTT and emerging 8K streams, and they currently hold 24.42% of product revenue.

Which region is expanding the quickest?

Asia-Pacific is the fastest-growing geography with a 7.05% CAGR through 2031.

How are remote production trends shaping procurement?

REMI workflows lower on-site costs and drive demand for IP routers, low-latency encoders and cloud production tools.

Page last updated on: