Sunglasses Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 23.01 Billion |

| Market Size (2031) | USD 31.06 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sunglasses Market Analysis by Mordor Intelligence

Sunglasses market size in 2026 is estimated at USD 23.01 billion, growing from 2025 value of USD 21.67 billion with 2031 projections showing USD 31.06 billion, growing at 6.18% CAGR over 2026-2031. Premiumization accelerates as consumers associate eye protection with wellness, style, and digital connectivity rather than simple sun blocking. Technology-enabled models encourage incumbents and start-ups to push research and development boundaries. Regional contrasts also shape opportunity; North America contributes most revenue, yet Asia-Pacific posts the fastest unit gains as middle-class cohorts adopt aspirational brands. Amid these drivers, sustainability commitments by leading producers raise material standards and create new differentiation levers through bio-based acetate, recycled polymers, and transparent supply chains.

Key Report Takeaways

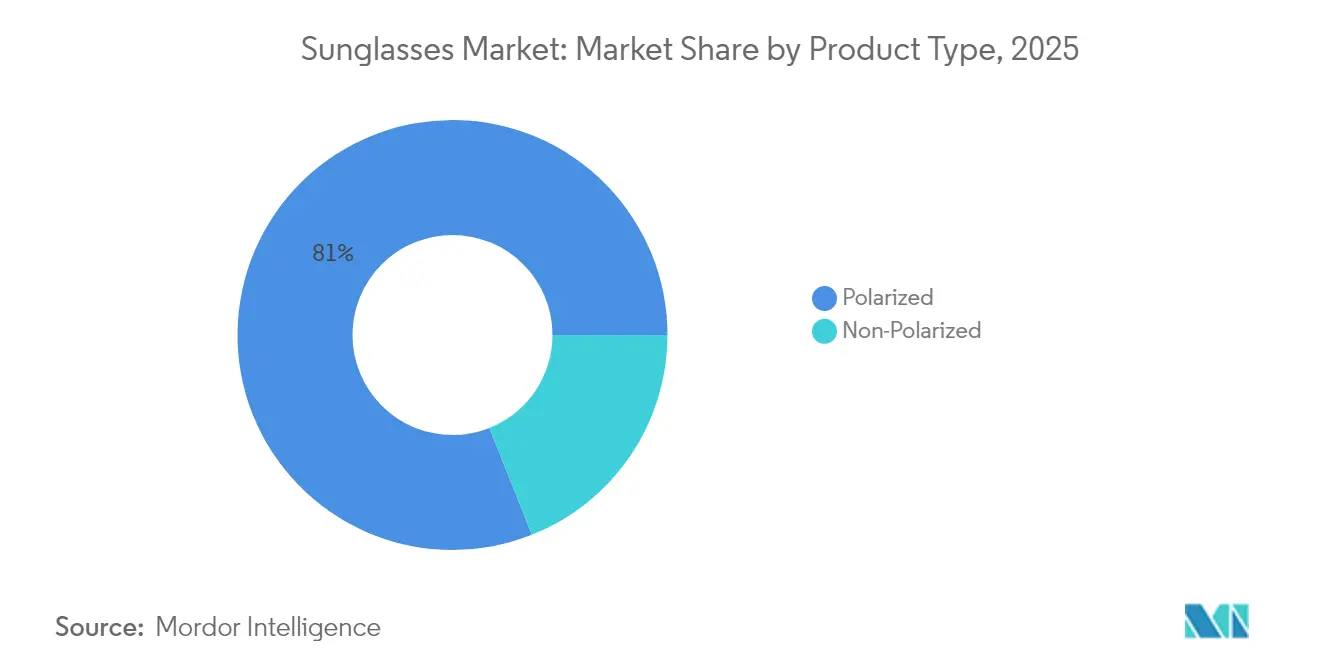

- By product type, polarized sunglasses held 81.02% of sunglasses market share in 2025 while non-polarized variants are expanding at a 6.68% CAGR to 2031

- By end user, women accounted for 54.21% of the sunglasses market in 2025, whereas the kids segment is forecast to register a 6.27% CAGR through 2031

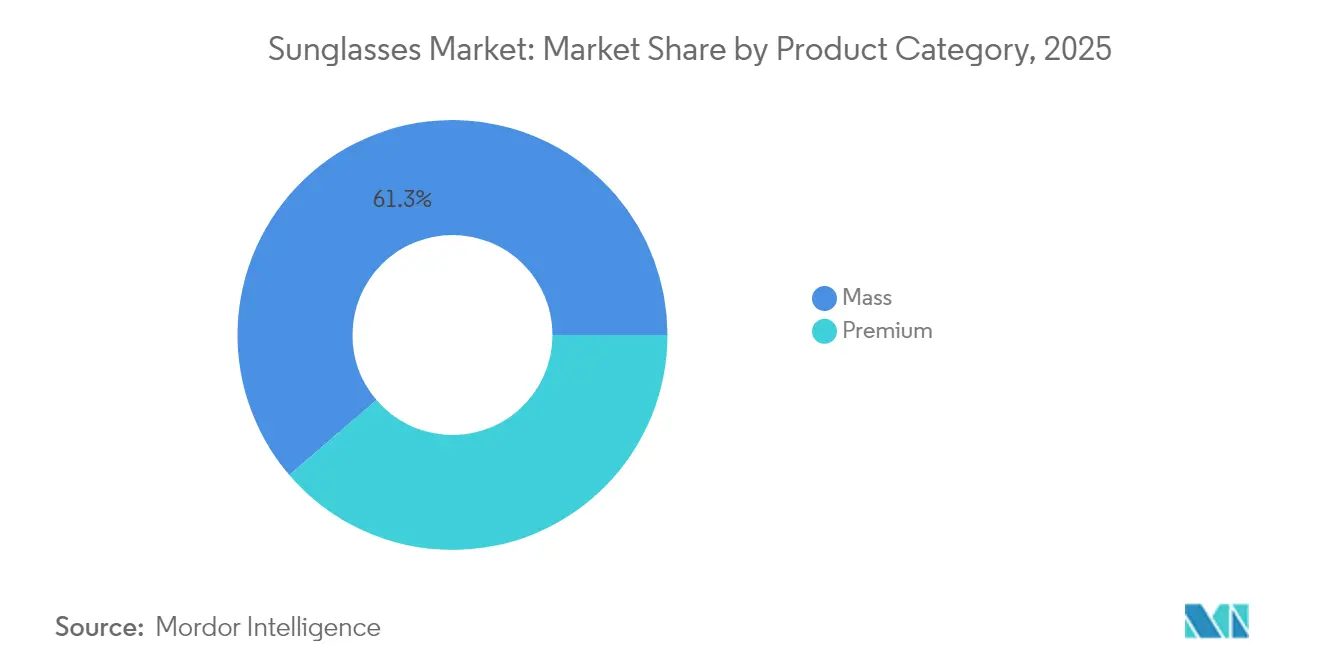

- By product category, mass offerings captured 61.28% of 2025 revenue and premium lines are projected to post a 7.05% CAGR to 2031

- By distribution channel, offline outlets delivered 74.35% of 2025 turnover and online platforms are on track for an 8.33% CAGR through 2031

- Geographically, North America commanded 32.30% market share in 2025, while Asia-Pacific is projected to grow at a 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sunglasses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness of UV protection and eye health | +1.2% | North America and Europe lead, global spillover | Medium term (2–4 years) |

| Fashion trends and rapid product cycles | +1.5% | Global, pronounced in Asia-Pacific cities | Short term (≤ 2 years) |

| Brand awareness and celebrity/social media influence | +0.9% | North America and Europe focal points | Short term (≤ 2 years) |

| Rise in outdoor activities and sports participation | +1.1% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Demand for eco-friendly bio-based frame materials | +0.7% | Europe and North America lead, Asia-Pacific rising | Long term (≥ 4 years) |

| Lens technology innovation | +1.0% | Global, faster adoption in developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising consumer awareness of UV protection and eye health

Health-conscious consumers are increasingly viewing sunglasses as essential medical devices rather than mere fashion accessories, leading to a surge in the premium segment. Reinforcing this perception, the FDA classifies sunglasses as Class I medical devices under 21 CFR 886.5842, mandating impact-resistant lenses and specific labeling standards. Meanwhile, ISO 12312-1:2022 standards ensure 100% UV protection and define transmittance categories, setting quality benchmarks that help distinguish genuine products from counterfeits. Research by The Vision Council in 2024 revealed that while only 11% of adults own sports-specific eyewear[1]Source: The Vision Council, “The Vision Council Releases Focused Insights Report in Advance of National Sunglasses Day”, visioncouncil.org, those who do express high satisfaction, especially for hiking and cycling. This discrepancy highlights a significant untapped demand as consumers shift from generic eyewear to specialized protection. Furthermore, the regulatory landscape not only offers a competitive edge to compliant manufacturers but also erects barriers against low-quality imports. As consumers become more aware of UV protection and eye health, sunglasses are evolving from mere fashion statements to vital health products, fueling market demand, spurring innovation, and expanding the consumer base.

Fashion trends and rapid product cycles

Luxury sunglasses brands capitalize on celebrity partnerships and social media influence to accelerate style turnovers, reducing traditional seasonal cycles. For Gen Z, sunglasses represent accessible luxury, driving consistent demand throughout the year beyond the typical summer season. The Paris Olympics spurred a rise in demand for sporty sunglasses, with Oakley reporting a remarkable 140% increase in searches during the event. This rapid trend evolution creates inventory management challenges for retailers but rewards brands capable of quickly converting runway trends into mass production. Fashion-conscious consumers increasingly seek limited editions and collaborative releases, compelling traditional companies in the eyewear market to adopt fast-fashion strategies. The evolving fashion trends and accelerated product cycles are transforming sunglasses into fast-moving consumer fashion goods, encouraging frequent purchases, fostering innovation, and expanding global market reach.

Brand awareness and celebrity/social media influence

Social media platforms have shifted sunglasses marketing from seasonal pushes to ongoing brand engagement, especially targeting younger audiences. Today, celebrity endorsements demand genuine integration over mere product placement, given consumers' heightened scrutiny of influencer authenticity. Companies like Warby Parker have led the way in adopting virtual try-on technology, easing the purchasing process while ensuring brand engagement through digital avenues. Features on Instagram and TikTok allow for direct purchases, sidestepping conventional retail channels and reshaping competitive landscapes. This evolution favors brands with a robust digital footprint, posing challenges to traditional models reliant on wholesale. Influencer marketing is often perceived by consumers as more authentic and trustworthy compared to traditional advertisements, fostering brand loyalty and driving repeat purchases. Effectively utilizing celebrity endorsements and social media enhances brand visibility, establishes emotional connections with target audiences, and generates strong market demand for sunglasses.

Rise in outdoor activities and sports participation

The growing popularity of outdoor activities such as hiking, cycling, and skiing is driving the demand for high-performance eyewear. These products provide UV protection, minimize glare, and enhance visibility during intense activities. According to the Sports and Fitness Industry Association, 58.6% of the U.S. population engaged in outdoor sports in 2024[2]Source: Sports and Fitness Industry Association, "2025 Sports, Fitness, and Leisure Activities Topline Participation Report", sfia.org. Casual adventurers increasingly prefer versatile lenses that adapt seamlessly from daily commutes to weekend hikes, fueling demand for multipurpose eyewear with anti-glare treatments and durable frames. Sports apparel brands expanding into eyewear licensing are leveraging cross-merchandising opportunities. By incorporating color-coordinated designs and athlete endorsements, they are effectively increasing sales. As recreational activities diversify, categories must segment offerings based on activity intensity and tailor features accordingly. These shifting dynamics are driving the growth of the global sunglasses market, in line with the rising popularity of outdoor and sports activities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit products | -0.8% | Asia-Pacific hotspots, emerging markets | Medium term (2–4 years) |

| Inventory and style obsolescence | -0.5% | Fashion-forward regions | Short term (≤ 2 years) |

| Emergence of alternative corrective solutions | -0.4% | Global | Medium term (2–4 years) |

| Regulatory scrutiny of blue-light protection claims | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit products

Counterfeit sunglasses undermine legitimate market growth by offering substandard UV protection while mimicking premium brand aesthetics. Reported cases of counterfeits in e-commerce in Italy were 509 in 2023, according to the "Ministry of the Interior, Italy[3]Source: Ministry of the Interior in Italy, "Criminal Analysis Service", governo.it. Counterfeit products typically fail ISO 12312-1:2022 standards for UV protection and impact resistance, creating consumer safety risks that damage category credibility. E-commerce platforms increasingly struggle to enforce regulations as counterfeiters enhance their ability to replicate authentic packaging and documentation. Emerging markets, characterized by higher price sensitivity, are particularly vulnerable, as consumers are more likely to purchase counterfeit alternatives. The widespread presence of counterfeit sunglasses not only threatens consumer safety but also limits growth opportunities for legitimate brands. This market fragmentation introduces low-quality products, harming the industry's overall reputation and profitability.

Inventory and style obsolescence

As fashion cycles accelerate, retailers grapple with inventory management, struggling to predict style longevity and optimal stock levels. Fast-fashion dynamics shrink traditional seasonal planning windows, compelling retailers to commit to styles before consumer preferences solidify. The luxury sunglasses market, with its focus on limited editions and collaborative releases, intensifies this challenge, as brands juggle exclusivity against volume needs. While digital-native brands like Warby Parker navigate these waters adeptly through direct-to-consumer models and data-driven demand forecasting, traditional companies reliant on wholesale find themselves more vulnerable. Mid-tier brands, caught in the crossfire, face heightened challenges: they neither possess the luxury cachet to command premium prices nor the mass-market reach to absorb inventory losses. This predicament is further complicated in regions with pronounced seasonal shifts, where unsold summer stock proves difficult to offload elsewhere.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Polarized Strength, Non-Polarized Momentum

The polarized sunglasses category commanded 81.02% of 2025 revenue due to superior glare mitigation that benefits drivers, anglers, and snow-sport enthusiasts. Within this slice of the sunglasses market, adoption by professional athletes and safety-minded motorists anchors stable demand. However, non-polarized lenses are forecasting a 6.68% CAGR (2026-2031), outpacing the broader sunglasses market. Growth stems from fashion houses that prefer color-accurate lenses to showcase frame artistry and social media aesthetics. Gen Z buyers in urban settings often regard sunglasses as interchangeable accessories, prompting purchases based on stylistic novelty rather than optical performance. Manufacturers hedge by offering swappable lens kits that let users toggle between polarized and standard options, thereby capturing value across preference cohorts.

Aesthetic freedom remains the non-polarized lenses’ strongest appeal because tint uniformity supports bold frame palettes and lens gradients. Designers leverage this flexibility to release limited-edition drops in sync with streetwear collaborations. Meanwhile, polarized suppliers add mirror coatings, hydrophobic layers, and prescription compatibility to sustain price premiums and offset commoditization. Marketing narratives increasingly position polarized items as functional tools for active lifestyles, while non-polarized models are framed as statement pieces that complement seasonal wardrobes.

By End User: Women Dominate, Kids Advance

Women represented 54.21% of 2025 purchases, a leadership owed to higher replacement cadence and fashion-forward consumption. Female shoppers often curate collections for different occasions, driving multi-pair ownership. Loyalty programs and influencer marketing tailored to style guides further lock in repeat cycles. Conversely, the kids segment will grow at a 6.27% CAGR (2026-2031) as pediatricians underscore early UV exposure risks. As parents prioritize preventive eye health, branded children’s ranges emphasize shatter-resistant lenses and hypoallergenic materials.

Women’s categories increasingly integrate adjustable nose pads and lightweight composites to enhance comfort, recognizing that many female consumers wear sunglasses alongside cosmetics or headwear. Men’s demand tends to gravitate toward sport-specific or technology-heavy models, yet remains steady rather than explosive. Kid-oriented merchandising often pairs sunglasses with themed apparel in retail sets, nudging impulse buys at checkout. Licensing with popular animation franchises also amplifies appeal without compromising safety standards.

By Product Category: Mass Volume, Premium Upswing

Mass products retained 61.28% share in 2025, underpinned by affordability and wide retail penetration. Value-oriented consumers, especially in emerging economies, gravitate toward robust construction that promises basic UV coverage at accessible prices. Premium lines, posting a 7.05% CAGR (2026-2031), capture escalating disposable incomes and aspirational gifting. Up-market collections highlight hand-polished acetate, titanium hinges, and proprietary lens formulas. Technology infusion, such as voice assistants or heads-up display projections, further validates elevated price tiers.

Mass manufacturers optimize economies of scale by centralizing production in cost-competitive regions and consolidating raw-material procurement. Packaging still meets FDA impact-resistance labeling so that functional assurances remain credible. Premium makers invest in boutique store layouts, concierge repairs, and custom engraving services to reinforce experiential value. Sustainability certifications such as bio-acetate badges furnish an additional storytelling layer that resonates with affluent, eco-conscious buyers.

By Distribution Channel: Storefront Experience, Digital Surge

Offline venues produced 74.35% of 2025 revenue because try-on fit and lens customization continue to influence conversion. Brick-and-mortar outlets also facilitate professional adjustments for prescription inserts and frame alignment, services that online platforms imitate but cannot fully replace. Yet e-commerce channels are advancing at an 8.33% CAGR (2026-2031), empowered by augmented-reality sizing tools and hassle-free returns that mitigate hesitation. Omnichannel operators such as Warby Parker integrate appointment booking, in-store pick-up, and mobile payment links to blur channel boundaries.

Physical retailers upgrade in-store diagnostics with digital lens scanners and style recommendation kiosks, elevating perceived expertise. Showroom models, where consumers browse samples and receive home-delivered finished pairs, reduce inventory storage costs yet preserve experiential touchpoints. An expanding store base and broad geographic coverage are helping major players grow offline sales worldwide. For instance, as of September 2023, EssilorLuxottica operated 3,834 corporate stores in North America, with 1,661 of these being Sunglasses Hut locations, demonstrating the continued importance of physical retail presence in the sunglasses market. Online storefronts gather extensive browsing analytics, feeding design iterations and personalized email marketing that boosts lifetime value. Regulatory guidance requiring impact-resistant disclosures applies equally across channels, incentivizing consistent quality messaging.

Geography Analysis

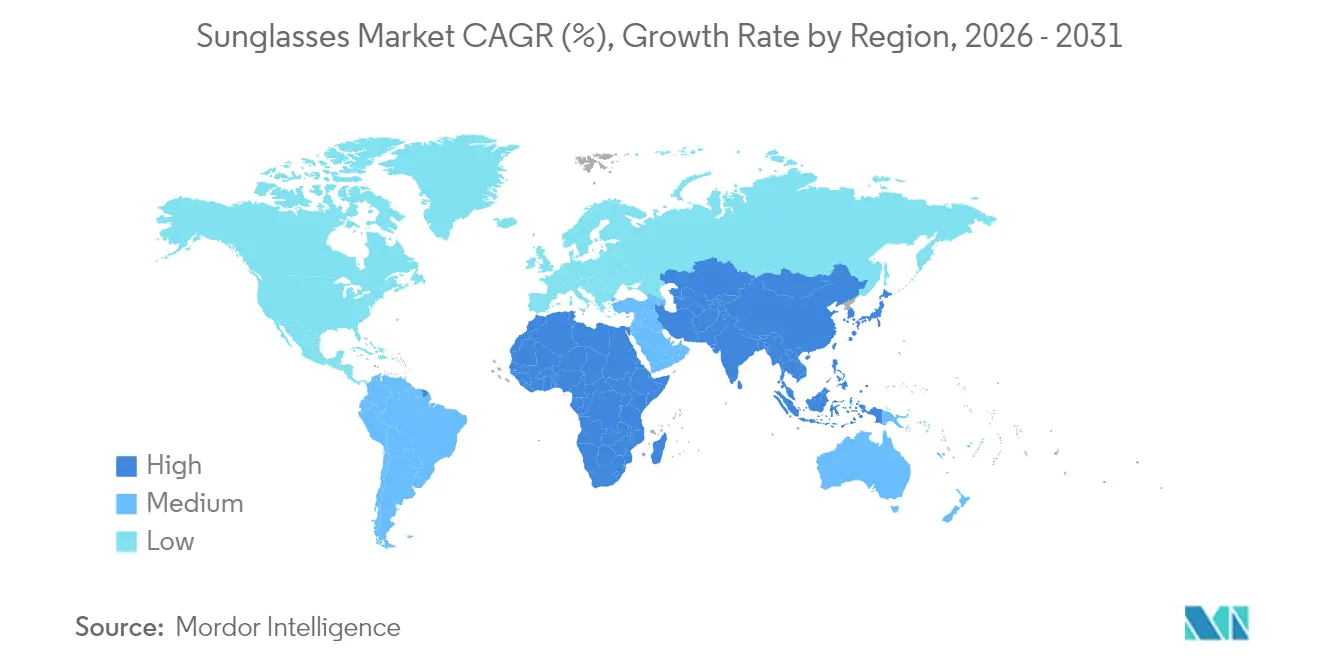

In 2025, North America contributed 32.30% of global sales, supported by robust health education efforts, an active outdoor recreation culture, and compliance with regulatory standards such as 21 CFR 886.5842, as noted by the FDA. Households regularly replace scratched or lost pairs, ensuring consistent unit turnover. The demand for prescription-ready sunwear is rising as the aging population seeks solutions that combine vision correction with glare protection. Retailers are boosting profit margins by incorporating insurance billing. Additionally, industry associations sustain public interest, even during colder months, through their annual National Sunglasses Day campaigns.

Asia-Pacific is projected to post a 7.45% CAGR to 2031, the fastest among regions. Rising middle-class purchasing power aligns with rapid urbanization, where fashion influences spread via social media. Manufacturing proximity allows brands to execute trend-responsive micro batches, shortening supply chains and reducing landed costs. However, counterfeit prevalence remains a headwind, eroding consumer trust and compressing legitimate brand margins. Governments in China and India have begun joint enforcement drives with customs agencies to intercept low-quality imports, but digital marketplace policing still lags. Europe combines heritage, luxury, sustainability leadership, and harmonized CE rules that streamline cross-border trade. Brands leverage centuries-old design legacies from Italy and France to justify premium positioning. Environmental regulations encourage rapid adoption of recycled nylon lenses and bio-based frames, aligning with younger buyer values. Optical chains in Germany and the Nordics pilot recycling programs that exchange discounts for returned end-of-life frames, embedding circular-economy practices.

South America and the Middle East and Africa remain underpenetrated yet promising. Economic volatility occasionally suppresses discretionary purchases, but improving distribution infrastructure is widening access. Duty-free zones at international airports function as trial hotspots where travelers experiment with premium models before domestic availability. Brands forging local assembly partnerships can sidestep import tariffs and reduce counterfeit risk by cutting supply lead-times.

Competitive Landscape

The global sunglasses market is moderately concentrated, with major players including EssilorLuxottica SA, Safilo Group S.p.A., Kering SA, Marcolin SpA, and De Rigo Vision S.p.A. EssilorLuxottica, at the forefront, synergistically controls lens science, frame design, and wholesale distribution, boasting an estate of over 18,000 stores. This integrated approach not only grants the conglomerate leverage over raw-material suppliers but also bolsters its marketing prowess, sustaining iconic franchises like Ray-Ban and Oakley. Furthermore, its vertical integration accelerates the rollout of innovations, such as Transitions Gen S, by compressing iteration cycles through internal research and retail feedback loops.

Kering Eyewear, Safilo Group, Marcolin, and De Rigo Vision, through licensing agreements, manage esteemed fashion labels, transforming brand equity into lucrative eyewear royalties. Meanwhile, midsized specialists carve out niches with artisanal craftsmanship or performance focus. Direct-to-consumer newcomers harness agile online platforms to offer affordable designs, using social insights to refine colorways and shapes. While the rise of smart glasses brings tech companies into the fray, established optical players retain a competitive edge with their optical-quality expertise and regulatory knowledge, areas where consumer electronics firms often falter.

Major players in the eyewear market employ strategies such as product launches, partnerships, expansions, and mergers and acquisitions to bolster their market share. For instance, in June 2025, Kering Eyewear made headlines with its acquisition of Italian manufacturer Lenti, a move aimed at expanding its industrial capacity. Such strategic maneuvers not only deepen manufacturing capabilities but also lessen dependence on third-party suppliers, provide a buffer against currency fluctuations, and safeguard intellectual property. In parallel, Safilo's decade-long licensing agreement with Victoria Beckham not only enriches its luxury portfolio but also underscores the continued viability of multi-brand licensing, especially when vertical integration poses economic challenges. Thus, the competitive landscape is shaped by the delicate balance between agile creative design and the demands of capital-intensive production.

Sunglasses Industry Leaders

-

EssilorLuxottica SA

-

Safilo Group S.p.A.

-

Kering SA

-

De Rigo Vision S.p.A.

-

Marcolin SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Safilo Group announced ten-year global licensing agreement with Victoria Beckham and renewed multi-year licensing agreement with Carolina Herrera, strengthening its luxury brand portfolio .

- June 2025: Kering Eyewear acquired Italian manufacturer Lenti, expanded its manufacturing capabilities and vertical integration strategy to compete more effectively with EssilorLuxottica's comprehensive value chain control

- December 2024: Essilor Luxottica launched Transitions Gen S and Ray-Ban Change products, representing advances in dynamic eyewear technology that combine traditional UV protection with adaptive functionality

- July 2024: Oakley introduced its latest innovation, the QNTM Kato sunglasses, during the Olympics. This launch highlights Oakley's growing association with the Olympic Games. The Olympics offer a premier global platform for athletes, making it an ideal stage to present its newest innovations.

Global Sunglasses Market Report Scope

Sunglasses are a form of protective eyewear designed primarily to prevent UV rays and high-energy visible light from damaging or discomforting the eyes. The global sunglasses market is segmented by product type, end-user, distribution channel, and geography. By product type, the market is segmented into polarized and non-polarized types. By end-user, the market is segmented into men, women, and unisex. The distribution channel is categorized into offline retail stores and online retail stores. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments. Source:

| Polarized |

| Non-Polarized |

| Men |

| Women |

| Kids |

| Mass |

| Premium |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Polarized | |

| Non-Polarized | ||

| End User | Men | |

| Women | ||

| Kids | ||

| Product Category | Mass | |

| Premium | ||

| Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the sunglasses market?

The worldwide sunglasses market size is USD 23.01 billion in 2026 and is forecast to reach USD 31.06 billion by 2031.

Which product type leads sales?

Polarized lenses lead with 81.02% of 2025 revenue, favored for glare reduction during driving and outdoor sports.

Which region is growing fastest?

Asia-Pacific shows the strongest momentum with a projected 7.45% CAGR through 2031, driven by rising middle-class consumers and fashion adoption.

How are online channels impacting sales?

E-commerce platforms are growing at an 8.33% CAGR due to virtual try-on tools and direct-to-consumer models, though offline stores still dominate volumes.

Page last updated on: