Sachet, Stick-Pack And Pouching Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

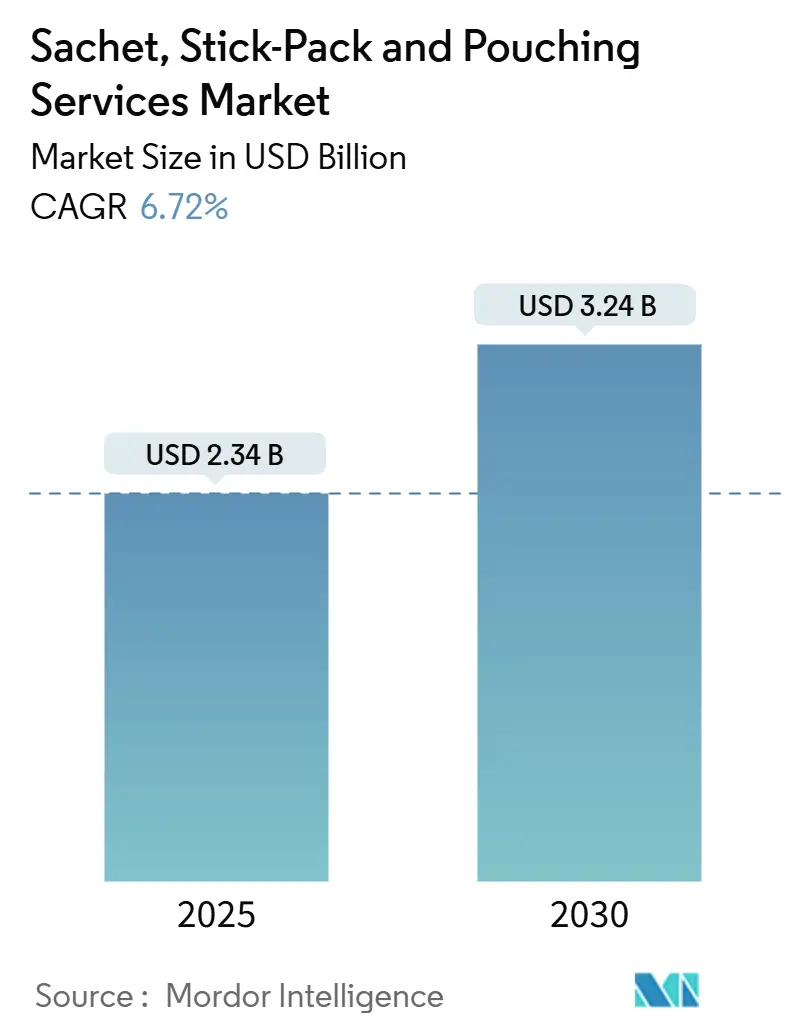

| Market Size (2025) | USD 2.34 Billion |

| Market Size (2030) | USD 3.24 Billion |

| Growth Rate (2025 - 2030) | 6.72% CAGR |

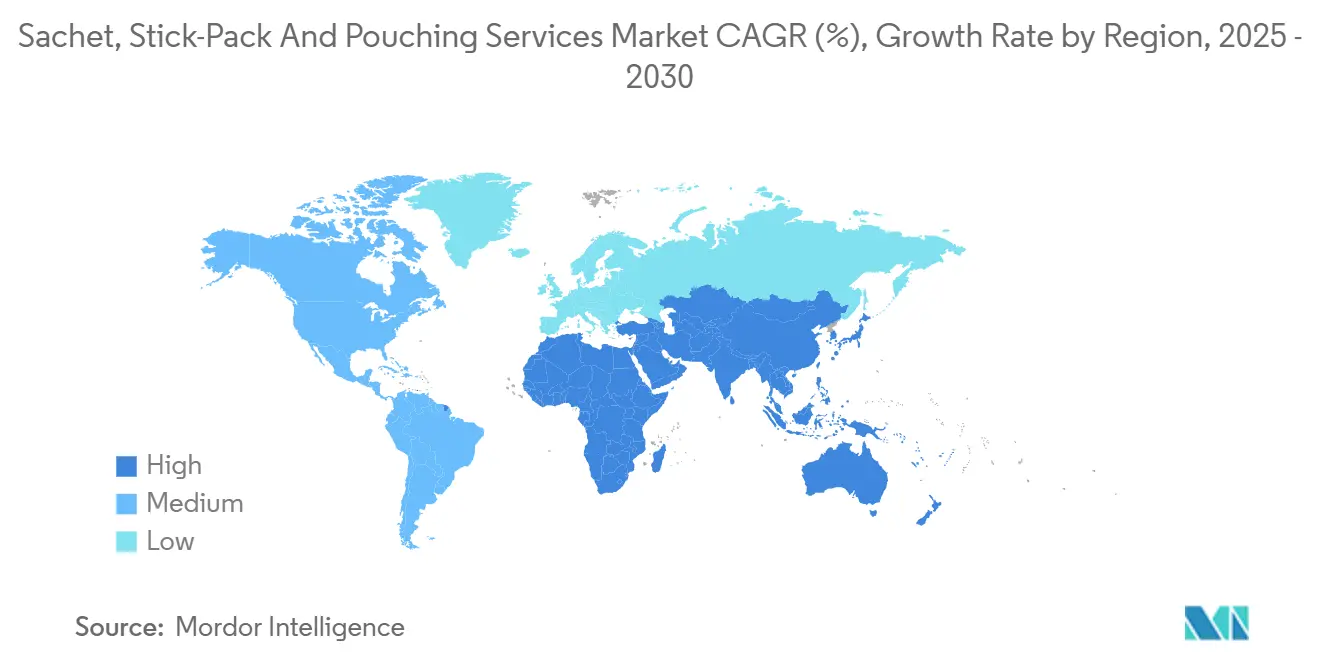

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sachet, Stick-Pack And Pouching Services Market Analysis by Mordor Intelligence

The Sachet, Stick-Pack and Pouching Services market size is estimated at USD 2.34 billion in 2025 and is projected to reach USD 3.24 billion by 2030, growing at a 6.72% CAGR over the forecast period. This solid trajectory reflects the alignment of brand and contract packers around single-serve convenience, driven by urban lifestyles, rising e-commerce penetration, and ongoing substitution from rigid containers toward flexible, portion-controlled formats. The Asia-Pacific region leads in current revenue due to its dense network of multilane filling assets, while the Middle East and Africa have the strongest growth outlook, thanks to expanding regional pharmaceutical manufacturing. Ongoing automation upgrades, sustainability-oriented material shifts, and consolidation among global flexible packaging suppliers continue to reshape cost structures, technology standards, and service portfolios. At the same time, strict regulatory regimes in healthcare, price volatility for polymer films, and shortages of skilled multilane line operators temper near-term profitability, but they also incentivize investments in digital quality controls and advanced training programs.

Key Report Takeaways

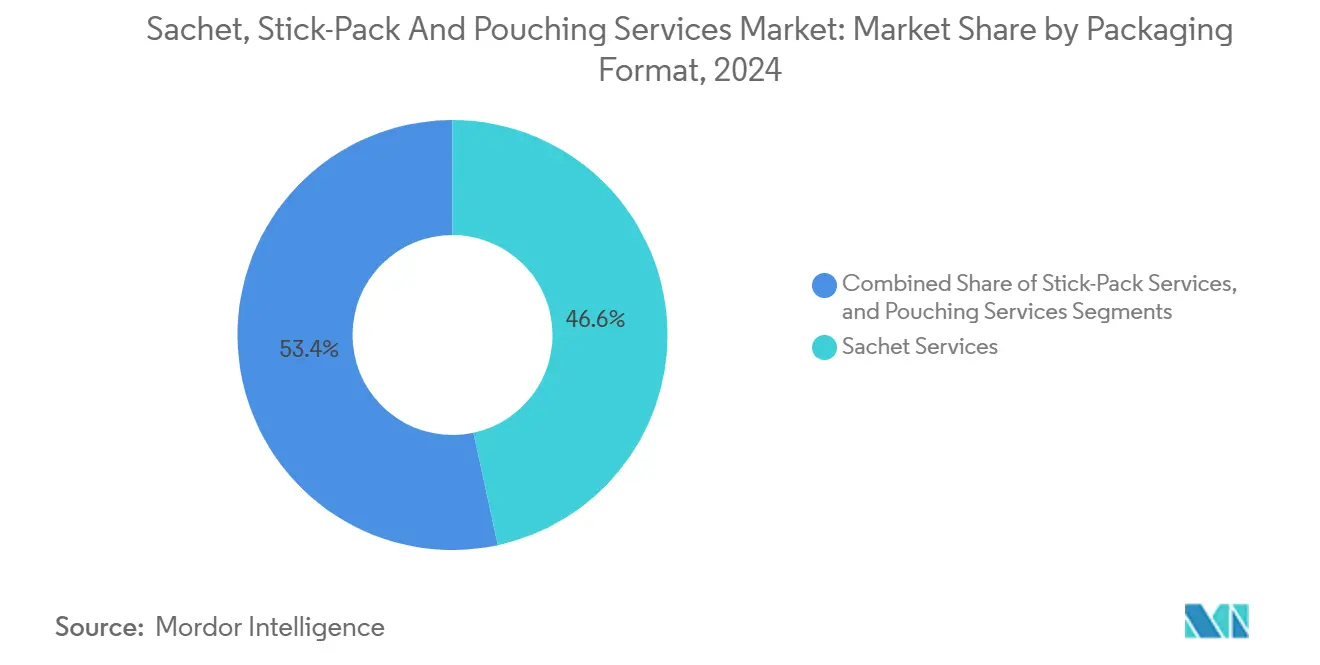

- By packaging format, Sachet Services captured 46.63% of the Sachet, Stick-Pack and Pouching Services market share in 2024.

- By filling technology, Sachet, Stick-Pack and Pouching Services market size for Stick-Pack Multilane Fillers is projected to grow at 8.05% CAGR between 2025–2030.

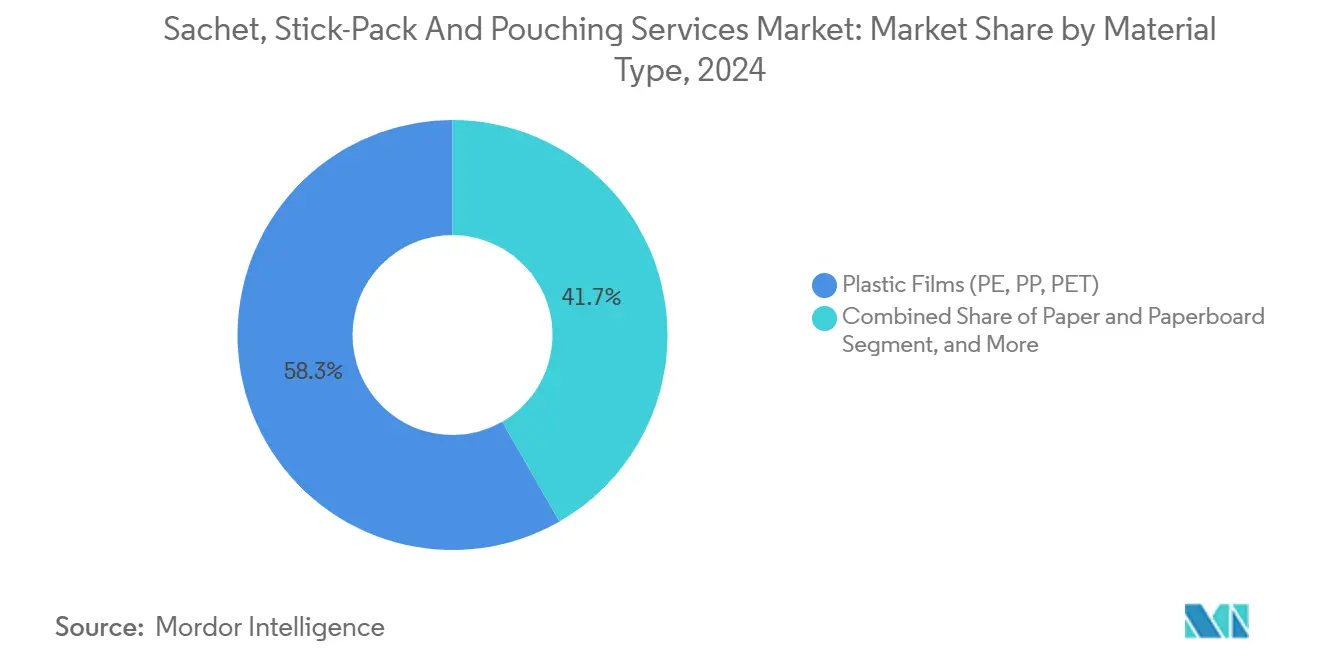

- By material type, Plastic Films captured 58.29% of the Sachet, Stick-Pack and Pouching Services market share in 2024.

- By end-user industry, Sachet, Stick-Pack and Pouching Services market size for pharmaceuticals is projected to grow at 8.93% CAGR between 2025–2030.

- By geography, Asia-Pacific captured 38.46% of the Sachet, Stick-Pack and Pouching Services market share in 2024.

Global Sachet, Stick-Pack And Pouching Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for single-serve convenience | +1.8% | Global with the strongest effect in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth of on-the-go pharmaceutical formats | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Cost efficiency versus rigid packaging | +0.9% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Expansion of e-commerce sample-size programs | +0.7% | North America and Europe, expanding into the Asia-Pacific | Medium term (2-4 years) |

| ASEAN multilane capacity build-out | +0.5% | Asia-Pacific core, spill-over to the Middle East and Africa | Short term (≤ 2 years) |

| Sustainability-linked mono-material pouches | +0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Single-Serve Convenience in Food and Beverages

Single-serve condiments, instant beverages, and seasoning packets now underpin the growth engine for co-packers serving foodservice and retail channels, providing portion control and freshness for time-pressed consumers. Asia-Pacific brand owners are increasingly outsourcing to regional service providers rather than purchasing specialized multilane machines outright, thereby freeing up capital for marketing and new-product development. E-commerce adds incremental momentum because lightweight sachets cut last-mile shipping costs while tamper-evident seals preserve product integrity. For restaurants and convenience stores, sachets reduce food waste, improve hygiene, and simplify inventory management, thereby reinforcing long-term demand even amid volatile raw material costs. In North America, contract packers market integrated design-to-fulfillment programs that combine artwork changes, short-run pilots, and rapid response for seasonal promotions, helping brands maintain shelf presence without overcommitting to inventory.

Growth of On-The-Go Pharmaceutical Dosage Formats

Leading pharmaceutical firms are embracing stick-packs to improve medication adherence, minimize dosing errors, and extend the shelf life of moisture-sensitive powders. Equipment suppliers demonstrate line speeds of up to 1,800 units per minute using servo-controlled multilane fillers, creating scale economies that narrow the cost premium relative to bottles. Post-pandemic self-care trends further lift demand for single-dose over-the-counter cold remedies, electrolytes, and functional nutraceuticals. Regulators mandate rigorous container-closure validation, so contract services with ISO 15378 and FDA-audited facilities capture a pricing premium. Growth also stems from nascent therapeutic categories, such as nasal dry-powder biologics, where precise 10-80 mg fills and ultra-low residual oxygen demand, specialized pouch films with aluminum or high-barrier EVOH layers are utilized.

Cost Efficiency Versus Rigid Packaging

Flexible packs can reduce total delivered costs by up to 22% through lighter freight weights, lower storage footprints, and reduced resin consumption per serving, a compelling proposition as packaging spend is projected to climb toward 14% of retail price by 2027. Shared co-packing lines amplify savings, as multiple brands can absorb fixed overhead across several SKUs. This efficiency resonates in emerging markets, where consumer purchasing power remains under strain, yet demand for branded packaged goods continues to climb. During global resin price spikes, larger contract packers leverage hedging strategies and multi-sourcing to stabilize input costs, whereas brand owners lacking scale rely on co-pack price transparency to manage cost volatility. Combined, these factors ensure flexible formats remain economically attractive relative to glass jars, tins, or PET bottles.

Expansion of E-Commerce Sample-Size Programs

Digitally native brands deploy 3-5 gram sachets and 10 milliliter pouches as low-risk entry points, allowing consumers to test scents, flavors, or supplement routines before purchasing full sizes. Amazon’s automated package-selection engine, for instance, matches product fragility and dimensional weight with optimally sized flexible films, lowering corrugate costs while preserving unboxing aesthetics. Personal care advertisers utilize QR-enabled sachets to link trial packs with loyalty programs, thereby driving repurchase metrics and capturing first-party data. Contract packers adapt by installing quick-change forming shoulders and digital printers that enable the switching of artwork within minutes, supporting hyper-segmented marketing campaigns. The model shifts inventory risk from the brand to the contract packer’s diversified scheduling, further boosting third-party demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile polymer film prices | -1.1% | Global, acute, where supply relies on imports | Short term (≤ 2 years) |

| Stringent pharma validation requirements | -0.8% | Global, especially developed markets | Medium term (2-4 years) |

| Shortage of skilled multilane operators | -0.6% | North America and Europe | Medium term (2-4 years) |

| Patent litigation on dosing-nozzle designs | -0.3% | Global, centered in major economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Polymer Film Prices

Sharp quarterly swings in BOPP and PET film raise working-capital needs and squeeze margins, especially for smaller contract packers lacking hedging instruments or multi-plant leverage.[1]Flexible Packaging Europe Secretariat, “Film Price Volatility Update,” flexiblepackagingeurope.org Geopolitical disruptions across shipping lanes inject further uncertainty into lead times and resin surcharges. Given that film can account for 60% of unit service cost, even modest price jumps trigger immediate renegotiations or surcharge clauses. Some service providers adopt dynamic pricing tied to commodity indexes, but brand owners resist, fearing retail price hikes. The turbulence accelerates material R&D into thinner gauges and mono-material laminates, aimed at offsetting raw material inflation while simplifying downstream recycling streams.

Stringent Pharma Validation Requirements

Current Good Manufacturing Practice (CGMP) rules drive exhaustive documentation, prolonged process qualification cycles, and continuous environmental monitoring, often extending commercial launch timelines by 6-18 months. Smaller entrants struggle with the capital expenses of cyclable cleanrooms, electronic batch records, and serialization systems required for high-risk sterile or biologic products. Legacy plants also face costly retrofits to meet ISO 8 particle controls on multilane fillers, which were originally designed for food powders. Consequently, the barrier favors established CDMOs with integrated packaging suites, limiting overall industry capacity elasticity and potentially delaying market entry for novel therapeutics if packaging partners cannot secure timely validation slots.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Format: Sachets Lead Traditional Applications

Sachets accounted for 46.63% of 2024 revenue, underscoring their entrenched use for condiments, instant beverage mixes, and culinary seasonings within the broader Sachet, Stick-Pack, and Pouching Services market share. Stick-packs, although smaller in total revenue, represent the fastest-rising format with an 8.27% CAGR, mirroring demand for precision-dosed nutraceuticals and travel-friendly pharmaceutical powders. Large co-packers operate parallel multilane machines to balance high-volume condiment sachets with narrower, higher-margin stick packs.

From a cost perspective, sachets remain the lowest entry format and hence dominate emerging-market demand for single-use oral rehydration salts and fortified sugar mixes. Stick-packs, by contrast, command a higher price per thousand units due to their hermetic, narrow seals and tear-notch precision, yet brands absorb this premium because unit-level revenues far exceed packaging costs. The evolution toward integrated desiccant channels inside stick packs further distinguishes the two formats in functional terms, providing formulators with new opportunities to extend shelf life without the need for multi-material overwraps.

By Filling Technology: VFFS Dominance Faces Multilane Challenge

Vertical Form Fill Seal platforms generated 47.56% of 2024 service revenue, offering unmatched flexibility across liquid, granule, and viscous product types within the Sachet, Stick-Pack and Pouching Services market. However, stick-pack multilane fillers, projected at an 8.05% CAGR, attract capex because they achieve compact footprints, servo-indexed draws, and rapid lane-count scaling for pharmaceutical contracts demanding million-unit batch sizes. Robotics-assisted secondary loading enhances overall equipment effectiveness, while vision-guided inspection systems detect seal defects in real-time, reducing rework.

Despite a higher upfront cost, multilane technology generates a lower unit cost above break-even volumes of roughly 250,000 packs per SKU, a threshold increasingly common for global supplement brands. As labor constraints intensify, particularly in the United States and Europe, service providers are retrofitting collaborative robots for case packing and palletizing, thereby reducing headcount needs and enhancing line availability. VFFS retains niche relevance for viscous sauces and cosmetics that require longer dwell times and heavier film gauges; yet most new pharmaceutical and nutraceutical installations favor multilane given its faster payback under contract manufacturing fee models.

By Material Type: Plastic Films Lead Sustainability Transition

Plastic films accounted for 58.29% of the total packaging material spend in 2024 across the Sachet, Stick-Pack, and Pouching Services market, leveraging proven barrier and sealing performance at a competitive cost. Regulatory and brand pressure accelerate the adoption of biodegradable and recyclable mono-material films, which show a 9.17% CAGR trajectory despite a higher price per kilogram. Co-packers collaborate with suppliers on blueloop PE-based laminates and PP-barrier variants to meet Extended Producer Responsibility fees anticipated in several U.S. states by 2027.[2]PMMI Business Intelligence, “Brand Owners Rely on Contract Manufacturing,” pmmi.org

Paper-based laminates grow modestly where grease resistance and moisture exposure are low, appealing to premium organic tea and spice brands seeking plastic-free claims. Aluminum foil laminates, although costly, retain critical importance for oxygen-sensitive pharmaceuticals and probiotic powders that require oxygen transmission rates of less than 0.1%. To mitigate sustainability cost gaps, some co-packers employ downgauging, which involves decreasing film thickness by 12-15% without sacrificing mechanical performance, thereby generating substantial resin savings and lowering Scope 3 emissions for brand customers.

By End-User Industry: Food Leads, Pharma Accelerates

Food and Beverages contributed 44.47% of 2024 revenue, solidifying their position as the largest segment in the Sachet, Stick-Pack, and Pouching Services market. High-volume condiment sachets for quick-service restaurants and single-serve coffee powders for retail drive baseline machine utilization. Meanwhile, Pharmaceuticals deliver the steepest 8.93% CAGR as single-dose therapies and adherence initiatives migrate toward flexible unit-dose packages that simplify dispensing and reduce microbial exposure.

Personal care brands sustain steady demand for fragrance samplers and skin-care trial packs, often featuring metallicized PE or recyclable PET-PE structures to ensure barrier integrity against volatile oils. Home care brands adopt pouching for enzyme-based laundry concentrates shipped in refill kits, capitalizing on e-commerce parcel rules that favor lightweight, leak-resistant formats. Across industries, SKU proliferation encourages shorter production runs, enhancing the relative competitiveness of contract packers who deploy rapid tool-less changeovers and late-stage digital printing.

Geography Analysis

The Asia-Pacific region accounts for 38.46% of global revenue, underpinned by high-density networks of sachet and stick-pack multilane lines serving both multinational and regional consumer goods groups. The region’s contract packers leverage cost-competitive labor, robust supplier ecosystems, and proximity to raw film producers to offer compelling export solutions, particularly for seasoning blends and OTC supplements. China and India dominate output volumes, while Vietnam, Indonesia, and Thailand are showing rising capacity additions, encouraged by government incentives and free-trade access to major food and pharmaceutical importers.

The Middle East and Africa, while currently a mid-single-digit revenue contributor, are projected to post an 8.56% CAGR through 2030, as Saudi Arabia, Egypt, and South Africa invest in local pharmaceutical fill-finish plants. Flexible packaging aligns with regional infrastructure realities, where cold-chain gaps, long transport distances, and fragmented retail networks favor lightweight, tamper-evident packaging. European machinery suppliers have partnered with Gulf-based CDMOs to install humidity-controlled stick-pack suites targeting export-grade oral rehydration salts, positioning the region as a nascent hub for African demand.

North America and Europe maintain sizeable, technology-intensive footprints driven by healthcare and premium food contracts requiring GMP compliance and serialized traceability. Labor shortages prompt accelerated automation, with lines integrating vision-guided robotics that raise overall equipment effectiveness by up to 80%. The mature customer base prioritizes agility and value-added engineering support, enabling contract packers to charge 10-15% service premiums over Asia-based alternatives for high-complexity SKUs. Nonetheless, near-shoring of consumer brands seeking shorter lead times spurs incremental volume repatriation to both regions, particularly for nutraceutical sachets and beauty samplers.

Competitive Landscape

The Sachet, Stick-Pack and Pouching Services market remains moderately fragmented, although consolidation is accelerating as scale, automation, and sustainability investments demand larger balance sheets. Amcor’s pending USD 8.43 billion acquisition of Berry Global merges two flexible packaging heavyweights, creating a combined research budget of roughly USD 180 million and broadening global co-packing reach. Contract-focused specialists, such as Econo-Pak and PCI Pharma Services, expand their square footage and technology portfolios to capture incremental shares in the food and drug segments, respectively.[3]Packaging Strategies Staff, “Merger of Two Titans,” packagingstrategies.com

Technology differentiation represents a key battleground: leaders deploy AI-driven quality inspection, in-line NIR spectroscopy for blend verification, and cloud-based OEE dashboards that provide real-time visibility to brand clients. Sustainability credentials, particularly in mono-material recycling trials and downgauging expertise, underpin long-term customer retention and pricing leverage. Pharmaceutical-grade operators also invest in serialization lines and digital batch record systems, thereby widening the compliance gap compared to generalist food sachet fillers.

Emerging disruptors target white-space niches such as nasal dry-powder biologics, retort-pouch probiotics, and post-consumer recycled film sachets. These entrants often partner with equipment OEMs to pilot proprietary dosing nozzles or to embed RFID/NFC inlays compatible with at-home adherence apps. While their revenue share remains limited today, their innovation pace pressures incumbents to accelerate R&D cycles and expand small-run flexible production suites.

Sachet, Stick-Pack And Pouching Services Industry Leaders

Assemblies Unlimited Inc.

Sharp Services, LLC

Ropack Pharma Solutions Inc.

Catalent Pharma Solutions Inc.

Glenroy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The International Journal of Pharmaceutical Sciences highlighted rising adoption of single-dose stick-packs and integrated RFID/NFC tamper-evident features in pharmaceutical packaging innovations.

- February 2025: Amcor completed the acquisition of Berry Global Group for USD 8.43 billion, creating a global leader in consumer packaging solutions with a combined annual R&D investment of USD 180 million. The transaction is expected to close mid-2025 pending regulatory approvals.

- December 2024: Econo-Pak expanded its Milford, Pennsylvania facility by 125,000 square feet, installing advanced food packaging automation lines to meet growing demand for high-volume co-packing services.

- September 2024: PCI Pharma Services committed over USD 365 million to new and expanded EU and U.S. sites for drug-device combination packaging, including a 545,000 square-foot project in Rockford, Illinois.

Global Sachet, Stick-Pack And Pouching Services Market Report Scope

| Sachet Packaging Services |

| Stick-Pack Packaging Services |

| Pouching Packaging Services |

| Plastic Films (PE, PP, PET) |

| Paper and Paperboard |

| Aluminum Foil Laminate |

| Biodegradable Films |

| Vertical Form Fill Seal (VFFS) |

| Horizontal Form Fill Seal (HFFS) |

| Pre-made Pouch Fill and Seal |

| Stick-Pack Multilane Fillers |

| Food and Beverages |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Home Care and Industrial |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Packaging Service Format | Sachet Packaging Services | ||

| Stick-Pack Packaging Services | |||

| Pouching Packaging Services | |||

| By Material Type | Plastic Films (PE, PP, PET) | ||

| Paper and Paperboard | |||

| Aluminum Foil Laminate | |||

| Biodegradable Films | |||

| By Filling Technology | Vertical Form Fill Seal (VFFS) | ||

| Horizontal Form Fill Seal (HFFS) | |||

| Pre-made Pouch Fill and Seal | |||

| Stick-Pack Multilane Fillers | |||

| By End-user Industry | Food and Beverages | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Home Care and Industrial | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the expected revenue for sachet and stick-pack contract services in 2030?

The Sachet, Stick-Pack and Pouching Services market is projected to reach USD 3.24 billion by 2030, reflecting a 6.72% CAGR from 2025.

Which region currently generates the highest revenue?

The Asia-Pacific region leads with a 38.46% share, owing to its extensive multilane filling infrastructure and strong demand for consumer goods.

Which packaging format shows the fastest growth?

Stick-Pack Services are expected to register the quickest pace at an 8.27% CAGR through 2030, primarily driven by demand from the pharmaceutical and nutraceutical sectors.

How do volatile resin prices affect contract packers?

Film costs can account for up to 60% of service expenses, so price fluctuations directly impact margins unless pass-through mechanisms or hedging strategies are in place.

Why do single-dose formats gain traction in pharmaceuticals?

Stick-packs improve dosing accuracy, enhance medication adherence, and meet stringent barrier requirements, making them an attractive option for self-administered therapies.

What sustainability initiatives are most common among leading co-packers?

Downgauging film thickness, adopting mono-material recyclable laminates such as blueloop, and integrating post-consumer recycled resins are the primary focus areas for reducing environmental impact.

Page last updated on: