Spouted Pouches And Fitments Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

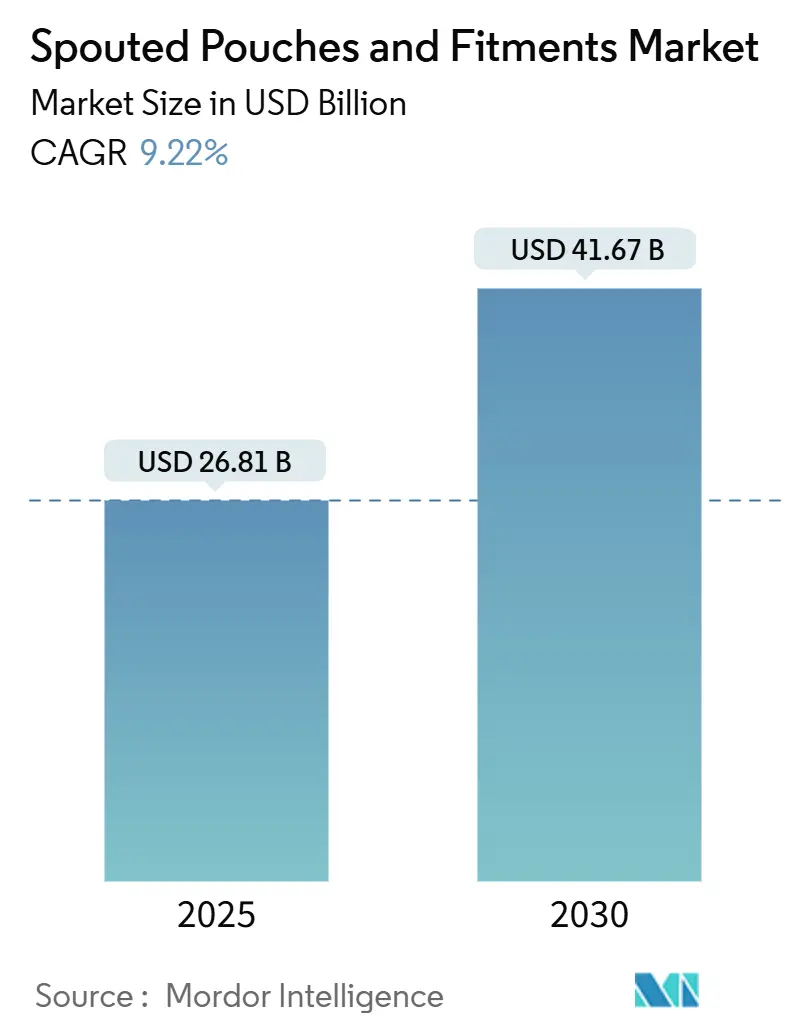

| Market Size (2025) | USD 26.81 Billion |

| Market Size (2030) | USD 41.67 Billion |

| Growth Rate (2025 - 2030) | 9.22% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spouted Pouches And Fitments Market Analysis by Mordor Intelligence

The spouted pouches and fitments market size is valued at USD 26.81 billion in 2025 and is forecast to reach USD 41.67 billion by 2030, advancing at a 9.22% CAGR. Demand accelerates as brands pivot from rigid formats toward flexible options that are lighter, safer during transit, and easier to open. Improvements in aseptic filling now enable the production of shelf-stable products without refrigeration, while mono-material barrier films alleviate recycling bottlenecks. Retailers favor the format because it travels well through e-commerce networks, lowers shipping costs, and cuts damage rates. Regulatory initiatives that limit the use of single-use plastics add further momentum, prompting rapid investment in bio-based substrates and recyclable closures. At the same time, global consumer lifestyles require portable, portion-controlled packs that can travel from stroller cup holders to remote job sites without leaking.

Key Report Takeaways

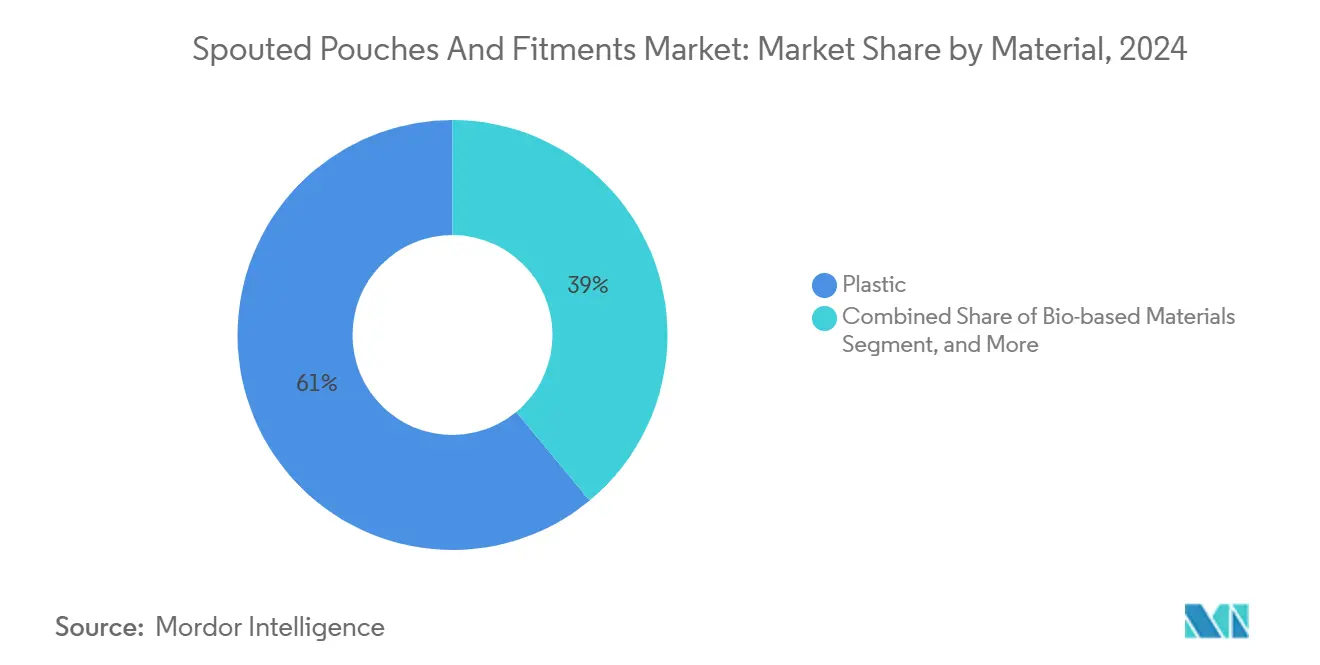

- By material, plastic captured 61.01% of the spouted pouches and fitments market share in 2024.

- By product configuration, the spouted pouches and fitments market size for side-gusseted formats is forecast to advance at a 10.87% CAGR between 2025 and 2030.

- By spout type, screw caps captured 52.23% of the spouted pouches and fitments market share in 2024.

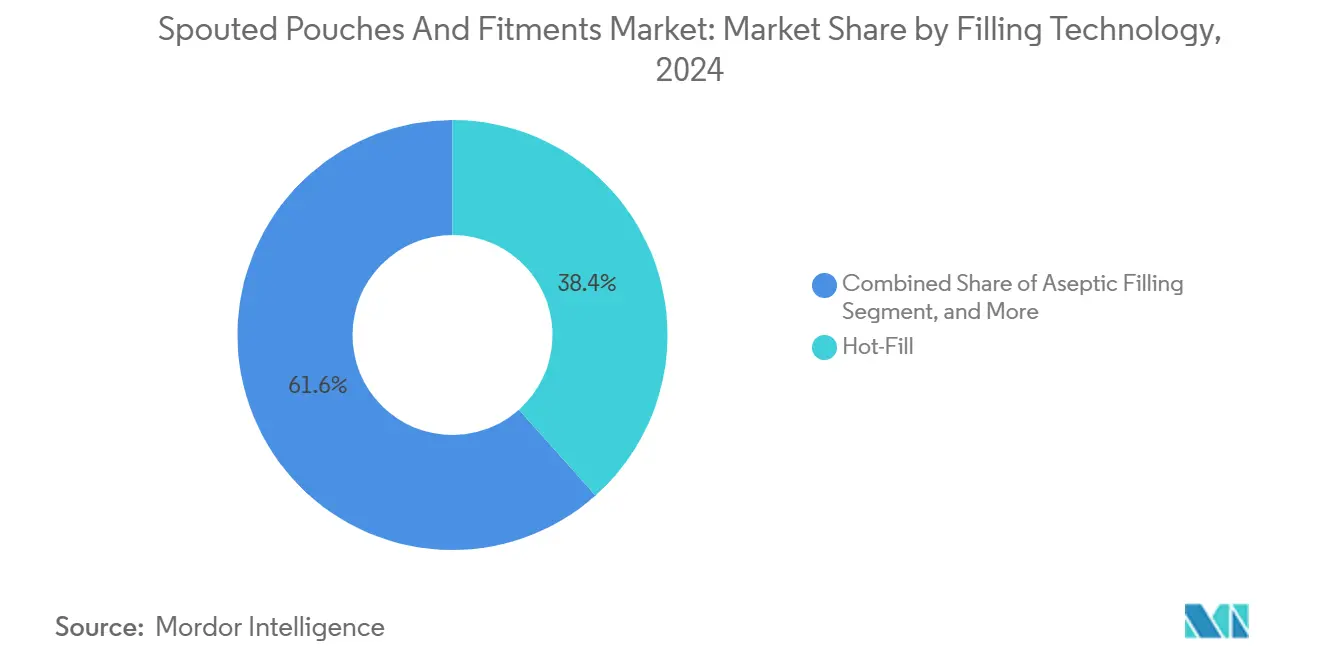

- By filling technology, the spouted pouches and fitments market size for aseptic systems is forecast to advance at a 10.49% CAGR through 2030.

- By application, food and beverage captured 60.51% of the spouted pouches and fitments market share in 2024.

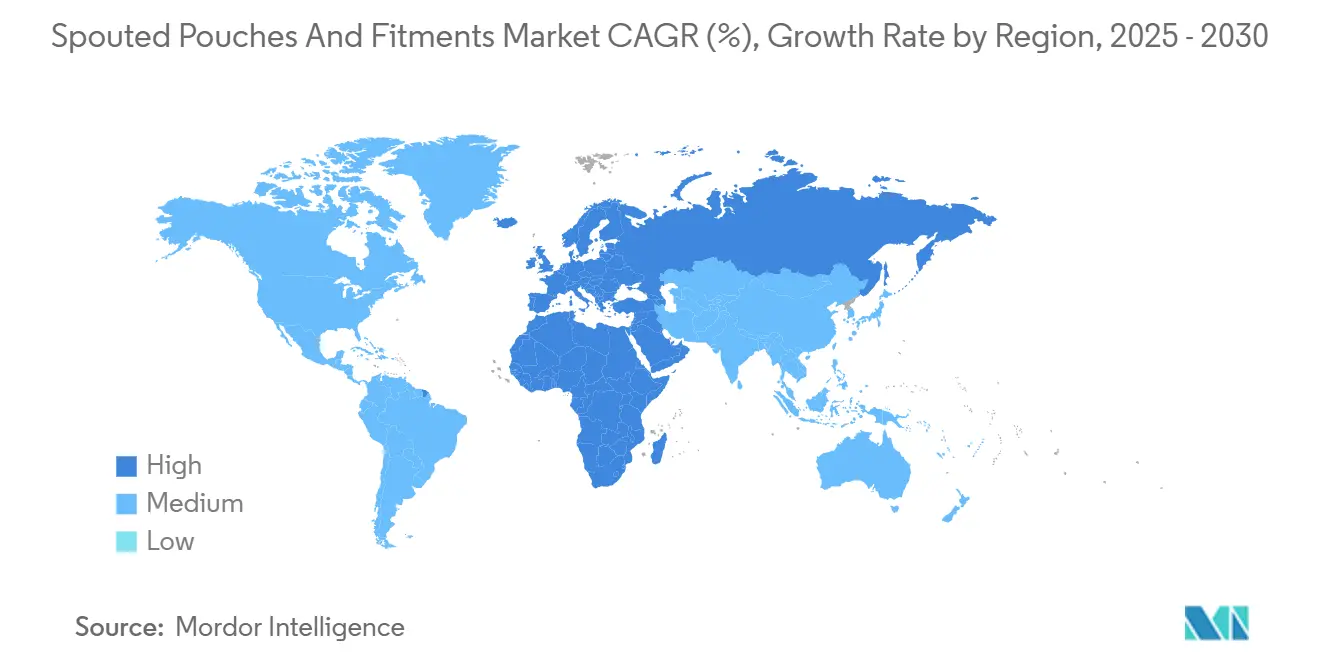

- By geography, the spouted pouches and fitments market size for Europe is forecast to advance at an 11.21% CAGR through 2030.

Global Spouted Pouches And Fitments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Convenient Baby Food Packaging | +1.8% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Growth of E-Grocery and Direct-to-Consumer Channels | +2.1% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Sustainable Lightweighting Imperatives | +1.6% | EU and North America core, expanding to APAC | Long term (≥ 4 years) |

| Fitment-Enabled Refill Models for Household Cleaners | +1.4% | North America and EU, pilot expansion to APAC | Medium term (2-4 years) |

| Pharmaceutical Adoption for Dose-Controlled Liquids | +1.2% | Global, timelines vary by region | Long term (≥ 4 years) |

| Emerging Cold-Chain Barrier Film Innovations | +1.1% | Global, temperature-sensitive goods | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient Baby Food Packaging

Parents want squeeze-and-serve meals that reduce utensil use and cut food waste. Brands respond with tamper-evident, choke-safe fitments that pass strict FDA contact rules, enabling on-the-go feeding in cars, parks, and day-care settings.[1]Tenco, “Pouchélite Manual Monoblock machine for spouted pouches,” Tenco, tenco.it Online grocery orders amplify the shift because flexible packs travel intact, whereas glass jars often break. Suppliers that certify both barrier safety and child-resistant design win bids from retailers rolling out private-label organic blends.

Growth of E-Grocery and Direct-to-Consumer Channels

Fulfillment centers prefer formats that cube efficiently and ship at low mass. Spouted pouches reduce void fill needs and arrive intact, maintaining high review ratings for fragile liquids. Start-up food brands leverage web sales to debut premium recipes in corner-spout packs that would fight for shelf space in stores. Extra space on the pouch exterior doubles as a marketing canvas, replacing in-store signage with bold, high-resolution graphics that travel straight to the doorstep.

Sustainable Lightweighting Imperatives

Corporate ESG scorecards push reductions in transport emissions and raw polymer use. Thinner mono-material films now equal conventional laminates in terms of puncture resistance, while reducing weight without sacrificing shelf life. Guala Pack’s all-polypropylene designs demonstrate drop-in recyclability with the rigid PP stream, easing take-back compliance in Western Europe.[2]Guala Pack, “Refill pouches are 3X sustainable,” Guala Pack, gualapack.com Brands insist on life-cycle data from suppliers to validate carbon savings, turning material science into a key differentiator.

Fitment-Enabled Refill Models for Household Cleaners

Concentrated detergents are dispensed into rigid containers at home, while lightweight refill pouches reduce plastic waste by up to 80%. Early pilots by Cleancult replaced single-use jugs with foil-lined flexibles that consumers snip, pour, and recycle curbside, where programs accept mono-polyolefins. Logistics partners experiment with closed-loop retrieval, utilizing UVC sterilization, which allows pouches to reenter the supply chain multiple times, thereby improving cost-per-use economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Multilayer Film Raw-Material Prices | -1.3% | Global, high hit to cost-sensitive segments | Short term (≤ 2 years) |

| Limited Recyclability of Laminate Structures | -0.9% | EU and North America, expanding worldwide | Medium term (2-4 years) |

| Capital Intensity of Aseptic Spout-Seal Machinery | -0.7% | Global, burdens SMEs | Long term (≥ 4 years) |

| Counterfeit Fitment Failures in Low-Cost Markets | -0.5% | Asia-Pacific and emerging regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Multilayer Film Raw-Material Prices

Rapid swings in polyethylene and polypropylene markets compress converter margins in food staples where packaging can equal double-digit cost of goods. Vertically integrated players hedge resin exposure through backward contracts, yet smaller firms struggle to pass highs onto private-label customers. Price uncertainty also pauses pilot runs for premium barrier layers that command extra cents per unit, stretching commercialization timelines.

Limited Recyclability of Laminate Structures

High-barrier laminates, such as those used to protect tomato purée or automotive fluids, rarely enter closed-loop recycling because regional sorting centers cannot separate the nylon, aluminum, and PET layers.[3]Ecover and Basis Research, “The Refillution Has Begun,” Ecover, storyblok.com European extended producer responsibility rules impose fees tied to end-of-life performance, raising operating costs for brands that cling to complex supply chains. The tension sparks research in chemical recycling and single-polymer oxygen barriers, though scale-up gaps keep collection rates low in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Drives Innovation

Plastic commanded 61.01% spouted pouches and fitments market share in 2024, anchored by polyethylene that seals at low temperatures and resists chemicals. Polypropylene expands in sauces that need hot-fill tolerance. The spouted pouches and fitments market size for plastics is on track for steady mid-single-digit growth as converters roll out thinner gauges that preserve dart impact performance. Bio-based polymers lead the growth chart at an 11.29% CAGR, helped by brand promises to phase out fossil feedstocks. Paper-plus-bio-coating skews to dry goods, while aluminum remains in premium coffee concentrates that demand near-zero oxygen ingress.

Manufacturers are moving toward mono-material pouches that coextrude tie layers inside PE or PP families, allowing for curbside recycling in North America and pilot sort lines in Europe. FDA food contact norms mandate migration testing, so suppliers perform exhaustive analysis to certify new resin blends. In the Asia-Pacific region, government grants offset capex for solvent-less adhesive lines that bond thin barriers without VOC emissions.

By Product Configuration: Stand-Up Formats Lead Market

Stand-up designs delivered a 58.39% share in 2024, favored by retailers because they display branding on the shelf while occupying a compact space in shippers. Side gusseted variants record the quickest 10.87% CAGR as their flat-bottom profile maximizes pallet density for e-commerce warehouses. The spouted pouches and fitments market size for side gusseted pouches is expected to double by 2030, as logistics costs per liter become a strategic KPI.

Flat formats hold a niche in sample trials and single-serve condiments where economics rule. A hybrid stand-up with corner gussets emerges for motor oil and windshield fluids, providing rigidity for garage settings. Equipment makers integrate servo-controlled taping that inserts spouts without manual touch, cutting labor hours and defect rates.

By Spout Type: Screw Caps Maintain Functional Leadership

Screw caps retained a 52.23% share of the spouted pouches and fitments market in 2024, as users trust the click-tight seal and reseal function. Brands also rely on wide industrial availability and child-resistant options. Corner spouts project an 11.79% CAGR, driven by beverage makers that want drip-free pours when consumers drink from the edge. Flip tops remain relevant in condiments that require one-handed squeezing, while straw-insert nozzles gain popularity among seniors who need controlled dosing.

Tooling houses innovate self-venting screw closures that equalize pressure in hot-filled fruit purées. Patents filed in 2024 outline overload stops that prevent cross-threading to maintain low complaint rates. Recyclers advocate for single-polymer spouts to ensure caps can remain attached and pass through sortation without contamination.

By Filling Technology: Hot-Fill Leads Processing Methods

Hot-fill accounted for 38.41% of the 2024 global revenue, as it balances capital costs and microbiological safety for acidified foods. Aseptic systems, although lower in share, post the fastest 10.49% CAGR. Producers targeting premium smoothies and pharmaceutical syrups switch to aseptic lines to avoid thermal flavor loss and gain longer ambient shelf life. The spouted pouches and fitments market size for aseptic formats is expected to touch high single-digit billions by 2030.

Retort pouches stay relevant for baby purées in Japan, whereas ambient fill targets household cleaners where shelf fungi risk is minimal. System builders like SIG bundle in-line sterilization, which cuts the need for pre-made pouch purchases, helping plants lower their consumable inventory. Engineers also roll out clean-in-place loops that shorten downtime between flavor changeovers.

By Application: Food and Beverage Dominance Faces Growth Competition

Food and beverages held a 60.51% market share in 2024 and are expected to remain the anchor category through 2030. Baby food, ready-to-eat grains, and yogurt drinks rely on easy squeeze-and-sip access. The spouted pouches and fitments market size for food and beverage applications benefits from next-generation corner spouts that allow for a controlled flow rate for thick purées, preventing mess.

Home and personal care posts the fastest 10.31% CAGR as refill models convert rigid detergent bottles into at-home dispensers. Shampoo bars dissolved in concentrate also flow into spouted refill packs. Industrial segments, such as lubricants, utilize large-volume fitments to minimize glugging and spillage, while pharmaceutical firms pilot single-dose pouches for rehydration salts in disaster zones.

Geography Analysis

The Asia-Pacific region represented 41.6% of global demand in 2024, underpinned by manufacturing clusters in China, India, and Thailand that operate at low unit costs. In Europe, the spouted pouches and fitments market size is projected to grow at a 11.21% CAGR through 2030, as cross-border e-commerce expands into tier-2 cities. Governments fund flexible-pack training centers, aiding small firms that supply local sauce brands.

North America and Europe exhibit slower unit growth, yet they shape regulatory standards for recyclable mono-structures and child-safe closures. FDA rulings on per- and polyfluoroalkyl substances push suppliers to drop fluorinated barriers, while European single-use plastic laws tax multilayer pouches. Brands meet mandates through PE-only laminates combined with EVOH in-layer oxygen sinks, maintaining a high barrier level while passing recyclability audits.

South America, the Middle East, and Africa contribute a smaller volume today, yet rising urbanization and reliance on shelf-stable imports build momentum. Brazilian fruit concentrate exporters opt for flexible packaging to reduce freight weight, while Gulf Cooperation Council importers prioritize long ambient life in desert climates. African dairy cooperatives are adopting corner spouts on aseptic milk pouches to withstand broken cold-chain events. Local manufacturing capacity expands as foreign OEMs lease modular fill-seal skids that drop into brownfield plants.

Competitive Landscape

The field remains moderately fragmented, with the top five owners below the 40% threshold. Global heavyweights AptarGroup, Gualapack, and Amcor integrate resin compounding, film extrusion, and spout molding under one roof to control cost and lead time. They court multinationals with turnkey lines that include logistics data, carbon scorecards, and design labs.

Mid-tier contenders specialize in niche technologies, such as ultrasonic spout-seal technology that bonds mono-PE without adhesives, thereby trimming cycle time. Equipment suppliers ALLIEDFLEX and Effytec license new servo platforms for corner spout insertion, which reduce changeover times, appealing to co-packers serving short-run digital campaigns. Start-ups tackle refill ecosystems, offering RFID tags that track pouch life cycles and issue deposit refunds once consumers return empties.

Patent filings cluster around dosing valves for medical nutrition and overload-protected screw caps for thick oils. Partnerships accelerate: resin majors team with closure molders to ensure polymer match, while e-commerce platforms feed damage-rate data back to pack designers for iterative improvement.

Spouted Pouches And Fitments Industry Leaders

AptarGroup Inc.

Gualapack S.p.A.

Amcor plc

Mondi plc

Glenroy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mondi partnered with Sherwin-Williams on refill stand-up pouches that replace 5-liter rigid paint cans.

- January 2025: Cheer Pack North America and Amcor launched an all-polyethylene pouch for Once Upon a Farm baby food, enabling recyclable curbside collection.

- October 2024: ALLIEDFLEX secured exclusive North American rights for Scaldopack spout insertion equipment, widening access for rigid-to-flexible converters.

- October 2024: Effytec, Dukane, and Hoffer Plastics co-developed ultrasonic sealing tech for mono-material PE pouches, elevating line speed and seal integrity.

Global Spouted Pouches And Fitments Market Report Scope

| Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Paper | |

| Aluminum Foil Laminate | |

| Bio-based Materials |

| Stand-up Spouted Pouches |

| Flat Pouches with Fitments |

| Side Gusseted Pouches |

| Screw Caps |

| Flip Top Caps |

| Nozzle with Straw |

| Corner Spouts |

| Aseptic Filling |

| Hot-Fill |

| Retort |

| Ambient Fill |

| Food and Beverage | Baby Food |

| Sauces and Condiments | |

| Dairy Products | |

| Beverages | |

| Ready-to-Eat Meals and Soups | |

| Home and Personal Care | Liquid Detergents |

| Hand Soap and Sanitizers | |

| Cosmetics and Toiletries | |

| Industrial | Automotive Fluids |

| Agricultural Chemicals | |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material | Plastic | Polyethylene (PE) | |

| Polypropylene (PP) | |||

| Polyethylene Terephthalate (PET) | |||

| Paper | |||

| Aluminum Foil Laminate | |||

| Bio-based Materials | |||

| By Product Configuration | Stand-up Spouted Pouches | ||

| Flat Pouches with Fitments | |||

| Side Gusseted Pouches | |||

| By Spout Type | Screw Caps | ||

| Flip Top Caps | |||

| Nozzle with Straw | |||

| Corner Spouts | |||

| By Filling Technology | Aseptic Filling | ||

| Hot-Fill | |||

| Retort | |||

| Ambient Fill | |||

| By Application | Food and Beverage | Baby Food | |

| Sauces and Condiments | |||

| Dairy Products | |||

| Beverages | |||

| Ready-to-Eat Meals and Soups | |||

| Home and Personal Care | Liquid Detergents | ||

| Hand Soap and Sanitizers | |||

| Cosmetics and Toiletries | |||

| Industrial | Automotive Fluids | ||

| Agricultural Chemicals | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the spouted pouches and fitments market in 2025?

The market is valued at USD 26.81 billion in 2025.

What is the forecast CAGR through 2030?

The market is expected to grow at 9.22% each year up to 2030.

Which region accounts for the highest consumption?

Asia-Pacific leads with 41.6% share of global volume in 2024.

Which application is growing the fastest?

Home and personal care products show the quickest climb at a 10.31% CAGR through 2030.

Why are side gusseted pouches gaining popularity?

They boost cube efficiency for e-commerce shipments and therefore lower logistics cost.

How do brands improve recyclability of spouted pouches?

They shift to mono-material PE or PP films and design tethered closures that pass curbside sortation programs.

Page last updated on: