Sachet Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.52 Billion |

| Market Size (2031) | USD 14.62 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

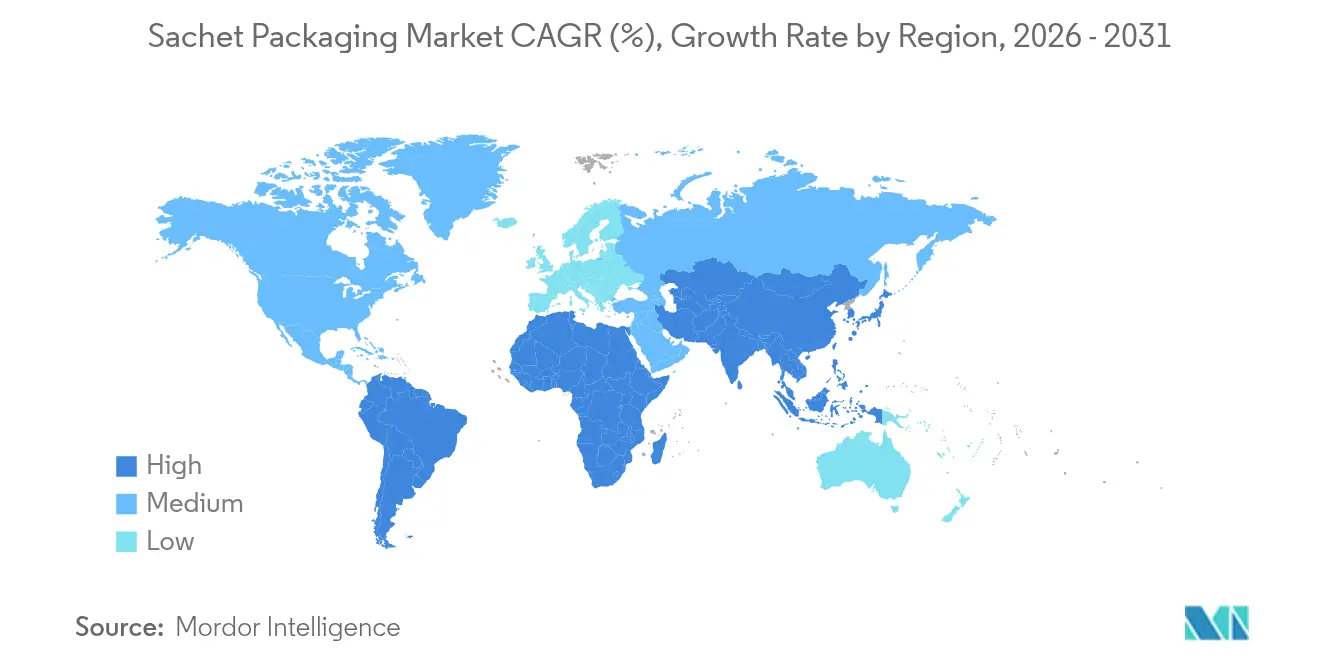

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

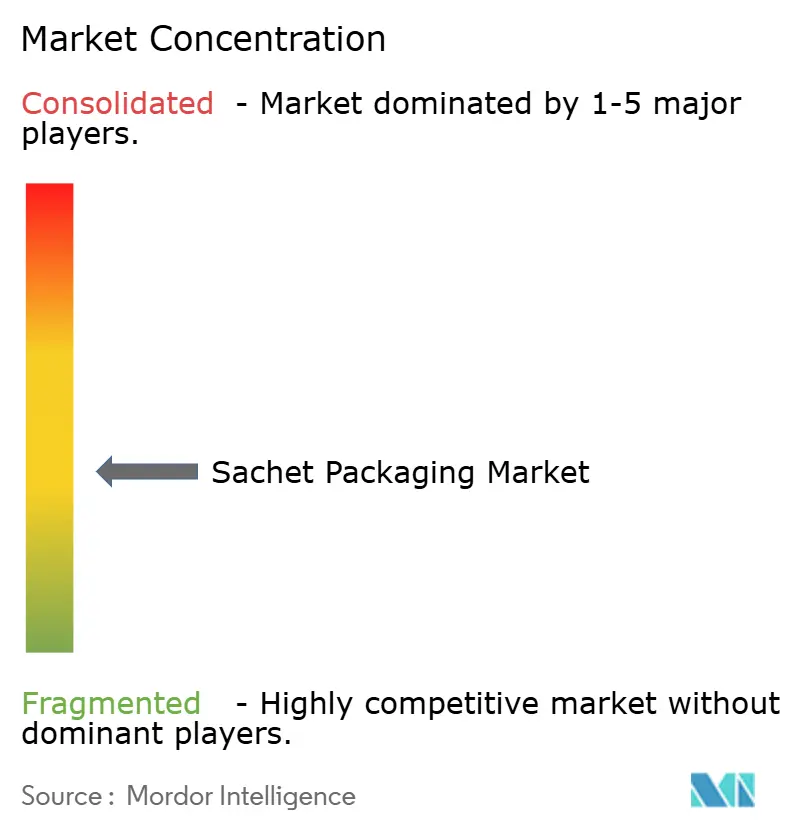

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sachet Packaging Market Analysis by Mordor Intelligence

The sachet packaging market size was valued at USD 10.98 billion in 2025 and estimated to grow from USD 11.52 billion in 2026 to reach USD 14.62 billion by 2031, at a CAGR of 4.88% during the forecast period (2026-2031). The expansion rides on mandatory unit-dose rules in regulated pharmaceutical markets, fast-growing e-commerce sampling programs, and deep-reach FMCG strategies in populous economies. Producers are re-engineering materials to comply with the European Union’s 2025 Packaging and Packaging Waste Regulation (PPWR), which enforces recyclability by 2028 and prohibits PFAS in food packaging from August 2026. Tariff-driven polymer cost spikes of 12-20% in the United States and volatile aluminum foil prices amplify the push toward paper and mono-material laminates that ease recycling flows. Automation upgrades in horizontal and vertical form-fill-seal lines sustain high throughput despite labor shortages, while recent mergers—most notably Amcor’s all-stock combination with Berry Global—signal faster innovation cycles and scale-driven cost leverage.

Key Report Takeaways

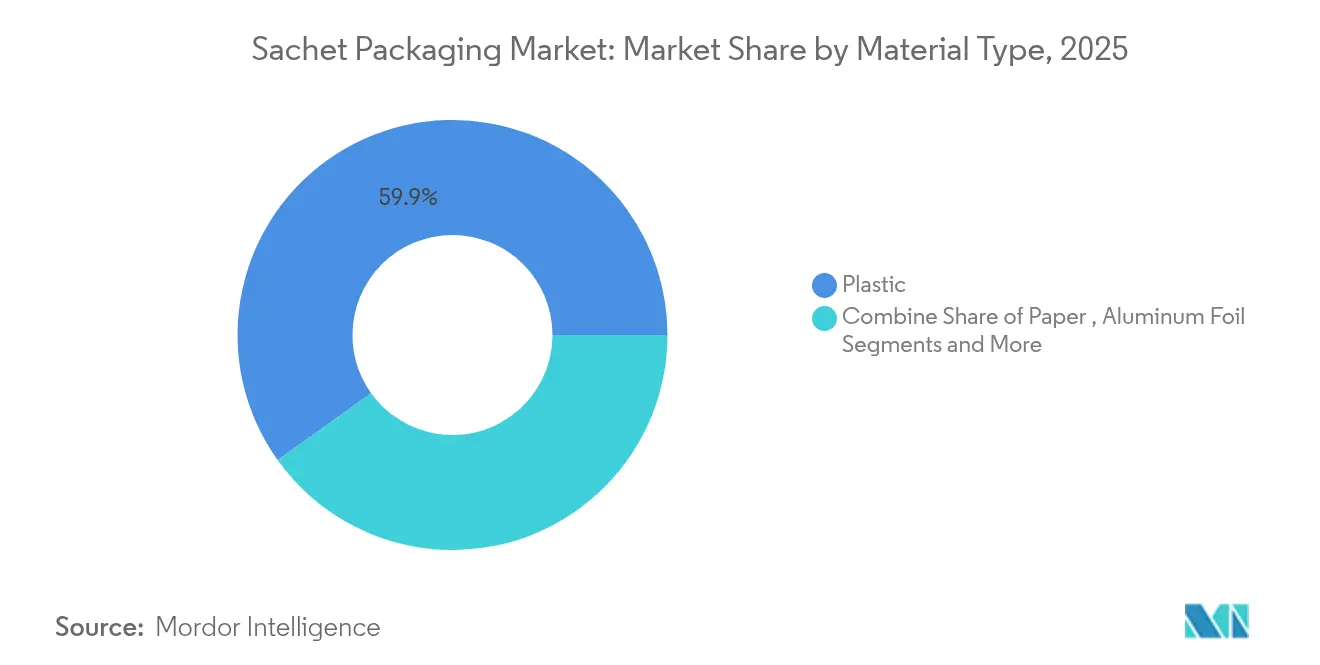

- By material type, plastic retained 59.88% of the sachet packaging market share in 2025; paper is the fastest-growing segment, advancing at a 7.31% CAGR through 2031.

- By application, food and beverage held 48.95% revenue share of the sachet packaging market in 2025, while pharmaceuticals posted the quickest CAGR at 7.89% to 2031.

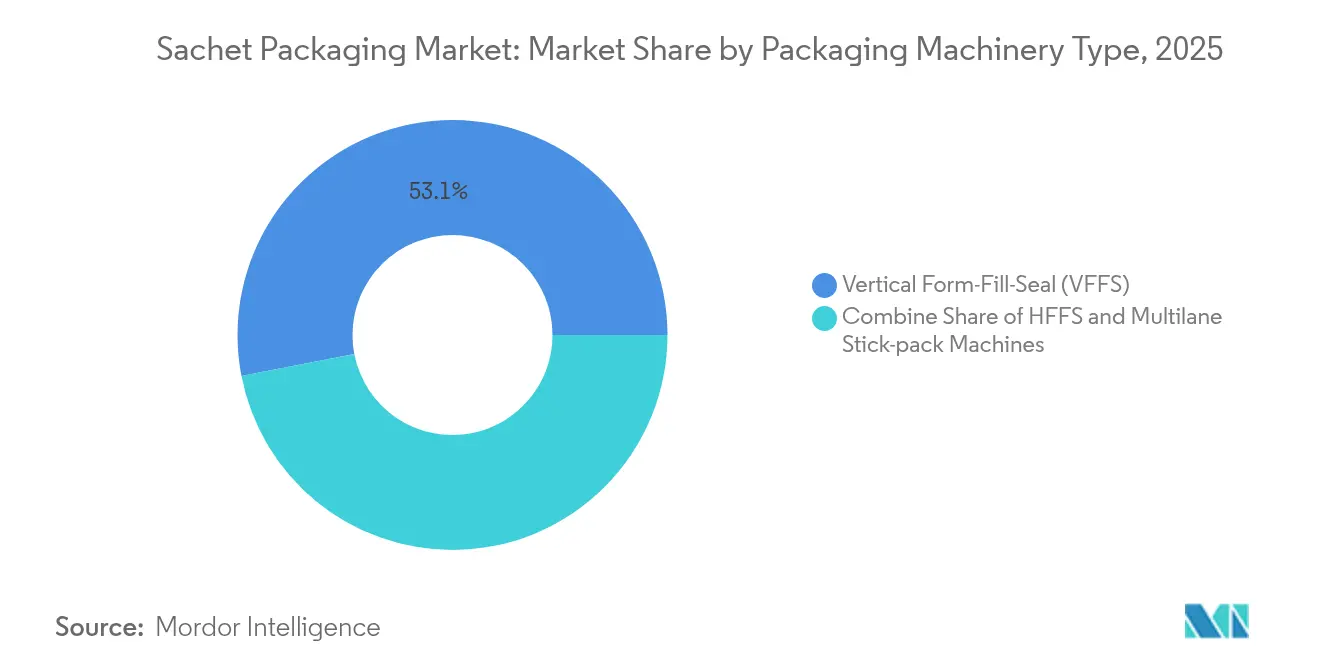

- By machinery, VFFS systems led with 53.05% share in 2025; HFFS lines register the strongest growth at 6.05% CAGR.

- By filling technology, powder applications commanded 38.02% share of the sachet packaging market size in 2025; liquid and viscous formats are set to expand at 7.45% CAGR.

- By geography, Asia-Pacific accounted for 38.12% of the sachet packaging market share in 2025; North America delivers the highest regional CAGR at 7.84% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sachet Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for lightweight, single-serve packs | +1.2% | Global; strongest in APAC | Medium term (2-4 years) |

| Rapid FMCG penetration in low-income, high-population markets | +1.8% | APAC core; MEA & LatAm spill-over | Long term (≥ 4 years) |

| E-commerce sample programs boosting micro-dose formats | +0.9% | North America & EU | Short term (≤ 2 years) |

| Dissolvable PVOH and water-soluble films unlock new use-cases | +0.7% | North America & EU early adopters | Medium term (2-4 years) |

| National anti-counterfeit mandates for unit-dose medicines | +1.1% | Regulated pharma markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Lightweight, Single-Serve Packs

Weight-optimized sachets cut material use by up to 60%, lowering freight costs and carbon footprints, as demonstrated by hand-sanitizer formats commercialized by T.H.E.M.Airlines, hotels, and ready-to-eat food brands favor these packs because they meet strict weight limits and hygiene protocols without compromising burst strength exceeding 450 lb. Premium labels deploy the sachet packaging market for trial size offers that slash customer-acquisition expense while preserving brand integrity. High-speed equipment capable of 1,600 packets per minute ensures that plant productivity offsets thin unit economics. Sustainability mandates and margin protection converge to accelerate adoption across sectors.

Rapid FMCG Penetration in Low-Income, High-Population Markets

Multinationals deploy sachet strategies to create affordable entry points for daily-purchase communities, especially in Indonesia where discarded sachets may reach 1.1 million t by 2030. [1]ABC News, “Sachets are cheap and easy to use…,” abc.net.auMicro-retail channels benefit from reduced inventory risk and smaller cash-cycle requirements. While the sachet packaging market drives brand presence, government waste targets such as Indonesia’s 30% packaging-waste reduction by 2029 foreshadow restrictions on sub-10 ml packs, nudging brands toward recyclable or soluble materials.

E-Commerce Product-Sample Programs Boosting Micro-Dose Formats

Beauty and personal-care labels rely on cosmetic sample sachets supplied by Zacros America to lift conversion rates via subscription boxes and online promotions. Pharmaceutical marketers extend the model to patient-starter kits that support adherence monitoring. Enhanced barrier coatings preserve volatile formulations during extended parcel-delivery cycles, while QR-enabled sachets capture usage analytics, turning the sachet packaging market into a data conduit.

Dissolvable PVOH and Water-Soluble Films Unlock New Use-Cases

Polyvinyl alcohol sachets dissolve entirely in water, eliminating post-use waste and broadening applications from crop-protection chemicals to concentrated detergents. Upgraded PVA blends with starch and cellulose improve tensile strength and biodegradation rates.[2]MDPI, “Synthetic Degradable Polyvinyl Alcohol Polymer…,” mdpi.comRegulatory acceptance remains uneven, but commercial composting infrastructure is expanding, positioning soluble films as a credible alternative to multilayer plastics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| Single-use-plastic bans and landfill restrictions | -0.8% | EU; select US states | Short term (≤ 2 years) |

| Volatile polymer and aluminum foil prices | -1.1% | Global; import-dependent regions | Short term (≤ 2 years) |

| Extended-Producer-Responsibility (EPR) fees on multilayer sachets | -0.6% | EU, North America, Australia | Medium term (2-4 years) |

| Micro-plastic legislation targeting <10 ml packs | -0.4% | EU focus; global ripple | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended-Producer-Responsibility Fees on Multilayer Sachets

New EPR rules in five US states, Australia, and the EU impose levies of EUR 0.10-0.50 /kg on complex laminates, squeezing high-volume low-margin SKU economics. Producers are redesigning toward mono-material structures and negotiating recycling-infrastructure partnerships to cap fee exposure, reshaping the cost baseline in the sachet packaging market.

Micro-Plastic Legislation Targeting <10 ml Packs

Upcoming EU proposals could restrict very small formats common in cosmetics and over-the-counter medicines, citing fragment accumulation in aquatic ecosystems. Compliance tension arises because unit-dose requirements collide with micro-plastic reduction goals, incentivizing rapid R&D in bio-based and soluble alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Momentum Builds as Plastic Holds Scale

Plastic laminates captured 59.88% of the sachet packaging market in 2025, underpinned by low cost and proven barrier protection. Paper-based variants are climbing at a 7.31% CAGR, as brand owners such as Mondelez switch confectionery multipacks to Saica’s recyclable paper wrappers. The sachet packaging market size for paper solutions is on track to double by 2030 as PFAS bans force coating reformulations that close the performance gap with plastics. Aluminum foil remains indispensable for moisture-sensitive pharmaceuticals but price volatility since late 2024 curbs volume growth.

Amcor’s AmFiber patent for high-barrier recyclable paper shows recovery of more than 80% fiber in standard repulping tests, offering converters a viable route to EPR cost relief. Investment in aqueous and bio-based coatings accelerates as the sachet packaging industry seeks drop-in solutions compatible with legacy filling equipment. Although sustainable materials still command a unit-price premium, scaling, regulatory deadlines, and brand commitments are converging to narrow the gap rapidly.

By Application: Pharma Growth Outpaces Food Dominance

Food and beverage commanded 48.95% of the sachet packaging market share in 2025 thanks to ambient-stable condiments, instant drinks, and seasoning blends that suit portion control in informal retail. Pharmaceuticals, however, are expanding at an 7.89% CAGR as serialization mandates favor unit-dose formats that deter counterfeits and improve dosage accuracy. The sachet packaging market size for medicines is forecast to exceed USD 2.18 billion by 2031, supported by 21 CFR 211.134 inspection rules that endorse individual-unit integrity.

Cosmetics brands leverage sachets for global sampling campaigns, while home-care players package concentrated detergents in precise‐dose sachets that limit spillage and overuse. Agricultural chemical suppliers deploy water-soluble PVOH sachets to ensure safe, direct-to-tank dilution, eliminating hazardous residue. Regulatory changes, such as India’s updated labelling rules effective 2024, intensify the information density required on each pack, prompting investment in high-resolution digital printing that preserves legibility on limited real estate.

By Packaging Machinery Type: HFFS Gains Speed and Gentleness

Vertical form-fill-seal (VFFS) lines accounted for 53.05% of sachet output in 2025, prized for flexibility across powders, liquids, and granulates. Horizontal form-fill-seal (HFFS) systems are growing 6.05% annually as new servo controls enable 80 cycles per minute on 16-lane configurations, reducing product drop height for fragile goods. Remote-diagnostic modules and predictive-maintenance algorithms embedded in modern HFFS frames cut unplanned downtime by up to 25%, appealing to contract packers servicing multi-SKU schedules.

FLtècnics’ AutoSplicer Pro lifts net line efficiency 10% by eliminating manual roll changeovers, trimming film waste and operator exposure. MULTIVAC’s Cooling@Packing platform integrates in-machine product chilling, enabling immediate post-bake sealing of bread and pastry sachets, a feature that unlocks new categories for the sachet packaging market. Equipment suppliers increasingly bundle machine learning modules that auto-tune sealing temperature based on laminate composition, ensuring consistent hermetic integrity regardless of substrate mix.

By Filling Technology: Liquids Close the Gap on Powders

Powder fillers held 38.02% share of sachet output in 2025, sustained by auger and vacuum dosing systems that dispense from 1 g to 10 kg with sub-1% weight variance. Liquid and viscous fillers are projected to grow 7.45% annually, propelled by servo-driven nozzles that achieve up to 1,600 packs per minute without foaming. GEA’s SmartFil platform offers more than 100 configuration permutations, letting dairy processors handle multiple SKUs on one line.

Spee-Dee’s direct-drive auger eliminates over 30 mechanical wear parts, slashing maintenance and boosting fill accuracy for pharmaceutical actives. Nichrome’s Intelweigh multi-head weigher integrates feedback loops that auto-correct dosing drift every 200 cycles, keeping giveaway below 0.3% of target weight. Across segments, demand for tool-less changeovers and CIP-ready wetted parts grows as the sachet packaging market expands into allergen-sensitive nutraceuticals and high-viscosity skincare serums.

Geography Analysis

Asia-Pacific generated 38.12% of the sachet packaging market revenue in 2025, leveraging vast consumer bases and agile informal retail structures. India’s flexible-packaging output is on course to exceed USD 12.72 billion in 2025, fueled by recycling-focused mono-material guidelines championed by Huhtamaki. China’s overhauled standards for food-contact materials under the Food Safety Law add stringent additive and migration limits that compel local converters to update ink and adhesive portfolios. Indonesia’s forecast of 1.1 million tons of sachet waste by 2030 has triggered a phased ban roadmap, encouraging early adoption of soluble films and recyclable papers.

North America exhibits the fastest growth at 7.84% CAGR, propelled by e-commerce sampling surges, stringent serialization in prescription medicine, and state-level EPR laws transferring disposal costs to producers. US import tariffs on plastics elevate domestic resin costs by 12-20%, nudging buyers toward locally sourced paper or bio-polymer alternatives. Pharmaceutical demand for child-resistant, unit-dose sachets creates high-margin niches that mitigate material cost inflation.

Europe navigates the transformative PPWR, which mandates full recyclability by 2028 and bans PFAS coatings in food packs from 2026. Germany’s updated food-contact guidelines tighten migration thresholds for adhesives, prompting accelerated qualification of water-based chemistries. Investments in depolymerization and fiber-recovery infrastructure support circularity goals, while consumer preference for portion control sustains demand in condiments and nutraceuticals. MERCOSUR’s draft PET recycling rules may shape future EU import requirements and create alignment opportunities for exporters.

Competitive Landscape

The sachet packaging market remains moderately fragmented, although consolidation is accelerating. The Amcor-Berry Global merger finalised in April 2025 forms a USD 3 billion-cash-flow entity with USD 650 million synergy targets, amplifying R&D muscle in barrier chemistries and paper replacements. Sonoco’s USD 3.9 billion purchase of Eviosys extends its metal and aerosol footprint, enabling cross-selling of sachet-compatible lidding films.

Patent analytics reveal more than 50 recent filings in moisture-control sachets, led by Constantia Flexibles and Evertis, indicating fierce competition in active-packaging functionalities. Futamura’s compostable film partnership introduces liquid-compatible bio-cellulose laminates, opening white-space in premium personal-care categories. Smaller firms capitalize on agility by offering bespoke digital-print runs and rapid material trials, positioning themselves as innovation feeders to larger conglomerates.

Automation and digitalization form new battlegrounds: equipment suppliers now embed AI vision to flag seal wrinkles in real time and predictive analytics that forecast component failure weeks in advance. Contract packers adopt these capabilities to guarantee 99.8% compliance rates demanded by pharmaceutical clients, differentiating on quality and traceability rather than solely on cost. Material producers meanwhile race to launch PFAS-free grease-barrier coatings before the 2026 EU deadline, reinforcing the pivotal role of chemistry innovation in future competitive advantage.

Sachet Packaging Industry Leaders

-

Huhtamaki Oyj

-

Sealed Air Corporation

-

ProAmpac Intermediate Inc.

-

Constantia Flexibles Holding GmbH

-

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor completed its all-stock combination with Berry Global, projecting USD 650 million in synergies by fiscal 2028.

- January 2025: The United Arab Emirates enacted a new Medical Products Law expected to influence pharmaceutical sachet standards.

- June 2024: India’s FSSAI re-operationalized amended food-labelling regulations affecting small-pack formats.

- May 2024: Xela Pack and Aveda launched recyclable paper-based hair-care sachets with 80% less plastic.

Global Sachet Packaging Market Report Scope

Sachets are small and portable, ideal for single-use servings or samples. Sachets are designed to protect the contents from moisture, light, and air, which helps maintain product quality, especially for food and pharmaceutical products. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The sachet packaging market is segmented by material type (Plastic, Paper, Aluminum and Other Material Types), by pack size (1 Ml To 10 Ml, 11 Ml To 20 Ml, 21 Ml To 30 Ml and Above 30 Ml), by application (Food, Pharmaceuticals, Personal Care & Cosmetics, Industrial and Other Applications) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Plastic |

| Paper |

| Aluminum Foil |

| Other Materials |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Home-care |

| Other Applications |

| Vertical Form-Fill-Seal (VFFS) |

| Horizontal Form-Fill-Seal (HFFS) |

| Multilane Stick-pack Machines |

| Powder |

| Liquid and Viscous |

| Granular |

| Paste |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Plastic | ||

| Paper | |||

| Aluminum Foil | |||

| Other Materials | |||

| By Application | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Industrial and Home-care | |||

| Other Applications | |||

| By Packaging Machinery Type | Vertical Form-Fill-Seal (VFFS) | ||

| Horizontal Form-Fill-Seal (HFFS) | |||

| Multilane Stick-pack Machines | |||

| By Filling Technology | Powder | ||

| Liquid and Viscous | |||

| Granular | |||

| Paste | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the sachet packaging market?

The sachet packaging market size stands at USD 11.52 billion in 2026 and is projected to hit USD 14.62 billion by 2031.

Which region is growing the fastest in sachet packaging?

North America leads growth with an 7.84% CAGR, driven by e-commerce sampling and tighter Extended Producer Responsibility laws.

Why are paper-based sachets gaining popularity?

Paper solutions meet new recyclability mandates like the EU PPWR while closing the performance gap with plastics through advanced barrier coatings.

How are regulations influencing pharmaceutical sachet demand?

Unit-dose and anti-counterfeit mandates, including 21 CFR 211.134 inspection rules, are pushing drug makers toward serialized sachet formats.

What technologies are advancing sachet filling speeds?

Servo-driven nozzles in modern liquid fillers now reach up to 1,600 packs per minute, while direct-drive auger systems boost powder dosing accuracy.

How will EPR fees affect sachet economics?

Producer-funded waste-management fees raise costs for multilayer sachets, prompting a shift toward mono-material and soluble alternatives that qualify for lower tariffs.

Page last updated on: