Retort Pouch Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.73 Billion |

| Market Size (2031) | USD 6.97 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

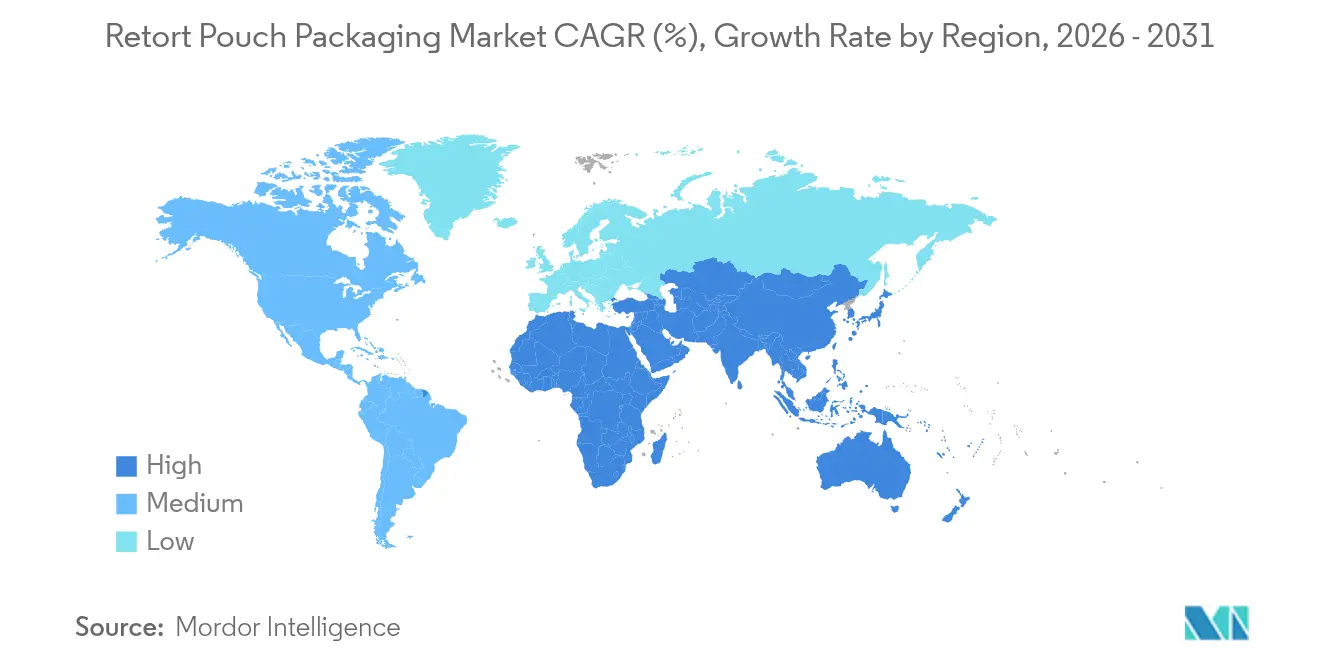

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retort Pouch Packaging Market Analysis by Mordor Intelligence

The retort pouch packaging market size was valued at USD 5.51 billion in 2025 and estimated to grow from USD 5.73 billion in 2026 to reach USD 6.97 billion by 2031, at a CAGR of 3.99% during the forecast period (2026-2031). Growth is fueled by rising demand for shelf-stable convenience foods, premium pet nutrition, and ongoing breakthroughs in high-barrier film technology that enable aluminum-free, recyclable constructions. At the same time, capital-intensive equipment, evolving recycling mandates, and fluctuations in foil supply temper new capacity additions, reinforcing the competitive edge of established converters. The Asia-Pacific region remains the volume anchor, thanks to urbanization and limited cold-chain coverage, while the Middle East and Africa show the quickest percentage expansion, as food import dependency and government procurement programs favor ambient formats.

Key Report Takeaways

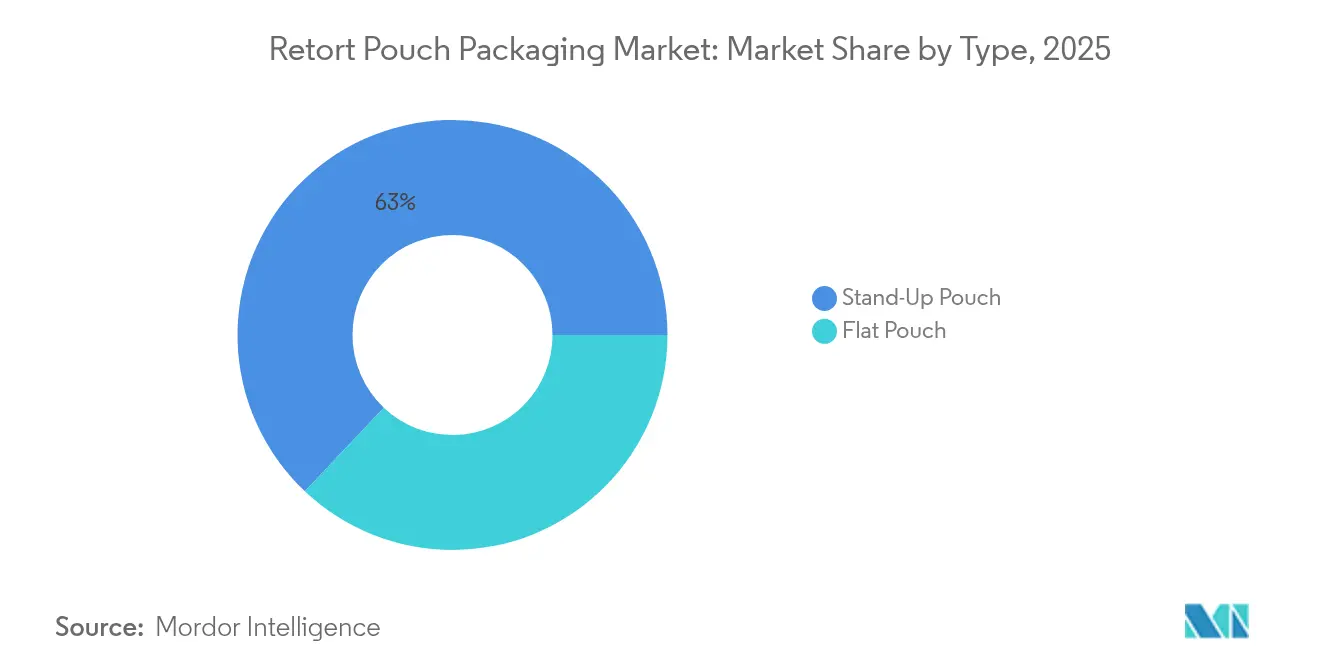

- By type, stand-up formats accounted for 62.95% of demand in 2025; flat pouches are projected to grow at a 5.42% rate from 2026 to 2031.

- By material, polypropylene accounted for 27.88% of the 2025 demand; paperboard is projected to advance at a 5.48% CAGR through 2031.

- By 2025, tear notches dominated the market with a 40.78% share; zipper closures are projected to grow at a 6.29% rate through 2031.

- By layer Structure, the 3-layer held 46.12% revenue share in 2025; the 5-layer is projected to grow at a 5.95% rate through 2031.

- By end-user, food applications led with a 58.25% revenue share in 2025; the pharmaceutical segment is projected to progress at a 5.61% CAGR through 2031.

- By geography, Asia-Pacific captured 39.75% of 2025 revenue; the Middle East and Africa are forecast to expand at a 6.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Retort Pouch Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Ready-to-Eat Meals | +0.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Advancements in High-Barrier Film Technologies | +0.7% | Europe, Japan, global spillover | Long term (≥4 years) |

| Growing Focus on Lightweight Sustainable Packaging | +0.6% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid Expansion of Pet Food Segment | +0.5% | North America and Europe, emerging Asia-Pacific | Short term (≤2 years) |

| Integration of Smart Packaging Features | +0.4% | Europe and North America, gradual Asia-Pacific uptake | Long term (≥4 years) |

| Expansion of Ambient Food Distribution Channels in Emerging Economies | +0.5% | Asia-Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ready-to-Eat Meals

Time-pressed households are replacing traditional canned goods with premium retort pouches that heat in under five minutes. Brands now position ethnic recipes, organic ingredients, and chef collaborations in stand-up pouches that command price premiums of 40-60% over metal cans. Quick-commerce warehouses, which favor ambient SKUs to avoid refrigeration costs, accelerate this shift. Regulatory clarity, such as explicit recognition of retort pouches under U.S. low-acid canned food rules, reduces compliance uncertainty for smaller processors. Together, these factors enhance retail visibility, differentiate the brand, and expand ambient reach while maintaining safety standards.[1]U.S. Food and Drug Administration, “21 CFR Part 113,” fda.gov

Advancements in High-Barrier Film Technologies

Silicon-oxide coatings, oriented high-density polyethylene, and hybrid organic-inorganic layers now achieve oxygen transmission rates under 3 cc/m²-day, enabling aluminum-free designs. MultiNanoLayer technology stacks 256 layers of polypropylene and polyvinyl alcohol to deliver 2.46 cc/m²/day at 121 °C, lowering material costs by 20-25% and permitting microwave use.[2]MDPI Polymers, “MultiNanoLayer Films Study,” mdpi.comBorealis’ XPP enhanced polypropylene maintains seal strength above 130 °C, eliminating delamination in all-polyolefin pouches. These advances broaden applications from low-acid soups to high-acid sauces, cut rely on foil use, and simplify recycling.

Growing Focus on Lightweight Sustainable Packaging

Extended producer responsibility fees in the European Union penalize multi-material laminates at a rate of up to EUR 0.80/kg, encouraging brands to adopt mono-material or fiber-based alternatives. Amcor’s AmFiber pouch swaps the outer polyester layer for barrier-coated paperboard, reducing plastic content 60% while retaining 121 °C retort capability.[3]Amcor, “AmFiber Paper-Based Pouch,” amcor.com ProAmpac has validated 30% post-consumer recycled polyethylene terephthalate in a retort structure approved for direct food contact. Converters that retrofit decontamination lines and secure recycled-resin supply gain an edge with multinational customers setting 2030 recycled-content targets.

Rapid Expansion of Pet Food Segment

Pet humanization drives the adoption of single-serve retort pouches, which offer freshness cues, portion control, and easy-open features. Senior cat products with tear notches and resealable zippers illustrate the potential for micro-segmentation. Regulatory differences, looser testing requirements for pet food than for human food, speed up innovation cycles. Co-packers are installing dedicated lines to prevent cross-contamination, enabling smaller brands to leverage retort without the need for FDA-audited infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Cost of Retort Equipment | -0.4% | Global, acute in emerging markets | Short term (≤2 years) |

| Recycling Challenges due to Multi-Layer Structures | -0.5% | Europe and North America, growing Asia-Pacific | Medium term (2-4 years) |

| Limited Thermal Resistance at Extreme Temperatures | -0.3% | Tropical and desert climates worldwide | Medium term (2-4 years) |

| Supply Chain Disruptions in Aluminum Foil | -0.3% | Europe, Asia-Pacific sourcing corridors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Cost of Retort Equipment

Automated pouch filling and sealing lines cost USD 180,000–280,000 for a modest output of 60 pouches per minute. Processors unable to finance such equipment often resort to co-packing agreements, which erode margins by up to 25%. Low-priced semi-automated Chinese systems (USD 9,800–12,800) reduce entry cost but deliver seal failure rates above 2%, disqualifying the product for multinational procurement. Capital barriers thus bifurcate the market between high-volume converters and niche premium players.

Recycling Challenges due to Multi-Layer Structures

Aluminum-polyolefin laminates resist mechanical and solvent-based separation, consigning most post-consumer pouches to landfill or incineration. Municipal sorters rarely detect thin foil layers, and only 5% of aluminum flexible packaging is recycled in Europe.[4]European Aluminium, “Recycling Rates and EPR Fees,” european-aluminium.eu Brands shifting toward silicon-oxide or ORMOCER coatings accept a 10-15% drop in barrier performance, shortening shelf life but avoiding high disposal fees. Technical breakthroughs, such as supercritical carbon-dioxide delamination, remain confined to post-industrial scrap, leaving a significant gap before achieving true circularity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stand-Up Formats Drive Retail Visibility

Stand-up formats accounted for 62.95% of the demand in 2025. Retailers favor the format for customizable graphics and efficient facings, while brands leverage shaped panels for ergonomic grip and pour control. Flat pouches, which expand at 5.42% through 2031, serve institutional food service, military contracts, and humanitarian aid, where stackability and pallet density take precedence over shelf appeal. The U.S. Department of Defense now permits flat retort pouches in Meal Ready-to-Eat rations, increasing payload efficiency on transport flights. Converters typically dedicate separate lines to each format, as forming collars and sealing jaws are not interchangeable. Shaped pouches introduced for baby food in 2024 boosted sales 9% by minimizing spillage during one-handed feeding. Despite higher tooling costs, shaped designs command 20-30% price premiums, making them attractive at retail price points above USD 3.00. The retort pouch packaging market size for stand-up variants is projected to expand steadily as supermarkets allocate more space in their ambient aisles to premium ready meals. Flat configurations will remain crucial where logistics cost per calorie transported is the primary metric, underscoring a dual-format landscape.

Second-generation stand-ups feature transparent windows and matte varnishes that offset the “industrial” perception long associated with foil pouches. Advanced laminators integrate near-field communication antennas beneath print layers without compromising seal integrity, linking shoppers to recipe videos and sourcing data. These smart add-ons are costly today but are increasingly being adopted by premium private-label ranges aiming to match the presentation of national brands. Within the retort pouch packaging market, regional converters that install digital presses are capturing short-run orders for ethnic cuisines and limited-time flavors, a revenue pool previously served by rigid jars. Meanwhile, flat pouches retain a material advantage in high-altitude air drops for humanitarian relief, where aerodynamic stability and puncture resistance are critical.

By Material: Paperboard Ascends as Sustainability Reshapes Specifications

In the retort pouch packaging market, polypropylene held a 27.88% share in 2025, driven by its reliable sealing properties and consistent global resin supply. However, retailers are beginning to favor paperboard laminates, accepting an 18-month shelf life, as opposed to the 24-month standard for all-plastic pouches. This shift is largely driven by the fact that 67% of European shoppers prioritize recyclability over shelf life for ambient foods. Looking ahead, paperboard is set to grow at a robust 5.48% CAGR through 2031. Amcor’s innovative AmFiber design substitutes the traditional outer polyester layer with a barrier-coated paperboard. This change not only slashes plastic usage by 60% but also ensures durability, withstanding temperatures of 121 °C for up to 50 minutes – a feat ideal for packaging vegetable stews, pasta meals, and gravies for pet food.

Billerud’s 2024 water-based coating has made significant strides, curbing moisture transmission to just 5 g/m²-day. This advancement paves the way for fiber pouches to venture beyond just dry mixes. However, it's worth noting that retort cooling condensation poses a risk, potentially degrading the moisture barrier in fillings with very low moisture content. The financials are favorable; a 20-30% retail price premium on products priced above USD 4.00 translates to an absolute cost increase of under 10%. This strategy enables premium brands to attract sustainability-conscious shoppers while maintaining their profit margins.

By Closure Type: Zipper Resealability Redefines Convenience

Tear notches accounted for 40.78% of 2025 closures because they integrate seamlessly into filling lines at a negligible cost. Yet, zipper systems are expected to expand by 6.29% through 2031, as consumers equate resealability with freshness and portion control. Coveris’ high-temperature polyethylene terephthalate zipper withstands 121 °C without profile deformation, enabling multiple re-closures in wet retort products. Spouts capture liquid categories, such as soups, gravies, and energy gel, offering controlled dispensing and single-handed use. Child-resistant spouts compliant with Consumer Product Safety Commission standards unlock potential in concentrated cleaners and pediatric medications.

Flip-top caps serve premium sports nutrition and on-the-go meal replacements, but add USD 0.03-0.04 per pack, limiting uptake below USD 3.00 retail price points. The retort pouch packaging market size for zipper variants is expected to continue expanding as pet owners demand resealable single-serve gravies and senior consumers seek easy-to-open features. Equipment upgrades are essential; installing an inline zipper applicator can lower throughput by 8-10%, but converters offset the slowdown with price premiums and customer stickiness. Hybrid closures, tear-notched plus zipper, are emerging for institutional packs, allowing for quick opening in kitchens while preserving leftovers.

By Layer Structure: Five-Layer Configurations Balance Barrier and Cost

Three-layer laminates, polyester/aluminum foil/polypropylene- accounted for 46.12% of the 2025 volume, offering a cost-effective path to an 18-month shelf life. Five-layer constructions are advancing 5.95% through 2031 as brands pursue 24-month guarantees without foil. A typical five-layer design utilizes polyester for printing, a tie layer for adhesion, nylon-MXD6 for the barrier layer, a second tie layer, and cast polypropylene for sealing. Co-extrusion now combines these layers in a single pass, reducing lamination time by 30% and improving interlayer adhesion, but it demands a capital outlay of over USD 2 million.

Four-layer designs offer a middle ground, trading 10-15% barrier loss for material savings. Seven-layer and nine-layer structures are designed for pharmaceuticals and medical devices that require redundant barriers, as specified in ISO 11607. Each additional layer adds around USD 0.015 to the unit cost and reduces line speed by 8-12%, which is acceptable when retail prices exceed USD 5.00. Within the retort pouch packaging market, converters capable of multistation co-extrusion secure long-term contracts with multinational food companies that desire consistent global specs. Smaller regional players focus on three-layer formats for government tenders where price outweighs shelf-life maxima.

By End-User: Pharmaceutical Segment Accelerates on Sterile Barrier Demand

Food applications dominated 2025 with a 58.25% share, leveraging 40-50% weight savings over cans and eliminating metallic flavor transfer. The pharmaceutical category, which is expected to expand at 5.61% through 2031, utilizes retort pouches as sterile barrier systems for pre-filled syringes and implant kits. Converters validate oxygen and moisture barriers according to ISO 11607, leveraging their existing expertise in high-temperature sealing. Beverages such as shelf-stable coconut water and plant-based milks utilize spouted pouches for portability; however, the thin liquid viscosity requires Cryovac’s dual-seal design to ensure hermetic integrity during retort.

Pet food is migrating quickly, premium cat entrées in shaped, zipper-sealed pouches command premiums of 15-25% over cans. Industrial lubricants and agrochemicals utilize retorts for extreme-temperature logistics, while cosmetics employ shaped pouches for single-dose serums delivered in aircraft amenity kits. The retort pouch packaging market share for medical devices will remain niche but lucrative, due to compliance barriers and low tolerance for failure.

Geography Analysis

Asia-Pacific contributed 39.75% of 2025 revenue, anchored by China and India where urban lifestyles lift demand for convenient meals and limited refrigeration infrastructure favors ambient formats. Government-backed food parks cluster converters, equipment makers, and brand owners, slashing transport costs and enabling just-in-time runs. Japan’s aging population buys premium stand-up pouches with transparent windows and QR codes that deliver preparation tips, while South Korea’s mandatory military service sustains institutional flat-pouch consumption. Stringent Chinese migration limits on food-contact materials effective 2024 are consolidating the retort pouch packaging market toward certified suppliers that can invest in analytical equipment, elevating quality baselines.

The Middle East and Africa is forecast to grow at 6.92% through 2031, fastest worldwide. Gulf Cooperation Council countries spend over USD 45 billion annually on food imports and stockpile shelf-stable meals for strategic reserves. Mondi’s new barrier-film plant in Turkey supplies regional converters, trimming reliance on distant foil suppliers and enabling aluminum-free structures suitable for the desert climate. Sub-Saharan African school feeding initiatives mandate locally processed fortified foods in retort pouches, guaranteeing baseline demand under government tenders. Capital scarcity remains the main brake; semi-automated lines satisfy current volumes but constrain long-term unit-cost competitiveness.

North America maintains sizable volume through ready-to-eat meals, premium pet food, and Department of Defense rations. U.S. brands such as Campbell’s install high-barrier stand-up lines to serve the 23% of households prioritizing convenience over scratch cooking. Mexico, leveraging USMCA tariff advantages, emerges as a nearshoring hub feeding southwestern U.S. distribution centers. European growth slows under extended producer responsibility fees that penalize non-recyclable laminates; brands accept 18-month shelf life in mono-material pouches to avoid EUR 0.50-0.80/kg penalties. Italy and Spain develop olive oil and tomato sauce pouches for export, capitalizing on Mediterranean authenticity cues. South American progress centers on Brazil and Argentina where modern retail gains share, though currency volatility complicates imported film procurement.

Competitive Landscape

The retort pouch packaging market exhibits a moderate level of fragmentation. Amcor, Sealed Air, and Mondi leverage proprietary lamination chemistries, global technical support teams, and multi-year contracts with multinational food companies. Constantia Flexibles’ new Dubai plant signals regional localization strategies that skirt import duties and shorten lead times.

Technology differentiation is widening. Converters investing in digital presses win limited-edition orders that rigid formats once held. Near-field communication tags and time-temperature indicators extend functionality from passive containment to data-rich engagement, opening new revenue streams in loyalty marketing and cold-chain compliance. Patent data indicate a surge in aluminum-free barrier coatings, retort-compatible zippers, and shaped pouch-forming dies. Meanwhile, regional players in Southeast Asia and Latin America deploy Chinese equipment that costs 30-40% less than Western lines, targeting organic baby food and ethnic meal kits, where small batches command high margins. Their price agility keeps pressure on multinationals to accelerate cost-down programs while maintaining stringent seal-integrity targets.

Market participants increasingly measure success by progress toward 2030 recycled-content mandates. Those lacking decontamination capacity for food-grade recycled resin risk exclusion from brand tenders. Consequently, capital allocation is shifting from raw extrusion tonnage to advanced cleaning, deodorization, and additive-blending steps. Players capable of delivering mono-material pouches that pass Association of Plastic Recyclers sortation tests and still survive 121 °C sterilization will capture future volume as regulators tighten recyclability definitions.

Retort Pouch Packaging Industry Leaders

Amcor PLC

Constantia Flexibles

Tetra Pak International SA

Mondi PLC

Coveris Holdings SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Mondi, a global leader in sustainable packaging and paper, has partnered with Proquimia to introduce paper-based stand-up pouches specifically designed for dishwashing tabs in Spain and Portugal.

- September 2024: Mondi finalized a USD 85 million barrier-film facility in Turkey, adding 15,000 t annual metallized-film capacity aimed at retort markets.

- August 2024: Huhtamaki acquired Elif Plastik of Turkey for EUR 120 million (USD 135 million), expanding Middle East retort pouch reach.

- July 2024: Amcor launched AmFiber, a paper-based retort pouch reducing plastic use by 60% while retaining 121 °C performance.

Global Retort Pouch Packaging Market Report Scope

The Retort Pouch Packaging Industry refers to the market for flexible, heat-resistant pouches designed for packaging ready-to-eat or processed food and beverages, pharmaceuticals, pet food, and other products. These pouches are engineered to withstand high-temperature sterilization processes, ensuring product safety and extended shelf life.

The Retort Pouch Packaging Industry Report is Segmented by Type (Stand-Up Pouch, Flat Pouch), Material (Polypropylene, Polyester, Aluminum Foil, Cast Polypropylene Film, Paperboard, Other Materials), Closure Type (Spout, Zipper, Tear Notch, Flip-Top Cap, Other Closure Types), Layer Structure (3-Layer, 4-Layer, 5-Layer, Above 5 Layer), End-User (Food, Beverages, Pharmaceutical, Pet Food, Other End Users), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Stand-Up Pouch |

| Flat Pouch |

| Polypropylene |

| Polyester |

| Aluminum Foil |

| Cast Polypropylene Film |

| Paperboard |

| Other Materials |

| Spout |

| Zipper |

| Tear Notch |

| Flip-Top Cap |

| Other Closure Types |

| 3-Layer |

| 4-Layer |

| 5-Layer |

| Above 5 Layer |

| Food |

| Beverages |

| Pharmaceutical |

| Pet Food |

| Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Type | Stand-Up Pouch | ||

| Flat Pouch | |||

| By Material | Polypropylene | ||

| Polyester | |||

| Aluminum Foil | |||

| Cast Polypropylene Film | |||

| Paperboard | |||

| Other Materials | |||

| By Closure Type | Spout | ||

| Zipper | |||

| Tear Notch | |||

| Flip-Top Cap | |||

| Other Closure Types | |||

| By Layer Structure | 3-Layer | ||

| 4-Layer | |||

| 5-Layer | |||

| Above 5 Layer | |||

| By End-User | Food | ||

| Beverages | |||

| Pharmaceutical | |||

| Pet Food | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the retort pouch packaging market by 2031?

The market is forecast to reach USD 6.97 billion by 2031.

Which region is expected to record the fastest growth in retort pouches through 2031?

The Middle East and Africa is projected to grow at a 6.92% CAGR, the highest of all regions.

Why are brands moving toward aluminum-free retort pouch structures?

Aluminum-free designs lower material costs, enable microwave use, and avoid high extended producer responsibility fees imposed on non-recyclable laminates.

How does nylon-MXD6 improve retort pouch performance?

When laminated with polypropylene, nylon-MXD6 delivers very low oxygen transmission rates that extend ambient shelf life to 24 months for oxidation-sensitive foods.

What factor limits small processors from installing retort pouch equipment?

Automated filling and sealing lines cost USD 180,000–280,000, posing a substantial capital barrier versus rigid-container lines.

Which closure type is gaining the most momentum in premium applications?

Zipper closures are expanding the quickest because resealability signals freshness and supports portion control.

Page last updated on: