Stand-Up Pouches Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

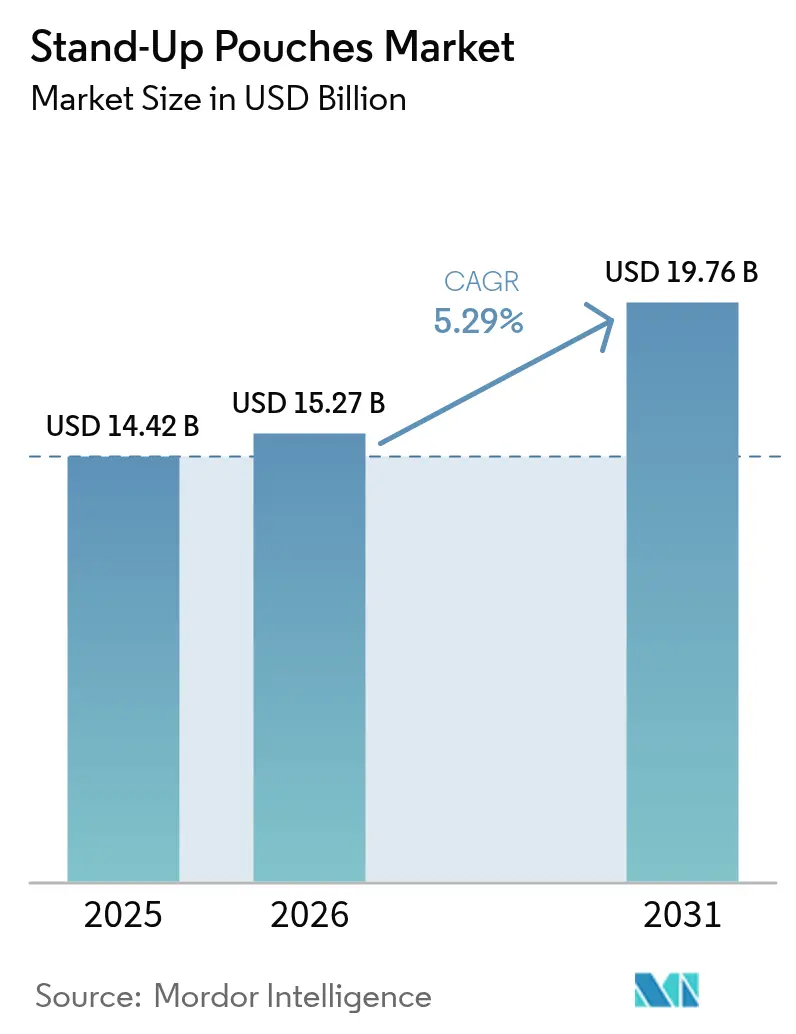

| Market Size (2026) | USD 15.27 Billion |

| Market Size (2031) | USD 19.76 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

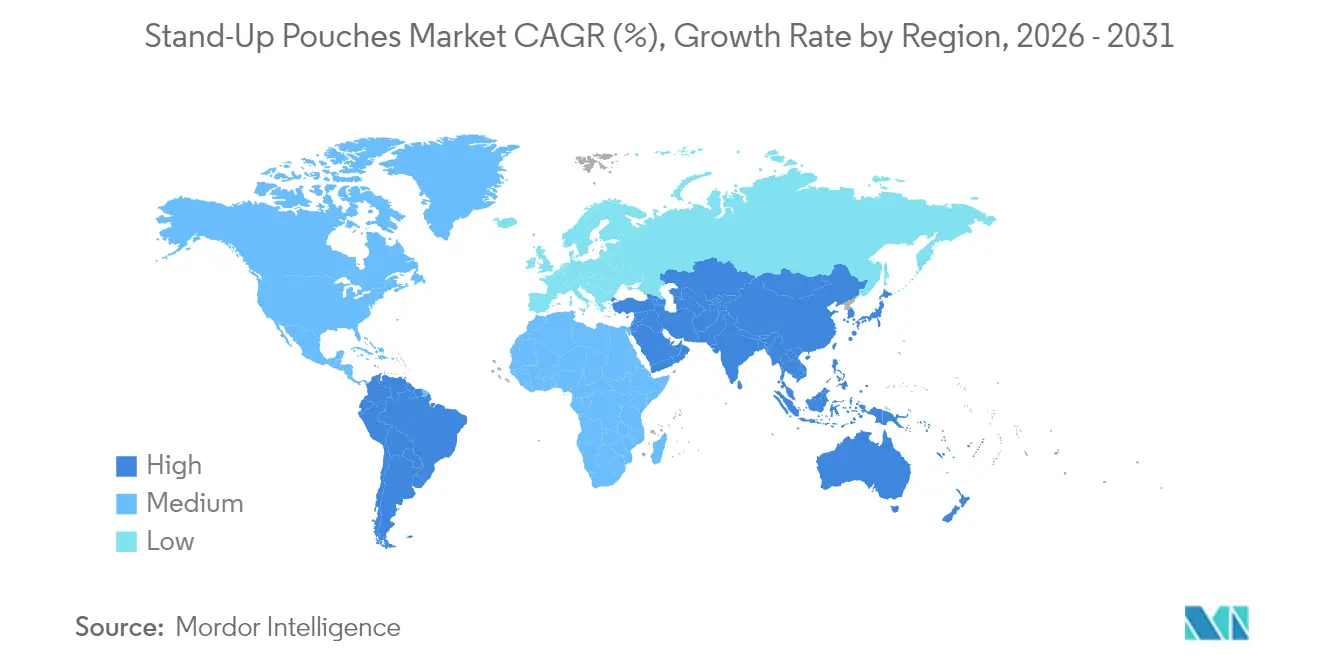

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stand-Up Pouches Market Analysis by Mordor Intelligence

The stand-up pouches market size was valued at USD 14.42 billion in 2025 and is estimated to grow from USD 15.27 billion in 2026 to USD 19.76 billion by 2031 at a 5.29% CAGR over 2026-2031. Sustained demand for convenient, lightweight packaging, tightening sustainability regulations and a wave of rigid-to-flexible conversions keep the stand-up pouches market on a steady growth path. Manufacturers are deploying mono-material laminates to comply with Europe’s Packaging and Packaging Waste Regulation 2025/40 and emerging U.S. extended-producer-responsibility laws, while brand owners in food, personal care, and beverages accelerate adoption to curb logistics costs and shrink carbon footprints. Capital investment in solventless lamination, machine-direction orientation, and digital printing is surging as converters race to unlock recycle-ready formats, support short production runs, and embed traceability features. Competitive intensity has deepened after Amcor finalized the USD 8.43 billion Berry Global deal in May 2025 and ProAmpac announced a USD 1.51 billion agreement to acquire TC Transcontinental Packaging in December 2025, moves that realign global film extrusion and pouching capacity. Persistent raw-material volatility around ethylene-vinyl-alcohol (EVOH) and nylon resins and the lack of curbside collection for multi-layer laminates remain structural headwinds, but ongoing capacity expansions in barrier-paper, mono-polyethylene and aseptic pouch lines give the stand-up pouches market additional resilience.

Key Report Takeaways

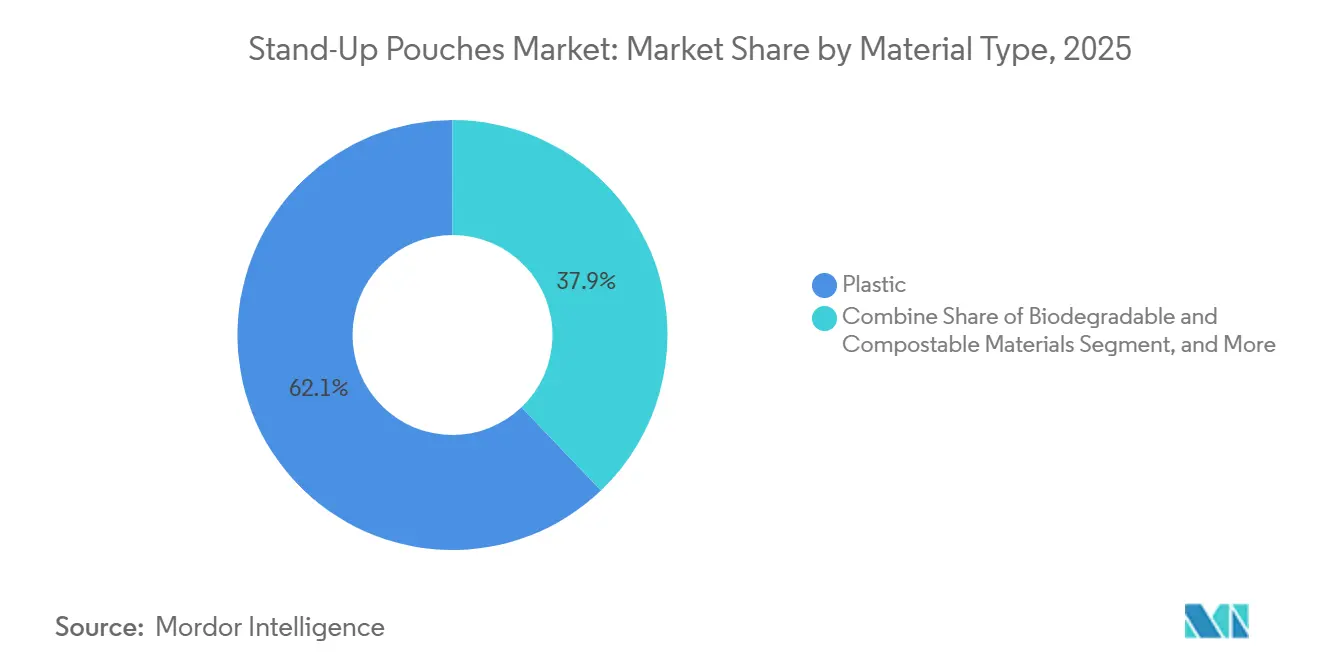

- By material type, plastic led with 62.13% of 2025 revenue, while biodegradable and compostable alternatives are projected to expand at a 6.07% CAGR through 2031.

- By product type, round-bottom (Doyen) pouches accounted for 40.32% of volume in 2025, whereas flat-bottom variants are forecast to post a 6.24% CAGR owing to shelf-stacking efficiencies.

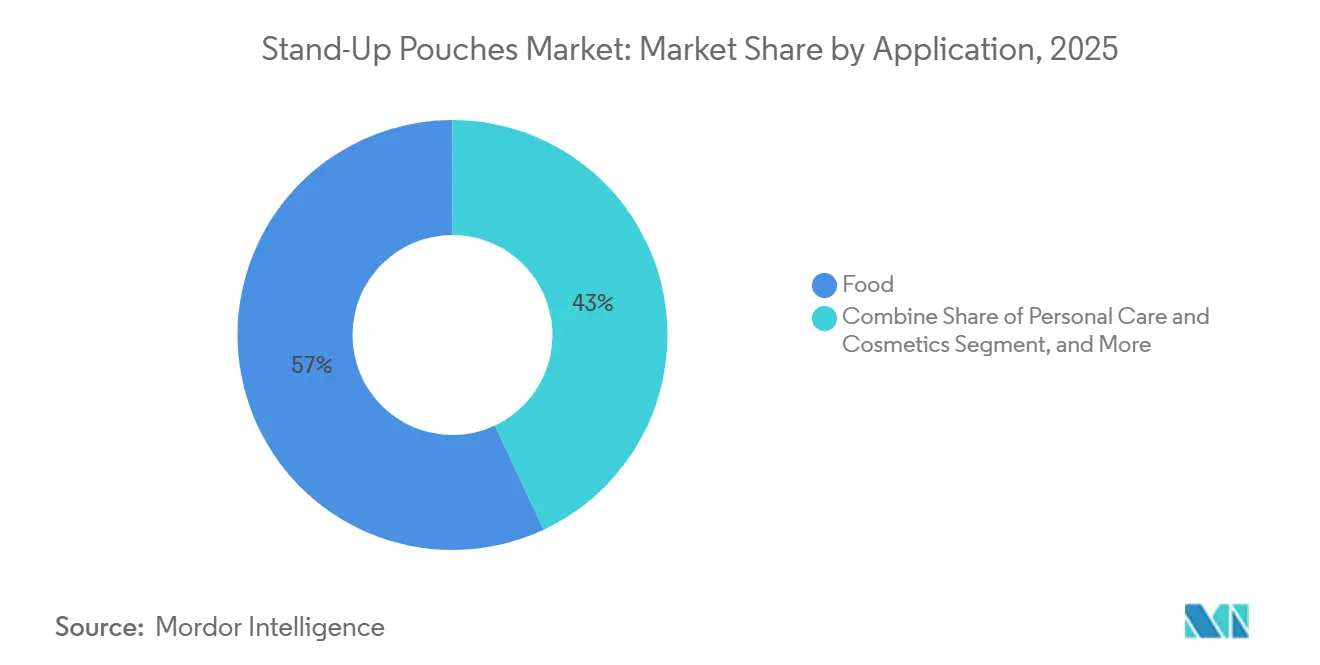

- By application, food accounted for 56.24% of global volume in 2025, yet personal care and cosmetics pouches are set to grow at a 6.32% CAGR, driven by refill and subscription models.

- By distribution channel, direct sales captured 69.42% of the 2025 value, but online channels are set to rise at a 5.69% CAGR as digitally printed, low-MOQ programs proliferate.

- By geography, Asia-Pacific represented 41.87% of 2025 revenue, while the Middle East and Africa region is expected to see the quickest regional climb at a 6.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Stand-Up Pouches Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient lightweight food packaging | +1.2% | Global, early gains in North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Sustainability regulations pushing mono-material recyclable pouch adoption | +1.3% | Europe, North America, spillover to Asia-Pacific | Medium term (2-4 years) |

| Cost savings from rigid-to-flexible conversions | +1.0% | North America and Europe, spillover to South America | Medium term (2-4 years) |

| Growth in e-commerce and on-the-go consumption | +0.9% | China, United States, Brazil | Short term (≤ 2 years) |

| Aseptic dairy expansion in Sub-Saharan Africa boosting aluminum-free pouches | +0.6% | Kenya, Nigeria, Ethiopia | Long term (≥ 4 years) |

| Nordic beauty refill culture accelerating easy-pour SKUs | +0.3% | Sweden, Norway, Denmark | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient, Lightweight Food Packaging

Single-serve and resealable pouches continue to replace cans and jars in snacks, confectionery, and pet food as consumers expect portability and portion control. Industry surveys confirm higher capital budgets for flexible lines, and brands are leveraging recycle-ready mono-polypropylene retort structures to match steel-can shelf life. Snack processors increasingly nest individually wrapped bites inside larger stand-up packs, slimming the mass of secondary packaging while preserving grab-and-go convenience. High-share zipper closures prolong freshness and dovetail with United Nations food waste targets. Consumer sentiment studies point to rising willingness to pay for formats perceived as eco-friendlier, further reinforcing the conversion wave. Global standards such as ISO 18601 now appear in tender documents issued by multinational food groups, effectively making flexible compatibility a mandatory baseline.[1] International Organization for Standardization, “ISO 18601 Flexible Packaging,” iso.org

Sustainability Regulations Pushing Mono-Material Recyclable Pouch Adoption

The European Union’s Packaging and Packaging Waste Regulation 2025/40 and a slate of U.S. EPR statutes oblige brands to fund recycling programs and meet recycled-content quotas, prompting the redesign of multi-layer laminates into mono-polyethylene or mono-polypropylene formats.[2]European Commission, “Packaging and Packaging Waste Regulation 2025/40,” EUR-Lex, eur-lex.europa.eu Converters have responded by installing high-output solventless laminators, machine-direction orientation lines, and in-house film-washing capacity. Constantia Flexibles opened new mono-PE extrusion assets in September 2025, citing surging order books for How2Recycle-compliant pouches. The combined Amcor-Berry footprint now controls one of the world’s largest recycle-ready film portfolios, giving large CPGs a single-source option for global roll-outs. Retailers such as Walmart and Tesco have tightened supplier scorecards, accelerating the shift to label-ready structures. Certification schemes under ISO 14021 and ISO 14024 have moved from “nice-to-have” to “must-have,” lengthening qualification cycles but offering marketing upside once achieved.

Cost Savings from Rigid-to-Flexible Conversions

Switching from glass, metal or paperboard to stand-up pouches slashes package weight by 60-80%, trimming freight bills and warehouse cube. U.S. flexible-packaging producers supplied materials that yielded USD 151 billion in economic output in 2024, a scale that underwrites investment in faster, lower-waste lines.[3] Flexible Packaging Association, “Industry Statistics and Economic Impact,” flexpack.org A 500-milliliter pouch generally consumes under 20 grams of film versus as much as 35 grams for an equivalent rigid container, a raw-material delta that flows directly to gross margin. Flat-bottom pouches, now the fastest-growing form factor, often replace secondary corrugated shippers in club and e-commerce channels, shaving total packaging costs by 15-20%. Mondi’s FunctionalBarrier Paper Ultimate, introduced following a EUR 16 million (USD 18.1 million) upgrade in Poland, broadens rigid-to-flexible options for dry-food brands seeking UK plastic tax relief. Digital-printing specialists such as ePac lower the economic order quantity to 5,000 units, allowing emerging brands to test SKUs without stranding inventory.

Growth in E-Commerce and On-The-Go Consumption

Parcel-ship durability standards for online grocery and subscription flows prioritize flexible packs that survive drops and vibration without outer cartons. A 2025 Packaging World survey shows that almost half of brands grow e-commerce volume despite margin pressure. Refill pouch programs, notably Garnier’s shampoo capsules, remove up to 70% of secondary material and appeal to eco-conscious millennials. In South America, where the stand-up pouches market already benefits from double-digit online grocery adoption, Amcor commissioned an MDO film line in Peru to localize supply and shorten lead times.[4]Amcor Plc, “AmLite HeatFlex Retort Solutions,” amcor.com Fresh-produce shippers such as Dole have adopted recyclable stretch films and pouch labels bearing QR codes that unlock traceability data in augmented-reality overlays. Digitally printed graphics also give brands the flexibility to rotate artwork for limited-edition drops without tooling delays.

Restraints Impact Analysis of Stand-Up Pouches Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited recycling streams for multi-layer laminates | -0.8% | North America and Europe | Medium term (2-4 years) |

| Volatile EVOH and nylon resin prices | -0.6% | Global, concentrated in Asia-Pacific and North America | Short term (≤ 2 years) |

| Migration contaminant worries over high-PCR cosmetics pouches | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Head-space failure incidents in >1 L retort soup pouches | -0.2% | Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Recycling Streams for Multi-Layer Laminates

Most legacy stand-up pouches layer polyethylene, polypropylene, EVOH, and aluminum in structures that municipal facilities cannot separate, forcing landfill or energy-from-waste disposal. China’s National Sword restrictions clamp down on export outlets, amplifying domestic sorting bottlenecks. India’s Plastic Waste Management Rules mandate producer responsibility yet lack nationwide collection coverage. Brand owners, therefore, juggle barrier durability with recyclability, a stark compromise in oxygen-sensitive foods such as coffee. Certification to the Association of Plastic Recyclers' design guidance offers partial mitigation, but consumer confusion around drop-off programs still limits capture rates. Compliance costs mount as EU and U.S. regulators tighten migration-testing requirements, extending launch timelines and dampening rapid format shifts.

Volatile EVOH and Nylon Resin Prices

High-barrier retort and aseptic pouches rely on EVOH and nylon 6, resins whose prices swing with crude markets and refinery turnarounds. ICIS data show polypropylene up 15% during 2024 while nylon fell 9%, leaving converters hedging spot buys or sharing surcharges with brand partners. Winpak’s latest report details margin compression and renegotiated quarterly price clauses. Smaller converters lack scale to buffer volatility and face a disadvantage against vertically integrated majors. The premium attached to compostable resins, often 30-50% above polyolefins, compounds capital risk on still-nascent applications.. Moreover, EU Regulation 2022/1616 requires EFSA approval for recycled plastic in food contact, adding EUR 50,000-100,000 (USD 56,500-113,000) per SKU in testing costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Stand-Up Pouches Market Segment Analysis

By Material Type:

Bioplastics Edge Toward MainstreamPlastic maintained a 62.13% revenue share in 2025, underlining polyethylene and polypropylene’s balance of sealability, heat resistance and cost. The stand-up pouch market for plastic is projected to grow steadily as high-clarity, low-gauge films proliferate in snacks and pet food. However, regulatory pressure has propelled biodegradable and compostable substrates to a 6.07% CAGR, fueled by polylactic acid and BASF ecovio blends that satisfy Europe’s single-use plastics rules. Pioneering brand pilots in coffee, dry mixes, and personal care underscore bioplastic momentum, albeit constrained by limited industrial-compost infrastructure beyond California and select EU cities. Metal-foil laminates linger in pharma and high-oxygen-barrier food niches but face substitution from aluminum-oxide-coated, PET, which eases curbside sortation. Paper-based pouches gained traction following Mondi’s launch of FunctionalBarrier Paper Ultimate, helping brands avoid the United Kingdom's plastic-packaging tax. Across categories, material choice now hinges on balancing barrier performance, recyclability certification, and regional waste-management realities, a trade-off shaping supply-chain collaboration.

Plastic dominance also reflects entrenched equipment ecosystems. Multilayer co-extruders, solventless laminators, and high-speed horizontal form-fill-seal machinery remain tuned for polyolefin films. Yet incremental retrofits enable converters to slot mono-material structures without wholesale line changes. Multinationals stipulate ISO 14001 environmental management compliance, accelerating the the shift toward lower-carbon resins. The stand-up pouches market share for biodegradable films will therefore widen as compostability labeling gains consumer recognition, but plastic will continue to anchor base volumes through 2031.

By Product Type:

Flat-Bottom Formats Win Shelf SpaceRound-bottom pouches accounted for 40.32% of 2025 volume, but flat-bottom designs are charging ahead at a 6.24% CAGR as club stores, warehouse retailers, and e-commerce operators prize their standability. A flat-bottom pack can replace an outer corrugated tray, cutting logistics expenditure and elevating billboard area for graphics, an attribute that resonates in visually crowded snack aisles. K-seal variants are used in high-load applications such as coffee and dog food, where pallet stability is non-negotiable. Spouted-shaped pouches, growing off a smaller base, tap beverage, baby food, and sauce formats enabled by SIG’s in-line aseptic sterilization, which removes third-party cost layers.

Digital printers favor flat-bottom canvases because bigger front and side panels accommodate variable data and interactive elements. The stand-up pouch market for flat-bottom products is thus benefiting from synchronized advances in press technology and quick-change pouch lines. As retailers expand private-label portfolios, flat-bottom options furnish premium cues without glass or can weight. Further share shifts hinge on equipment capex and improvements in seal integrity that let converters push line speeds while minimizing scrap.

By Application:

Personal Care Refills AccelerateFood accounted for 56.24% of the 2025 volume, yet personal care and cosmetics pouches exhibit the fastest growth at a 6.32% CAGR. Nordic refill schemes and direct-to-consumer brands highlight sachets and pillow packs that slide into durable dispensers, trimming plastic and shipping weight. Beverage pouches are gaining ground in outdoor sports and ready-to-drink cocktail occasions, leveraging resealable spouts and retort stability to displace glass bottles. Pet-food conversions from cans to recycle-ready retort pouches have boosted the market for stand-up pouches for wet dog food, since owners value portion control without a can opener. Healthcare and pharmaceutical pouches support unit-dose therapies, though stringent ISO 11607 testing slows mass-market crossover. Industrial-chemical formats use spouts for detergents and lawn-care concentrates, where controlled dosing beats rigid jug glugging.

The second wave of adoption centers on active and intelligent packaging. Color-changing oxygen scavengers and thermochromic inks now appear on confectionery and snack pouches, signaling freshness in real time and helping retailers cut shrink. Cosmetics brands embed QR codes that unlock ingredient stories, brand videos and refill reminders, strengthening loyalty loops. In beverages, shaped pouches with finger grips and anti-slip matte varnishes target school-lunch programs, while shelf-stable soup producers pilot one-liter retort packs that minimize warehouse space. Across categories, migration-testing expenses and limited composting infrastructure temper bioplastic penetration, but brand commitments to 95% recycle-ready packaging by 2025 keep momentum firmly positive.

By Distribution Channel:

Online Platforms Lower MOQ BarriersDirect converter-to-brand contracts retained 69.42% of 2025 value, anchoring high-volume SKUs for multinationals like Nestlé and PepsiCo. Annual supply agreements typically lock in film specs, quality audits and sustainability milestones, ensuring factory utilization for converters. Online channels, however, are scaling at a 5.69% CAGR as subscription boxes, crowd-funded launches and marketplace sellers prize digitally printed pouches with low minimum order quantities. ePac’s fleet of HP Indigo presses cuts MOQs to 5,000 units and slashes artwork changeover time, disintermediating traditional brokers. Distributors still serve regional food startups, but their share erodes as web-to-print portals quote two-week lead times.

Omnichannel fulfillment is reshaping package design. Brands must certify to Amazon’s Frustration-Free Packaging and major carriers’ drop-test protocols, which favor flexible packs that survive vibration without added void fill. QR-enabled labels convert parcels into digital engagement points, collecting scan data that feeds customer-relationship-management dashboards. Retailers also push near-real-time replenishment, prompting converters to hold blank rollstock and print late-stage graphics as orders flow. Meanwhile, social commerce in South America and Southeast Asia sparks micro-batch runs for influencer collaborations, reinforcing demand for agile, short-lead pouching lines. Over the forecast horizon, the boundary between direct and online channels blurs as converters embed e-commerce storefronts inside enterprise resource-planning portals, letting brand buyers place repeat orders 24/7 with dynamic pricing tied to resin indices.

Geography Analysis

APAC Stand-Up Pouches Market

Asia-Pacific supplied 41.87% of global 2025 revenue, powered by China’s same-day e-commerce fulfillment and India’s food-processing Production-Linked-Incentive subsidy. Domestic pouch makers in both markets are installing mono-material lines to align with National Sword import bans and evolving plastic-waste rules, actions that safeguard local supply and moderate import reliance. Japan’s aging consumer base values lightweight, easy-open packs, catalyzing premium soy sauce and miso refills. Australia and South Korea funnel digital-print investment into short-run SKUs for sports nutrition and organic baby food. Across the region, the stand-up pouch market continues to expand as cross-border e-commerce drives demand for parcel-optimized formats.

MEA Stand-Up Pouches Market

The Middle East and Africa region is forecast to post the fastest climb at 6.23% through 2031. Tetra Pak and Huhtamaki have commissioned aluminum-free aseptic dairy lines in Kenya, Nigeria, and Ethiopia, letting processors distribute milk without cold chains, a breakthrough for rural access. Agribusiness growth, projected by the African Development Bank to hit USD 1 trillion by 2030, accelerates export-grade pouch demand for cocoa, coffee and spices. Gulf Cooperation Council countries are pushing sustainability agendas tied to Saudi Vision 2030, prompting supermarkets to favor recyclable packaging.

North America Stand-Up Pouches Market

North America holds sizeable share but growth has cooled to regulatory compliance and premiumization plays. Extended producer responsibility laws now active in Oregon and pending in five more states make funding mechanisms for curbside collection explicit, nudging brands toward mono-material designs. Canada’s Québec and Ontario deposit systems contemplate flexible-film pilots, potentially unlocking new feedstock streams. Retailers mandate How2Recycle labeling to reduce bin contamination. U.S. resin volatility, compounded by hurricane-season outages along the Gulf Coast, injects cost unpredictability yet also spurs substitution with domestically recycled PE.

Europe Stand-Up Pouches Market

Europe maintains rigorous circular-economy goals under PPWR 2025/40, banning PFAS from August 2026 and setting recyclability thresholds for 2030. Germany and France move ahead on high-PCR content minimums, pressuring converters to deploy de-inking and delamination tech. The United Kingdom’s GBP 200-per-metric-ton plastic-packaging tax (USD 252) steers beverage brands into post-consumer recycled polypropylene caps that pair with mono-PE spouted pouches. Eastern Europe, illustrated by Gualapack’s EUR 12 million (USD 13.6 million) Ukrainian factory, attracts investment as near-shore production mitigates geopolitical freight risk.

LATAM Stand-Up Pouches Market

South America’s flexible-packaging spending, valued at USD 10.77 billion in 2026, will climb to USD 14.72 billion by 2035 on a 3.53% CAGR, with Brazil and Mexico dominant. Amcor’s new MDO film line in Peru exemplifies capacity localization that trims import duties and transit times for Andean snack exporters. Governments across the region edge toward EPR schemes, signaling future alignment with Northern Hemisphere sustainability benchmarks.

Competitive Landscape

The global stand-up pouches market displays moderate-to-high concentration: the top five players, Amcor, Mondi, Berry Global, Sonoco, and Sealed Air, command roughly 40-45% combined capacity. Amcor’s USD 8.43 billion integration of Berry Global cements a powerhouse controlling extrusion, lamination, and printing across four continents, expediting global mono-material roll-outs. ProAmpac’s USD 1.51 billion deal for TC Transcontinental Packaging, pending closure in early 2026, fortifies its food and pet-food franchise and adds barrier-paper know-how. Constantia Flexibles and Mondi funnel more than EUR 1.3 billion (USD 1.47 billion) into solventless laminators and MDO films, underscoring the capital heft needed to pivot away from mixed laminates.

Digitally focused challengers such as ePac carve out the short-run, high-mix niche, leveraging 58 HP Indigo presses slated for Gen5 upgrades. Their distributed network reduces freight miles and turnaround times, luring start-ups to sidestep traditional brokers. Technology leadership is also visible in SIG’s in-line aseptic spout system, which trims sterilization steps, and Winpak’s ReForm mono-material range that eliminates EVOH layers. Regional converters battle raw-material volatility, lacking Amcor-style scale to hedge resin costs, and often seek private-equity backing to fund upgrades.

Quality and sustainability certifications have become de facto barriers to entry. ISO 9001 and ISO 22000 registration appear in bid packets for multinational FMCGs. Converters failing to demonstrate closed-loop traceability risk exclusion from new product launches. On the opportunity side, rapid adoption of tethered caps and digitized traceability marks presents room for IP-driven differentiation. Overall, M&A momentum suggests further consolidation as buyers chase economies of scale and toolbox breadth.

Stand-Up Pouches Industry Leaders

Mondi PLC

Sonoco Products Company

Constantia Flexibles GmbH

ProAmpac LLC

Amcor Plc

- *Disclaimer: Major Players sorted in no particular order

Stand-Up Pouches Market Companies Covered in this Report

- Amcor Plc

- Mondi plc

- Sonoco Products Company

- Constantia Flexibles GmbH

- ProAmpac LLC

- Sealed Air Corp.

- Smurfit Kappa Group plc

- Uflex Limited

- Winpak Ltd

- Glenroy Inc.

- Flair Flexible Packaging Corp.

- Bischof + Klein SE

- Interflex Group

- Gualapack S.p.A.

- Coveris Holdings

- Printpack Inc.

- C-P Flexible Packaging

- Scholle IPN

- Taghleef Industries

Recent Industry Developments in Stand-Up Pouches Market

- January 2026: ProAmpac confirmed the regulatory filing phase for its USD 1.51 billion acquisition of TC Transcontinental Packaging, targeting completion in Q2 2026.

- October 2025: Amcor placed into commercial service a machine-direction orientation film line in Peru to support rising South America pouch demand.

- September 2025: Constantia Flexibles lifted mono-polyethylene film output at its Austrian hub, expanding supply of recycle-ready laminates.

- August 2025: Constantia Flexibles announced a EUR 100 million (USD 113 million) capacity build focused on solventless laminators for food and personal care pouches.

Global Stand-Up Pouches Market Report Scope

The Stand-Up Pouches Market Report is Segmented by Material Type (Plastic, Paper, Metal Foil, Biodegradable and Compostable Materials), Product Type (Doyen or Round Bottom, K-Seal, Plow or Corner Bottom, Flat Bottom, Other Product Types), Application (Food, Beverage, Personal Care and Cosmetics, Healthcare and Pharmaceuticals, Industrial and Household Chemicals, Other Application), Distribution Channel (Direct Sales, Indirect Sales), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Segmentation Overview

| Plastic | Polyethylene Terephthalate (PET) |

| Polyethylene (PE) | |

| Polypropylene (PP) | |

| Ethylene Vinyl Alcohol Copolymer (EVOH) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Biodegradable and Compostable Materials |

| Doyen / Round Bottom |

| K-Seal |

| Plow / Corner Bottom |

| Flat Bottom |

| Other Product Types |

| Food | Baked Food |

| Snack Food | |

| Pet Food | |

| Confectionery | |

| Other Food | |

| Beverage | |

| Personal Care and Cosmetics | |

| Healthcare and Pharmaceuticals | |

| Industrial and Household Chemicals | |

| Other Application |

| Direct Sales |

| Indirect Sales |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Plastic | Polyethylene Terephthalate (PET) |

| Polyethylene (PE) | ||

| Polypropylene (PP) | ||

| Ethylene Vinyl Alcohol Copolymer (EVOH) | ||

| Other Plastics | ||

| Paper | ||

| Metal Foil | ||

| Biodegradable and Compostable Materials | ||

| By Product Type | Doyen / Round Bottom | |

| K-Seal | ||

| Plow / Corner Bottom | ||

| Flat Bottom | ||

| Other Product Types | ||

| By Application | Food | Baked Food |

| Snack Food | ||

| Pet Food | ||

| Confectionery | ||

| Other Food | ||

| Beverage | ||

| Personal Care and Cosmetics | ||

| Healthcare and Pharmaceuticals | ||

| Industrial and Household Chemicals | ||

| Other Application | ||

| By Distribution Channel | Direct Sales | |

| Indirect Sales | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast will global demand for stand-up pouches grow between 2026 and 2031?

The market is projected to advance at a 5.29% CAGR, lifting value from USD 15.27 billion in 2026 to USD 19.76 billion by 2031.

Which material type shows the quickest expansion?

Biodegradable & Compostable materials are on track for a 6.07% CAGR through 2031.

Why are flat-bottom pouches gaining popularity at retail?

Their stable base removes the need for secondary cartons, cuts logistics costs by up to 20% and offers a larger print area for branding.

What is the biggest regulatory force shaping material choice?

The EU Packaging and Packaging Waste Regulation 2025/40 sets recyclability and PFAS bans that accelerate the shift to mono-material laminates.

Which region is expected to post the strongest growth?

The Middle East and Africa region is forecast to rise at a 6.23% CAGR, supported by new aseptic dairy lines and expanding agribusiness exports.

How concentrated is supplier power in this space?

The combined share of the five largest converters stands near 42%, giving the market a moderately consolidated profile.

Page last updated on: