Pouch Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

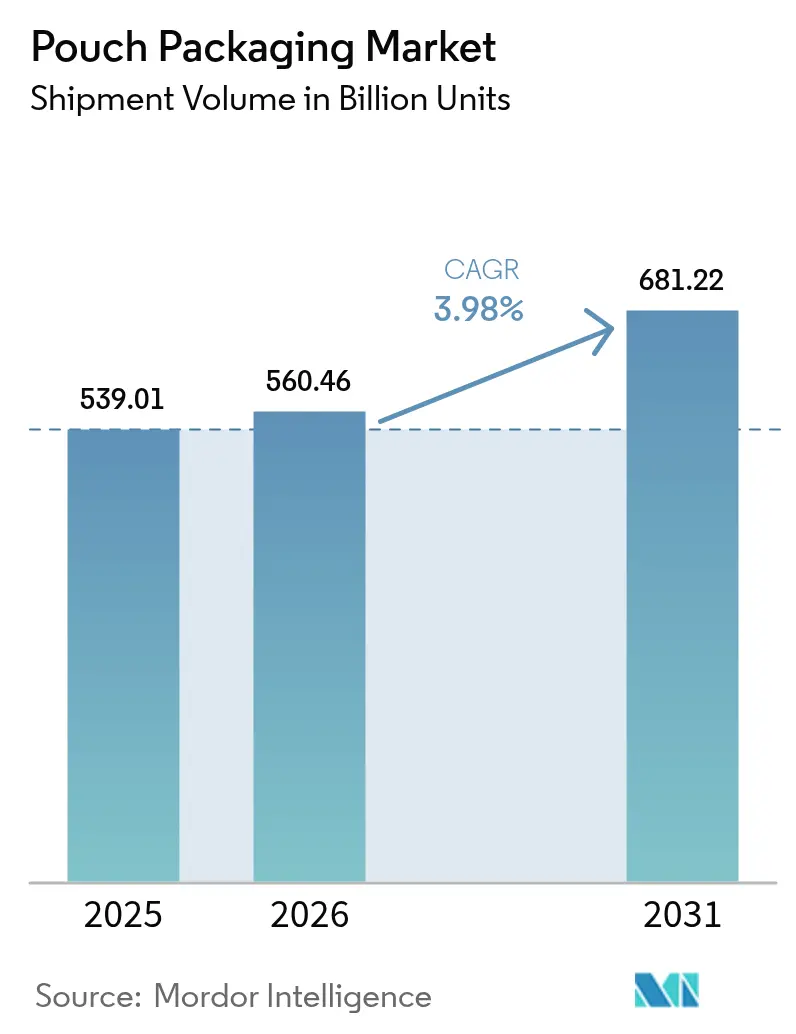

| Market Volume (2026) | 560.46 Billion units |

| Market Volume (2031) | 681.22 Billion units |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pouch Packaging Market Analysis by Mordor Intelligence

The pouch packaging market size was valued at USD 539.01 billion in 2025 and estimated to grow from USD 560.46 billion in 2026 to reach USD 681.22 billion by 2031, at a CAGR of 3.98% during the forecast period (2026-2031). This steady trajectory underscores the pouch packaging market’s transition from rapid early-stage growth to a more measured expansion supported by e-commerce logistics, convenience food trends, and tightening sustainability regulations. Brand owners continue to favor material-efficient flexible packs over rigid formats, while regulatory bodies endorse lightweight solutions that cut transport emissions. Technology investments now prioritize mono-material barrier films and recyclability compliance, shifting competitive advantage away from pure scale economics.

Key Report Takeaways

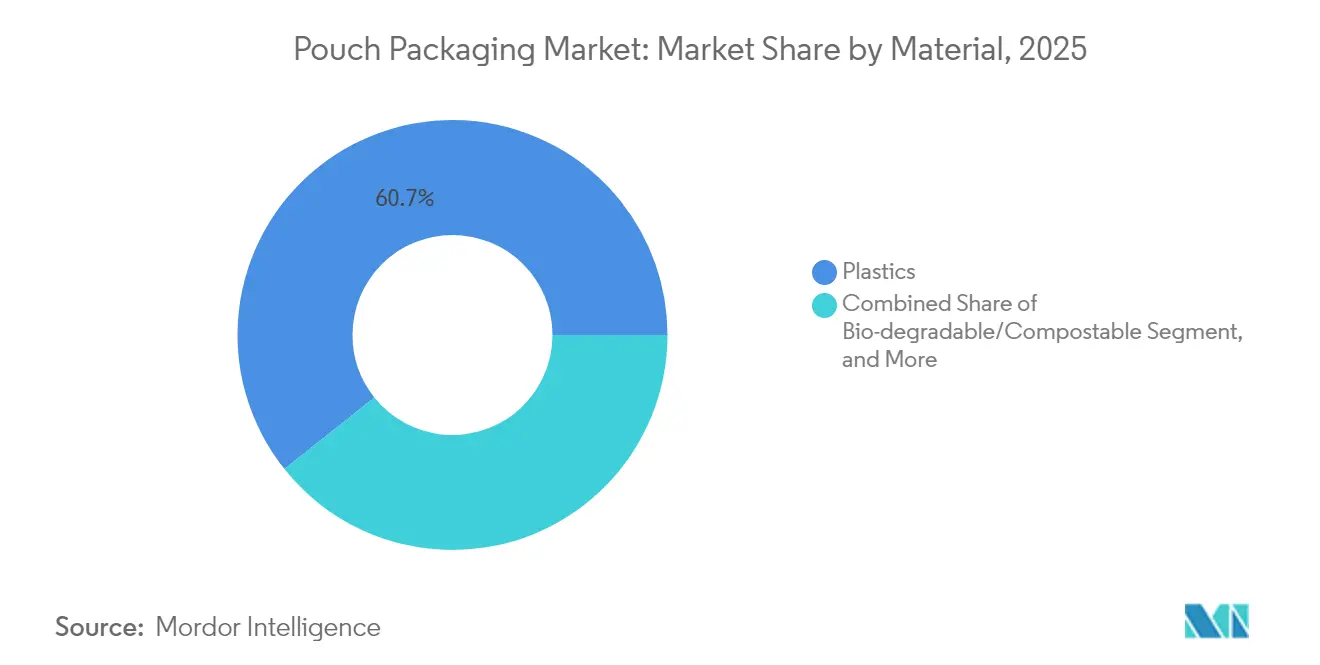

- By material, plastics led with a 60.72% pouch packaging market share in 2025, whereas bio-degradable and compostable substrates are projected to post the fastest 6.05% CAGR to 2031.

- By product type, flat pouches commanded 36.33% of the pouch packaging market size in 2025, while stand-up formats are set to expand at a 5.43% CAGR through 2031.

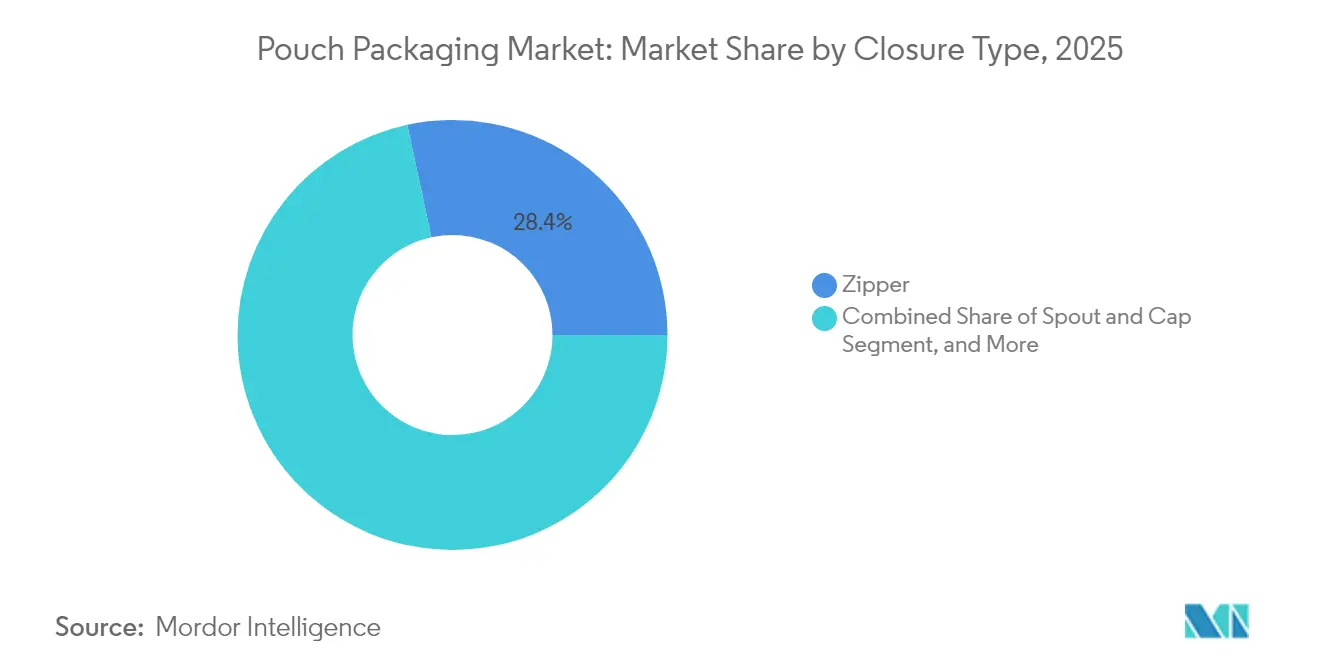

- By closure, zipper systems held 28.38% of the pouch packaging market share in 2025; spout-and-cap solutions are expected to grow at a 5.61% CAGR to 2031.

- By end-user, food applications accounted for 38.42% of the pouch packaging market size in 2025, and personal care and cosmetics are forecast to advance at a 5.88% CAGR to 2031.

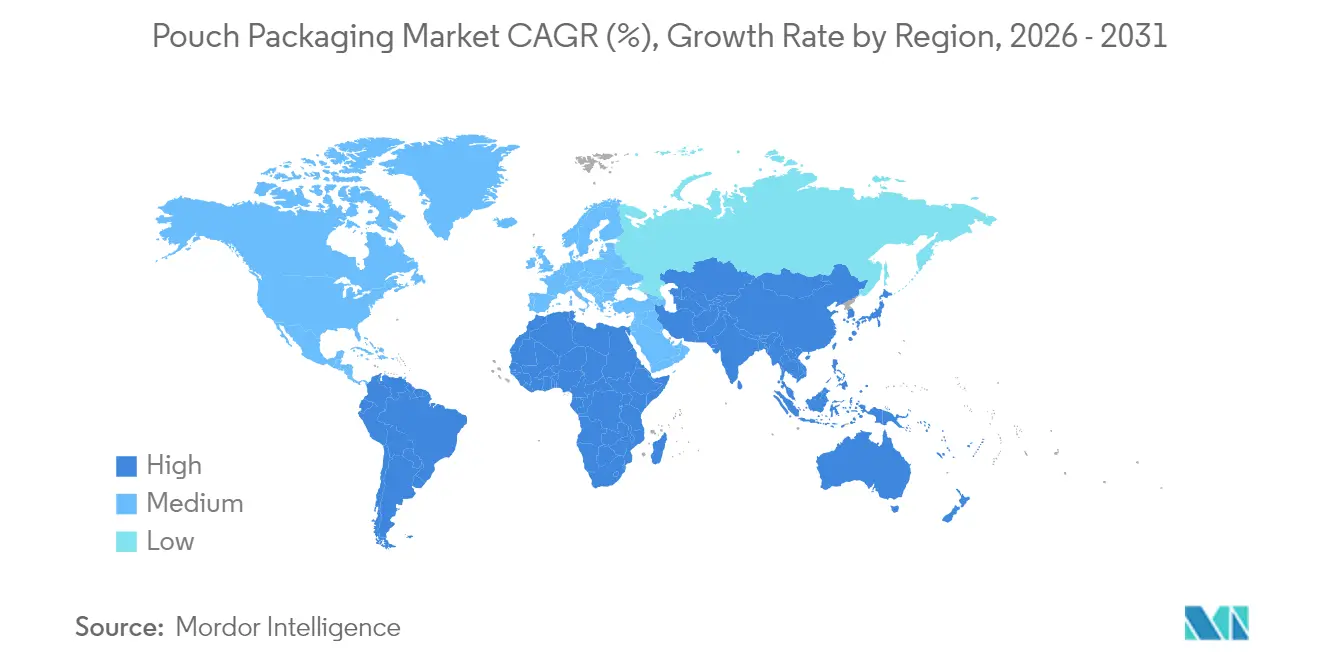

- By geography, Asia-Pacific captured a 39.54% pouch packaging market share in 2025 and is projected to record the highest 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pouch Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for cost-effective packaging and brand differentiation | +1.2% | Global, premium focus in North America and Europe | Medium term (2-4 years) |

| Surge in convenience and ready-to-eat food consumption | +0.9% | Asia-Pacific core, spill-over to global urban centers | Short term (≤ 2 years) |

| Sustainability-driven shift toward lightweight flexible packs | +0.8% | Europe and North America regulatory-driven, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Acceleration of e-commerce and direct-to-consumer logistics | +0.7% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Expansion of spouted pouches in industrial bulk applications | +0.4% | Industrial regions – North America, Europe, China | Medium term (2-4 years) |

| High-barrier mono-material film breakthroughs enabling recyclability | +0.3% | Technology leaders – Europe, North America, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Cost-Effective Packaging and Brand Differentiation

Inflationary pressure on consumer goods margins intensifies the search for packaging formats that cut material usage without compromising shelf appeal. Pouches typically use 70% less substrate than comparable rigid packs and provide a larger printable surface that supports high-resolution graphics. ProAmpac’s 2024 report shows curbside-recyclable pouches delivering 15-20% material cost savings for brand owners. Smaller brands leverage these economics to match the visual impact of multinationals, fostering market fragmentation and stimulating additional unit volumes across price-sensitive categories.

Surge in Convenience and Ready-to-Eat Food Consumption

Rising urbanization and smaller household sizes translate into greater reliance on single-serve, microwave-ready meals best suited to flexible formats. USDA data indicates 12% annual growth in ready meals across China’s tier-2 cities, with pouches gaining share due to uniform heating and steam venting capabilities. Premium baby-food players such as Once Upon a Farm capitalize on spouted pouches that extend shelf life and justify price premiums through superior functionality.

Sustainability-Driven Shift Toward Lightweight Flexible Packs

Lifecycle assessments consistently rank pouches ahead of rigid alternatives on greenhouse-gas emissions and transport efficiency. The EU Packaging and Packaging Waste Regulation mandates recyclability and material reduction targets that favor high-yield flexible solutions.[1]European Commission, “Packaging and Packaging Waste Regulation Implementation,” European Commission, ec.europa.eu Huhtamaki’s blueloop range demonstrates how mono-material PP and PE films now deliver barrier performance once reserved for multi-layer structures, aligning sustainability with functional needs

Acceleration of E-Commerce and Direct-to-Consumer Logistics

Online retail emphasizes dimensionally optimized, damage-resilient packs that survive automated sortation lines. Flexible pouches compress to minimize void fill, lowering parcel costs and carbon footprints. Sealed Air’s LIQUIBOX platform enables direct-to-consumer liquids once too heavy or breakable for rigid containers. Fulfillment centers report fewer breakages and higher throughput when switching to flexible designs, reinforcing adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating environmental and recycling challenges | -0.6% | Global, most acute in Europe and developed APAC | Short term (≤ 2 years) |

| Volatility in plastic-resin feedstock prices | -0.4% | Global, supply-chain dependent regions most affected | Short term (≤ 2 years) |

| Competition from emerging fiber-based flexible formats | -0.3% | North America and Europe primarily, expanding to APAC | Medium term (2-4 years) |

| Supply constraints for bio-based high-barrier resins | -0.2% | Global, concentrated in premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Environmental and Recycling Challenges

Flexible-film recycling infrastructure lags far behind that of PET bottles or metal cans, exposing brands to Extended Producer Responsibility fees. The Flexible Packaging Association notes only 4% of flexible films are mechanically recycled in the United States, leaving converters to fund costly take-back schemes. Meanwhile, proposed PFAS bans threaten barrier chemistries vital for food safety, creating uncertainty that slows capital spending on new lines.

Volatility in Plastic-Resin Feedstock Prices

Resin inputs represent nearly 70% of variable cost for pouch manufacturers. Supply disruptions or oil-price spikes can raise polyethylene and polypropylene spot prices by 20-30% within weeks, squeezing converters unable to pass costs along quickly. Asia-Pacific’s rapid demand growth accentuates regional imbalances, challenging smaller firms that rely on imported pellets and lack hedging capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastics Dominance Faces Bio-Material Disruption

Plastics retained a 60.72% pouch packaging market share in 2025, anchored by the affordability and processability of polyethylene and polypropylene. Yet bio-based and compostable materials are gaining a 6.05% CAGR foothold as regulators signal a future where end-of-life solutions trump historic cost-performance ratios. Leading converters integrate plant-derived resins with barrier coatings based on nanofibrillated cellulose that rival EVOH in oxygen-blocking capacity.

The pouch packaging market rewards mono-material breakthroughs that ensure recyclability while maintaining product protection. Patent filings for simplified structures rose 40% in 2024, demonstrating a material-science arms race. Converters investing in compatibilizers and solvent-free lamination position themselves to meet EU recyclability quotas ahead of the 2030 deadline. Meanwhile, aluminum foil usage holds steady in premium applications that demand near-zero oxygen ingress, though downgauging efforts continue.

By Product Type: Stand-Up Innovation Drives Premiumization

Flat formats still constitute 36.33% of the pouch packaging market size, reflecting entrenched applications in dry goods. Stand-up pouches, however, outpace at a 5.43% CAGR as retailers reward the vertical billboard effect on crowded shelves. Brands exploit gusseted bases and photo-realistic printing to signal premium value, even in commoditized categories such as snack nuts or pet treats.

Function-specific variants proliferate. Retort pouches enable shelf-stable ready meals, aseptic laminates chase beverage opportunities, and stick packs dominate single-serve nutraceuticals. Integrated rollstock-to-fill workflows deliver cost advantages for high-volume SKUs, whereas premade formats suit small batch runs. Gualapack’s integrated laminate, injection, and filling solution in Brazil exemplifies how end-to-end control lowers failure rates while accelerating time to market.

By Closure Type: Spout Systems Gain Functional Advantage

Zipper closures ruled 28.38% of the pouch packaging market share in 2025, offering simple resealability for snacks and dry mixes. Spout-and-cap systems are predicted to expand at a 5.61% CAGR, driven by liquid products seeking controlled dispensing for everything from refills of household cleaners to wine cocktails.

Designers increasingly specify mono-material PP or PE spouts that weld seamlessly to film structures, minimizing disassembly hurdles in recycling streams. Slider and valve closures cater to high-frequency opening needs or degassing requirements in coffee and industrial applications. Cost considerations remain decisive, yet a clear shift toward functionally differentiated closures signals a willingness to pay for consumer convenience.

By End-User Industry: Personal Care Adoption Accelerate

Food retained 38.42% of the overall pouch packaging market size in 2025, thanks to strong penetration in confectionery, frozen, and dry goods. Personal care and cosmetics are set to grow at a 5.88% CAGR as beauty brands embrace flexible packs for refill concepts and travel-friendly SKUs. High oxygen- and light-barrier laminates protect sensitive formulations, enabling prestige skincare to tout sustainability credentials without sacrificing product efficacy.

Pharmaceutical and medical segments value tamper evidence and dosage accuracy, with single-use sachets meeting safety protocols in clinics and home-health settings. Liquid home-care concentrates exploit the lightweight economics of spouted pouches, reducing shipping weight by up to 80% compared with rigid HDPE bottles. Across sectors, alignment with retailer refill stations and take-back initiatives is becoming a significant purchasing criterion.

Geography Analysis

Asia-Pacific led with 39.54% of the pouch packaging market share in 2025 and is forecast to record a 6.74% CAGR to 2031. China’s rapid shift toward packaged foods, propelled by organized retail and stringent food-safety laws, keeps demand buoyant. India’s modern trade expansion drives volume gains, while South Korea’s K-Beauty ecosystem exports flexible cosmetic packs worldwide. Regional converters benefit from proximity to virgin resin suppliers and cost-competitive labor, reinforcing localized supply chains even as multinational brand owners demand global harmonization of pack specifications.

North America exhibits a mature demand profile focused on premiumization and e-commerce readiness. Lightweight designs translate into shipping cost savings under dimensional-weight tariffs, pushing retailers toward house-brand pouch adoption. Europe’s regulatory drive toward recyclability accelerates mono-material rollouts, positioning flexible packs ahead of rigid glass and multilayer cartons on lifecycle metrics. Scandinavian markets pilot deposit schemes for flexible films, providing data for broader EU implementation.

South America and the Middle East, and Africa collectively offer emerging upside. Brazil’s dairy sector adopts spouted pouches for yogurt drinks, citing cold-chain energy savings. Gulf Cooperation Council nations import pouch-packed ready meals that withstand desert logistics, and African megacities rely on small-sachet formats for affordable daily necessities. Infrastructure hurdles remain, yet demographic momentum and rising disposable incomes will progressively close the gap with developed regions.

Mordor Intelligence provides coverage of the pouch packaging market across other key regional markets, including Latin America, Europe, North America, Asia, and Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Brazil, Italy, Canada, India, and Nigeria incorporating local coverage and market participation, as required.

Competitive Landscape

The pouch packaging industry balances moderate fragmentation with rapid technology-led consolidation. Patent activity in mono-material barriers now eclipses cost reduction as the primary arena of rivalry. Huhtamaki’s blueloop platform illustrates how proprietary polymer chemistries can lock in customers concerned about EU recyclability thresholds.[3]Huhtamaki, “blueloop Flexibles Platform Overview,” Huhtamaki, huhtamaki.com

Mergers and acquisitions center on know-how rather than footprint. TOPPAN’s USD 1.8 billion purchase of Sonoco’s Thermoformed and Flexible Packaging unit secures an instant network of 22 plants and 700 patents across the Americas. Converters that lack specialty film science pivot toward niche regional markets or co-packing services, avoiding direct clashes with innovation leaders

Capital expenditure increasingly targets recycling-compatible infrastructure over capacity additions. Chemical-recycling partnerships promise long-term feedstock stability, yet most remain pilot scale. As regulators impose Extended Producer Responsibility fees, companies that demonstrate closed-loop solutions gain a tender advantage with multinational brands. Consequently, intellectual property in solvent-free coatings and compatibilizers becomes strategic currency.

Pouch Packaging Industry Leaders

Aluflexpack Group

Constantia Flexibles Group GmbH

ProAmpac Intermediate, Inc.

Amcor plc

Bischof + Klein SE and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ProAmpac showcased new recyclable and compostable pouch solutions at SPC Impact 2025, underscoring its material-science roadmap for low-carbon flexible packs.

- April 2025: Sonoco completed the USD 1.8 billion sale of its Thermoformed and Flexibles Packaging business to TOPPAN Holdings, transferring 4,500 employees and 22 plants.

- February 2025: Amcor entered an agreement to acquire India-based Phoenix Flexibles to expand local capacity for food, home-care, and personal-care pouches.

- January 2025: ProAmpac introduced its ProActive PCR flexible-pouch range, incorporating higher post-consumer recycled content for food and non-food applications.

Global Pouch Packaging Market Report Scope

Pouch packaging is a flexible packaging product that is used for flowable liquid products. The study covers the pouch packaging market tracked in terms of volume (units). Pouch packaging is a flexible packaging product made from barrier films or paper or foil, depending on the end-user requirement. The study analyzes the factors that impact geopolitical developments in the studied market based on the prevalent base scenarios, key themes, and end-user industries-related demand cycles.

The Pouch Packaging Market is Segmented by Material Type ( Paper, Plastic and Aluminum), by Resin Type - Plastic ( Polyethylene, Polypropylene, PET, PVC, EVOH, Other Resins), by Product ( Flat ( Pillow and Side Seal), Stand Up), by End-User Industry (Food (Candy & Confectionery, Frozen Foods, Fresh Produce, Dairy Products, Dry Foods, Meat, Poultry, And Seafood, Pet Food, Other Food Products (Seasonings & Spices, Spreadables, Sauces, Condiments, etc.)), Beverage, Medical and Pharmaceutical, Personal Care and Household Care, and Other End-User Industries) and Geography (North America [United States and Canada], Europe [France, Germany, Italy, United Kingdom, Spain, Poland, Nordic and Rest of Europe], Asia-Pacific [China, India, Japan, Thailand, Indonesia, Vietnam, Australia and New Zealand, and Rest of Asia-Pacific], Latin America [Brazil, Mexico, Colombia, and Rest of Latin America], and Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, South Africa, Nigeria, Morocco and Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of volume (units) for all the above segments.

| Plastics | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride resin (PVC) | |

| Other Plastics | |

| Paper | |

| Aluminum Foil | |

| Bio-degradable/Compostable |

| Flat (Pillow and Side-Seal) |

| Stand-Up |

| Spouted |

| Retort |

| Aseptic |

| Stick-Pack / Sachet |

| Rollstock / Premade Pouch |

| Zipper |

| Spout and Cap |

| Tear-Notch |

| Slider |

| Other Closure Type |

| Food | Candy and Confectionery |

| Frozen Foods | |

| Fresh Produce | |

| Dairy Products | |

| Dry Foods and Cereals | |

| Meat, Poultry and Seafood | |

| Pet Food | |

| Other Foods (Sauces, Condiments, Spreads) | |

| Beverage | Alcoholic |

| Non-Alcoholic | |

| Medical and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Home Care and Household | |

| Other End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Material | Plastics | Polyethylene (PE) | |

| Polypropylene (PP) | |||

| Polyethylene Terephthalate (PET) | |||

| Polyvinyl Chloride resin (PVC) | |||

| Other Plastics | |||

| Paper | |||

| Aluminum Foil | |||

| Bio-degradable/Compostable | |||

| By Product Type | Flat (Pillow and Side-Seal) | ||

| Stand-Up | |||

| Spouted | |||

| Retort | |||

| Aseptic | |||

| Stick-Pack / Sachet | |||

| Rollstock / Premade Pouch | |||

| By Closure Type | Zipper | ||

| Spout and Cap | |||

| Tear-Notch | |||

| Slider | |||

| Other Closure Type | |||

| By End-User Industry | Food | Candy and Confectionery | |

| Frozen Foods | |||

| Fresh Produce | |||

| Dairy Products | |||

| Dry Foods and Cereals | |||

| Meat, Poultry and Seafood | |||

| Pet Food | |||

| Other Foods (Sauces, Condiments, Spreads) | |||

| Beverage | Alcoholic | ||

| Non-Alcoholic | |||

| Medical and Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Home Care and Household | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the pouch packaging market?

The pouch packaging market size is 560.46 billion units in 2026.

How fast is global demand for pouch formats projected to grow?

Volumes are expected to rise at a 3.98% CAGR, reaching 681.22 billion units by 2031.

Which region leads in both scale and growth?

Asia-Pacific holds a 39.54% share in 2025 and is set to grow at 6.74% CAGR through 2031.

How are sustainability regulations affecting pack design?

Rules such as the EU PPWR are accelerating the shift to mono-material pouches that enable mechanical recycling.

Which materials are gaining traction over conventional plastics?

Bio-degradable and compostable substrates are expanding at a 6.05% CAGR as regulators push for circularity.

What closure type is growing fastest?

Spout-and-cap systems are forecast to grow at 5.61% CAGR due to rising liquid applications.

Page last updated on: