Russia Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

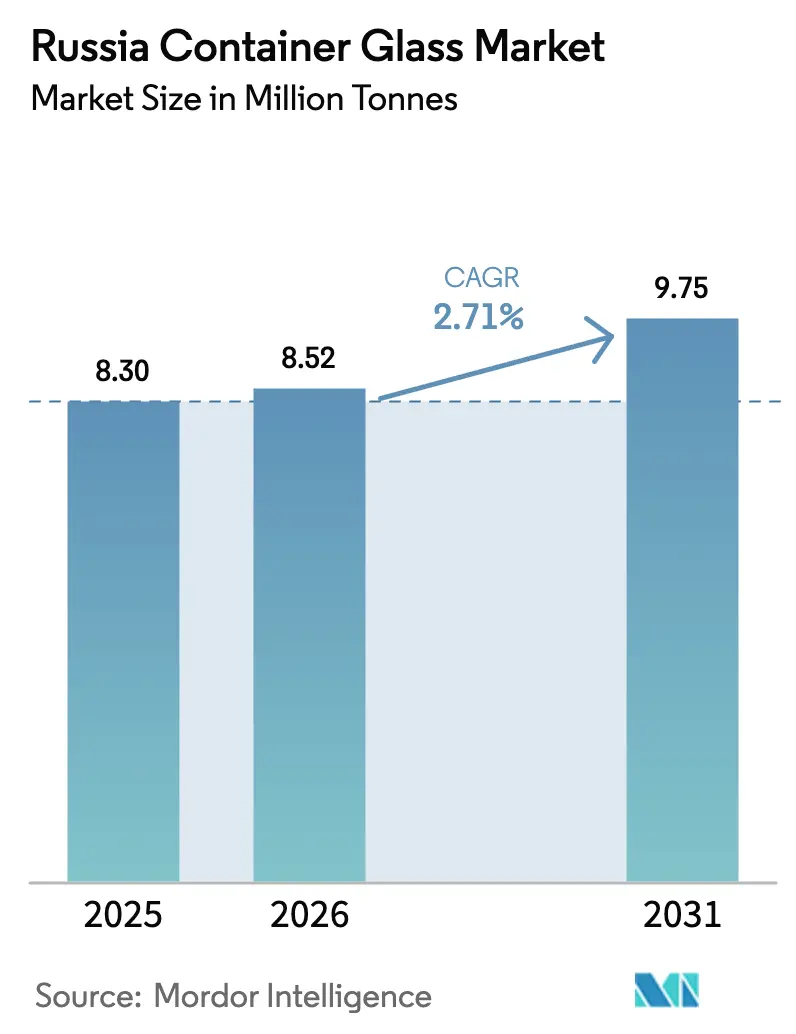

| Base Year Market Size (2025) | 8.30 Million tonnes |

| Market Volume (2026) | 8.52 Million tonnes |

| Market Volume (2031) | 9.75 Million tonnes |

| Growth Rate (2026 - 2031) | 2.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Container Glass Market Analysis by Mordor Intelligence

Russia Container Glass Market size in 2026 is estimated at 8.52 million tonnes, growing from 2025 value of 8.30 million tonnes with 2031 projections showing 9.75 million tonnes, growing at 2.71% CAGR over 2026-2031. Domestic demand from the beverages, pharmaceuticals, and premium food segments underpins expansion, even after glass production fell by about 60% in 2022-2024 due to Western sanctions that cut export outlets.[1]Ukrainian Energy, “Collapse of Russian Putinomics: Industrial Collapse Continues,” ua-energy.org Moscow’s premium consumption, Saint Petersburg’s design-driven packaging, improving recycling policies, and rising sustainability awareness continue to steer growth. Capacity rationalization by leading producers, combined with integration into cullet supply chains, is helping to stabilize furnace utilization. Meanwhile, energy-efficiency projects and automated inspection systems are helping to mitigate cost pressure. Still, logistical complexity in Siberia and energy volatility in the Northwest temper momentum.

Key Report Takeaways

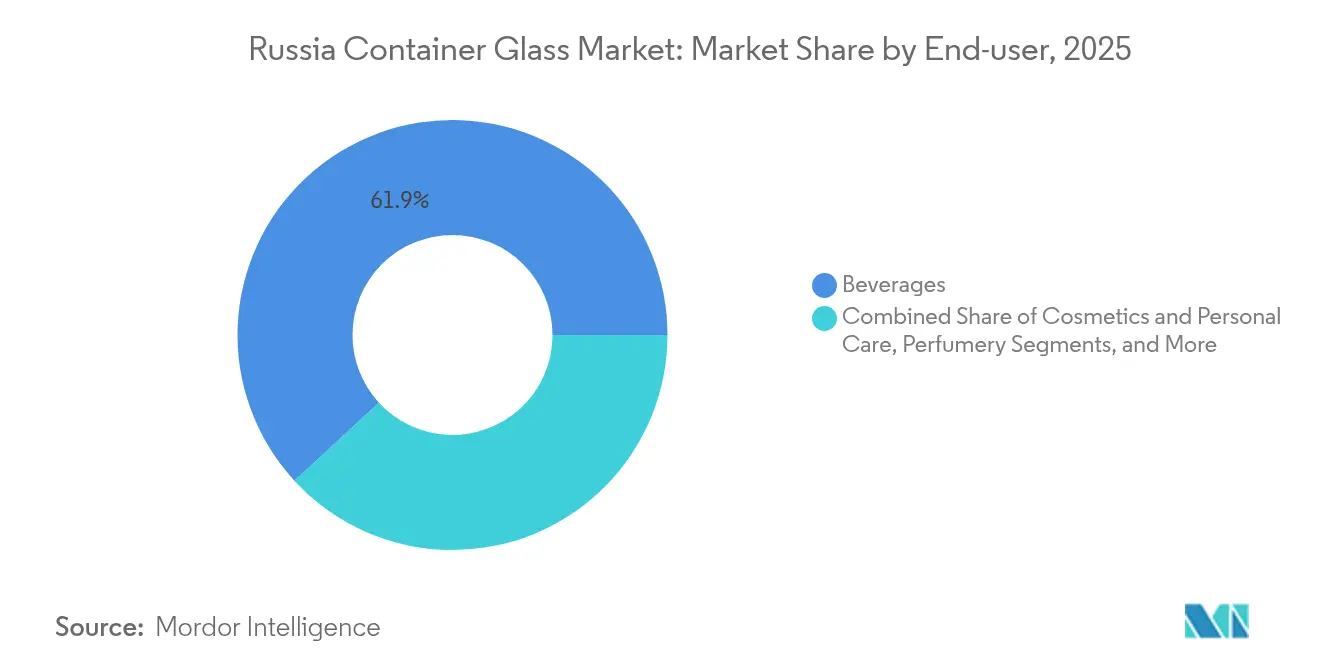

- By end-user, beverages accounted for 61.85% of the Russia container glass market share in 2025.

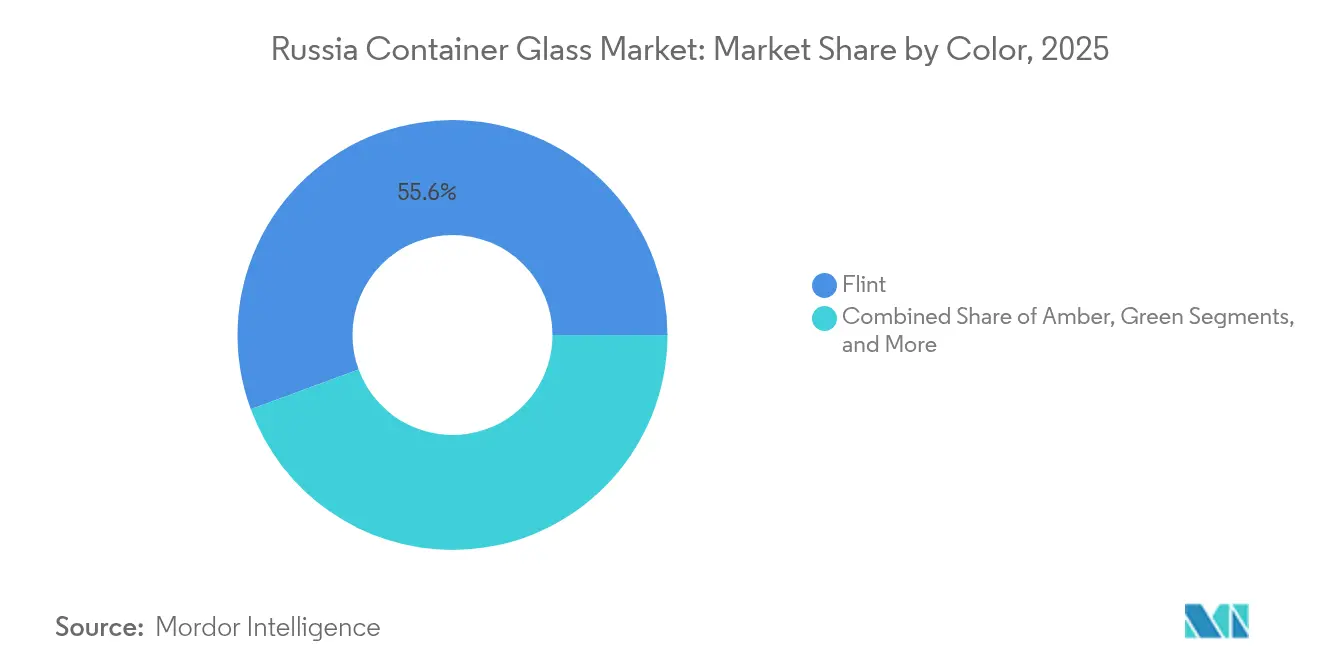

- By color, the Russia container glass market size for the amber glass segment is projected to grow at a 4.56% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand in Moscow drives glass packaging | +0.8% | Moscow Federal City, Central FD | Medium term (2-4 years) |

| Shift towards premium packaging in Saint Petersburg region | +0.6% | Northwestern FD | Medium term (2-4 years) |

| Expanding distribution networks boost Siberian glass industry | +0.4% | Siberian FD | Long term (≥ 4 years) |

| Volga region industrial diversity supports container glass production | +0.5% | Volga FD | Medium term (2-4 years) |

| Government recycling policies encourage local glass manufacturing | +0.3% | Nationwide | Long term (≥ 4 years) |

| Growing sustainability awareness promotes eco-friendly glass packaging | +0.4% | Major urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand in Moscow Drives Glass Packaging

Moscow channels the country’s highest purchasing power into premium food and beverage categories that rely on glass for shelf differentiation and perceived quality. Local authorities have implemented bell-type collection bins and private operator contracts since 2018, increasing the city’s municipal solid waste recycling rate from 20% in 2019 to a 60% goal by 2024, thereby expanding the cullet supply.[2]E3S Web Conferences, “Trends in the rational use of municipal solid waste,” e3s-web.org Robust demand for imported wines and craft spirits reinforces the Russia container glass market, while consumer willingness to pay for sustainable packaging fuels repeat orders. This virtuous cycle secures furnace load factors for nearby plants and incentivizes investment in design-rich bottle formats.

Shift Towards Premium Packaging in Saint Petersburg Region

Saint Petersburg’s status as a cultural hub and Baltic trade gateway lifts expectations for aesthetics and tactile quality in packaging, making glass bottles and jars the preferred medium for gourmet foods, wines and craft beverages. The regional workforce carries deep glass-making expertise stemming from a long industrial heritage, which supports value-added decoration and short production runs. Local hospitality venues and tourism flows strengthen demand for distinctive bottle shapes. Regulators in the Northwestern Federal District are steering procurement toward domestic suppliers, helping the Russia container glass market capture share previously held by imported packaging.

Expanding Distribution Networks Boost Siberian Glass Industry

Rail hub upgrades and new warehouse nodes from Omsk to Novosibirsk shorten lead times to resource-extraction and food-processing clusters across Siberia. Although freight distances remain long, modernized multimodal corridors reduce breakage and logistics cost per ton, enabling profitable delivery of heavier glass containers. Several beverage producers have announced line extensions into ready-to-drink teas and flavored spirits for Siberian consumers, anchoring predictable offtake volumes for local furnaces. Consequently, demand growth in the Russian container glass market is expected to emerge gradually in eastern territories once new capacity reaches commercial scale.

Volga Region Industrial Diversity Supports Container Glass Production

The Volga Federal District is home to dense networks of chemical, food, and automotive plants that utilize glass bottles and jars for internal consumption and inter-regional trade. Abundant silica sand deposits, natural gas pipelines, and brownfield furnace sites lower input costs, attracting both domestic and foreign investment. Manufacturers leverage rail links that radiate toward Moscow, the Urals, and the South to balance distribution. This multi-industry pull underpins steady orders, shielding the Russia container glass market from single-segment volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Logistical challenges increase costs in Eastern Russia | -0.7% | Far Eastern and Siberian FD | Medium term (2-4 years) |

| Energy and resource constraints affect Northwestern production | -0.9% | Northwestern FD | Short term (≤ 2 years) |

| Competition from alternative packaging reduces Southern glass demand | -0.5% | Southern FD | Medium term (2-4 years) |

| Aging infrastructure limits Central Russia glass manufacturing efficiency | -0.4% | Central and Volga FD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Logistical Challenges Increase Costs in Eastern Russia

Ports such as Vladivostok and Vostochny handle rising container throughput, but inland transport to mining and agri-processing sites remains hindered by sparse rail spurs and seasonal road closures.[3]RBC, “Russian wine outlook 2025,” rbc.ru Weight-to-value dynamics penalize glass bottles compared to lighter PET, prompting brand owners to adopt hybrid packaging or local canning. Higher diesel prices and wagon shortages increase delivered costs, which restrict the Russia container glass market beyond coastal cities, delaying sizable demand shifts until the infrastructure matures.

Energy and Resource Constraints Affect Northwestern Production

Gas pipeline maintenance, currency volatility in imported refractories and new emission fees for calcium carbonate at 53.8 RUB/ton and carbon particulates at 204.04 RUB/ton raise operating expenses for Saint Petersburg and Leningrad-area furnaces. Tight furnace rebuild schedules coincide with H1 2025 maintenance for six large tanks, briefly removing 70-80 days of capacity and creating bottle shortages for brewers RBC.RU. Manufacturers accelerate oxy-fuel conversion and advanced batch pre-heating, but capital outlays strain cash flow, potentially suppressing near-term output in the Russia container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverage Dominance With Pharmaceutical Upswing

Beverages generated 61.85% of the Russian container glass market share in 2025, driven by 83 million deciliters of vodka output and the expansion of alternative spirits lines. Total demand is forecast to rise in tandem with non-alcoholic labeling mandates that require robust, mark-ready bottle formats. The Russia container glass market size allocated to beverages benefits from scale economics, national brand marketing, and the cultural premium placed on glass for spirits. A countervailing factor is the cyclical heat load on furnaces; maintenance shutdowns anticipated in 2025 could temporarily tighten the supply and prompt breweries to consider imports or lighter packaging if bottle inventories dip.

Pharmaceutical containers, though smaller in tonnage, are projected to outpace all other applications with a 3.92% CAGR as domestic drug plants expand under import-substitution policies. Amber and Type II flint vials dominate antibiotics, vaccines, and nutraceuticals, aided by government procurement frameworks designed to localize production. Growth in serology and intravenous solutions also encourages the adoption of ISO-compliant molded glass formats. Consequently, the Russia container glass market size for injectable and oral dose packaging is expected to nearly double its kiloton contribution by 2030, providing a hedge against beverage cyclicality.

By Color: Flint Leadership, Amber Momentum

Flint maintained 55.62% of the Russian container glass market share in 2025, as its clarity suits mass-market vodka, juices, and table sauces. Furnace campaigns favor flint owing to broad downstream acceptance and minimal colorant overheads. However, contamination thresholds limit recycled content to around 40% before optical degradation occurs, leaving cost savings modest compared to colored melts. As sustainability targets become tighter, some beverage customers may opt for colored bottles to maximize cullet usage.

Amber glass will capture faster volume gains, advancing at a 4.56% CAGR, driven by pharmaceutical sterilization requirements and the brand aesthetics of craft spirits. UV-blocking performance extends the shelf life of biologics and artisanal beer, while color-tolerant cullet streams support recycled content of nearly 70%, reducing energy consumption in the furnace by 2-3% for every 10% of cullet added. Premium distillers are increasingly deploying embossing and metallic labeling on amber bottles to differentiate themselves in saturated vodka aisles. Consequently, the Russia container glass market share of amber is set to inch upward through 2031 despite flint’s entrenched base.

Geography Analysis

Moscow and the Central Federal District form the core demand nucleus of the Russia container glass market, absorbing a majority of premium bottles for spirits, soft drinks, and high-end food preserves. Proximity to media hubs and higher disposable incomes foster rapid product turnover, incentivizing brands to specify heavier flint bottles with embossed logos for shelf impact. The region’s recycling infrastructure, featuring over 5,000 bell-type bins, supplies cullet to plants in Vladimir and Dubna, thereby lowering batch costs and reducing transport miles.

The Northwestern Federal District, led by Saint Petersburg, specializes in premium-design packaging that targets export-oriented confectionery, seafood, and craft alcohol. Baltic Sea proximity facilitates inbound silica sand and outbound filled product flows. Nonetheless, natural gas price swings and furnace rebuild timetables challenge supply reliability, prompting Verallia and Sisecam to share contingency stockpiles and cross-ship from Volga sites when outages occur.

The Volga Federal District’s industrial landscape supports automakers, petrochemicals, and agribusiness, resulting in steady demand for jars and bottles. Abundant raw materials, combined with rail corridors to European Russia, position the Volga region as a balancing producer that helps backfill shortages elsewhere. Siberia and the Far East remain volume laggards due to freight dispersion and container imbalance, but new multimodal depots promise incremental gains. The throughput of 2.16 million TEU across major Far Eastern ports in 2023 underscores the rising trade that will ultimately lift packaging demand once inland routes improve.

Southern regions exhibit higher PET penetration due to fruit-juice clusters, but shifting consumer perceptions of plastic are prompting wineries to adopt thicker green bottles. Meanwhile, Ural and defense-oriented districts have enjoyed a manufacturing revival under sanctions-driven import substitution, spurring container orders for chemicals and specialty lubricants. Centralized ecology legislation obliges all federal subjects to align with 60% waste-sorting objectives by 2025, homogenizing the cullet supply landscape for the Russia container glass market.

Competitive Landscape

The Russian container glass market exhibits moderate concentration, led by Sisecam, Verallia, Avangard-Glass, and regional players such as CHSZ Group. Capital intensity and long furnace lifecycles erect entry barriers; as a result, cumulative furnace capacity de facto dictates market share positions. Sisecam operates sites in Gorokhovets, Pokrovsky, Ufa, Kuban, and Kirishi, with a combined annual capacity of approximately 280,000 tonnes. Meanwhile, Verallia has five furnaces in Mineralnye Vody and Kamyshin, which supply southern and central bottlers.

Strategic moves emphasize vertical integration into soda ash and cullet. Sisecam’s USD 285 million takeover of Ciner’s U.S. soda assets in January 2025 secures a low-cost alkali supply, hedging against fluctuations in the ruble and logistical bottlenecks. Verallia is optimizing furnace scheduling and price modeling following a 25.8% decline in H1 2024 sales in Northern-Eastern Europe; the firm reported volume recovery in Q1 2025 as Russian beverage lines resumed purchases.

Domestic contenders are tailoring their offerings to regional niches: Avangard-Glass supplies Central Russian vodka brands with flint flasks; Vladimir Glass targets pharmaceutical vials; and CHSZ Group focuses on southern wine bottles. Technology adoption features include inline camera inspection, predictive maintenance, and batch automation, which raise yields and enable shorter color campaigns. Many producers pursue ISO 9001, 14001, and 45001 certifications to reassure multinational beverage clients of quality and ESG compliance. The expected consolidation, as evidenced by O-I Glass’s intent to retire 7% of its global tank capacity by mid-2025, could open up acquisition prospects for cash-rich local firms.

Russia Container Glass Industry Leaders

Verallia Packaging

Avangard-Glass

Saverglass Group

Sisecam

Krasnoye Echo LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Ciner Glass secured EUR 504 million (USD 549 million) financing for a Belgian container glass plant of 1,300 t/day.

- July 2025: Construction started on a building-materials plant in Vargashi industrial park, Kurgan region, with RUB 300 million (USD 3.3 million) state support.

- May 2025: Beverage labeling rules under Resolution 887 extended the mandatory digital marking requirement to juices and soft drinks, thereby influencing bottle specifications.

- January 2025: Sisecam completed its USD 285 million purchase of Ciner Group’s U.S. soda ash interests, positioning the firm as the world’s largest soda ash supplier.

Russia Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Russia Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments..

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Russia container glass market in 2026?

It totals 8.52 million tons with a 2.71% CAGR projected to 2031.

Which segment holds the highest share of container glass demand?

Beverage packaging leads with 61.85% share of the Russia container glass market.

What color segment is growing fastest?

Amber bottles are forecast to expand at a 4.56% CAGR through 2031.

Which regions consume the most container glass?

Moscow-centric Central Federal District and Saint Petersburg-led Northwestern Federal District account for the bulk of demand.

What are key challenges facing Russian glass manufacturers?

High energy prices, logistics in Siberia and stricter emission fees weigh on operating costs.

Which companies dominate production capacity?

Sisecam and Verallia head the field, followed by Avangard-Glass and CHSZ Group.

Page last updated on: