Poland Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

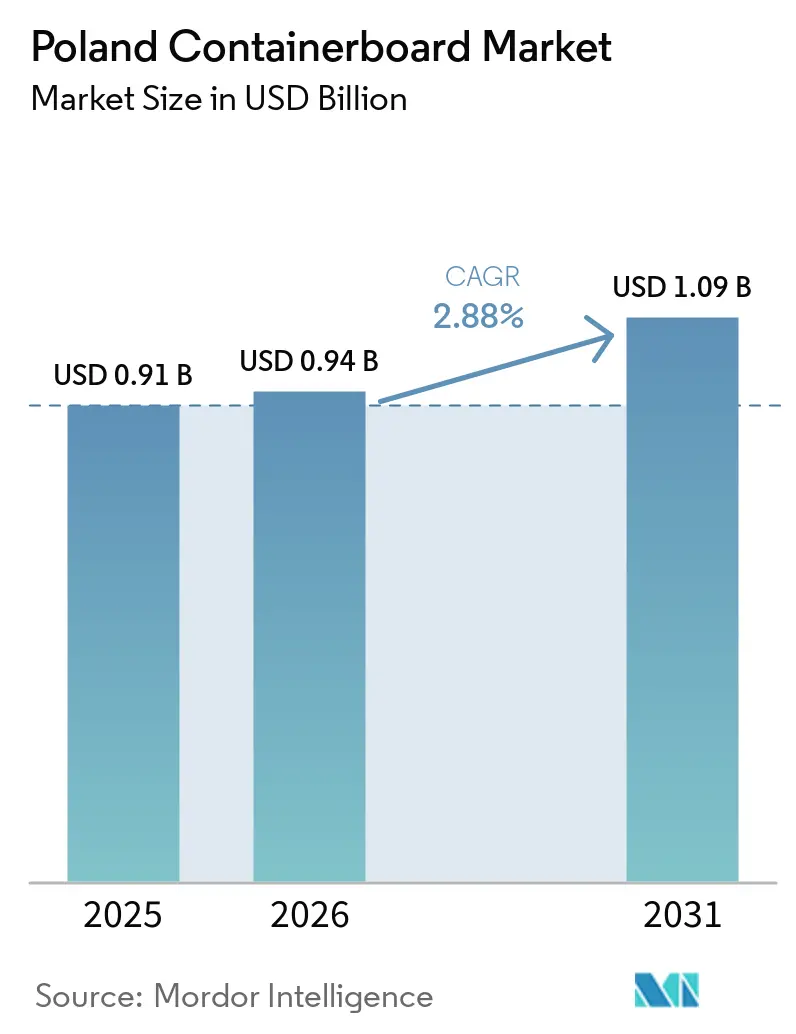

| Base Year Market Size (2025) | USD 0.91 Billion |

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 2.88% CAGR |

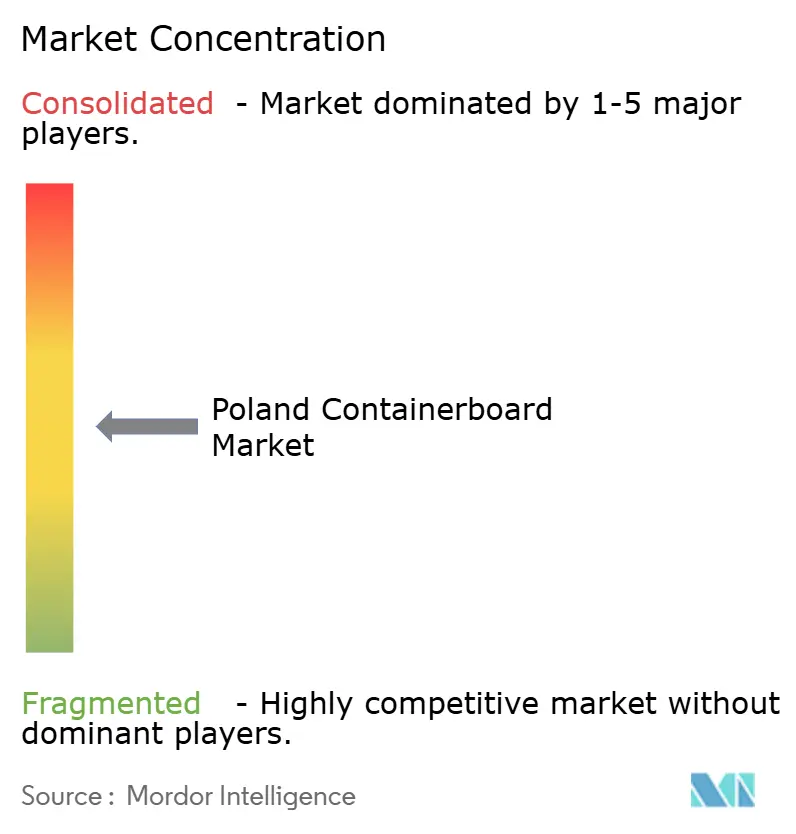

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Containerboard Market Analysis by Mordor Intelligence

The Poland containerboard market size is projected to expand from USD 0.91 billion in 2025 and USD 0.94 billion in 2026 to USD 1.09 billion by 2031, registering a CAGR of 2.88% between 2026 to 2031. The Poland containerboard market is moving through a period where parcel shipping, agri-food exports, and nearshored manufacturing are reinforcing each other and keeping baseline demand firmer than in several nearby markets. Polish mills entered 2026 operating near full capacity, and recycled grade price increases at the start of the forecast period showed that local supply and demand had tightened. The Poland containerboard market also reflects a gradual shift toward higher-performance grades as converters respond to heavier export loads, stricter box specifications, and more demanding industrial applications. Competition remains moderate because a small set of large international producers leads integrated capacity, while regional operators and converters continue to shape pricing and service levels. Margin pressure still matters in the Poland containerboard market because energy volatility and west European overcapacity can weigh on profitability, even as better local price transparency improves procurement visibility and supports more disciplined contracting.

Key Report Takeaways

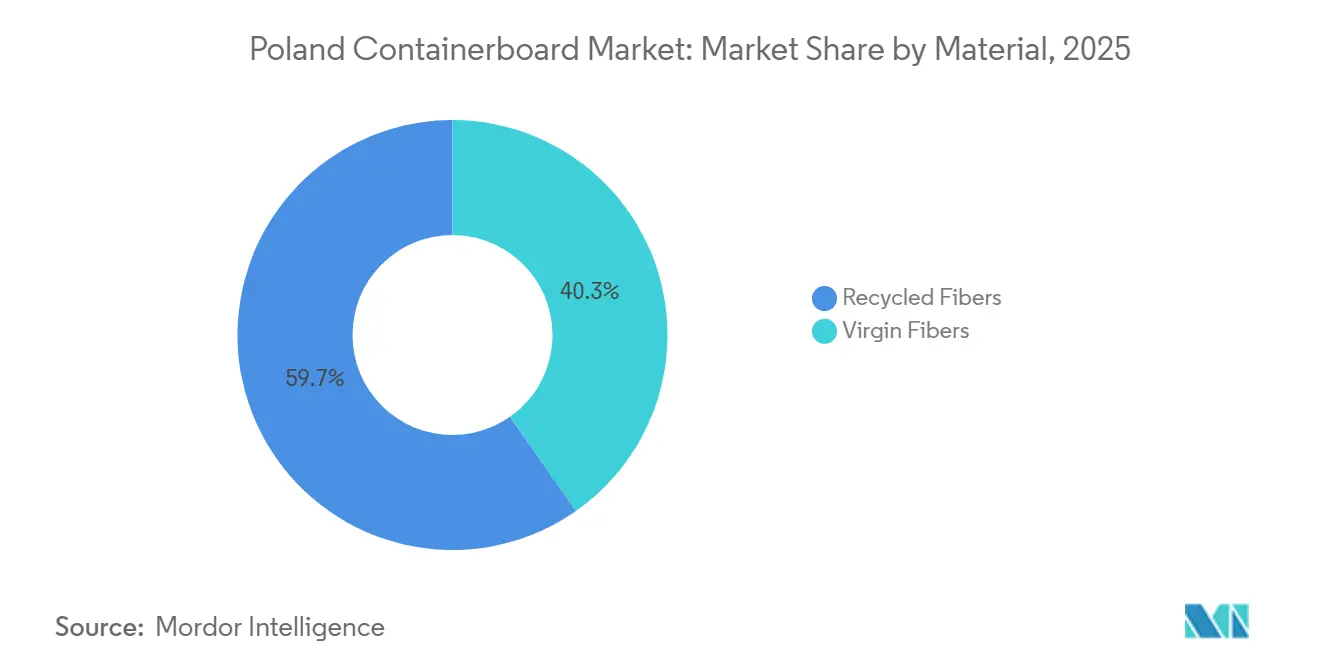

- By material, recycled fibers captured 59.74% of the Poland containerboard market share in 2025.

- By product type, the Poland containerboard market size for the kraftliners segment is forecast to advance at a 3.24% CAGR through 2031.

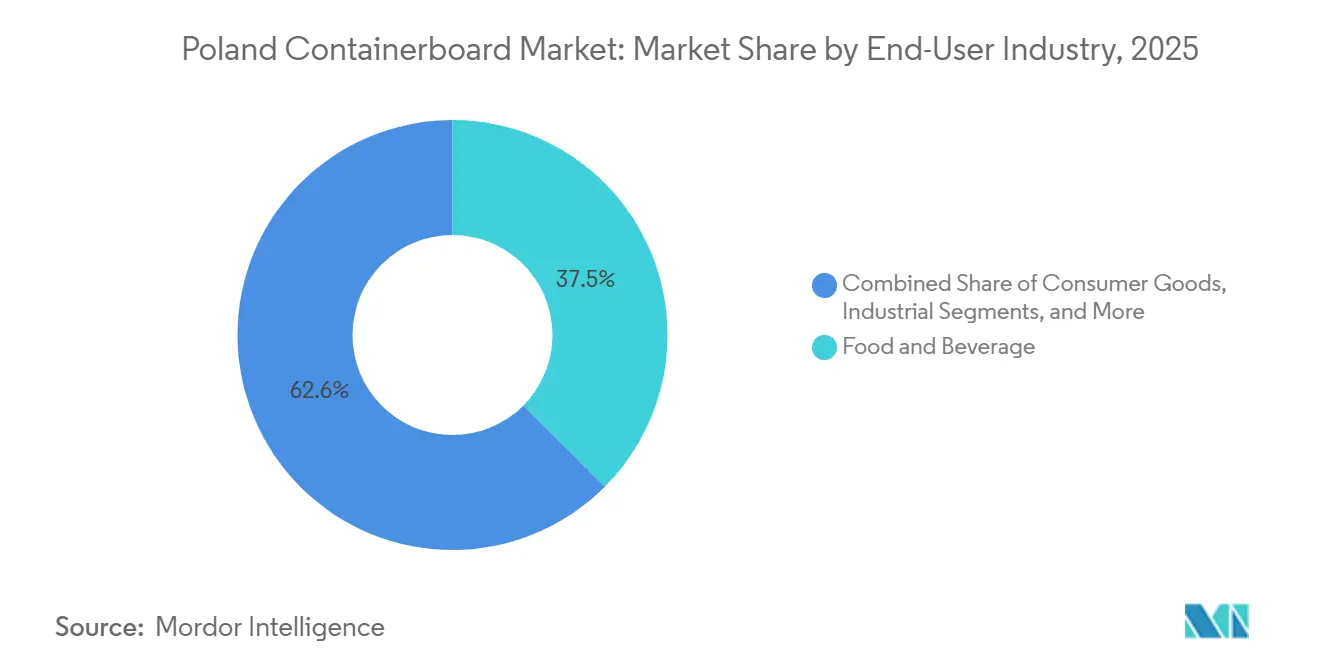

- By end-user industry, food and beverage captured 37.45% of the Poland containerboard market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce-Linked Box Specification Upgrading | +0.7% | National, with concentration in Masovia, Silesia, Łódź logistics corridors | Short term (≤ 2 years) |

| Growth in Recycled-Fiber Packaging Substitution | +0.6% | National, with spillover to EU export markets | Medium term (2-4 years) |

| Food and Beverage Export Packaging Demand | +0.5% | National, with volume concentration in Greater Poland, Pomerania, and Subcarpathia | Medium term (2-4 years) |

| Nearshoring of Appliance and Auto Supply Chains | +0.4% | Silesia, Masovia, Subcarpathia, spillover to Lower Silesia | Long term (≥ 4 years) |

| Premiumization in Heavy-Duty Kraftliner Applications | +0.3% | National, with industrial clusters in Silesia and Central Poland | Medium term (2-4 years) |

| Polish Price Transparency for Recycled Grades | +0.2% | National, with relevance to Central and Eastern Europe import-price benchmarking | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Linked Box Specification Upgrading

The Poland containerboard market is seeing a different packaging mix from western Europe because parcel lockers change how boxes are sized, stacked, and handled in last-mile delivery. Locker-ready formats need tighter dimensions and stronger edge-crush performance, which pushes converters toward more consistent testliner and fluting grades. InPost’s Q3 2025 parcel volumes rose 34% year over year to 351.5 million shipments, and that pace continues to force converters to review board specifications as order profiles change. Direct-to-consumer packaging also favors print-friendly surfaces, and that raises demand for grades that balance appearance, consistency, and transport protection. The result is that the Poland containerboard market is not only growing through parcel volume, it is also shifting toward sub-grades that carry better pricing and tighter technical requirements. This dynamic helps explain why faster-growing sub-grades can outperform the headline pace of the Poland containerboard market even when overall demand looks steady.

Growth in Recycled-Fiber Packaging Substitution

The Poland containerboard market continues to benefit from the retreat from plastic packaging, especially in applications where corrugated formats can replace trays, shrink film, or other single-use formats at scale.[1]Cepi, “Key Statistics 2024, European Pulp and Paper Industry,” CEPI, cepi.org Polish consumers showed a 74% preference for eco-friendly packaging by late 2024, which supports the commercial case for recycled-fiber contracts across consumer-facing categories. The strongest substitution is showing up in FMCG shelf-ready packaging and ambient food applications, where recycled board can meet both retail display and transport needs with lower material complexity. EPR rules and recyclability labeling are also making recycled-content thresholds harder to ignore in procurement, which supports ongoing demand for recycled testliner and fluting rather than virgin alternatives in mainstream uses. European containerboard consumption increased 5.8% to 29,922 thousand tonnes in 2024, and the sector accounted for 66.4% of all paper collected for recycling across Europe, underscoring how closely recycled-fiber demand is tied to the wider paper loop. In the Poland containerboard market, the market supports mills with strong recovered-paper access and gives recycled grades a durable volume advantage, even as some applications move up the quality ladder.

Food and Beverage Export Packaging Demand

Food exports remain one of the clearest demand anchors for the Poland containerboard market because packaging needs rise with both shipment volume and transit complexity.[2]Redakcja Trade.gov.pl, “Polski Sektor Rolno-Spożywczy Na Rynkach Międzynarodowych W 2025 Roku,” Trade.gov.pl, trade.gov.pl Poland’s agri-food exports reached EUR 58.4 billion, which was USD 63.1 billion at the 2025 average exchange rate, in 2025, and were 8.6% above 2024. Poultry, beef, chocolate, and dairy all expanded strongly, and these categories need moisture resistance, food-contact compliance, and dependable transit protection. As exporters widen their reach beyond nearby EU destinations, packaging must perform over longer routes and more variable handling conditions, which raises demand for heavier testliner and stronger fluting. That is why food and beverage accounted for 37.40% of demand in 2025, and why the Poland containerboard market continues to find support from export-oriented processors rather than solely from domestic consumption. This export linkage also favors mills and converters that can offer steady quality, certification readiness, and dependable delivery windows into the main food corridors of the Poland containerboard market.

Nearshoring of Appliance and Auto Supply Chains

Nearshoring is gradually changing the demand profile of the Polish containerboard market, because industrial packaging volumes rise when production shifts closer to Western European customers. Poland ranked 3rd in Europe on the Savills Nearshoring Index 2024, and manufacturing foreign direct investment was 45% above pre-pandemic levels, suggesting a deeper industrial base that needs stronger protective packaging. BSH Home Appliances Group’s 73,000 m² factory near Rzeszów, backed by a PLN 600 million (USD 149 million) loan, was expected to start production by mid-2026 and illustrates the scale of new industrial packing demand. Electronics and automotive activity also favor engineered corrugated packaging, where kraftliner offers better stacking strength and damage resistance than lower-spec recycled grades. The Poland-Germany manufacturing corridor remains important because industrial output, component flows, and packaging demand move together across it. In the Polish containerboard market, this creates a firmer demand floor for heavy-duty corrugated formats even when retail spending softens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recovered Paper and Energy Cost Volatility | -0.8% | National, with energy sensitivity highest in Central and Masovian mill clusters | Short term (≤ 2 years) |

| Western European Oversupply and Import Pressure | -0.5% | National, particularly bordering regions adjacent to German and Austrian mills | Medium term (2-4 years) |

| Margin Compression From Benchmark-Led Price Corrections | -0.3% | National, with spillover to export-oriented Polish converters serving EU buyers | Medium term (2-4 years) |

| Performance Limits of Recycled Grades in Wet and Heavy-Duty Chains | -0.2% | National, with application-specific impact in food exports and industrial packaging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Recovered Paper and Energy Cost Volatility

Input cost swings remain the sharpest near-term restraint on the Poland containerboard market because they coincide with margin pressures and contract timing. In early 2026, Dutch TTF natural gas moved above EUR 68/MWh (USD 73.4/MWh), and testliner producers faced cost increases of up to EUR 20/tonne (USD 21.6/tonne). Testliner production is especially exposed because its gas dependence is far above the broader European paper average, so the cost shock is not evenly distributed across grades. On the fiber side, Poland’s recovered paper market weakened in Q2 2025 as western European oversupply moved inward, distorting collection economics and procurement planning. Smaller independent mills are more exposed because they usually have fewer hedging tools and less vertical integration than larger groups, which increases consolidation pressure when costs move sharply. That is one reason the Poland containerboard market can show healthy demand and still experience restrained production decisions and weaker profitability at the mill level.

Western European Oversupply and Import Pressure

The Poland containerboard market also faces a structural price restraint because western European overcapacity can flow east even when domestic Polish demand remains solid. Billerud’s Q3 2025 results pointed directly to structural overcapacity in European board markets, and its containerboard revenue declined 16% year over year under that pressure. Poland saw capacity underutilization and falling prices throughout much of 2024 and H1 2025, as export opportunities remained limited and seasonal demand remained weak. Profit pressure spread beyond mills into the packaging chain, and net profitability in Poland’s broader packaging sector fell 37% year over year in H1 2025, even as revenue increased 4%. This shows that the Poland containerboard market is not constrained solely by weak end demand, but also by the cost floor and pricing behavior created by a larger regional surplus. The same pattern keeps import-exposed grades under pressure and makes disciplined procurement and selective capacity use more important across the Poland containerboard market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Lead While Virgin Grades Gain Ground

Recycled fibers held 59.74% of Poland's containerboard market share in 2025, maintaining their leading position, as Poland has a well-established recovered-paper ecosystem and cost-competitive supply chains for mainstream corrugated production. That leadership reflects the core structure of the Poland containerboard market, where recycled testliner and recycled fluting remain the practical choice for large-volume shipping cartons, shelf-ready packaging, and standard transport applications. Their position also aligns with current procurement behavior, as converters still need reliable supply, broad grade availability, and price points that work across food, retail, and parcel applications. Recycled grades, therefore, continue to set the tone for day-to-day mill utilization and pricing behavior across much of the Polish containerboard market. At the same time, recycled dominance does not eliminate the need for product upgrades when transit stress, export exposure, or premium box performance matter more.

Virgin fibers are forecast to grow at 3.16% CAGR, marking the fastest Poland containerboard market size expansion among material groups through 2031. That growth points to a premiumization shift within the Polish containerboard industry, as heavy-duty uses in appliances, automotive parts, and agricultural exports often require burst and edge-crush performance that recycled grades cannot deliver as consistently at lower grammages. Mondi completed a EUR 95 million (USD 103.1 million) investment at its Świecie mill in October 2024, adding 55,000 tonnes per year of kraftliner capacity while widening its grammage range.[3]Mondi, “Mondi Completes €95 Million Investment To Boost Efficiency And Sustainability At Świecie Containerboard Mill,” Mondi, mondigroup.com Certification standards such as FSC and PEFC are not mandatory in every tender, but they increasingly shape supplier choice in food-export and consumer-goods packaging because traceable sourcing has become a practical requirement in many contracts. European paper producers used 30,674 thousand tonnes of recycled paper in 2024, equal to 94.7% of production volume, demonstrating how closely the recycled route is linked to feedstock cycles across the region.[4]Cepi, “Key Statistics 2024, European Pulp and Paper Industry,” CEPI, cepi.org Within the Poland containerboard industry, that tight feedstock link helps explain why virgin capacity can win incremental growth even while recycled fibers remain dominant by volume.

By Product Type: Testliners Hold Scale While Kraftliners Gain Pace

Testliners accounted for 40.91% of Poland's containerboard market share in 2025, making them the largest product type, as they align with the recycled-heavy structure of domestic mill configurations. Their role remains central in the Polish containerboard market because they serve the broadest range of standard corrugated applications, including shipping cartons, retail-ready boxes, and e-commerce packaging. Testliners remain closely tied to recovered-fiber economics, so their pricing and availability often reflect wider movements in paper collection, energy, and mill operating rates. Fastmarkets launched standalone Polish recycled containerboard assessments in March 2025 for Testliner 2, Testliner 3, and Recycled Fluting, confirming that local trading activity had become large enough for formal country-specific coverage. That step matters because better price visibility supports contract benchmarking and gives buyers a clearer view of how the Poland containerboard market is moving in its highest-volume grades.

Kraftliners are projected to grow at a 3.24% CAGR, representing the fastest growth in Poland's containerboard market size across product types through 2031. This faster pace reflects stronger demand from appliance packaging, industrial shipments, and food-export loads, where higher stacking strength and moisture resistance matter more than the lowest input cost. Buyers who move from testliner to kraftliner usually pay more upfront, but they can also gain lighter box designs, fewer damage claims, and better full-cycle transport performance. Fastmarkets proposed new Polish price indices for virgin containerboard and white-top kraftliner in April 2026, with implementation planned for June 2026, which suggests that market depth in these grades is improving. That proposal signals a deeper, more mature trading environment for premium grades than Poland has had in the past. In the Poland containerboard market, the split between large-scale testliner demand and faster kraftliner growth reflects the current balance between cost discipline and higher-performance needs.

By End-User Industry: Food and Beverage Leads While Consumer Goods Accelerates

Food and beverage accounted for 37.45% of Poland's containerboard market share in 2025, making it the largest end-user industry, as Poland’s export-oriented food sector needs steady corrugated packaging volumes across many categories. The segment’s role in the Polish containerboard market is supported by demand from meat, dairy, confectionery, and other processed foods, where transport protection, moisture performance, and compliance standards all matter. Poland’s agri-food exports reached EUR 58.4 billion (USD 63.1 billion) in 2025, up 8.6% from 2024, underscoring the need for packaging to support exporters serving both nearby and distant markets. This keeps food packaging demand broad-based rather than dependent on a single subcategory, supporting box volumes even when some consumer segments soften. It also gives mills and converters that can meet food-contact and export specifications a stronger competitive position in the Poland containerboard market.

Consumer goods are forecast to expand at a 3.29% CAGR, the strongest Poland containerboard market growth among end-user groups through 2031. E-commerce remains the main driver, as parcel growth continues to lift demand for corrugated transit formats sized for locker networks and direct-to-consumer delivery. InPost’s Q3 2025 shipment growth of 34% shows how quickly order patterns can shift, and that growth keeps packaging demand closely tied to fast-moving retail categories such as fashion, electronics, and beauty. Other end-user groups also provide incremental support, including pharmaceuticals, for which capital inflows above EUR 1 billion (USD 1.08 billion) were reported for the 2024-2026 period in hubs such as Gdańsk and Poznań. That does not displace the scale of food and beverage, but it does broaden the end-market base of the Poland containerboard market and supports demand for more specialized corrugated formats. The result is an end-user mix where export food keeps scale, while consumer goods raise the growth rate and push more frequent specification changes across the Polish containerboard market.

Geography Analysis

Poland’s paper and board output reached 4.94 million tonnes in 2024, up 6.9% year over year, underscoring the scale of the country’s packaging-related paper manufacturing base. That production scale gives the Polish containerboard market a distinct regional role, as the country serves as a manufacturing base, a conversion center, and a packaging exporter within central Europe. The Poland containerboard market also sits between domestic corrugated demand and imported premium grades, especially kraftliner, which keeps local buyers exposed to both Polish conditions and wider European price movements. Germany, Sweden, and the Czech Republic remain key destinations for Polish corrugated packaging, which confirms that converters are competitive beyond the home market. This trade position helps the Polish containerboard market remain relevant even as Western European board markets soften.

Industrial activity is not evenly distributed across the country, which shapes where containerboard demand is strongest. Silesia remains the main industrial corridor for automotive parts and home appliances, so it continues to generate demand for stronger corrugated formats for finished goods and components. Lower Silesia and the Wrocław area also matter because converters such as SAICA Pack serve industrial and e-commerce accounts from this western corridor. Around Warsaw, Masovia reflects the consumer side of the Poland containerboard market, where logistics, parcel sorting, and retail distribution create the fastest-changing box specification requirements. Pomerania and the Gdańsk-Gdynia-Sopot corridor remain important because they support export flows for processed food and other goods that need reliable transport packaging. The corrugated board market stayed on a positive path in Q1 2026, with deliveries in January and February above prior-year levels and the trend continuing into March.

Compared with several Western European peers, the Polish containerboard market benefits from later-cycle demand growth and a manufacturing base that continues to attract production from higher-cost countries. At the same time, dependence on imported higher-grade kraftliner leaves converters exposed when foreign price benchmarks move in ways that differ from those of local recycled grades. This means the geography of the Polish containerboard market is not only domestic but also tied to cross-border supply, regional industrial relocation, and export packaging flows. As domestic premium-grade investments mature and utilization improves, the country should be better positioned to reduce this dependence in the Polish containerboard market.

Competitive Landscape

The Poland containerboard market is moderately consolidated at the production level because a limited group of large international suppliers controls much of the integrated mill and converting base. Mondi, Stora Enso, Smurfit WestRock, and the enlarged International Paper-DS Smith platform shape the competitive center of the Polish containerboard market through scale, grade mix, logistics reach, and depth of vertical integration. Regional and domestic operators still matter because they compete on responsiveness, converting flexibility, and customer proximity, especially in applications that need shorter lead times or more tailored formats. This creates a market structure where no single supplier sets pricing, but a small group of large players still sets the strategic direction of the Polish containerboard market. Western European overcapacity also affects competition, as import pressure can alter Polish pricing even when local demand remains comparatively firm.

Recent strategic moves show how leading companies are positioning themselves for a more demanding operating environment. In April 2026, Smurfit Westrock launched rail links from its Hoya mill in Germany to Polish production sites, cutting more than 1,400 truck journeys per year and lowering CO2 emissions by 1,500 tonnes annually, which shows that logistics decarbonization is becoming a real selling point in customer negotiations. In May 2026, Saica Group completed its acquisition of Thimm Group, bringing their shared TOP Packaging activity in Poland under a single management structure and strengthening scale across several European markets. International Paper’s January 2025 merger with DS Smith created a larger sustainable packaging platform with more than 230 packaging plants across EMEA and operational teams in Kraków and Gdańsk. Mondi’s completed investment in Świecie and VPK Group’s continued focus on integrated corrugated capabilities show that capacity, quality, and vertical alignment remain central competitive tools. These moves suggest that the Poland containerboard market is rewarding players that can combine paper supply, converting reach, service reliability, and clearer sustainability credentials.

White-space opportunities in the Poland containerboard market still center on food-contact-certified recycled grades and lightweight but high-burst fluting for e-commerce and industrial handling. Those areas remain attractive because customer specifications are moving faster than some legacy mill configurations. Compliance also matters more than before because recyclability labeling, recycled-content traceability, and broader Green Deal alignment increasingly shape supplier qualification. That gives better-positioned companies a durable advantage in the Polish containerboard market, especially when certification, logistics discipline, and technical support are offered together.

Poland Containerboard Industry Leaders

Mondi plc

Stora Enso Oyj

Smurfit Westrock plc

International Paper Company

VPK Group NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Saica Group completed its acquisition of Thimm Group, Thimm's 2024 revenue was EUR 539 million (USD 584.7 million) at the 2024 average exchange rate, consolidating two European family-owned packaging entities with a history of joint operations in Poland through the TOP Packaging venture. The transaction creates a stronger integrated player combining Saica's recycled containerboard production with Thimm's corrugated converting assets across Germany, Poland, France, the Czech Republic, and Romania.

- April 2026: Smurfit Westrock launched new railway connections from its Hoya mill in Germany to its production sites in Poland, including the expanded Pruszków facility with an annual capacity of 500 million boxes. The initiative eliminates over 1,400 truck journeys annually, reduces CO2 emissions by 1,500 tonnes per year, and delivered double-digit improvement in delivery performance.

- April 2026: Polish containerboard mills implemented further price increases for recycled grades for April deliveries, with additional kraftliner price hikes under active discussion, as mills operated near full capacity facing rising costs for raw materials, energy, and transport.

- February 2026: Stora Enso reported increased packaging paper production capacity at its Ostrołęka, Poland mill, as part of a combined 20,000 tpy expansion across its Varkaus and Ostrołęka sites, per its 2025 annual report. Ostrołęka is Stora Enso's largest Polish plant with approximately 1,540 employees.

Poland Containerboard Market Report Scope

The Poland Containerboard Market encompasses the production, distribution, and consumption of containerboard materials used in manufacturing corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Poland Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Poland containerboard sector?

The Poland containerboard market was valued at USD 0.91 billion in 2025, reached USD 0.94 billion in 2026, and is projected to reach USD 1.09 billion by 2031 at a 2.88% CAGR.

Which material type leads demand in Poland?

Recycled fibers led with 59.70% share in 2025 because Poland's recovered-paper ecosystem and mainstream corrugated demand continue to favor recycled grades.

Which product type is growing the fastest through 2031?

Kraftliners are the fastest-growing product type with a 3.24% CAGR, supported by industrial packaging, food-export needs, and heavier-duty box specifications.

Why does food and beverage remain the largest end-user group?

Food and beverage held 37.40% share in 2025 because Poland's strong agri-food export base keeps demand high for moisture-resistant and food-compliant corrugated packaging.

What is driving faster growth in consumer goods packaging demand?

Consumer goods is projected to grow at 3.29% CAGR, mainly because parcel shipping and locker-based e-commerce are increasing the need for corrugated transit packaging.

What are the main risks affecting profitability for producers?

Energy and recovered-paper cost volatility, along with western European oversupply, are the main pressures because they can weaken margins even when domestic demand stays resilient.

Page last updated on: