Ruminant Feed Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

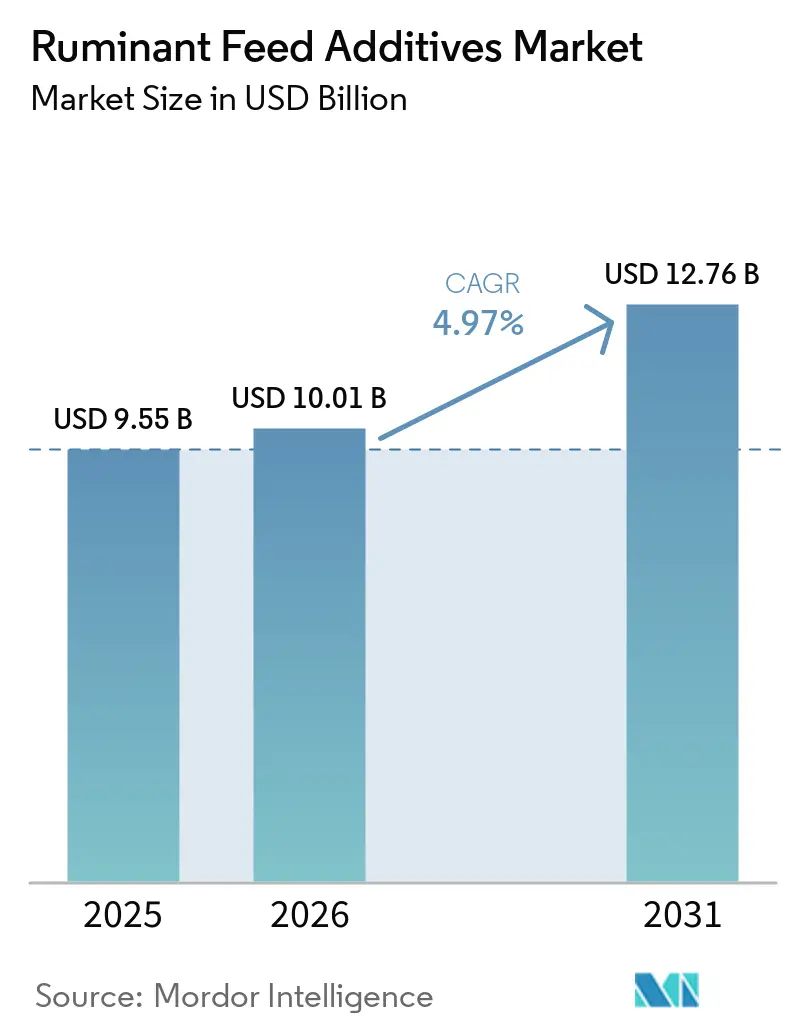

| Market Size (2026) | USD 10.01 Billion |

| Market Size (2031) | USD 12.76 Billion |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ruminant Feed Additives Market Analysis by Mordor Intelligence

The ruminant feed additives market size was valued at USD 9.55 billion in 2025 and is projected to grow from USD 10.01 billion in 2026 to reach USD 12.76 billion by 2031, at a CAGR of 4.97% during the forecast period (2026–2031). The ruminant feed additives market is driven by steady demand as dairy and beef producers push for higher output per animal while maintaining feed efficiency. The ruminant feed additives market is also benefiting from the shift away from antibiotic growth promoters, which is lifting the role of acidifiers, probiotics, phytogenics, enzymes, and other functional products in daily rations. Another change in the ruminant feed additives market is the rising commercial value of methane-reducing solutions, which is shifting supplier attention toward specialty actives with stronger pricing power. Large suppliers are adjusting their portfolios and capacity plans to capture this shift in the mix, which is changing how value is distributed across premixes, protected amino acids, probiotics, and sustainability-linked additives. The ruminant feed additives market is therefore growing on both volume demand and product mix improvements, with mature regions still setting the commercial pace because they combine herd scale, regulatory readiness, and greater adoption of precision feeding tools.

Key Report Takeaways

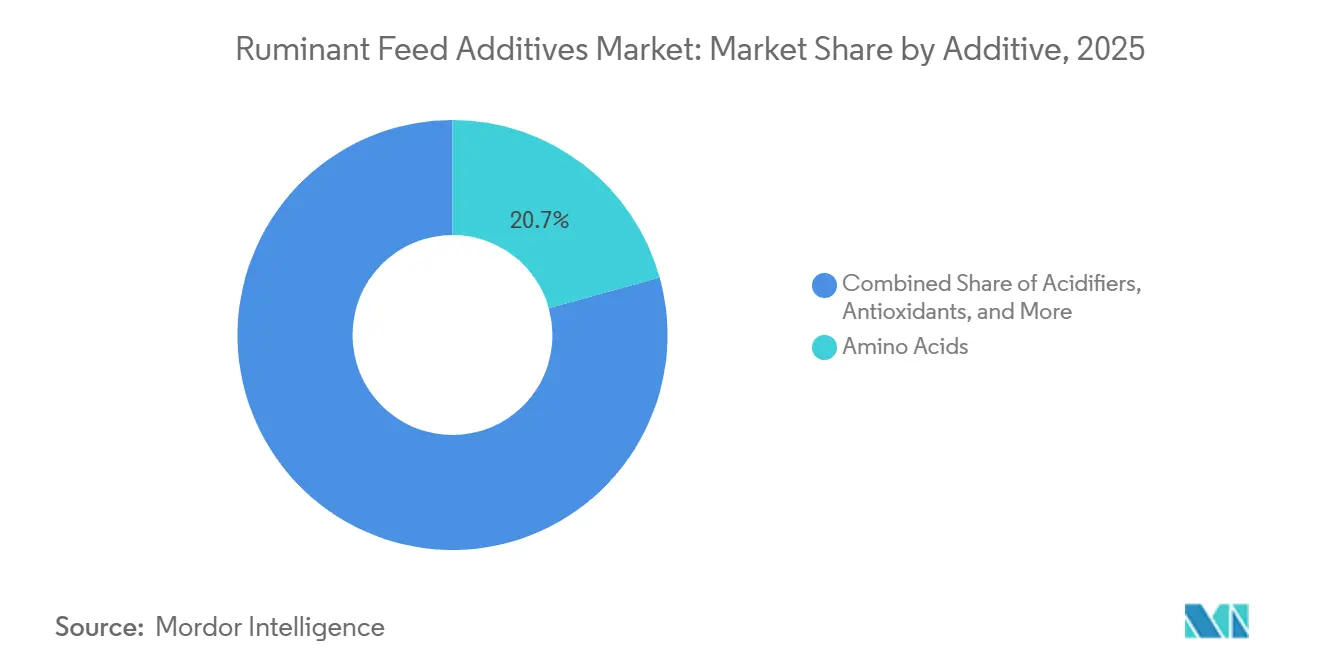

- By additive, amino acids held 20.7% of the ruminant feed additives market share in 2025, while acidifiers are projected to grow at a 5.8% CAGR through 2031.

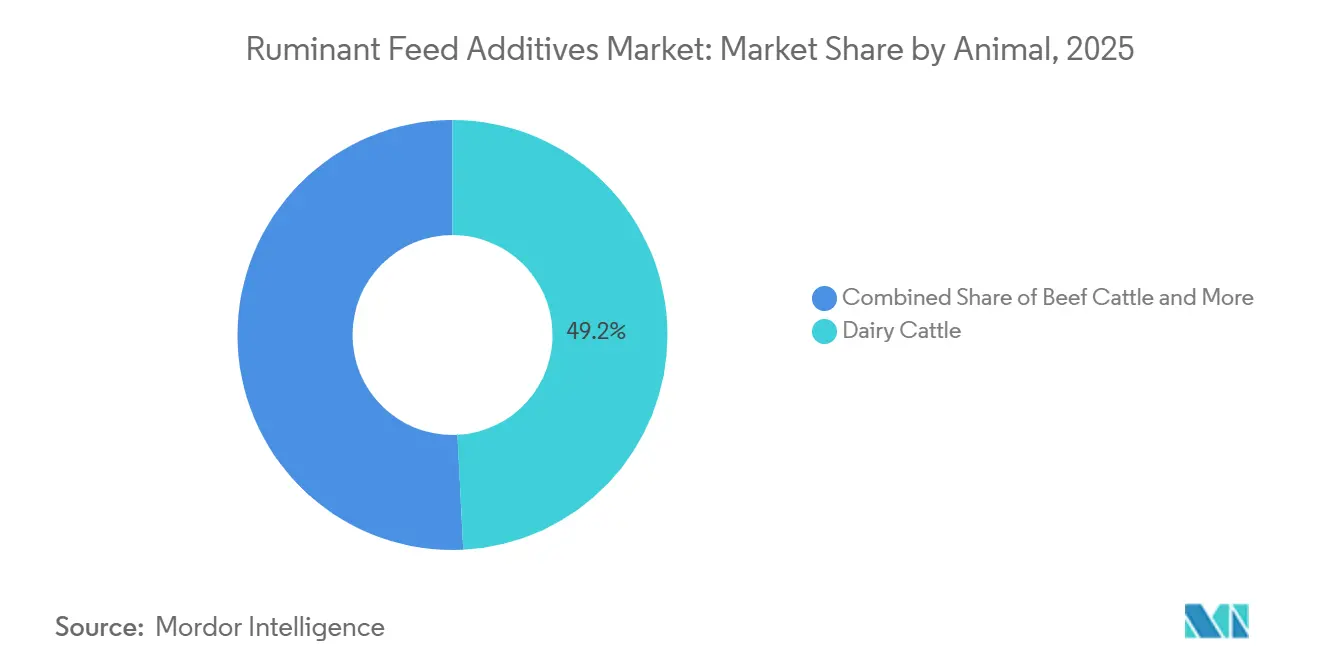

- By animal, dairy cattle accounted for 49.2% of market value in 2025, while beef cattle are forecast to expand at a 5.6% CAGR through 2031.

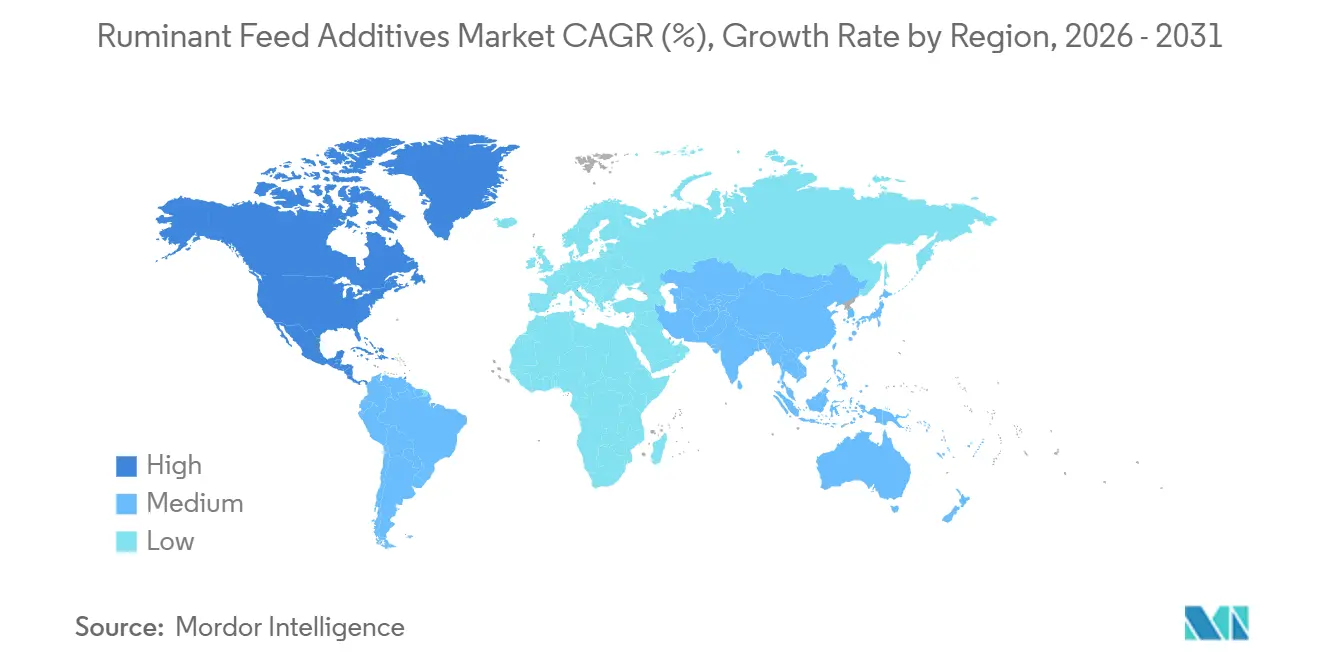

- By geography, North America accounted for 38.0% of the ruminant feed additives market in 2025 and is also projected to record the fastest regional CAGR of 6.1% through 2031.

- By company, Cargill, Incorporated, Archer Daniels Midland Company, DSM-Firmenich, Evonik Industries AG, and BASF SE together accounted for a significant market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ruminant Feed Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for milk and meat productivity gains | +1.5% | Global, with core concentration in Asia-Pacific, North America, and South America | Medium term (2-4 years) |

| Antibiotic-free production shifting demand toward functional additives | +1.2% | Global, with stronger relevance in North America and Europe | Short term (≤ 2 years) |

| Methane-reduction economics improving return on specialty additives | +0.8% | North America, Europe, and Australia, with spillover to Brazil and Japan | Medium term (2-4 years) |

| Expansion of precision feeding in dairy and feedlot operations | +0.7% | North America and Europe, expanding into large Asia-Pacific dairy systems | Medium term (2-4 years) |

| Growth of young animal nutrition programs in commercial herds | +0.5% | Asia-Pacific, South America, and Africa | Long term (≥ 4 years) |

| Rising use of rumen health and microbiome modulation solutions | +0.6% | Global, with concentration in North America, Europe, and large-scale Asia-Pacific dairy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Milk and Meat Productivity Gains

The ruminant feed additives market continues to draw its most stable support from the need to improve milk yield, milk solids, growth rates, and feed conversion in commercial herds. Alltech reported that global compound feed production exceeded 1.44 billion metric tons in 2025, and ruminant feed remains one of the areas where specialty additives offer a higher value per ton than standard formulations [1]Source: Alltech, “2026 Global Feed Survey,” Alltech, alltech.com.. In dairy systems, higher-yielding genetics narrow the nutritional gap between what forage can supply and what the animal needs, keeping demand firm for protected amino acids, minerals, vitamins, and rumen support products. Productivity targets are also becoming more closely linked to sustainability targets because higher output per animal lowers the emissions intensity of each kilogram of milk or meat produced. That combination reinforces the role of premium nutrition programs and keeps the ruminant feed additives market tied to structural efficiency goals rather than short-term feed cycles alone.

Antibiotic-Free Production Shifting Demand Toward Functional Additives

The ruminant feed additives market is benefiting from the growing shift toward antibiotic-free production systems in both dairy and beef operations. With the removal or strict limitation of antibiotic growth promoters, producers are seeking alternative solutions to support digestion, gut health, immunity, and consistent performance. A 2025 meta-analysis published in the Journal of Advanced Research reported that non-antibiotic feed additive combinations resulted in statistically significant improvements in livestock growth performance and immune function across various species[2]Source: L. Liu et al., “Meta-Analyses of the Global Impact of Non-Antibiotic Feed Additives on Livestock Performance and Health,” Journal of Advanced Research, doi.org.. This trend is driving increased use of probiotics, prebiotics, phytogenics, enzymes, acidifiers, and multi-component formulations in commercial ruminant diets. The shift is notable as producers are moving away from replacing single ingredients with another single ingredient, instead adopting integrated programs that combine multiple functional modes of action. This approach is increasing the average expenditure per animal in many organized herds and is steering the ruminant feed additives market beyond basic mineral and vitamin supplementation.

Methane-Reduction Economics Improving Return on Specialty Additives

The ruminant feed additives market is seeing stronger interest in methane-reduction solutions as the business case for large dairy and feedlot operators becomes clearer. A study in 2025 found that 3-NOP supplementation reduced methane yield by an average of 25.9% in beef cattle and 26.4% in dairy cattle at a 60 mg/kg DMI dose. Additional research further supports the role of feed additives in reducing enteric methane emissions in dairy systems, thereby strengthening their commercial applicability [3]Source: Correa Lage et al., “Rumen-Protected Methionine for Dairy and Beef Cattle: Current Perspectives on Methionine Role, Supplementation Strategies, Metabolism, Health, and Performance,” Frontiers in Animal Science, frontiersin.org.. At the company level, DSM-Firmenich kept Bovaer within its core business while divesting the wider Animal Nutrition and Health division, indicating that methane-linked actives are being treated as strategic assets rather than standard portfolio items. That decision matters because it signals confidence that sustainability-linked additives will command better margins and more durable demand. As carbon frameworks, processor commitments, and on-farm efficiency targets increasingly overlap, the return profile for methane inhibitors is becoming strong enough to support broader adoption across the ruminant feed additives market.

Growth of Young Animal Nutrition Programs in Commercial Herds

The ruminant feed additives market is growing due to increased focus on calves and other young ruminants in commercial herds. Producers are emphasizing early rumen development, minimizing health setbacks, and achieving faster progress toward breeding or finishing milestones, as these factors significantly impact lifetime productivity and replacement costs. This trend is driving demand for specialized feeding programs that incorporate acids, yeast, protected nutrients, trace minerals, and gut support products, moving beyond reliance on standard starter feeds. In organized dairy and beef systems, early-life nutrition is increasingly recognized as a cost-management strategy, as improved survivability and early performance gains enhance herd management economics. This impact is particularly pronounced in regions where commercial herd management is becoming more structured, and feed decisions are transitioning from dealer-led purchases to program-based nutrition planning. Consequently, young-animal feeding is emerging as a key growth area for the ruminant feed additives market, especially in regions undergoing herd modernization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of specialty additives versus conventional premixes | -0.5% | Global, with higher pressure in Africa, Asia-Pacific smallholder systems, and South America | Short term (≤ 2 years) |

| Feed ingredient price volatility compressing formulator margins | -0.4% | Global, with stronger pressure in Asia-Pacific and South America | Short term (≤ 2 years) |

| Slower commercial adoption outside large-scale herds | -0.3% | Africa, the Middle East, and smallholder Asia-Pacific systems | Medium term (2-4 years) |

| Lengthy approval and labeling requirements for novel actives | -0.3% | Global, especially in Europe and other highly regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialty Additives Versus Conventional Premixes

The ruminant feed additives market still faces a clear price barrier when specialty products are compared with conventional mineral and vitamin premixes. Evonik Industries AG announced a 10% global net price increase for MetAMINO in March 2026, indicating that protected amino acids and synthetic nutrition remain exposed to production pressures[4]Source: Evonik Industries AG, “Evonik to Increase Its Global Price for MetAMINO,” Evonik Industries AG, evonik.com.. In smallholder and semi-commercial systems, that price gap matters more because feed budgets are tighter and product returns are harder to measure on an animal-by-animal basis. Producers in those systems often stay with simpler premixes even when performance benefits from specialty formulations are known. The commercial issue is not only affordability, but also proof of value at the farm level, especially where advisory support is limited. This means the ruminant feed additives market can grow faster in cost-sensitive regions only when suppliers pair higher-value products with practical service, clearer response metrics, and more accessible packaging.

Slower Commercial Adoption Outside Large-Scale Herds

The ruminant feed additives market still has a sizable access gap outside large-scale dairy farms and organized feedlots. Many producers in South and Southeast Asia, Sub-Saharan Africa, and parts of the Middle East manage animals in systems where individual measurement, controlled feeding, and formal advisory support remain limited. Precision feeding can improve production efficiency, but it also highlights the importance of data collection and system capabilities, which are harder to build for smaller operators. This matters because high-performance additives show their value most clearly when producers can track milk solids, growth, health events, or feed conversion with discipline. Without that structure, specialty products can be seen as optional rather than necessary, even when long-term benefits are real. As a result, the ruminant feed additives market remains more developed in intensive systems, while adoption in fragmented herd bases will likely follow the pace of farm modernization rather than product innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive: Amino Acids Dominate; Acidifiers Set the Pace for Growth

Amino acids accounted for 20.7% of the ruminant feed additives market share in 2025, making them the largest additive category in the industry. This dominance reflects the consistent use of rumen-protected lysine and methionine in high-producing dairy rations, where protein balance is carefully managed. Key products in this category include Mepron from Evonik Industries AG, Smartamine and MetaSmart from Adisseo France SAS, and AjiPro-L from Ajinomoto Co., Inc. Additionally, vitamins, probiotics, and phytogenics hold significant positions due to their roles in promoting health stability, supporting metabolism, and enabling antibiotic-free feeding practices across diverse herd systems. The evolving category mix indicates that the ruminant feed additives market is increasingly driven by ingredients designed to support specific production or health outcomes, rather than solely by broad inclusion products.

Acidifiers are projected to grow at a compound annual growth rate (CAGR) of 5.8%, the fastest among additive types in the ruminant feed additives market through 2031. This growth is attributed to the adoption of antibiotic-free formulation practices and the increased use of calf starter programs to improve gut health and reduce early digestive stress. Acidifier blends are gaining popularity due to their dual benefits of hygiene control and rumen adaptation, making them valuable across various stages of the production cycle. Additionally, the importance of mycotoxin management and enzyme use is rising as climate variability impacts feed quality and as advanced feeding systems enable better quantification of digestibility improvements. Consequently, the industry is shifting towards multi-functional product portfolios rather than single-purpose ingredients. This trend is driving the development of a broader premium product mix, with growth increasingly focused on categories aligned with health, precision feeding, and sustainability objectives.

By Animal: Dairy Cattle Lead Value; Beef Cattle Accelerate on Efficiency Economics

Dairy cattle accounted for 49.2% of the ruminant feed additives market size in 2025, making dairy the largest end-use segment by value. The segment carries the highest per-head additive intensity because intensive lactation programs depend on precise nutrition support across protein balance, metabolism, mineral status, and rumen function. Nutreco received a Dutch grant in 2025 to develop on-farm solutions to reduce nitrogen emissions in dairy herds without sacrificing milk output, demonstrating how nutrition programs are being shaped by productivity and environmental targets simultaneously [5]Source: Nutreco, “Nutreco Receives Dutch Grant to Develop On-Farm Solutions to Target Nitrogen Emissions,” Nutreco, nutreco.com.. That dual requirement raises the bar for suppliers, as farms increasingly want products that can support both output and compliance in a single program. It also favors companies that can offer advisory tools and performance data alongside physical ingredients. In the ruminant feed additives market, dairy remains the value anchor, as large commercial herds continue to justify higher spend on targeted nutrition.

Beef cattle are forecast to grow at a 5.6% CAGR through 2031, making them the fastest-growing animal segment in the ruminant feed additives market. Growth is being supported by feedlot intensification in North America and South America, where feed efficiency and emissions performance are becoming more commercially important. Other ruminants, including sheep, goats, and buffalo, account for the remaining value base and continue to expand steadily in countries where animal populations are large but formal supplementation remains underdeveloped. This creates a two-speed picture where dairy still leads spending intensity while beef creates faster incremental growth. Taken together, both segments are keeping the ruminant feed additives market broad-based rather than dependent on one animal class alone.

Geography Analysis

North America held 38.0% of the ruminant feed additives market share in 2025 and is also projected to grow with the fastest regional CAGR of 6.1% through 2031. That leadership is unusual for a mature region, but it aligns with the structure of the ruminant feed additives market, as North America combines large dairy farms, large feedlots, high additive penetration, and greater readiness for specialty products. The United States drives most of that demand because herd scale, commercial nutrition services, and environmental pressure have all moved in the same direction. Canada adds further depth to the region, as organized dairy systems and regulatory development support the adoption of specialty additives. Mexico remains an important growth pocket because dairy and beef operations are becoming more commercial and more connected to formal premix supply. These conditions keep North America in a dual role as the largest and fastest-growing regional contributor to the ruminant feed additives market.

Asia-Pacific is the second-largest regional market. China, India, and Australia drive demand due to their large herd bases and steady growth factors, including output expansion, modernization, and increased use of formal feed. In August 2025, DSM-Firmenich inaugurated a new Animal Nutrition and Health plant in Jadcherla, India, to locally produce Mycofix for the region, demonstrating confidence in long-term demand and the benefits of a localized supply chain[6]Source: DSM-Firmenich, “dsm-firmenich Opens New Animal Nutrition and Health Plant in Jadcherla, India,” DSM-Firmenich, dsm-firmenich.com.. The region plays a significant role in the ruminant feed additives market, as rising animal protein consumption and herd modernization are expanding the commercial base beyond advanced dairy systems. While adoption varies across farm sizes, the overall trend is positive, with organized production growing and more producers transitioning from basic supplementation to functional nutrition programs.

Europe is projected to grow steadily, driven by stringent regulations on feed safety, animal health, and environmental performance. These factors make Europe a key market for premium additives, as compliance often requires products with robust technical support and proven efficacy. South America is also projected to experience steady growth, led by Brazil and Argentina, where export-oriented beef and dairy systems are enhancing efficiency and scale. Africa and the Middle East are projected to grow at a moderate pace, though both regions face challenges such as limited infrastructure and higher import dependency. However, selected dairy and feedlot clusters in these regions are gradually developing.

Competitive Landscape

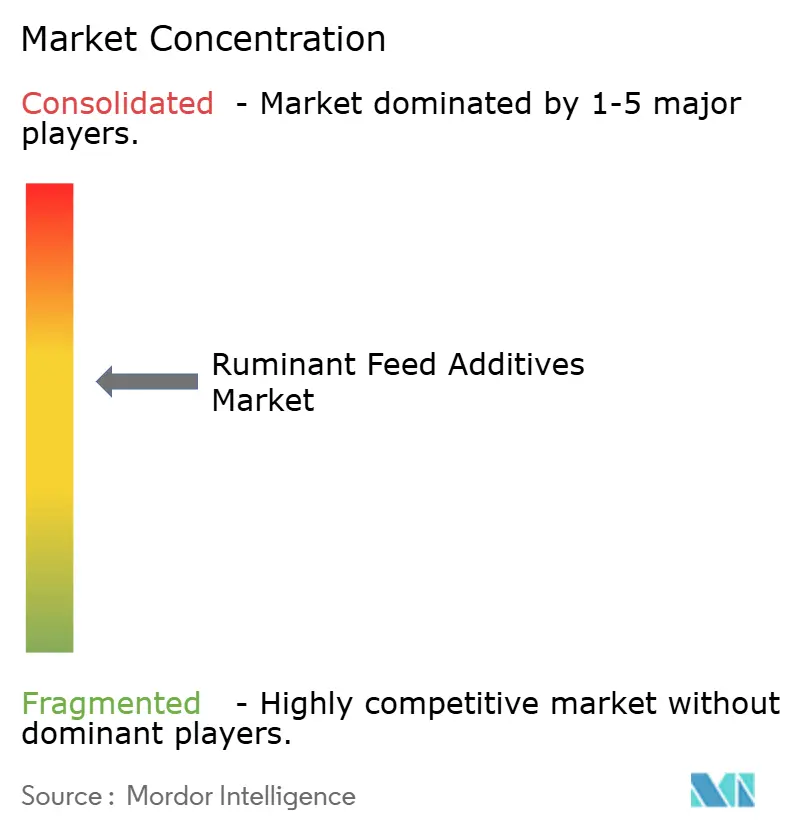

The ruminant feed additives market is moderately consolidated, with the top five players, such as Cargill, Incorporated, Archer Daniels Midland Company, DSM-Firmenich, Evonik Industries AG, and BASF SE, collectively holding a significant market share as of 2025. The market structure indicates that scale remains important; however, competition persists due to the active presence of specialty ingredient suppliers in areas such as probiotics, yeast, methane reduction solutions, and protected nutrition products. Leading companies are adopting strategies that balance portfolio simplification with increased investment in high-value assets. Additionally, there is a growing emphasis on innovation-driven segments and differentiated product offerings to enhance competitive positioning within the market.

BASF SE has focused on reshaping its portfolio to prioritize higher-return areas. In September 2025, the company finalized the sale of its food and health performance ingredients business to Louis Dreyfus Company. Subsequently, in November 2025, BASF announced an agreement for Biochem to acquire its global glycinate business. Additionally, the company evaluated strategic options for its feed enzyme business, highlighting the ongoing reassessment of capital allocation in lower-margin categories[7]Source: BASF SE, “BASF Evaluates Strategic Options for Feed Enzyme Business,” BASF SE, basf.com.. These actions indicate that the ruminant feed additives market is becoming more selective, with leadership increasingly dependent on the quality of the product mix rather than solely on volume.

Technology and technical services are emerging as critical competitive factors in the ruminant feed additives market. Companies are expanding digital and on-farm solutions that directly connect nutrition strategies to productivity, efficiency, and environmental outcomes. Recent advancements in areas such as heat-stress management and emissions reduction are driving a more results-oriented approach to product adoption. While the market remains competitive, suppliers with strong scientific validation, regulatory expertise, and the ability to demonstrate measurable on-farm performance improvements are gaining a competitive edge.

Ruminant Feed Additives Industry Leaders

Cargill, Incorporated

Archer Daniels Midland Company

DSM-Firmenich

Evonik Industries AG

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Evonik Industries AG announced a 10% global net price increase for MetAMINO (DL-methionine 99%, feed grade), citing cost pressures at its global methionine production hubs, which is anticipated to support overall pricing strength in amino acid–based ruminant feed additives and reinforce value growth across the ruminant nutrition market.

- September 2025: Evonik Industries AG launched BoruCare Capsin, a plant-based product for dairy cattle containing capsaicinoids, polyphenols, and flavonoids to address nutrient deficiency in early lactation and heat stress, thereby driving the ruminant feed additives market through increased adoption of functional, plant-based solutions that improve animal health and productivity under stress conditions.

- August 2025: DSM-Firmenich opened a new feed additive plant in Jadcherla, Hyderabad, India, the company’s first such facility in the country, producing Mycofix locally for the Asia-Pacific region, thereby driving the ruminant feed additives market through improved regional supply, reduced import dependence, and faster access to mycotoxin management solutions.

Global Ruminant Feed Additives Market Report Scope

Feed additives are commercially manufactured products used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

The Ruminant Feed Additives Market Report is Segmented by Additive (Acidifiers, Amino Acids, Antibiotics, Antioxidants, Minerals, Binders, Enzymes, Flavors & Sweeteners, Mycotoxin Detoxifiers, Phytogenics, Pigments. Prebiotics, Probiotics, Vitamins, and Yeast), by Animal (Beef Cattle, Dairy Cattle, and Other Ruminants), and by Geography (Africa, Asia-Pacific, Europe, Middle East, North America, and South America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Acidifiers | Fumaric Acid |

| Lactic Acid | |

| Propionic Acid | |

| Other Acidifiers | |

| Amino Acids | Lysine |

| Methionine | |

| Threonine | |

| Tryptophan | |

| Other Amino Acids | |

| Antibiotics | Bacitracin |

| Penicillins | |

| Tetracyclines | |

| Tylosin | |

| Other Antibiotics | |

| Antioxidants | Butylated Hydroxyanisole (BHA) |

| Butylated Hydroxytoluene (BHT) | |

| Citric Acid | |

| Ethoxyquin | |

| Propyl Gallate | |

| Tocopherols | |

| Other Antioxidants | |

| Binders | Natural Binders |

| Synthetic Binders | |

| Enzymes | Carbohydrases |

| Phytases | |

| Other Enzymes | |

| Flavors & Sweeteners | Flavors |

| Sweeteners | |

| Minerals | Macrominerals |

| Microminerals | |

| Mycotoxin Detoxifiers | Binders |

| Biotransformers | |

| Phytogenics | Essential Oil |

| Herbs & Spices | |

| Other Phytogenics | |

| Pigments | Carotenoids |

| Curcumin & Spirulina | |

| Prebiotics | Fructo Oligosaccharides |

| Galacto Oligosaccharides | |

| Inulin | |

| Lactulose | |

| Mannan Oligosaccharides | |

| Xylo Oligosaccharides | |

| Other Prebiotics | |

| Probiotics | Bifidobacteria |

| Enterococcus | |

| Lactobacilli | |

| Pediococcus | |

| Streptococcus | |

| Other Probiotics | |

| Vitamins | Vitamin A |

| Vitamin B | |

| Vitamin C | |

| Vitamin E | |

| Other Vitamins | |

| Yeast | Live Yeast |

| Selenium Yeast | |

| Spent Yeast | |

| Torula Dried Yeast | |

| Whey Yeast | |

| Yeast Derivatives |

| Beef Cattle |

| Dairy Cattle |

| Other Ruminants |

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Turkey | |

| United Kingdom | |

| Rest of Europe | |

| Middle East | Iran |

| Saudi Arabia | |

| Rest of Middle East | |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | Argentina |

| Brazil | |

| Chile | |

| Rest of South America |

| By Additive | Acidifiers | Fumaric Acid |

| Lactic Acid | ||

| Propionic Acid | ||

| Other Acidifiers | ||

| Amino Acids | Lysine | |

| Methionine | ||

| Threonine | ||

| Tryptophan | ||

| Other Amino Acids | ||

| Antibiotics | Bacitracin | |

| Penicillins | ||

| Tetracyclines | ||

| Tylosin | ||

| Other Antibiotics | ||

| Antioxidants | Butylated Hydroxyanisole (BHA) | |

| Butylated Hydroxytoluene (BHT) | ||

| Citric Acid | ||

| Ethoxyquin | ||

| Propyl Gallate | ||

| Tocopherols | ||

| Other Antioxidants | ||

| Binders | Natural Binders | |

| Synthetic Binders | ||

| Enzymes | Carbohydrases | |

| Phytases | ||

| Other Enzymes | ||

| Flavors & Sweeteners | Flavors | |

| Sweeteners | ||

| Minerals | Macrominerals | |

| Microminerals | ||

| Mycotoxin Detoxifiers | Binders | |

| Biotransformers | ||

| Phytogenics | Essential Oil | |

| Herbs & Spices | ||

| Other Phytogenics | ||

| Pigments | Carotenoids | |

| Curcumin & Spirulina | ||

| Prebiotics | Fructo Oligosaccharides | |

| Galacto Oligosaccharides | ||

| Inulin | ||

| Lactulose | ||

| Mannan Oligosaccharides | ||

| Xylo Oligosaccharides | ||

| Other Prebiotics | ||

| Probiotics | Bifidobacteria | |

| Enterococcus | ||

| Lactobacilli | ||

| Pediococcus | ||

| Streptococcus | ||

| Other Probiotics | ||

| Vitamins | Vitamin A | |

| Vitamin B | ||

| Vitamin C | ||

| Vitamin E | ||

| Other Vitamins | ||

| Yeast | Live Yeast | |

| Selenium Yeast | ||

| Spent Yeast | ||

| Torula Dried Yeast | ||

| Whey Yeast | ||

| Yeast Derivatives | ||

| By Animal | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| By Geography | Africa | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | Iran | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What will be the projected value of the ruminant feed additives market by 2031?

The market is anticipated to grow from USD 10.01 billion in 2026 to USD 12.76 billion by 2031, registering a CAGR of 4.97% during the forecast period (2026-2031).

Which additive category leads current demand in ruminant nutrition?

Amino acids lead the mix with 20.7% of 2025 value, supported by demand for rumen-protected lysine and methionine in high-producing dairy systems.

Which additive category is growing the fastest through 2031?

Acidifiers segment is projected to record the fastest growth at a 5.8% CAGR, supported by antibiotic-free feeding programs and young animal nutrition use.

Why does North America lead this space despite being a mature region?

North America held 38.0% of 2025 value and is still projected to grow at 6.1% because it combines large herd systems, high additive use, and stronger readiness for specialty solutions.

Why are dairy cattle still the largest revenue contributor?

Dairy cattle accounted for 49.2% of 2025 value because intensive lactation systems require higher per-head spending on amino acids, minerals, vitamins, and rumen support products.

Page last updated on: