Medicated Feed Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 12.72 Billion |

| Market Size (2030) | USD 16.75 Billion |

| Growth Rate (2025 - 2030) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

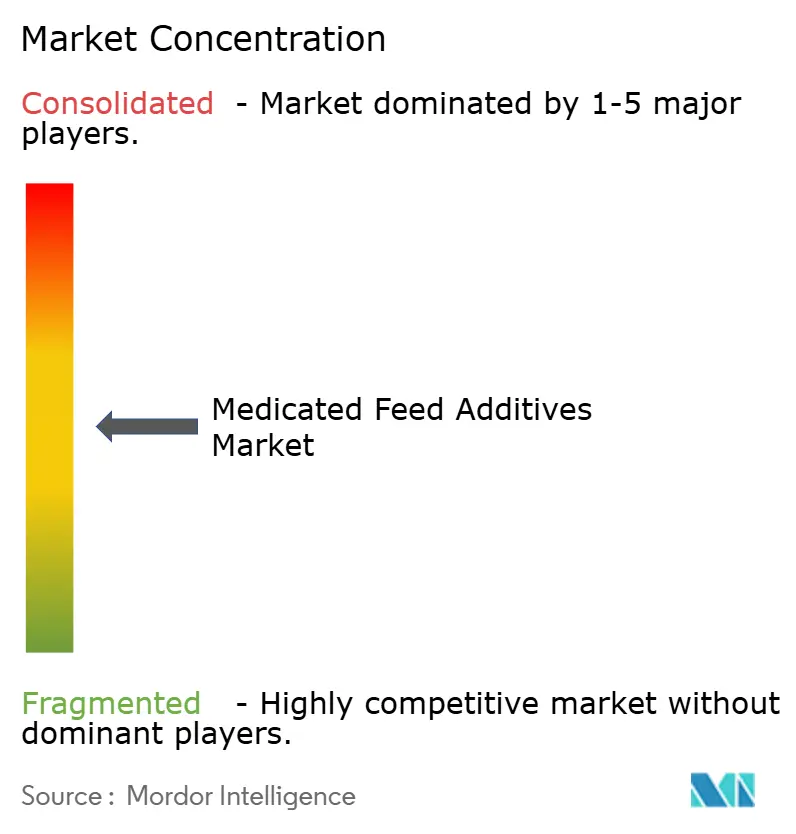

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medicated Feed Additives Market Analysis by Mordor Intelligence

The medicated feed additives market size reached USD 12.72 billion in 2025 and is anticipated to grow to USD 16.75 billion by 2030, at a CAGR of 5.66%. The growth is driven by regulatory compliance requirements, increased biosecurity investments, and growing demand for antibiotic alternatives. The expansion of high-density livestock operations, increased use of digital prescription platforms, and enhanced supply chain programs by major producers contribute to the sustained demand for medicated feed formulations. According to the Food and Agriculture Organization, the global cattle population increased from 1,767 million animals in 2022 to 1,785 million animals in 2023, indicating potential market growth. Industry consolidation through acquisitions has enhanced product portfolios and geographical presence of major suppliers, while regulations on antibiotic growth promoters have increased demand for alternatives such as probiotics, essential oils, and ionophores. The market faces challenges from raw material price fluctuations, particularly for vitamins A and E, following the July 2024 German facility fire, leading companies to implement hedging strategies and diversify suppliers. The growth of e-commerce platforms and direct farm delivery systems has improved market accessibility, particularly for small and medium-scale producers seeking regulatory-compliant and economical solutions.

Key Report Takeaways

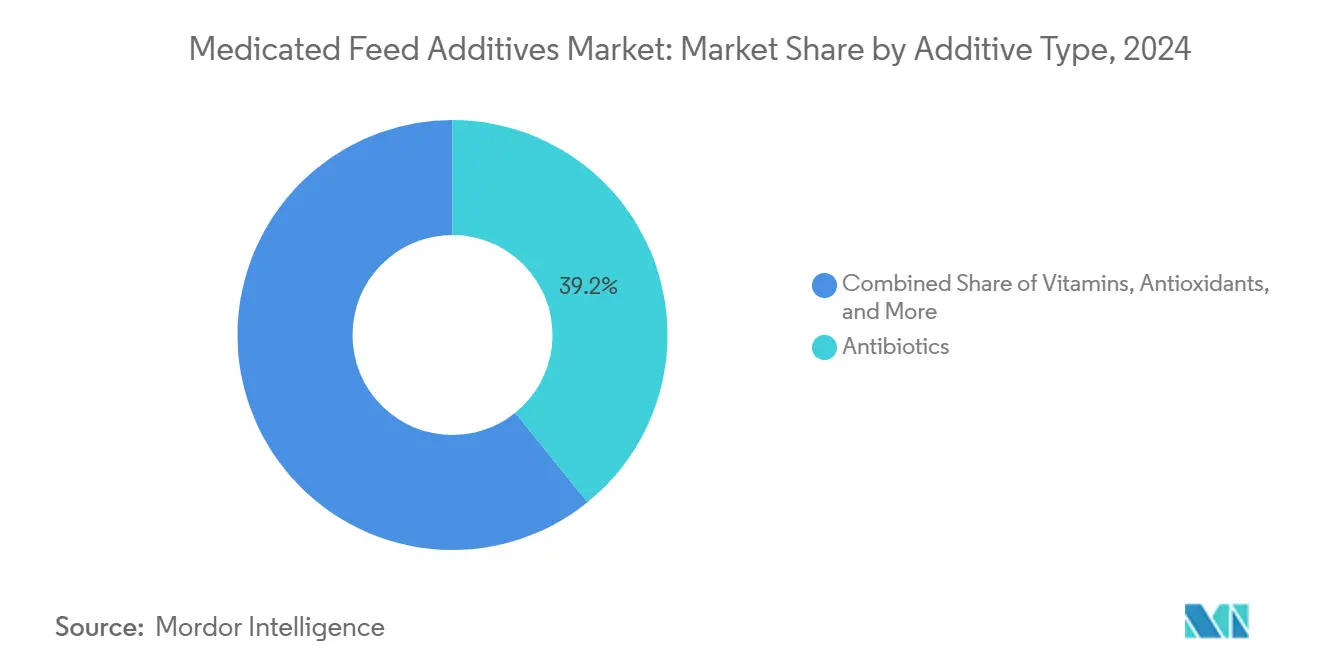

- By type, antibiotics held 39.2% of the medicated feed additives market share in 2024, whereas probiotics are forecast to record the fastest 7.8% CAGR through 2030.

- By mixture type, supplements led with 41.5% of the medicated feed additives market size in 2024, while premixes are projected to post a 6.5% CAGR to 2030.

- By animal type, poultry commanded 34.1% revenue share in 2024, and aquaculture is advancing at a 7.1% CAGR through 2030.

- By geography, North America accounted for 33.9% market share in 2024, while the Asia-Pacific is anticipated to expand at a 6.2% CAGR to 2030.

- The market is moderately fragmented, with the top five players, Cargill, Incorporated, ADM (Archer Daniels Midland Company), Phibro Animal Health Corporation, Elanco Animal Health Incorporated, and Adisseo Group (A Bluestar Company), together accounting for a minority of global sales in 2024.

Global Medicated Feed Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in prophylactic use amid transboundary diseases | +1.1% | Asia-Pacific and Africa | Medium term (2-4 years) |

| Intensifying biosecurity protocols in industrial livestock units | +1.0% | North America and Europe | Long term (≥ 4 years) |

| Integration of prescription digital platforms improving compliance | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Rapid commercialization of novel ionophore alternatives | +0.9% | Global | Medium term (2-4 years) |

| Mandated medicated feed programs during disease outbreaks | +0.8% | Global | Short term (≤ 2 years) |

| Rise of e-commerce distribution channels for medicated feed additives | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Prophylactic Use Amid Transboundary Animal Diseases

The prevalence of severe diseases, including African swine fever and avian influenza, has shifted focus toward preventive measures instead of treatment approaches. During disease outbreaks, national veterinary authorities permit prophylactic medicated feed, maintaining consistent demand for ionophores, coccidiostats, and immune modulators[1]Source: Food and Agriculture Organization, “Standard Veterinary Treatment Guidelines,” FAO, fao.org. Farm operators understand that prevention is more cost-effective than treatment, particularly in high-density livestock facilities where mortality rates can increase rapidly. The implementation of multiphase shuttle programs, which alternate different active ingredients, helps manage resistance development. Manufacturers offering comprehensive anticoccidial product portfolios benefit from increased sales volumes. Regulatory bodies in the United States and European Union have established clear guidelines differentiating between approved prophylactic use and prohibited growth promotion, simplifying preventive product approvals and providing clarity on compliance standards for integrators.

Intensifying Biosecurity Protocols in Industrial Livestock Units

Feed-based interventions, including acidifiers and probiotics, are now integral components of biosecurity plans aimed at reducing pathogen levels in animal digestive systems. Farms certified under Cargill, Incorporated's TRANSFORM program reported a 96% decrease in mortality rates, highlighting the effectiveness of feed additives in biosecurity protocols. Digital monitoring systems enable real-time tracking of pathogen levels, allowing nutritionists to modify medicated feed formulations as needed. This comprehensive approach integrates gut health management through combinations of organic acids, essential oils, and trace minerals. The regulatory framework now distinguishes between feed-based biosecurity measures and therapeutic applications, facilitating faster approvals for preventive feed additives.

Integration of Prescription Digital Platforms Improving Compliance

The United States Veterinary Feed Directive requires documented veterinary oversight for medically important antibiotics. Digital platforms such as myAnimalRx streamline prescription validation, dosage scheduling, and withdrawal tracking, ensuring regulatory compliance while maintaining prescription revenue for veterinary clinics. Large-scale producers managing multiple feed formulations across animal growth stages benefit from improved operational efficiency and data analysis of additive performance. Online direct-to-farm platforms combine transparent pricing with regulatory compliance features, making these services more accessible to small-scale producers.

Rise of E-commerce Distribution Channels for Medicated Feed Additives

E-commerce platforms have made medicated feed additives more accessible to producers who previously relied on scattered dealer networks. Modern logistics systems manage temperature-controlled shipping and hazardous material requirements, reducing delivery times. Digital documentation and remote veterinary support help meet regulatory requirements, enabling smaller producers to confidently purchase medicated feed additives. Specialized online marketplaces combine product information with sales of niche products like organic probiotics, increasing their market reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating global phase-out of antibiotic growth promoters | -1.4% | Europe and North America | Long term (≥ 4 years) |

| Escalating active-ingredient costs due to pharma supply-chain shocks | -0.9% | Global | Short term (≤ 2 years) |

| Emergence of nutraceutical substitutes reducing medicated demand | -0.7% | North America and Europe | Medium term (2-4 years) |

| Complex multi-country licensing requirements for feed mills | -0.5% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Global Phase-Out of Antibiotic Growth Promoters

The European Union banned growth-promotion claims in 2006 and strengthened veterinary antibiotic oversight in 2022. The United States implemented Food and Drug Administration Guidance for Industry 263, which required prescriptions for all medically important antibiotics in 2025[2]Source: Lindsey Garner, “Antibiotic Use and the Veterinary Feed Directive,” Mississippi State University Extension, msstate.edu. Under these regulations, producers must obtain veterinary approval for each antibiotic use through an established veterinarian-client-patient relationship. These restrictions reduced the use of specific antibiotics while driving innovation in alternative feed additives, including probiotics, phytogenics, and enzymes that deliver comparable performance benefits without antimicrobial resistance concerns.

Escalating Active-Ingredient Costs Due to Pharma Supply-Chain Shocks

The July 2024 fire at a German vitamin manufacturing facility led to a Force Majeure declaration for vitamins A and E, causing spot prices to reach five-year highs. Feed manufacturers sought alternative suppliers, which increased raw material costs and reduced profit margins for medicated feed additives manufacturers. Companies have responded by maintaining higher inventory levels, validating additional suppliers, and sourcing critical ingredients from multiple geographical locations to minimize price fluctuations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Additive Type: Antibiotics Dominate but Probiotics Accelerate

Antibiotics account for 39.2% of the medicated feed additives market share in 2024. The segment's significant share stems from the extensive use of tetracyclines, bacitracins, and ionophores for disease control in poultry and swine production. Despite stricter prescription regulations, veterinarians continue prescribing these active ingredients for confirmed bacterial infections, maintaining consistent demand. The prevalence of coccidiosis and necrotic enteritis in broilers, combined with post-weaning diarrhea in piglets, sustains antibiotic usage, particularly in regions with established veterinary oversight systems.

The probiotics segment is projected to grow at a 7.8% CAGR through 2030. Regulatory pressure for residue-free meat production and increasing consumer demand for natural products drive the adoption of live microbial supplements as performance enhancers and immune modulators. Specific probiotic strain combinations show feed conversion ratio improvements and pathogen control capabilities comparable to antibiotics. The Food and Agriculture Organization's recognition of probiotics as supportive therapy facilitates their adoption across animal species. Manufacturers focusing on genomic characterization and microencapsulation technologies achieve premium pricing while ensuring product stability in pelleted feed.

By Mixture Type: Supplements Lead while Premixes Gain Momentum

Supplements accounted for 41.5% of the medicated feed additives market size in 2024. Their single-function formulations enable direct top-dressing or mill incorporation without the need for dedicated dosing equipment, making them suitable for small- to medium-scale operations. Feed nutritionists commonly incorporate vitamins, trace minerals, and individual antibiotics through supplement packages, allowing recipe adjustments based on local ingredient variations.

Premixes are projected to grow at a 6.5% CAGR. These formulations, which combine multiple active ingredients with carrier materials for improved uniformity, are preferred by integrated producers and contract feed mills. Recent developments, such as DSM-Firmenich's additives manufacturing facility in Egypt, which is scheduled to open in 2024, aim to reduce delivery times and meet traceability requirements. The transition from on-farm mixing to commercial premixes is driven by improved quality control, reduced separation of micro-ingredients, and efficient inventory management.

By Animal Type: Poultry Remains Core while Aquaculture Surges

Poultry accounts for 34.1% of the medicated feed additives market share in 2024. The segment's high demand stems from rapid turnover, standardized production cycles, and established anticoccidial programs. Products such as Maxiban and Monteban remain essential for preventing broiler diseases, while layer operations depend on vitamin-fortified supplements to maintain shell quality.

The aquaculture segment exhibits the highest growth rate at 7.1% CAGR. The intensive farming of salmon, shrimp, and tilapia increases susceptibility to waterborne pathogens. Merck KGaA, Darmstadt's acquisition of Elanco Animal Health Incorporated, scheduled for completion in February 2025, enhances research capabilities for bath-stable and water-stable formulations designed for marine and freshwater systems. The adoption of recirculating aquaculture systems supports precise feed dosing, increasing the importance of medicated pellets in health and growth management.

Geography Analysis

North America held 33.9% of the medicated feed additives market share in 2024. The United States Food and Drug Administration's Veterinary Feed Directive ensures access to medically important antibiotics under veterinary supervision, maintaining steady demand while enforcing food safety standards. The region's established veterinary infrastructure, feed mill automation, and prescription digital platforms support market stability. While workforce adjustments at Cargill, Incorporated and other major companies may affect service capacity, substantial poultry, swine, and cattle production continues to drive additive consumption.

Asia-Pacific is projected to grow at a 6.2% CAGR through 2030. China and India are improving regulatory frameworks for feed imports and additive registration through the Ministry of Agriculture and Rural Affairs and the Food Safety and Standards Authority of India, respectively. Growth in aquaculture production, urbanization, and increased protein consumption drives investment in biosecure, high-density systems that require medicated feed for health management. International companies are establishing local premix facilities and technical support teams to address regional compliance requirements and language differences.

Europe maintains market significance despite strict antibiotic regulations. The European Medicines Agency and European Food Safety Authority's approval processes extend development timelines but ensure high safety and environmental compliance[3]Source: European Medicines Agency, “Feed Additive Evaluation Procedures,” EMA, ema.europa.eu. Producers are adopting probiotics, enzymes, and phytogenics to maintain performance, making the region a testing ground for antibiotic alternatives. South America demonstrates growth potential, driven by livestock export expansion and regulatory changes, including Argentina's Resolution 445/2024 prohibiting growth promoters, which increases demand for approved alternatives. Brazil's self-regulatory framework promotes quality systems that benefit established brands.

Competitive Landscape

The market is moderately fragmented, with the top five players - Cargill, Incorporated, ADM (Archer Daniels Midland Company), Phibro Animal Health Corporation, Elanco Animal Health Incorporated, and Adisseo Group (A Bluestar Company) - accounting for a minority in the medicated feed additives market share in 2024. Companies are expanding their portfolios through strategic acquisitions and divestitures. Phibro acquired Zoetis' medicated feed additive business for USD 350 million in 2024, gaining USD 400 million in revenue and six manufacturing facilities. DSM-Firmenich sold its Feed Enzymes Alliance stake to Novonesis for EUR 1.5 billion (USD 1.6 billion) in June 2025, enabling investment in specialty additives. Elanco gained market advantage through early approval of Bovaer, its methane-reduction product.

Product development focuses on antibiotic alternatives, methane-reduction compounds, and digital services. Companies are implementing data-driven advisory platforms to demonstrate additive performance through farm-level results. Supply chain reliability has become a competitive advantage, as demonstrated during the 2024 vitamin shortage when companies that maintained consistent supply secured long-term customer contracts.

Growth opportunities exist in emerging aquaculture and ruminant segments, particularly where specialized formulations and technical support are limited. Increasing regulations create higher entry barriers, benefiting large-scale operators with established regulatory compliance teams and global manufacturing networks. The market is anticipated to see continued moderate consolidation as medium-sized companies seek economies of scale for regulatory compliance and research investment.

Medicated Feed Additives Industry Leaders

Cargill, Incorporated

ADM (Archer Daniels Midland Company)

Phibro Animal Health Corporation

Elanco Animal Health Incorporated

Adisseo Group (A Bluestar Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Kemin Industries, Inc. introduced PROSIDIUM, a feed pathogen control system that uses peroxy acids to eliminate Salmonella and viruses in animal feed, improving feed and food safety. The company unveiled the system at VIV Asia 2025, focusing on enhanced biosecurity through uniform distribution application solutions.

- October 2024: Phibro Animal Health Corporation acquired a portfolio of medicated feed additives and water-soluble products from Zoetis Inc. for USD 350 million. The acquisition included 37 product lines, including Avatec, BMD, and Zoamix, which are used in cattle, swine, and poultry production. This transaction expanded Phibro's animal health and nutrition capabilities, while enabling Zoetis to redirect investments toward vaccines and biologics.

- August 2024: Boehringer Ingelheim India established a strategic distribution partnership with Vvaan Lifesciences Private Limited for its pet parasiticide portfolio. This collaboration, part of Boehringer Ingelheim India's Animal Health Accelerated Growth Plan (AGP), aims to expand market reach and enhance customer value in the medicated feed additives market.

- July 2024: Merck Animal Health acquired the aquaculture business from Elanco Animal Health Incorporated. This acquisition strengthens Merck Animal Health's position in the aquaculture industry by providing comprehensive solutions for fish health, welfare, and sustainability across aquaculture, conservation, and fisheries operations.

Global Medicated Feed Additives Market Report Scope

Medicated feed additives are fed to animals for nutritional purposes and medicinal purposes, to prevent, treat, or control bacterial infections, coccidiosis, and worms, and to prevent mortality. The Medicated Feed Additives Market is Segmented by Additive Type (Antibiotics, Vitamins, Antioxidants, Amino Acids, Prebiotics, Probiotics, Enzymes, and Other Additive Types), Mixture Type (Supplements, Concentrates, Premixes, and Base Mixes), Animal Type (Ruminants, Poultry, Swine, Aquaculture, and Other Animal Types), and Geography into North America (United States, Canada, Mexico, and Rest of North America), Europe (Germany, United Kingdom, France, Spain, Russia, Italy, and Rest of Europe), Asia-Pacific (China, India, Japan, Australia, and Rest of Asia-Pacific), South America (Brazil, Argentina, and Rest of South America), Middle-East (Saudi Arabia, United Arab Emirates, and Rest of Middle-East), and Africa (South Africa, Egypt, and Rest of Africa). The report offers the market size and forecasts in terms of value (USD million).

| Antibiotics |

| Vitamins |

| Antioxidants |

| Amino Acids |

| Prebiotics |

| Probiotics |

| Enzymes |

| Other Additive Types |

| Supplements |

| Concentrates |

| Premixes |

| Base Mixes |

| Ruminants |

| Swine |

| Poultry |

| Aquaculture |

| Other Animal Types |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Additive Type | Antibiotics | |

| Vitamins | ||

| Antioxidants | ||

| Amino Acids | ||

| Prebiotics | ||

| Probiotics | ||

| Enzymes | ||

| Other Additive Types | ||

| By Mixture Type | Supplements | |

| Concentrates | ||

| Premixes | ||

| Base Mixes | ||

| By Animal Type | Ruminants | |

| Swine | ||

| Poultry | ||

| Aquaculture | ||

| Other Animal Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the medicated feed additives market?

The medicated feed additives market size reached USD 12.72 billion in 2025 and is projected to rise to USD 16.75 billion by 2030.

Which animal segment is growing the fastest?

Aquaculture applications are forecast to grow at a 7.1% CAGR through 2030 as global fish and shrimp production expands.

How are regulations impacting antibiotic use in feed?

Rules such as the U.S. Veterinary Feed Directive and EU antibiotic bans require veterinary prescriptions and are encouraging shifts toward probiotics and other alternatives.

Why are premixes gaining popularity in feed mills?

Premixes deliver multiple active ingredients in a single, quality-controlled package, improving traceability and reducing mixing errors while supporting compliance.

What major merger reshaped the competitive landscape recently?

Phibro Animal Health Corporation's USD 350 million acquisition of Zoetis Inc.'s medicated feed additive portfolio added six plants and USD 400 million in revenue, boosting its global reach.

Page last updated on: