Rugged Router Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.46 Billion |

| Market Size (2031) | USD 8.68 Billion |

| Growth Rate (2026 - 2031) | 9.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

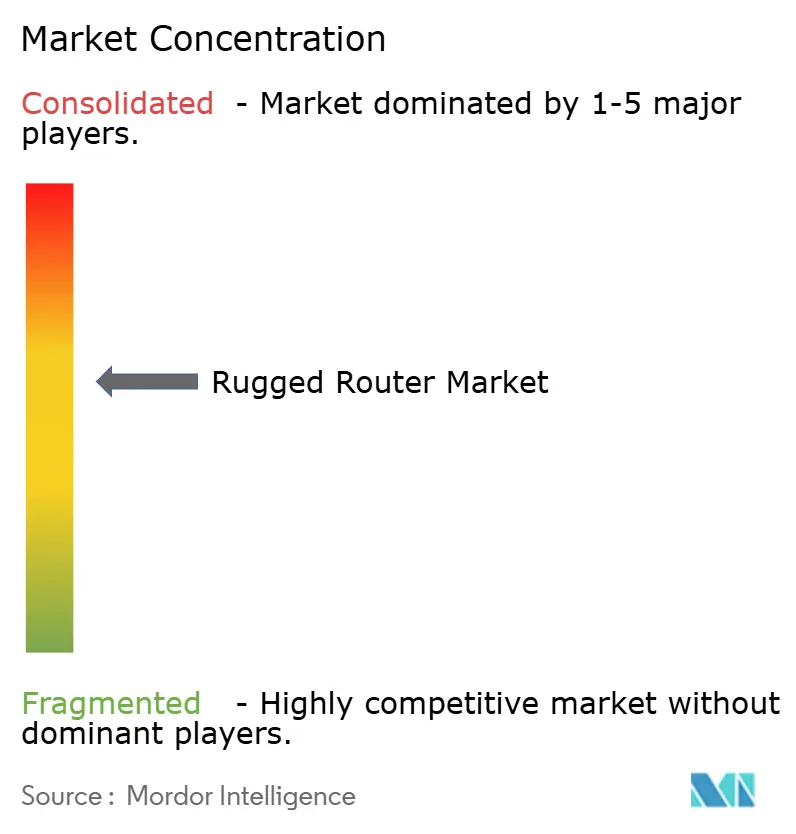

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rugged Router Market Analysis by Mordor Intelligence

The rugged router market size is projected to expand from USD 5.31 billion in 2025 and USD 5.46 billion in 2026 to USD 8.68 billion by 2031, registering a CAGR of 9.71% between 2026 to 2031. Momentum is shifting because field operators now treat hardened connectivity as a prerequisite for edge intelligence, autonomous vehicles, and real-time control loops rather than as an ad-hoc upgrade. Private 5G spectrum awards, railway safety mandates, and zero-trust defense networks are accelerating refresh cycles, while hardware convergence folds switching, routing, and security into a single IP67 enclosure. Software subscription models are displacing one-time capital purchases, and vendors able to orchestrate multi-radio links from the cloud are gaining wallet share.

Key Report Takeaways

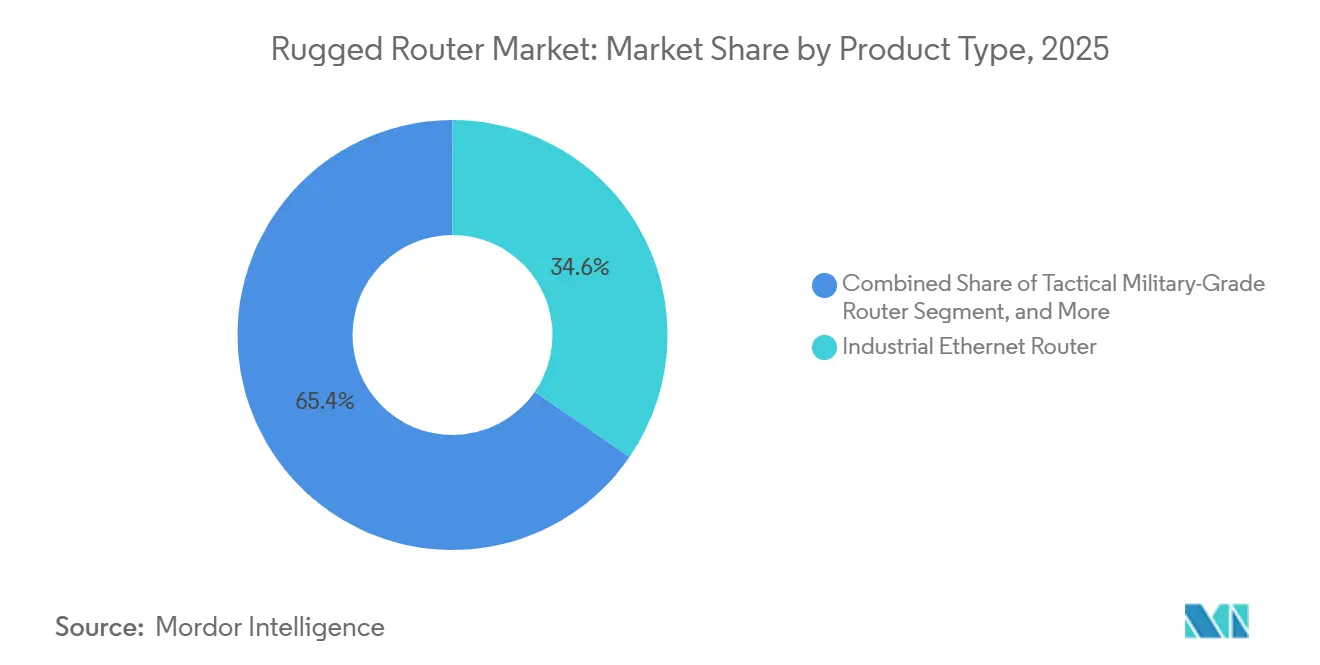

- By product type, Industrial Ethernet accounted for 34.6% of the rugged router market share in 2025, whereas tactical, military-grade platforms are forecast to grow at a 11.12% CAGR through 2031.

- By connectivity technology, 4G and LTE together held 46.23% of the rugged router market in 2025, yet 5G installations are advancing at a 9.87% CAGR through 2031.

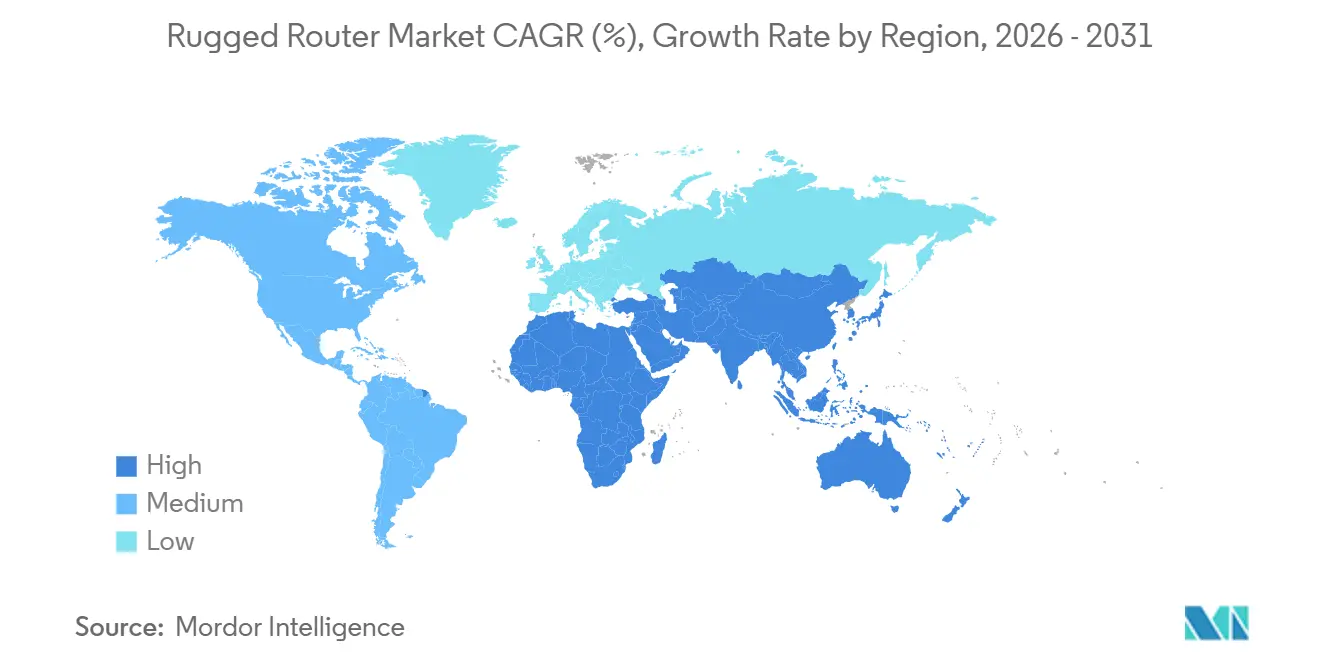

- By geography, North America accounted for 31.34% of revenue in 2025, while Asia-Pacific is projected to expand at a 11.34% CAGR through 2031.

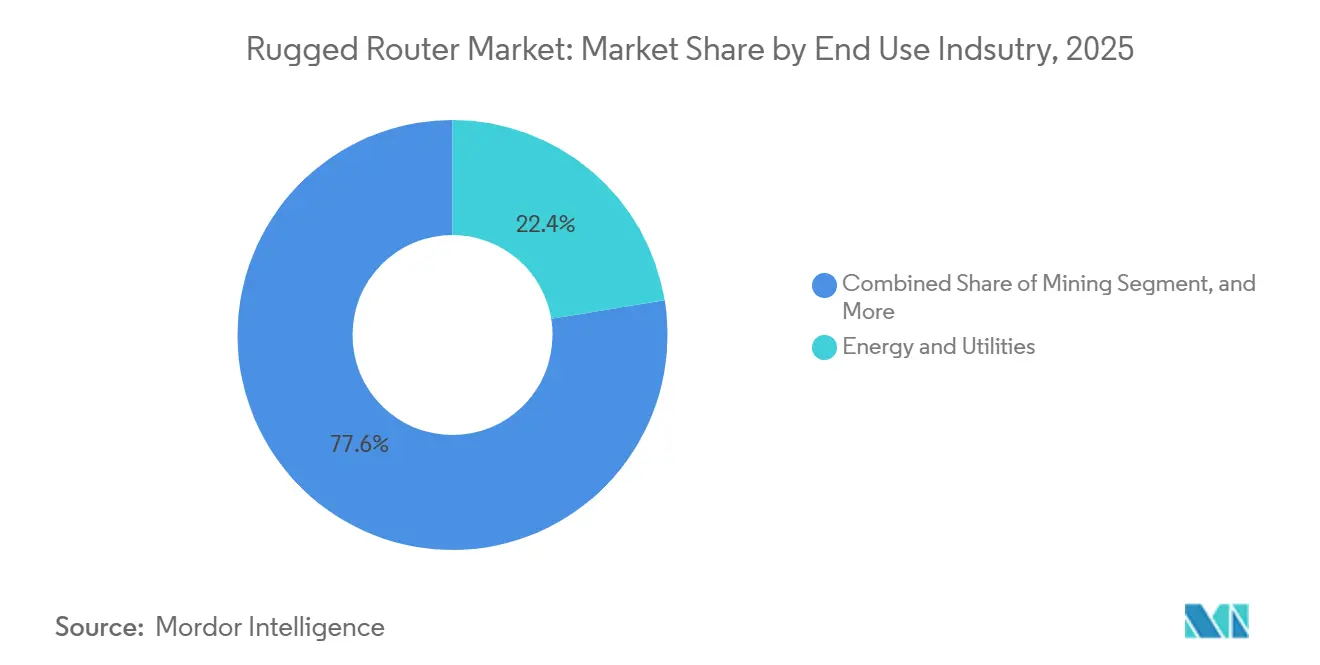

- By end-use industry, Energy and utilities accounted for 22.42% of the rugged router market in 2025, whereas mining is set to grow the fastest, with a 10.12% CAGR to 2031.

- By deployment mode, Fixed or stationary deployments accounted for 42.16% of shipments in 2025, but portable and handheld form factors are growing at a 12.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rugged Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Edge Computing in Harsh Environments | +2.1% | Global, early adoption in North America mining and Asia-Pacific manufacturing | Medium term (2-4 years) |

| Integration of 5G NR in Industrial Connectivity | +1.9% | Global, led by Europe rail digitization and Middle East energy | Medium term (2-4 years) |

| Rising Demand for Remote Asset Monitoring in Energy Sector | +1.5% | Middle East, North America shale basins, offshore Asia-Pacific | Short term (≤ 2 years) |

| Military Modernization Programs Focusing on Tactical Networking | +1.3% | North America, Europe, Asia-Pacific defense corridors | Long term (≥ 4 years) |

| Growing Adoption of Ruggedized IoT Gateways in Smart Mining | +1.1% | Asia-Pacific, South America | Medium term (2-4 years) |

| Regulatory Push for Railway Positive Train Control Systems | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Edge Computing In Harsh Environments

Inference workloads that were historically processed in centralized or regional data centers are increasingly shifting to edge-based, fanless gateways mounted directly on autonomous rigs, drilling systems, and remote wellheads. Advanced drilling platforms now execute sub-50 ms machine vision and control loops locally, eliminating backhaul latency and enabling real-time decision-making in mission-critical environments. Similarly, rugged edge devices equipped with embedded AI compute and private LTE connectivity process seismic and operational data at the asset level rather than transmitting it to distant cloud environments. This transition is driving silicon convergence, in which compute, storage, and routing functions are integrated into compact, IP67-rated enclosures engineered to withstand temperatures from -40 °C to +75 °C, thereby reinforcing demand for high-performance rugged routers.[1]Epiroc, “Deep Automation 3D,” epiroc.com

Integration of 5G NR In Industrial Connectivity

Standalone 5G introduces capabilities such as network slicing and time-sensitive networking that materially exceed 4G performance in industrial environments. Large-scale private 5G grids are now connecting thousands of distributed assets across expansive operational areas, enabling deterministic, low-latency communication for critical infrastructure. Concurrently, industrial-grade routers are integrating multi-radio architectures that combine 5G, Wi-Fi 7, and SD-WAN to segment operational technology traffic, such as SCADA, from enterprise IT networks, thereby improving both security and reliability. Additionally, the emergence of 5G RedCap modules reduces power consumption for edge devices and smart-grid sensors, making deployments more cost-efficient. As a result, greenfield infrastructure projects from 2026 onward are increasingly specifying 5G-native architectures, positioning multi-radio orchestration and seamless network management as key procurement criteria.[2]FreeWave Technologies, “ES1000 Edge Gateway,” freewave.com

Rising Demand for Remote Asset Monitoring In Energy Sector

Private, mission-critical communication networks are expanding across upstream energy and grid infrastructure, driving demand for highly specialized rugged routers. Sub-GHz spectrum deployments now enable wide-area coverage across large oilfield geographies, supporting thousands of field devices operating under extreme climatic conditions. Industrial-grade routers compliant with IEC 61850-3 are increasingly deployed to ensure deterministic communication and reliable grid protection. At the same time, advanced networking hardware integrates precise time-synchronization capabilities, allowing microsecond-level event stamping to support grid stability and autonomous microgrid islanding. In offshore and remote environments, hybrid satellite and LTE-enabled routers ensure continuous telemetry even during terrestrial network outages. As a result, insurers and regulators are mandating uninterrupted data transmission for risk monitoring and compliance, directly increasing capital expenditure cycles and accelerating router refresh budgets across energy operators.[3]Cradlepoint, “R2400 Rugged Router,” cradlepoint.com

Military Modernization Programs Focusing on Tactical Networking

Modern defense networks are shifting toward resilient, multi-layered communication fabrics that integrate tactical radios, satellite links, and 5G into unified overlays capable of dynamically rerouting traffic under contested conditions. This architecture ensures continuity of operations even when individual nodes are degraded or denied. Concurrently, compact, lightweight routers are embedding advanced security features such as Type 1-grade encryption, enabling secure voice and data exchange for dismounted personnel in real time. Additional capabilities, including inertial navigation, allow these systems to function effectively in GNSS-denied environments, which are increasingly common in electronic warfare scenarios. As military doctrine prioritizes mobility, decentralization, and edge-level decision-making, procurement is shifting away from vehicle-mounted systems toward man-portable networking units, positioning portable rugged routers as the fastest-growing segment within the tactical communications market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for Rugged Networking Hardware | -1.2% | Global, acute in South America and Africa mining | Short term (≤ 2 years) |

| Limited Availability of Rugged 5G Components During Early Roll-out | -0.9% | Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Compatibility Issues with Legacy Industrial Protocols | -0.6% | North America and Europe | Medium term (2-4 years) |

| Complex Certification Requirements Across Global Rail Standards | -0.4% | Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure for Rugged Networking Hardware

Rugged networking hardware has a materially higher upfront cost than commercial-grade alternatives, creating a structural adoption barrier in price-sensitive industries. A typical MIL-STD-810H compliant router ranges between USD 2,000-5,000, versus approximately USD 400 for standard commercial units, extending payback periods beyond 5 years in sectors such as mining, where cost discipline is strict. In defense applications, tactical-grade systems can exceed USD 15,000 per unit due to embedded encryption, multi-radio integration, and hardened design requirements. In rail, compliance with EN 50155 standards adds an incremental USD 10,000-20,000 per carriage over lifecycle deployments, further inflating the total cost of ownership. While subscription-based models such as Cradlepoint NetCloud shift expenditure toward OPEX and reduce initial capital burden, resistance persists among operators who prefer asset ownership over recurring fee structures, limiting penetration in conservative procurement environments.

Limited Availability Of Rugged 5G Components During Early Roll-out

Tight supply of advanced 5G modem chipsets has constrained near-term product rollouts, with several industrial networking vendors delaying next-generation SKUs due to allocation bottlenecks. At the hardware level, millimeter-wave radios introduce higher thermal loads, requiring larger heat dissipation systems within sealed IP67 enclosures. This creates a secondary constraint, as increased form factor and thermal design complexity slow hazardous-area certifications such as ATEX Zone 2, pushing approval cycles toward approximately nine months. The combined effect of component shortages and certification delays is elongating deployment timelines across industrial projects. As a result, many system integrators in Asia-Pacific are continuing to specify dual-mode 4G solutions as a transitional architecture, deferring full 5G adoption until supply stability and certification throughput improve, likely closer to 2028.[4]Digi International, “Component Constraints Impact,” digi.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tactical Platforms Outpace Established Ethernet Lines

Industrial Ethernet accounted for 34.6% of the rugged router market share in 2025, reflecting its entrenched role in deterministic, wired industrial networks. However, tactical routers are projected to grow at a 11.12% CAGR, driven by defense modernization and the need for resilient, multi-layered communications in contested environments. Multi-waveform bonding architectures enable seamless failover across radio, satellite, and cellular links, ensuring continuity even under jamming or node failure. Concurrently, industrial platforms are converging capabilities, with solutions such as Cisco Catalyst IR8300 integrating SD-WAN and dual 5G modems to eliminate standalone security and routing appliances, improving operational efficiency.

Pricing differentials remain a defining structural factor. Industrial Ethernet routers typically range from USD 2,000-5,000, while 4G cellular units range from USD 800-1,500, and 5G variants range from USD 1,800-3,500. In contrast, tactical-grade systems command USD 15,000-25,000 due to advanced encryption, ruggedization, and multi-radio integration. These elevated ASPs disproportionately inflate revenue contribution despite a relatively smaller installed base. At the same time, increasing demand for integrated switching, routing, and security functions is reducing cabinet footprint and driving procurement toward unified, multi-function appliances, effectively dissolving traditional device segmentation across industrial and utility deployments.

By Connectivity Technology: 5G Adoption Accelerates Despite 4G Dominance

4G and LTE accounted for 46.23% of rugged router shipments in 2025, reflecting their entrenched installed base and reliability in brownfield industrial environments. However, 5G routers are expanding at a 9.87% CAGR as private spectrum deployments and industrial 5G networks scale across utilities, energy, and transport sectors. Vendors are prioritizing backward compatibility to reduce migration friction, with platforms such as Cradlepoint R2400 enabling LTE fallback to ensure continuity during phased upgrades. This hybrid approach reduces switching risk and supports gradual capital deployment, rather than requiring a full infrastructure replacement.

At the architecture level, resilience is becoming a non-negotiable procurement criterion. Dual-radio configurations capable of sub-50 ms failover between cellular links are now embedded in tender specifications, particularly for mission-critical operations. Additionally, satellite-cellular convergence is addressing coverage gaps in ultra-remote or disaster-prone regions, where terrestrial networks remain unreliable. Solutions such as Meridian5G M1-R illustrate this shift by bonding satellite and 5G connectivity to maintain uninterrupted command and control. This evolution toward multi-path, software-orchestrated networking is redefining performance benchmarks and accelerating adoption of hybrid communication stacks.

By End-Use Industry: Mining Emerges As The Fastest Riser

Energy and utilities accounted for 22.42% of rugged router revenue in 2025, supported by grid modernization, substation automation, and distributed energy integration. However, mining is set to outpace all sectors with a 10.12% CAGR through 2031, driven by the rapid adoption of autonomous haulage, remote operations, and edge-based analytics in harsh environments. Large-scale deployments of autonomous truck fleets and fully connected mine sites demonstrate operational viability at scale, while extreme climate deployments validate hardware resilience under conditions such as -40 °C. These factors reinforce mining as a high-growth, high-dependency vertical for rugged networking infrastructure.

Beyond mining, transportation, manufacturing, and oil and gas, each contributes 12-18% of total market revenue, reflecting diversified demand across industrial automation, rail signaling, and upstream energy operations. Public safety is also emerging as a growth segment, with dedicated broadband networks enabling rugged routers to be embedded in patrol vehicles and mobile command units. This expands use cases toward real-time video, incident response coordination, and secure field communications.

By Deployment Mode: Portable Nodes Gain Momentum

Fixed installations represented 42.16% of rugged router shipments in 2025, reflecting their continued role in substations, rail infrastructure, and industrial sites where permanent connectivity is required. However, portable and handheld units are scaling faster at a 12.13% CAGR, driven by defense mobility requirements and field-based operations. Lightweight, man-packable systems are replacing vehicle-mounted architectures as militaries prioritize distributed, rapidly deployable communication nodes. Battery-powered designs with multi-hour endurance enable off-grid functionality, while integrated multi-radio capabilities ensure connectivity across contested or infrastructure-poor environments.

In parallel, maritime demand is expanding as vessels require resilient, always-on communication for navigation, crew welfare, and operational coordination. Hybrid connectivity solutions that combine satellite bands with cellular networks are increasingly standard to maintain coverage across open seas and nearshore zones. Products such as KVH TracNet H90 illustrate this shift by bonding a Ku-band satellite with LTE to deliver continuous bandwidth. The convergence of portability, energy efficiency, and hybrid networking is therefore redefining deployment models, pushing vendors to optimize for weight, power consumption, and multi-path communication resilience.

Geography Analysis

North America accounted for 31.34% of rugged router revenue in 2025, anchored by federally mandated rail safety systems and defense network modernization programs. Positive Train Control deployments continue to require dual-cellular, GNSS-integrated routers to ensure real-time train separation and operational safety across extensive rail networks. In parallel, military mesh networking initiatives are accelerating demand for secure, resilient communication infrastructure. Harsh-environment deployments in Canadian mining operations further reinforce regional demand, where routers rated for -40 °C enable continuous tele-remote operations and video streaming. The region benefits from strong regulatory enforcement, high technology adoption, and consistent capital allocation across transport, defense, and resource sectors.

Asia-Pacific is projected to grow at 11.34% CAGR through 2031, driven by large-scale infrastructure digitization and industrial automation. Australia leads in autonomous mining, with operators deploying private LTE and 5G networks to support real-time vehicle control and analytics in remote environments. India’s BharatNet initiative is expanding rural broadband coverage, with domestic vendors scaling deployment of over 130,000 routers to connect underserved regions. Simultaneously, China is advancing RedCap-based IoT deployments to enable cost-efficient industrial connectivity. Underground 5G trials in Australian mines highlight the region’s push toward high-bandwidth, low-latency applications, reinforcing Asia-Pacific as the fastest-growing market with diversified demand drivers.

Europe’s growth is tied to railway digitization under ETCS Level 2 and 3, which requires secure, interoperable communication systems across cross-border rail networks. Vendors are integrating multiple functions such as signaling and passenger connectivity into unified platforms, reducing hardware redundancy. In the Middle East, investment is accelerating through large-scale energy sector digitization, including private 5G oilfield networks and sub-GHz wide-area deployments for upstream operations. South America shows steady adoption in mining-intensive economies such as Chile and Peru, although commodity price volatility constrains 5G investment cycles. Africa remains a nascent market, with demand concentrated in South African mining and Nigerian oil operations, where satellite backhaul remains critical due to limited terrestrial infrastructure.

Competitive Landscape

Large incumbents such as Cisco Systems, Siemens AG, and Cradlepoint maintain leadership through global support networks, extensive certification portfolios, and deep integration across routing, security, and industrial automation stacks. Their value proposition centers on reliability, lifecycle management, and compliance with multi-region standards, which are critical for utilities, transportation, and defense buyers. Product innovation is increasingly focused on convergence, as seen with Belden Inc. introducing platforms that embed virtualized security functions to reduce hardware sprawl and simplify network architecture in regulated environments.

Challengers, including Teltonika Networks, Robustel, and Digi International, are competing aggressively on price and flexibility, particularly in mobile and small-scale industrial deployments. These vendors often undercut incumbents significantly, enabling faster adoption in cost-sensitive use cases such as logistics, remote monitoring, and SME industrial automation. At the same time, niche innovators such as Meridian5G are differentiating through hybrid connectivity models, including satellite-cellular bonding, which addresses persistent coverage gaps in remote or disaster-prone environments.

Specialized players such as Moxa Inc. are building competitive advantage through compliance-led differentiation, with certifications like IEC 62443-4-2 positioning them strongly in critical infrastructure segments. However, gaps remain across the market, particularly in highly demanding applications such as ATEX Zone 0 hazardous environments and advanced satellite bonding capabilities. These white spaces create entry points for agile newcomers who can combine ruggedization, advanced security, and multi-network orchestration.

Rugged Router Industry Leaders

Cisco Systems Inc.

Sierra Wireless Inc.

Advantech Co. Ltd.

Digi International Inc.

Cradlepoint Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Belden launched the BRS-5G industrial switch with network slicing and virtual firewalls.

- April 2026: Viasat introduced the Tactical Mission Fabric for multi-link bonding in contested zones.

- March 2026: Digi International released the IX25 5G industrial router with optional Wi-Fi 6E.

- March 2026: Belden announced a Virtual Firewall add-on for industrial networks.

Global Rugged Router Market Report Scope

The rugged router market comprises networking devices engineered to operate reliably in harsh environmental conditions, including extreme temperatures, vibration, humidity, and electromagnetic interference. These routers enable secure, continuous data transmission across mission-critical applications in industries such as energy, transportation, mining, defense, and industrial automation, supporting technologies like LTE, 5G, and industrial Ethernet for remote and mobile connectivity.

The Rugged Router Market Report is Segmented by Product Type (Cellular, Industrial Ethernet, Wireless Mesh, Tactical Military-Grade, snd Software-Defined), Connectivity Technology (4G/LTE, 5G, Wi-Fi 6/6E, Dual Connectivity, and Satellite Backhaul), End-Use Industry (Energy and Utilities, Transportation and Logistics, Oil and Gas, Mining, Manufacturing, Military and Defense, Public Safety, and Smart Cities), Deployment Mode (Fixed, Mobile Vehicle-Mounted, Portable, and Marine), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cellular Rugged Router |

| Industrial Ethernet Router |

| Wireless Mesh Router |

| Tactical Military-Grade Router |

| Software-Defined Rugged Router |

| 4G / LTE |

| 5G |

| Wi-Fi 6 / 6E |

| Dual Connectivity (Cellular and Wi-Fi) |

| Satellite Backhaul Enabled |

| Energy and Utilities |

| Transportation and Logistics |

| Oil and Gas |

| Mining |

| Manufacturing |

| Military and Defense |

| Public Safety |

| Smart Cities / Infrastructure |

| Fixed / Stationary |

| Mobile Vehicle-Mounted |

| Portable / Handheld |

| Marine / Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Type | Cellular Rugged Router | |

| Industrial Ethernet Router | ||

| Wireless Mesh Router | ||

| Tactical Military-Grade Router | ||

| Software-Defined Rugged Router | ||

| By Connectivity Technology | 4G / LTE | |

| 5G | ||

| Wi-Fi 6 / 6E | ||

| Dual Connectivity (Cellular and Wi-Fi) | ||

| Satellite Backhaul Enabled | ||

| By End-Use Industry | Energy and Utilities | |

| Transportation and Logistics | ||

| Oil and Gas | ||

| Mining | ||

| Manufacturing | ||

| Military and Defense | ||

| Public Safety | ||

| Smart Cities / Infrastructure | ||

| By Deployment Mode | Fixed / Stationary | |

| Mobile Vehicle-Mounted | ||

| Portable / Handheld | ||

| Marine / Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the rugged router market be by 2031?

The rugged router market size is forecast to reach USD 8.68 billion by 2031, expanding at a 9.71% CAGR from 2026, per Mordor Intelligence.

Which segment currently holds the largest share?

Industrial Ethernet led with 34.6% rugged router market share in 2025, driven by substation and factory automation deployments.

Which region is expected to grow the fastest during the forecast period?

Asia-Pacific is projected to post the highest CAGR at 11.34% through 2031, supported by BharatNet and smart mining investments.

Why are tactical military-grade routers gaining momentum?

Defense agencies are moving to zero-trust, self-healing 5G and SATCOM meshes, pushing tactical routers to an 11.12% CAGR through 2031.

What restrains faster 5G adoption in industrial routers?

High upfront hardware costs and tight supply of rugged 5G components have stretched lead times to nine months, slowing upgrades in price-sensitive regions.

How concentrated is supplier power in this market?

The top three vendors hold about 35-40% of global revenue, indicating moderate concentration that still leaves room for specialized challengers.

Page last updated on: