Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 18.13 Billion |

| Market Size (2031) | USD 28.02 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

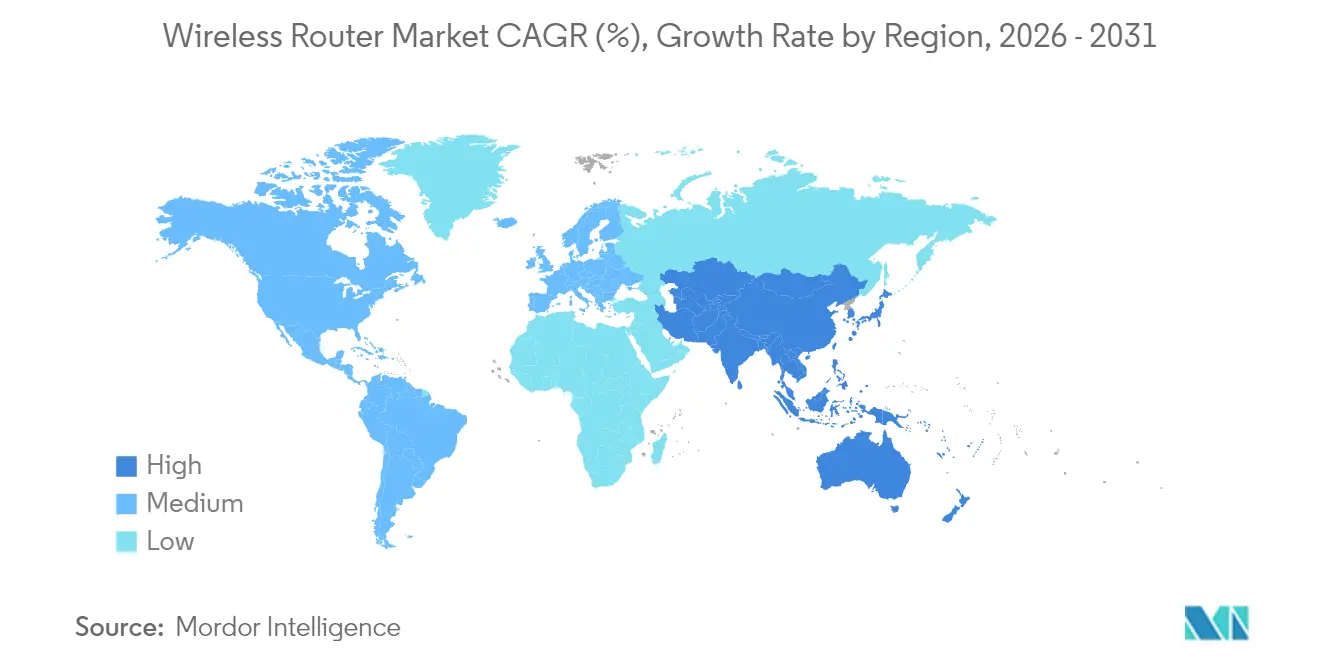

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wireless Router Market Analysis by Mordor Intelligence

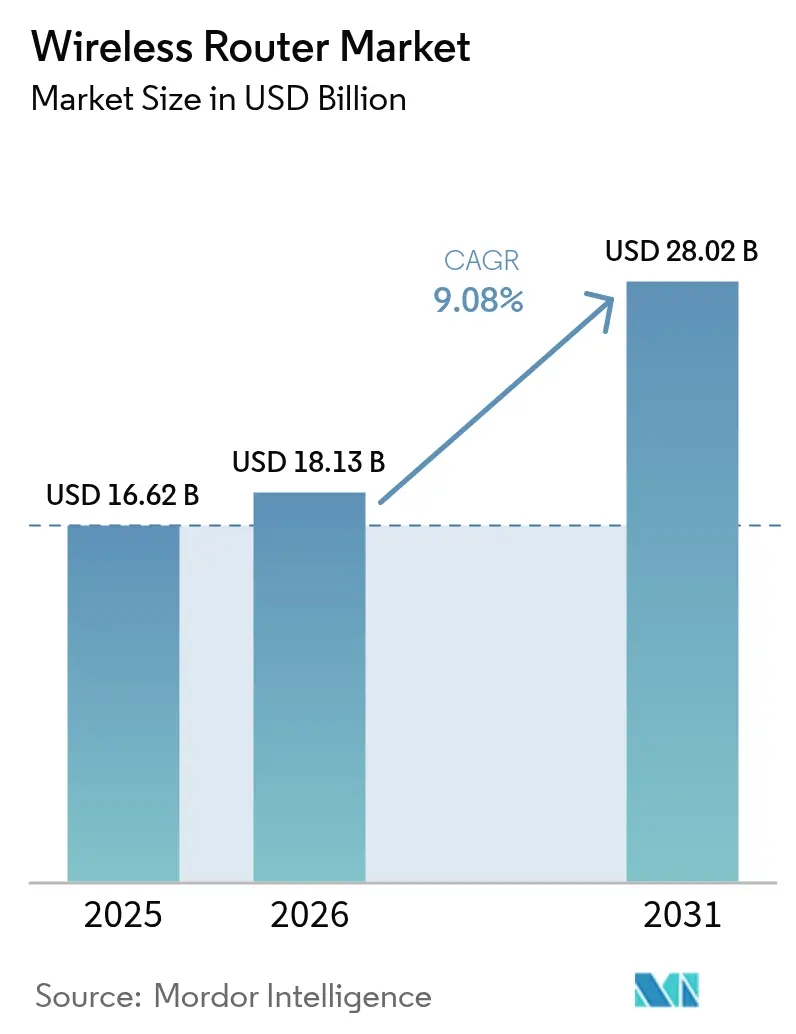

Wireless router market size in 2026 is estimated at USD 18.13 billion, growing from 2025 value of USD 16.62 billion with 2031 projections showing USD 28.02 billion, growing at 9.08% CAGR over 2026-2031. Growth springs from surging enterprise digitalization, rising residential bandwidth needs, and rapid commercialization of Wi-Fi 7. Device shipments for Wi-Fi 7 totaled 269 million units in 2024 and are projected to exceed 2.1 billion by 2028, underscoring pent-up demand for multi-gigabit performance. A parallel boom in 6 GHz Wi-Fi hardware—807.5 million units shipped in 2024—confirms strong ecosystem readiness as 63 nations free portions of the 6 GHz band for unlicensed use. Mesh systems, higher-bandwidth tri-band designs, and ISP-managed CPE bundles are expanding total addressable demand, while fixed-wireless access and semiconductor supply constraints create pockets of volatility. Vendors now race to add AI-powered management and network-as-a-service features to preserve pricing power and mitigate intensifying price competition from low-cost Chinese suppliers.

Key Report Takeaways

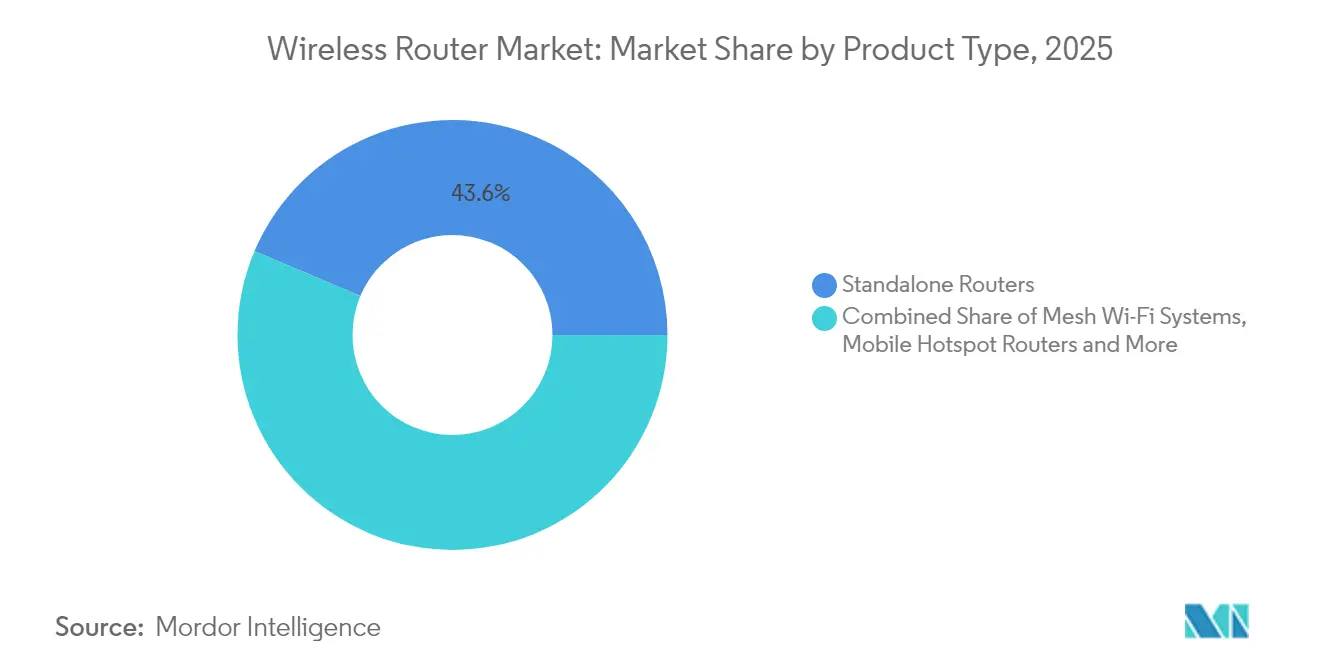

- By product type, standalone routers led with 43.62% of wireless router market share in 2025; mesh Wi-Fi systems are projected to expand at an 11.74% CAGR through 2031.

- By Wi-Fi standard, Wi-Fi 5 accounted for a 41.55% share in 2025, while Wi-Fi 7 is advancing at a 24.74% CAGR to 2031.

- By frequency band, dual-band systems held 49.10% share in 2025; tri-band designs are poised for 15.62% CAGR as 6 GHz adoption broadens.

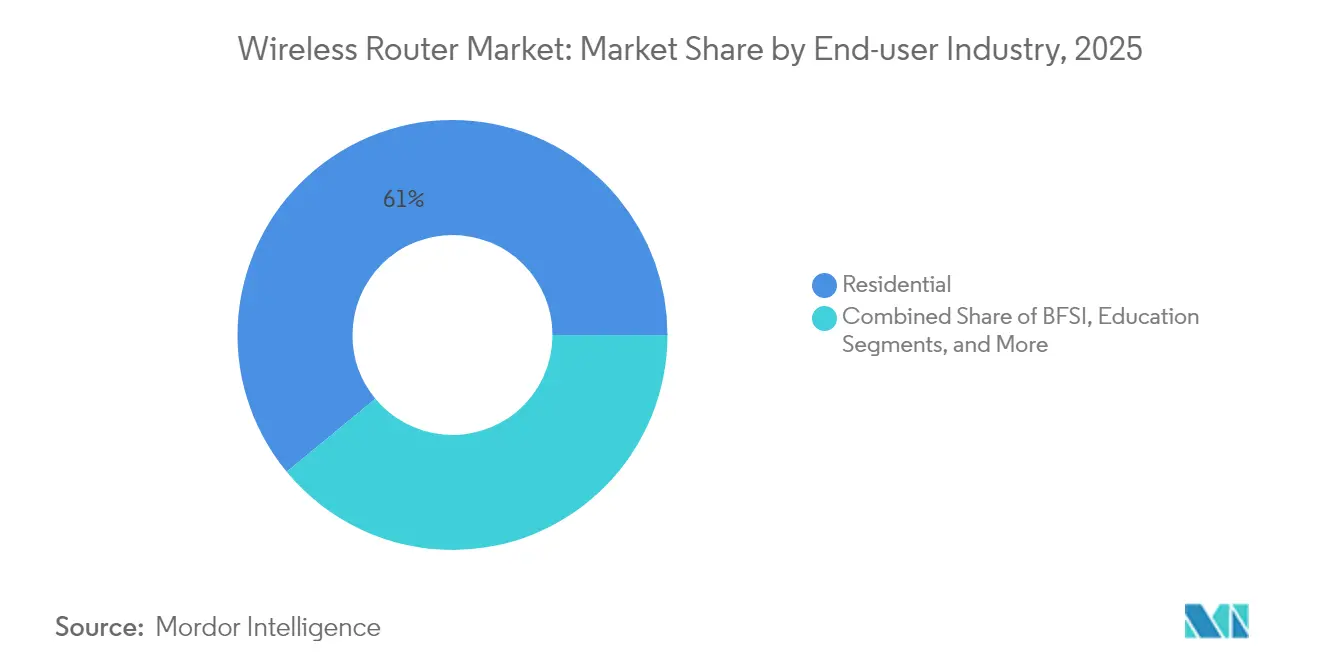

- By end-user, residential applications represented 60.98% share in 2025, whereas enterprise deployments are set to climb at a 9.72% CAGR on the back of AI workload growth.

- By distribution channel, ISP-bundled sales commanded a 45.62% share in 2025, while online retail is forecast to rise at an 11.12% CAGR through 2031.

- By geography, Asia-Pacific dominated with a 33.55% share in 2025; South America is projected to be the fastest-growing region at a 10.47% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wireless Router Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing internet traffic and connected devices | +2.1% | Global; APAC and North America lead | Medium term (2-4 years) |

| Enterprise digitalization and bandwidth demand | +1.8% | North America and EU; expanding to APAC | Short term (≤ 2 years) |

| Rapid adoption of Wi-Fi 6/6E and Wi-Fi 7 | +2.3% | Global, driven by developed markets | Medium term (2-4 years) |

| Mesh Wi-Fi as an ISP-managed service | +1.4% | North America and EU | Short term (≤ 2 years) |

| Government-funded rural broadband CPE | +0.9% | Rural regions worldwide | Long term (≥ 4 years) |

| Emerging Wi-Fi sensing applications | +0.5% | North America and EU early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Internet Traffic and Connected Devices

More than 21.1 billion Wi-Fi devices are active worldwide, and another 4.1 billion are expected to ship in 2024, saturating legacy networks and prompting upgrades to multi-gigabit routers. Roughly one-fifth of residential broadband users now exceed 1 TB of monthly data, stressing quality-of-service thresholds. IoT growth in smart factories, smart cities, and autonomous mobility deepens the need for low-latency throughput that Wi-Fi 7’s 320 MHz channels can deliver. Enterprises face device-density headaches when Wi-Fi 6 access points hit practical limits, forcing investment in next-generation radios. The result is an accelerated refresh cycle favoring vendors with Wi-Fi 7 portfolios.

Enterprise Digitalization Driving Bandwidth Demand

Forty-five percent of enterprises already trial both Wi-Fi 6 and private 5G in parallel, highlighting a preference for converged wireless fabrics. Manufacturing plants adopt Wi-Fi 7 to run AI-enabled robotics, sub-millisecond supervisory control, and machine-vision analytics. Quarterly router orders tied to AI infrastructure surpassed USD 350 million among leading suppliers in 2025. Subscription-based network-as-a-service models lower capex barriers, allowing faster rollouts. In short, bandwidth-hungry applications and flexible financing coalesce to push the wireless router market forward.

Rapid Adoption of Wi-Fi 6/6E and Wi-Fi 7

The Wi-Fi 7 certification program launched in January 2024, triggering 231.4 million device shipments that year and putting enterprise AP penetration on course to reach 10% of total shipments in 2025. Multi-link operation lets access points use 2.4 GHz, 5 GHz, and 6 GHz simultaneously, delivering real-world rates between 6 Gbps and 15 Gbps—far above Wi-Fi 6 ceilings[1]“Wi-Fi 7 speeds: What enterprises can expect,” Meter, meter.com . ISPs in markets such as France bundle Wi-Fi 7 routers with gigabit fiber to curb churn and raise ARPU. Yet client-device adoption still lags, as only 87% of new PCs support 320 MHz channels, creating a short-term asymmetry that nonetheless keeps router demand robust.

Mesh Wi-Fi as a Managed Service by ISPs

Cloud-managed mesh platforms like TP-Link’s Aginet have already been adopted by hundreds of North American ISPs, confirming service-provider appetite for recurring revenue beyond connectivity. Amazon’s eero now reports that roughly one-third of its customers come via ISP partnerships, validating the model’s scale. Managed mesh offerings improve whole-home coverage, enable proactive troubleshooting, and reduce support calls. Vendors also extend the concept to SMBs through platforms such as Airties Pro, broadening the serviceable base. The value proposition rests on a premium experience rather than raw hardware margin, lifting average selling prices despite commoditization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Network-security complexity & skill gaps | -1.2% | Global, acute in developed markets | Short term (≤ 2 years) |

| Mobile/5G broadband substitution risk | -1.6% | Global, led by urban markets | Medium term (2-4 years) |

| Semiconductor supply-chain volatility | -0.8% | Global manufacturing impact | Short term (≤ 2 years) |

| Uneven global release of 6 GHz spectrum | -0.7% | Regional fragmentation worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Network-Security Complexity and Skill Shortages

A 3.8 Tbps DDoS attack exploiting the ASUS router CVE-2024-3080 illustrated the sector’s exposure to firmware vulnerabilities[2]Rescana Research Team, “CVE-2024-3080 critical vulnerability in ASUS routers,” Rescana, rescana.com. Meanwhile, telecom operators report a 33% shortfall in qualified network engineers, particularly for emerging Wi-Fi 7 security and WPA3 configurations. Enterprises face higher deployment costs due to specialist consulting needs, stretching project lead times. Small firms often default to lax settings, heightening breach risks and limiting the adoption of premium routers with advanced threat detection.

Mobile/5G Broadband Substitution Risk

Fixed-wireless access counted nearly 12 million U.S. subscriptions by end-2024 and could top 20 million by 2028, offering consumers a cable-free alternative to in-home Wi-Fi[3]Fitch Ratings, “Fixed wireless access growth disrupts U.S. telecom market,” fitchratings.com . Telcos pitch 5G service as cheaper and simpler than fiber, and private 5G networks appeal to enterprises for mobility-first use cases. While Wi-Fi still enjoys capacity and indoor-coverage advantages, cellular encroachment tempers long-run growth expectations for the wireless router market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mesh Systems Drive Innovation

Standalone routers retained a 43.62% share in 2025, yet the mesh category is on track for an 11.74% CAGR through 2031 as users seek wall-to-wall coverage and self-optimizing performance. The wireless router market size tied to mesh deployments is forecast to expand in tandem with multi-gigabit fiber rollouts. ISP adoption of cloud-managed platforms such as Aginet and eero for Service Providers reinforces growth momentum. In contrast, mobile hotspot routers gain renewed relevance by embedding 5G radios, while industrial models address harsh-environment requirements.

Mesh vendors now bake in AI algorithms, Wi-Fi 7 multi-link operation, and 320 MHz backhaul channels to sustain premium pricing. Standalone designs increasingly target gamers, featuring tri-band radios and latency-shaping engines. Industrial routers leverage SD-WAN overlays to connect remote assets securely. Collectively, these sub-segments illustrate how innovation niches defend margin even as entry-level hardware commoditizes.

By Wi-Fi Standard: Wi-Fi 7 Accelerates Market Transformation

Wi-Fi 5 still commands 41.55% share thanks to mass-market affordability, but Wi-Fi 7 shipments are set for a 24.74% CAGR that will reshape the wireless router market. Enterprise demand for 6-15 Gbps real-world throughput pushes early adoption, and the wireless router market size linked to Wi-Fi 7 could surpass Wi-Fi 6 by the decade’s end. Certification has eased multi-vendor interoperability concerns, although higher power requirements necessitate PoE switch upgrades.

Wi-Fi 6 remains a bridge technology, offering OFDMA efficiency to budget-constrained buyers. Legacy Wi-Fi 4 devices persist in niche IoT settings where cost and power trump speed. In advanced regions, procurement roadmaps now include phased Wi-Fi 7 rollouts paired with edge-compute investments, ensuring future-proof capacity without forklift overhauls.

By Frequency Band: Tri-Band Configurations Gain Momentum

Dual-band models held a 49.10% share in 2025, but tri-band and quad-band designs should post a 15.62% CAGR as 6 GHz spectrum opens. Vendors exploit the fresh 1,200 MHz channel block to dedicate clean 320 MHz links for backhaul, enhancing mesh resilience. The wireless router market share advantage for dual-band gear narrows each year, particularly in regions that have cleared the full 6 GHz band for unlicensed use.

Single-band SKUs endure in cost-sensitive IoT and industrial control applications. Regulatory fragmentation—China’s decision to reserve 6 GHz for 5G, for example, forces manufacturers to produce region-specific SKUs, complicating supply chains. Nevertheless, multi-band flexibility remains a key differentiator in premium and enterprise segments.

By End-User Industry: Enterprise Segment Drives Premium Adoption

Residential demand still accounts for 60.98% of 2025 revenue, fuelled by hybrid-work lifestyles and smart-home adoption. Enterprise deployments, however, are rising at a 9.72% CAGR, contributing an outsized share of the incremental wireless router market size. BFSI leads with latency-critical trading floors, while healthcare outfits deploy Wi-Fi 7 to connect telemedicine devices securely.

Public-sector budgets anchored by the USD 42.45 billion BEAD program expand rural connectivity, channeling funds toward advanced CPE. Retailers leverage analytics-ready Wi-Fi to automate inventory and personalize shopper engagement. Collectively, enterprise verticals propel router ASPs above commodity levels.

By Distribution Channel: Online Retail Accelerates Direct Sales

ISP bundles comprised 45.62% of 2025 shipments, reflecting carriers’ push to lower churn with premium CPE. Online marketplaces are forecast for 11.12% CAGR, capturing consumers who favor direct hardware ownership and subscription-based support plans. As a result, the wireless router market size derived from e-commerce continues to rise disproportionately.

Traditional brick-and-mortar stores maintain a foothold for hands-on evaluation, particularly in emerging markets. ISPs, meanwhile, are pivoting to managed-Wi-Fi subscriptions that package hardware, software, and analytics into predictable monthly fees. Vendors like NETGEAR already report USD 35 million in annual recurring revenue from such services.

Geography Analysis

Asia-Pacific held 33.55% of global revenue in 2025, buoyed by 5G rollouts, smart-city programs, and ongoing manufacturing digitization. National initiatives in Singapore and South Korea anchor demand for Wi-Fi 7 backbone connectivity, while Chinese vendors navigate overseas regulatory headwinds tied to security scrutiny. Hyperscale data-center expansion throughout the region further bolsters enterprise orders for high-throughput routers.

North America remains pivotal, thanks to aggressive fiber builds and sizable BEAD funding that directs equipment to underserved rural zones. Fixed-wireless access surpassed 12 million subscribers in 2024, simultaneously pressuring and complementing router sales via hybrid cellular-Wi-Fi gateways. Enterprises already account for 2% of Wi-Fi 7 AP shipments, a figure expected to quintuple by 2025.

Europe posts steady gains behind multi-gigabit fiber and phased 6 GHz clearance. France leads Wi-Fi 7 adoption, showcasing how premium CPE differentiates broadband tiers. Germany and the U.K. prioritize Industry 4.0 and secure networking, driving demand for tri-band routers with WPA3 and AI-powered threat analytics. Regulatory nuances post-Brexit still complicate certification timetables, nudging vendors toward localized logistics strategies.

South America registers the fastest trajectory at 10.47% CAGR on the back of fiber-to-the-home expansion and rural-connectivity subsidies. Brazil spearheads rollouts, while regional currency volatility forces creative pricing models. Emerging markets in the Middle East and Africa are leveraging smart-city ambitions to pilot Wi-Fi 7 in hospitality, education, and public-sector environments, laying groundwork for long-term demand.

Regulatory Landscape

Wireless routers face overlapping radio, cybersecurity, and supply-chain compliance requirements, with market access tied to spectrum rules and equipment authorization regimes. In the United States, the Federal Communications Commission (FCC) governs device authorization and has active actions under the Secure Networks Act framework, including updates tied to the Covered List that influence which residential router hardware can be authorized for sale and deployment. Spectrum policy also shapes feature availability, as 6 GHz access varies by country, even as many markets have opened portions of the band for unlicensed use.

Industry-led certification is a second compliance gate that shapes procurement, particularly for ISP bundles and enterprise deployments. The Wi-Fi Alliance launched Wi-Fi CERTIFIED 7 in January 2024 to formalize interoperability for IEEE 802.11be features (including operation across 2.4 GHz, 5 GHz, and 6 GHz), and certification requirements emphasize modern security baselines such as WPA3 and Protected Management Frames. As Wi-Fi 7 moves into wider commercial deployments, vendors and ODMs increasingly synchronize product roadmaps with certification timelines to reduce channel friction and shorten operator qualification cycles.

Value Chain Analysis

The wireless router value chain is largely horizontal: Wi-Fi and networking silicon (Wi-Fi chipsets, CPUs, RF front-end components, and memory) feed into OEM/ODM platform design, manufacturing and final assembly, then flow through ISP procurement and bundling, enterprise channels, and online and offline retail. Silicon power is concentrated among a small set of chipset suppliers (Broadcom, Qualcomm, MediaTek, Realtek, and Intel), and leading-edge fabrication dependence (notably on TSMC for many nodes) creates a chokepoint when capacity is tight. On the assembly side, residential CPE output is concentrated among a relatively small group of ODMs such as Sercomm, Arcadyan, Hitron, Askey, Sagemcom, Vantiva, Arris, and others, which manufacture across high-volume, cost-optimized footprints.

Supply-chain risk management has become a differentiator as router BOMs absorb higher DRAM and NAND requirements for Wi-Fi 7, mesh backhaul, and added security and management functions, while components such as memory and substrates can constrain shipment timing. Manufacturing geography is also shifting, with China-centered assembly supplemented by migrations to Vietnam, India, and Mexico to diversify risk and meet changing procurement requirements from large operators. Operator-driven software platforms (cloud-managed mesh and managed Wi-Fi) pull more value toward firmware, telemetry, and lifecycle management, shifting margins from one-time hardware sales to services and support contracts.

Competitive Landscape

Competition is moderate yet heating fast as incumbent networking giants juggle commoditization and feature races. TP-Link dominates consumer channels but now confronts a U.S. criminal antitrust probe over pricing tactics. Cisco safeguards enterprise leadership with integrated security and service-provider relationships. In July 2025, HPE finalized a USD 14 billion acquisition of Juniper Networks, doubling its networking footprint and intensifying pressure on Cisco.

Strategic pivots center on software and AI. NETGEAR generated USD 35 million in recurring subscription revenue in 2024, underscoring a shift toward service-led monetization. Amazon’s eero leverages the retail giant’s commerce engine to undercut rivals and expand ISP partnerships. Airgain targets fleet connectivity with 5G-Wi-Fi gateways, carving a niche in vehicular networking.

Innovation hot spots include AI-driven network analytics, managed-service orchestration, and rugged industrial designs. Vendors differentiate on silicon roadmaps—early Wi-Fi 7 chipsets with 4096-QAM and 320 MHz support—and on zero-trust security layers. Overall, pricing competition persists, but feature innovation and services sustain margin opportunities for market leaders.

Wireless Router Industry Leaders

ASUSTeK Computer Inc.

Netgear Inc.

D-Link Corporation

Huawei Technologies Co. Limited

TP-Link Technologies Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wi-Fi 7 commercialization is creating clear whitespace for premiumization, particularly where 6 GHz operation is permitted and where ISPs use CPE differentiation to reduce churn. Mesh platforms and gaming-focused routers are capturing a larger share of value, even as overall consumer router unit volumes face pressure from ISP-provided gateways and deferred retail upgrades. 2026 market signals point to higher-value segments (mesh and gaming) rather than broad-based unit expansion. Vendors that pair tri-band and 6 GHz hardware with cloud management and subscription features, including managed mesh programs used by ISPs and recurring-revenue services highlighted by vendors such as NETGEAR, have more room to defend ASPs amid price competition.

Regulatory and standards milestones are also opening targeted opportunities. In the United States, the FCCs 6 GHz framework (effective April 27, 2026) provides structure for additional unlicensed device operation modes. In Europe, harmonization steps, including Ukraines May 6, 2026 update aligning conditions for Wi-Fi 6E and Wi-Fi 7 in the 5945-6425 MHz band, support clearer go-to-market planning in parts of the region. On the technology horizon, the IEEE 802.11bn task group (Wi-Fi 8) is progressing on ultra-high reliability concepts such as extended multi-link operation and latency-oriented enhancements, expanding the set of enterprise, industrial, and time-sensitive connectivity use cases where determinism matters alongside peak throughput.

Recent Industry Developments

- April 2026: ASUS announced the ProArt Router PRT-BE5000, bringing Wi-Fi 7 features into its creator-focused ProArt ecosystem. The announcement pushes Wi-Fi 7 further beyond gaming and enterprise into prosumer studio networking and supports higher ASP-focused segmentation.

- October 2025: TP-Link announced the Archer GE400 dual-band Wi-Fi 7 gaming router as part of its Wi-Fi 7 gaming lineup expansion. The product positioning targets latency-sensitive use cases and supports value growth in retail channels where buyers pay for differentiated performance and software features.

- January 2024: The Wi-Fi Alliance launched the Wi-Fi CERTIFIED 7 program to formalize interoperability for IEEE 802.11be capabilities. Certification availability accelerated multi-vendor compatibility validation and lowered procurement friction for enterprise and service-provider rollouts that require standardized security and band operation testing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the wireless router market is measured as the revenue earned from selling wireless routers that provide Wi-Fi connectivity, across home, small office, and enterprise settings, and across major Wi-Fi standards and form factors.

Scope exclusions: Services revenue (such as managed Wi-Fi subscriptions, installation labor, and extended warranties) is excluded from the market value.

Segmentation Overview

- By Product Type

- Standalone Routers

- Mesh Wi-Fi Systems

- Mobile Hotspot Routers

- Industrial/Rugged Routers

- By Wi-Fi Standard

- 802.11n (Wi-Fi 4)

- 802.11ac (Wi-Fi 5)

- 802.11ax (Wi-Fi 6)

- 802.11be (Wi-Fi 7)

- By Frequency Band

- Single-Band

- Dual-Band

- Tri-/Quad-Band

- By End-user Industry

- Residential

- Enterprise

- BFSI

- Education

- Healthcare

- Media and Entertainment

- Retail

- Government and Public Sector

- Other Enterprises

- By Distribution Channel

- Online Retailers

- Offline (CE Stores, Hypermarkets)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by pinning down the demand and supply signals that can be checked in public data before assumptions are made. We typically review standards and certification updates from bodies such as IEEE and Wi-Fi Alliance, and we also use spectrum and equipment rules from regulators such as the FCC and comparable agencies in other regions.

To size and sanity-check adoption, we use broadband and household connectivity indicators from sources such as the International Telecommunication Union, World Bank, OECD, and national statistics offices, alongside trade and shipment context from customs portals and industry association publications. Company filings, annual reports, earnings presentations, and reputable press help map product cycles, including Wi-Fi 6E and Wi-Fi 7 timing, plus shifts in channel mix. Where additional coverage is needed, we also use paid subscriptions for company financials and intelligence, news and financials, and patent databases to track feature direction and public claims. These sources are illustrative only, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary interviews and surveys test what the desk research signals cannot explain end-to-end, especially pricing movement, mix shifts between standalone and mesh, and enterprise replacement timing. We speak with stakeholders across the value chain, including product managers, channel partners, network integrators, and large buyers, then cross-check the inputs across APAC, EMEA, and the Americas so the model does not lean on one region's adoption pattern.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 43% |

| Mid tier: 47% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 20% | Managers: 51% | Americas: 21% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach that reconstructs addressable router spend by linking connected households and business sites to router ownership, refresh cycles, and average selling prices across key Wi-Fi standards. Once that total is formed, we use selective bottom-up checks to keep it realistic, such as cross-checking supplier revenue exposure, sampling online and offline price points, and using channel feedback on unit velocity, which are then used to adjust extreme outputs.

A few inputs typically move the total most: the installed base of broadband homes, the share of fiber and gigabit plans, Wi-Fi 6 and 6E penetration in new purchases, early Wi-Fi 7 readiness, mesh system attach rates, and the split of online versus store-led sales. When country-level data is thin, we handle the gap by using proxy indicators like urban households, average data usage, and the observed mix in comparable markets, then re-testing with interview feedback.

For the forecast, we run scenario analysis so different upgrade-speed paths can be applied to standards adoption and pricing. The selected scenario is then aligned to what primary respondents consider the most likely replacement cycle and feature uptake over the next few years.

Data Validation & Update Cycle

Outputs are validated through several checks so the final number is not driven by a single weak assumption. We compare implied units, pricing, and refresh cadence against independent signals such as broadband subscriber trends, retail price bands, and standard transition timing, then review and correct outliers before sign-off.

A second analyst review re-checks definitions, conversions, and any large year-on-year jumps. If a variance traces back to one weak input, follow-up outreach is triggered to confirm the assumption. Reports refresh annually, with interim updates when material events occur, and a final pre-delivery pass ensures clients receive the most current view.

Mordor Intelligence's Wireless Router Market Estimate Compared With Other Published Estimates

Published market sizes for wireless routers do not always match, even when the titles look similar, because the scope and counting logic can shift in small but important ways. Differences usually come from what is treated as product revenue versus service revenue, the base year used, and the assumed speed of price declines during a Wi-Fi generation change.

For wireless routers, the spread is often driven by whether mesh systems, mobile hotspot routers, and rugged or industrial models are counted fully, and whether the study follows an adoption-led model tied to connected homes and business sites or relies on a simpler trend-line projection. Currency timing and the use of aggressive versus conservative upgrade scenarios for Wi-Fi 6E and Wi-Fi 7 also shift the total, particularly when a study is not refreshed close to major chipset and standards milestones.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.13 B (2026) | |

| Industry Publisher A | USD 15.64 B (2023) | Uses an earlier base year and a different standard list focus, which can understate the later-cycle lift from mesh adoption and Wi-Fi 6E and Wi-Fi 7 transition timing. |

| Industry Publisher B | USD 14.10 B (2025) | Anchors sizing to a 2025 value and extends the forecast to 2035, which can change the implied price erosion curve and the mix split between standalone and mesh compared with a 2026 anchored model. |

The table shows that the biggest differences come from base-year choice and how the model treats mix and pricing across standards. By separating device revenue from add-on services and tying demand to connected households, enterprise site needs, and refresh cycles, the estimate stays traceable to clear inputs, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the projected value of the global wireless router market in 2031?

It is forecast to reach USD 28.02 billion by 2031, growing at a 9.08% CAGR.

How fast will Wi-Fi 7 adoption grow over the forecast period?

Wi-Fi 7 router shipments are set for a 24.74% CAGR through 2031 as enterprises and ISPs seek multi-gigabit capabilities.

Which router product type is expanding the quickest?

Mesh Wi-Fi systems are the fastest-growing, advancing at an 11.74% CAGR as whole-home coverage and managed services gain traction.

Which sales channel is gaining most rapidly?

Online retail is rising at an 11.12% CAGR due to direct-to-consumer demand and subscription-based support models.

Why is Asia-Pacific the largest regional market?

Robust 5G deployments, smart-city initiatives, and extensive manufacturing digitization give Asia-Pacific a commanding 33.55% revenue share.

Page last updated on: