Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Rugged Server Market Report is Segmented by Type (Semi-Rugged, Fully-Rugged, and More), Enterprise Size (SMEs and Large Enterprises), End-User (Military and Defense, Aerospace, and More), Form Factor (Rack-Mount, Blade, and More), Cooling Type (Passive and Fan-Based/Active), Memory Capacity (Less Than 256 GB, 256 - 512 GB, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

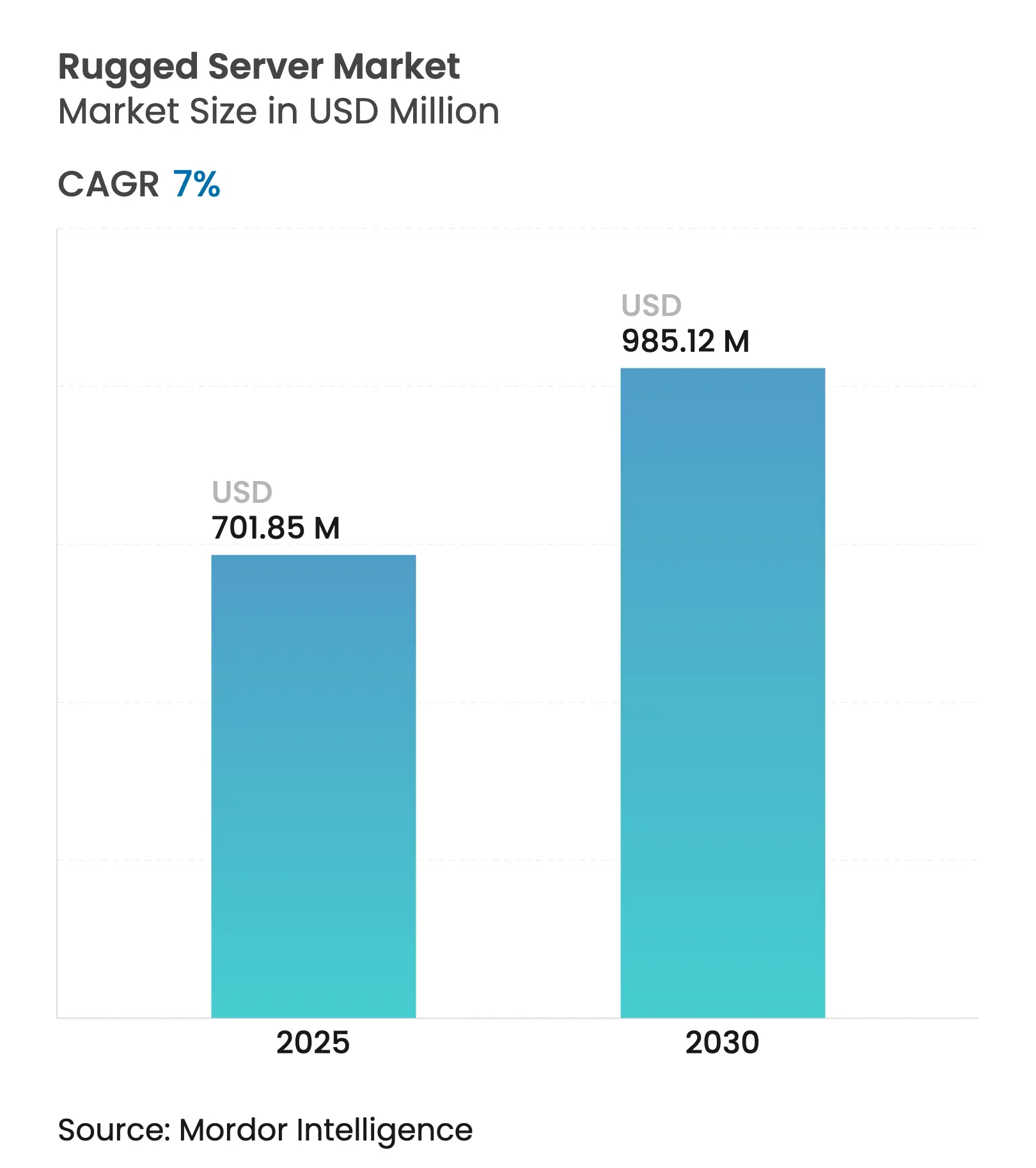

| Market Size (2025) | USD 701.85 Million |

| Market Size (2030) | USD 985.12 Million |

| Growth Rate (2025 - 2030) | 7.00 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The rugged server market is valued at USD 701.85 million in 2025 and is forecast to reach USD 985.12 million by 2030, advancing at a 7.0% CAGR. Edge-computing build-outs, zero-trust security mandates, and continued defense modernization underpin the upward trajectory. North America retains leadership, supported by high military outlays and mature aerospace supply chains, while Asia-Pacific posts the fastest rise as China and India digitize defense and factory floors. Fully-rugged platforms hold sway thanks to MIL-STD-grade tolerance, yet ultra-rugged variants are expanding as uncrewed vehicles and remote sites call for greater shock and temperature endurance. Vendor activity centers on integrating cyber-hardening, AI acceleration, and modular SWaP-optimized form factors to meet mission-specific demands.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing

demand in defense and aerospace

Increasing

demand in defense and aerospace

| +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

| Geographic Relevance:

North

America, Europe, Asia-Pacific

| Impact Timeline:

Medium

term (2-4 years)

|

Industrial

automation and IIoT expansion

Industrial

automation and IIoT expansion

| +1.7% | Global, Asia-Pacific focus | Long term (≥ 4 years) | |||

Edge-computing

roll-outs in harsh sites

Edge-computing

roll-outs in harsh sites

| +1.5% | Global | Medium term (2-4 years) | |||

Modular

SWaP-optimized servers for UAVs and UGVs

Modular

SWaP-optimized servers for UAVs and UGVs

| +0.9% | North America, Europe | Medium term (2-4 years) | |||

Zero-trust

cyber-hardening mandates

Zero-trust

cyber-hardening mandates

| +0.6% | North America, Europe | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing demand in defense and aerospace

Massive investments in autonomous systems and AI-enabled battlefield networks are fueling rugged server uptake across air, land, and sea platforms. In 2024, the U.S. Department of Defense issued thousands of contracts above USD 25,000 for hardened computing upgrades, signaling entrenched replacement cycles for legacy hardware[1]U.S. Department of Defense, “Contracts For Dec. 1, 2024,” defense.gov. Platforms such as Mercury Systems’ RES HD blade series allow rapid module swaps while sustaining classified data handling in contested zones. SOSA-aligned mission computers, including the ROCK3 launched in 2025, demonstrate how certification and security now guide system architecture, not simply physical durability. European forces follow suit through NATO tactical cloud pilots, cementing a medium-term demand pipeline for high-reliability compute nodes.

Industrial automation and IIoT expansion

Manufacturers are moving analytics from central data centers to shop-floor assets, exposing servers to vibration, dust, and fluctuating temperatures. Siemens’ new Simatic IPC BX-59A with integrated NVIDIA GPU offers 25-fold AI acceleration for quality control at the edge, cutting inspection latency while coping with ambient heat and debris. Automotive paint shops and semiconductor fabs are early adopters, using rugged enclosures to house predictive-maintenance algorithms that must run continuously. These deployments expand the rugged server market addressability beyond traditional defense segments, especially across Asia-Pacific, where electronics firms pursue lights-out factories.

Edge-computing roll-outs in harsh sites

Retail chains, energy utilities, and telecom operators are extending compute resources to unmanned rooms, curbside cabinets, and offshore platforms. Dell’s PowerEdge XR series delivers rack-class performance inside shortened, sealed chassis able to withstand dust, humidity, and a wide temperature span. NativeEdge management software reduces truck rolls by enabling remote BIOS and firmware control, aligning with zero-touch maintenance objectives. As 5G expands and AI inference happens closer to sensors, rugged server demand aligns with broader edge-infrastructure CAPEX flows.

Modular SWaP-optimized servers for UAVs and UGVs

Unmanned systems impose tight limits on size, weight, and power, yet require high compute density for autonomy and sensor fusion. Mercury Systems’ NanoSWITCH FLEX provides managed Ethernet switching in an IP67 case that rides aboard drones and ground robots while tolerating -40 °C to 71 °C extremes. Comparable fanless mission computers weigh under 2 kg, enabling longer flight endurance. Defense primes increasingly specify modular payload bays, enabling server refresh through plug-and-play cards rather than airframe redesigns, lifting demand for short-depth, conduction-cooled motherboards.

Zero-trust cyber-hardening mandates

U.S. Executive Orders and NATO directives push defense agencies toward hardware root-of-trust, secure boot, and encrypted storage on every deployed node. Mercury Systems’ acquisition of Star Lab in 2025 underscores how embedded security software now shapes procurement criteria. Vendors integrate FPGA-based cryptography and tamper detection to pass Defense Federal Acquisition Regulation Supplement (DFARS) clauses. Short-term impacts are significant in North America and Europe as programs rush to meet compliance deadlines.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High

initial capital cost

High

initial capital cost

| -0.8% | Global, higher in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.8%

| Geographic Relevance:

Global,

higher in emerging markets

| Impact Timeline:

Short

term (≤ 2 years)

|

COTS

non-rugged substitutes gaining spec upgrades

COTS

non-rugged substitutes gaining spec upgrades

| -0.5% | Global | Medium term (2-4 years) | |||

Traceable,

ITAR-compliant supply-chain constraints

Traceable,

ITAR-compliant supply-chain constraints

| -0.4% | North America, Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High initial capital cost

Rugged servers are often priced at 2-3 times comparable commercial units, stretching SME budgets. Acquisition outlays are compounded by specialized mounting kits, environmental testing, and user training. Financing schemes and pay-as-you-use contracts are emerging to soften the burden. Semi-rugged SKUs, positioned between consumer and military grades, open a bridge market but still face resistance where operational risk tolerance remains high.

COTS non-rugged substitutes gaining spec upgrades

Mainstream server vendors now add conformal coating, advanced cooling, and extended temperature ratings to data-center models, blurring category lines. ASUS displayed liquid-assisted cooling and reinforced sockets on its 2024 platforms aimed at AI clusters, indirectly threatening dedicated rugged suppliers by narrowing performance deltas[2]ASUS, “Extreme Cooling Solutions Unveiled at CloudFest 2024,” asus.com. Over the medium term, differentiation will rely more on secure provenance, MIL-STD validation, and bespoke chassis shapes than on raw component specification.

By Type: Ultra-rugged servers penetrate extreme deployments

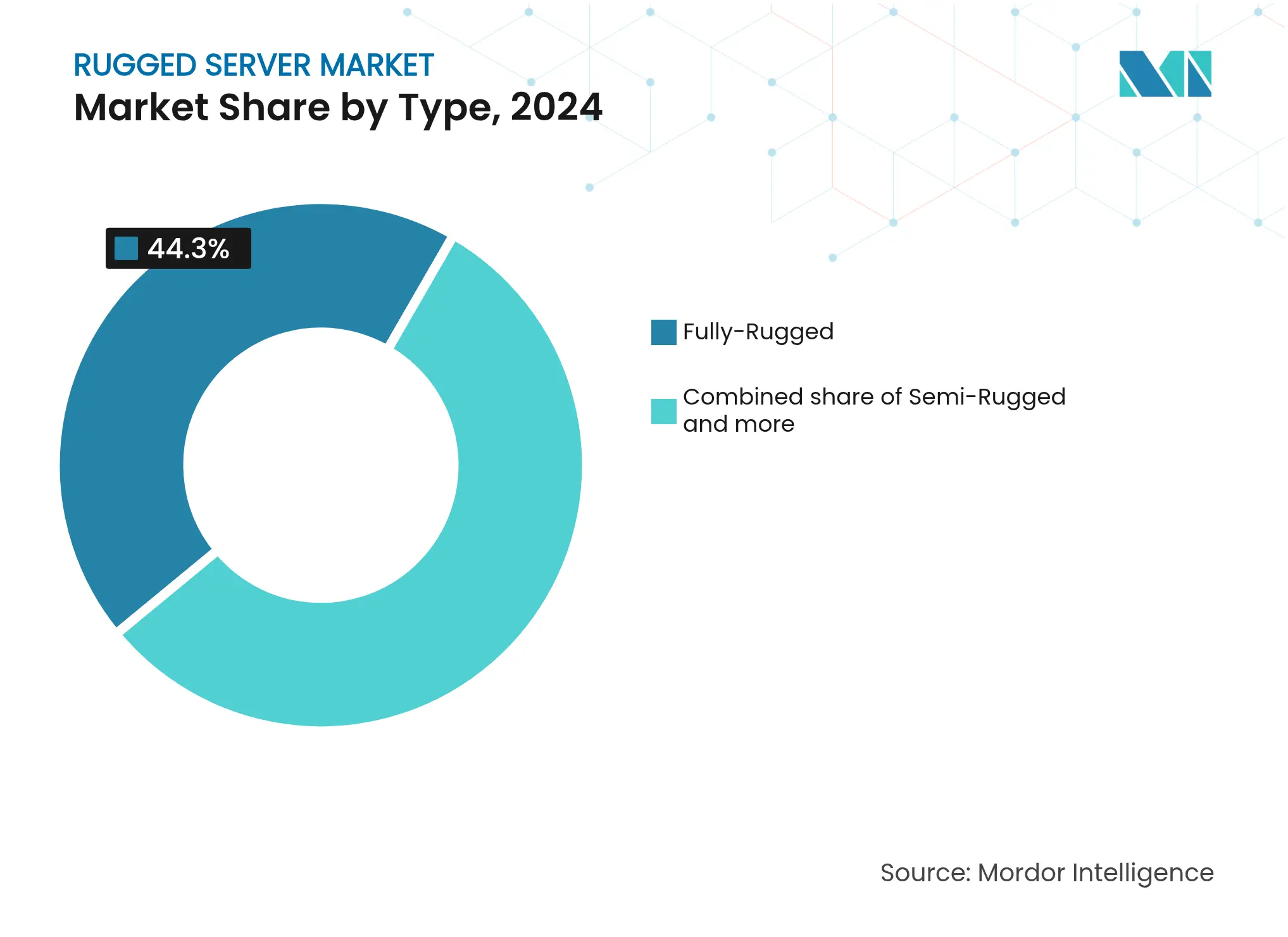

Ultra-rugged configurations post the fastest 7.3% CAGR through 2030 thanks to drone swarms, Arctic monitoring, and deep-sea stations. Crystal Group’s RE3423M, sealed to IP67 and shock-rated to 40 g, illustrates market appetite for hermetically sealed processing nodes that function without pressurization or HVAC. Fully-rugged units maintain leadership with a 44.3% share by balancing compute density with standard MIL-STD-810 certification. Semi-rugged fills transitional needs where airflow is available and budgets remain tight. The rugged server market continues to fragment into mission-specific SKUs rather than consolidated form factors.

By Enterprise Size: SMEs accelerate edge adoption

SMEs are set to grow at 7.9% CAGR as modular appliances allow point-solution rollouts. Advantech’s NVIDIA Jetson-powered MIC-770 V3 brings AI inference and fanless cooling into sub-USD 5,000 budgets, removing historical entry barriers[3]Advantech, “MIC-770 V3 Wins IoT Edge Computing Excellence Award,” advantech.com. Large enterprises hold 65.7% share on account of broad fleet deployments across factories, depots, and forward operating bases. They drive demand for centralized management frameworks that span both data-center and field assets, nudging rugged server vendors to support mainstream software stacks such as Red Hat and VMware.

By End-user: Aerospace sets the growth pace

Aerospace leads future expansion at 7.5% CAGR as aircraft migrate to distributed processing for fly-by-wire and sensor fusion. Mercury Systems’ SOSA-aligned ROCK3 shows 20× performance gains while meeting DO-178C safety rules, revealing the direction for cockpit and UAV payload servers. Military and defense still command a 30% share due to continual upgrade cycles, but now emphasize AI model hosting and cyber-resilience. Telecom and IT sectors adopt rugged gear for rural 5G edge nodes, while oil, gas, and mining continue to need explosion-proof enclosures.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Form Factor: Modular designs create flexibility

Modular/short-depth units achieve a 7.4% CAGR through 2030, driven by vehicle, shipboard, and roadside cabinet installations where space is limited. The ATMOS Server Stack integrates a 32-core Intel Xeon and NVIDIA L4 GPU in a 2U-sized sealed case, demonstrating high compute-per-litre density. Rack-mount servers remain dominant with a 48% share, favored for permanent command centers. Blade systems thrive where rapid swap-out is vital, and VPX standards dominate sensor pods requiring tight integration with RF front ends.

By Cooling Type: Passive systems gain reliability edge

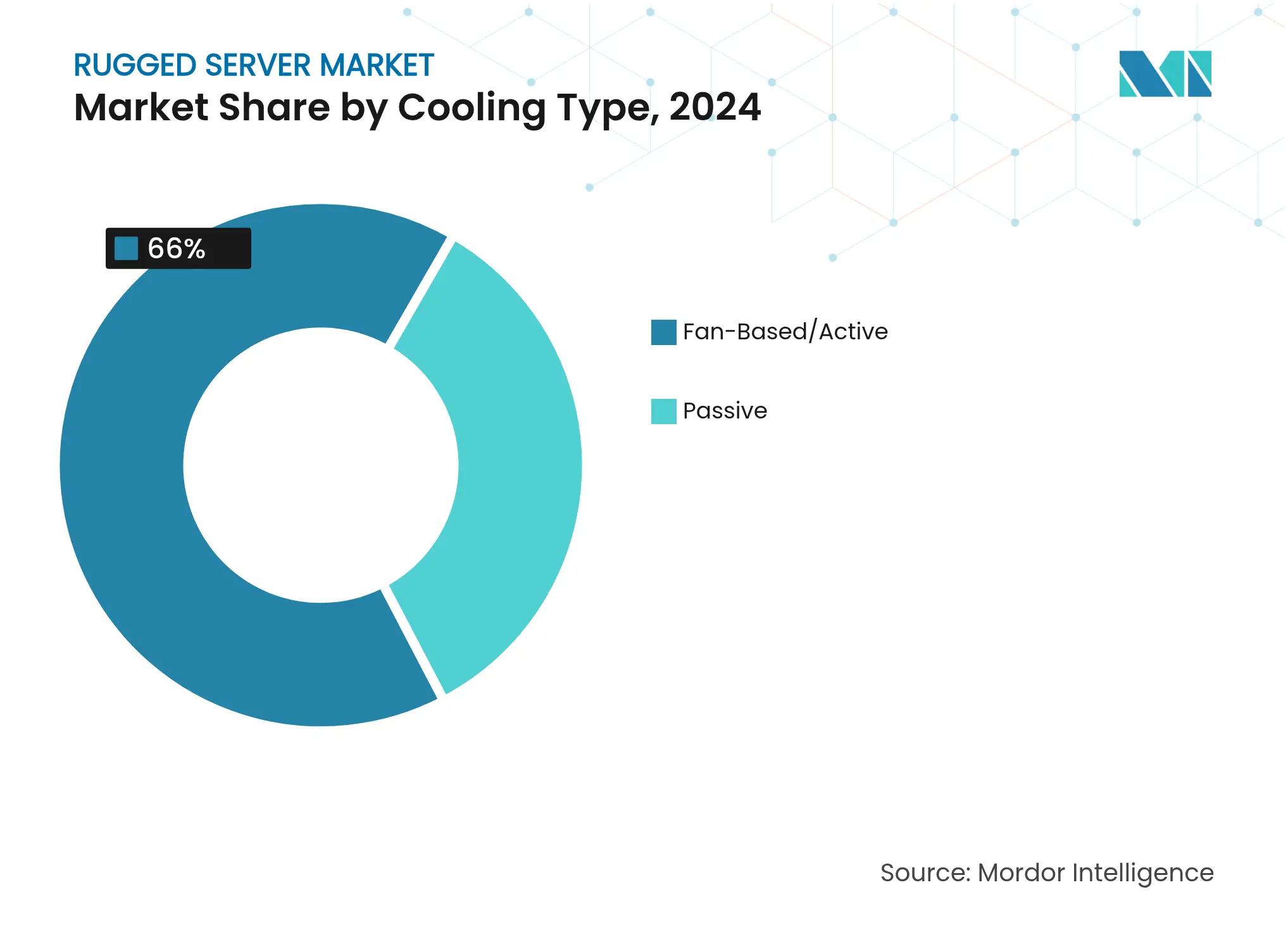

Passive cooling climbs at 7.5% CAGR on the promise of zero moving parts. Neousys’ fanless design sustains full CPU load at 70 °C ambient, proving feasibility for desert or engine-room placement[4]Neousys Technology, “Fanless Computer Withstands 70 °C Operation,” neousys-tech.com. Active fan solutions still control 66% share because AI accelerators and high-core CPUs generate heat that conduction plates alone cannot dissipate. Hybrid liquid loops appear in specialized builds, such as KAYTUS V3’s two-phase cold plates designed for edge AI clusters.

By Memory Capacity: More than 1 TB tiers support AI

High-capacity SKUs above 1 TB sprint at 8.3% CAGR as multi-sensor fusion and on-board model training underline the need for local data staging. Meanwhile, 256-512 GB keeps the largest 46% slice of the rugged server market size, covering most real-time control applications. Suppliers balance DIMM count against shock tolerance, driving innovation in board stiffeners and power conditioning.

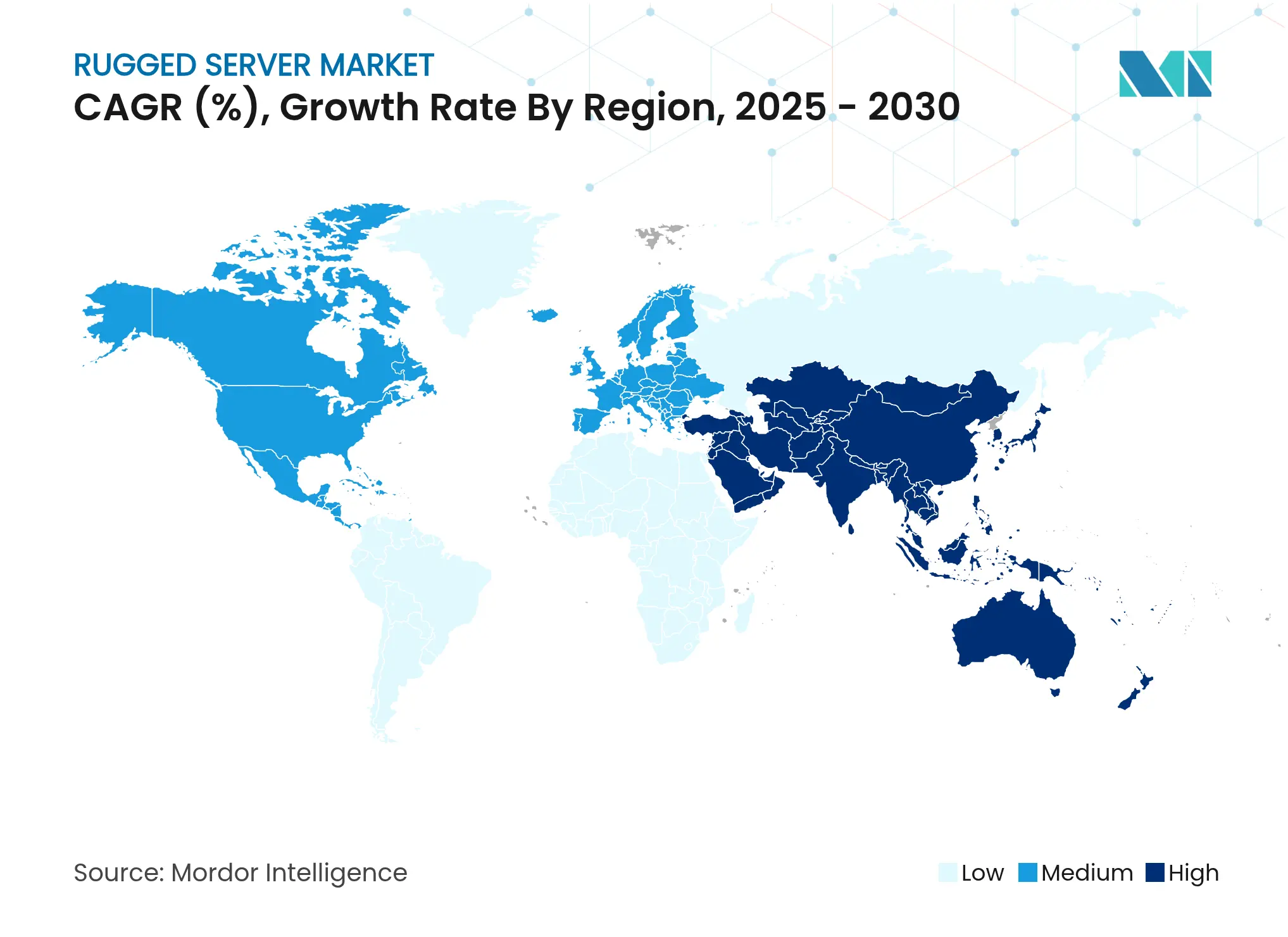

North America commands a 38% share, anchored by U.S. defense procurement and the presence of Dell Technologies, Mercury Systems, and Crystal Group. Federal investments in autonomous combat vehicles and secure communications channel substantial funding into rugged server platforms[5]U.S. Department of Defense, “Contracts For Dec. 1, 2024,” defense.gov. Industrial users, notably in aerospace manufacturing along the U.S. Sun Belt, expand the regional base.

Asia-Pacific registers the fastest 8.1% CAGR to 2030. China and India raise defense outlays for secure tactical networks, while electronics export hubs deploy rugged edge nodes to converge OT and IT. The evolving U.S.–South Korea tech pact highlights South Korean memory and foundry depth, reinforcing supply chains for rugged server components.

Europe maintains solid demand through the United Kingdom, Germany, and France as each pursues sovereign data infrastructure. Energy grids and rail operators adopt hardened compute for substation monitoring and wayside analytics. South America, led by Brazil, introduces rugged servers into homeland-security programs and Industry 4.0 lines in São Paulo state. The Middle East and Africa rely on ruggedized compute for oil-field telemetry and border surveillance, where temperature extremes test equipment limits.

Market Concentration

Market concentration is moderate. Diversified IT giants co-exist with niche specialists. Mercury Systems broadened its portfolio by acquiring Star Lab, embedding anti-tamper software into hardware to serve classified programs. Siemens fuses rugged IPCs with GPU acceleration, claiming 25-fold AI speed-ups that shorten quality-control cycles. Crystal Group and Trenton Systems exploit agility to deliver platform-specific chassis, especially for ultra-rugged or fanless builds. Acquisition pipelines focus on cybersecurity and AI middleware to extend beyond physical ruggedness toward secure, autonomous edge solutions.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the rugged server market as purpose-built rack, blade, modular, and embedded compute nodes that ship with reinforced chassis, conformal-coated boards, and MIL or IEC grade thermal, shock, vibration, and EMI certifications so the units maintain full performance in defense, aerospace, oilfield, and edge data center environments. According to Mordor Intelligence analysts, revenues track factory-gate sales of new ruggedized hardware and pre-installed firmware only, recorded in U.S. dollars.

Scope Exclusions: Consumer-grade hardened laptops, tablets, and general industrial PCs are not counted.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts completed interviews with hardware engineers at leading integrators, defense acquisition officers across North America and APAC, and IT architects running edge gateways in oil and gas and telecom towers. These conversations helped us verify real-world duty cycles, discount curves, and the speed at which newer XR-class servers replace legacy racks before we triangulated the final model.

Desk Research

We began by mapping published defense capital-outlay tables from the U.S. Department of Defense, NATO support agency procurement logs, and Indian MoD capital budgets, which reveal annual shipment pools for mission-critical compute. Trade association dashboards such as the RFID Journal's edge computing tracker, the International Energy Agency's remote asset database, and airline retrofit statistics from ICAO offered complementary demand signals.

Next, we layered technical literature from IEEE Xplore, ruggedization patent clusters extracted through Questel, and shipment line items parsed from Volza customs data to benchmark typical ASP bands and memory configurations. Company 10-Ks, investor decks, and press releases filled pricing and capacity gaps, while news sweeps from Dow Jones Factiva flagged material contract wins. This list is illustrative; many additional open and paid sources supported data collection and validation.

Market-Sizing and Forecasting

A top-down model reconstructs global demand by aligning rugged server penetration rates to installed platforms, defense vehicles, airborne ISR pods, offshore rigs, and micro data centers visible in the desk research streams. Select bottom-up checks, such as sampled supplier roll-ups and channel ASP times volume snapshots, fine-tune totals. Key variables include defense modernization outlays, aerospace fleet retrofit counts, active edge data center deployments, average rugged server ASP shifts, and memory density progression. We applied multivariate regression with scenario analysis to forecast 2026 to 2030, letting coefficient weights mirror consensus ranges gathered during primary research. Gaps in bottom-up samples are bridged by historical price-volume elasticity observed in earlier product cycles.

Data Validation and Update Cycle

Outputs pass a two-step analyst review where variance greater than three percent against external benchmarks triggers re-contact of sources. We refresh models annually, and interim updates occur when large procurement announcements or regulatory changes materially alter baseline assumptions. A final quality check is conducted before every client delivery.

Why Mordor's Rugged Server Baseline Earns Stakeholder Trust

Benchmark comparison

Published market values often diverge because firms frame scope differently, convert currencies on varied dates, or project unit prices without confirming field discounts. We openly state our inclusions, ground inputs in verifiable public data, and revisit price ladders each year, which is where Mordor Intelligence differentiates.

Key gap drivers versus other publishers are narrower hardware scope, aggressive or conservative ASP decay curves, and older refresh cadences that miss new defense edge compute rollouts.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 701.85 M | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 713.2 M | Regional Consultancy A | Counts rugged industrial PCs and applies single global ASP | ||

USD 643.8 M | Global Consultancy B | Uses 2023 currency baseline and excludes modular short-depth servers | ||

USD 652.0 M | Industry Association C | Relies on 2020 to 2021 shipment ratios with no recent defense orders |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.