Robotic Dentistry Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

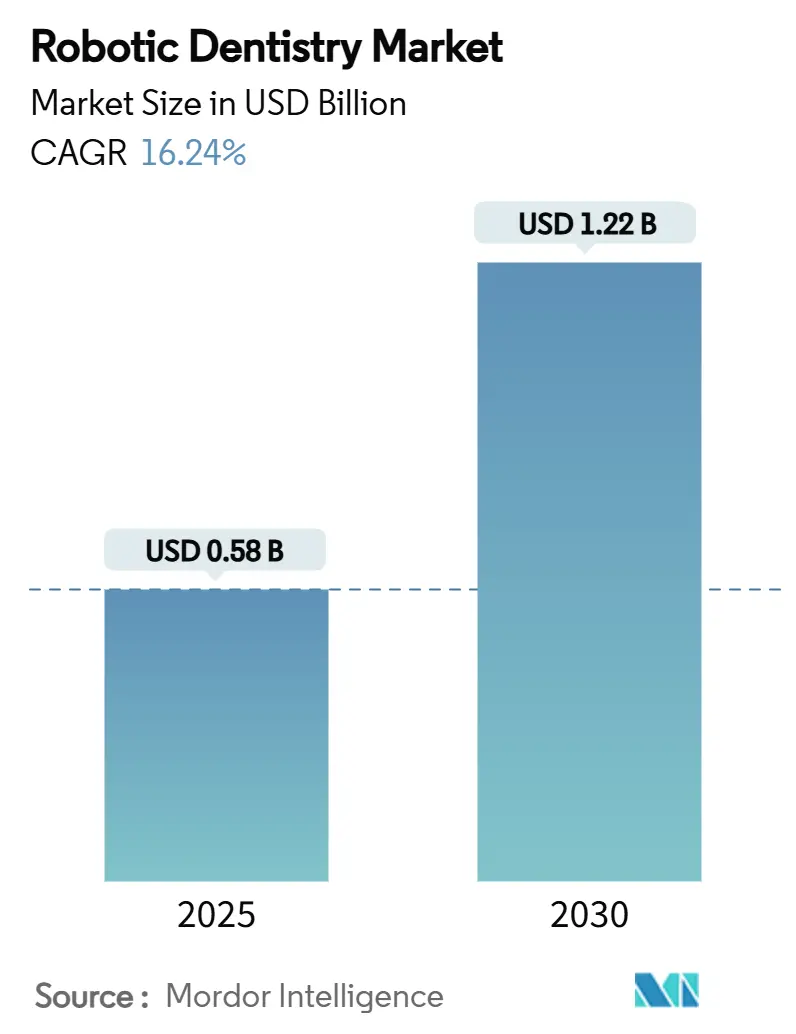

| Market Size (2025) | USD 0.58 Billion |

| Market Size (2030) | USD 1.22 Billion |

| Growth Rate (2025 - 2030) | 16.24% CAGR |

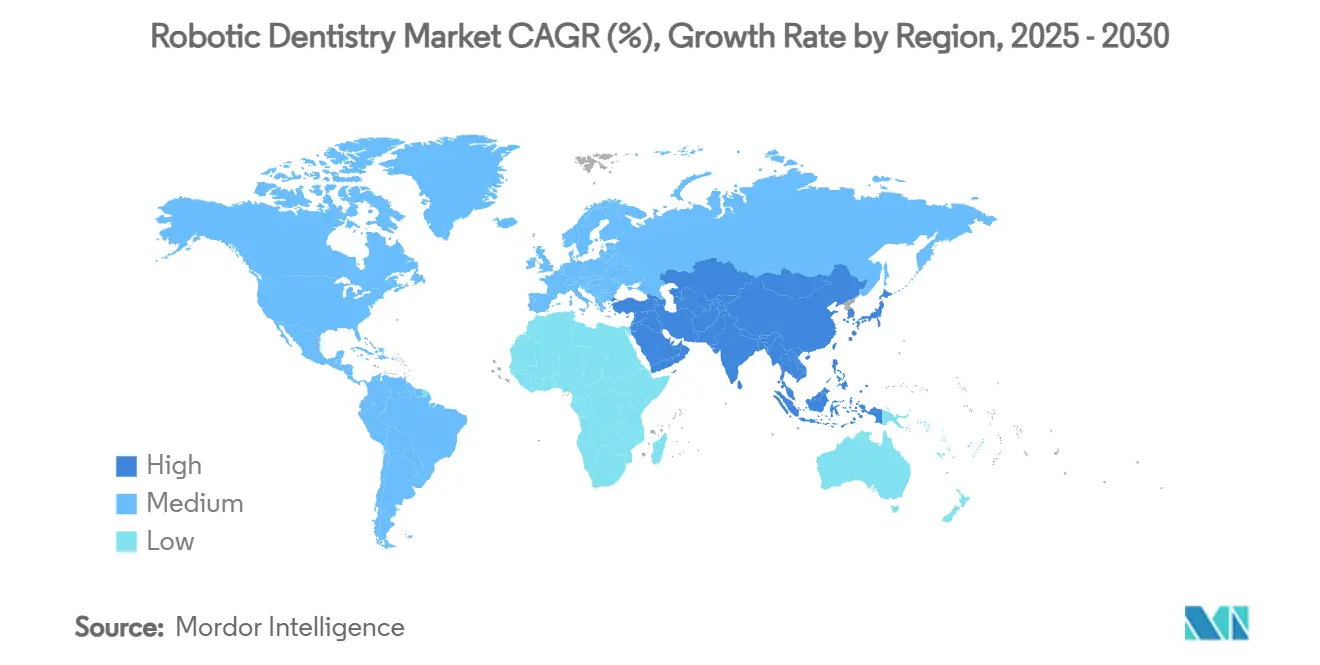

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Dentistry Market Analysis by Mordor Intelligence

The global robotic dentistry market size reached USD 576 million in 2025 and is forecast to advance to USD 1.22 billion by 2030, registering a 16.24% CAGR over the period. Strong momentum comes from precision-medicine expectations, aging populations that demand complex prosthetic care, and steady breakthroughs in autonomous surgical platforms. Digital workflow consolidation, reliable haptic feedback at sub-millimeter accuracy, and cloud-linked analytics are rapidly moving robot-assisted dentistry from early adoption toward routine practice. Capital is flowing from both strategic investors and dental service organizations, while regulators in North America and Asia-Pacific continue to clarify pathways for autonomous systems. Simultaneously, cybersecurity readiness and data-privacy compliance have become board-level priorities for manufacturers and large clinic groups as connected devices multiply.

Key Report Takeaways

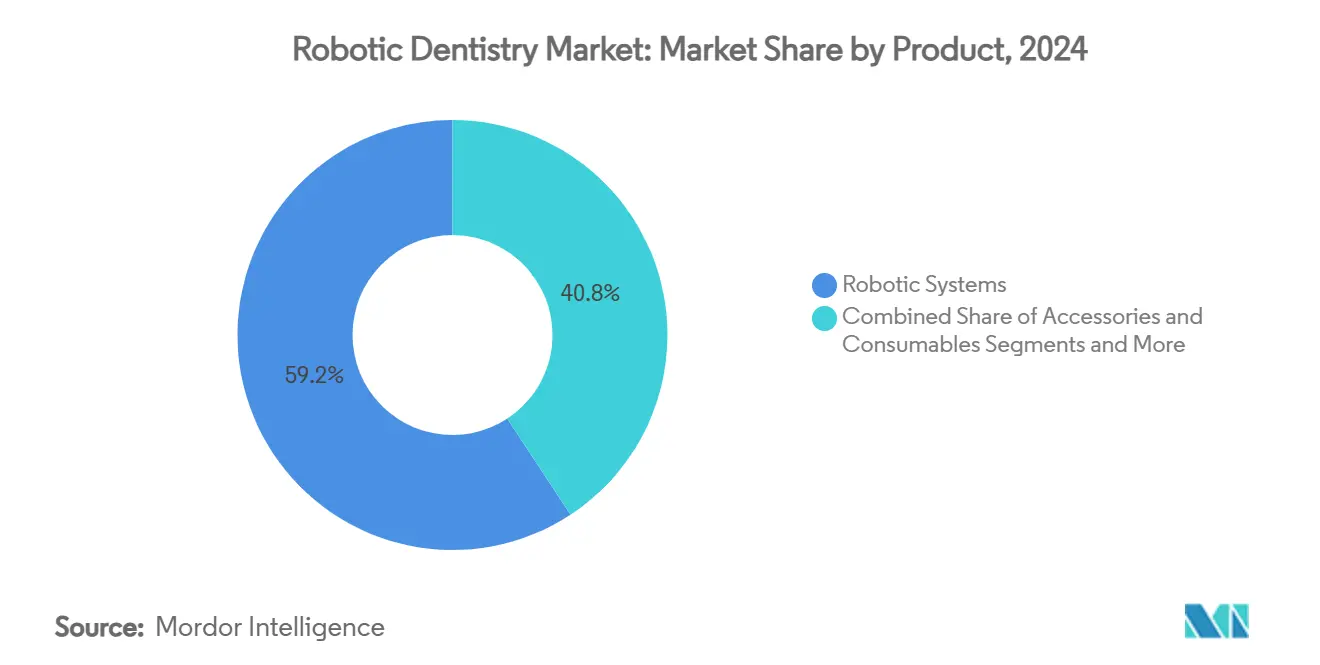

- By product, robotic systems held 59.24% of the robotic dentistry market share in 2024, whereas software and services are on track for a 20.43% CAGR through 2030.

- By technology, semi-autonomous navigation platforms led with 51.66% of the robotic dentistry market share in 2024; fully autonomous systems are projected to expand at 19.36% CAGR to 2030.

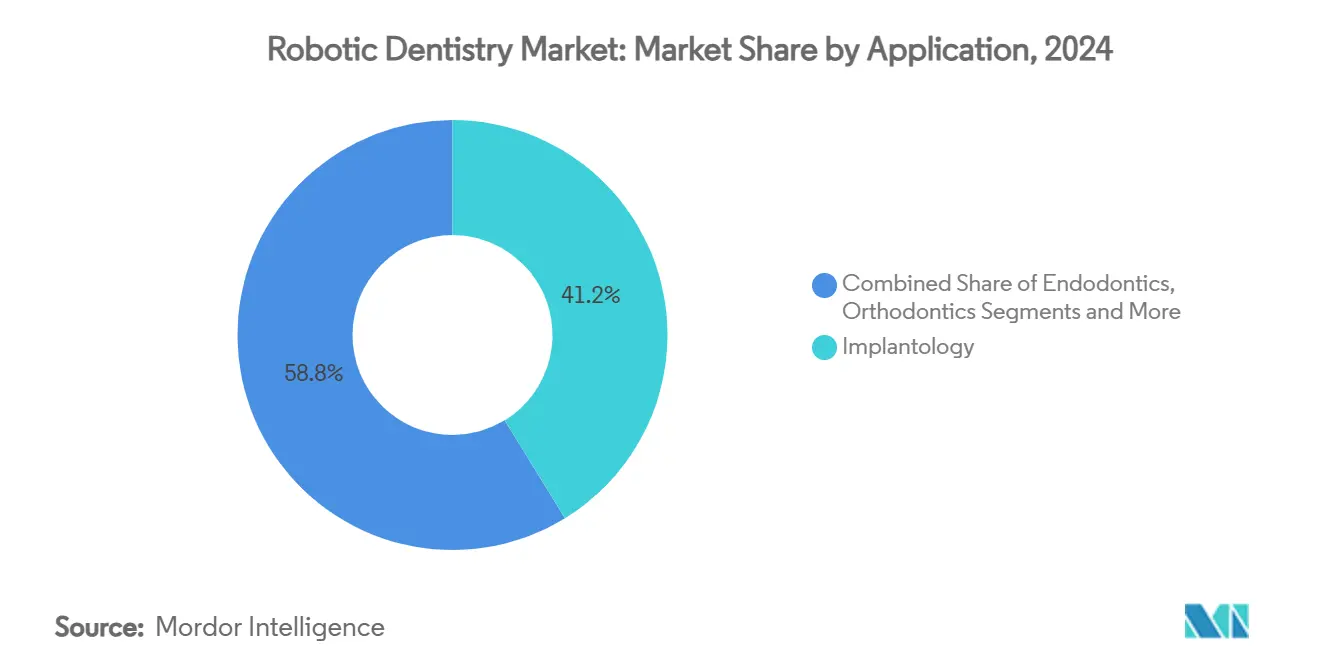

- By application, implantology accounted for 41.24% share of the robotic dentistry market size in 2024 and endodontics is advancing at a 19.25% CAGR through 2030.

- By end user, dental hospitals commanded 46.44% revenue share in 2024, while specialty clinics record the highest projected CAGR at 18.46% to 2030.

- By geography, North America controlled 39.45% of the robotic dentistry market in 2024; Asia-Pacific is forecast to post an 18.35% CAGR between 2025-2030.

Global Robotic Dentistry Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing accuracy needs in dental implantology | +3.2% | North America, Europe, expanding globally | Medium term (2-4 years) |

| Rising global geriatric & edentulous population | +2.8% | APAC and Europe accelerating, global reach | Long term (≥ 4 years) |

| Shorter chair-time and higher clinic throughput | +2.1% | North America, Europe, APAC | Short term (≤ 2 years) |

| Reimbursement expansion for robot-assisted oral surgery | +1.9% | North America, select European markets | Medium term (2-4 years) |

| Integration of haptic-feedback micro-robots | +1.7% | United States, Germany, Japan | Long term (≥ 4 years) |

| Dental group-practice cap-ex pooling models | +1.4% | North America, emerging in Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Accuracy Needs in Dental Implantology

Autonomous platforms now deliver angular deviations below 1.08 degrees, outperforming dynamic navigation systems by 53% and traditional freehand techniques by a wider margin. Sub-millimeter precision lowers the risk of nerve injury and sinus perforation during complex cases. Integration of optical coherence tomography lets surgeons adjust trajectories in real time, boosting implant survival rates while allowing novice clinicians to deliver expert-level placement outcomes.[1]Jianping Chen et al., “Comparison of the accuracy of a novel implant robot surgery and dynamic navigation system in dental implant surgery,” BMC Oral Health, bmcoralhealth.biomedcentral.com

Rising Global Geriatric & Edentulous Population

Longer life expectancy means more years living with prosthetic needs. Robotic flap-less approaches reduce surgical trauma, accelerate healing in patients with reduced bone density, and enable immediate loading for full-arch rehabilitation. Clinical investigations of zygomatic implant placement confirm comparable accuracy to conventional methods yet markedly shorter recovery windows, aligning with the mobility limits of older adults.[2]Changjian Li et al., “Autonomous robotic surgery for zygomatic implant placement,” International Journal of Implant Dentistry, journalimplantdent.springeropen.com

Shorter Chair-Time & Higher Clinic Throughput

Robotic guidance cuts appointment times for complex implant cases from roughly three hours to about ninety minutes in early adopter centers. The predictable workflow supports tighter scheduling, lifts daily patient capacity, and reduces operator fatigue. Practices report steadier cash flow as fewer follow-up appointments are required for adjustments, enhancing overall profitability.

Reimbursement Expansion for Robot-Assisted Oral Surgery

Insurers in the United States and select European markets have begun covering robot-supported implant protocols after clinical evidence demonstrated lower complication rates and fewer costly revisions. Recent classification rulings that recognize advanced dental technologies as medically necessary treatments are creating precedents for broader coverage of autonomous procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost & ROI uncertainty | -2.3% | Emerging markets most affected | Short term (≤ 2 years) |

| Limited trained oral surgeons for robotics | -1.8% | Global, acute in rural regions | Medium term (2-4 years) |

| Cyber-security & data-privacy hurdles | -1.2% | Strictest in EU, North America | Medium term (2-4 years) |

| Slow regulatory pathways for micro-robot approvals | -0.9% | Varies by jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & ROI Uncertainty

Purchase prices above USD 150,000 challenge solo practices in emerging economies. When factoring in annual service contracts, dedicated floor space, and staff certification, many dentists delay investment until patient volumes rise or group-practice financing becomes available.

Limited Trained Oral Surgeons for Robotics

University curricula are beginning to include hands-on robotic modules, yet supply of credentialed operators lags demand. Surgeons require several dozen cases before operative times normalize, creating short-term productivity dips. Industry-sponsored academies seek to shorten the curve but must scale rapidly to unlock broader adoption.[3]STRAUMANN GROUP, “Launches DANA, the Digital Academy North America,” straumann.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Systems Dominate Revenues While Software Accelerates Value Creation

Robotic systems captured 59.24% of the robotic dentistry market in 2024, reflecting the hardware foundation upon which practices build digital workflows. Accessories and consumables posted steady order growth as installed bases widened. Software and services, however, delivered a forecast-leading 20.43% CAGR. Subscription-based planning modules, AI-driven restorative design, and cloud analytics now generate recurring income that cushions manufacturers against cyclic capital spending. In 2024 software modules supporting automated crown design achieved 94% clinician acceptance, underscoring the stickiness of integrated digital ecosystems.

For clinics, platform-agnostic software shortens case planning time, aligns multi-disciplinary teams, and lessens reliance on specialized technicians. These operational gains reinforce system utilization, pushing the robotic dentistry market size for digital services.

By Technology: Semi-Autonomous Leadership Faces Rising Autonomous Adoption

Semi-autonomous navigation held 51.66% of the robotic dentistry market share in 2024 thanks to surgeon familiarity and regulatory comfort with supervised modes. Fully autonomous platforms should grow at 19.36% CAGR as algorithmic reliability and real-time imaging converge. Early human studies delivered implant placement success without manual intervention, signaling a tipping point once reimbursement and liability frameworks mature. Tele-operated systems remain niche yet invaluable for extending expert care into underserved regions via 5G connectivity.

Integration of force-feedback sensors and adaptive path planning is closing the gap between supervised and unsupervised modalities. As a result, the robotic dentistry industry expects the autonomous tier to approach one-third of total market value by decade’s end.

By Application: Implantology Maturity Spurs Endodontic Acceleration

Implantology retained 41.24% of the robotic dentistry market share in 2024 and is forecast to expand at 14.2% CAGR as surgeons rely on sub-millimeter placement accuracy to secure primary stability in challenging bone conditions. Robotic guidance minimizes crestal bone loss, supports flap-less protocols, and enables same-day full-arch loading, making the modality the reference standard for edentulous rehabilitation in high-volume centers.

Endodontics is the fastest-growing application, advancing at a 19.25% CAGR as micro-robotic navigation catheters let clinicians negotiate calcified canals that once required surgical retreatment. Early clinical pilots show 22% shorter procedure times and fewer perforations than traditional rotary instruments, translating into predictable outcomes even for general dentists with limited microsurgical training. Orthodontic, prosthodontic, and maxillofacial indications round out the portfolio; wire-bending robots, AI-driven crown design, and osteotomy assistants are gradually broadening the robotic dentistry market size beyond implant-centric workflows.

By End User: Hospitals Anchor Training While Clinics Propel Growth

Dental hospitals commanded 46.44% of 2024 revenues by combining operating-room infrastructure, residency programs, and bundled purchasing that eases capital outlays. Institutional settings also serve as validation sites where manufacturers gather post-market evidence for expanded indications, reinforcing confidence among regulators and insurers.

Specialty clinics are the momentum engine, projected to grow at 18.46% CAGR as group practices pool capital and rotate systems across multiple locations to maximize uptime. DSOs use standardized robotic protocols to shorten learning curves and deliver consistent patient experiences, a model that accelerates payback in markets with intense retail competition. Ambulatory surgery centers and academic institutes play supporting roles by offering overflow capacity, niche procedures, and translational research that feeds next-generation tool development, ensuring every end-user tier contributes to future adoption waves.

Geography Analysis

North America retained 39.45% share in 2024 on the strength of sophisticated insurance models, venture investment, and an active innovation pipeline. FDA predicable-change guidance that allows software-only upgrades without fresh submissions further accelerates iteration. Active system density now exceeds 1.7 units per 100 dentists in major metropolitan areas.

Europe follows with robust adoption in Germany, Switzerland, and the Nordic countries where structured reimbursement and high implant penetration intersect. Regulatory alignment under the Medical Device Regulation has slowed some launches, yet pan-EU cybersecurity standards position the region as a reference market for safe connected care.

Asia-Pacific is the headline growth story, forecast at 18.35% CAGR. China’s ongoing harmonization of implant material codes, Japan’s super-aged society with high edentulism rates, and South Korea’s digital-dentistry culture combine to create fertile ground. Leading suppliers have announced local manufacturing and training hubs to satisfy demand and meet domestic content rules.

Latin America and the Middle East & Africa remain emerging, yet urban private clinics in Brazil, Mexico, the United Arab Emirates, and Saudi Arabia are piloting robots to differentiate premium service lines. Targeted government incentives and public-private partnerships could accelerate penetration after 2027.

Competitive Landscape

The Robotic Dentistry sector is moderately concentrated. Established dental implant and imaging companies leverage distribution scale and installed digital ecosystems to bundle robots with scanners and CAD/CAM mills. Specialized robotics start-ups differentiate through proprietary kinematics, AI planning engines, and ultra-compact form factors.

Strategic collaborations dominate: implant manufacturers integrate navigation algorithms, while optics firms contribute real-time imaging modules. Recent FDA guidance that supports predetermined change-control plans lets leading vendors push software updates that expand indication sets without user downtime, shortening innovation cycles and sustaining brand loyalty.

Cyber-resilience has emerged as a battleground. Market leaders now publicize ISO/IEC 27001 certifications and bug-bounty programs, signaling maturity that reassures hospital IT departments. On the service side, predictive maintenance analytics tied to cloud telemetry minimize unplanned disruptions and strengthen annuity revenue.

Robotic Dentistry Industry Leaders

Neocis Inc.

X-Nav Technologies

Dentsply Sirona

Planmeca Oy

ZimVie Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Align Technology launched the Invisalign system with mandibular advancement blocks for Class II correction in the United States and Canada, extending clear-aligner indications.

- January 2025: Dental Innovation Alliance invested in Perceptive, a start-up that combines advanced imaging, AI, and robotics to expand access to precision dentistry.

- July 2024: Straumann Group completed capacity expansion in China to support rising demand for digitally integrated implant solutions.

- May 2024: Neocis secured USD 20 million to accelerate development of its Yomi robotic implant platform.

Global Robotic Dentistry Market Report Scope

| Robotic Systems |

| Accessories & Consumables |

| Software & Services |

| Autonomous Robotic Systems |

| Semi-Autonomous Navigation Robots |

| Tele-Operated / Telerobotic Systems |

| Implantology |

| Endodontics |

| Orthodontics |

| Prosthodontics |

| Oral & Maxillofacial Surgery |

| Others |

| Dental Hospitals |

| Specialty Dental Clinics |

| Ambulatory Surgery Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Robotic Systems | |

| Accessories & Consumables | ||

| Software & Services | ||

| By Technology | Autonomous Robotic Systems | |

| Semi-Autonomous Navigation Robots | ||

| Tele-Operated / Telerobotic Systems | ||

| By Application | Implantology | |

| Endodontics | ||

| Orthodontics | ||

| Prosthodontics | ||

| Oral & Maxillofacial Surgery | ||

| Others | ||

| By End User | Dental Hospitals | |

| Specialty Dental Clinics | ||

| Ambulatory Surgery Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the robotic dentistry market in 2025?

The robotic dentistry market size stands at USD 576 million in 2025.

What CAGR is forecast for robotic dental systems through 2030?

A 16.24% CAGR is projected from 2025 to 2030.

Which product segment is expanding fastest?

Software and services are forecast to grow at 20.43% CAGR, outpacing hardware sales.

Which region is expected to lead growth?

Asia-Pacific is projected to deliver the fastest expansion with an 18.35% CAGR through 2030.

What is the main restraint facing smaller clinics?

High upfront costs combined with uncertain return on investment continue to deter many small practices.

Page last updated on: