Upper Limb Prosthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

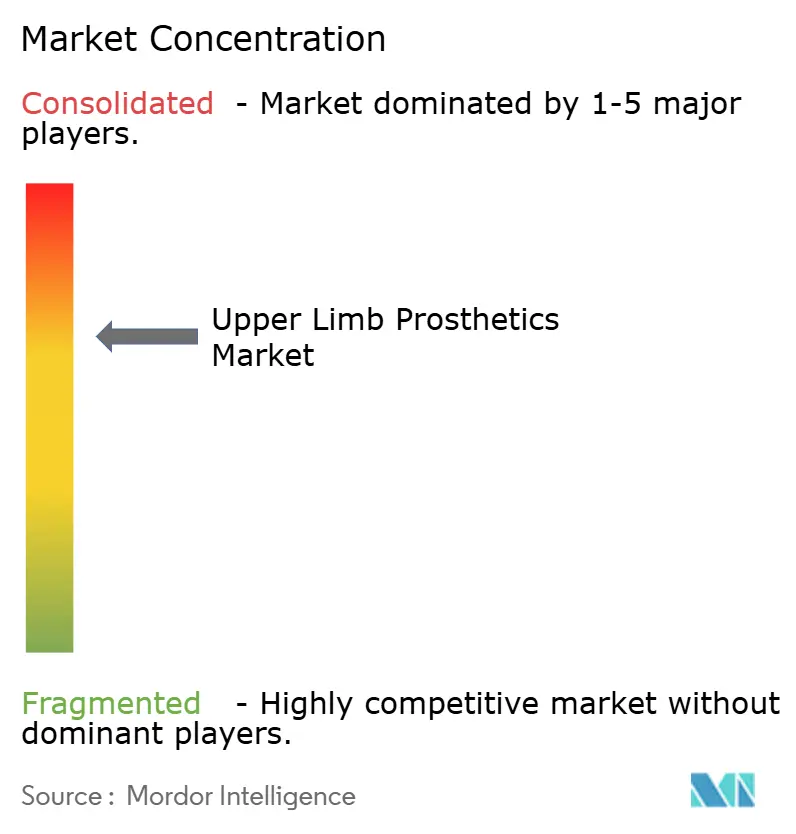

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Upper Limb Prosthetics Market Analysis by Mordor Intelligence

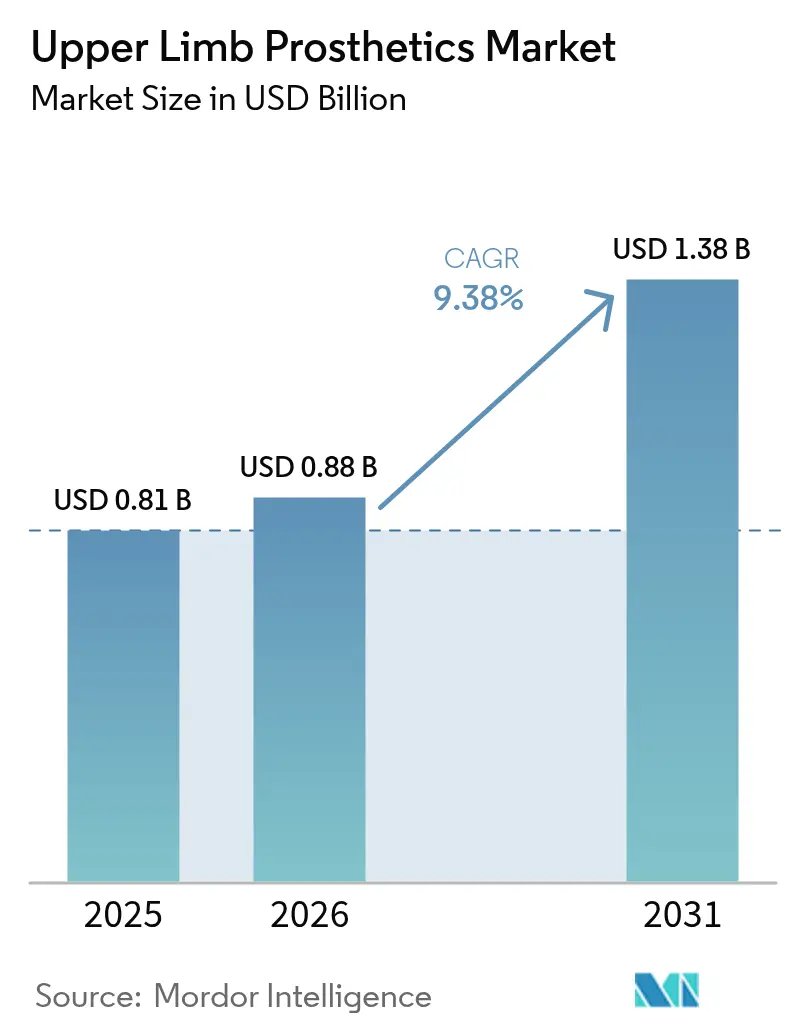

The Upper Limb Prosthetics Market size was valued at USD 0.81 billion in 2025 and is estimated to grow from USD 0.88 billion in 2026 to reach USD 1.38 billion by 2031, at a CAGR of 9.38% during the forecast period (2026-2031).

Reimbursement reform in the United States, Europe, and Japan is widening access to powered devices, while defence-funded research in osseointegration and neural interfaces is migrating into civilian clinics. Multi-articulated hands equipped with pattern-recognition control and vibrotactile feedback are replacing passive cosmetic limbs, reducing training time and improving task accuracy. Ageing populations in OECD countries continue to push vascular and diabetic amputation volumes upward, amplifying long-term demand. At the same time, additive manufacturing is compressing production lead times for paediatric bionic arms from eight weeks to ten days, bringing entry-level myoelectric solutions below the USD 10,000 price threshold.

Key Report Takeaways

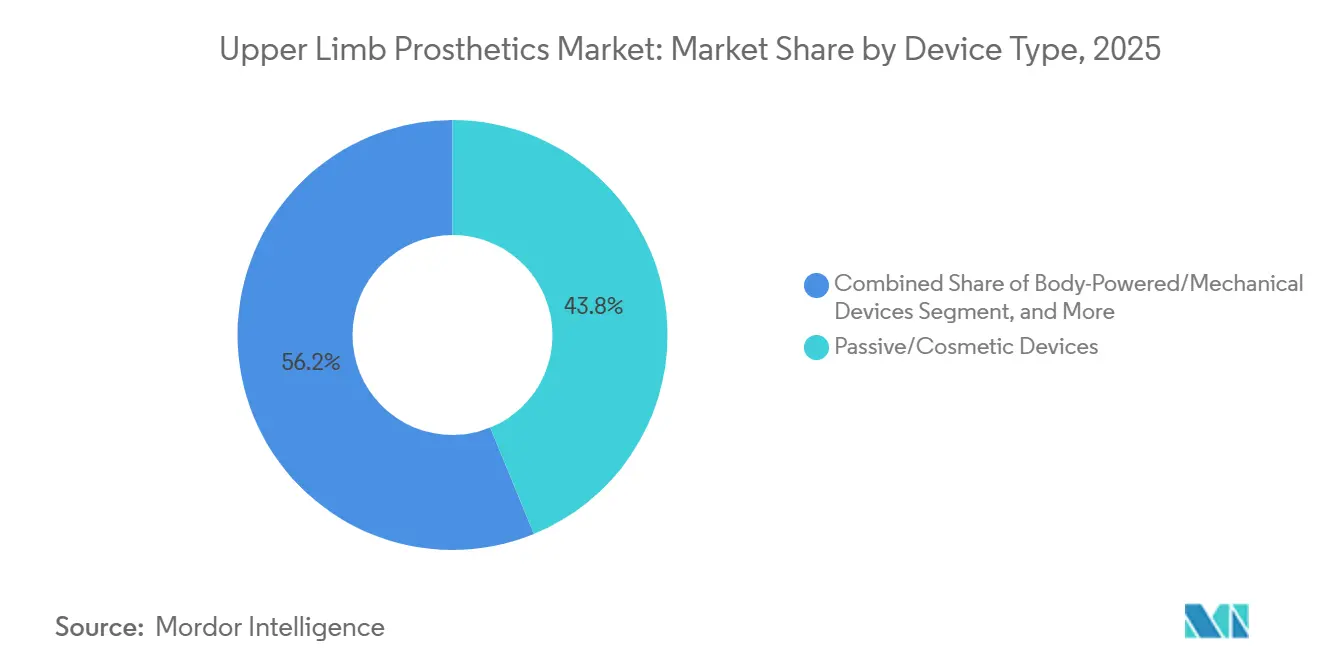

- By product type, passive and cosmetic devices accounted for 43.82% of the upper-limb prosthetics market share in 2025. Myoelectric and powered devices are projected to advance at a 10.06% CAGR between 2026 and 2031.

- By component, hand and other terminal devices accounted for 34.27% of the upper limb prosthetics market in 2025. Prosthetic elbows are set to register the fastest growth, expanding at an 11.63% CAGR through 2031.

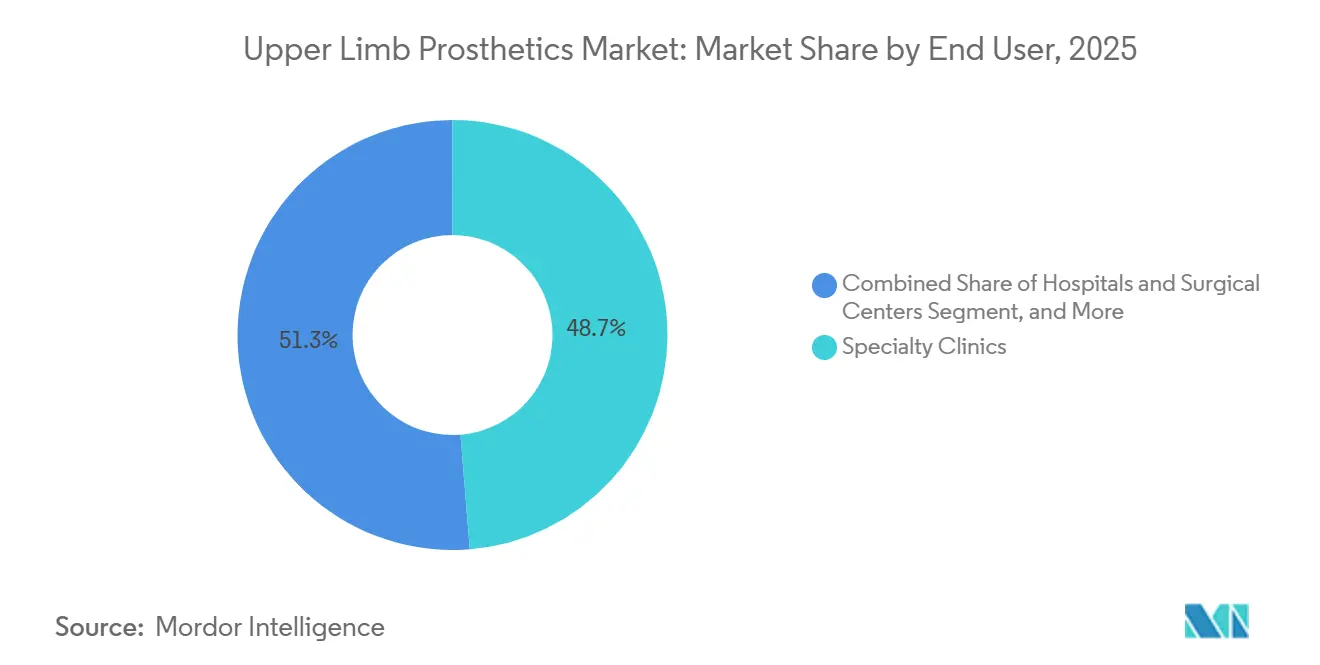

- By end user, specialty clinics accounted for 48.72% of end-user revenue in 2025. Rehabilitation centers are expected to grow at a 9.92% CAGR over 2026-2031.

- By geography, North America led with 43.18% of global revenue in 2025. Asia-Pacific is forecast to post the fastest regional expansion, rising at a 12.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Upper Limb Prosthetics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-population-driven vascular & diabetic amputations surge | +2.1% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Emergence of AI-based sensory feedback systems enhancing user acceptance | +1.8% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Rapid advances in myoelectric control algorithms & multi-articulated hands | +1.5% | Global, led by North America & Europe R&D hubs | Medium term (2-4 years) |

| Wider reimbursement expansion in veteran & worker-comp programs | +1.3% | North America, Europe, Australia | Short term (≤ 2 years) |

| 3D-printed, low-cost paediatric bionic arms addressing unmet needs | +0.9% | Global, with early adoption in UK, Middle East, Southeast Asia | Medium term (2-4 years) |

| Defence-funded osseointegration R&D crossing over to civilian clinics | +0.7% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing-Population-Driven Vascular & Diabetic Amputations Surge

The global population aged 65 and older reached 761 million in 2024 and continues to expand at 3.1% annually, pushing demand for upper-limb devices in regions where chronic disease intersects with advanced surgical capacity.[1]United Nations Department of Economic and Social Affairs, “World Population Ageing 2024,” UN.ORG Vascular complications from uncontrolled diabetes account for roughly 54% of non-traumatic upper-limb amputations across OECD economies, and diabetic patients face a 15-fold higher amputation risk than non-diabetic cohorts. Japan now reimburses myoelectric prostheses for individuals aged 70 or older, reflecting a policy shift that took effect in April 2025. A longer post-amputation life expectancy means patients routinely require multiple socket replacements, battery upgrades, and software updates over 15-20 years of device use. Consequently, the driver represents a structural, not cyclical, reallocation of healthcare budgets toward durable medical equipment that safeguards independence and lowers long-term care spending.

Emergence of AI-Based Sensory Feedback Systems Enhancing User Acceptance

High-density electromyography paired with machine-learning algorithms now enables prosthetic hands to recognize eight or more grip patterns from only two electrode sites, cutting cognitive load and shortening training periods from 18 weeks to four.[2]Coapt LLC, “Complete Control System Technical Documentation,” COAPTENGINEERING.COMSensory feedback delivered via vibrotactile actuators reduces object-drop rates by 41% during daily living tasks. Commercial roll-outs such as the TASKA Hand integrate fingertip force sensors that dynamically modulate motor torque, allowing delicate operations like food preparation without manual mode changes. By converting a traditionally open-loop device into a bidirectional human-machine interface, AI-enabled systems are accelerating user adoption and decreasing abandonment rates.

Rapid Advances in Myoelectric Control Algorithms & Multi-Articulated Hands

Commercial hands now deliver 14 selectable grip patterns with proportional speed control, while targeted muscle reinnervation surgery creates new EMG sites that support simultaneous shoulder, elbow, and hand movement. The LUKE Arm, cleared for expanded Medicare coverage in 2024, offers ten powered joints and foot-pedal adjuncts for bilateral amputees. Although lithium-polymer packs limit continuous use to 8-12 hours, next-generation solid-state batteries promise 30% higher energy density by 2028, extending charge cycles closer to full-day operation. Hardware miniaturization, surgical innovation, and algorithm refinement are jointly shrinking the performance gap between biological and prosthetic limbs.

Wider Reimbursement Expansion in Veteran & Worker-Comp Programs

The U.S. Department of Veterans Affairs removed prior authorization for myoelectric and osseointegrated systems in January 2025, cutting lead times by up to six months. TRICARE lifted its lifetime cap for upper-limb prosthetics to USD 125,000, while Medicare introduced HCPCS code L6026 with an allowable charge of USD 18,500 for pattern-recognition controllers.[3]Centers for Medicare & Medicaid Services, “HCPCS Code Updates and Prosthetic Coverage,” CMS.GOV Early provision of advanced devices has been shown to reduce long-term disability payments by 23% through faster return-to-work timelines. Similar expansions in California, Texas, and New York workers’ compensation schemes reinforce the view that high-function systems yield downstream economic benefits.

Restraints Impact Analysis of Upper Limb Prosthetics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & lifetime maintenance cost of powered prostheses | -1.4% | Global, acute in emerging markets and rural areas | Medium term (2-4 years) |

| Shortage of skilled prosthetists for complex upper-limb fittings | -0.9% | Global, severe in Asia-Pacific, Middle East, Africa | Long term (≥ 4 years) |

| Battery-life & durability gaps in multi-DOF devices | -0.7% | Global, impacting industrial and agricultural users | Short term (≤ 2 years) |

| Fragmented national regulatory pathways slowing cross-border launches | -0.6% | Global, particularly EU-Asia regulatory divergence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Lifetime Maintenance Cost of Powered Prostheses

Entry-level myoelectric hands start at USD 20,000, while multi-articulated systems with closed-loop feedback exceed USD 120,000, pricing out 68% of global amputees who live in low- or middle-income countries where annual per-capita health spending falls below USD 500. Ownership costs escalate with socket replacements every 3-5 years, battery swaps every two years, and software updates that command USD 500-1,000 annually. Even in the United States, average Medicare beneficiaries face USD 6,200 in out-of-pocket expenses for an advanced device despite coverage. Although modular 3D-printed designs reduce acquisition costs for paediatric users, progress remains incremental, constraining penetration in price-sensitive markets.

Shortage of Skilled Prosthetists for Complex Upper-Limb Fittings

Only 4,200 certified prosthetists practice in the United States, equating to one per 79,000 residents, and fewer than one-third are trained in advanced myoelectric fittings. Rural patients often travel 500 miles for device tuning, delaying functional rehabilitation by three to six months. Internationally, the gap widens: sub-Saharan Africa averages one prosthetist per two million people, and Southeast Asia reports one per 800,000 [WHO.INT]. Tele-fitting pilots show promise but face licensure barriers that limit interstate or cross-border practice. Until education pipelines and regulatory frameworks evolve, the clinician shortfall will continue to curb device adoption, especially for transhumoral and shoulder-disarticulation cases that demand high-skill installations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Upper Limb Prosthetics Market Segment Analysis

By Product Type:

Passive Devices Anchor Share, Powered Systems Drive GrowthPassive and cosmetic limbs dominated the upper-limb prosthetics market, accounting for 43.82% in 2025, supported by price points of USD 3,000-8,000 that meet the needs of appearance-focused users. Body-powered solutions held roughly 28% of unit volume, appealing to industrial laborers who value mechanical endurance in harsh settings. Powered myoelectric devices are projected to post a 10.06% CAGR over 2026-2031, fueled by reimbursement gains and AI-enabled control that lowers training barriers. Hybrid TMR-enabled systems remain niche but deliver simultaneous multi-joint control, redefining standard-of-care protocols in academic centers.

The bifurcated landscape sends high-volume, low-margin demand toward passive devices in emerging economies, while high-value growth concentrates in powered systems across insured markets. Paediatric programs increasingly adopt low-cost printed bionics until skeletal maturity, after which users upgrade to multi-articulated hands. Meanwhile, the durability of body-powered gear is securing a loyal base among agriculture and construction workers, even as sensor-equipped hands begin to encroach on that space.

By Component:

Terminal Devices Lead, Elbows AccelerateHand and other terminal units captured 34.27% of 2025 revenue, reflecting universal need across amputation levels and concentrated R&D in grip diversity and cosmetic realism. Elbow mechanisms, once limited to single-axis hinges, are forecast to climb at an 11.63% CAGR thanks to multi-DOF joints that enable overhead reach and reduced compensatory shoulder motion.

Investment is tilting toward elbows because functional outcomes for transhumeral amputees historically lag behind those of transradial cases. Devices such as the DynamicArm introduce proportional speed control and automatic damping that cut contralateral shoulder pain by one-third. Simultaneously, miniaturized gearboxes have shrunk wrist diameters to 50 mm, making powered rotation viable for small adults and older children. Realistic silicone covers for terminal devices continue to address psychosocial factors that influence overall device acceptance.

By End User:

Specialty Clinics Dominate, Rehabilitation Centers Gain GroundSpecialty clinics accounted for 48.72% of 2025 revenue, leveraging deep expertise in socket fabrication and EMG electrode placement to successfully fit complex cases. Rehabilitation centers are on track for a 9.92% CAGR as payers adopt bundled-care models that tie reimbursement to functional milestones rather than device delivery volume. Hospitals contribute about 28% of revenue, mostly in immediate post-amputation stabilization before referring patients to outpatient facilities.

The trend signals convergence: specialty clinics are embedding physical therapists, and rehabilitation centers are hiring prosthetists to deliver turnkey care models. Bundled payments encourage multidisciplinary coordination, rewarding providers who can demonstrate improved return-to-work rates and reduced secondary injuries. Over time, this integration is expected to shift share gradually toward comprehensive platforms capable of managing the entire patient journey.

Geography Analysis

North America Upper Limb Prosthetics Market

North America led the upper-limb prosthetics market, accounting for 43.18% of global revenue in 2025. Canada’s single-payer provinces reimburse myoelectric solutions for traumatic amputees but maintain stricter functional criteria for vascular cases, creating regional disparities. Mexico relies on small workshops producing passive limbs at USD 500-1,200, though a federal program launched in 2024 aims to open 12 myoelectric centers by 2028.

Europe Upper Limb Prosthetics Market

Germany, the United Kingdom, and France accounted for 68% of that figure, aided by statutory insurance that reimburses up to EUR 80,000 (USD 87,000) per device. The region’s transition to the Medical Device Regulation initially slowed launches but is now smoothing cross-border approvals, lowering compliance costs for multinationals.

APAC Upper Limb Prosthetics Market

Asia-Pacific is expected to deliver the fastest growth, expanding at a 12.71% CAGR through 2031. Japan’s super-aged society has prompted insurance to cover powered devices for seniors over 70. China’s local manufacturers are scaling up output with facilities capable of producing 8,000 units per year, targeting price points 40% below those of Western analogues. India faces affordability constraints, yet it distributed 1,200 printed limbs in 2025 under a national disabilities program. Australia’s NDIS funds up to AUD 150,000 (USD 98,000) per prosthesis, making the country a per-capita leader in powered adoption.

MEA and South America Upper Limb Prosthetics Market

Markets in the Middle East and Africa remain underpenetrated; GCC nations import high-end devices for their citizens, while migrant laborers rely on charity-funded prosthetics. South America is concentrated in Brazil and Argentina, where partial reimbursement leaves out-of-pocket gaps of USD 8,000-15,000 for powered systems, limiting uptake to higher-income groups.

Regulatory Landscape

Upper limb prostheses are regulated as medical devices, with the United States using the FDA framework in 21 CFR Parts 800-1299. Upper extremity prostheses fall under physical medicine devices, and higher-complexity powered systems are generally addressed under Class II pathways with special controls (for example, 21 CFR 890.3450). This affects documentation depth, testing, and post-market obligations for multi-articulated hands and advanced control modules.

For global commercialization, conformity to international standards supports cross-border launch readiness and interoperability, especially for mechanical safety and performance validation. Manufacturers commonly reference ISO standards for component description, classification, and mechanical testing (for example, ISO 16955 for upper-limb prosthesis mechanical testing), which supports repeatable verification as pattern-recognition control, sensory feedback, and novel interface technologies enter routine production.

Competitive Landscape

The upper-limb prosthetics industry is characterized by moderate concentration. Incumbents leverage vertical integration and deep payer relationships, while newcomers such as Open Bionics, COVVI, and TASKA differentiate through modular 3D-printed designs that drop paediatric device costs below USD 10,000.

Technology forms the chief battleground. USPTO filings for 2024-2025 include 47 patents on osseointegrated electrode arrays and 62 on vibrotactile feedback, underscoring industry-wide migration toward closed-loop control. AI-driven algorithms like Coapt’s Complete Control raise task-completion accuracy to 92% within four weeks of training, a leap that shortens rehabilitation cycles. Direct-to-consumer subscription models are emerging: Open Bionics offers USD 150 monthly service that covers socket changes and software updates, unbundling acquisition from lifetime upkeep.

Private equity is consolidating specialty clinics to build national networks capable of negotiating volume rebates and winning bundled-care contracts. Hanger Clinic’s 2025 acquisition of 14 practices raised its footprint to 850 U.S. locations, positioning it for multi-year Veterans Affairs tenders. Automotive and electronics suppliers are eyeing entry via partnerships, drawn by the cross-applicability of their battery and sensor expertise. As cost discipline improves, margins on entry-level powered systems are likely to compress, intensifying competition.

Upper Limb Prosthetics Industry Leaders

Össur

Fillauer LLC.

Steeper Inc.

Ottobock SE & Co. KgaA

Ortho Europe

- *Disclaimer: Major Players sorted in no particular order

Upper Limb Prosthetics Market Companies Covered in this Report

- Arm Dynamics

- Blatchford

- BrainRobotics

- College Park Industries

- Coapt

- COVVI Ltd

- DEKA Integrated Solutions

- Fillauer

- Hanger Clinic

- Mobius Bionics LLC

- Motorica LLC

- Naked Prosthetics

- Ortho Europe

- Ottobock

- Ossur

- Protunix

- Proteor SAS

- RSLSteeper

- Steeper

- TASKA Prosthetics

Market Opportunities and Future Outlook

A whitespace is emerging at the intersection of powered upper-limb prosthetics and neuromuscular interface control. Device makers are moving beyond incremental grip and battery upgrades toward tighter human-machine integration, with February 2026 providing a direct signal. Ottobock partnered with Blue Arbor Technologies and made a USD 5 million investment to advance the RESTORE Neuromuscular Interface System, which holds an FDA Breakthrough Device designation and participates in the TAP Pilot, indicating an active pipeline for next-generation control that can be integrated into clinical fitting workflows.

Beyond interfaces, providers and service delivery capacity are becoming a practical commercial lever. Manufacturers are expanding patient care footprints to improve access, follow-up tuning, and payer engagement across fragmented markets. Ottobock also expanded its patient care network through the May 2026 acquisition of the patient care business of Blatchford Ltd. in Norway, adding a regional platform that can support advanced fittings and ongoing device management. In parallel, additive manufacturing and digitized production workflows support faster customization for pediatric and specialty segments, aligning with the shift toward software-upgradable devices and clinic-efficient fitting models.

Recent Industry Developments in Upper Limb Prosthetics Market

- June 2026: Össur Europe B.V. finalized investment in warehouse automation with Element Logic to implement AutoStore at Eindhoven site (go-live planned October 2026). The company is expanding logistics automation for upper-limb prosthetics distribution and increasing regional fulfillment capacity.

- June 2026: Fillauer Europe became primary distributor of the Zeus Hand by Aether Biomedical across the Nordic region. This move broadens access to high performance devices and expands distribution coverage in Europe.

- February 2026: Blue Arbor Technologies announced strategic partnership with Ottobock with a $5 million investment to advance the RESTORE neuromuscular interface system. The partnership accelerates development and supports potential commercialization of neuromuscular control in upper limb prosthetics.

Upper Limb Prosthetics Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers prosthetic devices and key components used to replace function and form in the upper limb, from shoulder and upper arm through elbow, forearm, wrist, and hand. Revenue is counted for products sold for primary fitting and for replacements driven by wear, upgrades, and clinical follow-up.

Scope exclusions: We exclude lower-limb prosthetics, general orthotics, and stand-alone rehabilitation services that are not billed as part of the prosthetic device supply.

Segments Covered in This Report

- By Product Type

- Passive / Cosmetic Devices

- Body-Powered / Mechanical Devices

- Myoelectric / Powered Devices

- Hybrid & TMR-Enabled Devices

- By Component

- Prosthetic Hand / Terminal Device

- Prosthetic Wrist

- Prosthetic Elbow

- Prosthetic Shoulder & Upper Arm

- By End User

- Specialty Clinics

- Hospitals & Surgical Centers

- Rehabilitation Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with clarifying the treated demand pool and the care pathway, so we can separate clinical need from actual device purchasing. We lean on public health and population context from sources such as the World Health Organization, the US CDC, the National Center for Health Statistics, and national health ministries, and then map reimbursement and coding signals using public payer schedules where available.

On the supply side, we review device approvals and safety updates from regulators such as the US FDA and the European Commission medical device framework, and we use peer-reviewed clinical literature to understand adoption of myoelectric and hybrid solutions and typical replacement cycles. Company annual reports, investor decks, and reputable press are used to align product mix, regional exposure, and pricing direction, with selective checks from paid subscriptions focused on company financials, patent databases, and shipment-level trade statistics where relevant. These examples are not exhaustive, and many other public sources were also used for data collection, validation, and clarifying assumptions.

Primary Interviews and Surveys

Primary work was used to test what is actually being purchased and fitted, and to stress-check pricing and mix assumptions that do not show up cleanly in public data. We spoke with prosthetic clinic decision makers, rehabilitation professionals, component distributors, and product specialists across major regions so the model reflects differences in reimbursement, patient access, and technology adoption.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | APAC: 45% |

| Mid tier: 57% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 16% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

We built the market using a top-down pathway that reconstructs demand from the amputee and limb-difference pool, the share that is clinically eligible, and the share that is actually fitted through prosthetic clinics and hospitals, which is then translated into value using region-specific average selling prices. To keep results grounded, we also ran selective bottom-up checks using sampled price lists, typical component bundles (hand, wrist, elbow, and related hardware), and channel feedback on annual fitting volumes, and then adjusted totals where the two views did not reconcile.

Key inputs included procedure and trauma signals that drive new fittings, replacement timing by device type, the mix shift between body-powered and myoelectric solutions, reimbursement friendliness by country, and observed pricing direction for advanced terminal devices. Forecasts were developed using scenario analysis around technology uptake and access to care, and the forward variables were reviewed with interviewees so adoption and replacement assumptions stayed realistic. When country-level detail was thin, we used proxy ratios from similar reimbursement systems and then tightened the estimate through regional expert re-contacts.

Data Validation & Update Cycle

Validation is done through stepwise checks so the final totals align with independent signals like regional share patterns, pricing bands by technology level, and the implied number of annual fittings. Outliers are flagged and reviewed, and when a variance cannot be explained by a clear scope or pricing reason, we re-check inputs and reconnect with sources before internal sign-off.

Reports are refreshed annually, with interim updates when major events could change pricing, reimbursement access, or supply availability. Before delivery, an analyst performs a last review pass so the numbers and assumptions reflect the latest public releases and confirmed market feedback.

Mordor Intelligence's Upper Limb Prosthetics Market Sizing Compared With Other Published Estimates

Published market sizes for upper limb prosthetics can vary widely, even when the topic sounds the same at first glance. The gaps usually come from what is counted as an upper-limb solution, how component bundles are treated, and whether the sizing logic follows patient fittings versus manufacturer shipment views.

The table also shows that some sources report a much larger 2024 to 2026 value band, and in Mordor Intelligence's model, only upper-limb prosthetic devices and core components (from shoulder and upper arm through elbow, wrist, and hand) are counted, instead of folding in broader limb prosthesis categories or adjacent assistive devices. Differences can also be driven by whether average selling prices are assumed to rise quickly with high-end myoelectric adoption, how replacement cycles are timed, and whether currency conversion uses a single-year rate or a multi-year average.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.88 B (2026) | |

| Global Consultancy A | USD 1.00 B (2026) | Uses a broader device basket where more add-ons and service-linked charges can be captured in the value line, and pricing is often applied as a higher blended ASP across technology tiers. |

| Industry Publisher B | USD 1.50 B (2024) | Anchors the series on a 2024 manufacturer and trade view with different currency timing, and the scope can include wider prosthesis categories beyond strictly upper-limb components, which inflates the headline total. |

Looking across the three figures, the spread is mainly explained by scope boundaries, pricing build-up choices, and the year used for the headline number. Our approach stays traceable to clear demand drivers like fittings, replacements, and realistic price bands by technology level, which makes the final market size easier to interpret and replicate.

Key Questions Answered in the Report

How large will the upper limb prosthetics market be by 2031?

It is projected to reach USD 1.38 billion by 2031, reflecting a 9.38% CAGR over 2026-2031.

Which device type is expanding fastest?

Powered myoelectric systems are forecast to grow at 10.06% CAGR, the highest among all product types.

What region shows the strongest growth outlook?

Asia-Pacific is expected to post the quickest expansion at a 12.71% CAGR through 2031.

Which component segment is gaining traction most rapidly?

Prosthetic elbows, driven by multi-DOF mechanisms, are projected to advance at an 11.63% CAGR.

Why are specialty clinics so dominant in device fittings?

They hold 48.72% of 2025 revenue due to their specialized expertise in socket design and EMG calibration, which are essential for advanced myoelectric fittings.

Page last updated on: