Neuroprosthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

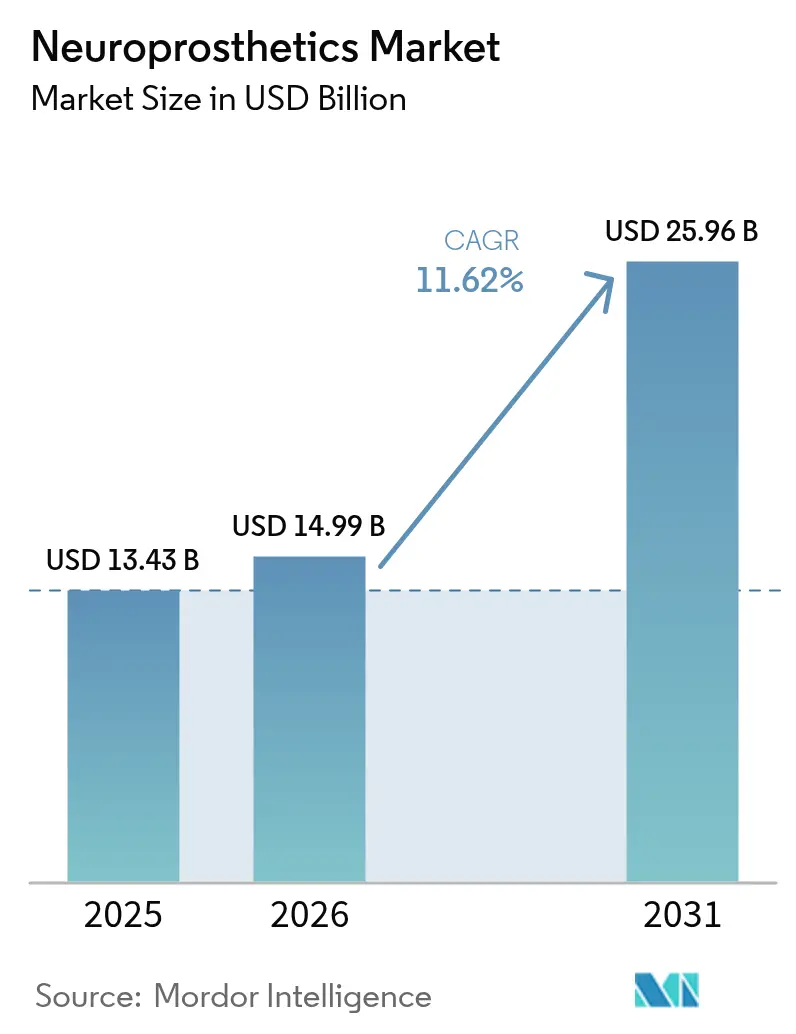

| Market Size (2026) | USD 14.99 Billion |

| Market Size (2031) | USD 25.96 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

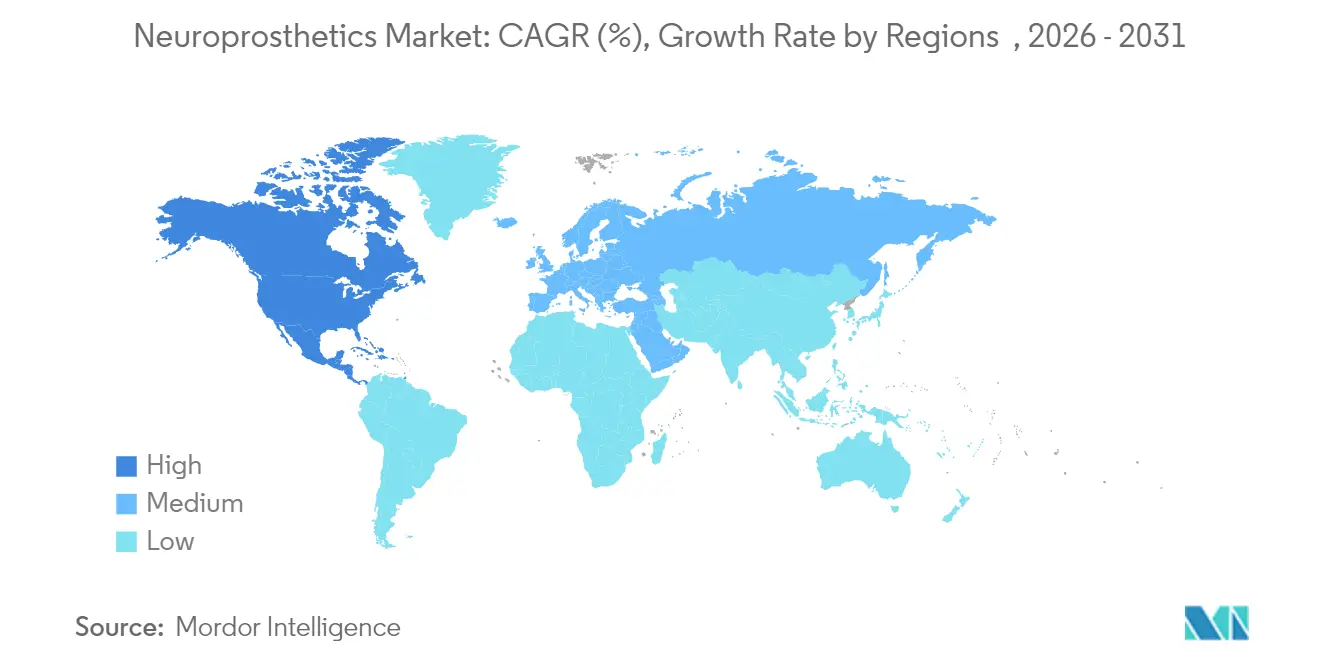

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Neuroprosthetics Market Analysis by Mordor Intelligence

Neuroprosthetics market size in 2026 is estimated at USD 14.99 billion, growing from 2025 value of USD 13.43 billion with 2031 projections showing USD 25.96 billion, growing at 11.62% CAGR over 2026-2031. This swift expansion mirrors the transition from open-loop stimulation systems to closed-loop adaptive platforms that fine-tune therapy in real time. Miniaturized electronics, flexible biomaterials, and on-device artificial-intelligence algorithms now merge to deliver durable implants that outlast earlier generations while lowering surgical revision rates. Heightened FDA Breakthrough Device designations since 2024, broader Medicare coverage for neuromodulation procedures, and growing clinical evidence across motor, sensory, and psychiatric indications further unlock adoption. Venture capital inflows, averaging USD 1.4 billion per year since 2023, continue to fund novel brain-computer interfaces that target unmet needs in paralysis and severe depression, strengthening long-term demand across the Neuroprosthetics market.

Key Report Takeaways

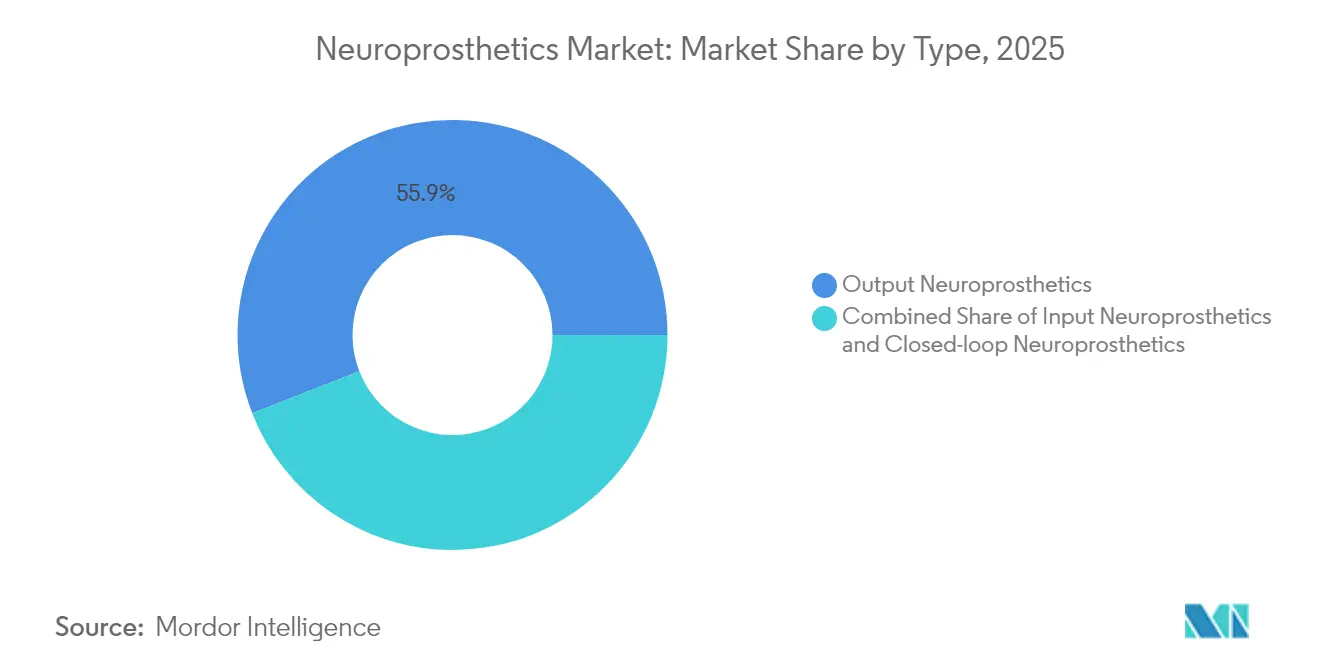

- By type, output neuroprosthetics held 55.92% of the Neuroprosthetics market share in 2025, while closed-loop adaptive systems are advancing at a 11.94% CAGR through 2031.

- By component, implantable devices accounted for 62.98% share of the Neuroprosthetics market size in 2025; software algorithms are forecast to expand at 12.33% CAGR to 2031.

- By technique, deep brain stimulation led with 36.42% of the Neuroprosthetics market size in 2025, yet cortical and peripheral nerve stimulation are climbing at 12.75% CAGR between 2026-2031.

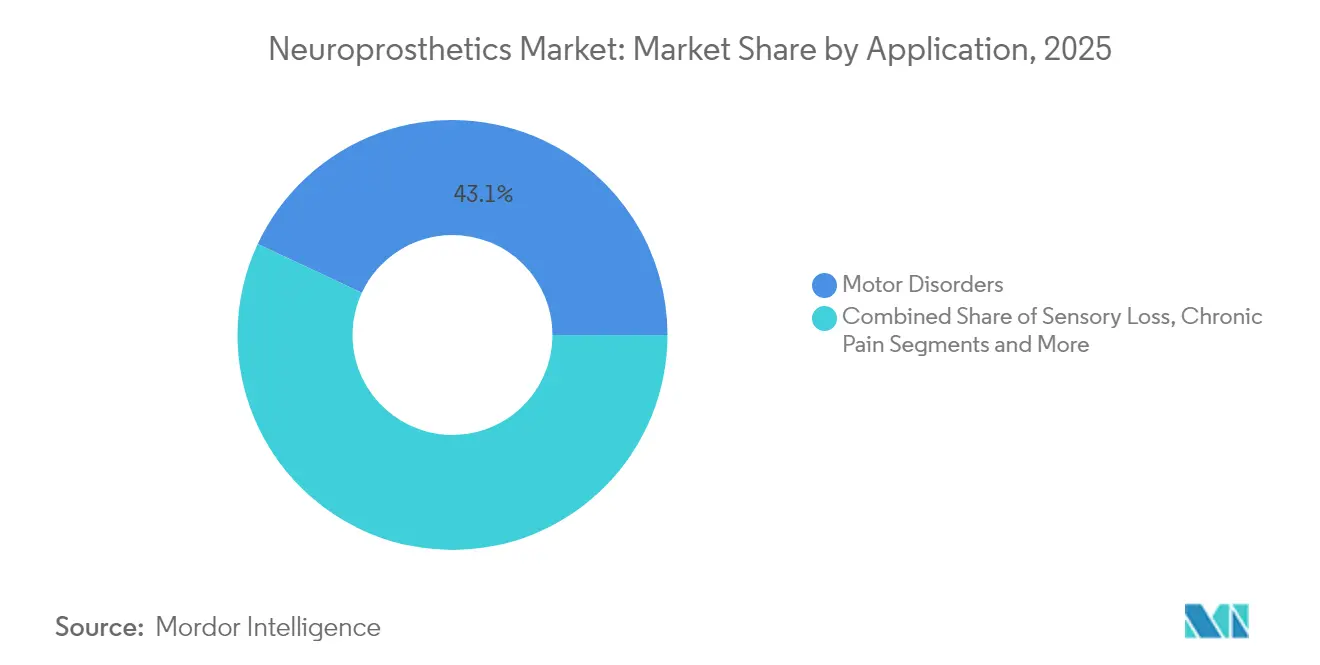

- By application, motor-disorder treatments captured 43.05% of the Neuroprosthetics market share in 2025, whereas cognitive and psychiatric uses are set to grow at 12.78% CAGR to 2031.

- By end user, hospitals managed 59.87% of the Neuroprosthetics market size in 2025, but home-care and ambulatory settings show the fastest momentum at 12.84% CAGR through 2031.

- Regionally, North America commanded 42.91% revenue in 2025; Asia-Pacific is the fastest-growing geography at 13.16% CAGR for the Neuroprosthetics market to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Neuroprosthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neurological disorders | +2.1% | Global, with concentration in aging populations of North America & Europe | Long term (≥ 4 years) |

| Escalating incidence of sensorineural hearing loss | +1.8% | Global, particularly developing markets in APAC | Medium term (2-4 years) |

| Technological miniaturisation & biomaterial advances | +2.3% | North America & EU leading innovation, APAC manufacturing scale | Medium term (2-4 years) |

| Expanding reimbursement for neuromodulation implants | +1.9% | North America primary, EU secondary adoption | Short term (≤ 2 years) |

| Bio-hybrid neural interfaces entering clinical pipelines | +1.4% | North America & EU research hubs | Long term (≥ 4 years) |

| Military & space-agency funding for human-machine augmentation | +1.2% | North America, with emerging programs in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neurological Disorders

Stroke and Parkinson’s incidence continues to rise among populations over 65, prompting sustained demand for multimodal neuroprosthetic therapies [1]Zhiyong Li, “Global Neurological Disorders Burden 2024,” World Health Organization, who.int. Age-linked stroke and Parkinson’s disease trends raise annual caseloads and prompt sustained demand for multi-modal neuroprosthetic therapies that address motor, cognitive, and sensory deficits concurrently. Six-year follow-up data on responsive neurostimulation show an 82% median seizure cut in treatment-resistant epilepsy, underscoring chronic efficacy. Health-economic models demonstrate that device longevity beyond eight years offsets higher up-front expenses, positioning neuroprosthetics as first-line rather than last-resort options across the Neuroprosthetics market.

Escalating Incidence of Sensorineural Hearing Loss

Urban noise exposure and industrialization accelerate cochlear-implant uptake, while next-generation bilateral electrode arrays equipped with graphene conductors preserve residual hearing and improve spatial sound perception [2]Mingxia Chen, “Kirigami-Pattern Electrodes Enable 3D Neural Recordings,” Frontiers in Neuroscience, frontiersin.org. Pediatric early-implant programs lengthen individual device-upgrade cycles, expanding the lifetime value pool within the Neuroprosthetics market. Smartphone-linked sound-processing software now personalizes acoustic profiles, differentiating premium cochlear systems.

Technological Miniaturization and Biomaterial Advances

Kirigami-pattern electrodes and ultra-thin graphene layers permit 3D neural signal capture with minimal tissue trauma. Wireless power modules extend functional lifespans past 15 years, cutting battery-replacement surgeries. Neuromorphic chips running on microwatts allow continuous on-board analytics without thermal damage, delivering precision stimulation and data-rich insights that enhance clinician decision making across the Neuroprosthetics market.

Expanding Reimbursement for Neuromodulation Implants

CMS reimbursement rates, ranging USD 6,700-34,000 for spinal cord and deep brain procedures, legitimize value-based payment models that tether payment to functional gains. Private insurers mirror these policies, boosting covered-lives penetration. The FDA Breakthrough Devices Program further compresses approval timelines, providing commercial tailwinds for companies launching closed-loop systems inside the Neuroprosthetics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & surgical costs of implants | -1.8% | Global, particularly pronounced in developing markets | Short term (≤ 2 years) |

| Availability of pharmacological / physical rehabilitation alternatives | -1.4% | North America & EU where alternative therapies are well-established | Medium term (2-4 years) |

| Shortage of specialised functional-neurosurgery talent | -1.6% | Global, with acute shortages in APAC and emerging markets | Long term (≥ 4 years) |

| Ethical & regulatory hurdles around elective cognitive enhancement | -1.1% | North America & EU regulatory jurisdictions, China developing frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Surgical Costs of Implants

Implantable pulse generators priced USD 24,000-60,000 and procedure bills surpassing USD 100,000 restrict access, especially where neurosurgical centers remain sparse. Only 200 facilities worldwide host the multidisciplinary expertise required, bottlenecking diffusion of the Neuroprosthetics market into lower-income regions until novel leasing or risk-sharing payment options scale.

Availability of Pharmacological / Physical Rehabilitation Alternatives

New neurological drugs, virtual-reality physical therapy, and transcranial magnetic stimulation give clinicians reversible options that many patients attempt before consenting to permanent implants. Telehealth cognitive-behavioral platforms further delay device uptake, capping near-term growth in certain Neuroprosthetics market segments until head-to-head outcome data prove superior cost-utility ratios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Adaptive Systems Drive Therapeutic Precision

Closed-loop systems capture physiological feedback to auto-adjust stimulation, driving a 11.94% CAGR through 2031. Output devices still controlled 55.92% of the Neuroprosthetics market in 2025 thanks to mature deep brain, spinal cord, and cochlear franchises. Input interfaces that decode cortical intent now bridge paralyzed users to external robotics, widening the Neuroprosthetics market addressable base. Continuous algorithm refinement reduces clinic visits and supports superior long-term outcomes, making adaptive platforms the strategic growth engine over the forecast window.

Bidirectional designs that merge sensing and stimulation inside one implant underscore the sector’s evolution toward integrated precision-medicine tools. Commercial launches such as Medtronic’s Inceptiv spinal stimulator showcase real-time compound-action-potential tracking that locks analgesia within individualized therapeutic windows . As hospital systems favor devices that minimize re-programming workloads, adaptive units gain formulary preference, amplifying their influence on overall Neuroprosthetics market expansion.

By Component: Software Intelligence Transforms Hardware Platforms

Implantable hardware captured 62.98% revenue in 2025, yet AI-driven software modules are growing at 12.33% CAGR as manufacturers layer machine-learning analytics atop legacy devices. External wearables process high-bandwidth cortical recordings, reducing implant complexity while sustaining signal fidelity. Predictive-maintenance dashboards flag battery depletion and impedance drift, lowering unscheduled clinic appointments across the Neuroprosthetics market.

Regulatory frameworks now permit post-market software upgrades outside costly surgical revisions, extending product life cycles. NeuroPace’s cloud-linked seizure analytics illustrate the pivot toward digitally differentiated offerings; incoming FDA guidance on machine-learning-enabled medical devices should further cement software subscriptions as recurring revenue channels within the Neuroprosthetics market.

By Technique: Peripheral Approaches Challenge Central Dominance

Deep brain stimulation retained 36.42% of the Neuroprosthetics market size in 2025, anchored by Parkinson’s and essential-tremor successes. However, cortical and peripheral nerve stimulation are scaling at 12.75% CAGR through 2031 as minimally invasive stent-electrodes and percutaneous leads trim surgical risk. Endovascular brain-computer interfaces that deploy via cerebral veins avoid craniotomies altogether, opening the Neuroprosthetics market to hospitals lacking advanced neurosurgery suites.

Peripheral programs targeting vagus and tibial nerves broaden use cases into depression, inflammation, and bladder dysfunction, diversifying revenue streams. Multi-target regimens that pair brain and peripheral sites gain clinical interest for complex disorders, signaling an era where hybrid paradigms reshape therapeutic algorithms across the Neuroprosthetics market.

By Application: Psychiatric Indications Reshape Treatment Paradigms

Motor disorders still delivered 43.05% revenue in 2025, yet psychiatric and cognitive uses are climbing at 12.78% CAGR to 2031. Treatment-resistant depression trials using closed-loop cortical implants reveal robust, rapid symptom relief, pushing regulators to draft indication-expansion guidance. Cochlear and emerging retinal prostheses continue to dominate sensory-loss revenues, while memory-supportive hippocampal stimulators enter Phase II studies aimed at Alzheimer’s disease, setting fresh demand vectors inside the Neuroprosthetics market.

Military and aerospace agencies finance augmentation research that seeks to enhance operator cognition and man-machine integration. Although elective enhancement remains ethically contentious, these grants accelerate platform maturation, indirectly benefiting therapeutic segments of the Neuroprosthetics market through technology spillovers.

By End User: Home Care Transforms Delivery Models

Hospitals accounted for 59.87% sales in 2025 because surgical implantation and initial programming occur in tertiary centers. Yet remote-care platforms and clinician-supervised patient apps drive a 12.84% CAGR for home and ambulatory settings. Secure mobile dashboards let users titrate stimulation within predefined limits, shrinking follow-up clinic load and tapering overall care costs across the Neuroprosthetics market.

Rehabilitation clinics leverage portable brain-computer-interface headsets for at-home stroke recovery, capturing reimbursements for digital therapy sessions. As payers endorse outcome-based contracts, decentralized models that combine telemetry, telehealth, and AI-guided coaching will capture a growing slice of the Neuroprosthetics market.

Geography Analysis

North America delivered 42.91% of 2025 global revenue, supported by dense functional-neurosurgery networks, Medicare payment coverage for closed-loop stimulators, and FDA Breakthrough Device pathways that shorten commercialization time. United States hospital groups now negotiate risk-share contracts that tie payment tranches to objective mobility or seizure-reduction milestones, accelerating real-world evidence generation and fueling continued Neuroprosthetics market growth.

Europe follows with stringent Medical Device Regulation standards that reinforce user safety while preserving a pan-regional CE-mark route to market. Countries such as Germany apply health-technology-assessment filters that reward implants delivering verifiable quality-of-life gains; this evidence-centric stance nurtures sustainable adoption curves. EU-funded Horizon Europe consortia invest in biodegradable electrodes and adaptive cortical interfaces, ensuring indigenous innovations feed directly into regional Neuroprosthetics market pipelines.

Asia-Pacific is the fastest-growing cluster, projected at 13.16% CAGR through 2031. China’s National Medical Products Administration is piloting USD 902 reimbursement codes for invasive brain-computer-interface placements, while the Ministry of Industry and Information Technology lists neural interfaces as a strategic emerging industry. Japan and South Korea translate advanced semiconductor supply chains into cost-efficient implant manufacturing, whereas India scales neuro-rehabilitation centers that extend device access beyond Tier-1 cities. Together these moves support a more democratized Neuroprosthetics market landscape by decade’s end.

Competitive Landscape

Incumbent giants such as Medtronic, Abbott, and Boston Scientific anchor legacy franchises, leveraging decades-long clinician relationships and post-marketing safety archives. Their combined revenue still exceeds half of the Neuroprosthetics market, yet software agility and niche indication focus allow emerging firms to punch above their weight. Neuralink’s minimally invasive sewing-machine robot and Synchron’s endovascular electrode stent secured FDA Investigational Device Exemptions in 2024, proving start-ups can navigate stringent U.S. regulation.

Strategic consolidation is underway: Globus Medical’s USD 250 million purchase of Nevro in 2025 buys closed-loop spinal pain technology and cross-sells it through Globus’s spine-surgery channel. Boston Scientific broadened its stimulation portfolio with WaveWriter SCS FDA clearance in February 2024, underscoring the premium placed on adaptive therapy engines. Patent analytics reveal densest filings around flexible graphene conductors and wireless-power telemetry, domains where university spin-outs like Blackrock Neurotech and Paradromics license key know-how to wider industry, enriching the competitive tapestry of the Neuroprosthetics market.

Longer term, advantage will gravitate toward vendors that couple multi-site sensing, edge AI, and cloud analytics into subscription-priced ecosystems. Those capabilities create data lock-in and pave the way for value-based payment contracts, positioning integrated digital-hardware players to secure incremental Neuroprosthetics market share as health systems pivot to outcome-linked procurement

Neuroprosthetics Industry Leaders

Medtronic PLC

LivaNova PLC

Demant A/S

MED-EL

Cochlear Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Boston Scientific won FDA approval for WaveWriter SCS Systems to treat chronic low-back and leg pain, enabling tailored paresthesia-free therapy delivery.

- January 2024: Abbott received FDA clearance for the Liberta RC deep-brain-stimulation system, the smallest rechargeable DBS device that supports remote programming for Parkinson’s and essential tremor patients.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the neuroprosthetics market as all implantable or body-worn electronic systems that interface with central or peripheral nerves to restore, replace, or modulate lost motor, sensory, or cognitive functions. Devices range from deep-brain stimulators and spinal cord stimulators to cochlear, retinal, and adaptive closed-loop motor prostheses.

Scope exclusion: non-invasive neuromodulation tools such as transcranial magnetic stimulation and wearable EEG headsets are outside this estimate.

Segmentation Overview

- By Type

- Input Neuroprosthetics

- Output Neuroprosthetics

- Closed-loop/Adaptive Neuroprosthetics

- By Component

- Implantable Device

- External Wearable Unit

- Software & Algorithms

- By Technique

- Deep Brain Stimulation (DBS)

- Spinal Cord Stimulation (SCS)

- Vagus Nerve Stimulation (VNS)

- Cortical & Peripheral Nerve Stimulation

- By Application

- Motor Disorders (Parkinson’s, Essential Tremor, etc.)

- Sensory Loss (Auditory, Visual)

- Cognitive & Psychiatric Conditions (Alzheimer’s, Depression, PTSD)

- Chronic Pain & Epilepsy

- By End User

- Hospitals

- Specialty & Rehabilitation Clinics

- Home-care & Ambulatory Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor investigators interviewed practicing neurosurgeons, rehabilitation physicians, and biomedical engineers across North America, Europe, and Asia-Pacific, alongside payor policy advisors. Conversations verified average selling prices, surgical learning-curve effects, and emerging reimbursement triggers that secondary data alone could not capture.

Desk Research

Our analysts collected baseline volumes, procedure tariffs, and reimbursement milestones from tier-1 public sources such as the U.S. Centers for Medicare & Medicaid Services, Eurostat surgical activity files, Japan MHLW device approvals, and WHO Neurological Disorders dashboards. Industry run-rate pricing was gauged through 10-K filings, FDA 510(k) summaries, and investor decks, then cross-checked on D&B Hoovers and Dow Jones Factiva for company-level revenue splits. Additional insights came from specialty associations, including Cochlear Implant International, International Neuromodulation Society, and the European Brain Council. The list above is illustrative; many other open datasets informed evidence gathering.

Market-Sizing & Forecasting

A top-down reconstruction starts with documented implant procedure counts by technique and geography, augments them with prevalence-to-treatment penetration for Parkinson's, chronic pain, and sensorineural hearing loss, and applies weighted ASPs to reach 2025 value. Select bottom-up checks, including supplier revenue roll-ups and channel audits, align totals. Key drivers modeled include aging population growth, neurological disorder incidence, Medicare coverage expansions, device ASP erosion, and venture funding velocity. Multivariate regression with scenario analysis projects these variables to 2030, while ARIMA guards against over-fitting short-cycle shocks. Gaps where hospital volume logs are partial are bridged by regional implant-to-procedure ratios validated during physician interviews.

Data Validation & Update Cycle

Outputs undergo variance scans against independent import data and peer publications before a two-step analyst review, then senior sign-off. Reports refresh annually; material regulatory or recall events trigger interim model updates, and a final data sweep occurs immediately prior to client delivery.

Why Mordor's Neuroprosthetics Baseline Commands Confidence

Published estimates frequently diverge because firms pick differing device baskets, pricing ladders, and update cadences. Our disciplined scope selection and annual refresh keep decision-makers anchored to reality.

Key Gap Drivers: rivals sometimes mix non-implant neuromodulation tools, apply single-country ASPs globally, or lock inflation factors for the whole forecast horizon, leading to inflated totals or steeper CAGRs than clinical adoption supports.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.43 B (2025) | Mordor Intelligence | |

| USD 14.62 B (2024) | Global Consultancy A | Includes diagnostic neuro devices and applies constant USD without currency realignment |

| USD 14.75 B (2024) | Trade Journal B | Counts non-implant BCIs and projects volume on uniform 15 % CAGR absent reimbursement checks |

| USD 16.47 B (2025) | Industry Association C | Blends neuromodulation consumables and lacks explicit ASP sourcing, lifting base value |

Taken together, the comparison shows how Mordor's carefully bounded device list, mixed-method model, and live refresh cadence deliver a balanced, transparent baseline that executive teams can reliably build plans upon.

Key Questions Answered in the Report

How big is the Neuroprosthetics Market?

The Neuroprosthetics market size stands at USD 14.99 billion in 2026 and is set to reach USD 25.96 billion by 2031 at an 11.62% CAGR.

Which segment is growing the fastest in the Neuroprosthetics market?

Closed-loop adaptive systems are the fastest-growing type segment, projected to climb at 11.94% CAGR through 2031 due to real-time feedback capabilities.

Who are the key players in Neuroprosthetics Market?

Medtronic PLC, LivaNova PLC, Demant A/S, MED-EL and Cochlear Limited are the major companies operating in the Neuroprosthetics Market.

Which is the fastest growing region in Neuroprosthetics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How dominant is deep brain stimulation compared with emerging techniques?

Deep brain stimulation held 36.42% of 2025 revenue, yet cortical and peripheral nerve stimulation are expanding faster at 12.75% CAGR as minimally invasive methods mature.

Page last updated on: